27.1 – Overview

Before we get started with this chapter, I need to inform you that this chapter (and the chapter on Index funds) is not authored by me (Karthik). These two chapters are authored by Bhuvan, a brilliant colleague of mine, who is quite knowledgable on this topic and asset management in general.

In fact, the next chapter on asset allocation will be authored by another gentleman (and a good friend of mine) from the industry who is super knowledgeable about everything related to market finance.

I’d like to thank these folks for helping me with this module and sharing their wisdom with all of us.

Read on.

—

In chapter 6 & 7, we discussed the basics of a mutual fund and how it works. In chapter 16, we specifically talked about index funds. I had mentioned that we would discuss a relatively new category of funds in the Indian context called smart-beta funds and ETFs, but this got delayed. The idea with this chapter is to give you a working knowledge of these funds.

The term smart-beta evokes a lot of strong opinions among investment professionals. Although it sounds fancy, it largely means nothing and is largely a marketing term. Smart-beta broadly speaking is a catch-all term for factor investing and any weighting methodology which deviates from traditional market-cap weighting. If you remember from the previous chapter on index funds, an index fund tracks a market-cap-weighted benchmark like a Nifty 50, Nifty 500 etc.

Just as a refresher, a market-cap-weighted index weights stocks based on their market cap (outstanding shares X current price). Higher the market cap, higher the weight in the index. Nifty 50 is an example.

Similarly, there are ETFs based on fundamentally weighted indices. For example, an index that weights stocks based on earnings, a combination of fundamental metrics such as earnings, dividends, profitability etc.

27. 2 – What is a factor; you might be wondering?

A factor is a broad, persistent driver of the returns of a stock. Put another way, in factor investing, you target securities that exhibit a particular characteristic that drives their returns. Remember this definition, and we’ll come back this in a bit. But before we do, it is also important to understand a little bit of history for context.

Factor investing results from continued academic research starting with the Capital asset pricing model (CAPM), efficient markets hypothesis (EMH) etc. CAPM states that a single factor, the market factor or beta, drives returns, but this didn’t stick. Factor investing became mainstream when Eugene Fama and Kenneth French published their landmark research paper The Cross-Section of Expected Stock Returns.

In the paper, Fama and French added two more factors – Value and size and market factor. This meant that there were other drivers of stock returns than just market risk; this was what came to be known as the Fama French 3-factor model. In 2014 this became a 5-factor model when two new factors— profitability and investment factors were added.

Apart from the famous Fama French factors, other factors like Momentum and Low Volatility also have been discovered. What do these factors mean? Here’s a nifty explanation from Robeco of the most commonly used factors:

| Value | The tendency of inexpensive securities, relative to their fundamentals, to outperform over the longer term. |

| Momentum | The tendency of securities that have performed well in the recent past to continue to perform well, and for securities that have performed poorly to continue to perform poorly. |

| Low risk | Refers to the observation that low-risk securities tend to earn higher risk-adjusted returns than high-risk securities. |

| Quality | The tendency of securities issued by sound and profitable companies to outperform those issued by less sound and profitable companies, and the market as a whole. |

| Size | The tendency of bonds issued by companies with little debt outstanding and small-capitalization stocks to outperform the market. |

So, investors look for stocks that exhibit these traits and then build these factor portfolios.

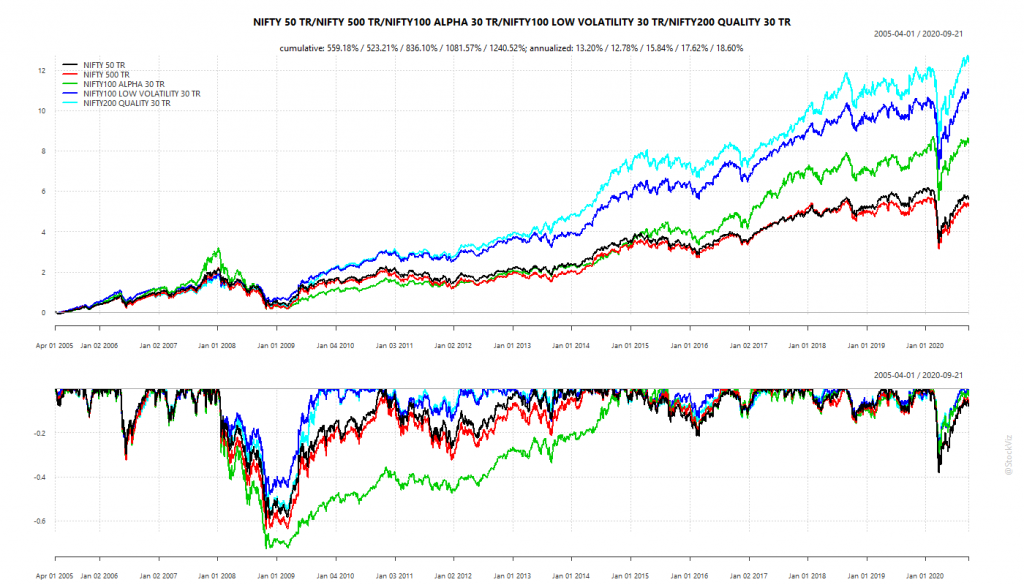

How have factors performed in India? There isn’t much data in India, and most of the factor or smart beta indices are pretty new. But here’s how momentum, quality, and low volatility have performed vs the Nifty 50 and 500.

The charts are from Shyam who runs Stockviz.

Impressive returns all around. Low volatility, in particular, has been impressive with shallow drawdowns. Nifty Alpha, a proxy for momentum has been impressive but comes with sharp drawdowns.

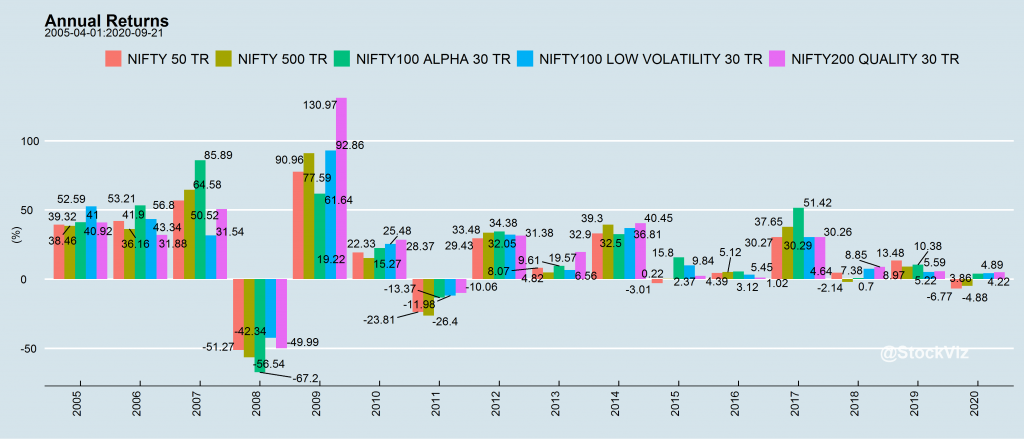

Here are the annual returns for a more granular look.

The charts are from Shyam who runs Stockviz.

But, it’s also important to understand why these factor premiums exist in the first place. There are broadly 3 reasons market practitioners and academics propose:

Risk-based: Factor premiums exist because investors need to be compensated for the additional risk they bear. For example, academic literature shows that value stocks, i.e. cheap stocks, tend to outperform expensive stocks over the long run. But cheap stocks more often than not tend to be cheaper because they have a higher chance of going bankrupt. Or in the case of an economic downturn, value stocks will be the first ones to go out of business.

Behavioural-based: This camp believes that these factor premiums exist because of behavioural biases among investors. For example, this camp says that the value premium exists because investors chase glamorous growth stocks and ignore cheap stocks, i.e. your value stocks. Similarly, this camp believes that the momentum effect exists because of investor under-reaction and overreaction. They under-react to good news or good earnings and then over-react, causing a feedback loop which pushes prices higher.

Structural issues: This camp says that factor premiums exist because of structural reasons like illiquidity, high transaction costs, difficulty in applying leverage etc.

Like with all things, it’s not just one thing, and it might be a combination of multiple reasons. Humans are complex beings, and the markets are complex adaptive systems. It would be unwise to conclude anything else.

At this point, you might have ignored everything I just wrote after the charts because the returns look so good. But, not so fast. In investing there are no free lunches except for diversification probably.

27.3 – Smart-beta funds in India

Smart beta or factor funds are relatively new in India. The first smart beta ETFs were just launched about 4-5 years back. There a few quant funds from Reliance, Tata, and DSP. But unlike a smart beta ETF, the methodologies of these funds aren’t fully transparent.

Having said that, these are just index returns, and real-life trading performance is always different due to costs, slippage, changes in market microstructure etc. Our markets have evolved a lot since 2005 from when these indices start. You could argue that they have become a lot efficient.

Given that we are just seeing the launch of the first few smart-beta funds in just the last few years, we don’t have a lot of live trading data yet. But here’s how quality, value, and low volatility ETFs have performed vs Niftybees

This data is from 2019, and it’s not a lot to conclude, but it is evident that not all factors perform all the time.

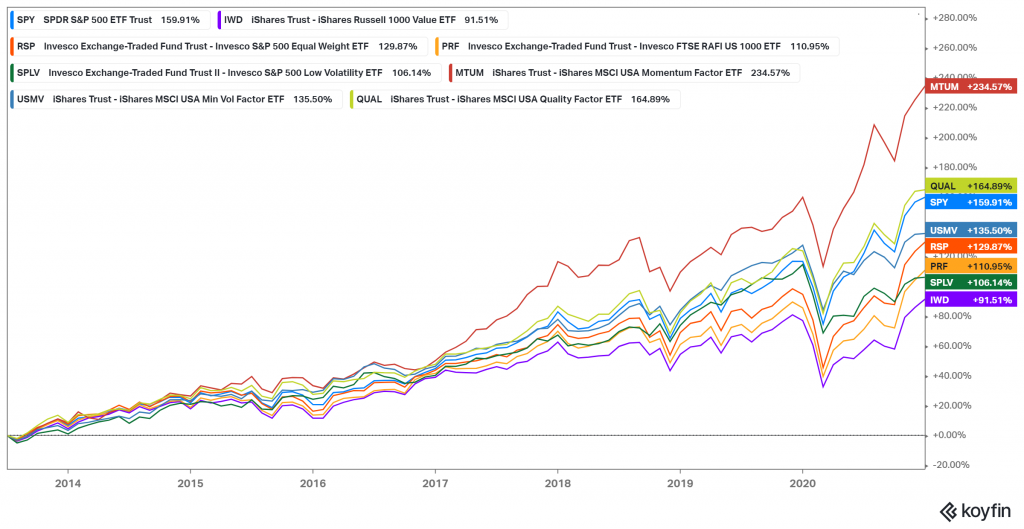

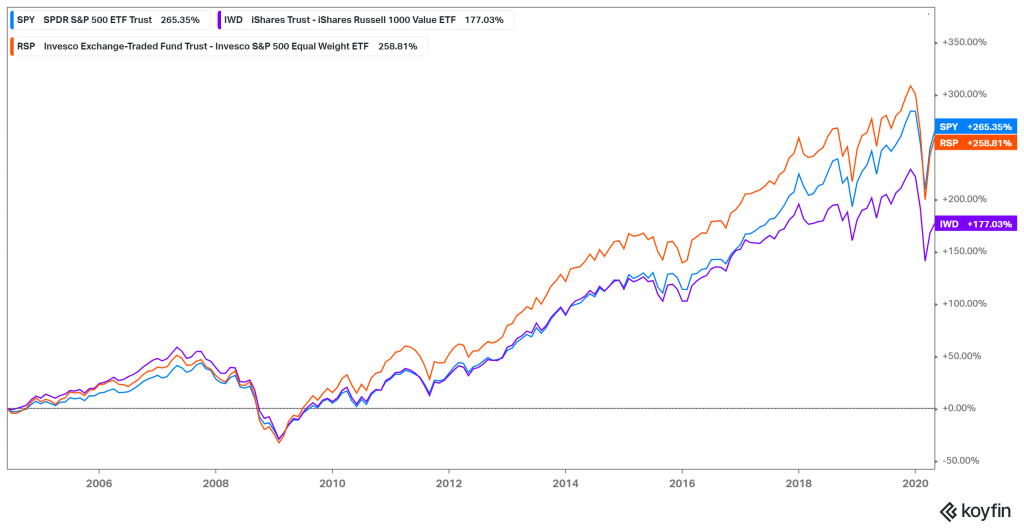

Factor or smart beta ETFs have a longer trading record in the US and here’s how some of the popular smart ETFs have performed vs the S&P 500. Of course, this chart is subject to starting point bias because this was the point from which continuous trading data was available for all major factor ETFs but didn’t change the conclusion.

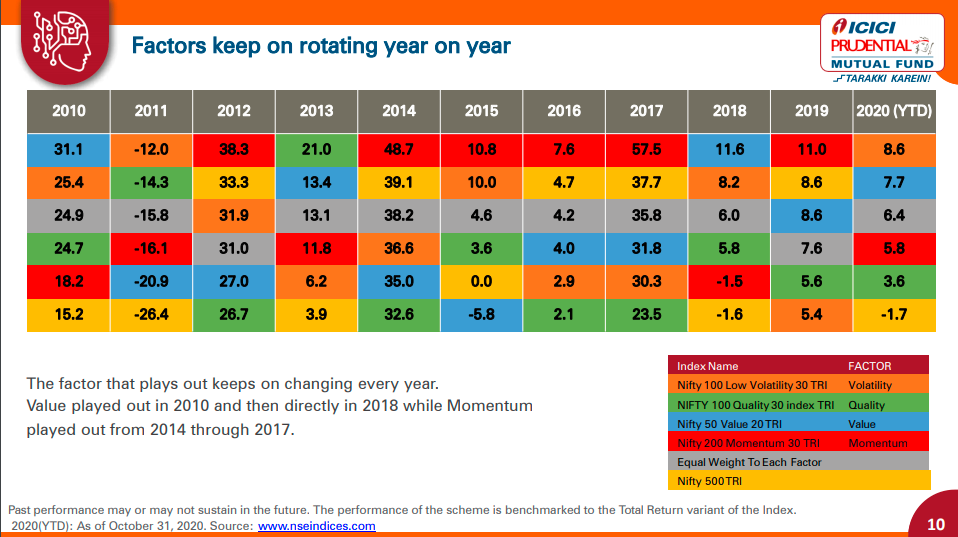

As you can see, factors are cyclical and can go a long time underperforming simple broad market index funds. Here’s data in the Indian context, notice how the top factors keep changing.

Value (IWD) has underperformed the S&P 500, dominated by growth stocks for over a decade now. Mind you; I’m using these US examples since the data is readily available and the Indian markets aren’t the same as the US.

Now imagine if you had put 100% of your money in value, not that many would. Now bear in mind that, no two factors ETFs are the same. Each factor can be defined and implemented in 100 different ways. For example, as defined in Fama and French’s paper, the value was the price to book, but each value ETF or index has a different methodology such as price to sales, EBIT/TEV, forward earnings, or a mix of value metrics. This leads to a wide dispersion in returns among the same or similar funds.

27.4 – Do smart-beta funds work?

There are broadly speaking two views of thought. On the sceptical side, many people view factors as backtests and that they are a result of data mining that doesn’t work as advertised. Then, there are a few who believe that they might have worked in the past but don’t anymore.

On the other side, you have true believers in factors. Several asset management companies manage 100s of billions on factor strategies. Dimensional Fund Advisors (DFA) was most notable among them, which was founded by David Booth and managed over $500 billion in assets in various factor strategies. David Booth was a student of Eugene Fama at the Chicago School of Business. Fama also serves on the board of DFA.

I personally think that factors do work overtime, but the factor premiums aren’t static; they ebb and flow over time. You have to bear a lot of pain for that premium and have really long-term horizons to harvest that premium.

Having said that investors also must be cognizant that the markets have indeed changed and keep changing over time. In the 90s, when the first factors were discovered, you could argue that the markets still had many inefficiencies and retail investors still made up a good chunk of the markets.

Today, everybody has all the data at the click of a button on smartphones, and there are millions of CFA holders, hedge funds that manage trillions of dollars constantly seeking new inefficiencies. Even in India, mutual funds, PMS’, AIFs, HFT traders, institutions have become dominant players in the markets.

Have the factors been arbitraged away? Unlikely, investors shouldn’t just look at past returns of indices and backtests and have the same expectations. The probabilities are the premiums might not as be as large as they seem.

The proliferation of data and computing power has also led to 100s of new factors resulting from data mining. If you look at the backtests of some of these factors, they look amazing, but they are spurious at the end of the day. Practitioners and academics have termed this as the “factor zoo”.

27.5 – Should you invest in smart-beta funds?

I do not think investing 100% of your equity allocation in smart-beta funds is a good idea. Nor do I think that smart-beta funds should be viewed as replacements for index funds or good diversified active funds that perform consistently – emphasis on good and consistent.

But we’ve seen in the previous chapter on index funds that a vast majority of active funds don’t beat their benchmarks. I do think smart-beta funds are a good replacement for poorly managed discretionary active funds. The bulk of your equity allocation should be good consistent diversified active equity funds or in index funds. And then you can invest in smart-beta funds for that chance of extra returns.

But do remember, factors can go a long time underperforming simple index funds. These premiums are also sensitive to the amount of money chasing them. So, as more such funds are launched in India, and more money flows into them, the factor premiums might not always be as large as they once were. Remember, there are no free lunches in the markets, and every choice you make as an investor comes with trade-offs. You need to endure that pain if you hope to harvest those additional returns, say, a simple index fund.

One solution is to diversify among factors, there are multi-factors funds that invest in multiple factors, but we don’t have many of those in India yet. ICICI alpha low volatility ETF, which was recently launched, combines two momentum and low volatility. Similarly, DSP Quant Fund and the likes of Tata Quant Fund also are multi-factor funds. But their methodologies aren’t as transparent as index-based smart beta ETFs.

We see AMCs slowly launching these funds, and hopefully, we’ll have more choices in the next couple of years.

Key Takeaways from this Chapter

- The idea with this chapter was to give you a working understanding of smart beta and factor investing. I think you need to dive deeper if you wish to allocate to these funds. There are some amazing resources on factor investing, and a cursory Google will surface them. Please dive deeper before investing in these funds.

- Smart beta is just a marketing term. There is no smart beta or dumb beta.

- Smart-beta funds are nothing but factor funds or funds that have alternatively weighted indices unlike Nifty 50 which is market-cap-weighted

- The live performance of factor funds can be different than the indices.

- Factors can be highly cyclical, and individual factors can underperform simple diversified funds or index funds for decades.

- If you want to invest in factor funds, diversification among factors is an important consideration.

- Investing based on the past performance of factors is a terribly bad idea.

Will there be a chapter on different factors seprately like momentum, value?

Like how these funds manage these strategies so that we can learn and decide if it\’s for us. Example being momentum has outperformed benchmarks in backtests for 20+ years, but the backtest does not contain impact costs like expense ratio and more importantly 6 months rebalancing churn.Although even after the impact costs, these do well.

Would love if you can explain these terms, thanks for everything you have put through these modules!

You can actually backtest post charges. That said, I dont really have a plan for different chapter. However, do check the fact sheet of the fund you are interested, you will get a fair idea of what to expect and if the fund is for you or not. While you read the fact sheet, you need to be aware that its a marketing doc, so be critical of its content 🙂

I am a big fan, Thank you for writing these modules. but please write this chapter as well in your words. its quite complicated to understand.

Ah, thanks for the kind words, Sheena. I\’ll look into this again 🙂

Hi can you please share the list of smart beta ETFs available throgh zerodha.

If you have a specific ETF in perspective, then please look up for that on the market watch in Kite.

Please give me consistency perform smart alpha &

Beta

List with return 1,2,3,4,5,6,7 year details

Sorry, not sure what you mean by this 🙂

Change of Author is noticeable This chapter was difficult to understand. as it is not explained in layman terms.

Yeah, each author is different 🙂

I have trading account in zerodha, how can I invest in smart beta etf?

Please do call the support desk for this, they will be happy to guide you through it.

Really enjoying this module. It\’s factual and easy to understand.

There\’s one more factor coming up in funds – weightage. What are your views on it? Basic google regarding seemed like a good factor to me.

It is interesting, weights play a big role in how your returns roll. 🙂

Hi Karthik sir and members, I have went through Personal Finance module and was wondering if we can consolidate all the available (atleast) Equity funds and assess them on standard set of parameters like rolling returns, standard deviations of it, 3/5/10 year XIRR, their Sortino ratio, alpha etc. so that one can shortlist top risk adjusted candidates without being biased just because of name/reputation/unawareness of other funds. Please let me know if it will add any value, I will start compiling it and will share it. Thanks!

That will be nice, maybe you can compile, share, and publish it for public good 🙂

The way you explain things are so simple and easy to understand highly impressed. I would request you if you can start writing about analyzing different sectors like Banking Module, Chemical Sector Module etc., That would surely help people like us.

Thats on the list of things to do, Naveen 🙂

Ok sir, will do it. But the best attribute about you is you reply to every comments. I wish I can thank you physically.

Your wishes are good enough for all of us. Happy learning, Jyoti!

Great resources of innovative knowledge.

Help-Can you please guide how to search smart beta funds in Coin app. I searched typing value, some funds popped up. Is it the right process to search smart beta funds?

Jyoti, Coin search should lead you to these funds. Please call the support if you have issues finding them.

Dear Karthik Sir,

Just a simple suggestion, would you able to write the date on the top of when the chapter was released? So one can know if this is a new chapter or old chapter?

Secondly, when ever you edit a previous chapter, can you make the edits in a different color or show us the edit history so if I have read the chapter I would know what has been edited and understand better?

Thanks for the good stuff sir,

If possible could you share a mailing address so that I can send you sweets as a token of thanks?

What you have helped me with, I will never be able to repay you so the least I can do is send something like this.

just one clarification. Like in Stocks, if a company gets bankrupt like RCOM, DHFL etc then the price falls…. Say if I invest in NIFTYBEES. If in future Nippon company itself get into some trouble like almost bankrupt, then will my units of NIFTYBEES be safe??

Then most likely the company will be bought over…btw, Nippo bought Reliance capital which bought Benchmark Asset management if I\’m not wrong.

Hii Karthik !!

I love your way of teaching complicated personal finance in a not so complicated manner.

I would love it if you also include a module/lesson on NPS and compare it with MF.

Thanks for the kind words, Anvesh. Yes, plan to include that as well. Hopefully soon 🙂

Hi Karthik!

Can\’t thank you enough for the basics on stock markets module, I was wondering if you would add smallcases here or anywhere in a separate module?

Sincere gratitude and regards,

Thanks, Manav. No intentions of adding a chapter on smallcase, let me check though.

With ETFs, you have to worry about the liquidity and ensure you are placing the orders at the iNAV. And ETFs make sense if you have some sort of a tactical investing strategy.

Had written about it here: https://tradingqna.com/t/what-is-an-etf-and-how-does-it-work/66411

With index funds, you don\’t have to worry about anything.

Hi,

I am curious to know how can I invest in foreign exchange markets through mutual funds, e.g. some fast developing economies such as Vietnam.

Maybe we can use some chapters to explain this as well 🙂 .

Thanks.

Which is the best SIP schiem

Please tell B\’s me.

Do check this chapter – https://zerodha.com/varsity/chapter/how-to-analyse-an-equity-mutual-fund/

Hey Kulsum,

Thanks for your explanation, am asking the pros and cons of buying(SIP) ETF\’s directly from the trading account instead of investing in an index fund MF (SIP).

Great explanation,

If we want to invest(SIP), Nifty 50 ETF (or) Nifty 50 index fund, which you will suggest and why.

Thanks.

Hey Yuvaraj,

Nifty 50 consists of 50 biggest stocks in India and Nifty Next 50 consists of the next 50 biggest companies. Nifty Next 50 tends to be far more volatile than Nifty 50. So you can compare how the indices behave and then match that with your risk capacity, risk tolerance and your goals and then you can figure out where to invest – either Nifty 50, Next 50 or a combination of both.

//Investing based on the past performance of factors is a terribly bad idea.//

I don\’t agree with this, it\’s an important part of fundamental evaluation of stock.

Also I don\’t agree with calling value stocks as cheap stocks, I think value investing itself one main stream just like growth investing.

This is my opinion only

Just investing based on past performance was the qualifier to be specific 🙂 Of course, you have to consider it, but most retail investors just look at the past returns of factors.

>> Also I don’t agree with calling value stocks as cheap stocks, I think value investing itself one mainstream just like growth investing.

As the saying goes \”value lies in the eyes of the beholder\”. When talking about the \”Value factor\”, you are talking about stocks that are cheap based on a metric like P/B or a combination of metrics.

Nice explanation

Happy learning 🙂