20.1 – Expense Ratio

In the last chapter, we discussed the ‘Rolling Returns’, and why rolling returns offer a better insight into the return pattern compared to a simple point to point return. Continuing from the previous chapter, we will discuss a few more important metrics related to mutual funds.

In this chapter, we focus on the expense ratio of a mutual fund. Of course, this is the 20th chapter in this module, and I suppose we have mentioned ‘expense ratio’, in passing multiples times. However, we never formally introduced the concept of the expense ratio of a mutual fund. So let us do that before we proceed.

Think about services like Tata Sky, Netflix, Swiggy, or even Dunzo, these are all services that you consume fairly regularly (I assume) and therefore you pay for it. Why would you pay for it? Well, because there is a real cost involved. For example, a Dunzo executive has to ride his bike to the store, pick up the item, deliver the same to your house. So there is fuel, labour, tech, and other expense involved. Hence we pay a fee to cover for these costs plus a tiny bit extra which adds to the profit of the company.

Likewise, managing your investments in a Mutual Fund is also a service and the service is offered by the Asset Management Company (AMC), and needless to say, you have to pay for it.

The fee mutual fund charges are called, ‘The Total Expense Ratio’ or TER.

Why do the AMCs charge? Well, they have expenses to bear – custodian fees, Trustee, RTAs, fund managers, admin, brokers, distributors, advertisements, and of course, as a business, they need to be profitable too.

At this point, there are two possible paths available to us – deep dive into what, why, how of TER or get a working knowledge of TER.

I prefer we stick to the latter. As a Mutual fund investor, all you need to be aware of is that mutual fund investments are not free, and you have to pay for it.

However, most of the first time investors would like to believe that mutual fund investments are free because they never make an explicit payment to an AMC for the fund management services. In fact, no one explicitly pays an AMC.

The service fee, i.e. the TER is charged in a very convenient and hassle-free manner, so much so that you wouldn’t even know you’ve paid for it 🙂

As a mutual fund investor, all you need to know is –

- How is the fee charged?

- How much is the fee charged?

- Techniques to save on TER.

I’ll use a very simplified example and address these questions. The idea is to give you rough working knowledge on TER and not the exact math behind.

Assume a certain AMC charges a TER of 1%, i.e. a fee of Rs.1,000/- per year for every Rs.1,00,000/- invested. Now, this fee is not collected from you the moment you invest or on a monthly/quarterly/half-yearly or yearly basis. The fee is collected from you daily, without even you being aware of it.

Let me explain –

Rs.1,000/- is the charge on an annual basis. If you do the math, this works out to –

1,0000/365

=Rs.2.73/-

So as long as you are invested, Rs.2.73/- is deducted from your funds daily. The question is, how do they charge and take this money on a daily basis.

Assume the starting NAV of the fund is Rs.10/-. Since you’ve invested Rs.1,00,000/- you are entitled to receive

= Rs.1,00,000/10

= 10,000 units.

After you invest assume the very next day the fund gains 1%. That means, the new NAV is –

=10*(1+1%)

= 10.1

And the value of your investment is

= 10.1 * 10,000

= Rs.1,01,000/-

However, the AMC needs Rs.2.73/- from you as a fee. Hence they will deduct this money from the value of your investment =

Rs.1,01,000/- minus Rs.2.73/-

= Rs.1,00,997.3/-

Or the actual NAV applicable (and declared) is –

= Rs.1,00,997.3 / 10,000

= 10.09973.

Note, the NAV is 10.09973 after deducting the TER. Before TER the NAV is 10.1.

So the point to note is –

- The NAV that is declared is after deducting the TER

- The money is collected from you from your investments

- Money is deducted daily

Now in the example, we worked with the assumption that the value of the investments increases by 1%. Even if the value of the fund decreased, the fund will still go ahead and charge what they are supposed to charge.

Besides, there are plenty of nuances to TER calculation. For instance, SEBI has mandated the maximum TER a fund can levy over an Equity and Debt fund. SEBI has also proposed a maximum TER proportionate to the fund asset under management for a given scheme. The fund should also consider the weighted average sum of your investments. So as you can imagine, there are many subtleties involved.

There are professional ‘fund accounting’ companies which incorporate the SEBI guidelines and help the AMCs do the math and ascertain the TER on a weighted average basis. As an investor, I don’t think it is necessary to dwell into these technicalities as long as you know much you are paying.

Also, when you are selecting a fund for investment, the TER is not a standalone factor to consider. TER is no doubt important, but just because a fund is charging say 2%, you should not ignore everything else about the fund and decide not to invest.

Yes, if you have to shortlist between two funds of the same type including the return profile, for example, an overnight fund, then it makes sense to look at the fund with a lower TER and invest in it.

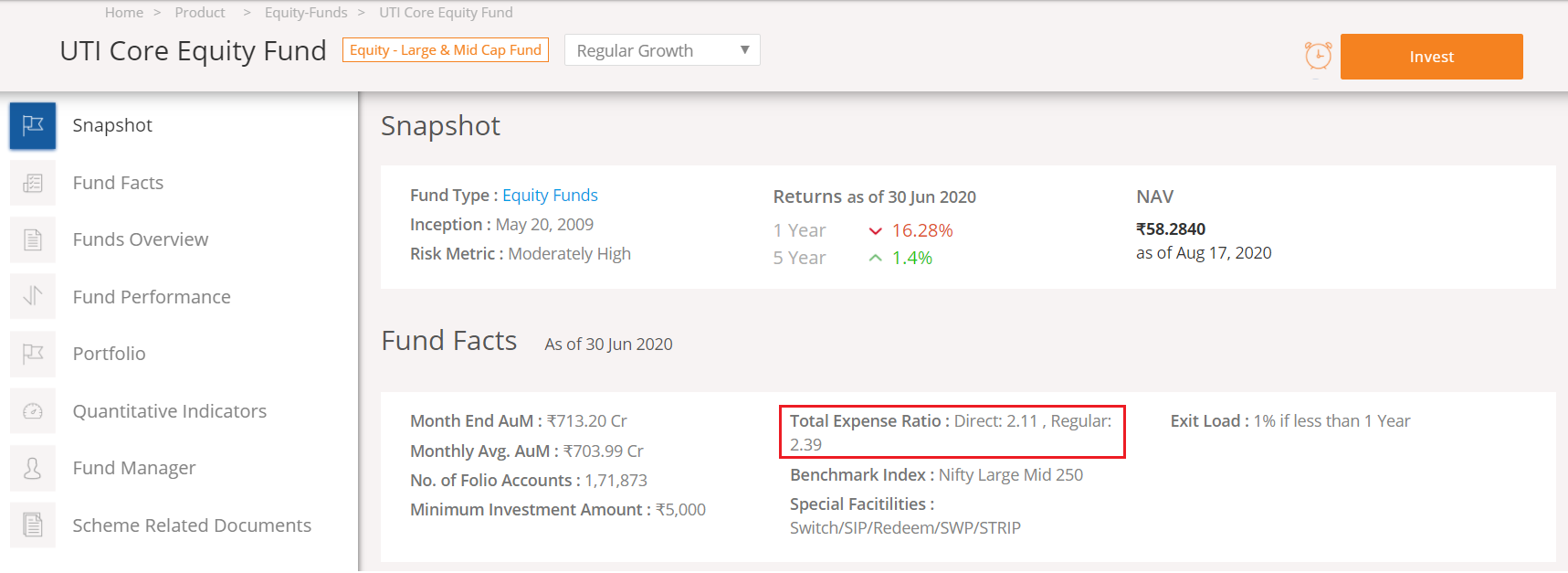

Now, here is a snapshot of the UTI Core Equity fund and the TER it charges –

As you can see, the fund charges 2.11% for Direct plan and 2.39% for the regular plan.

Now the obvious question – what is the difference between direct and regular plan and why two different TER for these funds.

20.2 – Direct and Regular plans

If you are a 90’s kid, growing up in Bangalore, then you’d probably remember few ice cream brands – Vadilal, Dollops, Kwality, and Joy. My favourite was Joy Ice cream, not because it was any different than Vadilal, but because the Joy Ice cream factory was 500 meters from my house.

It was a small factory with a little retail outlet at the factory’s entrance. At this factory-owned retail outlet, a choco bar stick was sold at Rs.14/- whereas the same was sold at Rs.18/- in a shop called ‘Anu stores’, which still is about 1km away. Whenever my parents felt generous, they would give me some money to buy ice creams; I’d run to the factory retail shop and pick up a couple of ice cream sticks for the family. While the kids were happy with the ice cream, my folks were happy with the savings.

Good old days 🙂

Now, why do you think the factory sold the ice cream at Rs.14/- while Anu stores sold the same ice cream at Rs.18?

Well, because the owner of Anu stores needed an incentive to sell Joy ice cream. Without the incentive, why would anyone sell a product, right? That’s the reason Joy Ice cream as a company would mark up the price to include the shop owners incentive and sell the choco bar at Rs.18/-.

However, at the factor’s retail outlet, there is no incentive because the Joy Ice cream as a company would make whatever it had to make by selling the ice cream directly to the customer at Rs.14/-.

I suppose this is a simple business model to understand.

Same goes with Mutual Funds.

You can choose to buy Mutual Funds in two ways –

- From the AMC directly

- Via a distributor

When you buy a mutual fund directly from the AMC, it is called a ‘Direct’ transaction. The direct transaction is comparable to me buying the ice cream from the factory owned retail outlet.

However, if you buy a mutual fund from a distributor, then it is comparable to buying the ice cream from Anu stores.

Now the seller of a regular mutual fund needs an incentive to sell the mutual fund; hence the AMC marks up the TER and passes the additional TER to the distributor and the distributor network. Hence, for any given fund, the TER or the expense ratio for a regular fund will always be higher compared to the direct fund.

Which leads us to an important point – every mutual fund scheme is available in two avatars or two plans –

- Direct Plan

- Regular Plan

While everything remains the same, only the TER changes. Have a look at the snapshot below; I’ve taken this from HDFC AMC website –

As you can see above, we are looking at the HDFC Top 100 Fund (Growth). There are two variants available to you – Direct and regular. The first in the list is the direct plan, where they have explicitly mentioned that it is a direct plan. The second in the list is the regular plan. The AMC has not explicitly mentioned that it is a regular plan, but is implied.

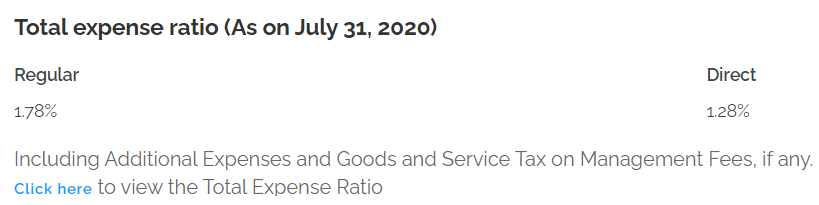

The TER for both these funds is different. Here is the snapshot –

The TER for Direct is 1.28%, and Regular is 1.78%. The additional TER of 0.5% in the regular fund is to ensure the distributor is adequately compensated for selling the Mutual Fund.

It is very important to comprehend the fact that the TER is paid by you, i.e. the investor to the AMC and therefore the distributor.

When you buy from the AMC directly, there is no distributor, hence no distributor commission, hence lesser TER. The lesser the TER, the higher the returns for you.

At this stage, you may be clear about the fact that the TER for regular funds is higher compared to its direct counterpart. You may have also understood the fact that the fund is the same – same strategy, same portfolio, same fund manager, same risk, etc., but the TER or the expense ratio is different.

The difference in TER is mainly to incentivize the Mutual fund agent or the mutual fund distributor to sell the AMCs fund. You may have a couple of questions by now –

- Who are these ‘MF agents or distributors’ trying to convince you to buy regular plans?

- Why would anyone opt for regular funds given that these have higher TER?

- If the two funds are same, then why is the NAV of direct fund higher compared to the NAV of the regular fund (refer to the snapshot above)

The MF agents could be your local bank manager or that annoying uncle who always turns up on Sunday mornings to try to sell some ‘financial scheme’. The distributor could be an online website as well, where you buy the mutual fund yourself.

Regardless of who the distributor is, you need to remember that when you buy a regular MF, you are paying a higher TER fee.

Does that mean buying a regular plan and paying a higher TER is bad?

Well, no.

If you know nothing about Mutual fund investment, and you need help with this, then you should opt for an advisor who will advise and keeps track of everything on your behalf (markets, MF performance, rebalancing etc.). Under such a circumstance, it makes sense to buy a regular MF from the agent to compensate him or her for the advisory work and the continuous handholding services.

However, if you are comfortable dealing with Mutual funds (which hopefully is the case because you are reading this module), then it does not make sense to opt for a regular fund. You are better off investing in a direct fund and save on costs.

Hopefully, this explains who these distributors are and why one should opt or not opt for regular funds.

The last question, i.e. why the NAV of direct funds is higher compared to a regular fund is perhaps the most asked question.

The confusion is this – the NAV of the regular fund is lesser. Hence the units are available for a cheaper price, why pay more for the direct fund given the fact that the NAV for direct funds is higher.

For example, look at the NAVs for HDFC Top 100 fund –

- Direct plan NAV is 460.5

- Regular plan NAV is 438.4

The difference is almost Rs.22/- per unit. It is only natural to want to buy the regular fund considering it is cheaper.

Well, the problem is in the way we perceive the NAV. If you look at NAV as a price you pay to acquire the mutual fund, then, yes, the regular fund NAV looks cheaper, and it seems like a smart decision to pay a lesser amount and buy the regular plan.

However, if you look at the NAV not as an asset price, but rather as the value of an asset, then you will soon realise that the regular plan is less valuable compared to the direct plan. After all, the NAV stands for ‘Net Asset Value’, and not ‘Net Asset price’, I hope you get the subtle difference 🙂

Think of NAV as of the latest value of the asset you’ve acquired.

In the next chapter, we will continue to discuss a few more mutual fund metrics.

Key takeaways from this chapter

- Investment in Mutual fund is not free; there is a fee applicable.

- The applicable fee is called the ‘Total Expense Ratio’ or simply the expense ratio

- The TER is expressed as an annual percentage charged

- The TER is charged daily

- The NAV that is declared is post TER deduction

- For a given fund, TER for the direct plan is lesser compared to the regular plan

- For a given fund, the NAV for the regular plan is always lesser compared to the direct plan

Heyyy Karthik

I have read all the modules till now all of em are great btw , my doubt is what exactly will i get benefited from Regular i mean will they help me cover my loss if it happens or guide me in someway ?? how exactly .

You mean to say the benefit of a direct fund? Well, since its lower expense ratio, the savings is higher and therefore your overall returns.

No, there is no advantage by buying regular. You may as well buy direct especially if you are going to a platform like COIN and placing an order yourself.

Hi,

Assuming one is taking a direct plan and another one regular plan. The lower NAV gives me more units in regular compared to direct and vice versa however at the end of the day, it is the X amount which I have invested is my investment and not how many units of NAV I have. Then how does it matter if I buy regular or direct plan? Doesn\’t the difference in NAV nullifies the impact of different TER?

Exactly, its the value of the NAV that matters. In direct, the NAV value will be higher compared to that of a regular plan.

I still didnt understand this part and it wasnt explained clearly.

Which part, Srikanth? Please do share your concern here, will be happy to help.

You’re right that both Regular and Direct plans let you invest the same amount, so the number of units isn’t the key factor. However, from what I understood, the difference in NAV between the two plans doesn’t cancel out the impact of the expense ratio.

The lower NAV of a Regular plan doesn’t mean it’s cheaper, it only reflects that higher expenses have already been deducted from its returns over time. Since Regular plans have a higher Total Expense Ratio (TER), they grow at a slightly slower rate every day compared to Direct plans. Over the long term, this small daily difference compounds, leading to noticeably lower returns in Regular plans.

So, the Direct plan gives higher returns than regular simply because it has lower ongoing costs.

That is right. The weight of extra return (by virtue of lower TER), reflects in higher NAV in a direct fund.

Hey, I have been reading this and believe me this is one of the best and most detailed and easy to grasp for a complete beginners, I really want to thank for all the hard work behind this content generation.

There\’s a minor mistake on this page in example there it says 10000/365=2.73 it\’s should be 1000/3.

Thanks 😊.

Thanks for the kind words, Dipesh, and thanks for pointing the error. Will fix it 🙂

so(The NAV that is declared is after deducting the TER)

is the sentence you typed, in this sentence, I have a query{1. I have used Coin and suppose Nippon India\’s small-cap direct growth NAV is 193/- so if I have not invested how the expense ratio is deducted, I could not understand it.}

2. if the expense ratio is 0.63% then I assume I invest 1000/monthly;1000*12=12000+16% return=13,920-0.63% TER then ₹13,832.304 is my Net gain isn\’t it os I am paying ₹87.696 as Expense ratio is it correct ??

1) The NAV you see is post expense ratio. Its deducted for the people who have invested 🙂

2) No, its not correct. Its 0.63% of the value of your assets, which is taken in small portions across the year.

let the no of units brought using same invested amount say in regular X shares and in direct Y shares. the difference is (X – Y), clearly it is positive. will this difference isn\’t enough to compensate the NAV difference between (direct – regular) nav ?

Nope, overtime the compounding effect kicks in and the weight of NAV starts to show up.

Is the XIRR displayed in Coin platform after expenses or before considering the expenses?

Its based on the NAV, which is declared after the expenses.

If we invest a certain amount on one of mutual fund on regular fund, then what are the charges on percentages are going to be deducted in future? is it only as per expense ratio that matters or some other factors on which some portion of the amount goes to agent or distributor?

It is largely the expense ratio, as indicated by the TER.

Thank You.

Happy learning, Mehul.

Sir,

I thought of starting investing in Index & Mutual fund in Large/Mid/Small cap segments. Meanwhile, I would require if you could kindly help with the below:

(i) Like the AMC has TER, does zerodha has any charges to invest in Index/Mutual fund?

(ii) I thought of investing in 6 funds (Index funds for large/mid/small & mutual funds for large/mid/small). I have plans to transact through lumpsum amount for the 6 funds multiple times in a month.

Now, we know that to get delivery of stocks, zerodha charges a certain amount each time. Now, to invest multiple times in Index/Mutual fund, does zerodha has any such charge? Or if zerodha doesn\’t have any charge, should I have to remain cautious about other costs when I transact multiple times through lumpsum amount. Please help to understand.

1) No. But there is a demat AMC changre which is the same for stocks and MFs.

2) Sure

No charges for transacting in MFs. You can also check this – https://zerodha.com/charges/#tab-equities

I have been investing in regular mutual fund for last 7-8 years through MF broker. After realizing about TER, now i am planning to move from Regular to Direct. I can start New Direct SIP, but What action should i take on the invested amount? If i redeem, it will attract good tax amount. Would that still be beneficial and compensated in next 3-4 years. Please explain.

Ah, nothing much that can be done Santosh 🙁

Do talk to your CA once on what the tax situation could be.

I have been going through these lessons, it\’s very impressive how clearly you have explained everything with the help of suitable examples which makes it further easy to understand. Thank You

Thanks, Aniket. Glad you liked the content. Happy learning.

in your last reply – what do you mean by seeing the NAV of the dividend plans

Ah sorry, ignore. You mentioned it was a income distribution plan.

As per our above conversation for the scheme (Aditya Birla Sun Life Banking & PSU Debt Fund – Interim – IDCW) the difference is because the direct plan late than regular plan. But, the plan was started in Jan 1, 2013 as when every other plan was launched and at that time this was not the case, the difference in regular and direct plan NAV\’s came somewhere in May 2018 and since it is like this

Btw, are you seeing the NAV of dividend plans? If not, the time difference is probably the reason, Shivansh.

(“Aditya Birla Sun Life Banking & PSU Debt Fund – Interim – IDCW” direct plan has lower NAV than its regular plan) if there\’s no possible reason or explanation of this, then is this some kind of a market violation or something like that ?

Not really, it is most likely because of what you found out – the massive delay in having a direct plan.

I got the reply from the AMC about why (“Aditya Birla Sun Life Banking & PSU Debt Fund – Interim – IDCW” direct plan has lower NAV than its regular plan) they are saying that it because the \”\”the direct plan was launched later than the regular plan\”\”, after these many days this is best possible reason they have come up with.

Could you please tell me a lil bit about the technical explanation someone gave you for the same

The answer you got was better than what I got as that dint make any sense 🙂

Hey Karthik, did you had any luck finding out why (\”Aditya Birla Sun Life Banking & PSU Debt Fund – Interim – IDCW” direct plan has lower NAV than its regular plan). I tried contacting the AMC again over the mail but haven\’t got any response yet

Not really, but someone told me that there is a technical explanation for this. Will try and dig that, and if its interesting, maybe will do a post as well.

Yes, definitely, I won\’t fall for them selling me a ULIP because if I am buying a ULIP, then there\’s something wrong with me that even after learning such in-depth content on personal finance from you, I am falling for this

Happy learning and investing, Shivansh 🙂

yes, I tried contacting them but they just gave me runaround every time and I am still not able to contact the right person in the AMC who can help me in the matter and I don\’t think they will be able to, cause each and every person is more interested in selling me a ULIP when I have query in mutual fund

Haha, but I do hope you wont do that 🙂

Hey Karthik,

Did you find out why (“Aditya Birla Sun Life Banking & PSU Debt Fund – Interim – IDCW” direct plan has lower NAV than the regular plan)

I\’ve asked a few people, but did you manage to speak to the AMC?

Dear Karthik,

Thanks for sharing the wealth of knowledge, Just a question: Why Zarodha sales direct plan on plaform, what do they get out fo it if it is not from TER

Thanks, Jay. There are so many theories as to why we do offer this for free, but its just that its easy and convenient to transact across all assets for our customers. Thats the only reason 🙂

sure I\’ll do check with Aditya Birla AMC but, can you please inform me on my mail if you find something cause I am sure you\’ll be able to find the reason quicker than me

Will comment here if I figure Shivansh.

Yes, I have checked the NAV on multiple websites even on the AMFI website and even in the factsheet of the plan, “Aditya Birla Sun Life Banking & PSU Debt Fund – Interim – IDCW” direct plan has lower NAV than the regular plan

I\’ll try and check internally, but meanwhile you should check with Aditya Birla AMC too. Do let us know whatever why if you happen to figure 🙂

is it because the scheme gives interim dividend?

Sorry, didn\’t quite get that. Can you please elaborate on the query?

I was analysing some mutual funds but found something strange. \”Aditya Birla Sun Life Banking & PSU Debt Fund – Interim – IDCW\” direct plan has a lower NAV than its regular plan and I also found that this first happened in May 2018 and has been continuing since then. How\’s this possible?

Not possible Shivansh, I think there must be some mix up. Can you double check again? Thanks.

Nicely explained 🙂

Glad you liked the content, Prejtha. Happy learning.

Typo alert!

SHOULD BE

1,000/365

=Rs.2.73/-

AND, NOT

1,0000/365

=Rs.2.73/-

Ah, thanks for pointing. Will fix it.

Hey, while explaining above that expense ratio is charged on a daily basis you gave an example that \”if we invest 1,00,000/- and expense ratio is 1% then 1,000/- will be charged per year\” but the expense ratio will keep on changing on a daily basis dependent on our investment value, it will not be fixed for the whole year. Right?

The % is fixed, the value will change. We have an entire series on personal finance here – https://www.youtube.com/watch?v=6sq2o1atWLY&list=PLX2SHiKfualGsjgd7fKFC-JXRF6vO73hk

Hey Karthik,

You said mutual funds deduct 2.73 rupees every day, but what happens in the case of weekend or other trading holidays?

Do they deduct them that time as well?

When there is a change in NAV, they do.

In case someone still wondering how to switch existing regular mutual fund to direct, it seems mfcentral app/website allows this.

Ah ok, need to double check this.

Thank you Karthik Sir for all of this valuable information. You explain these concepts very well. I will try to use all the information as I start my Personal Finance Journey. Really grateful for you and Zerodha for educating us.

Happy learning, Rohan. Glad you found the content useful!

Why AMC\’s launch zero expense ratio schemes?

There are no zero-expense ratio schemes, right?

sir

any MF past NAV kha milegi ?

Check the AMFI website.

sir one more doubt

invest in mf lets assume 5000rs per month ….for simple ..forget up/downs in investment

so sir expesnse charged on 3rd month 15000rs per hoga kya ?

Expense ratio will be charged on a daily basis 🙂

HELO

NAV of regular plan why cheap …muje smje nhi aaya …plz expln sir …..

Think of NAV as the value of the asset, not as the value of the price you pay. When you look at it, the NAV of regular fund looks less valuable.

Dear Karthik,

There is a typo in the sentence

\”As an investor, I don’t think it is necessary to dwell into these technicalities as long as you know much you are paying.\”.

\’how\’ is missing. It should be \”you know how much you are paying\”.

Its funny, when I read that line, I read \’how,\’ although it was missing. I will add, thanks for pointing.

Tell me whether I should buy Direct or regular plan in MF

From where to buy Direct as in my account it is not mentioned

I\’d suggest you buy Direct funds for obvious reasons. You can buy via Coin – https://coin.zerodha.com/

Can Zerodha charge, after some time, that TER will be charged holdings?

There is no holiday for TERs 🙂

Who will be custodian if my mf holding? How can i track this on daily basis

Your units will be in your demat account, from where you can track this.

Typo error: Ch 20.1 refers to Rs 1000 per Yr, and 10000/365=2.73 as per day charge. It should be 1000/365=2.73

—

Rs.1,000/- is the charge on an annual basis. If you do the math, this works out to –

1,0000/365

=Rs.2.73/-

—

Ah, sorry about that and thanks for pointing it out. I will try and fix it.

what can be the reasons when expense ratio is increased in a mutual fund other than the change in AUM of the fund

These AMCs change based on their own logic, very hard to keep track 🙂

Thanks karthik for explaining so nicely.

But I am not able to understand the last point, if Regular plan NAV price is less compare to direct plan ( in our example it is 22 which is quite a considerable amount) how we are saying regular plan is less valuable.

Think about it from the perspective of post-invest. For your investment to be valuable, you want a higher NAV, right?

1,0000/365 is incorrect. it should be 1000/365

Yes, thats a typo 🙂

Hi Kartik ,

U said AMC charges Expenses daily, but if we redeem our mutual fund before 1 year, will that fees be charged only for the number of days while we were invested in that fund, or 365 days charges will be applied

Yes, it will be.

Expense ratio is calculated as a Percentage of what ? Like for eg . expense ratio of a fund is 1% , then 1% of what value ?

It is the percentage of your net asset invested in the fund. Basically the value of your investment.

I see that you\’ve answered the first question in the next module itself. So you may please skip that!

Hi Karthik,

Thank you for your efforts in creating this wonderful resource!. I have a couple of questions :

1. If the TER is charged as a %age on value of assets, then suppose :

In Year 1, I invest 100000 which grows (say 10%) to 110000 at start of the next year. Then for the first year the TER will be charged for 100000 and for the next year, TER will apply to 110000. This means as the value increases, the cost eaten up by the TER will also grow. Is this right? Probably this is the argument for Index Funds.

2. Let\’s say I am looking to invest in a MF, with the regular NAV being 12 and direct NAV being 13.5. From the point of view of the number of units I would hold, I would have a lesser number of units in the direct plan as compared to the regular plan to begin with. However, as the value of the MF grows, is it the case that the cost to the higher TER of the regular plan would result in the net value of the direct plan being higher?

Thanks again for your efforts.

1) Yes, but it is not year-wise. AMCs have a technique to deduct this fee, as a weighted average cost of assets.

2) Thats right. Direct plan you hold lesser units, but they are more valuable compared to the regular plan.

If I have invested 10,000 and say after 15 years my fund value is 1,00,000.

At the 15th year TER is charged for 1,00,000 or the initial investment done i.e. 10,000.

Regards,

Ashwath

It\’s always on the average assets held for the last x number of months. So TER is on 1L.

I have been enjoying reading your content Karthik. Great job!

We as buyers of a mutual fund pay for the additional TER for the lifecycle of our investment if we go with the regular plan. But the distributor has to sell the fund to me only once. So for the rest of the time, I remain invested, I am paying for the distributor\’s incentive to sell to others. Is that understanding correct? From what I have seen, most distributors don\’t really advise on managing the investment once they have sold the mutual fund to a client.

Thats absolutely correct, Devang. It is a simple logic that most people fail to understand 🙂

Hi,

If i switch my MF from regular plans to direct plans then do I have to pay for MF distributer? I was investing through agent but now recently I had converted funds to direct plans.

Not really, no payments to the agent here.

Hi

Will the expense ratio for the same mutual fund differ between applications? For example can zerodha claim 0.46% and can another app claim 1.23%?

Is that even possible?

Nope, the expense ratio is set by the AMC, has to be the same across platforms.

Regarding the NAV of direct and regular plan, as the mutual fund grows wont the both NAV grow at the same rate? So does that mean the growth of my return be same had i opt for any of the plans?

The growth rate will remain the same. The percentage return itself varies. For example, you buy a direct MF at 12 and I buy a regular MF at 10. Both grow at 5%, which means NAV is now 12.6 and 10.5, but after deducting for expense ratio, direct\’s NAV could be 10.3 and regular\’s NAV maybe at 12.5, making the direct fund more valuable.

This is brilliant, Karthik. I wish this were there when I was in school. Such modules should be made a part of school curriculum. So many people would be able to retire comfortably :). I think investing an hour a day in each module and reading the comments that follow can be the best knowledge investment one can make. Keep it going!

I had a small query – Can I invest in direct plans in a minor\’s name? My twin kids are about a year old and I have invested lumpsum amounts in regular plans in their name – mainly from the documentation support that I can get through an advisor. However, after reading this module, I am tempted to invest future amounts in direct plans. How easy is the process?

Thanks for the kind words, Abhishek.

Yes, you can invest in direct MF in a minor\’s name. Check this – https://support.zerodha.com/category/account-opening/offline-account-opening/articles/can-i-open-an-account-in-my-child-s-name

But the process of lump sump to direct conversion is a pain. You will have to sell all the lumpsum units and then reinvest the same in direct funds.

When I started investing in MF, I chose a regular fund. Should I convert it to a direct fund now? It\’s been 2 years since then.

Better late than never 🙂

I read from the pdf and come here for the blurred images in the pdf 😀

Sorry about that, Manish. I\’ll see what can be done about this.

Hi Karthik,

Thanks for these excellent modules. The examples that you give to explain complicated financial terms is amazing and easy to understand. For a layman like me with Engineering background who knows how to make money by building complicated structures but dont know how to invest money for good returns, your modules provide excellent foundation to understand things.

I would really appreciate if you provide similar type of information on crypto currencies. That would be very helpful

Thank you

Sunil

Thanks for the kind words, Sunil! Unfortunately I don\’t know anything about Crypto, cant really comment or write about it 🙂

Hey Karthik, thanks for this module!

A small typo – 1,0000/365 should be 1,000/365

Thanks, will take a look 🙂

Regarding Open ETF, How would the price get Set (I’m looking for NAV Value). I’m thinking to apply for Open ETF but unable to get like bid values.( I’m assuming Same as IPO )

I’m looking for Open ETF Nippon India NIFTY Pharma ETF – Growth Plan So I’m unable to get Bid Price

Could you please help me on this.

If there is any Chapter, Please let me know, Seems I missed.

P.S: Due to incomplete question, I\’m posting Again with Complete Information.

Saurabh, its market-driven, please place a limit order and wait for a fill.

I’m looking for Open ET Nippon India NIFTY Pharma ETF – Growth Plan So I’m unable to get Bid Price

Its market-driven, please place a limit order and wait for a fill.

Thanks Karthik for taking us through this wonderful knowledge series on Mutual Funds. It definately upgrades an individual from thinking \’Regular\’ to thinking \’Direct\’. Thats the kind of transformation it brings about. Hats off to your efforts.

I had a query. Is there any difference between Expense Ratio and Total Expense Ratio ? Almost, all MF products specify as Expense Ratio and in a few cases we see Total Expense Ratio. Do we need to dig in further if TER is not specified ?

Thanks for the kind words, Vinod.

No, both expense ratio and total expense ratio refers to the same. TER is just called an expense ratio.

I’m looking for Open ET Nippon India NIFTY Pharma ETF – Growth Plan So I’m unable to get Bid Price

I\’m looking for Open ETF <>, So I\’m unable to get Bid Price

Sorry, dint get that.

Regarding Open ETF, How would the price get Set (I\’m looking for NAV Value). I\’m thinking to apply for Open ETF but unable to get like bid values.( I\’m assuming Same as IPO )

Could you please help me on this.

If there is any Chapter, Please let me know, Seems I missed.

Sorry, which ETF are you referring to here?

Expense Ratio Deduction Can we find in any Transaction Report ?

I don\’t think so, Saurabh.

Sr ,can fund houses change the expense ratio of a fund like after 5-6 years, if fund is giving good returns

Yes, they can.

I was interested in Mirae tax saving fund, I checked different apps like zerodha, groww, it shows more expense ratio than on their fund page. For E.g: 0.79 in zerodha, groww and 0.29 on Mirae fund page. Why is that?

Are you sure you are checking the right funds? Let me check anyway. But the rate you see on the fund\’s factsheet is the latest and most accurate one. Sometimes they may change the TER and it will be delayed on our site with a slight delay.

As a person looking to invest directly, could you brief me on the numbers I need to monitor continuously and the frequency of monitoring? (SIP Plan).

I believe, as you say, the key is to stay long but what should trigger one to reconsider the investment choice?

Review your portfolio once a year. Look for the overall market performance and your fund\’s performance. If you have multiple funds in a portfolio, then look at it from a portfolio perspective. If there are laggards in the portfolio, inspect why. Also, do look at the risk, see if the fund is taking an excess risk in order to chase down returns.

Dear Karthik,

Hi,

Can you again brief the difference between Direct NAV and Regular NAV with some examples.

Because when I get the same part of asset in regular plan then why should I pay more in Direct plan for the same part of asset.

Please revert

Think about an investment in a real estate plot. After you invest, you want the price to go higher and higher right, so that what you hold is more valuable. So now think about the NAV of direct and regular form, which one do you think is more valuable? Direct right? Because its NAV is higher.

But, while investing / buying \’Regular\’ you get more units for the same amount invested as the NAV is lesser as compared to Direct.

Hmm, what about that John? What you need to look at is the growth rate.

Hey, Karthik

First of all, thanks for the beautiful module. I have a doubt in specific to expense ratio.

Say, today I bought 10 units of Small cap equity fund from fund house A. The expense ratio stated was 1%. After one year, the found house has increased the TER to 1.5%. Now(after 1 year) the units that I\’m holding will be charged with the new TER or older one?

The new TER, Mahesh. However, I\’ll also need to double-check this.

Best explanation. I was browsing on How TER is deducted.. this article explains it clearly.. with examples..

Happy reading!

Hi Karthik,

I kind off getting the below point you trying to make and also confused at same time, but is there anyway you can explain this with one small example please ? Thanks

“However, if you look at the NAV not as an asset price, but rather as the value of an asset, then you will soon realise that the regular plan is less valuable compared to the direct plan. After all, the NAV stands for ‘Net Asset Value’, and not ‘Net Asset price’, I hope you get the subtle difference “

Ok, assume the NAV for a direct plan MF is 13 and the regular plan is 12.25. In fact, at any given point the NAV of regular will always be lesser than its direct plan equivalent. When people look at evaluating this to invest, they usually think that the NAV of a regular plan is less and invest in it.

But think about it – after you buy, you want a higher price for the asset you own right? By virtue of its design, the direct plan will always be more valuable compared to the regular plan (hence the higher NAV for direct).

I have invested in a direct flexi cap fund for over a year and now since the fund doesn\’t perform well I have stopped the SIP. Should I redeem the units and pay LTCG or hold it?

Depends on why you decided to invest in the flexi cap in the first place. What sort of return expectation did you have from the flexi cap?

Sure sir just reposting it. Hi Karthik,

Must say your articles are simply superb to consume. I have one question, I have my sip going on in couple of funds(HDFC mid cap and icici large cap) through fundsupermart India since 2015. I realized my expense ratio is higher only after reading your article but I want to know if there is any option to shift my mutual funds units to direct plan through zerodha ? I am NRI , just mentioning this in case if it will cause any issues to move to direct plan.

Sorry, I guess I missed your query earlier. The easiest way would be to sell and buy again in direct form, but since you are an NRI, this can be an issue. I\’d suggest you create a ticket, someone from MF team will get in touch to help you with this.

Just in case , did you missed my query ?

Have I? Can you please repost in case I have?

Hi Karthik, Thanks for this series. I am enjoying it. I have one question though, what could be the incentives for apps/sites selling Direct Mutual funds without charging any Annual Maintenance charge?

I don\’t know about others, but for us, we make revenues from the broking business and hence can afford to give MFs for free.

Hi Karthik,

Must say your articles are simply superb to consume. I have one question, I have my sip going on in couple of funds(HDFC mid cap and icici large cap) through fundsupermart India since 2015. I realized my expense ratio is higher only after reading your article but I want to know if there is any option to shift my mutual funds units to direct plan? I am NRI , just mentioning this in case if it will cause any issues to move to direct plan.

Thank you Karthik for these wonderful notes!

Have a Q:

You have mentioned that NAV is calculated after deducting the TER.

If I want to simplify: New NAV(Day 1) = [Old NAV(Day 0) * No of units – TER Expense per day]/No. of units

The first term on Right hand side is dependent only on Old NAV as No. of units cancel in numerator and denominator.

However, the second term has expense per day/no of units and hence, is dependent on the no. of units you buy.

So, to summarize, the NAV will be different for different investment amounts.

Am I understanding it right?

Prajwaj, the calculation is more complex than what you\’ve indicated here. The NAV will be the same for all investors.

Can you please tell me procedure of it? Or point to such resource?

Redeem all your regular funds, invest the proceeds into the direct funds. That\’s about it 🙂

Hi Karthik,

I have been doing MF investments for last 2 years in the form of SIP with regular plan through distributor. Now that I\’ve my zerodha coin account. I was wondering if it\’s possible to move those regular plans to direct? And How?

If it\’s not possible to change regular to direct plan. Does it make sense to stop/break those SIP and start through coin in the same funds? Stopping SIP and moving them in such way would affect my returns and compounding done so far. What do you suggest?

Thanks for the help! All these varsity article are very helpful

I understand I\’ve been through the same situation long back. The only real way is to do a hard stop and move without spending too much time in the transition. Compounding wont break as it is just a transition.

Hi Sir,

Thank you so much for this module, it is highly explanatory.

I have two doubts

1) While explaining the TER you took example (of course for simplicity) for Lumpsum amount invested (Rs 1,00,000) if we invest through SIP TER calculation would be same?

2) In the example, you have assumed that TER is 1% annually of the investment made. But when I checked TER for Kotak Equity Opportunities Fund (or for all equity funds managed by Kotak) the TER is changing almost weekly whether for the direct plan or regular plan. So how an investor should calculate the annual TER?

Thank you

1) Yes, TER is the same for both lumpsum and SIPs

2) That\’s right, AMCs change the TER, but I think the change is not on weekly basis but rather on a quarterly basis.

Few Data like Expense Ratio of MFs is not matching between Coin and RupeeVest. Which one is considered more updated/authentic?

I\’d say Coin 🙂

How much brokerage taken by you in coin.

None.

Hi,

I have been investing through MF for last 3 years on monthly SIP basis. All the schemes are \’regular\’ schemes. There is 1 year period for exit load in all schemes. If I want to withdraw from these schemes then can I withdraw the entire amounts because the schemes have completed 1 year period or can I withdraw only the monthly SIPs for which 1 year period is over? eg can I withdraw the amount invested until August 2020 or amount until August 2019 for which SIP have completed 1 year?

Please help clarify the procedure on exit from MFs?

Thanks, Chander

SIPs have a lock-in of 3 years, each SIP has to complete 3 years. The other scheme can be pulled of if they have completed a year without any exit load constraint.

great explanation sir!, are you also thinking to launch something related to financial modelling?, please let me know. Thank you

Yes, next module 🙂

Hi

I was wondering for investing in index fund which is better in terms of return generated nifty50 index fund or the sensex index fund. What would you suggest.

Nifty 50. The next chapter is about this itself.

Pls provide the PDF version of this module..Thankyou in advance..

Module has to be complete sir. I\’ve mentioned this so many times already 🙂

Thanks Karthik, I put my first salary in all PPF, so that I could buy time for waiting for your concluding article 🙂

Wow! Thats a lot of pressure on me now, will try my best to hurry up 🙂

Hey Karthik! Have been following varsity MF series for a long time and am waiting for the article on designing a MF portfolio. When is that article coming?

I\’ll try and gather pace on this, the next chapter is on bench marking and few other things. Maybe after that.

Dear Sir,

You are doing Wonder full Job, Please keep it up.

Happy reading, Vivek!

Hi Karthik,

Could you please make PDF copy available for this module?

Yes, but I need to finish this module first. This is still work in progress.

Hi sir, very nicely written. When can we accept the next chapter?

Sometime next early next week.

Sir I know I am getting ahead of time here but I am just very excited so I am asking this. If you can reveal this, please tell me how many more chapters are more in this module and what the next module is going to be. I am asking this as a long term reader of Varsity and I just feel personal finance module does not hold the candle to some of the other modules you\’ve authored. I hope you do not take this the wrong way. I am eagerly waiting for the next module.

Thank you.

Few more chapters in this module, Sundeep. Btw, if you cant tell me why its not holding the candle, it will help me improve and focus better. Thanks for the feedback 🙂

why don\’t this module have download option ?

Will be available after the module is complete.

Good read, but pls clarify me something. Even if we go directly to the AMC website I could see Regular plans as well, if they (AMC) are selling MF directly then why the regular plans are seen and who is the broker/advisor here ?

Vijay, which AMC is this? Can you please share the link? Ideally, it does not makes sense. If it is a regular plan, then there would be a ARN number to it, which will tell you who the distributor is.

Great Module Karthik. Really Looking forward to next chapter.

One more thing – Sector wise and company wise fund allocation Information of a mutual fund is not available on the desktop version of Coin. Please show that information so that a Zerodha customer like me can make more informed investment decisions.

Regards

Will put up the next chapter soon, Sharan. Coin will be updated soon 🙂

Canara robeco regular growth plan ab isse band karke ya pause krke equity me invest karna thik rahega …. Through zerodha please relay

Why do you want to stop your investment?

dear karthik sir ,

thanks for such amazing explanation . eagerly waiting for next chapter .

Happy reading, Venkatesh!

Thank you so much Sir.

You have literally told the basic truth , which these mutual funds company doesn\’t explain easily.

I\’m looking forward to see various other hidden topics.

Keep going.

All the best.

Happy reading and I\’ll try and update the next chapter soon.

Thanks for the post! All the while I was thinking that we have to subtract the ER from the fund returns(shown on money control etc) to arrive at the final return

Ah no, its deducted by the fund itself.

Thanks Karthik for the article.

I didn\’t know that TER is taken away on daily basis before reading this article. Thanks for the information.

And also, how the NAV calculation you shared in this article.

Please also tell us about how to choose good Mutual Fund , I mean what should we look for when choosing a mutual fund other than TER & NAV.

Please reply

Vicky, that is the direction we are heading in. Before going into fund selection, we need to ensure we are comfortable with few basic MF technicalities.

Hello Karthik,

The work you do is amazing.

I am looking forward to invest in Index funds. Apart from expense ratio, are there any hidden costs that I should look for?

Thank you!

Not really, TER includes all the expense.

Ap amc ki mf website pe chek kar sakti hai aur kis fund nav check karna chahati hai

Dear Sir,

Are Mutual Fund bought from Zerodha are Direct or regular Funds, as you previously said they are direct funds but there will be some extra TER charges if bought from Zerodha instead of Direct AMC, Please clarify.

Vivek, Zerodha Coin platform offers only direct mutual funds.

Hi,

Thank you for explaining concepts in simple way. I am waiting for the chapter on ETFs. It was supposed to be 17th chapter after index funds.

I know, its taking a bit longer than expected. Will try and finish that soon 🙂

Well explained… Thanks…

However, i wonder would the NAV of the direct MFs offered directly from the corporate website of the MF differ from the NAV of the same fund taken through online free fund management Apps like zerodha kuvera etc..? Considering the example of of factory Gate outlet and the Anu store for the ice-cream…

As a distributor of funds, we can choose which one to distribute, either regular or Direct. Zerodha Coin distributes direct funds, so its as good as buying the ice cream at the factory\’s retail outlet 🙂

Well explained… However, i wonder would NAV of a fund differ from direct plans by onl

Hope that is clear now 🙂

Very well explained. Thanks to zerodha coin.

Happy reading and investing 🙂

All my investments are in Regular plan. Can I now convert it to Direct plan?

To convert, you will have to sell the units and then buy back the same funds in direct plan.

Great work Sir….just out of curiosity…when has direct mutual funds started implementing in India.

I think Direct started mid to late 2000\’s if I\’m not wrong.

Hi Karthik, I\’m zerodha account holder and started investing via coin, this is direct or regular plan?

Zerodha Coin offers only Direct funds.

Hi Karthik,

Quick question – lets suppose I invested in one Equity scheme having TER of 1.5% and after 15 years of investments I redeem all my units then that time do I need to give this TER of 1.5% upront or Nothing as this will have been accomodated in NAV on daily basis as explained above?

Regards,

Nischal Kumar

Like I mentioned, there are no explicit payments you make to the AMC. The TER will be deducted everyday, for however long you have been invested in.

Hi Karthik,

Please look into this. By mistake you have mentioned 10,000 instead of 1,000. 😀

\”\”Rs.1,000/- is the charge on an annual basis. If you do the math, this works out to –

1,0000/365

=Rs.2.73/-\”\”

Ah, ok. Will do, thanks for pointing 🙂

Hi Karthik

Are listed mutual funds direct or regular? How can I identify?

Also if you could explain open vs closed end mutual funds that would be really helpful.

Thank you.

A direct MF will have to explicitly state that the fund is direct, else its regular. All MF on Zerodha Coin are direct. I think U have discussed the difference between open and close ended funds in one of the earlier chapters. Request you to please look at it. Thanks.

ETF & Smart beta you promised, are they yet to come or did I miss them?

Yet to come Sir. Hopefully soon.

Hi sir , I wanted to know which brokers accepting mutual fund as collateral for options writing..

Not sure, Arun.

Explained the sdetails in a a very simple and understandable way.

Happy reading, Deepak 🙂

Sir I have searched a lot about \’Clean Data\’. I know one needs clean data for backtesting, but I do not understand what it really means. Can you briefly explain what it means? It would help me a lot.

Thank you.

Please do approach an exchange approved data vendor for this, they will provide you clean data.

Hi Karthik,

If we can do all things with ourself in direct plan thats okay. But if I’m giving an amount for managing my MFs in regular plan then what are the besides benefits of the same? Is they only keeping view on my Mfs or something other benefits too. Its little bit confusing.

They keep track and are supposed to advice you on managing your portfolio.

Karthik, when would you put this Personal finance module on the Varsity app?

Thanks for this brilliant module, looking ahead for new topics.

Rohan, the module will be available on the app later this year.