4.1 – Two sides of the same coin

Do you remember the 1975 Bollywood super hit flick ‘Deewaar’, which attained a cult status for the incredibly famous ‘Mere paas maa hai’ dialogue ☺? The movie is about two brothers from the same mother. While one brother, righteous in life grows up to become a cop, the other brother turns out to be a notorious criminal whose views about life is diametrically opposite to his cop brother.

Well, the reason why I’m talking about this legendary movie now is that the option writer and the option buyer are somewhat comparable to these brothers. They are the two sides of the same coin. Of course, unlike the Deewaar brothers there is no view on morality when it comes to Options trading; rather the view is more on markets and what one expects out of the markets. However, there is one thing that you should remember here – whatever happens to the option seller in terms of the P&L, the exact opposite happens to option buyer and vice versa. For example if the option writer is making Rs.70/- in profits, this automatically means the option buyer is losing Rs.70/-. Here is a quick list of such generalisations –

- If the option buyer has limited risk (to the extent of premium paid), then the option seller has limited profit (again to the extent of the premium he receives)

- If the option buyer has unlimited profit potential then the option seller potentially has unlimited risk

- The breakeven point is the point at which the option buyer starts to make money, this is the exact same point at which the option writer starts to lose money

- If option buyer is making Rs.X in profit, then it implies the option seller is making a loss of Rs.X

- If the option buyer is losing Rs.X, then it implies the option seller is making Rs.X in profits

- Lastly if the option buyer is of the opinion that the market price will increase (above the strike price to be particular) then the option seller would be of the opinion that the market will stay at or below the strike price…and vice versa.

To appreciate these points further it would make sense to take a look at the Call Option from the seller’s perspective, which is the objective of this chapter.

Before we proceed, I have to warn you something about this chapter – since there is P&L symmetry between the option seller and the buyer, the discussion going forward in this chapter will look very similar to the discussion we just had in the previous chapter, hence there is a possibility that you could just skim through the chapter. Please don’t do that, I would suggest you stay alert to notice the subtle difference and the huge impact it has on the P&L of the call option writer.

4.2 – Call option seller and his thought process

Recall the ‘Ajay-Venu’ real estate example from chapter 1 – we discussed 3 possible scenarios that would take the agreement to a logical conclusion –

- The price of the land moves above Rs.500,000 (good for Ajay – option buyer)

- The price stays flat at Rs.500,000 (good for Venu – option seller)

- The price moves lower than Rs.500,000 (good for Venu – option seller)

If you notice, the option buyer has a statistical disadvantage when he buys options – only 1 possible scenario out of the three benefits the option buyer. In other words 2 out of the 3 scenarios benefit the option seller. This is just one of the incentives for the option writer to sell options. Besides this natural statistical edge, if the option seller also has a good market insight then the chances of the option seller being profitable are quite high.

Please do note, I’m only talking about a natural statistical edge here and by no way am I suggesting that an option seller will always make money.

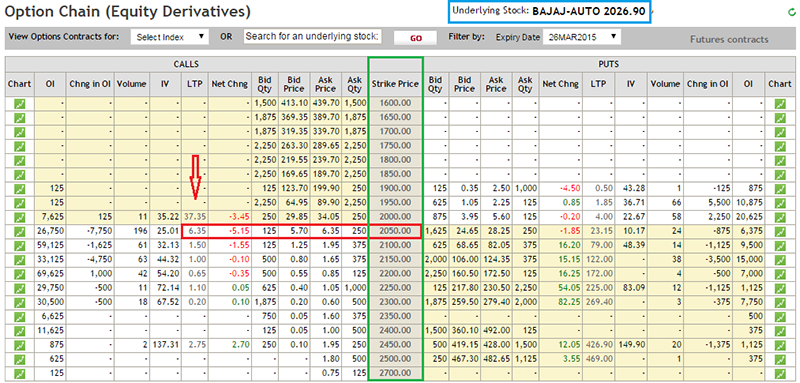

Anyway let us now take up the same ‘Bajaj Auto’ example we took up in the previous chapter and build a case for a call option seller and understand how he would view the same situation. Allow me repost the chart –

- The stock has been heavily beaten down, clearly the sentiment is extremely weak

- Since the stock has been so heavily beaten down – it implies many investors/traders in the stock would be stuck in desperate long positions

- Any increase in price in the stock will be treated as an opportunity to exit from the stuck long positions

- Given this, there is little chance that the stock price will increase in a hurry – especially in the near term

- Since the expectation is that the stock price won’t increase, selling the Bajaj Auto’s call option and collecting the premium can be perceived as a good trading opportunity

With these thoughts, the option writer decides to sell a call option. The most important point to note here is – the option seller is selling a call option because he believes that the price of Bajaj Auto will NOT increase in the near future. Therefore he believes that, selling the call option and collecting the premium is a good strategy.

As I mentioned in the previous chapter, selecting the right strike price is a very important aspect of options trading. We will talk about this in greater detail as we go forward in this module. For now, let us assume the option seller decides to sell Bajaj Auto’s 2050 strike option and collect Rs.6.35/- as premiums. Please refer to the option chain below for the details –

Let us now run through the same exercise that we ran through in the previous chapter to understand the P&L profile of the call option seller and in the process make the required generalizations. The concept of an intrinsic value of the option that we discussed in the previous chapter will hold true for this chapter as well.

| Serial No. | Possible values of spot | Premium Received | Intrinsic Value (IV) | P&L (Premium – IV) |

|---|---|---|---|---|

| 01 | 1990 | + 6.35 | 1990 – 2050 = 0 | = 6.35 – 0 = + 6.35 |

| 02 | 2000 | + 6.35 | 2000 – 2050 = 0 | = 6.35 – 0 = + 6.35 |

| 03 | 2010 | + 6.35 | 2010 – 2050 = 0 | = 6.35 – 0 = + 6.35 |

| 04 | 2020 | + 6.35 | 2020 – 2050 = 0 | = 6.35 – 0 = + 6.35 |

| 05 | 2030 | + 6.35 | 2030 – 2050 = 0 | = 6.35 – 0 = + 6.35 |

| 06 | 2040 | + 6.35 | 2040 – 2050 = 0 | = 6.35 – 0 = + 6.35 |

| 07 | 2050 | + 6.35 | 2050 – 2050 = 0 | = 6.35 – 0 = + 6.35 |

| 08 | 2060 | + 6.35 | 2060 – 2050 = 10 | = 6.35 – 10 = – 3.65 |

| 09 | 2070 | + 6.35 | 2070 – 2050 = 20 | = 6.35 – 20 = – 13.65 |

| 10 | 2080 | + 6.35 | 2080 – 2050 = 30 | = 6.35 – 30 = – 23.65 |

| 11 | 2090 | + 6.35 | 2090 – 2050 = 40 | = 6.35 – 40 = – 33.65 |

| 12 | 2100 | + 6.35 | 2100 – 2050 = 50 | = 6.35 – 50 = – 43.65 |

Before we proceed to discuss the table above, please note –

- The positive sign in the ‘premium received’ column indicates a cash inflow (credit) to the option writer

- The intrinsic value of an option (upon expiry) remains the same irrespective of call option buyer or seller

- The net P&L calculation for an option writer changes slightly, the logic goes like this

- When an option seller sells options he receives a premium (for example Rs.6.35/). He would experience a loss only after he losses the entire premium. Meaning after receiving a premium of Rs.6.35, if he loses Rs.5/- it implies he is still in profit of Rs.1.35/-. Hence for an option seller to experience a loss he has to first lose the premium he has received, any money he loses over and above the premium received, will be his real loss. Hence the P&L calculation would be ‘Premium – Intrinsic Value’

- You can extend the same argument to the option buyer. Since the option buyer pays a premium, he first needs to recover the premium he has paid, hence he would be profitable over and above the premium amount he has received, hence the P&L calculation would be ‘ Intrinsic Value – Premium’.

The table above should be familiar to you now. Let us inspect the table and make a few generalizations (do bear in mind the strike price is 2050) –

- As long as Bajaj Auto stays at or below the strike price of 2050, the option seller gets to make money – as in he gets to pocket the entire premium of Rs.6.35/-. However, do note the profit remains constant at Rs.6.35/-.

- Generalization 1 – The call option writer experiences a maximum profit to the extent of the premium received as long as the spot price remains at or below the strike price (for a call option)

- The option writer experiences a loss as and when Bajaj Auto starts to move above the strike price of 2050

- Generalization 2 – The call option writer starts to lose money as and when the spot price moves over and above the strike price. Higher the spot price moves away from the strike price, larger the loss.

- From the above 2 generalizations, it is fair to conclude that, the option seller can earn limited profits and can experience unlimited loss

We can put these generalizations in a formula to estimate the P&L of a Call option seller –

P&L = Premium – Max [0, (Spot Price – Strike Price)]

Going by the above formula, let’s evaluate the P&L for a few possible spot values on expiry –

- 2023

- 2072

- 2055

The solution is as follows –

@2023

= 6.35 – Max [0, (2023 – 2050)]

= 6.35 – Max [0, -27]

= 6.35 – 0

= 6.35

The answer is in line with Generalization 1 (profit restricted to the extent of premium received).

@2072

= 6.35 – Max [0, (2072 – 2050)]

= 6.35 – 22

= -15.56

The answer is in line with Generalization 2 (Call option writers would experience a loss as and when the spot price moves over and above the strike price)

@2055

= 6.35 – Max [0, (2055 – 2050)]

= 6.35 – Max [0, +5]

= 6.35 – 5

= 1.35

Though the spot price is higher than the strike, the call option writer still seems to be making some money here. This is against the 2nd generalization. I’m sure you would know this by now, this is because of the ‘breakeven point’ concept, which we discussed in the previous chapter.

Anyway let us inspect this a bit further and look at the P&L behavior in and around the strike price to see exactly at which point the option writer will start making a loss.

| Serial No. | Possible values of spot | Premium Received | Intrinsic Value (IV) | P&L (Premium – IV) |

|---|---|---|---|---|

| 01 | 2050 | + 6.35 | 2050 – 2050 = 0 | = 6.35 – 0 = 6.35 |

| 02 | 2051 | + 6.35 | 2051 – 2050 = 1 | = 6.35 – 1 = 5.35 |

| 03 | 2052 | + 6.35 | 2052 – 2050 = 2 | = 6.35 – 2 = 4.35 |

| 04 | 2053 | + 6.35 | 2053 – 2050 = 3 | = 6.35 – 3 = 3.35 |

| 05 | 2054 | + 6.35 | 2054 – 2050 = 4 | = 6.35 – 4 = 2.35 |

| 06 | 2055 | + 6.35 | 2055 – 2050 = 5 | = 6.35 – 5 = 1.35 |

| 07 | 2056 | + 6.35 | 2056 – 2050 = 6 | = 6.35 – 6 = 0.35 |

| 08 | 2057 | + 6.35 | 2057 – 2050 = 7 | = 6.35 – 7 = – 0.65 |

| 09 | 2058 | + 6.35 | 2058 – 2050 = 8 | = 6.35 – 8 = – 1.65 |

| 10 | 2059 | + 6.35 | 2059 – 2050 = 9 | = 6.35 – 9 = – 2.65 |

Clearly even when the spot price moves higher than the strike, the option writer still makes money, he continues to make money till the spot price increases more than strike + premium received. At this point he starts to lose money, hence calling this the ‘breakdown point’ seems appropriate.

Breakdown point for the call option seller = Strike Price + Premium Received

For the Bajaj Auto example,

= 2050 + 6.35

= 2056.35

So, the breakeven point for a call option buyer becomes the breakdown point for the call option seller.

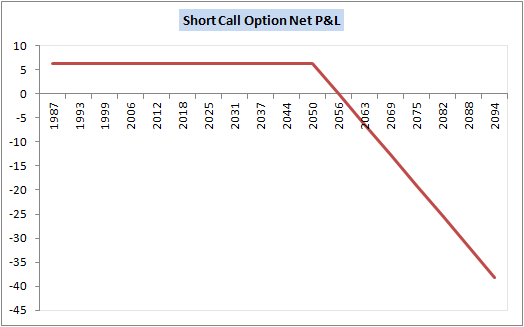

4.3 – Call Option seller pay-off

As we have seen throughout this chapter, there is a great symmetry between the call option buyer and the seller. In fact the same can be observed if we plot the P&L graph of an option seller. Here is the same –

The call option sellers P&L payoff looks like a mirror image of the call option buyer’s P&L pay off. From the chart above you can notice the following points which are in line with the discussion we have just had –

- The profit is restricted to Rs.6.35/- as long as the spot price is trading at any price below the strike of 2050

- From 2050 to 2056.35 (breakdown price) we can see the profits getting minimized

- At 2056.35 we can see that there is neither a profit nor a loss

- Above 2056.35 the call option seller starts losing money. In fact, the slope of the P&L line clearly indicates that the losses start to increase as and when the spot value moves away from the strike price

4.4 – A note on margins

Think about the risk profile of both the call option buyer and a call option seller. The call option buyer bears no risk. He just has to pay the required premium amount to the call option seller, against which he would buy the right to buy the underlying at a later point. We know his risk (maximum loss) is restricted to the premium he has already paid.

However, when you think about the risk profile of a call option seller, we know that he bears an unlimited risk. His potential loss can increase as and when the spot price moves above the strike price. Having said this, think about the stock exchange – how can they manage the risk exposure of an option seller in the backdrop of an ‘unlimited loss’ potential? What if the loss becomes so huge that the option seller decides to default?

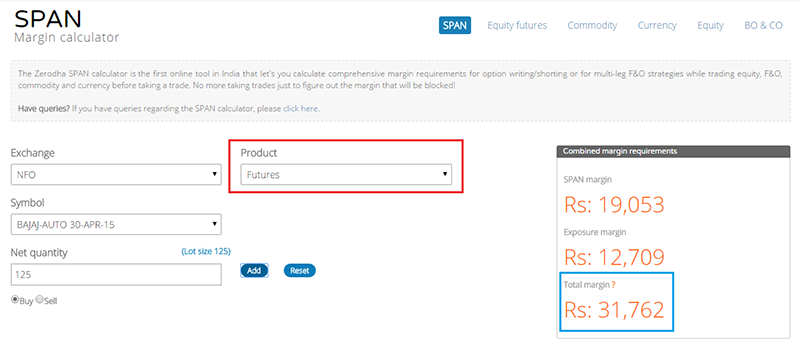

Clearly, the stock exchange cannot afford to permit a derivative participant to carry such a huge default risk, hence it is mandatory for the option seller to park some money as margins. The margins charged for an option seller is similar to the margin requirement for a futures contract.

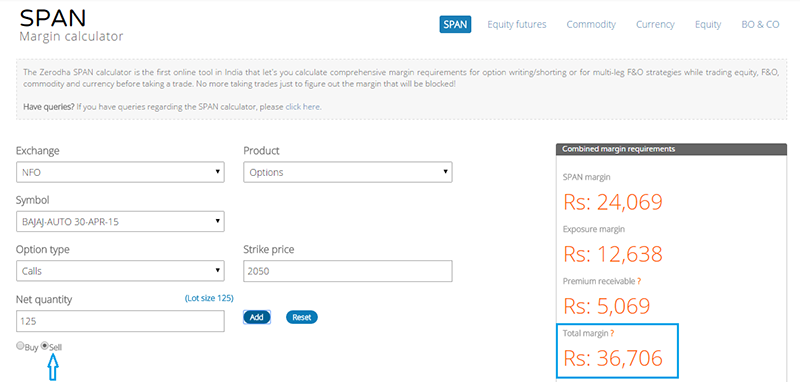

Here is the snapshot from the Zerodha Margin calculator for Bajaj Auto futures and Bajaj Auto 2050 Call option, both expiring on 30th April 2015.

And here is the margin requirement for selling 2050 call option.

As you can see the margin requirements are somewhat similar in both the cases (option writing and trading futures). Of course there is a small difference; we will deal with it at a later stage. For now, I just want you to note that option selling requires margins similar to futures trading, and the margin amount is roughly the same.

4.5 – Putting things together

I hope the last four chapters have given you all the clarity you need with respect to call options buying and selling. Unlike other topics in Finance, options are a little heavy duty. Hence I guess it makes sense to consolidate our learning at every opportunity and then proceed further. Here are the key things you should remember with respect to buying and selling call options.

With respect to option buying

- You buy a call option only when you are bullish about the underlying asset. Upon expiry the call option will be profitable only if the underlying has moved over and above the strike price

- Buying a call option is also referred to as ‘Long on a Call Option’ or simply ‘Long Call’

- To buy a call option you need to pay a premium to the option writer

- The call option buyer has limited risk (to the extent of the premium paid) and an potential to make an unlimited profit

- The breakeven point is the point at which the call option buyer neither makes money nor experiences a loss

- P&L = Max [0, (Spot Price – Strike Price)] – Premium Paid

- Breakeven point = Strike Price + Premium Paid

With respect to option selling

- You sell a call option (also called option writing) only when you believe that upon expiry, the underlying asset will not increase beyond the strike price

- Selling a call option is also called ‘Shorting a call option’ or simply ‘Short Call’

- When you sell a call option you receive the premium amount

- The profit of an option seller is restricted to the premium he receives, however his loss is potentially unlimited

- The breakdown point is the point at which the call option seller gives up all the premium he has made, which means he is neither making money nor is losing money

- Since short option position carries unlimited risk, he is required to deposit margin

- Margins in case of short options is similar to futures margin

- P&L = Premium – Max [0, (Spot Price – Strike Price)]

- Breakdown point = Strike Price + Premium Received

Other important points

- When you are bullish on a stock you can either buy the stock in spot, buy its futures, or buy a call option

- When you are bearish on a stock you can either sell the stock in the spot (although on a intraday basis), short futures, or short a call option

- The calculation of the intrinsic value for call option is standard, it does not change based on whether you are an option buyer/ seller

- However the intrinsic value calculation changes for a ‘Put’ option

- The net P&L calculation methodology is different for the call option buyer and seller.

- Throughout the last 4 chapters we have looked at the P&L keeping the expiry in perspective, this is only to help you understand the P&L behavior better

- One need not wait for the option expiry to figure out if he is going to be profitable or not

- Most of the option trading is based on the change in premiums

- For example, if I have bought Bajaj Auto 2050 call option at Rs.6.35 in the morning and by noon the same is trading at Rs.9/- I can choose to sell and book profits

- The premiums change dynamically all the time, it changes because of many variables at play, we will understand all of them as we proceed through this module

- Call option is abbreviated as ‘CE’. So Bajaj Auto 2050 Call option is also referred to as Bajaj Auto 2050CE. CE is an abbreviation for ‘European Call Option’.

4.6 – European versus American Options

Initially when option was introduced in India, there are two types of options available – European and American Options. All index options (Nifty, Bank Nifty options) were European in nature and the stock options were American in nature. The difference between the two was mainly in terms of ‘Options exercise’.

European Options – If the option type is European then it means that the option buyer will have to mandatory wait till the expiry date to exercise his right. The settlement is based on the value of spot market on expiry day. For example if he has bought a Bajaj Auto 2050 Call option, then for the buyer to be profitable Bajaj Auto has to go higher than the breakeven point on the day of the expiry. Even not it the option is worthless to the buyer and he will lose all the premium money that he paid to the Option seller.

American Options – In an American Option, the option buyer can exercise his right to buy the option whenever he deems appropriate during the tenure of the options expiry. The settlement is dependent of the spot market at that given moment and not really depended on expiry. For instance he buys Bajaj Auto 2050 Call option today when Bajaj is trading at 2030 in spot market and there are 20 more days for expiry. The next day Bajaj Auto crosses 2050. In such a case, the buyer of Baja Auto 2050 American Call option can exercise his right, which means the seller is obligated to settle with the option buyer. The expiry date has little significance here.

For people familiar with option you may have this question – ‘Since we can anyway buy an option now and sell it later, maybe in 30 minutes after we purchase, how does it matter if the option is American or European?’.

Valid question, well think about the Ajay-Venu example again. Here Ajay and Venu were to revisit the agreement in 6 months time (this is like a European Option). If instead of 6 months, imagine if Ajay had insisted that he could come anytime during the tenure of the agreement and claim his right (like an American Option). For example there could be a strong rumor about the highway project (after they signed off the agreement). In the back of the strong rumor, the land prices shoots up and hence Ajay decides exercise his right, clearly Venu will be obligated to deliver the land to Ajay (even though he is very clear that the land price has gone up because of strong rumors). Now because Venu carries addition risk of getting ‘exercised’ on any day as opposed to the day of the expiry, the premium he would need is also higher (so that he is compensated for the risk he takes).

For this reason, American options are always more expensive than European Options.

Also, you maybe interested to know that about 3 years ago NSE decided to get rid of American option completely from the derivatives segment. So all options in India are now European in nature, which means the buyer can exercise his option based on the spot price on the expiry day.

We will now proceed to understand the ‘Put Options’.

Key takeaways from this chapter

- You sell a call option when you are bearish on a stock

- The call option buyer and the seller have a symmetrically opposite P&L behaviour

- When you sell a call option you receive a premium

- Selling a call option requires you to deposit a margin

- When you sell a call option your profit is limited to the extent of the premium you receive and your loss can potentially be unlimited

- P&L = Premium – Max [0, (Spot Price – Strike Price)]

- Breakdown point = Strike Price + Premium Received

- In India, all options are European in nature

Hi, if I wish to go short on Nifty at current levels which is the best way to go about it

Futures or Put options (or sell call option), depends on your capital and risk appetite.

But this calculation is according to American options.

India follows European right?

No, its all European options in India.

If I am writing a stock call/put option for one lot and if I own the 1 lot stock with me, do i still need to provide margin, can I not provide my individual stock holding itself as a margin for that 1 lot

Yes, you need to.

You can extend the same argument to the option buyer. Since the option buyer pays a premium, he first needs to recover the premium he has paid, hence he would be profitable over and above the premium amount he has received, hence the P&L calculation would be ‘ Intrinsic Value – Premium’.

in the above paragraph, should it be \”….profitable over and above the premium amount he has PAID (not received)…..\”

thanks

Ah yes, thats right. Please ignore the typo.

could you tell me the difference between selling a call option vs exercising the option on expiry

Check this Denver – https://youtu.be/Llp4xW2GI4s?si=Mmo0EUyx881kmQF1

Sir,

You said that you cannot exercise option until its expiry but can square off it any time.

I am familiar with the \”squaring off\” for any position but what Exercising an option really mean I Didn\’t get it.

Please explain it.

Saurabh, check this – https://youtu.be/Llp4xW2GI4s?si=6XaVDUqD0Lj4ZaSm

Dear Karthik

Question:

If i buy a call on day one say of bank…SBi at 855 as market was going up….however on second day it start went going down below strike price due to china effect tremendously…..so do i have to wait for expiry day as total loss will be premium paid only….or sell it at say 770 and still loss will be premium paid only

You can exit it at any point, Priya. No need to wait till expiry.

As told by you in India we follow European options i.e exit only on spot price on tge expiry day and here in comment u said dnt wait for expiry…… bit confused please explain

Dont wait for expiry if you want to close the position. There is a difference between booking P&L and actually closing the session. YOu can check this – https://youtu.be/Llp4xW2GI4s?si=YMODrTZFau9MCl1x

Sir tell me the premium that we pay during contract if the price go according set strike price that premium we\’ll get back or not.

You can, provided you decide to close your postion.

Who is the owner of the land or the flat?from whom he purchased it?

Not sure. But that is besides the point right?

Hi Karthik. Thank you for the amazing course. Learned a lot.

Today (26Sep24), I sold a Nifty call 26200 (expiring today) early in the day and observed that towards the close of day like at about 10:59 when Nifty spot was around 26185, the 26200 call was still at 16. Since the call was expiring in about 1 minute, I thought the 26200 call should be much less than 16 based on how Call Options have behaved in the past near to expiry.

Check this Jim, this should help – https://www.youtube.com/watch?v=eJiouVUWEb0&list=PLX2SHiKfualEyD05J9JsklEq1JFGbG6qJ&index=15

I bought a weekly call spread. How can I unwind before expiry ?

You simply square off the positions and ensure all positions are closed. Thats it 🙂

If Nifty spot price is 25000 and I sell one lot Nifty 24800 put option with Margin money of 75000 , and the next day there is a gap down of 2500 points and Nifty opens at 22500, and I have no spare margin money in my trading account, what will be my loss? Will my position be automatically squared off by NSE and will my loss be limited to ₹62500, even if Nifty further falls to 20000?

Thats right, but NSE wont square off, but the broker will.

Good evening Karthik Sir,

My question is related to covered calls.

My question may seem to you like very basic or idiotic and I\’m sorry for that.

Hope you\’ll appreciate all Q\’s however silly they may be.

In Options related book written by Mahesh Chander Kaushik [SEBI registered & also he has written few more books (https://www.blogger.com/profile/01822348572318400909) , he also has a youtube channel ]

As per Mahesh Sir when I already have units worth one lot of say NIFTY selling option calls or selling puts is very safe or in others words it is loss proof.

He says by selling option calls of around 5% more than current NIFTY value we\’ll get premium as mostly NIFTY will not cross more than 5% by expiry.

Say NIFTY goes beyond 5% then we loose premium as NIFTY crossed the strike price we chose while selling the calls.

As per Mahesh Sir though I lost premium and I\’m in loss but as NIFTY number increased the value of my one lot worth of units of NIFTY also increased so I\’m kind of not in loss.

Is this kind of covered option selling really very safe? No losses at all?

If it was so safe then everyone would have bought one lot worth of NIFTY units and keep selling option calls…

Karthik Sir, what is your view on this scenario?

Thanks & Regards,

Santosh

I guess I answered this for you already 🙂

Hi, if I wish to go short on Nifty at current levels which is the best way to go about it

Future or buy puts, or sell calls.

When I can square off my position before expiry why are you calling it European

You can square off your position anytime you wish, but settlement against physical delivery is only on the day of expiry. Do check this – https://www.youtube.com/watch?v=Llp4xW2GI4s&list=PLX2SHiKfualFiusiT9G5uE9jU3vetvW2x&index=12

Hi,

Can I buy back a sold call option the very next day?

Suppose I have SBI 750 CE and I have sold the same. Now the share price is at 740, however the next day the price has increased to 747.

I do not want to wait for it to come in the money and want to buyback this option at the earliest with the little profit that I have made.

Can this be done?

Thanks!

Yes, you can do that and there is no need to wait till expiry.

can any one square off the call option sell position anytime before expiry or the option writer have to wait till the expiry because it had taken the premium of the call??Plz,answer.

Yes, you can square off the position anytime you wish, no need to wait till expiry.

Hi sir, Who actually write/sell the call option. Can a retail trader write a call/put option?

Sir,

When engaging in valid serious option trading, Is it essential to hedge our positions all the time 100% due to the uncertainties in the market. Given that anything can happen at any time, is hedging mandatory for those looking to make a living through option trading? Additionally, in options simulators like the one in Sensibull, does the maximum loss displayed represent the absolute limit, meaning any unforeseen events will not result in a loss exceeding that amount?

Having a hedged position/spread is always good. It is capital protection, but also comes with limited profit potential. Yes, max loss represents all known risks.

Hello, I want to ask whether we can use stocks in demat as margin. I got 3875 stocks of PFC. I want to sell otm calls and generate revenue. Do I still need the margin?

And does margin requirements change when stock reaches or goes above the strike I have choosen. Can I block my shares instead of cash?

Yes, you\’d still need margins for this Vishesh.

Hello sir,

I really appreciate your effort of offering quality content on F&O. Sir I have one confusion and I would be grateful if you solve it.

I have heard many people on youtube and read in many online articles on derivative trading that when we sell our bought call option or buy back our sold position, may be because of reasons such as stop loss hit or exiting the position, price of the underlying goes up or goes down accordingly. Don\’t you think these statements are wrong since F&O are derivative instruments and derive their value from underlying security. If this is true then don\’t you think we should say that we sell our bought call when price of the underlying moves up (hit target) or down (hit stop loss) rather than saying that selling or buying options incline or decline the price of underlying.

Do you think selling or buying options in themselves push the underlying value of security or index up or down. Or up and down movement of underlying make us exit or enter option positions.

correct me if I am wrong.

Thanks in advance.

This happens once in a way when there is excess short or long positions built up. Think about this – markets are rallying, traders have built up long positions. One fine day markets starts showing weakness, and everyone starts to sell to book profits. When too many traders sell at once, the price tends to fall. This is called long unwinding/profit booking or in case of shorts, its called short covering.

Isn\’t it an complicated and advanced form of gambling

Not really, trades can be setup by design, and anything by design is not gambling. Which is what we are trying to explore in Varsity, happy reading 🙂

Hi, was looking to understand who issues options in India?

All the blogs and articles that I have come across talk about option trading meaning there’s already an option contract in the market. But who is the option issuer? Who issues the contract for the very first time

The exchanges spawn options as and when old contracts expire and new ge issued.

Hi karthik, whats the difference between settlement of option (say call) and selling a call option

Have explained in detail in the options module itself 🙂

Why margin is required, if an option seller holds share in demat account?

There is no guarantee that you will continue to hold shares as long as have the option position open right?

Hi Karthik,

If I sell a Call Option let say at the rate of 284 (1 lot) on October 30, 2023 and square off my position on October 31, 2023 at the rate of 400 (1 lot) what will be my actual loss (will it only be the price difference or anything else).

Thats right, your P&L will be the difference between the buy and sell premium.

Hello Sir, Please Reply.

My Question Is , what Happens When Sell A call Option Of current week Expiry And at the same time, buy Call Option of Same STRIKE PRICE of Next Month Expiry.

There Will Be difference in the time decay.

But Will I Be Able To Capture this difference when Market Moves Beyond my Range?

No, that is becuase the premiums are not just a function of time, but also volatility. Even if you capture the time premium, you wont be able to get the volatility premium.

Hi kartik from this I have understood that option buyer can exercise it\’s position only on the day of expiry . But a option seller can exercise it\’s position before expiry , intraday . whether it\’s correct or not please correct me if I were wrong.

Both the buyer and seller can initiate and close positions anytime they want, but can exercise their respective rights only on the day of expiry.

Hi Karthik,

I have very dumb question and need your help to understand the Theta decay in overnight position.

Assume I sell Call option and Put option just before the close of the market.

in Bank Nifty

Both sold 1 Lot

Call sold at 300 Rs

Put sold at 300 Rs

Next day morning before 9:15 AM :

Call price would show 300 and Put price would show 305(After NSE average adjustment) and Booked P&L would be showing as -5 Rs.

Now My question is being Option seller is this amount credited to Demat account overnight or I have to start my trade with -5rs P&L ?

Unlike in futures trading, there is no M2M here. YOu will realise the loss only upon square off of the position.

Hi Karthik ,

I am planning to short sell Tata motors at 670 CE and 570 PE ( Short strangle ) and get a premium of about 8000

If At the date of expiry tata motors is trading at 630

My question is should I square off both the 670 CE and 570 PE before expiry inorder to avoid physical delivery or since these two options are OTM will they expire worthless?

Is short selling stock option risky than index option ?

Can you also the explain the rule for physical delivery of stock option while option selling 🙂

physical delivery of stock option is only for ITM and ATM or does it also include OTM stock options ?

if both options are worthless upon expiry, then you can let it be. No need to square off. Yes, single options is way more risky than index. Physical delivery is only for ITM options and not OTM or ATM. The last chapter in this module explains that.

Hi ..

Thanks for information ..

Question is if index moves above our strike price and premium and starts making loss … Can we close option SELLING…?

Yes, you can Arun.

if my view is bearish and i want to short then what will be the process? can I first buy a CE that sell CE? or first sell CE that buy CE for hedge.

You can sell a call or buy a put option, Satish.

Hi,

If I have the underlying and write options, do I need to pay margin ?

Yes, margins are compulsory.

Hi Kartik

My query is regarding Nfty50 weekly option.

On the expiry date Nifty 50 ATM-19650, OTM-19700, OTM – 19750. OTM – 19750 premium was Rs.11.40 at 12.10 AM. Nifty 50 trend was clearly downward. If I sale OTM – 19750 for Rs.11.40 and exit at Rs.2.00 with stoploss at 16.50, then is this deal will be safe and profitable.

No one can answer that for you, Kishor. No guarantee in the market 🙂

I sold Call options. On the date of expiry, the scrip was lower than the Strike price, so the premium value during closing was 0.10.

Do I still need to square off? Or Squaring off is not required, as the Call option cannot be exercised eitherways.

No need, since the option is worthless at the time of expiry, no need to square off the position.

Hi Karthik,

Can you please explain how profits will differ in case of squaring off vs exercising in futures . As in options they differ by premium

Sumit, I\’d suggest you check this – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

kartik sir, there are only European options available in Indian market still, I buy and sell at any time before expiry happens, just like American. European and American smees the same to me, so can you please clarify how they are different.

The difference is in settlement of options 🙂

Hi kartik,

I followed a strategy shown on tv,in which I bought 1 CE of LT at strike price 2400 at 20.60 and sold 2 CE of LT strike price 2440 at 7.70. now this was bought on Friday.

If I hold this till expiry then in this case how the profits will be calculated,kindly advise as what should be done in such a case.

Thank u

NikhilB

Nikhil, you can actually put feed the values in Sensibull and get the exact values.

There is a calculation error when calculating P&L for a spot price of 2072.

The calculation 6.35-22 should give -15.65 and not -15.56.

Thanks for sharing, checking this.

so selling a call option which will expire worthless, so i need not buy that option, right? i mean there will be no penalty for this? and i will not be in any contract??

so can i sell an option lets say at 0.05 and expect returns generated from this? i mean that option is like 10000 shares a lot, so i will generate a profit with no cost incurred?? is this understanding right?

So the option itself expires worthless, so there is no need to buy a worthless option 🙂

I sold a let\’s say 100CE call option at 2 rs. but at the day of expiry the stock price is 90, but i\’m not able to buy the option because no one is there to sell 100CE option. So, it will remain an open position for me. what will happen in this case?

i\’m talking about stock option, not index options.

Since its an OTM option, it will expire worthless.

Can option selling is possible without margins by holding stock in required lots

No, thats not possible 🙂

Margin required for Selling options = Margin for Future – premium amount.

BUT WHEN WE PLACE AN ORDER IN ZERODHA, THE SYSTEM ASKS MARGIN FOR FUTURE + PREMIUM AMOUNT.

Though it get reduced after activation of the order. I request ZERODHA to make necessary changes in the system to state the correct required margin at the time of placing orders. @ Karthik Rangappa

Ashok, you will see the margins and charges on the order window page when placing an order.

Sir,

Like in futures we get the full benefit even in cash settlement if not prolonged to expiry. However, in options does it only mean physical settlement upon exercising and no privileges of cash settlement?

Yes, but if held to expiry, all stock options are cash settled.

Sir,

Like in futures, we understood that it is better to get out of deal before the expiry to avoid physical settlement. In options, the exercise can be done only at the expiry date.

(i)I would like to know whether this exercise has to be done from the trader end or the exchange will do on its own?

(ii)If the exchange does, will it also cost for physical settlement?

(iii)If the trader can also exercise on the day of expiry, can it be any timing on the day on or before 3:20 pm?

1) Exchange and broker takes care of this. You don\’t have to do anything.

2) Yes

3) No, only post-market closes.

Sir,

I asked you the above query, however, could you please check if the below is correctly mentioned or am I missing something here:

(i) From a buy call option perspective, if I square off the option before expiry date, then P&L will be based on premium only. And when someone square off his buy position on the expiry date, his P&L will be based on Max [0, (Spot Price – Strike Price)] – Premium Paid.

However, to enjoy the P&L \”Max [0, (Spot Price – Strike Price)] – Premium Paid\”, does the exchange need to square off the position or I can myself close the position on the expiration day anytime and enjoy P&L \”Max [0, (Spot Price – Strike Price)] – Premium Paid\”.

If you hold the position o expiry, then the position will be deemed closed and settlement will happen. Do check the link i shared earlier.

Sir,

For my above query as below:

(i) At one place you mentioned that “For example, if I have bought Bajaj Auto 2050 call option at Rs.6.35 in the morning and by noon the same is trading at Rs.9/- I can choose to sell and book profits”

Does that mean one can square off before expiry too in European market. Please help to understand here.

However, at several instances in your discussion, it was understood that positions in call options can only be squared off at the expiry day.

Please help to understand this subtle difference. I am totally confused.

Check this, Anirban – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

Sir,

As understood that all options are now European in nature and the buyer could only exercise his right on the expiry day at the closing. Now I have a query here below:

(i) At one place you mentioned that \”For example, if I have bought Bajaj Auto 2050 call option at Rs.6.35 in the morning and by noon the same is trading at Rs.9/- I can choose to sell and book profits\”

Does that mean one can square off before expiry too in European market. Please help to understand here.

(ii) Unlike NSE restriction, are American options there in BSE trade?

1) Yes thats right.

2) All options are European in nature.

Hi,

In the US market when you have 100 share i.e one lot of a share. if I go for covered call they will be take if the stock exceed the price.

Similar manner if I have a sample infy 400 stock if I want to do a covered call, just go and do a call sell. Please explain what happens at the end of the expiry, if the price crosses the covered call price. Whether the broker will take the existing stock automatically or do I need to pledge before trading.

if so how to do that.

Thanks

K.Udayakumar

So if you sell a call, and the call goes in the money, then you are liable to give delivery of shares. If you have the required shares in DEMAT, then your shares will be debited from the demat account (physical delivery) i.e. assuming you don\’t have any other positions to offset the short ITM call position.

Hi Karthik,

I want to know about the time decay benefits, like if I sell the options at a price like 15 on expiry morning.

Now as per my knowledge as time pass and expiry is about to close, and premium reduces.

and I am selling the position around 3 PM, am I into profit as a result of time decay or lose?

Thanks

Your profit or loss depends on the change in premium, Onkar. For you to be profitable, the premium has to reduce from 15. The lower the premium goes, the higher your P&L.

karthik sir , Thank you sir! . I love your module, your course available for purchase in advance level.

Thanks for the kind words, Amit. No, we don\’t have any paid course.

Hi sir..

I entered into short strangle on Monday and find the spot price is within range on Tuesday .I find the total premium paid by me as unsettled credit in my funds position .Suppose I squared off on Tuesday after noon …how much credit can I get..

Ex: I paid premium of Rs.3203 on Monday and squared off on Tuesday when my profit is 1460.In this case how much profit can I receive after square off. Pl clarify

Regards

Since this is EQ, you will receive the entire premium/profit on the same day, Shiba. Of course, you can withdraw it only on T+1 basis.

Hi,

I am a call writer (suppose). I actually want to be because I have some free cash of 20/25L. Just tell me these few things dear.

a) I Sell Company X 500CE strike at a premium of 5 for 1000 shares on 15th March for expiry of 30th March. The CMP of Co X is 450.

b) Then my immediate income is 5000 rupees as the max premium. Right ? First question – When does this 5000 get credited to my account ?

c) Second question – During the period till expiry, does any change in the premium price from 5 (to either higher or lower) change anything in my income of 5000?

d) On the expiry, the market price of Co X remains below 500 and therefore obviously I earn all my premium. Correct ? Tell me within the 15 days till expiry if any change in the premium price would in any way change my income of premium even if the CMP of X stays below 500?

Yes, that\’s right. You get 5000, which is credited immediately to your account. You will lose if the premiums increase beyond five and go higher. You will get to retain the entire premium as long as the spot remains below the strike price.

Hi Karthik,

Please can you correct me if i am wrong.

I go for a call option and suppose the strike price is – 150, Premium – 10 as on 10th April

Expiry date – 20th May

scenario 1

date – 19th April, Spot Price – 150 and premium is 30

We can book profit on premium (20 x total number of shares) but we can execute the option on the expiry date. (without paying double brokerage)

scenario 2

date – 24th April

Spot price – 170, Premium – 30

We can book profit = {(170-50) + (30-10)} x total number of shares – how about the brokerage in this situation?

Scenario 3

Date – 20th May

Spot Price – 200

Profit – 200-150= 50

50-10 (premium) x total no of shares

Thanks in advance!

1) No, such a thing is not possible

2) Rs.20 per executed trade

3) NOt sure what the question is for scenario 3 🙂

Can we sell a option with 17 days to expiry (eg. current date 18-02-2023 I want to sell 09-03-2023)??

Yes, you can do that Sourab.

Thank you very much for your reply.

As you said \”The contract is between the latest buyer and seller.\”

Does not it mean, in this case, that I would be the latest seller of contract ?

Since I am a new comer to the world of options, your elaborated answer will enhance my understanding in this regard. Which will be very grateful of you. Thanks once again.

But your sell offsets the initial buy, right? Every two trades done in the opposite direction and same quantity offsets your position. For example, buy 100 shares of Infy, sell 100 shares of Infy means you are out of the market. Likewise, buy 10 lots of Infy call options and sell 10 lots of Infy call options (both belonging to same strike), means you are out of the market and your positions are squared off.

Hi,

I do have little confusion regarding call option which is described as below.

Suppose I bought a stock call option at premium of 5INR in carry forward mode from some seller in the market. Then to book profit from the option trading, I have sold that call option contract at premium of 10INR to another buyer. Now, this buyer of that call option does not sell it further and kept it till the expiry date. At that expiry date, if he wants to exercise that call option, then who is liable to make delivery of underlying stock to that last holder of the call option ? Is it me in this case or the original/first writer/seller of the call option contract ?

Its not you since you have sold the option and are out of the market. The contract is between the latest buyer and seller.

When and how an option buyer will execute the option contract.?

Please check the video series that I shared in the previous comment.

Please make a video/explanation on when an option buyer will execute the options contract. When an option seller has to obay the contract? Does the option seller has to obey though he has squared off..?? Any possibility of short delivery in option selling when sold an option in normal/delivery mode.

Please make explain the intricasies of this executing an option contract.

Naresh, can you check this – https://www.youtube.com/watch?v=-mO0YOTcCiQ&list=PLX2SHiKfualFiusiT9G5uE9jU3vetvW2x

Hi

I Bought a stock at 2000 of 1 lot of shares i.e 300 and write a call option for current month at 2200 CE @ 50 Rs and end of the month the spot is at 2300 i am ready to give delivery @2200 but now my question is wat is my profit

i.e 50+200(2000-2200) =250

am i right or wrong please inform me

thanks in advance please.

So you will deliver at 2200, while the market price is 2300. So you lose 100 here.

But the strike price I chose was otm at expiry . Why physical settlement? kindly tell me.

What will be my p&l?

There is no physical settlement for options that expire OTM. It is only for options that have an intrinsic value upon expiry.

But the strike price I chose was otm at expiry . Why physical settlement? kindly tell me

Sorry, if the option is OTM upon expiry, then it will be worthless and hence no settlement required.

sell strike price 380 call @6.1 (quantity: 1100)

Spot price 365 at expiry .

What happened if I don\’t exit my position or there have no buyers and what will be my p&l ?

The option will be physically settled upon expiry, Shankar.

call sell otm @6.10 strike 380.

At the expiry day strike price 350.

On expiry day What will happen if I don\’t exit my position ? And what will happen if there have no buyers for exit my sell position?

Upon expiry, the option will be physically settled by the broker.

Hi Karthik,

If suppose i have sold long term options like say 1month to expiry. A black swan event occurs and by chance i am out of town basically not responding to short margin calls.

When and How does zerodha square off my options? Like what is the procedure followed. And if i have less margin am i liable to pay anything extra other than blocked funds if zerodha was unable to square off(very low probability) at right time before all my blocked funds are utilised?

The company will try to reach you/communicate with you to inform you about the short margin and that you need to fund your account to topup the short margin. In case there is no response, the company will square off the position on your behalf.

Hello sir, just wanna thanks for this amazing super easy to understand content

Just asking out of curiosity, do you still trade in option..?😊

Hi Saurabh, thanks for the kind words. We are restricted to trade, it is a company policy. So no, I don\’t trade options now 🙂

1 Point I didn\’t understand that: How the settlement will be done in case of IV …if the spot price > strike price. Because anyway seller has to pay the difference between Sport Price and Strike price then how IV play role here (Because IV for that particular strike price is High R8)

Example: Current price of XYZ share is 2050/- & I opt buy option of Strike price of 2070/- at price of 6 Rs. for Qty. 125.

Total Paid Premium = 125 * 6 = 750

now my breakeven point is 2070+6= which is 2076.

Now I\’m considering that stock closing at 2080 then according to last chapter I\’m in profit of (Spot Price – Strike Price)

(2080 – 2070 = 10) where I\’m in profit of 10*125 = 1250 Rs. in which if I deduct paid premium 1250-750 = 500 is Net Profit.

But at the same time IV of 2070 is 10 – 6(paid premium) = 4.

Now how the settlement will work here will I get 500 which is net profit or my IV 4 * 125 = 500.

OR Both are same?

Ashish, please do check this – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

hey karthik

what is more profitable -trading premium before expiry or trading option(exercising right) at expiry

can you clarify with a real stock data example

It purely depends on the market condition. But if you\’ve sold options, you can retain the entire premium only upon expiry, provided the option is OTM. But this does not necessarily mean you have to wait till expiry. Its a call you have to take based on how the market is moving.

In case of equity you have only 2 possible trqnsactions

Buy Equity

Sell Equity

But in option you have

Buy call option

Sell call option

Buy put option

Sell put option

Can you compare each of the above with example

I\’ve explained that in this module and this video series – https://www.youtube.com/watch?v=-mO0YOTcCiQ&list=PLX2SHiKfualFiusiT9G5uE9jU3vetvW2x

Got it. Thanks a lot for your help! 🙂

Sure, happy learning 🙂

Hi Karthik,

Thanks a lot for explaining the concept. I still have one more doubt. So, in case I am seeing the price being OTM near end of the month, should I need to square off at the last Thursday or keep it as it is still the last Thursday of month to get the keep all the entire premium of 17.85.

If its, OTM and the option has no value, you can let it be. Consider squaring off if its ITM.

Hi Karthik,

Thank you for the amazing sessions!!

I have a silly doubt. For example – If an I have sold a call option and underlaying values for that call option is

Spot price – Rs. 816

Strike price – Rs.820

Premium – 17.85

lot size -500

In this scenario, will my profit be

P&L = Premium – Max [0, (Spot Price – Strike Price)]

=17.85 – Max[0,(816-820)]

=17.85

=500(lot size)*17.85 = Rs. 8925

So, will i get profit of Rs. 8925 or say at the time of square off , premium is say 13. so, 8925 -(500*13) = 8925-6500= Rs.2425?

So , for option seller will profit be always difference between margins?

Thanks again for your help!

Thats right. You get to keep the entire premium of 17.85, if the option expires OTM. Always take the difference between the premiums to figure the P&L.

Please clarify what happens if I buy a call option and do not sell it on expiry day? Do I have to bear any penalties and what are the charges?

No penalties, but upon expiry, the option will be physically settled.

How does open interest (OI) decrease before expiry?

That\’s because the market participants are interested in closing down their existing positions and not really interested in starting new ones.

So, in both option buying and option selling ,stop loss should be with -ve sign. Am I correct in getting it sir?

Here are two examples.

1) I enter a long trade at 100, with a stop loss of 5 points. So my SL is 95 here.

2) I enter a short trade at 100, with a stop loss of 6 points. So my SL is 106.

The point is that the SL is a number which you subtract from your entry price when you are long and deduct from your entry price when you are short.

Thanks a lot sir for prompt response.but should I be putting -ve sign while putting stoploss or it should be + sign . As I generally put – ve sign in stoploss while buying option . While selling should it be +ve ?

No, think about it as a percentage. YOu bought at 100, you have a 5% SL tolerance…so you get out at 95. Dont think about it from +ve and -ve numbers perspective.

Can u please guide me in detail how to put stoploss while selling call against the shares in my demat account when am doing covered call ? I mean ,it’s in percentage while putting stoploss. 1)How to calculate stoploss in percentage? 2) should we be removing -ve sign while putting stoploss while selling calls? Please guide in detail. Regards -VIKRAM MARDHEKAR

Here is an example – assume you have 1000 shares of Infy and you intend to sell Infy call option. The price of the option is say 20.

In a pure-covered call, you don\’t really put a SL. The idea is if the call goes against you, you deliver shares. But if you do intend to put an SL, say 10%, then you wait for a decline in your call option by 10%. So at Rs.18, you exit the position. Rs.2 = 10% of 20.

Replies are excellent.

My query

Suppose I sell 50 nifty put option today, say at prrmium 10, then without waiting for the expiry date, I square up on the same day at premium of 20.

How much I pay for initial transaction.

How much I get when I square up

Regards.

50 is 2 lots.

Strike price is immaterial.

The P&L is the difference between the buy price and the sell price of the premium.

Hi sir one more query

Different between excercise the right and trading the premium

Have discussed this here in the video series, do check that – https://www.youtube.com/watch?v=-mO0YOTcCiQ&list=PLX2SHiKfualFiusiT9G5uE9jU3vetvW2x

Hi kartik sir

Will I have to pay margin or premium while buying a call option

Please reply

You will have to the premium i.e. lot size * premium.

Hi

I want to use sensibull whats app alerts.

I am outside india, so I can\’t use my Indian whatsapp number to receive the alerts.

Is there any way out? Maybe email alerts?

I\’m not sure if they have anything related to this. But I\’d suggest you check with them once.

Hi

Is there any data source to get high low close price of options at any strike price we want?

YOu can check Sensibull for this.

So if I sold the 100 CE as in the previous example, and the spot price is 110.

Intrinsic Value of a Call option = Spot Price – Strike Price

=110-100 = 10 Rs, for a lot size of 50 loss comes to 10*50=500 Rs?

Yes, thats right.

Hi

I just saw your statement \”Illiquid options are all settled by the exchange upon expiry. The P&L will be calculated per the option’s intrinsic value upon expiry.\”

Can you please explain this with an example?

So lets say you buy a 100 CE. After you buy the option turns illiquid and you are unable to square off. Now, upon expiry assume the spot is at 110. The 100 strike will be settled keeping the intrinsic price as 110.

Hi

If an option seller sells an ITM option and it becomes illiquid on expiry day, what happens to the seller?

Can we sell options on weekly NIFTY in zerodha?

The illiquid option, upon expiry will be settled by the exchange. Yes, you can.

I wont be squaring off. 650 LTP was the last price on Thursday for that option. Friday new series began.

I guess I can get 650 because it is automatically squared off.

What happens to the illiquid put option? How is that settled? What will be my profit /loss as I sold it initially for 1000 Rs.

Illiquid options are all settled by the exchange upon expiry. The P&L will be calculated per the option\’s intrinsic value upon expiry.

Hi

I am doing some paper trading selling options for weekly expiry. I sold a call option at 1000 Rs LTP. On expiry day the LTP was 650. So the profit/loss for this is 1000-650=350 Rs correct?

Similarly I sold a put option for 1000 Rs, but on expiry day the LTP is showing blank. So what happens to this option?

Yes, provided you squared off at 650. Most likely there are no trades and the option is illiquid.

Hi

Is it possible to set stop loss limit orders for option selling?

Yes, you can.

Good evening Karthik,

Last time i made a strategy on sensibull consisting of nifty futures & options, it was showing 700 rupees profit at any direction. I executed the trade & ended up with 2100 rupees loss. Why do sensibull showed such inaccurate data ? I want to test other similar strategies but it would be of no use on sensibull, as it is showing completely wrong payoffs

Hemant, its mostly some error in the inputs. I\’d suggest you check with Sensibull for this.

Can Option writer make stop loss? How?

Yes, they can. Its the same way as you\’d place a SL for a short futures position.

How much money need to sell a out of the money call option

You can check the margins on Kite itself.

Yes but backtesting results say that I will be winning most of the time small and loosing large for few times. But lossses in loosing trades will be always higher than I gain in profitable trades.

This is generic feature of option selling but how do I manage losses in case market move against me so that at end of year(s) I will be in net positive position?

In my previous comment I have posted backtesting results and respective calculations.

One way (as mentioned in my previous comment) is to buy OTM options. These losses usually occur because of a rapid move, so a hedge may help you cut these losses.

I am selling 1 SD away call option and if I buy slightly OTM call then I will have to pay more than I get. Essentially I am getting in *net pay* position than *net get*

You are selling a lower strike than the higher price, so you should technically receive more than what you pay.

This is going to be long comment. Please clarify my issue

Used historical data is from 2012 to August 2022 and I have assumed all weekly expiries here. Data is calculated using Pandas library. Below is the table of how many times 1 SD away call side was broken and how many times 1 SD away put side was broken in that particular year and last column has total number of expiries in that year for Bank Nifty options.

Year Call side Put side Expiries

2012 5 3 50

2013 8 13 52

2014 1 6 52

2015 2 13 53

2016 9 10 52

2017 7 5 52

2018 10 8 52

2019 7 11 52

2020 9 6 53

2021 3 2 52

2022 5 5 34

Now we have bank nifty strikes with difference of 100 points (25000, 25100, 25200 and so on). Let\’s say I am option seller so I will calculate 1 SD and will sell strike (call side) above 1 SD. To hedge my position, I will buy it\’s immediate next strike. Why immediate next? because this is what I can do to limit my loss at 2500 Rs (Bank Nifty lot size of 25 so 100 point difference in strikes will result in not more than 2500 Rs loss in case market goes against me). Buying any other strike for hedging will give me loss in multiple of 2500 (5000 for 2 strikes away, 7500 for 3 strikes away and so on).

So here I selling let say 36000 CE and buying it\’s immediate next 36100 CE. This is my hedged position. Now as I am buying immediate next strike, I will not be able to even gain 10 points. Even then let\’s assume I can gain 10 points and lot of 25 will result in 250 Rs profit per lot for me when market stays below my sold strike. and this position will result in max loss of 2500 Rs if gone wrong. Now below is table of how much profit and loss I could have made if I follow same set of execution from 2012 till date for 1 lot of bank nifty.

Year Profit Loss Net

2012 11250 12500 -1250

2013 11000 20000 -9000

2014 12750 2500 10250

2015 12750 5000 7750

2016 10750 22500 -11750

2017 11250 17500 -6250

2018 10500 25000 -14500

2019 11250 17500 -6250

2020 11000 22500 -11500

2021 12250 7500 4750

2022 7250 12500 -5250

Here I am assuming, I will be adding fresh capital required to trade 1 lot if my current capital in account is less than required to trade 1 lot. If I sum the the Net column I get -43000 which clearly a loss (I have not even yet considered brokerages and other charges). These are results for 1 lot and with higher capital loss will amplify only!

Now here are some points I have noted:

– Clearly we can see that winning rate of this strategy in incredibly higher (we are loosing hardly 10 out of 50 expiries)

– But, loosing trades (which are very less in count) are resulting in heavy losses which in turn take out all profits and sometimes more than that

Possible ways I may be doing it wrong:

– I am hedging it in completely wrong way

– I may be using wrong strategy (selling 1 SD away call and buying immediate next one) for this kind of system (system with higher winning rate but I am loosing at end. Means I am not using system in proper way.)

– Am I choosing wrong combinations of strikes?

and at end, how do I tackle with this?

This is a known behavior of these strategies. In most cases it results in a profit, but when it goes out of wack, the losses can be high…high enough to wipe out the gains made over several expires. One reason why this happens is because of the sharp movement in prices around expiry…and one of the ways to tackle this is by buying slightly OTM options a hedge. Slightly OTM is cheaper as well and increases the overall profitability. Do give this a try.

When I sell a call option, I buy it\’s immediate next strike for hedging. So my max loss will be not more than 25*100 (assuming I am trading on bank nifty). Even in this case When I go for 1 SD levels and play around, lets say market breaches 1 sd level for 10 times out of 50 (total expiries in year, weekly) then I will be in loss at end of year.

I hardly get 13-15 points after Hedging and I am risking at 100 points for this. So for 40 times I will earn 15*25*40= 15000 rs and in only 10 loosing trades, I will loose 10*2500 = 25000 rs.

How can I tackle with this? And I suppose market can actually break 1 sd level for 10 times in market

This is a bull call spread essentially. I\’d suggest you check the chapter on that for more insights 🙂

I checked that comment. Here\’s what I understood

– log returns are easier to calculate than actual traditional method so it makes sense to use log returns as they are not much different from actual returns calculated using traditional formula

– If I am developing a system then I can go for simple returns (calculated using traditional formula)

So I am using Pandas library of Python to backtest how many times underlying has broken particular SD level. So I can use simple returns over log returns.

Please correct me if I am missing something here

Its the other way round right?

Sure! Thank you!

I calculated daily returns using traditional formula

returns = (latest close – previous close) / previous close

and other way is to do it by logarithmic

returns = log(latest close / previous close)

My question is how this two ways differs?

I saw around 60-100 points difference in final calculations. What are advantages/disadvantages of one over other from option selling perspective. Which one I should use?

I have explained this in queries (Volatility application chapter), can you please check that once?

Hello Team, there seems to be multiple typos is European vs AMerican Call Option topic. Please review it

Will review this again, thanks.

How do we dispose a short call option ?

By disposing of, do you mean to exit? If yes, it is just like the way you went shorted it. Go ahead, press the buy button and close the position. Or from the positions tab, click on exit.

Yes I have done the same. I might have messed up with posting here but I have done as you taught for selling

Good luck, and I hope this works in your favor.

I posted here results but not sure if it is visible or not as I am not able to see but when I repost it it says, duplicate comment detected.

Yeah, when you post a comment with the link, it comes for moderation and won\’t be available immediately.

Basically I have used simple logic to generate this data. I simply fetched data from NSE and calculated mean and std dev for last 252 days of daily returns as per strategy. Then I projected these figures (mean and std dev) for specified days like 4,3,2,1 (to create positions on Friday, Monday, Tuesday, Wednesday respectively) since I generally trade weekly options. I have not considered weekends as trading days so used 4 days projection for creating short position on Friday and 6 days basically as market will be shut anyways for 2 days.

By leveraging window functions of pandas library, I (I mean my laptop 😁) ran these operations for each day till end. and at end all generated results are exported to csv file.

Now I can simply compare closing price on expiry date with std dev levels 4 days prior to that expiry and count how many times these levels were broken, by how much points they were broken if so and so on as per need.

This comparing and counting work can also be automated but I am not yet till that level. Working on it!

Here is sample file for bank nifty levels to sell options on Friday (4 days prior to expiry) :https://drive.google.com/file/d/1_79-RAhSYJxG0SYcciVkILvYFydaRByw/view?usp=sharing

Also I have build some technical indicators and their BackTesting. Here is GitHub link for this: https://github.com/Dhananjay-B/QuantPack

Got it. But I hope you convert SD value by multiplying with Sqrt of time. I hope you get favorable results 🙂

Thank you! Also I would like to share that I learnt to backtest trading strategies using Python. Our option selling strategy (based on standard deviation) now can be tested in few minutes for last 10-15 years data!

Amazing. Do share the results 🙂

Hello sir!

Let say I short stock call option just before expiry and market remained in favor of me till expiry. I want to know are there any cases where I will suffer a loss except the directional movement of stock?

No, not really. Your loss depends on the option\’s intrinsic value, which upon expiry is dependent on the directional movement of the stock.

Can we hold option sell position till expiry ? (example – if we sell next month option.)

Yes, you can hold to expiry.

How does the settlement of covered call selling? It means I have a stock and I am selling the call of that stock. If that stock goes above the exercise price, does Zerodha deducts the premium and settle loss/profit OR Zerodha takes the underlying shares from demat and credit the value of exercise price? Thanks

If you have written a call option, that means that if the strike turns ITM at expiry, then you are obligated to give delivery of shares. So shares will be debited from your demat account and delivered to the buyer.

Hello Karthik,

I have got a question. Can you please explain or tell me in which condition a buyer of a Call Option will get his premium back ?? Or is there no condition as such that exist ??

Whenever the buyer squares off the position (either call or put), the buyer receives the premium which is prevailing in the market at that point.

Hi Karthik,

If i take a option position for expiry for one of this week and one for next week.

Will the one expiring in the next week also squared off by Zerodha when this week option expires on Thursday.

For example i take a position for 11th Aug and 18th Aug Will 18thAug will be squared off on 11th Aug if i don\’t sell it on 11th Aug ?

No, square-off will happen only for the one which is expiring.

I dont Understand what is squaring off. it would be Helpful if u explain with example

Assume you buy a stock at 107 and sell the stock at 110 for a profit of Rs.3. Here when you sell at 110, you are essentially squaring off your long position at 107.

Hello

I might be wrong, still I would like to express my view……… I think in 4.2 para……. The highlighted word \”disadvantage \”……… should be advantage……… Because option buyer has advantage in only one situation out of three when price increases

Perhaps, will look at it again 🙂

Hi, Karthik

Suppose if I am selling option in Nifty 50 only as a intraday trader. I want to know whether I am allowed to exit my position any time whenever I want during the day or there is any particular rule

Thanks

You can exit anytime you wish; no need to wait for a particular time.

Understanding option was a humongous task. You really sir, has done an excellent work in simplifying for us.

Wanted to confirm if I understood correctly.

buyers: only premium is considered when squaring off before expiry, but squaring off by exchange following expiry means now along with premium IV will also be considered during settlement.

settlement for seller : Before expiry difference in premium and post expiry get to keep the only the premium and no IV will be considered as per your P&L statement example. Am I correct sir?

Thanks Ajay. Glad you liked the content here.

Before expiry – If you sq off before expiry, the difference in premium is considered for P&L

At expiry – The intrinsic value of options is considered

You can also check this – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

How to measure whether a spread is high or low? I know how to find the spread, (subtract bid-ask)..but after finding the spread..what do I compare it with?

Nifty is the most liquid futures contract. You can compare the stock spread with Nifty\’s.

How do you judge the liquidity of a futures contract?

I get the liquidity risk part.

But then what is the point of saying in future there is always a buyer for every seller?

To check the liquidity of a contract, you simply check the difference between the bid and ask, this is called the bid-ask spread. The higher the spread, the lower is the liquidity. The tighter the spread, the higher the liquidity.

So if you don\’t find a buyer or a seller for your contract that you already own, that means there is at least 1 counter party to you who is refusing to sell or buy. In such cases you can always hold to expiry and upon expiry, the exchanges will settle the contract for you.

But in futures contract isn\’t there a buyer for every seller and vice versa? That is decided when both sides enter the contract. So I don\’t understand how low liquidity can be a factor for futures.

For cash I can understand, as there is no seller guaranteed when you buy the shares.

So imagine you bought a futures contract and the price has increased after you bought, you now want to book profits, but there are no one who will buy this from you. That means you are stuck right? This is liquidity risk.

If your stock has low liquidity in the cash sector, does it mean it is also low liquid in the fno sector?

Highly likely, Jay.

Hello sir!

Sir on Sensibull or any other platform, they show us our probability of profit(PoP) when we set our trade using different legs. I am not sure how actually this PoP is interpreted.

Let\’s say, I executed 100 trades each having 88% probability of profit. Does that mean with such kind of PoP, out of 100 trades executed, 88 trades will be profitable and rest 12 will be loosing?

Please clarify!

I guess this is based on each trade and not on the entire set. Maybe you should write to Sensibull team to figure this 🙂

Hi Karthik, my doubt is when we sell an option, we get the net premium. If the option is expiring worthless is there anything that we need to buy back that option maybe say at 0.5 or 0.25 etc to get the profit or we can just the options to expire and get the M2M profit ?

You can just let it expire worthless, Sai.

Hi Senthil, as the premium has become 245, your profit would be 100 rs.

Dear Karthik sir,

Suppose I sold an option whose strike = 8500CE Premium = Rs.20. I square it off before expiry.

Today Spot = 8450 & Premium = Rs.30 What would be my P/L? Please help.

YOu will lose 10.

Good evening Mr.Karthick

I buy today the bank nifty call option strike 34500 when the spot was 34327 premium was 345. If I square of the position tomorrow for premium 245 then my loss will be 100 or entire premium which I paid?

Yes, thats correct.

Dear Karthik sir,

Suppose I sold an option whose strike = 8500CE Premium = Rs.20. I square it off before expiry.

Today Spot = 8450 & Premium = Rs.30 What would be my P/L? Thanks.

Hi Karthik, on this page you have given an option selling example with Stock options. It would have been more perfect if have given one more example with index option selling as well.

the index option selling profit/loss calculation is confusing very much.

thanks for your time and efforts.

In fact, it is easier with an index as everything is cash settled. Btw, which part is confusing, let me know, maybe I can help.

Ultimate clarity through this Q/A segment !

Happy learning, Tarun 🙂

I buy jubilant food call option of strike price 520 at 12.90 premium..now share goes down and premium comes to 9 …can i sell call at 9 and book loss on premium ?

If i sell at 9 how much loss is possibile??

Yes, you can. The difference in premium i.e. 12.9 – 9 will be your loss.

Hi

I just went through your brokerage calculator for currencies. Say I buy something for 80 and sell for 90.

The brokerage should be 20 because there is one transaction.

But in the calculator it shows 40. Is brokerage being charged once when you buy (20) and when you sell (40)?

Its 20 for each leg, so 20 + 20 = 40.

Yes, I want to place target and SL together. OCO works only for intraday and not delivery, so how to set up something similar to OCO for delivery.

What about commodities and currencies? Are they physical or cash settled?

GTT works when you want to place a buy order for something you have not already bought. Supppose I have sold a contract, and want to set a buy order as stop loss for the same contract at a higher, will GTT help me?

I could set another separate buy order for GTT at a higher price but that is not the same as setting stop loss for the same contract.

I think you want to place both target and SL together. Why don\’t you try OCO, where one order cancels the other?

Hi

What happens to a future if it is not cancelled on expiry day?

Are ALL futures cash settled? I mean if I buy for 100 and the close price is 110 without me closing, I get approximately 10 back in my account.

Is there any alternative to setting stop loss everyday. Similar to GTT, you set a stop loss market order once for a trade and that is it. The current system of logging daily to place stop loss is annoying.

If you dont close before expiry, then the futures is physically settled (stock futures) and cash-settled if its index futures. More on that here – https://zerodha.com/varsity/module/futures-trading/

YOu can use GTT for futures, check this – https://support.zerodha.com/category/trading-and-markets/kite-features/gtt/articles/gtt-fno

Hi,

Can u say the exact difference between futures and options?

Please do read the two modules 🙂

Hello Karthik,

one doubt regarding option selling.

example

if i sell HDFC APR 2200 CE for premium 40 (lot size 300) on 26th April and on 27th April if i buy(close yesterdays sell option ) hdfc apr 2200 ce when the premium is at 22, what will be my profit ?

will it be 18*300 = 5400 ?

thanks ,

deepak

40-22 is your profit.

if you have bought Call Option which is presently a deep OTM strike, can you sell a call at the same strike and lot size and tap your loss rather than squarring off your position…

thanks

Nope, that will sq off the position.

In the chapter of buying and selling options (call and put) you have written down break even as breakdown point. It is just a typo and nothing big as the point has been driven home in finesse.

Not a typo, its breakdown point when the prices starts to trend down.