31.1 – Overview

It’s a new year, and that means it’s time to review your personal finances. Most tips about reviewing personal finances tend to be about investing, which always annoys me. I don’t know why, but people forget that there’s “personal” before “finance” and that the “personal” matters more than “finance.”

Any plan without considering your unique life circumstances will always be incomplete. In this post, I’ll highlight the important aspects that you should take care of when managing your personal finances. It’s not possible to cover everything because something will be unique to your situation.

This post is for people who are still working and have started their personal finance journeys, as well as those who haven’t. The financial review process for retired people will be different, and I’ll try writing about it in the future.

31.2 – Don’t be scared

Everything about money is uncertain, and we are hardwired to hate uncertainty. A study showed humans find not knowing what will happen more stressful than knowing something bad will happen for certain. You would’ve also heard that losing something hurts twice as much as gaining something—this is called loss aversion. But there’s more to it. We also prefer the known over the unknown—this is called ambiguity aversion.

But why do we hate uncertainty?

Another study showed that losing money activates the same brain regions that also process pain. In a sense, losing money feels like getting punched in the face.

When reviewing your personal finances, you will have to make tough decisions whose outcome you won’t know for decades. It’s easy to get tricked by our brains into avoiding this uncertainty by doing nothing or taking the easy way out. I’m not saying nonsense like, “don’t be afraid.” Know that you will always be afraid when making financial decisions and be aware that we can be our own worst enemies.

For new investors

One reason people don’t think about their personal finances is because they are scared. Questions like “What if I make a mistake?”, “Will I lose money if I do this?” or “This sounds too complex” stop people from getting started. Making mistakes is part of the process; how else will you learn? But there’s no bigger mistake than having the time and ability to take care of your personal finances but not doing so.

The first step will always be the hardest. But as you start taking care of your finances, you will learn, and things will become easier. It’s the same with anything that seems difficult in life.

When making important financial decisions, it’s ok to be scared—we aren’t robots. But avoiding decisions due to fear is the difference between a happy retirement and a miserable one. You might be thinking, all this motivational stuff sounds nice, but how do you deal with the fear of uncertainty? The rest of the post is dedicated to answering that question.

31.3 – A time for reflection

The phrase “the map is not the territory” was coined by the Polish scholar Alfred Korzybski. It means that our assumptions about reality are not the actual reality. This also applies to personal finance. We often have a map of our personal finances, but the territory tends to be different. That’s because life happens, and you can’t plan life—you just have to deal with it.

It’s a tragedy that personal finance has become all about what [insert product name] to buy. Financial products are a means to an end and not the end itself. An important aspect of your personal finance review process is to take a moment to reflect on your life circumstances.

What does this mean?

A year is a long time, and a lot can happen. Think about all that has happened in the past year because major life events can affect your finances. Having this big picture view of your life makes it easier to act.

For perspective, think about the last three years. We’ve lived through a pandemic that upended our lives, a historic spike in inflation that has increased the cost of living, and a terrible economic environment that has led to sharp pay cuts and job losses. Then there might be changes in your life, such as marriage, having a kid, family emergencies, job losses, business failures, etc. All these events affect your personal finances.

Then there’s also the fact that money is a deeply uncomfortable subject, and we rarely discuss it with our parents and partners. Often, financial shocks come as a surprise because of the lack of communication. Personal finance isn’t just about you; it’s also about your dependents and partner.

Take the case of the elderly, like your parents, etc. They are the most vulnerable to financial fraud and mis-selling. Most parents don’t discuss their finances with their kids. So if they are defrauded or if they buy some terrible product, the kids don’t discover it for years, and it’s often too late to do anything. There have been countless cases where senior citizens have lost their retirement kitties to such fraud.

Having a holistic view of you and your dependents is important.

For new investors

This applies to new investors as well. Even before you get to the “where to invest” and “what product to buy,” know where you are. Money conversations might feel like opening Pandora’s box—open it!

31.4 – Know where your finances are

The next step is to take a financial inventory and figure out your net worth.

Why?

Knowing how your finances stack up is like getting a full body health checkup, it’s the bare minimum you can do every year. Your net worth is your assets minus liabilities. But before that, you need to analyze your cashflows. I know that sounds dreadful but figuring out the health of your finances without knowing your inflows and outflows is impossible. You don’t have to track every single spend, either. You can look at your aggregate inflows and outflows every month.

I know gathering the details is painful, but most banking apps provide basic spending analysis. If you are using other personal finance apps, then this can be easier. You can also use a spreadsheet to do this. Use this Morningstar template guide to start.

As an aside, now that most banks are part of the account aggregator framework, we will see more robust personal finance tools in the future.

Tracking your cashflows can help you figure out where your expenses are increasing. This will help you cut down on unnecessary spending and save more. But the biggest advantage is that it can help you avoid lifestyle creep or lifestyle inflation. It’s the tendency for your expenses to increase as your income grows. Nothing damages your retirement readiness like a stagnant saving rate and increasing expenses.

Once you’ve analyzed your cashflows, you can build your personal balance sheet or net worth statement. Your net worth gives you a starting point for understanding how your finances stack up. Tracking how it evolves can help you understand the strengths and weaknesses of your personal finances. It makes it easier to change things and improve your finances.

Start by making a list of all your assets and liabilities.

Assets

- Cash balances in all your bank accounts.

- Investments across fixed deposits, stocks, mutual funds, bonds, insurance, pensions, annuities, chit funds, Govt savings schemes, etc.

- A realistic value if you own a house, jewelry, art, etc. Estimating the values of illiquid assets like houses can be hard, but you can use a reasonable guesstimate based on similar properties, online sales data, or other prices. It’s better to be conservative when estimating.

- Other assets

Liabilities

- Housing loan balances

- Loan balances for all other loans like car loans, personal loans, buy now pay later (BNPL), loans against securities, loans against insurance, jewelry, etc.

- Other loans and liabilities

Use a spreadsheet to calculate your net worth–your assets minus liabilities. You can use this Morningstar template as a guide.

Without knowing your net worth, managing your finances is like shooting in the dark.

Consolidate whatever you can

Reviewing your finances will also help you figure out if your finances are scattered across different platforms. You should consolidate your finances because it makes managing them easier. For example, investing in mutual funds on a different platform doesn’t make sense if you already have a Zerodha account or any other broking account that offers direct mutual funds. You get all the details of you and your family from your back-office in a few clicks.

- If you are married, involve your partner when reviewing your finances.

- If your parents are taking care of their own finances, you should encourage them to review their finances. If you are taking care of their finances, review them and ensure your parents are financially set.

- You might also have multiple accounts with multiple brokers, banks, and platforms. Close them all unless needed.

- If you have any toxic products like endowment policies, traditional insurance policies, ULIPS, etc., it’s best to get rid of them. They are costly and opaque. They just make the insurance companies richer and you poorer.

Reviewing all your finances can be a clarifying exercise because it forces you to think about all aspects of your life.

31.5 – Review your goals

Now that you have a broad idea of your finances, the next step is to review your financial goals.

Finance is the only industry where people argue about everything, and goal setting is one of them. Some think that you’re doomed without setting goals because setting goals helps you be realistic and focus on tangible outcomes. But others argue that we don’t know our goals, and even if we do, they keep changing. They think setting specific goals can distort risk perceptions, cause investors to take outsized risks, induce tunnel vision, become narrowly focused, miss the bigger picture, and lead to bad behavior once a goal is met.

The truth, as always, lies somewhere in between. We’re kind of hardwired to think in terms of goals. Think about the end of the month when you get your salary, you mentally start allocating that money to various buckets like rent, savings, shopping, etc. This is called mental accounting, and it was made famous by Nobel laureate Richard Thaler. Goals-based investing harnesses that natural tendency.

Being outcome-oriented is risky, and we don’t always know our goals. Even if we do, they change. If you’re saving to buy a house after 5 years, you will likely change your mind about what house, where, etc., in year 5.

Morningstar had conducted a study in which they asked people to list their top 3 goals, after which they showed everyone a list of common financial goals. After seeing the master list of goals, 73% of the people changed at least one of the top 3 goals.

Some people advocate for possibilities planning that starts with figuring out what’s possible to achieve and then planning for those goals. I prefer this approach because it’s more flexible. Most financial plans fail because they aren’t flexible. They ignore that life is unpredictable and that we have to be adaptable. Reminds me of that old saying, “Man plans, and god laughs.”

There’s no right or wrong way to manage your personal finances. Some people save as much as possible without specific goals, some just have generic goals, and some have specific goals. You have to figure out what works for you and stick with it. Focus on building good systems rather than trying to be specific. All you can do is control the processes, you can’t control the outcomes.

How to review your goals?

A few things to remember if you have goals:

- Goals should be well-defined. For example, I want to retire in 2065 with 10 crores and withdraw 4% every year.

- Estimate the cost of the goal.

- Calculate the amount you need to save and adjust it for inflation. The SEBI website has useful calculators to help you plan.

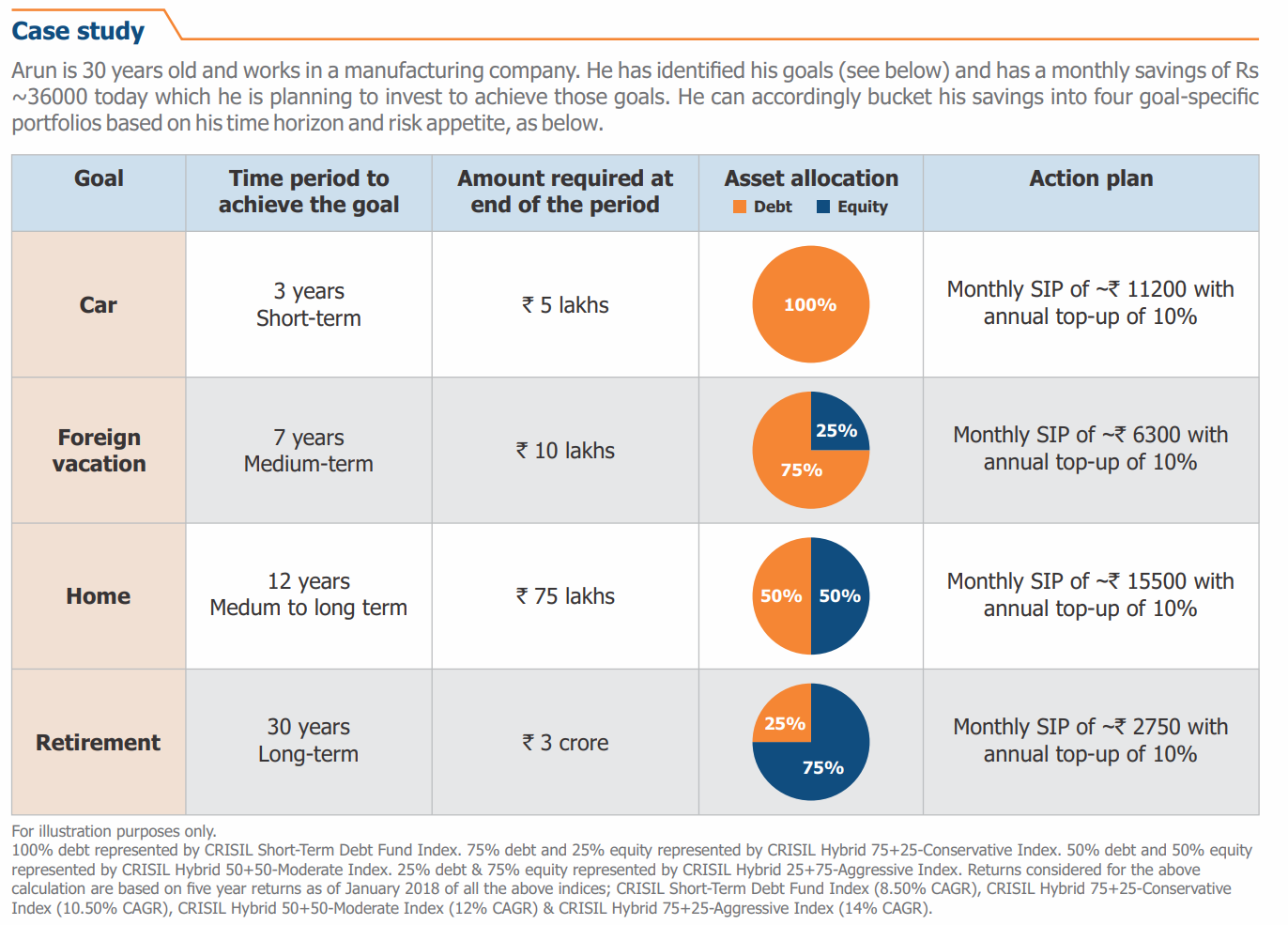

- Figure out the right asset allocation for each goal with reasonable return assumptions. Here’s an example:

A few things to keep in mind

Always have reasonable return assumptions. Take a look at the return assumption in the footer of the image above. Assuming 12% for a 50% equity and 50% debt portfolio and 14% for a 75% equity and 25% debt portfolio is a recipe for disaster. Just because Nifty has given returns of 12% historically doesn’t mean you assume the same rate in your planning.

Moreover, you won’t invest 100% in equity, and for long-term goals like retirement, you have to reduce your equity exposure as you get closer to your retirement. The blended returns of equity, debt, and gold won’t be 15% but lesser. Having a reasonable assumption for your longest goals, like retirement, is important. If you get higher returns, then that’s a bonus.

For shorter-term goals, under 5 years, use a savings bank, FD, or liquid fund returns.

Know the difference between risk tolerance and risk capacity.

- Risk tolerance is your ability to withstand market volatility.

- Risk capacity is how much risk you can take at a goal level.

For example, let’s say you are 30 years old and want to retire at 60. Since the goal is 30 years away, you can take more risk with a higher equity allocation. Even a 70% equity and 30% debt portfolio will be ok.

But let’s assume you want to buy a house in 7 years, you are an aggressive investor, and you don’t care about market volatility. It still doesn’t make sense to take more risks because this is a short-term goal. Even though you have a higher risk tolerance, the risk capacity for the goal is low. You are taking on sequence risk if you put 60% in equity for a 7-year goal. In other words, what happens if the market falls 50% in year 6?

Aligning your goals with your values

An issue with setting goals is that we don’t think about the things that matter to us. With or without realizing it, we all follow an internal compass. We work hard toward the things that matter and are meaningful to us. It might not always be obvious, but we tend to have a fuzzy idea.

When thinking about your goals, lean into this. Think about the things that matter to you and your most deeply held values, and you’ll notice that your goals revolve around your values. I know these are very vague topics, but personal finance is not a math problem, it’s a people problem. By no means is this a simple process. You must ask yourself the hard questions. This is the role of a financial advisor, but you can do this on your own as well.

I love George Kinder’s three questions for financial planning.

Question 1: Design Your Life

I want you to imagine that you are financially secure, that you have enough money to take care of your needs, now and in the future. The question is, how would you live your life? What would you do with the money? Would you change anything? Let yourself go. Don’t hold back your dreams. Describe a life that is complete, that is richly yours.

Question 2: You Have Less Time

This time, you visit your doctor who tells you that you have five to ten years left to live. The good part is that you won’t ever feel sick. The bad news is that you will have no notice of the moment of your death. What will you do in the time you have remaining to live? Will you change your life, and how will you do it?

Question 3: Today’s the Day

This time, your doctor shocks you with the news that you have only one day left to live. Notice what feelings arise as you confront your very real mortality. Ask yourself: What dreams will be left unfulfilled? What do I wish I had finished or had been? What do I wish I had done? [Did I miss anything]?

George is the father of financial life planning, and he devised these questions to force people to think about the things that matter to them. If you notice, each question pushes you to think deeper. These questions can also evoke strong emotions like guilt, shame, regret, and profound sadness. But working through those emotions can help you work, save and invest toward the goals that matter most and bring meaning

31.6 – Debt

Managing debt is a key aspect of personal finance. It doesn’t matter if you are an investing genius and you are outperforming Warren Buffett, bad debt management can ruin you.

Before you review, gather all the relevant details of your liabilities. Most forms of debt have a terrible reputation, but not all debt is bad. The costliest debt is bad, period! Unless you have overextended yourself, loans like housing loans and reverse mortgages can be useful.

Once you have all the details of your loans, it’s not hard to figure out the issue.

Here’s a broad range of interest rates for major loan categories.

| Loan types | Interest rates |

| Credit cards | Up to 42% |

| Lending apps | Up to 36% |

| Personal loans | Up to 36% |

| Loan against property | 8%-25% |

| Housing loans | Up to 15% |

| Loan against securities | Up to 15% |

| Auto loans | 8%-20% |

| Education loans | 8%-16% |

Credit card loans are the worst because the interest rates can go as high as 42%. In the hands of people who know how to manage a credit card, it can be an useful tool. If not, it’s a deadly trap.

Loans from lending apps are the next worst. Housing loans tend to be the largest and paying them off might not be possible. Depending on the interest rate, paying them as per the loan schedule might be ok. But if you can afford to pay extra every month, it can reduce the amount of interest you pay. That’s because, early on, most of your EMIs go toward interest rather than paying the principal.

Not paying off costly loans like credit cards and personal loans is a bad idea. Even before you save or invest, your priority should be to clear these costly loans. Here are some simple strategies you can follow.

Snowball method

Make a list of all your loans and arrange them by the outstanding amount, from small to large. Make the minimum payments on all the loans except the smallest loan. Use the amount remaining to pay the smallest loan. Paying off the smaller loans, move on to the others and clear them all.

Avalanche method

Make a list of all your loans and arrange them by the interest rate—from the highest to the lowest. Make the minimum payments on all the loans except the loan with the highest interest rate. Use the amount remaining to pay it. Once that is paid off, move on to the next.

If you are lucky enough to have a high salary but also high debt, not clearing your loans early is stupid. Paying off a loan is like earning a guaranteed return, and the mental peace of not having debt is priceless.

Credit score

It’s also important to check your credit scores annually. Your credit score determines your creditworthiness. India has four credit bureaus: Experian, Equifax, TransUnion CIBIL, and CRIF Highmark. These companies monitor your loans and assign a score from 300-900—the higher your score, the better your creditworthiness. 750+ is what you should aim for.

All the credit bureaus provide a free report, which you can download from their websites. You might also see wrong details in your report, which affects your credit score. In such cases, you can raise a dispute on the credit bureau’s website and have it fixed. Your credit score depends on the credit type, mix, and duration, among other factors. At a basic level, not taking too many loans and paying all your dues on time is a good start. Here are a few more tips.

31.7 – Insurance

At this stage, you might be thinking, why am I not talking about investments? It’s a tragedy that personal finance has become all about investing and products. It’s important to play defence before you play offense.

Why?

It should be obvious but let me spell it out anyway. Let’s assume that you don’t have emergency savings or insurance but a high savings rate, a good investment portfolio, and excellent returns. If you were to have a health emergency, your investments would become your insurance and emergency fund. Most Indians are just one serious health incident away from ruin—it sounds depressing, but that’s the sad truth. Even people with decent incomes in India don’t have any insurance. When hit with emergencies, they end up depleting their savings or taking high interest loans.

The 2 key types of insurance you need are

- If you have dependents, term insurance (life insurance).

- Health insurance.

Term insurance

If you have dependents, then having life insurance is critical. A term insurance policy pays out in the case of your death. The ideal cover depends on factors like your income, expenses, family situation, etc. But at a basic level, the insurance cover should replace the lost income in the case of your death. So, if you have a cover of Rs 1 crore invested in an FD at 7%, the monthly interest would be Rs 57,994. Would that be enough for your dependents to lead a comfortable life? You also have to assume inflation because expenses increase every year. The rule of thumb is the higher the cover, the better it is.

Health insurance

I cannot stress the importance of health insurance because health costs have and will continue to rise. Paying for them out of your pocket is impractical. Starting with a base policy of Rs 10–20 lakhs and then adding a top-up policy as necessary will go a long way. Shrehith, from Ditto, had written a wonderful post on choosing health insurance cover. He’s also written an entire module on health insurance in detail, which I recommend reading.

Review

- Check if you have appropriate term insurance cover. Use this guide as a reference.

- Check if you have adequate health cover and the right policy. Here are a few things you need to watch out for when picking a health insurance policy.

- Avoid any insurance products that mix insurance and investments. They are toxic products that offer the worst of both worlds.

Having said that, insurance is a personal product that depends on your unique life circumstances. It’s always wise to speak to an insurance advisor. If you need help with an existing product or need to buy a new policy, you can speak to an advisor from ditto.

For newbies

If you are just starting your personal finance journey, ensure you have adequate insurance cover before you do anything. It’s important to protect both yourself and your dependents.

31.8 – Emergency fund

The next important item on your personal finance checklist should be to create an emergency fund. Apart from health emergencies, life will throw you 100 other curveballs, from job losses to house repairs. You can’t sell your investments in these situations, and taking debt is a bad idea. An emergency fund is meant to help you deal with such situations.

How much should you have as an emergency fund?

It depends. The common advice is to keep between 3 and 12 months of your living expense as emergency funds. But, if you have a high degree of job predictability or are young, you can afford to have a smaller reserve. But having a bigger reserve is a good idea if you are a contract worker, have a high-income job, or have an uncertain job.

Where to park your emergency fund?

An emergency fund should always be liquid and be accessible anytime. You cannot use stocks to park your emergency fund because they are volatile. Stick to instruments that you can access easily, like liquid mutual funds. You will have second thoughts about parking such a large amount in a place where the returns are low. The goal of an emergency fund isn’t to generate returns but to cover your emergencies.

Liquidity of the emergency fund matters more than the returns.

A few pointers

- The right amount of money to put in a liquid fund depends on the nature of your income and expenses. The higher the predictability and security, the smaller the emergency reserve you can have.

- There’s no need to go overboard and have 5 years of your salary in an emergency fund. Aim to achieve a reasonable balance.

- If you are young, you need not have a 6 months emergency fund on day 1. You can start a SIP and build it up. You can also add money whenever you get bonuses or large cash inflows.

- Don’t chase returns with your emergency fund. You will regret it.

Very useful article. I like the point that personal finance is not only about where to invest, but also about understanding your own situation, cashflow, goals, debt, insurance, and emergency planning. Many people focus only on returns and forget the basics. A proper yearly review can really help avoid mistakes and make better financial decisions

One 100% with you on it 🙂

Happy learning!

This was such a clear and practical read on the importance of regularly reviewing your personal finances. I really appreciated how it emphasizes starting with the basics—understanding your income, expenses, assets, and liabilities—before jumping into investments or financial products. The idea of treating personal finance as a “living system” that needs to be updated as life changes really stood out. It’s a strong reminder that financial stability comes from awareness, discipline, and consistent review, not just one-time planning.

Hello Dear,Excellent financial awareness article about personal loan India services. Understanding repayment structure and loan conditions is essential before borrowing money.

Hello Karthik Sir

The morningstar template that you mentioned is not available. Is it possible for you to share it?

Thanks and regards

Ah, they must have changed the location on the website. Can you check with them once?

I have checked on the website, its not showing up.

Great insights on personal finance! The step-by-step breakdown makes it easier for beginners to understand budgeting and investments. I also found similar value-driven content on Rare Design Hive. which focuses on creativity and design. Both perspectives together can truly shape smarter decisions for financial and personal growth.

Alright, good luck!

Each watch list top daily change nifty 50 ,bank nifty, sensex reading pl

Ah, not sure. Have you checked the website, maybe they have relocated the URL?

Sorry – i just saw your reply on an earlier comment on this same topic- kindly ignore this question.

Sure, no issue. Good luck.

Thank you Karthik sir for such a wonderful and kind hearted gift of knowledge you provide for free. I also believe sir that knowledge should be accessible to all of us who have a burning desire to learn and grow. Once I have certain amount of money, skill or knowledge in my life. I will surely share it with everyone who have a deep burning desire to learn. Happy Diwali in advance sir. May you be happy and family too.

Thanks, Rishi. I do hope you learn, grow, and enlighten others along the way. Happy Deepavali 🙂

Eight years means 96 monthly installments, right? Initially, I was planning to do it over a 3-year period (36 monthly installments), but after reading a Reddit post, I reconsidered extending it to 10 years (120 monthly installments). However, taking inflation and the value of time into account, I decided to stick with the 3-year option. But now that you\’ve mentioned 8 years, I\’m starting to rethink it. Is there something I\’m missing? I\’m not sure if I\’m overlooking anything.

Its just that higher the time the higher is the odds of beating volatility and generating a positive return.

If I have a lump sum amount and want to invest it in mutual funds through SIPs, what would be the ideal duration to distribute it?

I\’d say you give it at least 8 years 🙂

Hi Karthick,

First of all kudos to the great work you are doing !!! Really like your way of writing and explaining things.

I am investing in Mutual Funds for past 2 years, I am 29 now. I have few queries on Mutual Funds

1. I commonly see suggestions like don\’t invest huge amount in small cap mutual funds. But if my goal is to take out this money after 8-10 years, is it still a risky investment where I may need to face losses? or will my money be able to sustain drops in market given the duration is long.

2. We have seen in past there were few fund houses which got merged with other or got shutdown or discontinued fund schemes, when such thing happens and if the market is not doing well at that time, what are the odds that I might end up in loss?

1) 8-10 years is a good time to absorb the market volatility. But I\’d feel more comfortable with mid cap fund. This is purely based on your risk appetite.

2) Usually thats rare, but when it happens, you are unlikely to lose money as the new units will be with the merged entity.

Karthik,

Big fan of your work!

You have mentioned to diversify the portfolio. So, Im planning to balance the risk by investing in other commodities like real estate, gold etc.

1. To invest in gold, there are so many options. Physical gold, gold funds, gold ETF, SGB etc. which one is better investment as part of diversifying the portfolio because I don\’t have much idea on these apart from physical gold.

2. Is there any modules that zerodha is planning to launch for gold investment options?

Thanks!

1) I\’d have suggested SGBs, but there is some confusion with that post 2024 interim budget, so maybe Gold ETFs or funds.

2) You can look at Gold ETFs on kite or Gold funds on Coin.

I was very very eager for downloading Morning Star Spreadsheet, but the link lead to a page where the excel is not available, teacher.

Can you please try downloading from another browser?

Hey, I couldn\’t access the Morningstar templates for the personal cashflow statement and balance sheet

Can you check on their website directly? Maybe they have changed the location.

The whole course is a gold-mine for beginners like me. Thank you Karthik.

Glad you liked it, happy learning 🙂

Morningstar template for cash flow is not available in that link. Can you provide any other link or template?

Your narration is really good, very organised and simple explanations.

Ah, why not check the annual report?

Hi Karthik,

I do not find anything mentioned about RD ( Recurring deposit). Isn\’t this a risk free avenue for building a short term corpus by doing monthly recurring investment? Alternative to liquid fund may be? Just wanted to get some perspective although I might be wrong.

Short term corpus is possible by option for any of these fixed income product, but what is not possible is \’short term wealth creation\’. I think many ppl get confused here and opt for the wrong product to address a financial goal.

I am learning a lot from this module, thank you.

I have a novice question: why can\’t we opt to park our emergency funds in a bank FD (which more or less have same returns as a debt/ liquid fund). Is it due to lock in duration?

Bank FD is also fine. The main thing with emergency corpus is that the capital should be protected with low volatility, so bank FD fits that definition.

Hi, first of all thanks for so much financial education.

2 issues with PDF versions :

– Most of the images in the PDFs are blurred

– The last 2 chapters of this module (personal finance review) are not included in the PDF version.

Checking on this, thanks.

As young who has just started to earn ,is it ohk to follow the 50-30-20 rule,as per the income in the first month:-

1)50% or more will go entirely in -Term plan.

Then we will have to wait for next month for Health Insurance after which we can go for the emergency liquid fund from 3 rd month.

Yours thought on this?

Thanks in Advance!

Yes, Paras. Get term and health isnurance and then you can startup building your emergency fund and start investing. You can build your emergency fund slowly, there\’s no need to wait to start investing until you have created your emergency fund.

It has been 3 years since I started my monthly SIPs in 3 MFs. I am increasing the SIP amount every year from 5k to 10k to 15k. Is this increment a prudent approach ? I am want to put down as much money in these MFs as possible as I may not be able to save later !!

Yes, it should be ok 🙂

Good luck!

Thank you

Good insights worth following. Thanks for the valuable information

Happy learning!

Let\’s Make India Trade!

Hello Karthik sir you elaborate every topic nicely in varsity. I want to ask can I get the whole module of varsity in pdf so that I can print it and read and make notes from our of it.

We have provided PDF at the end of every module which you can download, Kiren. Please feel free to download.