18.1 – Striking it right

The last couple of chapters have given a basic understanding on volatility, standard deviation, normal distribution etc. We will now use this information for few practical trading applications. At this stage I would like to discuss two such applications –

- Selecting the right strike to short/write

- Calculating the stoploss for a trade

However at a much later stage (in a different module altogether) we will explore the applications under a different topic – ‘Relative value Arbitrage (Pair Trading) and Volatility Arbitrage’. For now we will stick to trading options and futures.

So let’s get started.

One of the key challenges an option writer always faces is to select the right strike so that he can write that option, collect the premium, and not really be worried about the possibility of the spot moving against him. Of course, the worry of spot moving against the option writer will always exist, however a diligent trader can minimize this.

Normal Distribution helps the trader minimize this worry and increase his confidence while writing options.

Let’s have a quick recap –

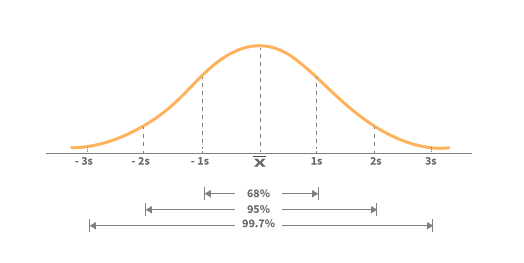

The bell curve above suggests that with reference to the mean (average) value –

- 68% of the data is clustered around mean within the 1st SD, in other words there is a 68% chance that the data lies within the 1st SD

- 95% of the data is clustered around mean within the 2nd SD, in other words there is a 95% chance that the data lies within the 2nd SD

- 99.7% of the data is clustered around mean within the 3rd SD, in other words there is a 99.7% chance that the data lies within the 3rd SD

Since we know that Nifty’s daily returns are normally distributed, the above set of properties is applicable to Nifty. So what does it mean?

This means, if we know Nifty’s mean and SD then we can pretty much make an ‘educated guess’ about the range within which Nifty is likely to trade over the selected time frame. Take this for example –

- Date = 11th August 2015

- Number of days for expiry = 16

- Nifty current market price = 8462

- Daily Average Return = 0.04%

- Annualized Return = 14.8%

- Daily SD = 0.89%

- Annualized SD = 17.04%

Given this I would now like to identify the range within which Nifty will trade until expiry i.e 16 days from now –

16 day SD = Daily SD *SQRT (16)

= 0.89% * SQRT (16)

= 3.567%

16 day average = Daily Avg * 16

= 0.04% * 16 = 0.65%

These numbers will help us calculate the upper and lower range within which Nifty is likely to trade over the next 16 days –

Upper Range = 16 day Average + 16 day SD

= 0.65% + 3.567%

= 4.215%, to get the upper range number –

= 8462 * (1+4.215%)

= 8818

Lower Range = 16 day Average – 16 day SD

= 0.65% – 3.567%

= 2.920% to get the lower range number –

= 8462 * (1 – 2.920%)

= 8214

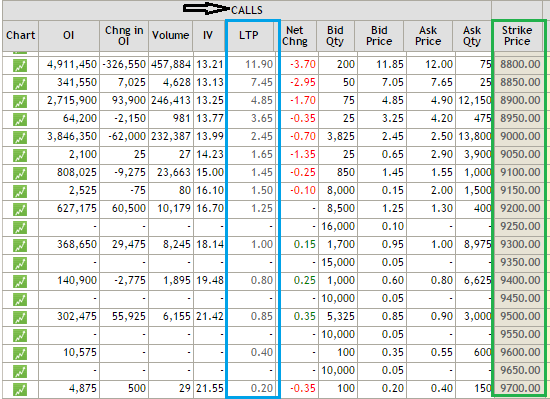

The calculation suggests that Nifty is likely to trade anywhere in the region of 8214 to 8818. How sure are we about this, well we know that there is a 68% probability for this calculation to work in our favor. In other words there is 32% chance for Nifty to trade outside 8214 and 8818 range. This also means all strikes outside the calculated range ‘may’ go worthless.

Hence –

- You can sell all call options above 8818 and collect the premiums because they are likely to expire worthless

- You can sell all put options below 8214 and collect the premiums because they are likely to expire worthless

Alternatively if you were thinking of buying Call options above 8818 or Put options below 8214 you may want to think twice, as you now know that there is a very little chance for these options to expire in the money, hence it makes sense to avoid buying these strikes.

Here is the snapshot of all Nifty Call option strikes above 8818 that you can choose to write (short) and collect premiums –

If I were to personally select a strike today it would be either 8850 or 8900 or probably both and collect Rs.7.45 and Rs.4.85 in premium respectively. The reason to select these strikes is simple – I see an acceptable balance between risk (1 SD away) and reward (7.45 or 4.85 per lot).

I’m certain many of you may have this thought – if I were to write the 8850 Call option and collect Rs.7.45 as premium, it does not really translate to any meaningful amount. After all, at Rs.7.45 per lot it translates to –

= 7.45 * 25 (lot size)

= Rs.186.25

Well, this is exactly where many traders miss the plot. I know many who think about the gains or loss in terms of absolute value and not really in terms of return on investment.

Think about it, margin amount required to take this trade is roughly Rs.12,000/-. If you are not sure about the margin requirement then I would suggest you use Zerodha’s margin calculator.

The premium amount of Rs.186.25/- on a margin deposit of Rs.12,000/- works out to a return of 1.55%, which by any stretch on imagination is not a bad return, especially for a 16 day holding period! If you can consistently achieve this every month, then we are talking about a return of over 18% annualized just by means of option writing.

I personally use this strategy to write options and I’d like to share some of my thoughts regarding this –

Put Options – I don’t like to short PUT options for the simple reason that panic spreads faster than greed. If there is panic in the market, the fall in market can be much quicker than you can imagine. Hence even before you can realize the OTM option that you have written can soon become ATM or ITM. Therefore it is better to avoid than regret.

Call Options – You inverse the above point and you will understand why writing call options are better than writing put options. For example in the Nifty example above, for the 8900 CE to become ATM or ITM Nifty has to move 438 points over 16 days. For this to happen, there has to be excess greed in the market…and like I said earlier a 438 up move takes a bit longer than 438 down move. Therefore my preference to short only call options.

Strike identification – I do the whole exercise of identifying the strike (SD, mean calculation, converting the same w.r.t to number days to expiry, selecting appropriate strike only the week before expiry and not before that. The timing here is deliberate

Timing – I prefer to short options only on the last Friday before the expiry week. For example given the August 2015 series expiry is on 27th, I’d short the call option only on 21st August around the closing. Why do I do this? This is to mainly ensure that theta works in my favor. Remember the ‘time decay’ graph we discussed in the theta chapter? The graph makes it amply evident that theta kicks in full force as we approach expiry.

Premium Collected – Because I write call options very close to expiry, the premiums are invariably low. The premium that I collect is around Rs.5 or 6 on Nifty Index, translating to about 1.0% return. But then I find the trade quite comforting for two reasons – (1) For the trade to work against me Nifty has to move 1 SD over 4 days, something that does not happen frequently (2) Theta works in my favor, the premiums erode much faster during the last week of expiry favoring the option seller

Why bother ? – Most of you may have this thought that the premiums are so low, why should I even bother? Honestly I too had this thought initially; however over time I have realized that trades with the following characteristics makes sense to me –

- Visibility on risk and reward – both should be quantifiable

- If a trade is profitable today then I should be able to replicate the same again tomorrow

- Consistency in finding the opportunities

- Assessment of worst case scenarios

This strategy ticks well on all counts above, hence my preference.

SD consideration – When I’m writing options 3-4 days before expiry I prefer to write 1 SD away, however for whatever reason when I’m writing the option much earlier then I prefer to go 2 SD away. Remember higher the SD consideration, higher is the confidence level but lower is the premium that you can collect. Also, as a thumb rule I never write options when there is more than 15 days for expiry.

Events – I avoid writing options whenever there are important market events such as monetary policy, policy decision, corporate announcement etc. This is because the markets tend to react sharply to events and therefore a good chance of getting caught on the wrong side. Hence it is better safe than sorry.

Black Swan – I’m completely aware that despite all the precaution, markets can move against me and I could get caught on the wrong side. The price you pay for getting caught on the wrong side, especially for this trade is huge. Imagine you collect 5 or 6 points as premium but if you are caught on the wrong side you end up paying 15 or 20 points or more. So all the small profits you made over 9 to 10 months is given away in 1 month. In fact the legendary Satyajit Das in his highly insightful book “Traders, Guns, and Money” talks about option writing as “eating like a hen but shitting like an elephant’.

The only way to make sure you minimize the impact of a black swan event is to be completely aware that it can occur anytime after you write the option. So here is my advice to you in case you decide to adopt this strategy – track the markets and gauge the market sentiment all along. The moment you sense things are going wrong be quick to exit the trade.

Success Ratio – Option writing keeps you on the edge of the seat. There are times when you feel that markets are going against you (fear of black swan creeps in) but only to cool off eventually. When you write options such roller coaster feelings are bound to emerge. The worst part is that during this roller coaster ride you may be forced to believe that the market is going against you (false signal) and hence you get out of a potentially profitable trade.

In fact there is a very thin line between a false signal and an actual black swan event. The way to overcome this is by developing conviction in your trades. Unfortunately I cannot teach you conviction; you will have to develop that on your own J. However your conviction improves as and when you do more of these trades (and all trades should be backed by sound reasoning and not blind guesses).

Also, I personally get out of the trade when the option transitions from OTM to ATM.

Expenses – The key to these trades is to keep your expense to bare minimum so that you can retain maximum profits for yourself. The expenses include brokerage and applicable charges. If you short 1 lot of Nifty options and collect Rs.7 as premium then you will have to let go few points as expense. If you are trading with Zerodha, your expense will be around 1.95 for 1 lot. The higher the number of lots the lesser is your expense. So if I were trading 10 lots (with Zerodha) instead of 1, my expense drastically comes down to 0.3 points. You can use Zerodha’s brokerage calculator to get the details.

The cost varies broker to broker so please do make sure your broker is not greedy by charging you ridiculous brokerage fees. Even better, if you are not with Zerodha, it is about time you join us and become a part of our beautiful family ☺

Capital Allocation – An obvious question you might have at this stage – how much money do I deploy to this trade? Do I risk all my capital or only a certain %? If it’s a %, then how much would it be? There is no straight forward answer to this; hence I’ll take this opportunity to share my asset allocation technique.

I’m a complete believer in equities as an asset class, so this rules out investment in Gold, Fixed Deposit, and Real Estate for me. 100% of my capital (savings) is invested in equity and equity based products. However it is advisable for any individual to diversify capital across multiple asset classes.

So within Equity, here is how I split my money –

- 35% of my money is invested in equity based mutual funds via SIP (systematic investment plan) route. I have further divided this across 4 funds.

- 40% of my capital in an equity portfolio of about 12 stocks. I consider both mutual funds and equity portfolio as long term investments (5 years and beyond).

- 25% is earmarked for short term strategies.

The short term strategies include a bunch of trading strategies such as –

- Momentum based swing trades (futures)

- Overnight futures/options/stock trades

- Intraday trades

- Option writing

I make sure that I do not expose more than 35% of the 25% capital for any particular strategy. Just to make it more clear, assume I have Rs.500,000/- as my capital, here is how I would split my money –

- 35% of Rs.500,000/- i.e Rs.175,000/- goes to Mutual Funds

- 40% of Rs.500,000/- i.e Rs.200,000/- goes to equity portfolio

- 25% of Rs.500,000/- i.e Rs.125,000/- goes to short term trading

- 35% of Rs.125,000/- i.e Rs.43,750/- is the maximum I would allocate per trade

- Hence I will not short more than 4 lots of options

- 43,750/- is about 8.75% of the overall capital of Rs.500,000/-

So this self mandated rule ensures that I do not expose more than 9% of my over all capital to any particular short term strategies including option writing.

Instruments – I prefer running this strategy on liquid stocks and indices. Besides Nifty and Bank Nifty I run this strategy on SBI, Infosys, Reliance, Tata Steel, Tata Motors, and TCS. I rarely venture outside this list.

So here is what I would suggest you do. Run the exercise of calculating the SD and mean for Nifty, Bank Nifty on the morning of August 21st (5 to 7 days before expiry). Identify strikes that are 1 SD away from the market price and write them virtually. Wait till the expiry and experience how this trade goes. If you have the bandwidth you can run this across all the stocks that I’ve mentioned. Do this diligently for few expiries before you can deploy capital.

Lastly, as a standard disclaimer I have to mention this – the thoughts expressed above suits my risk reward temperament, which could be very different from yours. Everything that I mentioned here comes from my own personal trading experience, these are not standard practices.

I would suggest you note these points, understand your own risk-reward temperament, and calibrate your strategy. Hopefully the pointers here should help you develop that orientation.

This is quite contradicting to this chapter but I have to recommend you to read Nassim Nicholas Taleb’s “Fooled by Randomness” at this point. The book makes you question and rethink everything that you do in markets (and life in general). I think just being completely aware of what Taleb writes in his book along with the actions you take in markets puts you in a completely different orbit.

18.2 – Volatility based stoploss

The discussion here is a digression from Options, in fact this would have been more apt in the futures trading module, but I think we are at the right stage to discuss this topic.

The first thing you need to identify before you initiate any trade is to identify the stop-loss (SL) price for the trade. As you know, the SL is a price point beyond which you will not take any further losses. For example, if you buy Nifty futures at 8300, you may identify 8200 as your stop-loss level; you will be risking 100 points on this particular trade. The moment Nifty falls below 8200, you exit the trade taking the loss. The question however is – how to identify the appropriate stop-loss level?

One standard approach used by many traders is to keep a standard pre-fixed percentage stop-loss. For example one could have a 2% stop-loss on every trade. So if you are to buy a stock at Rs.500, then your stop-loss price is Rs.490 and you risk Rs.10 (2% of Rs.500) on this trade. The problem with this approach lies in the rigidity of the practice. It does not account for the daily noise / volatility of the stock. For example the nature of the stock could be such that it could swing about 2-3% on a daily basis. As a result you could be right about the direction of the trade but could still hit a ‘stop-loss’. More often than not, you would regret keeping such tight stops.

An alternate and effective method to identify a stop-loss price is by estimating the stock’s volatility. Volatility accounts for the daily ‘expected’ fluctuation in the stock price. The advantage with this approach is that the daily noise of the stock is factored in. Volatility stop is strategic as it allows us to place a stop at the price point which is outside the normal expected volatility of the stock. Therefore a volatility SL gives us the required logical exit in case the trade goes against us.

Let’s understand the implementation of the volatility based SL with an example.

This is the chart of Airtel forming a bullish harami, people familiar with the pattern would immediately recognize this is an opportunity to go long on the stock, keeping the low of the previous day (also coinciding with a support) as the stoploss. The target would be the immediate resistance – both S&R points are marked with a blue line. Assume you expect the trade to materialize over the next 5 trading sessions. The trade details are as follows –

- Long @ 395

- Stop-loss @ 385

- Target @ 417

- Risk = 395 – 385 = 10 or about 2.5% below entry price

- Reward = 417 – 385 = 32 or about 8.1% above entry price

- Reward to Risk Ratio = 32/10 = 3.2 meaning for every 1 point risk, the expected reward is 3.2 point

This sounds like a good trade from a risk to reward perspective. In fact I personally consider any short term trade that has a Reward to Risk Ratio of 1.5 as a good trade. However everything hinges upon the fact that the stoploss of 385 is sensible.

Let us make some calculations and dig a little deeper to figure out if this makes sense –

Step 1: Estimate the daily volatility of Airtel. I’ve done the math and the daily volatility works out to 1.8%

Step 2: Convert the daily volatility into the volatility of the time period we are interested in. To do this, we multiply the daily volatility by the square root of time. In our example, our expected holding period is 5 days, hence the 5 day volatility is equal to 1.8%*Sqrt(5). This works out to be about 4.01%.

Step 3. Calculate the stop-loss price by subtracting 4.01% (5 day volatility) from the expected entry price. 395 – (4.01% of 395) = 379. The calculation above indicates that Airtel can swing from 395 to 379 very easily over the next 5 days. This also means, a stoploss of 385 can be easily knocked down. So the SL for this trade has be a price point below 379, lets say 375, which is 20 points below the entry price of 395.

Step 4 : With the new SL, the RRR works out to 1.6 (32/20), which still seems ok to me. Hence I would be happy to initiate the trade.

Note : In case our expected holding period is 10 days, then the 10 day volatility would be 1.6*sqrt(10) so on and so forth.

Pre-fixed percentage stop-loss does not factor in the daily fluctuation of the stock prices. There is a very good chance that the trader places a premature stop-loss, well within the noise levels of the stock. This invariably leads to triggering the stop-loss first and then the target.

Volatility based stop-loss takes into account all the daily expected fluctuation in the stock prices. Hence if we use a stocks volatility to place our stop-loss, then we would be factoring in the noise component and in turn placing a more relevant stop loss.

Key takeaways from this chapter

- You can use SD to identify strikes that you can write

- Avoid shorting PUT options

- Strikes 1 SD away offers 68% flexibility, if you need higher flexibility you could opt for 2SD

- Higher the SD, higher is the range, and lower is the premium collected

- Allocate capital based on your belief in asset classes. It is always advisable to invest across asset classes

- It always makes sense to place SL based on daily volatility of the stock

Hello Sir,

Thank you for creating the financial educational content which is comprehensive and yet, easy to understand.

In the calculation above I am unable to understand how the annualized numbers were arrived.

Daily Average Return = 0.04%

Annualized Return = 14.8%

Daily SD = 0.89%

Annualized SD = 17.04%

However, as per my calculation Annualized Return is .04*252 = 10.08% and Annualized SD = .89*sqrt(252) = 14.12%.

Is my calculation correct or I am doing something wrong?

That is correct, but instead of 252, some prefer to take the full calendar year as opposed to just the number of trading days.

Dear Karthik Big fan of yours, please can you adjust the calulations to identify the strike based on the new exiry days regime. Now as we have expiry on Tuesday for Nifty, it will be better you can explain that from this perspectove

Thanks, Ramen. Its just the day shift, nothing changes.

Hi Karthik I have question regarding expiry, let suppose i sold many OTM call to receive the premium, so to get exit out of the trade on expiry day, do I need to exit before 3:30 PM or leave them, and broker will settle them automatically in CASH?

and let suppose there is seller when we want to square of the position. then how we will buy back? and if we were unable to do so, then what will hapen?

It depends, if there are buyers, your order will go through, else it wont.

You can leave it to expiry, the option will expire worthless anyway. Problem is if it turns ITM, then there will be settlement basis the price.

hi karthick sir

i have calculated the nifty daily mean/average for 18.09.2024 to 17.09.2025

the value is -.008%

is that correct or not sir

what to do if the value is negative sir

If Nifty has trended down during that period, it could be -ve right?

Hi Sir,

Can I use Volatility based targets for stocks that only have a support and no resistance, to Calculate if the RRR values are greater than 1.5, as they are near their all time high.

Of course, you can. Vol based SL has nothing to do with support and resistance levels, you can treat them independently.

Hi karthik in current chapter example we are multiplying 2SD

volaitlity normal distribution

Average + 2 SD (Upper Range) and Average – 2 SD (Lower Range)

= 1.15% + 2* 5.73% = 12.61%

= 1.15% – 2* 5.73% = -10.31%

but in previous chapter

ie;(volatility-applications) example why are we adding 1 to 4.215% it should multiply

Upper Range = 16 day Average + 16 day SD

= 0.65% + 3.567%

= 4.215%, to get the upper range number –

= 8462 * (1+4.215%)

= 8818

Hi karthik in the below chapter ex we are multiplying 2SD

volaitlity normal distribution

Average + 2 SD (Upper Range) and Average – 2 SD (Lower Range)

= 1.15% + 2* 5.73% = 12.61%

= 1.15% – 2* 5.73% = -10.31%

but in below example why are we adding 0ne it should multuply for 1SD

volatility-applications

Upper Range = 16 day Average + 16 day SD

= 0.65% + 3.567%

= 4.215%, to get the upper range number –

= 8462 * (1+4.215%)

= 8818

Dorry, not sure if I got your query fully, but for 1 SD, the co efficient is 1 right?

do we have to calculate daily and annualized value for average and standard deviation manually everytime. OR we can just get the data from nse website. I have been able to find daily and annualized volatility of nifty contracts but not averages. Can we have this data over nse?

For quick reference, you can always take it from the website.

Dear Karthik,

First of all, thank you for the excellent content. I tried applying these principles for identifying the strike price of Nifty 50 but got few questions here.

1. I have downloaded the Nifty50 historical data on 27-Jun-25

2. Calculated volatility (Standard deviation) whose value is 0.86%

3. Daily average = -0.02%

4. SPOT of Nifty 50 = 25,620

5. Date of Option expiry = 3-Jul-25

6. Days to expiry = 4 days (Not counting Saturday and Sunday)

Calculations:

4 Days SD 1.72%

4 Days Average -0.10%

Upper Range 1.62% and strike price = 25621

Lower Range -0.88% and strike price 25621

Here I am confused. The Upper range and Lower range are same. The strike price is just 1 point above the spot. Am I doing something wrong? Can you please comment on this?

I guess I found the mistake. I am multiplying the SPOT value with logarithmic %. I should first convert them into exponential and them multiply with SPOT.

But I would like to hear from you (Karthik) if I have missed anything.

Ah ok. Glad you figured 🙂

I think you subtracted volatility and added average incorrectly (or vice versa). Can you please double check?

Hi Karthik,

Let\’s say we have a two year daily closing price data of nifty. Starting from the 2nd year if I find out the natural log of the yearly returns and then standard deviation, does this standard deviation approximately equal to the yearly standard deviation using square root method?(daily std dev * sqrroot(252))

Thanks,

Siva

Yes, on approximation, it does 🙂

At the bottom in \”note\” section where we calculate 10 days volatility, why we have multiply it with 1.6 instead of 1.8??

Probably some error

Dear Mr Rangappa,

Thank you very much for the entire Zerodha Varsity series. The entire series is an outstanding compilation and most of my knowledge of trading and investing is from the wonderful, lucid chapters that you have written. I cannot thank you enough for the same.

After going through this Chapter, I was wondering how to estimate the time that I \”expect\” (5 days in the chapter above) to hold the position. In the aforesaid text, it is one of the inputs based on which we are computing the volatility. How do I form this kind of an expectation.

Kindly guide me.

Kind regards,

Thanks Barun for the kind words, and I\’m glad you liked Varsity.

These expectations can be draw by looking at historical volatility and comparing with the present day volatility.

Hi karthik, first of all i would like to thank you for writing such great modules in a simplified manner.However just wanted to clarify that in the last topic of this chapter \”volatility based stoploss\”, you have directly subtracted the standard deviation of 5 days from the expected entry price instead of subtracting it from 5 days average & then converting it in exp(%) to get the range of the stock price for next 5 days.could you please provide the rational behind it…as same was not exercised in the previous chapters.

Here is the exact calculation for determining the price range:

Calculate daily log returns.

Calculate the mean and standard deviation (SD) of the log returns series.

The 68% confidence interval is:

Current Price × exp(mean × time ± SD × √time)

The 95% confidence interval is:

Current Price × exp(mean × time ± 2 × SD × √time)

This process involves computationally intensive tasks such as calculating log returns and exponentials.

Under the following circumstances, the above calculations can be approximated with simpler methods:

Short time periods: When the time period is small, the term (mean × time) becomes negligible compared to (SD × √time). That is, mean × time << SD × √time.

Small daily movements (<10%): When daily percentage movements are less than 10%, percentage returns and log returns are nearly equal. Since percentage returns are computationally faster to calculate than log returns, they are often used as an approximation.

A computationally faster approximation method is:

Calculate percentage returns.

Calculate the mean and standard deviation.

The 68% confidence interval is:

Current Price × (1 ± SD × √time)

The 95% confidence interval is:

Current Price × (1 ± 2 × SD × √time)

I might have switched between the approximate and accurate methods in different chapters.

If you are implementing a system, a good rule of thumb is:

Use the simpler method by default. If the calculated price range exceeds 20%, recalculate using the accurate method. Otherwise, proceed with the approximation.

In last but 2nd para airtel volatility is 1.8*sqrt of 10 for 10 holding days right?

It is mentioned 1.6

Ah, need to check. Will get back.

Hey Karthik, I think something is wrong with the video, as it runs only 41 seconds. Could you help me out with this?

Thank you

Ah, I think there was one more. Will share.

Thanks a lot

Happy learning!

Hello Karthik, Excellent Module on option trading.

I have a doubt, How can I use Volatility based stop loss for trading options?

Found an old video, please excuse the quality, but the concept stays intact 🙂

https://www.youtube.com/live/IrSZBgFCf00?si=yHpYjy69YKRnL8wl

the video lasts 41 seconds

Hello Karthik,

I have a doubt, Last chapter you have taken exponential to convert the LN % to regular % for calculating range , and In this Module here you have added and subtracted 1 from the (avg+sd & avg-sd), which one is correct.

Can you please clarify on this? Are both the same?

These are two different techniques, Arun. I\’ve explained this in earlier comments.

Just Gone through Nassim Nicholas Taleb\’s framework on building a barbell portfolio.

Where 90% of the assets are parked in a safest side(Hyperconservative) like t-bills and 10% of the assets are parked in speculative bets(Hyperagressive) like option portfolio, high beta stocks.

I think it\’s an amazing approach to apply in real life to deal with randomness and black swan events.

The payoff graph in sensibull (\”Unlimited Loss\”) might give crazy amount of anxiety while dealing with selling overnight strangles. 🙂

Hahah, sure. This has been practiced for a long time now. The core and satellite approach to portfolio building also works on similar lines.

hi, sir can you please also explain what to do if i get a negative average/mean value.

Its possible, especially when the returns are trending down. Maybe buy puts 🙂

when will you make a chapter on \”volatility arbitrage\” as you said at the starting of this chapter there\’s already one on pair trading

Ah, check option strategies. Straddle, strangles etc are all part of Vol arb.

No worries, but can you please clear out a few points for me?

1. To calculate daily average for a year, I should divide the daily returns by 252? Is there any website where the daily average is available?

2. For the SD, I can refer the NSE website, right?

3. If I use the ln(y\’day\’s price/today\’s price), the calculation for the range for the next 7 day is

=((daily average * 7)(-/+)(SD*sqrt(7)))

This would be really helpful, thank you:)

1) No, you need to multiply daily return with 252.

2) Yes, you can.

3) Yes.

Hi Karthik, can you please confirm if the following calculation for Nifty sep 19 expiry is right?

spot: 25388.9

days: 7

dailyAverage: -0.000927225

dailySD: 0.0087

AvgForGivenDays(7): -0.006490578

SDForGivenDays(7): 0.023018036

Lower Range 24639.70875

Upper Range 25808.514

Thanks a ton:)

Ah, wont be able to do that Dixit 🙂

Since there is a higher chances that the data lies in the range, so we can make more accurate decisions?

Makes sense to think of this in terms of range, as opposed to a specific value.

In the 1 example; why did you select 1SD and not 2/3 SD? since 2 and 3 SD are more accurate than 2sd right?

What makes you say that?

Hello Karthik Garu…you changed my views on seeing option trading…still in progress but would like to appreciate the way you put all things together and explain it in awesome manner. Thanks again sirji…No questions right now…

Thanks for the kind words, Suresh. I hope you continue to enjoy learning on Varsity 🙂

Thanks for clarifying.

hello sir, i have a confusion in last chapter u have taken exponential to convert the LN % to regular % for calculating range , and here u have just added and subtracted 1 from the (avg+sd & avg-sd), whichich is correct. can u please clarify on this? i mean the last step of range calculation is different in previous chapter.

They are two different methods, Manohar. Either is fine.

Sir, I am asking this.. In the volatility application section, you have explained how to predict the total price movement

of a stock/index by adding/subtracting daily volatility to the previous day closing price. But my question is instead of using the closing price of the previous day, how can we predict today\’s price range by using the yesterday\’s price range of a stock/index? I hope I am able to make you understand my question now.

Kindly help me with this sir.

Got it. But developing a sense of where the volatility is heading on a daily basis is as good as getting a perspective of the daily range. Stock returns is a good is a better input for this than the previous day\’s range.

Hello Karthik sir,

You have explained how to today\’s price movement by adding/subtracting daily volatility from today\’s opening price.

But I have a slightly different query here. Instead of using opening price, if I consider yesterday\’s range. Suppose

yesterday\’s range was 500 points. How to predict today\’s price range using yesterday\’s range (500). Please help me

with this sir.

Regards

Sandeep.

Sandeep, slightly confused with this. Can you pls add more context?

While calculating the range of Nifty, can\’t we just directly add or subtract the Std. Deviation from the spot? What significance does the mean add in the calculation?

Yes, you can.

In the example you have shown this.

Upper Range = 16 day Average + 16 day SD

= 0.65% + 3.567%

= 4.215%, to get the upper range number –

= 8462 * (1+4.215%)

= 8818

What if I use exponential feature of Excel via results IS not same

Ah, not sure. Can you double check the formula you have used in excel once?

Hi Karthik

In the lower and upper bounds calculation, since 4.215% is the log value, the lower bound should be 8462*exp(4.215%)=8826 and not 8818.

Checking on this, Yaqoot.

sir. here what is meant by daily average is that

Daily avg of the price change.

Noted. Thanks much!

Sure, happy learning 🙂

Hi Karthik,

Thank you for first of all for detail explanation. I had a small question.

In your example for you quoted Current market price as \”Nifty current market price = 8462\” , so my question is :As the prices keep changing by the second , do we take the lowest or the highest price of the day the underlying is trading at or average of the both to calculate upper/lower for the next 16 days.

In most cases, you take the closing price of the day, Deepen.

Hi Karthik,

This chapter was great, especially the option strategy you talked about.

Thank you very much.

Thanks, happy learning Rajol!

😊

sorry i has a correction

Annualized SD = 0.89*SQRT(245)= 13.93

what ever its not Annualized SD = 17.04%,Annualized SD = 17.04%?

where i make mistake?

I need to double check as well. But if there was a mistake, others would have pointed out by now 🙂

if the chance of decimal misplacement that will the observation day (252). what ever i got the observation date from

your previous comments that was 12-aug-2014 to 10 -aug- 2015. the total observation from these date is 245 days then i calculate the

Annualized Return= 0.04*245= 9.8

Annualized SD = 0.89*SQRT(245)= 14.13(sorry the previous comment i mentioned % sign i had not taken in the calculation)

even i gave to chatgpt then i got these answer

Annualized Return= 0.04*252= 10.08

Annualized SD = 0.89%*SQRT(252)= 14.13

Sure, let me also check from my end.

Daily Average Return = 0.04%

Annualized Return = 14.8%

Daily SD = 0.89%

Annualized SD = 17.04%

Annualized Return= 0.04*252= 10.08

Annualized SD = 0.89%*SQRT(252)= 14.13

HOW YOY GOT 14.8,17.04 ? THIS I DID CURRECT WHERE I MISSED?

Must be some decimal misplacement?

Hi Karthik,

The method you suggested for writing call that is 1 week before expiry in OTM. I got a basic doubt.

Below is the data of Banknifty 28 Dec 49100 Call (expiry is today, BANKNIFTY closed at 48500):

O:24, H:75, L:0.1, C:0.1

What is the problem in this approach: I can sell the call option in the morning for 24 rupees and wait till evening because anyway I am confident upto some extent that this call will remain OTM, and eventually premium will goes to zero. I can earn all the premium. It\’s not just about this OTM, there are other strikes higher than this which are also doing the same.

I don\’t have to wait for 1 week, on the last day of expiry I can write call and earn easy safe money. Please help me to understand, is there something I am missing in above approach?

You can do that Arnav, but the assumption here is that the intrday volatility wont shoot up driving the premiums higher. If that happens, you will have trouble with your option.

If Banknifty has a volatility of 14% on 1st week expiry and 15% on next week expiry then how to consider the daily volatility? bcoz it evincing a pretty miniscule number when weekly volatility is divided by the square root of time

plz suugest. Thanks!

You can assume its avg of 14% and divide it by sqrt of time.

Sir if today nifty is trading at 20919

And vix is 12.83 can we predict niftys range for 1yr, 1m ,1w range by just spotprice and vix .

Can we say that nifty range gor next 1 yr can be upper 20919+12.83% and lower range 20919-12.83%

Yup, you can.

Sir on pagen no 144 of module 5, we have

nifty spot 8547 and nifty volatility 16.5% by above information we have calculated nifty\’s

lower estimate =8547-(16.5%*8547)=7136

Upper estimate =8547+(16.5%*8547)=9957

Spot-(annual volatility*spot)=lower estimate

Spot+(annual volatility*spot) = upper estimate

Above calulaion suggest that nifty is likely to trade between 7136 and 9957

BUT,

ON page no 163 and 164 we have spot 8337 and daily volatility 1.046%

Therefore annual volatility is 16.61%

By above info we have calculated nifty upper range = spot*(average+1SD)

Lower range spot *(average-1SD)

Upper range =10841

Lower range = 7777

My question is why we need (avarage + 1SD )and (Average – 1SD) to find range

Why dont we just take 1SD for one year ie 16.61 %

By which we get

upper range= spot+(volatility*spot)

8337+(16.61%×8337) =9721

Lower range = spot-( volatility*spot)

8337-(16.61%*8337) =6952

Why in first case we used

Spot+(volatility*spot)and spot-(volatility*spot) to find range and in second why we used different formula

(Avarage+ 1SD) and (Avarage-1SD) to find range. Why we needed average to calculate range , please help im not so good at maths and i have just started to read this module,

Here is the exact calculation for determining the price range, especially if you are using log method (next chapter).

1. calculate daily log returns

2. calculate mean & SD of log returns series

3. 68% confidence interval is current price * exp (mean*time +/- SD* sqrt(time))

4. 95% confidence interval is current price * exp (mean*time +/- 2*SD*sqrt(time))

The process involves computationally intensive tasks such as calculating log returns, calculating exponential of a value etc.

Under the following circumstances, the above calculations can be approximated with more simpler calculations

1. Short periods of time: When time is small, (mean * time) is so small that it hardly makes any difference to the final value i.e. mean * time << SD * sqrt(time)

2. When daily percentage movement 20%, recalculate with accurate method, otherwise you can process with approximation.

Hi Karthik, great chapter. I have one doubt though, early on in the chapter, the lower range is calculated by multiplying current price times one plus average return for the number of days plus the standard deviation. However, in the later section, you have calculated the lower range simply by multiplying current price with standard deviation for the number of days. I believe the method mentioned above i.e. (Current price * ( 1 + average return + standard deviation) is not an appropriate way to calculate the upper or lower range. The method which is used in the last section of the chapter seems to be the appropriate one. Could you kindly help double check the same. Thanks

These are two different techniques, I\’d suggest you stick to the one which you find easier to implement.

im just beginner and trying to understand option trading, i have been using your module 5 and it helped me a lot to understand basics.

I was reading volatility chapter (17.4 ) and im so confused about the range as on page no 144 (15.3) we calculated range by just volatility ,but in 17.4 (page no 163)we are calculating range by avg+volatility ,

My question is why the upper range is not 8337+(16.5%*8337) or lower range 8337-(16.5%*8337) ie why not the upper

Range9712 and lower range 6961

Prasad, is is that only right? Not sure if I\’m missing something.

Hi Karthik,

Thank you for the articles.

I have a question regarding how you calculated the SL for Airtel. You calculated the volatility to be 1.8% but then you directly deducted the volatility from the price. But in previous chapters, you always added and deducted the average from SD to arrive at the Upper Range and lower range. Why we skipped that step here?

I was expecting it.

Upper range = (Average daily volatility * 5) – (Volatility or SD SQRT (5) )

Can you please clarify

Both are fine, Vasanth, especially when the daily mean is very low.

Sir, I have 2 douts

1st, why you calculate reward from SL

(417-385=32), Not from expected entry price 395.

And 2nd thing is,

When we got the new SL 375.

Then, with the new SL, only the risk is changing, why is the reward not changing?

new risk is 395-375=20 point.

Then the Reward will be 417-375=42 point.

But you calculate RRR (32÷20=1.6%)

That means Reward is 32.

That is correct, please do check the comments, others have also pointed this out.

Oh I see, 🫥. Then don\’t you think that probability in this bharti airtel trade is very minimal , the reward is 22 points and risk is 20 points. Coming to approx 1:1 RR. And can we use this volatility based stoploss technique while trading USD INR?

Yes, you can apply to any asset that has a time series of prices.

\”Step 3. Calculate the stop-loss price by subtracting 4.01% (5 day volatility) from the expected entry price. 395 – (4.01% of 395) = 379. The calculation above indicates that Airtel can swing from 395 to 379 very easily over the next 5 days. This also means, a stoploss of 385 can be easily knocked down. So the SL for this trade has be a price point below 379, lets say 375, which is 20 points below the entry price of 395.

Step 4 : With the new SL, the RRR works out to 1.6 (32/20), which still seems ok to me. Hence I would be happy to initiate the trade.\”

Hello karthik sir,

I could not get the RRR calculation in step 4: my entry price is 395 , my target price is 417, and my stop loss is 375. so my reward is (target{417}- entry{395}) = 22 points and risk is entry – stoploss price (395-375) = 20 points. How 32 is coming in the step 4 calculation ? Please guide me 🙂.

I think I made a typo 🙈

Hi Karthik

Can you please guide how to predict daily, weekly and monthly Nifty range using INDIA VIX.

It will be helpful for all of us. Thanks in advance.

You can use the same volatility-based prediction technique (based on normal returns distribution) we discussed here.

Hello sir i have a doubt In previous module for getting upper and lower range of nifty 50 you first convert log percentage into regular percentage then you multiple exponential of that into nifty current market price to get nifty range in numbers BUT in this module you did not convert log percentage into regular percentage you directly multiply with current market price and add that to CMP to get upper range of nifty same you did to find lower range you did this 8462 * ( 1 + 4.215% ) = 8818 same method you did to find lower range you did not multiply exponential of 4.215% to 8462 MAY BE I AM ASKING SILLY QUESTION MY MATHS IS WEEK PLEASE ELABORATE THIS THANKS IN ADVANCE

hello sir ,I have a doubt in this module please solve this as soon as possible ! in previous module for finding the nifty range of 1 year , you calculated 1 st 1 year average and 1 year standard deviation then you added and subtracted S.D. from average range of nifty in percentage for 1 year . ( THEN YOU SAID CONVERT LOG PERCENTAGE INTO REGULAR PERCENTAGE ) then you multiply EXPONENTIAL of log percentage into 8337 nifty level BUT in this module you directly multiply 16 standard deviation with current market price and added with current price for geting nifty 16 day upper range same you did to get lower range YOU DIDN\’T CONVERT LOG PERCENT INTO REGULAR PERCENT WHY????? please explain in detail thanks in advance

They are two different techniques, Vinayak. I\’ve explained this in the comments above 🙂

That is an excellent explanation sir. But in this case we are calculating SL for short duration trades(4 days in this case). But what about long duration trades. For eg if one is bullish on NIFTY and want to initiate a put bull spread at 19000 on a long term contract like monthly or even a 15 days duration, wont the volatility based SL be deep in the money? We cant place SL so deep right? In that case, could you tell how you would approach such a situation? Thanks.

The good part is that you can scale volatility to whatever time frame you are working on. But yes, the SL may turn out deep. Alternate to this is to go by fixed % method, where you conclude that you wont risk more than 3% of 5% of the capital.

Got it Sir. I gave this chapter another read and 2 questions popped up in relation to Index trades. I hope you could answer this.

1. As you have mentioned, there are a lot of instances where the trade seems to end up against me, due to which I exit, only to find out that the trade takes a U turn and finally ends in my favour. So these days I want to strictly exit the trade only when my breakeven point reaches. I totally understand that it is difficult to teach conviction. But could you point me to some books which can make me do this better? (I have noted all the other books you have suggested throughout the entire module)

2. You have mentioned that you will quit your call option position if it turns ATM or ITM. Lets assume a situation where the spot goes against you and ends near your breakeven point 2 days before expiry. At this moment, your position is still an OTM and the You have 2 more days for expiry. What would you suggest in this situation?

– Exit the trade fearing that the spot might open gap up or gap down extending the losses (or)

– Would you still wait for the contract to become ITM before exiting?

Since RR is not good in most strategies, I guess you can understand why I\’m asking this. Thanks for guiding me as a good Mentor🙂.

1) This is quite common, Sathish. The only way ard this is to place logical stop losses. Something like a volatility-based SL. As far as reading material is concerned, I\’d suggest you look at the articles in inner worth.

2) Its very hard to answer this. It helps to have a system in place where in these decisions are driven by factors defined in your system. But at ATM, I may not panic, but if the positions goes deep ITM, you need to be worried 🙂

Since we are calculating SD and then selecting the strike away from 1SD, doesn\’t the breakeven itself act as a stoploss. Do we need a seperate volatility based stop loss? Thanks.

It does act as a SL, but you do need to have a SL as it serves as another layer of protection 🙂

Can i use volatility stop loss for intraday option trading

Yup, you can do that.

Sir I have already asked regarding not so attractive risk reward when deploying this SD calculation in hedged strategies like iron condor. But in Sensibull the SD calculation result seems to be vastly different from the results using this chapter\’s method. I guess the formula used in Sensibull is 1SD = Spot Value x ATM IV% * SQRT(n/365), where \’n\’ is the number of days. If I use this the RR is much better. Can I use this method for hedged strategies? Thanks

Yeah, you can Sathish. They probably use the ATM IV for proxy implied volatility.

I\’m just getting more confused 🤔

In this eg. You have taken daily average return and daily SD

In prior eg. You took average returns of 2 days log returns ?

I have got the concept but can u explain the calculation\’s in easy way.

These are two different techniques. You can opt for either one, I\’d suggest the daily average range.

Hi sir,

1.Will you please explain the calculation\’s you did for Nifty

8462*(1+4.215%) why did you add 1.

2. And in prior slide you used exponential to do the same.

1) You add 1 to get the percentage incremental value.

2) Sorry dint get the complete context here.

Hello,

Amazing Karthik sir.

I keep regularly reading this explanation of selling call options it\’s an eye opener

It\’s an eye opener, if you had any more such magical articles please provide the link.

You are a great teacher

Regards,

Mukesh

Ps , pls share from which source to get nifty daily average and daily sd

Thanks for the kind words, Mukesh. I\’m glad you liked the content. Not sure who publishes the daily SD values.

Dear Karthik,

A very well written article, request when you have time pls post more on selling put options along with the source of getting accurate S.D and Average to get a proper picture.

Thanks once again.

Regards,

Mukesh

Noted, will try and do this Mukesh.

Hi Karthik, Great content.

I have some queries,please guide me,

1.is above strategy of writing deep OTM options which are outside 1SD or 2SD range financially feasible when margins have become larger compared to earlier??

2.Now as nifty has weekly expiry,so what strategy you adopt regarding writing options as now the Friday becomes the first day of weekly series meaning still is it wise to write on fridays or when lesser number of days are there for expiry say 1 or 2 days?

Thanks in advance 🙂

1) These are typically short-term trades; if you have the capital, then why not 🙂

2) I\’d suggest you look at Tuesday or Wednesday for writing. Perpahse it strikes a balance in terms or theta decay and premiums.

Hi Karthik,

Came across you notes and have been going through the options section to improve my learnings. Your explanations and notes are fantastic. Thanks for doing this.

Quick question, on the last example (volatility based stops) where you have noted Reward (417-385) = 32 should that be (417-395) = 22 as the entry price is 395?

Neel, thanks. I need to double-check this, but you do get the gist I suppose.

First of all, I thank you for your efforts to enlighten people like me. It is just that I am unfortunate that I have been reading the Zerodha Varsity contents very late, after around more than 7 years.

I have a doubt in this chapter:

In the previous chapter you multiplied the CMP to exponential of (Average% + SD%) or (Average% – SD%) to get the results. In this chapter you multiplied CMP to (1 + Average% + SD%) or [1- (Average% – SD%)] to get the results, without using exponential function.

If we use in this chapter the formula that you used in the previous chapter, we get the higher limit as 8826 and lower limit as 8218, which seems OK. However; if use [1 +/- exponential of (Average% + SD%)] and [1 – (Average% – SD%)] we get bizarre results.

My concern is that when we multiply CMP by exponential of (Average% + SD%) or (Average% – SD%), we get the return after certain period. And, therefore; we need to add return to CMP to get the upper and lower limits. But, if we do so, we get 18015 instead of 8818 and 244 instead of 8214.

I hope I could able to explain my concern to a level where you would be able to get it. I hope you will address my doubt that which one we use and why.

Rahul, its better late than never. Sharing a response I had shared earlier –

Here is the exact calculation for determining the price range

1. calculate daily log returns

2. calculate mean & SD of log returns series

3. 68% confidence interval is current price * exp (mean*time +/- SD* sqrt(time))

4. 95% confidence interval is current price * exp (mean*time +/- 2*SD*sqrt(time))

The process involves computationally intensive tasks such as calculating log returns, calculating the exponential of a value etc.

Under the following circumstances, the above calculations can be approximated with more simpler calculations

1. Short periods of time: When time is small, (mean * time) is so small that it hardly makes any difference to the final value i.e. mean * time << SD * sqrt(time)

2. When daily percentage movement 20%, recalculate with accurate method, otherwise you can process with approximation.

Sir,

I am trying to follow your guidelines for normal swing trade in the capital markets and finding it good (till date). However, I am only 2 months old to this market. I have read the futures segment and I am now going through the options learning. However, I could sense that there are a lot many variables in F&O trading, specially in options.

Thus, I feel I should go for paper trading for quite some time in F&O and intraday/MIS before actually come to these derivatives market. But I have no idea how/where to paper trade. Could you please guide here?

Instead of paper trade, i\’d suggest you buy sell 1 lot of CDS contracts. In terms of margin, it is not much, but it gives you a lot more confidence in understanding the market.

Hello again there,

Once again very insight full and eye opening session for me. Expecting lot more to come.

I have following 03 queries regarding Volatility based Stop Loss:

1) You assumed the Airtel trade to hit the target in 5 days. How flexible can these be in days? Because our volatility calculations will be based on these days.

2) Is it okay to take into consideration Daily Volatility of stocks/ indices (although they based on Futures) mentioned on NSE website?

3) I would like to have more insights on \’Trailing Stop Loss\’. Where can I fine one?

Thank you in advance.

1) These are expectations based on numbers, but the actual outcomes may vary a bit, so its best to be prepared for that 🙂

2) Yup, it should be ok

3) Maybe this should help – https://www.youtube.com/watch?v=rSYyB9fBsSs&list=PLX2SHiKfualEyD05J9JsklEq1JFGbG6qJ&index=6

Please try the link now. My understanding about the volatility for a given stock/index is that it should be more or less the same for adjacent strikes. But here it looks odd, kindly clarify.

https://drive.google.com/file/d/174lSuxJrj70N8-yRg3zqzWPHR5QR_yOH/view?usp=drivesdk

More or less yes, but then it also depends on the demand and supply of each strike.

Please try the link now. My understanding about the volatility for a given stock/index is that it should be more or less the same for adjacent stikes. But here it looks odd, kindly clarify.

That depends on the demand and supply for the strikes as such.

Typo, it is actually May2023 expiry.

Hi Karthik, the below link is snapshot of the option chain of Nifty April2023 expiry. The premium of the red encircled strike is exorbitantly high, why?

https://drive.google.com/file/d/174lSuxJrj70N8-yRg3zqzWPHR5QR_yOH/view?usp=drivesdk

Unable to open, but if the premiums are high, always check whats happening with the volatility. Premiums increase if volatility has shot up.

Hi Karthik,

Wondering as to what motivates people to buy strikes outside 1SD when there is just 32% probability of such strikes transitioning to ITM and most of the times expiring worthless. Would you please apprise me on this?

Different opinions is what forms the market, some feel safe within 1SD, some with 3SD 🙂

Does this work on a weekly scale.

Yeah, it does. Everything remains the same, except that the timeline shirks.

How SD save to st chart in kite.

Mentioned Calculation in both chapter(Volatility normal distribution and Volatility Applications) are different from each other, it is confusing. Do we need daily average return or mean? Also mentioned Range calculation differently in both chapter. Can anybody explain this.

Its not Prashanth. These are two different techniques of calculation. I\’ve explained in the comments, and I request you to scroll through the comments. Thanks.

(Continued W.r.t last query). Because in both the situations, be it short straddle and the topic discussed here, we are dealing with the same situation, that is selling options without hedging, centered around major events and it is contradicting each other. Hence the confusion. Hope you get the point. So if you could clarify this, it would be helpful. Thanks Sir.

Got it, but like I mentioned, naked short positions are scary, but you certainly can initiate a spread to benefit from cooling volatility.

Yes sir. I have read the short straddle portion where you have mentioned that it is best to deploy this strategy around major events. Since here the information is contradicting that, I was confused as to how to approach this. That is why I asked. Thank You.

Ah ok. Naked positions are scary, spreads are ok 🙂

Another query Sir. I assume you have given this information based on non hedged based strategies. You have advised not to write put options due to potential fast downside movements. But if I were to use iron condor using SD, I have to write put options as well. So in this case is this irrelevant? Also would like to know whether you would not take even hedge based strategies like iron condor before major events. Thank you.

Yes, my point was mainly keeping a naked put in perspective. Hedged strategies are perfect for event-based trade setups.

Sir, You have mentioned that you avoid writing options before market events. But isn\’t that the time to write options as premiums would have swelled up and expect to come down eventually. Given the current situation, one way or the other too many events are lined up continously throughout the month. In that case it would be difficult to take even a single trade. Please kindly clarify about how to approach this.

I agree, I think in the later chapters (maybe option strategies), I\’ve explain this in more detail.

Hi Karthik, first of all, many thanks to you and Zerodha team for this initiative and for sharing your knowledge, this is extremely helpful for beginners like me…

I have 2 questions in this module:

– in previous module, once we found the range as [mean (+ and -) SD] in log percent form, we calculated absolute points using spot * exp(). But here in 18.1, we have used percentages directly to get the absolute values from percentages. How do we decide this…

– in 18.2 – volatility based calculation of stoploss..

If spot price is 395, target 417 and stop loss at 385, the reward would be 417 – 395 = 22, and the risk is 395 – 385 = 10, so RR ratio would be 2.2 – am I missing something here?

Thanks in advance..

Thanks, glad you liked the content.

1) For this, I had posted a detailed response in one of the comments earlier. Can you please check that?

2) This could be a typo, let me check 🙂

sir very good material.thanks but we need more and complete course on quantitative trading.again thank you for your effort and world class teaching.

Thanks for the kind words, Suresh. I\’ll check on this 🙂

Wipro one month return and one yr return is in Zerodha\’s Wipro search. it is negetive. pls illustrate the 16 days return to find higher and lower range price for call shorting. cmp is 390.45 and SD i have got from Fin box site as .97.

Ah, we have shared the steps to do the same. Request you to kindly download the data and execute the steps.

Hi Karthik,

Can you please give an example on how to use vol based stop loss in case of option selling. Since stop loss would be on premium and we are calculating upper range basis spot of Nifty, am not able to quantify how to translate that to premium value to place a stop loss for options.

Thanks

Nayan, one way to do this is to set up a SL based on the underlying. If you were to do this, then the underlying price works as a trigger to take action on the options trade. I\’ll probably do a video on this topic sometime soon 🙂

Sir, where to find daily volatility for a stock in Zerodha ? as you mentioned ATR is not really a standard deviation.

You can use the Bollinger band also, it is a volatility indicator.

Hello Sir, Currently I use weekly option for trading. I\’m interested in calculating the range based on 1sd and 2sd and selling the options. Can I know how many months previous data I should be analyzing if I\’m doing weekly options?

In 18.2 section..the Airtel example you have mentioned reward of 32

It should have been 22 (417-395)

And by that your reward to risk ratio also changes

Let me check this.

Sir, nice modules. Short and sweet. I am confused with average and standard deviation/volatility calculation. While mentioning examples you said average, STDEV. But in nifty it is mentioned average, annual average, and STDEV. No confusion in STDEV/Volatility. Since Volatility calculated as STDEV of daily return. Having confusion in calculation of daily return vs average. Sorry for basic query. Regards

Can you point of exactly what the confusion is? Isit the formula to calculate or something like that? It will help me give a better explanation 🙂

\”the SL on options is best derived based on the spot value\”

What does this mean?

Shouldn\’t we consider the volatility for SL in option?

Volatility of the spot, eventually thats what impact the option premium.

Hello sir, I am having trouble calculating daily average return and daily SD using excel sheet. Is there any other way I can calculate the same or any site presenting this data?

\”I personally use this strategy to write options\” – SD1 here\’s a chance of 68% that the spot wouldn\’t cross the upper estimate.

We\’ll be gaining around 1.5% in 16 days.

But what if it\’s a black swan event, how much are we at risk.

it\’ll be too much I think

Yes, the risk of black swan does exist 🙂

HI Karthik,

Brilliant content 🙂

I am still not clear about the stop loss for call / put option for both long and short. Could you please add an example

Thanks

Gourab

Glad you liked it, Gourab. Have explained both here – https://www.youtube.com/watch?v=-mO0YOTcCiQ&list=PLX2SHiKfualFiusiT9G5uE9jU3vetvW2x

Hi karthik, where can I find the returns and volatilty data on NSE site for indices??

I\’d suggest you download the bhavcopy, Venu.

i am using zerodha from 2016 , but after i was introduced to quant trade and got some basics . now when i read this it is really useful.

If someone would followed this they would have got 60 day challenge certificate. Really thank you for this great explanation.

Happy learning, Abhilash!

Hi Karthik

Can we predict the nifty range using INDIA VIX?

Yeah, you can get a range. I will be sharing a video on this on our Youtube channel soon. Please keep track on the update.

Hi Kartik

Thank you for the article

I had just 1 doubt

Lets say I am writing option on Fri 3:15 PM for next Thu Expiry

for calculating upper range I would take—- no of days avg + no of days standard deviation

My doubt is

Is the no of days 6 ( Sat to Thu)

OR

Is the no of days 4 (Mon to Thu) —- as Sat Sun are trading holidays.

I am not considering Fri in days calculation as I am writing option at 3:15 PM

You can consider Mon to Thursay.

Hello, Mr. Karthik on 11-10-22 I posted a question regarding the absence of Exponential in the current chapter. Later I read a previously posted reply:

(When you take log percentage, it\’s important to convert the same back to the regular % scale. In the 1st method, we are directly doing it, in the 2nd we are splitting it over 2 steps….both are essentially the same. Suggest you stick to the 2nd method.)

I humbly request you to elaborate on the splitting of 2nd method over two steps.

I prepared my excel sheet as per the exponential method and now I am eager to learn the math behind the second step.

Shalini, I\’ve put an explanation for this (responded to your previous query with the same); please do check that once.

In this chapter, the upper range is calculated as 8462 * (1+4.215%) and the lower range as 8462 * (1 – 2.920%) while in the previous chapter EXP(exponential) was used. Is it because the returns mentioned in this chapter are not daily log returns ?? Please explain utility of both formulas.

Shalini, I\’ve put up an explanation for this in the comments section (maybe a few months ago). Can you please check that once?

Sir,is the ATR a thing that is gonna be taught in upcoming chaps.

We have discussed ATR here – https://zerodha.com/varsity/chapter/supplementary-notes-1/

Sir,question to your reply of my above answer

So replacing 1 with 68%, isn\’t it possible

No, you should not be doing that.

Sir,

In one of the answer,you quoted \”If the movement of that 1 day is significant, then it will have the impact to change the volatility of the last 300 days. So better to include all data points.\”

Which all data points is reffered here?

We are talking about the stock price data here, Franklin.

Sir,

Here,I replaced 1 with 68%,as 1SD=68%.In a previous query,You have told,it is possible to do so.

Ah no, that 68% is the probability of the event, right?

Sir,it is said that

= 8462 * (1+4.215%)

can also be written as

8462 * (68%+4.215%)

But in the second case the answer turns out to different one

Sorry, I\’m not sure if I fully understand the logic of replacing 1 with 68%.

Sir, while finding the RRR, why have you taken stop loss(385) for the calculation of reward? Shouldn\’t the reward be calculated by subtracting 395(entry point) from the target?

Yes, thats right. I\’ve overlooked this, I will fix this 🙂

Hi Karthik,

What is the best way to learn trading, any course? books or it comes by time?

I just want to perfect the basics to technical analysis and option trading before starting but not finding where to get started from

You are in the right place to learn to trading, Saif! Please explore all the modules here that are available for you.

Big Thank you Karthik Sir and Zerodha for your efforts to make the options learning simlifty.

Happy learning 🙂

Thanks very much for sharing these finer details. These articles are fantastic.

I\’m a beginner and don\’t know how big is the market. But wanted to understand a buyer, seller mindset. What would happen to your option selling strategy, if all of the traders adapt it ?. There would be no option buyers right ? (i.e market has more sellers than buyers.).

Can you please through some standard deviation of failing on a trade because there are no buyers ? (on the list of stocks and indexes you have mentioned). in case if there are buyers, why would they buy which are outside 1SD when so close to expiry ?

A trade happens only when the buyer and seller agree to transact. The buying interest dies when liquidity dries up, and if you are holding on to a position, it will get settled by the broker.

In the 16 day calculation, why haven\’t you converted the upper range (4.2% something) from logarithmic to normal using e^(4.2%)? This was done in the previous chapter, but not here.

There are two different techniques. I have explained both in detail in one of the comments above. Please do check that once.

Is there any study available in kite which plots these SD range values for 1 SD, 2 SD etc.

Asking this since manually calculating it will tke lot of time.

You can use the bollinger bands for this, Sandeep.

I have a doubt sir. In the section of selling call options u calculated the strike price as present price + no days to expiry × average daily return + daily volatility x sqrt of time to expiry. But in the section in stop loss u just calculated it as present price – daily volatility x sqrt of time. Why hv u excluded the average daily return x no of days? Is it bcz it is a short term trade?

Yeah, short-term and usually the average is very small to make a difference over the short term.

First of all thanks for great job. I have a doubt regarding predict range of underline price(such as index and stocks).

In chapter-17 where you discuss standard Deviation and Normal Distribution you use exponential % but in chapter-18 where you discuss regarding selection of right strike you didn\’t exponential %, you use only normal % why?. Please clarify to me.

Thanks Saroj. I have posted an in-depth explanation about this in one of the above comments. Please do check that once. Thanks.

You have done a great job sir . But I have a doubt .In the last chapter we took exponential to calculate the ranges, but here I could see that they are straight away calculated in % terms.Is there anything that I missed out.

Thanks Arun. I have posted an in-depth explanation about this in one of the above comments. Please do check that once. Thanks.

Being SD a compounded return, shouldn\’t the upper range number be equal to 8462 * exp(4.215%), instead of 8462 * (1+4.215%) ?

Loris, I have posted an elaborate response to this in an earlier comment. Can you please take a look at that? Thanks.

How many days daily average returns should we see for a stock or index?

At least for 1 year, Sunny.

Sir,what all trades are meant by \”Momentum based swing trades (futures)\”.

It just means that you buy a stock or index with the intent to hold the stock for a few days.

Chapter-17,17.3

Sir,

Referring to the answer for my question asked on July 20,

Sir,if 1 can be replaced with 68%,so in case of 2SD,95% can be used,right?

But Sir ,in 2SD calculations given in Chapter-17,17.3,it isn\’t mentioned

Sir,please let me know where I went wrong?

Yes. 1 SD = 68% and 2 SD = 95%.

Sir,

\”Step 3:Calculate the stop-loss price by subtracting 4.01% (5 day volatility) from the expected entry price.\”

Here in step 3(above context),the volatility Percentage is subtracted and added from the entry price,but in previous calculations it\’s added to average,why is it so??

Two different techniques. Have posted a lengthy explanation in the comments (either in this chapter or the chapter of volatility cone). Please do check.

Sir,

Yes,in my second question,I meant 72%.

But my answer turns out to be 6110.

Sir,

How is annualized return calculated in calculation under 18.1 paragraph above,

\”Daily Average Return = 0.04%

Annualized Return = 14.8%\”

If it is obtained by multiplying 365 to the daily average return,then shouldn\’t it be 14.6%

Maybe a typo?

Sir,

But then the answer turns out to be 8462×(68%+4.215%)=8462×72.215 will be equal to a large number.Please tell where did I go wrong

Its 72% right?

Sir,

Here,to get the upper range number –

= 8462 * (1+4.215%)= 8818

Here does 1 in (1+4.225%) refers to 1 SD?

If it is so,Can 68% be used instead of 1?

Yup, it can be.

Dear Karthik sir,

Thanks so much for your reply. We are privileged to have you as Guru.

Happy learning, Sandeep 🙂

So if we can use simpler method, i.e, Current price * (1 +/-SD*Sqrt(time)) in case daily returns < 10% then this means that

in all the NIfty examples across chapters 17, 18 we could have used the simpler method for price range calculation as Nifty daily returns was < 10%. Right sir ?

Yes, thats right Sandeep.

Sir, I have gone through your comment. You\’ve said log returns as accurate & % returns as quick method.

1. You\’ve said that if the daily price movement is < 10%, we can go for % returns for quicker calculation.

By daily price movement you mean to say daily returns or Closing price – Opening price sir?

2. Can we use the log returns method by default irrespective of price movement %?

1) I mean the daily returns

2) Sure, its just that most ppl find it tedious 🙂

Dear Karthik sir

In section 18.1 Nifty example, Daily Average Return = 0.04% which is log return. So the price range calculation should be CMP*exp(Avg+-SD),

as you have told in Chapter 17. But here you have calculated the price range as CMP*(1+-Avg+-SD).

1. Why such difference in formulae when we are dealing with the same log returns?

2. Which formula you would suggest to use finally out of the two?

Sandeep, I posted a long explanation for this few days back. Please check the comments.

The premiums erode much faster during the last week of expiry favoring the option seller- Why is that sir?

Because there is lesser time to expiry.

In section 18.1, Nifty upper and lower range were calculated as spot*(1+upper range percentage) and spot*(1-lower range percentage) while in previous chapter section 17.4, Nifty upper and lower range were calculated as spot*exponential(upper range percentage) and spot*exponential(-lower range percentage). Why the difference?

I just posted this response to this y\’day, copy pasting the same –

Here are the exact steps to calculate the price range –

1) Calculate the daily log returns

2) Calculate the mean and SD

3) 68% confidence interval is – Current Price * Exp (mean*time +/- SD *Sqrt (time))

4) 95% confidence interval is – Current Price * Exp (mean*time +/- 2*SD *Sqrt (time))

The process in computationally intensive as it involves the calculation of mean, log returns, exponential etc. You can approximate it with simpler calculations –

1) For short time period (say for 1 year data), the (Mean*time) is so small that it hardly makes any difference to the final value i.e. Mean * time << SD * Sqrt (time) 2) When daily % movements 20%, then calculate using the accurate method.

using average vs spot to find range..what is the difference ?

Sorry, dint get that query, can you elaborate, please?

Sir what\’s the thing called collateral for option selling? I came across where we can put our money in FD or ETFs so that we will be earning interest and same money can be used for trading as well. I am bit confused about it. Can you briefly explain how actually it works ? From option selling perspective specifically

You can check this – https://support.zerodha.com/category/console/portfolio/pledging/articles/how-do-i-pledge-my-shares-to-get-collateral-margi

BAsically, the idea is simple, you pledge shares to get a margin and sell option basis the margins you\’ve received against the collateral.

Reward should be 417-395=22 so the

R/R ratio 22/10=2.2

Yup.

As per your experience, how much annual return a trader should expect? Surely it depends on once risk appetite and markets he is trading in but in general what % of annual return will you consider as descent return?

If you are trading full time, then the least you can expect is good FD rate * 2 times.

My current loss is taking on my head 😥 I lost my 1 month profit and more than that. In long run will it work really?

Maybe you should review the strategy step by step. If it is causing stress and not working in your favor, don\’t hesitate to pull the plug.

Thank you sir!

Also, when my shorted call option strike becomes ATM, should I exit it or should I wait hoping markets will return below 1 SD till expiry?

Recently when HDFC n HDFC Bank announced merger, Bank nifty actually broke 1 SD on same day itself but eventually it cooled off and ended below 1 SD

That really depends on your market conviction, Dhananjay 🙂

I shorted 1.5 SD bank Nifty Call option and today it became almost ATM. I exited, booked loss. More than that, I would like to know from your experience, what additional precautions I could have take while entering trade keeping in mind the current insane state of markets? As you said, one need to have his own intuition in markets but I would like to hear it from you. How you would you do that?

A basic check on how the market is positioned wrt to what you are trying to do (are you going against the trend), will help. 1.5sd is otherwise a good place to short. Maybe add 1 or 2 strikes as a buffer.

Hi Karthik Sir,

in the last chapter, we took exponential to calculate the ranges, but here I could see that they are straight away calculated in % terms.

Which one to use?

It depends, if its log returns, then you take exponential, else you can use the returns as is.

The reason we didn\’t consider average+SD while setting the stop loss as here we want limit our loss,when we consider about the Characterstics of normal distribution it gives us accuracy of 68%,95% and 99% when we add average in SD ,if we consider this while setting the stop loss the lower end would be far below the SD for call.Hence the risk reward ratio would not be favourable for us as compared to the stop loss set only with SD.

Is this justification right??

Do explain!

Thanks in advance!!

Paras, normal distribution is not about accuracy. Its about more about the odds. So when you say 68%, it means there is a 68% chance of the data falling within the range. So think about your risk and reward from this perspective.