9.1 – October 2017

The previous chapter hopefully has given you some insights into reading a mutual fund factsheet. The factsheet lists some of the good to know information about a mutual fund. Do remember, the factsheet also doubles up as a marketing document for the Asset Management Company (AMC), hence read through the fund’s factsheet with a pinch of salt.

Starting from this chapter, we will shift our focus on the mutual fund categories. The idea is to discuss the main categories and a few subcategories of mutual funds.

Please note, the term ‘subcategory’ in the context of mutual fund categories does not exist, but I think it makes life simpler if you thought about the mutual fund categories this way.

I’m not sure if we can cover all the subcategories in this module. For example, Debt fund as a main mutual fund category has nearly 16 different subcategories, equity as a category has about 10/11 subcategories. Given this, as you can imagine, discussing the entire gamut of MF categories will digress us from the central theme of this module which is personal finance. The idea here is to lay down a foundation for you to understand the main mutual fund category (and a few subcategories) and hopefully, this foundation will help you understand the many subcategories of mutual fund schemes.

No discussion on the mutual fund universe is complete without touching upon the SEBI’s October 2017 circular on MF categorisation. This circular from SEBI was fairly significant, and it helped simplify the MF universe. To appreciate why this SEBI circular is essential, we need to dig up a bit of history.

Back in the days, the mutual fund world was a bit chaotic. The asset management companies would float many different schemes with overlapping investment ideologies. These funds would often confuse or mislead investors. For example, an AMC would run a ‘large-cap fund’, which by definition should predominantly have only large-cap stock, but these AMCs would stuff in small-cap stocks, which as you can imagine bumps up the volatility (and the return) of the fund. A typical large-cap investor would sign up for the market returns plus lower volatility, but the presence of small-cap stocks in a large-cap fund kind of defeats the purpose.

Here are a bunch of other problems that existed pre-Oct 2017; these problems existed mainly due to the lack of proper mutual fund classifications and definitions.

Multiple funds – An AMC would launch numerous funds with similar investment objectives. For instance, it was common for an AMC to have multiple large-cap or mid-cap schemes, while all these funds had the same investment objective. The distinction between the funds was not too clear.

Lack of definition – While an AMC would title their scheme as a large or mid-cap fund, it would contain stocks from other market capitalisation. The problem occurred because there was no formal definition of market capitalisation.

Portfolio composition – The mutual fund schemes lacked a clear definition in terms of portfolio composition. For instance, the portfolio of a mid-cap fund is expected to hold mid-cap stocks, but it was common to find funds with a large proportion of small-cap stocks while the name of the fund suggested the fund was a mid-cap focused fund.

These problems led to a series of other issues. One of the major concerns was with benchmarking of funds. A large-cap fund is benchmarked against a Nifty 50 index; now we have a problem if a fund with small-cap stocks gets disguised as a large-cap fund and gets benchmarked against a large-cap index. The performance of such a ‘large-cap fund’ (at least in bull markets) is bound to get skewed and offers an abnormal positive return, often misleading the investor.

SEBI addressed these problems with the Oct 2017 circular. You can find the original circular here.

The circular clearly defined the market capitalisation of stock, which naturally solved a few legacy issues in the mutual fund world. As per the definition –

Large-cap stocks – 1st to 100th company in terms of full market capitalisation

Mid-cap stocks – 101st to 250th company in terms of full market capitalisation

Small-cap stocks – 250th company onwards in terms of full market capitalisation

With this formal definition, there was no longer ambiguity on the market capitalization, and the AMCs were now forced to comply with the definitions.

Further, SEBI mandated that an AMC can have only one scheme in any category (except for the thematic, index fund, and fund of funds). This mandate put a stop to AMCs offering a bouquet of schemes with an overlapping investment thesis. To make things clear, SEBI defined the portfolio composition as well. To put this context, post the circular, if an AMC were to run a large-cap fund, then SEBI not only defined what large-cap is but also set the minimum number of large-cap stocks (in % terms) the fund should hold in its portfolio.

Anyway, let us jump to the different mutual fund categories and subcategories and start exploring them. The idea here is to understand these categories and invest in them based on our financial situation in life.

9.2 – The Mutual fund universe

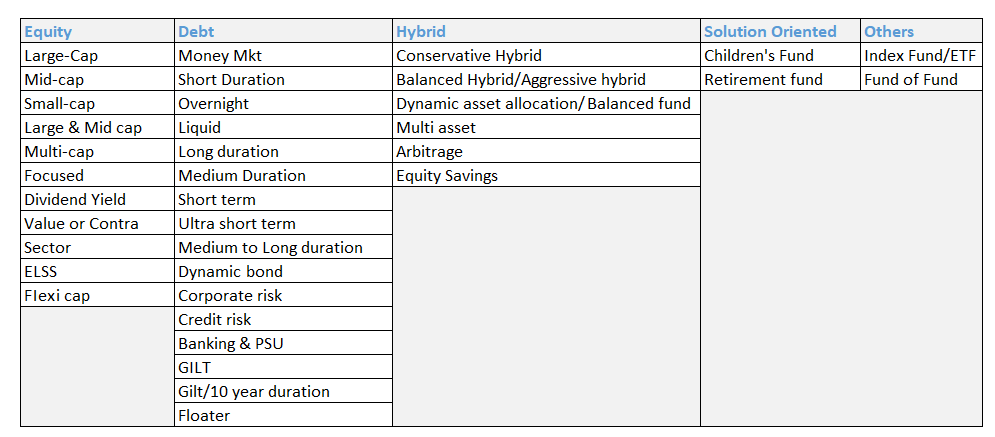

Primarily, there are five different categories of mutual funds under which there are many different categories. Think of them as a ‘category – subcategory’ way of classification. Here are the main categories –

- Equity

- Debt

- Hybrid

- Solution-oriented

- Other schemes

The entire ‘category – subcategory’ structure is as follows –

To begin with, we will focus on Equity as a category. As per SEBI’s circular, an AMC is supposed to run only one scheme per category. For example, an AMC can have only one large-cap, one mid-cap, one small-cap so and so forth.

However, under Equity, an AMC can have multiple sectoral funds.

9.3 – Equity Category

The equity category is perhaps the most popular MF category in terms of retail participation. As the name suggests, the schemes under the equity category invest in listed company shares. As you are aware, there are many different styles of investment in the market. A few of these popular styles have been picked and formally inducted into the ‘Equity category’. As you can see from the image above, there are nearly 11 different subcategories within the Equity category. Each of these categories is a different style of investing in the market, and they all differ in their risk and reward characteristics. However, the general philosophy of investing in an equity scheme remains the same, i.e. to generate wealth. What differs across these categories is essentially the timeline of this wealth generation and like I mentioned, the risk and reward.

Over the years, thanks to my profession, I’ve had the opportunity to interact with many people about mutual fund investing. One thing that I can tell you with confidence is that most of them approach mutual fund investing (at least in the equity funds) with unrealistic expectations. Some even go to the extent of looking at mutual funds as a proxy for direct stock investing. They almost have a trading attitude with their funds. Such an approach to mutual fund investing can have dangerous consequences for your capital.

Unless you have the right expectation and attitude towards equity investing, it is nearly impossible to generate wealth from mutual fund investing. So what is the right expectation/attitude when investing in an equity-oriented mutual fund.

Well, the true answer to this question depends on the exact subcategory of the mutual fund you are looking at. However, here are a few generic pitfalls to avoid –

- Not a short term solution – Equity oriented mutual funds are not a solution for your short term financial goals. By short term, I mean 2-3 years kind of time frame. Invest in equity-oriented funds only if you have the necessary time it deserves. To put this in context, I started investing in an equity mutual fund in 2006, it is the 14th year as of 2020, and I continue to invest in it. I’m not suggesting that you need to stay invested for this long a period, all I’m trying to say is that you need to have a super long term approach to mutual funds. I’d say at least ten plus years (my personal opinion). Anything lower than this can be a futile attempt at wealth creation.

- Why not short term? – One of the common follow up questions is why not consider equity mutual fund for short term investments. Well, there have been instances where short term mutual fund returns have swelled. It requires a great amount of market study to figure and time this. Now, if you as a common man investing in the market can time the market, then why invest in mutual funds at all? You may as well invest in stocks directly, right?

- Understand time – You may have heard of the saying, ‘time heals everything’. Well, this is true for market volatility as well. The market is volatile; this is the very nature of this beast. However, the only way for a common man to deal with volatility is to give your investment sufficient time. Hence, a short term approach to MF investing does not work.

- Don’t keep switching – I’ve seen investors switch between mutual funds as they would switch between their browsing tabs. Switching is essentially redeeming the units from ‘Fund A’ to invest in ‘Fund B’, for no real reasons. In my opinion, this cannot be packaged as long term investing. The true definition of long term investing is staying invested in a fund across a multi-year period (and across multiple market cycles). Of course, occasionally there will be justifiable reasons for you to switch between funds, we will identify these reasons at a later point.

- Headline investing – Most investors get carried away by newspaper headlines. A headline which remotely hints at ‘bearishness’, is taken way too seriously and used as a reason to exit an ongoing mutual fund investments. I’m guilty of doing this mistake myself. Back in 2007, I pulled out of a fund that was doing very well because I read a headline saying markets are likely to go down shortly. The problem here is not just with the withdrawal; it is actually with the fact that you are breaking an ongoing investment journey. I was never able to restart this investment.

Trust me; you will do far better than most of the investing public if you understand these basic points which make a big difference to your investing journey. Here is how my investments in Mutual funds have done till date –

These are all regular funds. Unfortunately, the direct fund option was not available back in the days. The returns would have been better, had I decided to invest in the same fund, direct option. I’m in the process to transition all my regular to direct funds. Hopefully, this table should look better over the next decade 🙂

Also, I think three large-cap funds in my portfolio is an overkill, and perhaps I should look at replacing at least two of these funds with a low-cost index fund. At a later stage, I’ll share my thoughts on this topic related to asset allocation and fund diversification.

We will now proceed to understand a few of these subcategories of equity mutual funds.

9.4 – The Equity mutual fund subcategories

Under the broad classification of equity funds, there are nearly ten subcategories. As you may have noticed, the name of these subcategories is quite descriptive and gives out a general idea about what to expect from such a fund.

Large-cap fund – As the name suggests, a large-cap equity fund indicates that the fund invests predominantly in large-cap stocks. These are the top 100 companies in India, with the largest market capitalisation. The expectation is that these companies are also market leaders in the industry they belong to. These companies are also supposed to be stable and safe. Examples of large-cap stocks include companies like TCS, Reliance, Infosys, HDFC Bank, etc.

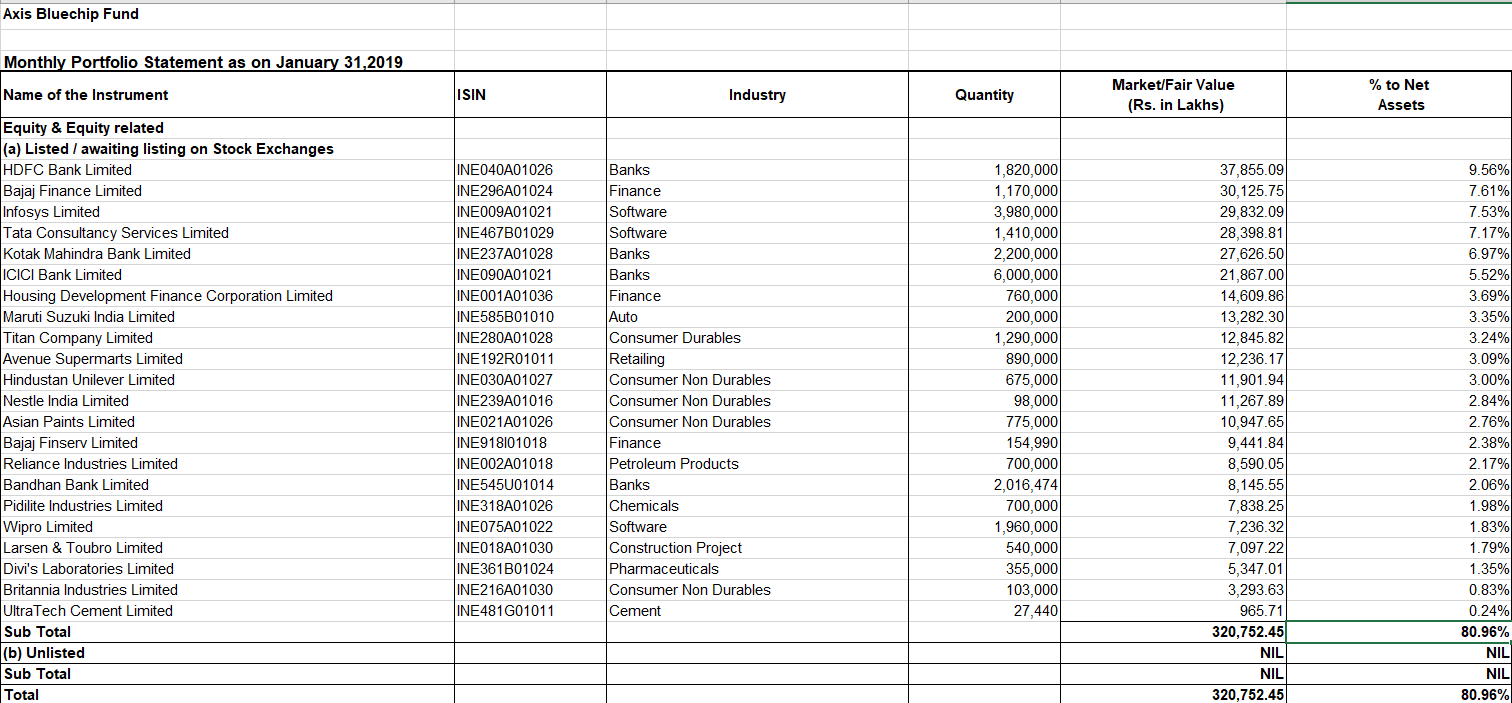

Have a look at the portfolio of one of the large-cap mutual fund schemes. This is the portfolio of Axis Bluechip fund –

As you can see, the portfolio predominantly contains large-cap stocks (80%), invested in varying proportions. The weight assigned to each stock is the fund manager’s prerogative. By the way, you may be interested to know that by regulation, once a month, the AMC is supposed to disclose the portfolio details. So go to the AMC’s website and lookup for any fund you are interested in, and you’ll find the portfolio details in the ‘statutory disclosure’, section.

Usually, when an investor decides to invest in a large-cap fund, he has a twin agenda – (1) capital appreciation in line with the markets, (2) low volatility. By low volatility here, I mean with respect to small and mid-cap funds.

In simple words, this means that the investor is looking at wealth creation but with not so much risk to his capital. Do remember, these are large-cap stocks, meant to be stable hence less volatile. Of course, by virtue of investing in the stock market either directly or via a mutual fund, the capital is exposed to volatility. Like I mentioned earlier, the only antidote to volatility is time. So it goes without saying that you need to stay invested for a long period to factor in the volatility and generate decent returns.

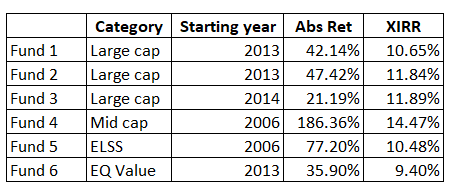

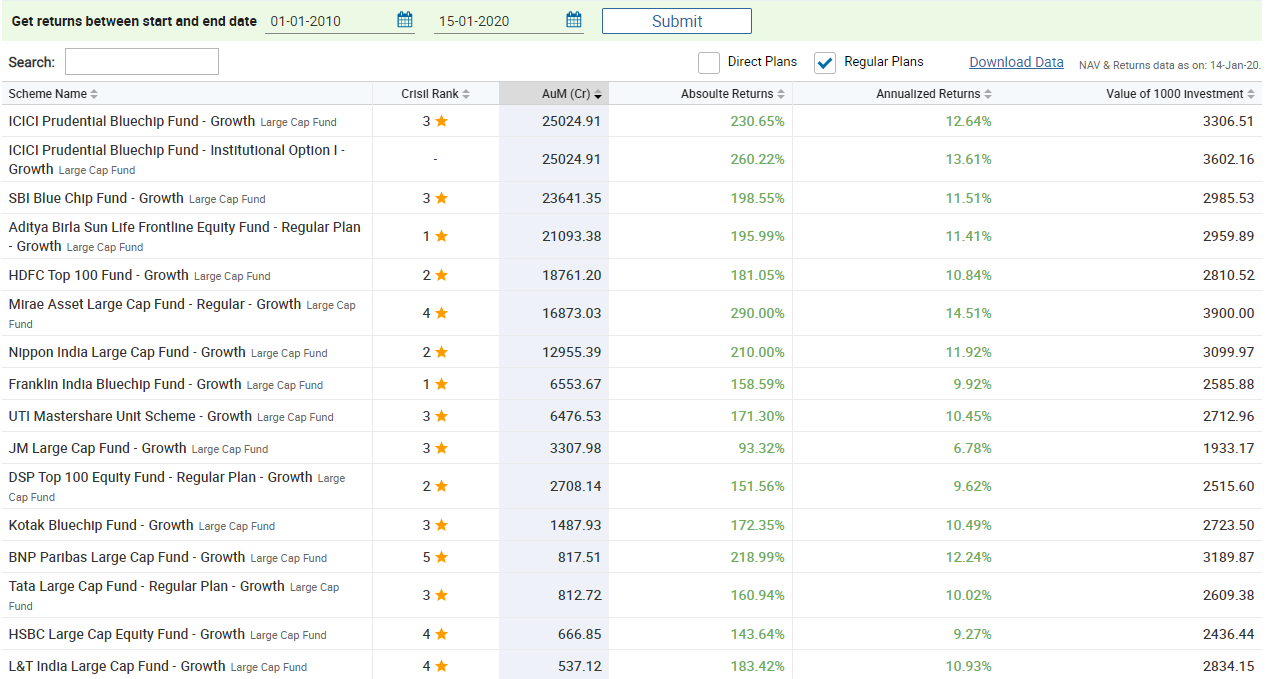

Here is a look at how the top large-cap mutual funds have performed over the last ten years. I’ve defined ‘top’, by considering the size of the fund’s AUM. I’ve taken this data from Moneycontrol –

The key point to note here is the positive return across all the funds against a long investment horizon.

Mid-cap/small cap/large & midcap funds – I guess the names are quite clear for us to know what to expect from the fund.

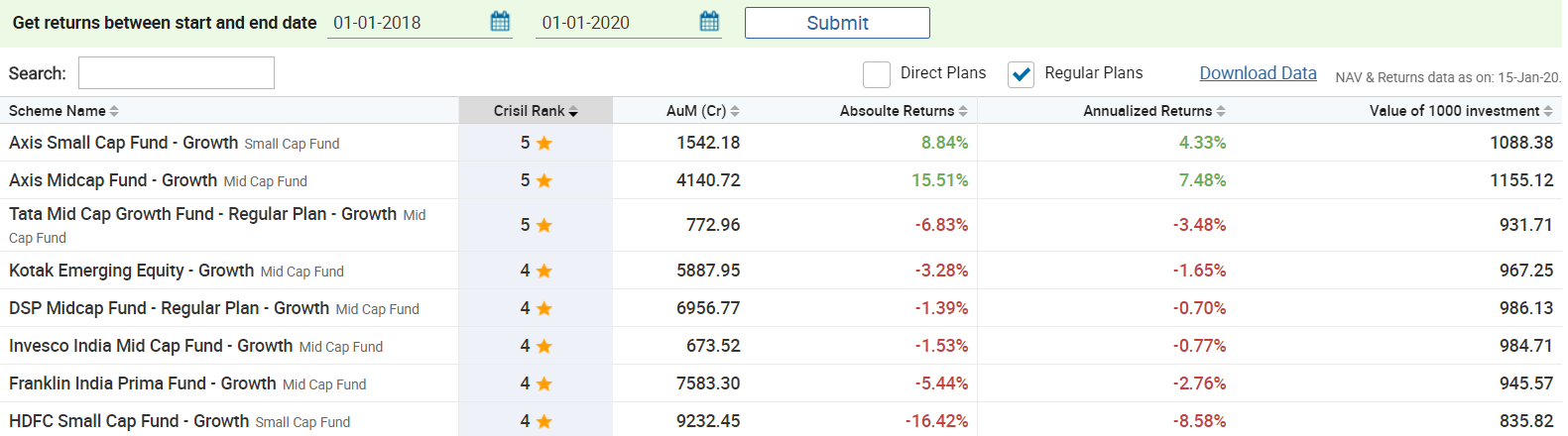

The mid-cap fund predominantly consists of mid-cap stocks and the small-cap funds contain small-cap companies. The volatility in mid and small-cap stocks is quite high. Like the large-cap stocks, investment in these funds should be long term. You cannot afford to invest on a short term basis in these funds. For example, here is how the small and mid-cap funds have performed over the last two years –

The last two years have been particularly bad for the small and mid-cap stocks, and this is evident across the fund’s returns. I’m not trying to say that the returns across all two years or three years (or any short term cycle) will always be bad. It depends on the market; however, for a common man, it is nearly impossible to time the market and calls the cycles. Hence when we invest, we should have a long term agenda, or at least have the intent to stay invested for the long term.

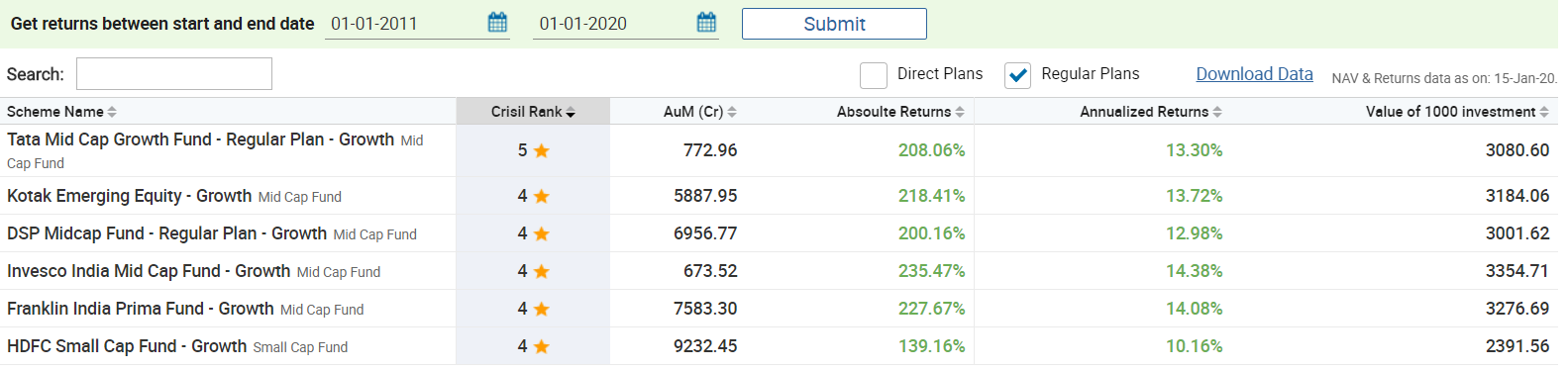

Here is how some of these small and mid-caps have performed over the last ten years –

All the funds have delivered a fairly decent positive return. Also, notice the ten-year performance of small and mid-cap funds are better than the large-cap funds; this should be evident to you because small and mid-cap funds are more volatile compared to large-cap funds.

The intent behind investing in either of these funds is the same as large-cap i.e. wealth creation over a long period. However, you expect a return much higher than a large-cap fund (against much higher volatility). This is obvious because the fund contains companies which have a long headroom for growth. As the company grows, so would the returns.

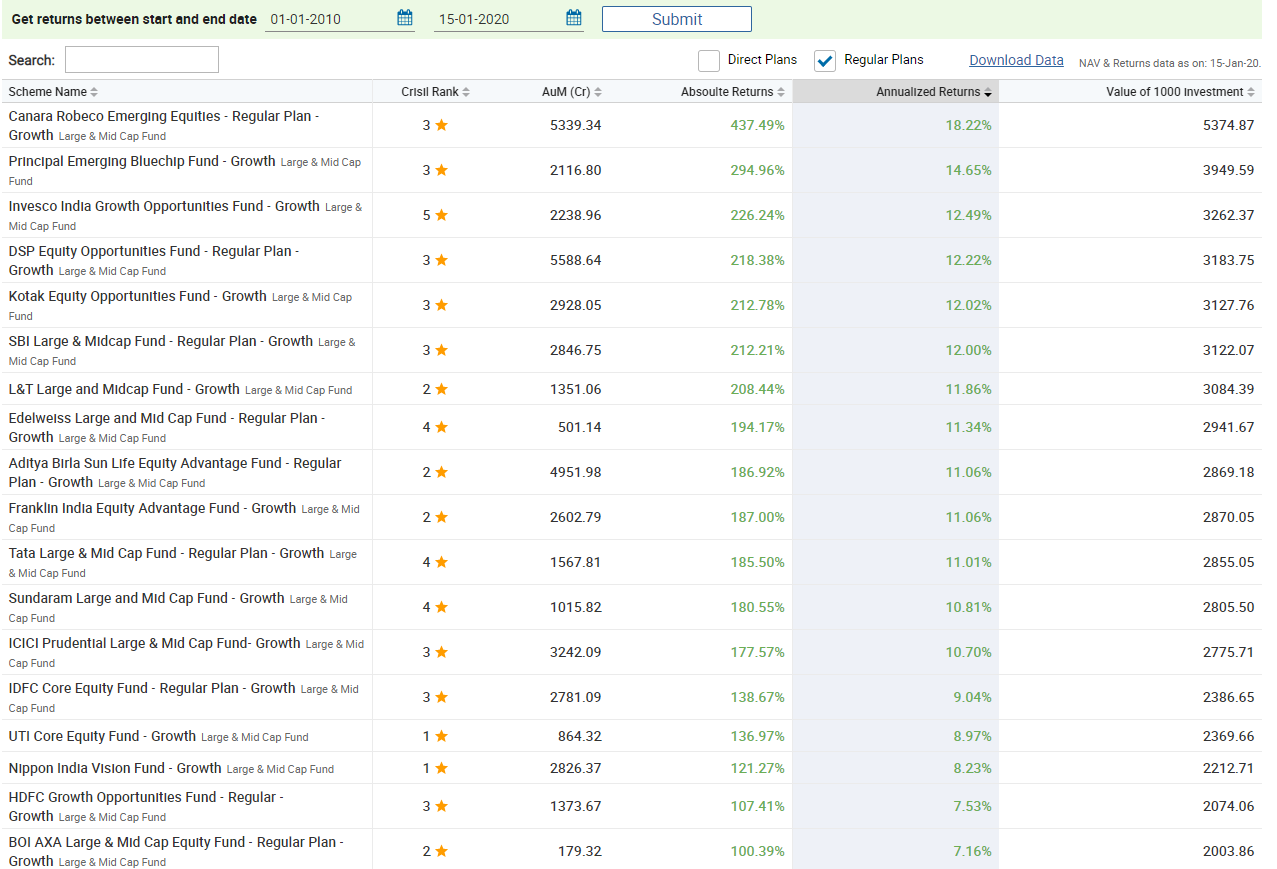

The large and mid-cap fund is a cocktail of both mid and large-cap stocks. Unlike an exclusive large/mid/small-cap fund, the ‘large & mid’ cap fund is expected to have 35% of its investment in large-cap and another 35% in mid-cap stocks. For example, this DSP large and mid-cap fund has stocks like Infosys, Airtel, HDFC Bank, and also, stocks like Hexaware, Hatsun Agro, and V Guard. Technically the fund can be a 65% large (or mid) and 35% mid (or large) cap stocks. The extent of the skew depends on the fund manager.

Since the large and mid-cap fund is a mixed bag, the expectation on the return front is slightly higher than a regular large-cap fund but lower than a small-cap fund. The risk is higher than a large-cap fund but lower compared to mid or small-cap fund. Here is how the returns for small and mid-cap stack up for the last ten years –

By the way, given that there are so many AMCs and therefore so many different funds for the same category, how would one narrow down on a single fund to invest in? Well, this is a different topic altogether, and it involves looking at various parameters on risk, returns, performance, and costs. We will take this up after we finish all our discussions on MF categories.

In the next chapter, we will discuss the remaining few Equity subcategories and then move to debt.

Key takeaways from this chapter

- Large-cap stocks – 1st to 100th company in terms of full market capitalization

- Mid-cap stocks – 101st to 250th company in terms of full market capitalization

- Small-cap stocks – 250th company onwards in terms of full market capitalisation

- Large-cap funds should contain at least 80% in large-cap stocks. Large-cap funds are expected to have lower volatility and steady returns

- Mid-cap and small-cap funds have higher volatility and return expectation compared to the large-cap funds

- Mid and large-cap stocks contain at least 35% each of mid and large-cap stocks.

Dear Karthik Sir,

I believe this section needs an update to align with the recent SEBI circular dated February 26, 2026, on the \”Categorization and Rationalization of Mutual Fund Schemes.\”

Will take a look at this, thanks.

Hi Karthik Sir,

My father started to invest in large cap growth – in regular plan from 2020 on behalf of me. but now i wanted to change it to a direct plan. should I need to redeem the fund or any suggestions?

Yes, unfortunately that is the only way to do that 🙂

Thank you so much for this great content kartik !!!

I have one doubt about nippon india small cap fund.

This fund looks great to me but one point concerns me. It has around 51000 cr of AUM which is around 12% of entire AUM of nipppn india mutual fund.My doubt is that ki kya itna huge AUM small cap segment absorb kr payega if AUM of this particular fund goes up in future ?

And If I start investing in this fund today, kya mere returns pr itne huge AUM ka negative effect aayega if AUM goes up in future ?

Abhishek, small cap is usually not as liquid as largecap stocks, so there will be some impact. But unfortunately, I dont know how this can be quantified.

Can you include information about index funds ?

We have explained that in a separate chapter.

Hello Karthik Sir,

I cannot express sincerely enough, what a saving grace your content is for financial illiterates such as myself. Never before I have felt this zeal in managing my finances.

A question though, I see plenty of both Direct and Regular schemes offered by several AMCs. As far as I can tell, there are no restrictions to what schemes we are buying. What would make anyone still choose Regular schemes in the first place? I see everyone suggests direct over regular. If that\’s the case, Why do we even have the option for regular schemes? What am I giving up by not choosing regular plans?

Thank you for your time, and everything you have created here.

Thanks Tarun, I\’m glad you like the content on Varsity!

For many out there, having an advisor who helps in managing mutual fund investments and advicing them from time to time matters. Thats the reason regular still exists, so that the distributor can earn some incentives.

Very knowledgable and seriously i have no words to express my inner happines and satisfaction.

Glad you liked it, Nabhi. Happy learning 🙂

For example, if you have a total gross yearly income of Rs.1,200,000/- then

you can choose to invest Rs.1,50,000/- in various 80C options and reduce the

tax burden. If you do so, your taxable income reduces to 1,050,000/-

This is not clear.

Please explain this and also if you can add one more example. That will be great.

Thank you

It just means that by choosing to save in an ELSS fund, you get a tax break under 80C. That means you pay lesser taxes.

Hey Karthik,

Thanks for such amazing content!

I had a question i.e. since the market is volatile, a company that is within top 100 in terms of market capital today could be in 101-250 tomorrow and vice-versa; Consider for eg. tomorrow TCS becomes a mid-cap share…

So does the fund manager keep track of all this? In order to follow the guidelines of SEBI, he will need to switch the allocation so that the veracity of the term small-cap, mid-cap and large-cap is held intact right? Or is it only at the initial time of creation of the fund that the fund manager should follow this ratio?

Yes, they will have to keep track of this and update on a regular basis.

Hi Karthik

First of all, thanks for putting out such great material. I\’m coming back from The MF Portfolio chapter and was wondering what sort of Financial Goals would justify investing in small cap and mid cap funds?

Thanks

Small cap, not sure…maybe you are young and have started investing and saving for retirement, so maybe a small portion of your portfolio could be allocated for smallcap 🙂

Hello Sir, Thank you for explaining MF topic in such a nice manner. Could you please explain about flexi cap funds also?

I think I have, if not, will try and make a small video on this, Sunil.

Varsity is a Treasure of Knowledge…Comprehensive, High Quality Content… Free of Cost…At our Fingertips… Truly Democratizing Knowledge… Great Work Karthik

Happy learning, Deepak!

Hi Karthik,

One of the fund fact sheets mentioned \”Giant, Large, Mid and Small\” as market caps. Does \”Giant\” mean 1st-50th company in terms of full market capitalization?

Thank you.

Giant? I\’m not sure about that 🙂

Hi Sir.. Is there any videos for mutual funds just like stock market.. If yes please share the link.. thank you

Not yet, but will make soon.

hi karthik,

just one doubt, they large cap fund example only 80% of the fund is allocated to large cap companies where does the rest 20% gets invested ?

It can be in cash and other companies with different market capitalization.

Sir what\’s the fundamental difference between a multicap fund and a flexi cap fund

Multicap fund has a mandate of investing 25% in large-cap, while Flexi cap is completely at the discretion of the fund manager.

Thanks for the reply Karthik.

But in the above categorisation table, you mentioned that equity funds are of 11 types. Means equity funds have 11 sub-categories.

So as per this, AMC should have maximum 11 equity funds.

So, still having the same doubt, what you mean by \”Under each category, AMC can have 1 fund\”.

Thanks

Thanks for the reply Karthik.

But in the above categorisation table, you mentioned that equity funds are of 11 types. Means equity funds have 11 sub-categories.

So as per this, AMC should have maximum 11 equity funds.

And on ICICI Prudential website https://www.icicipruamc.com/mutual-fund/equity-funds, I am seeing 25 Equity Fund cards.

So, still having the same doubt, what you mean by \”Under each category, AMC can have 1 fund\”.

Thanks

What I meant was that it can have only 1 fund under large cap, 1 under small, etc. I guess they are doing that in ICICI.

Hello Karthik,

Thanks for the educative content. 🙂

I am having doubt. You have mentioned that \”As per SEBI’s circular, an AMC is supposed to run only one scheme per category. For example, an AMC can have only one large-cap, one mid-cap, one small-cap so and so forth\”.

But when I am checking ICICI Prudential website https://www.icicipruamc.com/mutual-fund/equity-funds, I am seeing 25 Equity Fund cards.

Can you please explain how equity plan can have 25 equity funds?

Thanks

Equity is a generic term, under Equity there can be many categories. Under each category, AMC can have 1 fund.

Thank you for such a prompt response! 🙂

Good luck!

Hello Sir,

The SEBI 2017 circular mentions only Open-ended MF schemes. So, those guidelines are not applicable to closed-ended fund schemes?

Thank you.

All included I guess.

Thanks a ton for the module. Made me realise how much investing is important in life.

Good luck 🙂

Can a Fund house invest in its own company stocks? Say for example, we have HDFC Growth Opportunities Fund Direct- Growth(~ large cap fund), can this scheme invest in its own HDFC company stocks?

Perhaps they can. I\’m not sure about this 🙂

Hi Karthik,

Is there more content coming? When?

Next module is on financial modelling.

Hi Karthik,

Can you please explain little more on what the below means ? 1 to 100 , 101 to 250 , from 250 in terms of full capitalization ? Not getting what it means

Large-cap stocks – 1st to 100th company in terms of full market capitalisation

Mid-cap stocks – 101st to 250th company in terms of full market capitalisation

Small-cap stocks – 250th company onwards in terms of full market capitalisation

The first 100 companies with the largest market cap will be large-cap, the next 250 will be mid-cap, 250 onwards is small-cap. That\’s what it means.

Hi Sir,

Thank you for taking so much effort and care for the benefit of the general public. Really appreciated and inspired.

Happy learning, Pooja!

Sure sir, thank you for the suggestion. I\’m planning to invest for my own house purpose also sir. Probably for 10 years ( I\’ll be 32 by then). What would you suggest… learn fundamental analysis and prepare a portfolio for myself or go for another mutual fund?..

You can do either. At 42, being in markets for a while, I do a mix of both 🙂

Thank you for such a wonderful module sir. Recently I have graduated from college and started working. I have started SIP in NIFTY index fund and planning to hold it for retirement. Is it good thinking to hold on to single mutual fund till retirement? I\’m 22 now and im planning to hold for atleast 35 years. I have been doing swing trading in stocks but nothing for long term as of now.

Yup, that works. Btw, happy to see that you\’ve set long term targets at such young age 🙂

Review your funds once in 6 months just to be on the safer side.

Hi Sir, these are gold articles. I sincerely request you to please write articles on Personal Finance Part 2 covering aspects like major goals in a life and planning investments for that. Like here you covered retirement planning, please cover aspects like Life Insurance, Health Insurance and other major goals of life like child education, child marriage, world tour, house planning, and how to priorities luxury over basic necessary goal.

Thank You soo soo much for your valuable efforts. These are really worth gold advice.

Thanks, Prasoon. Glad you liked the content. Yes, I\’ll do Personal Finance Part 2 sometime soon 🙂

Hi Karthik,

You have mentioned that we should not change funds frequently. Is that true for ELSS too? I have noticed returns on ELSS are always lower so i was thinking of shifting all the money in ELSS that has finished lock-in period to some other fund. Is this a right thinking?

Very good material by the way. I am grateful my father made me get that SIP as soon as i started working 😊

Your father has set you on the right track 🙂

Yes, if the lockin is over, then move the ELSS funds to some other Equity fund, I\’m assuming you will invest for a long term, 10 yrs plus and still very young 🙂

Good luck!

Had a doubt while I was reading all your modules, Karthik.

With markets moving/ swinging, there is a high chance of change in the portfolio of an MF, right (a 1% change is also huge)? So, as an investor, how do I keep myself informed in the changes of the invested MF, so as to make a better decision?

Does Zerodha portal help me? Or is there a promo email I receive from AMC?

Or in the other case, how often do you think we as investors should check the change in the portfolio? (I\’m going for long-term, 3+ yrs at least)

The daily changes should not really concern you, especially if you are a long term investor, right?

Does mutual fund provide systematic increase in sip amount if market decrease and reduction of SIP as Market has risen above average

Ah not really, you will have to manage this yourself.

Sir, thanks for the educative content. Can you please let me know how to convert regular funds to direct funds? I invested through Geojit, was unaware of Coin back then 🙁

Nisha, you will have to sell the regular funds and then buy the same funds in direct mode.

Which is the tool that you use for finding top MFs based on AUM?

As of now, 3rd party websites like morningstar.

Question on buying stock vs Mutual fund

On one side, when we think of buying stocks by ourselves along with Fundamental analysis

(ofcourse), we consider the valuation of the company , PE multiple and look at the chart to find good entry price to buy. However, sometimes the stock looks very expensive so we make a decision to not invest in it for the time being, but may consider to buy it at later point when its within my price range.

On other side, before investing in mutual funds if we find that NAV of fund is high (Thanks to bull market). Is it right moment to start invest in it ?

Can we have a same rational thinking while buying Mutual fund as we had for stocks as I mentioned above ?

Thank you

The next chapter is exactly on this topic i.e. how to analyze an Eq mutual fund. Hopefully, I\’ll upload the same t\’row.

Is it a bad sign if a fund manager is managing too many funds?

I saw a fund manager from L&T AMC is managing more than 10 funds (in value research portal)

Hmm, not really. There will be professional investment teams for each fund.

Thanks a ton Karthik Sir…yes also doing this will save my future commissions 🙂

Good luck!

Hi Sir…

Just need your guidance on above regarding starting direct MF plan….. a Rather selling my existing regular plan ..i will just stop it and keep the money invested in the fund..will not sell it and will start new SIP with same fund with direct plan…is it possible to do that and will that be right strategy to do?

You can do that as well. Just that you will continue to pay commissions as long you stay invested in a regular fund 🙂

Hi Karthik Sir,

I am really in a love with the content and awareness you are creating really appreciated.

I had just one query on the below….

It\’s been almost 1 yr i am investing around 20k in Equity MFs through regular plan and also 10k in debt Fund also regular plan…. Should i convert it to direct plan or should continue with regular plan? Is it possible to convert regular plan to Direct plan keeping my same sip in same Fund?what is the procedure for the same?

This will really help to get great return..thanks in advance sir…please let me know your suggestion…

Any rough idea how much commission Adviser takes? Or how much return can i earn more with direct plan as compared to regular plan?

Thanks, Sandip!

I\’d suggest you switch to direct plan, but there is no easy way to do this. You will have to sell regular and buy direct.

Karthik, I invested in the Tata Health Pharma sector fund with a SIP of 500 monthly, so would you please let me know how long should I stay invested in this sector fund?

As sector funds are more volatile and dangerous but I am in my starting of career so that\’s why I thought of investing in the Pharma fund.

Appreciate your response on this.

Rohan, I\’m just not a fan of themes and sectoral funds. These are very cyclical and should be avoided. You are better off selecting a good equity diversified fund rather than a sectoral fund.

Suppose a large cap fund manager comes to the conclusion that the market is going to fall big in next 3 months. In this case, will he/she can just sell all stock and convert to cash and wait till market bottoms? Or he has to maintain 80% assets in those stocks according to SEBI rules and let the NAV drop?

He can move to cash for a short time, but not for an extended 3 month period.

Hi Karthik,

Thanks for such a wonderful chapters in simple language.

My query is, in all above charts you have selected for regular plan and its returns.

1. Why you selected regular plan as you reommand direct plan?

2. In same chart if we select direct plans then the return will be higher than regular plan?

1) No specif reason as such, I should have considered Direct actually 🙂

2) Of course. Direct if best if you know what you are dealing with.

hi karthik.

1-2, not more than that.

plz provide reason on it according to ur experience.

It will be overkill, thats why 🙂

hi karthik ,

according to u how many funds are optimum and sufficient in each category in a portfolio .plz answer it with a reason and logic

1.ELSS

2.index funds or etf

3.multicap

1-2, not more than that.

how to download nest software ?

thank you sir

Welcome!

sir ,

I have heard P.R Sundar sir saying that one can give MF as collateral and use it for margins , could you please explain about this in any separate chapter .

thank you .

Yes, few brokers accept FDs and MFs as collateral. For now, we accept only stock in demat.

Sir…first of all…thank you…mmyou have been a pillar of support for my dreams.thanks alot.maybe ill meet you someday day as a successful investor and a trader.now coming back to my question.are you planning to come up with something on exchange traded funds.i want to know about them.

Thanks for the kind words, I hope you do become successful 🙂

Yes, will include ETFs in this module.

Ok sir, these materials are very helpful. They have given a hope that I can really start investing in stocks. Very appreciable

Good luck, Piyush!

Is it correct if I switch now as my funds have negative returns now….shall I wait for my funds to give me positive return (when market recover), or should switch now with a loss??

Yeah, do wait and also check for the impact of tax.

I didn\’t understood from the article. Please tell me if I move from regular to direct from a fund…. whether I will loose any value of my investment. Or I will be allotted full. Is there any cut happens while switching?

To switch to direct, you will have to sell the entire lot in regular MF and rebuy the same in direct mode.

Hi brother, I have 4 mutual funds ( 1 small cap, 1 mid cap, 1 contra fund and one elss) in regular scheme. I opened it 1 and half year ago in monthly sip. Should I switch to direct coz the expense ratio is quite high. In every fund it\’s 1.5 % high.

Yes, it does make sense to switch and save costs right? Check this – https://support.zerodha.com/category/mutual-funds/moving-to-coin/articles/how-do-i-convert-my-regular-mutual-fund-investments-to-direct

Thank you so much for taking the time to reply sir.

Happy reading!

Karthik,

Quick question, I was just reading \’ One up on Wall Street\’ book and in that it mentions to keep a track on insider buying of the stock and growth rate of company. From Indian market perspective, where can we check the information of insider buying and does growth of company (CAGR) takes in account only sales, profit, earning or there are other factors as well we need to add in stock screener to get the results out of it?

Thank You.

That\’s quite tricky. Maybe you can track promoter buying, but that\’s already factored in. CAGR can be applied to any parameter – sales, income, EBITDA etc.

Hi Sir,

1) I am having a doubt in ETF\’s. An ETF belonging to a particular category of index should always mirror the price increase of the respective index right? What I am observing is if a Nifty 50 increases by 0.76 %, the ICICINIFTY which is of the same category increases only 0.46%. I am aware there will be a tracking error but a difference of > 1% is something I don\’t understand.

2) Today(15th April 2020) I saw two Gold ETF\’s showed a huge difference in increase in price. AXISGOLD is up by 7.95 %, GOLDBEES is up by 0.42%. Why is there a huge difference when both the ETF\’s are supposed to track the price movement of Gold?

Appreciate your help, sir!

Regards,

Tharun

1) ETFs mirror the index, both up or down. The difference is because of both tracking error and illiquidity of ETFs

2) This is true, unfortunately, because of the horrible liquidity.

Sir,

1) As you said, do the investments for long term or a minimum of 10 years span. But as an investor, if he did around 2 or 3 years, then he was not able to continue as a SIP, but he not withdrawing it, just keeping there. In this case what will be the return outcome?

2) Is there any case a MF stopped or closed with or with out prior information\’s, and the investors lost their investments?

1) He can do that. Returns will depend on the market

2) Nope, not that I\’m aware off

Thanks a lot for beautiful explanation and info.

If u can make a book or e book compiling all chapters above, would love to buy it, we all owe u that much at least.

Rgds

We will make a PDF of this but only when the module is complete. You can always download it and print it 🙂

Sir, it the pictures, you have compared the 10 year returns. Which site have you used to provide us the data?

I\’ve used Moneycontrol site for this.

Hi sir,

I was looking to invest in MF through Zerodha coin since the market is highly volatile now, I thought i will invest in Index funds. How do index funds work sir? All your articles help people like me to invest in stocks with broader knowledge.

The index fund follows the behaviour of an index. I do plan to write about this in the coming few chapters.

I also have one more query. Do Fund Managers of Mutual Funds also actively trade in the stocks held, through day trading or short term trading?

Hmm, day trading no. But they do have active positions, especially in arbitrage funds.

Dear Karthik,

Excellent study material. Zerodha University is definitely one of the key factors in making Zerodha a immense success story. Opened Zerodha account six month back and investing in equity. Want to invest in MF also through Zerodha Coin. Particular interest is the low cost index funds as mentioned by you. How ETF is different from MF? Are there any advantages of ETF over MF?

Also eagerly waiting for the other chapters in this series as mentioned in the beginning.

Hey, thanks so much for the kind words 🙂

I\’m adding the next chapter today. The plan is to write something comprehensive on ETFs as well 🙂

Thanks. I will be eagerly waiting.

Very informative information. Request to provide the complete information regarding Mutual Fund. Eagerly waiting.

We are working on it. Will add more content in the coming days.

Where is Equity Scheme Part 2 article ?

I\’m working on it, will be posted in a week 🙂

Why u stopped \”opinion\” on varsity app sir?

Keshav will restart that in a week or two 🙂

very useful article sir…please give its pdf…

The PDF will be available one when the module is complete. This module is work in progress.

Please provide download link on below this chapter

The PDF will be available once the module is complete. This is work in progress.