5.1 – Getting the orientation right

I hope by now you are through with the practicalities of a Call option from both the buyers and sellers perspective. If you are indeed familiar with the call option then orienting yourself to understand ‘Put Options’ is fairly easy. The only change in a put option (from the buyer’s perspective) is the view on markets should be bearish as opposed to the bullish view of a call option buyer.

The put option buyer is betting on the fact that the stock price will go down (by the time expiry approaches). Hence in order to profit from this view, he enters into a Put Option agreement. In a put option agreement, the buyer of the put option can buy the right to sell a stock at a price (strike price) irrespective of where the underlying/stock is trading at.

Remember this generality – whatever the buyer of the option anticipates, the seller anticipates the exact opposite, therefore a market exists. After all, if everyone expects the same a market can never exist. So if the Put option buyer expects the market to go down by expiry, then the put option seller would expect the market (or the stock) to go up or stay flat.

A put option buyer buys the right to sell the underlying to the put option writer at a predetermined rate (Strike price. This means the put option seller, upon expiry will have to buy if the ‘put option buyer’ is selling him. Pay attention here – at the time of the agreement the put option seller is selling a right to the put option buyer wherein the buyer can ‘sell’ the underlying to the ‘put option seller’ at the time of expiry.

Confusing? well, just think of the ‘Put Option’ as a simple contract where two parties meet today and agree to enter into a transaction based on the price of an underlying –

- The party agreeing to pay a premium is called the ‘contract buyer’ and the party receiving the premium is called the ‘contract seller’

- The contract buyer pays a premium and buys himself a right

- The contract seller receives the premium and obligates himself

- The contract buyer will decide whether or not to exercise his right on the expiry day

- If the contract buyer decides to exercise his right then he gets to sell the underlying (maybe a stock) at the agreed price (strike price) and the contract seller will be obligated to buy this underlying from the contract buyer

- Obviously, the contract buyer will exercise his right only if the underlying price is trading below the strike price – this means by virtue of the contract the buyer holds, he can sell the underlying at a much higher price to the contract seller when the same underlying is trading at a lower price in the open market.

Still, confusing? Fear not, we will deal with an example to understand this more clearly.

Consider this situation, between the Contract buyer and the Contract seller –

- Assume Reliance Industries is trading at Rs.850/-

- Contract buyer buys the right to sell Reliance to contract seller at Rs.850/- upon expiry

- To obtain this right, the contract buyer has to pay a premium to the contract seller

- Against the receipt of the premium, contract seller will agree to buy Reliance Industries shares at Rs.850/- upon expiry but only if contract buyer wants him to buy it from him

- For example, if upon expiry Reliance is at Rs.820/- then contract buyer can demand contract seller to buy Reliance at Rs.850/- from him

- This means contract buyer can enjoy the benefit of selling Reliance at Rs.850/- when it is trading at a lower price in the open market (Rs.820/-)

- If Reliance is trading at Rs.850/- or higher upon expiry (say Rs.870/-) it does not make sense for contract buyer to exercise his right and ask contract seller to buy the shares from him at Rs.850/-. This is quite obvious since he can sell it at a higher rate in the open market

- An agreement of this sort where one obtains the right to sell the underlying asset upon expiry is called a ‘Put option’

- Contract seller will be obligated to buy Reliance at Rs.850/- from contract buyer because he has sold Reliance 850 Put Option to the contract buyer

I hope the above discussion has given you the required orientation to the Put Options. If you are still confused, it is alright as I’m certain you will develop more clarity as we proceed further. However, there are 3 key points you need to be aware of at this stage –

- The buyer of the put option is bearish about the underlying asset, while the seller of the put option is neutral or bullish on the same underlying

- The buyer of the put option has the right to sell the underlying asset upon expiry at the strike price

- The seller of the put option is obligated (since he receives an upfront premium) to buy the underlying asset at the strike price from the put option buyer if the buyer wishes to exercise his right.

5.2 – Building a case for a Put Option buyer

Like we did with the call option, let us build a practical case to understand the put option better. We will first deal with the Put Option from the buyer’s perspective and then proceed to understand the put option from the seller’s perspective.

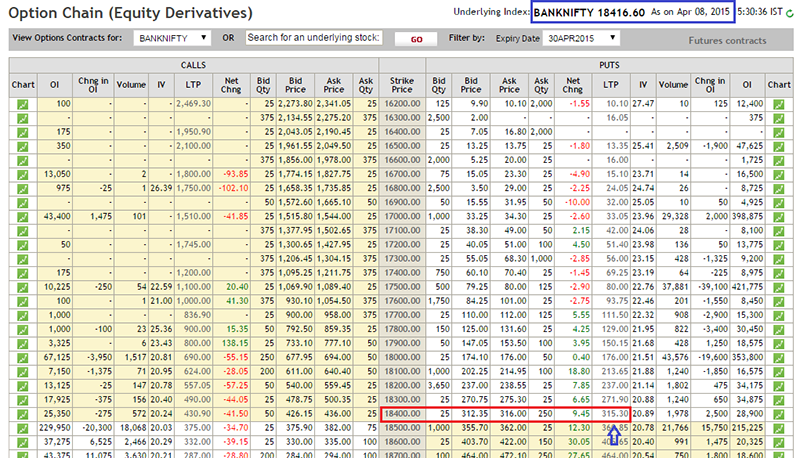

Here is the end of day chart of Bank Nifty (as on 8th April 2015) –

Here are some of my thoughts with respect to Bank Nifty –

- Bank Nifty is trading at 18417

- 2 days ago Bank Nifty tested its resistance level of 18550 (resistance level highlighted by a green horizontal line)

- I consider 18550 as resistance since there is a price action zone at this level which is well spaced in time (for people who are not familiar with the concept of resistance I would suggest you read about it here

- I have highlighted the price action zone in blue rectangular boxes

- On 7th of April (yesterday), RBI maintained a status quo on the monetary rates – they kept the key central bank rates unchanged (as you may know RBI monetary policy is the most important event for Bank Nifty)

- Hence in the backdrop of technical resistance and lack of any key fundamental trigger, banks may not be the flavour of the season in the markets

- As a result of which traders may want to sell banks and buy something else which is the flavour of the season

- For these reasons I have a bearish bias towards Bank Nifty

- However shorting futures maybe a bit risky as the overall market is bullish, it is only the banking sector which is lacking lustre

- Under circumstances such as these employing an option is best, hence buying a Put Option on the bank Nifty may make sense

- Remember when you buy a put option you benefit when the underlying goes down

Backed by this reasoning, I would prefer to buy the 18400 Put Option which is trading at a premium of Rs.315/-. Remember to buy this 18400 Put option, I will have to pay the required premium (Rs.315/- in this case) and the same will be received by the 18400 Put option seller.

Of course, buying the Put option is quite simple – the easiest way is to call your broker and ask him to buy the Put option of a specific stock and strike and it will be done for you in a matter of a few seconds. Alternatively, you can buy it yourself through a trading terminal such as Zerodha Pi We will get into the technicalities of buying and selling options via a trading terminal at a later stage.

Now assuming I have bought Bank Nifty’s 18400 Put Option, it would be interesting to observe the P&L behaviour of the Put Option upon its expiry. In the process, we can even make a few generalizations about the behaviour of a Put option’s P&L.

5.3 – Intrinsic Value (IV) of a Put Option

Before we proceed to generalize the behaviour of the Put Option P&L, we need to understand the calculation of the intrinsic value of a Put option. We discussed the concept of intrinsic value in the previous chapter; hence I will assume you know the concept behind IV. Intrinsic Value represents the value of money the buyer will receive if he were to exercise the option upon expiry.

The calculation for the intrinsic value of a Put option is slightly different from that of a call option. To help you appreciate the difference let me post here the intrinsic value formula for a Call option –

IV (Call option) = Spot Price – Strike Price

The intrinsic value of a Put option is –

IV (Put Option) = Strike Price – Spot Price

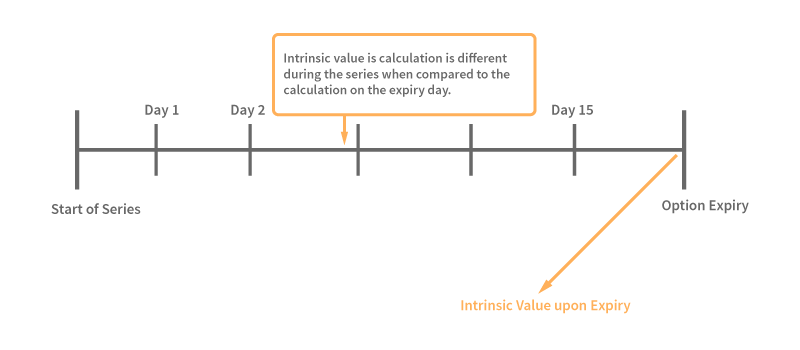

I want you to remember an important aspect here with respect to the intrinsic value of an option – consider the following timeline –

The formula to calculate the intrinsic value of an option that we have just looked at is applicable only on the day of the expiry. However, the calculation of the intrinsic value of an option is different during the series. Of course, we will understand how to calculate (and the need to calculate) the intrinsic value of an option during the expiry. But for now, we only need to know the calculation of the intrinsic value upon expiry.

5.4 – P&L behaviour of the Put Option buyer

Keeping the concept of intrinsic value of a put option at the back of our mind, let us work towards building a table which would help us identify how much money, I as the buyer of Bank Nifty’s 18400 put option would make under the various possible spot value changes of Bank Nifty (in the spot market) on expiry. Do remember the premium paid for this option is Rs 315/–. Irrespective of how the spot value changes, the fact that I have paid Rs.315/- will remain unchanged. This is the cost that I have incurred in order to buy the Bank Nifty 18400 Put Option. Let us keep this in perspective and work out the P&L table –

Please note – the negative sign before the premium paid represents a cash out flow from my trading account.

| Serial No. | Possible values of spot | Premium Paid | Intrinsic Value (IV) | P&L (IV + Premium) |

|---|---|---|---|---|

| 01 | 16195 | -315 | 18400 – 16195 = 2205 | 2205 + (-315) = + 1890 |

| 02 | 16510 | -315 | 18400 – 16510 = 1890 | 1890 + (-315)= + 1575 |

| 03 | 16825 | -315 | 18400 – 16825 = 1575 | 1575 + (-315) = + 1260 |

| 04 | 17140 | -315 | 18400 – 17140 = 1260 | 1260 + (-315) = + 945 |

| 05 | 17455 | -315 | 18400 – 17455 = 945 | 945 + (-315) = + 630 |

| 06 | 17770 | -315 | 18400 – 17770 = 630 | 630 + (-315) = + 315 |

| 07 | 18085 | -315 | 18400 – 18085 = 315 | 315 + (-315) = 0 |

| 08 | 18400 | -315 | 18400 – 18400 = 0 | 0 + (-315)= – 315 |

| 09 | 18715 | -315 | 18400 – 18715 = 0 | 0 + (-315) = -315 |

| 10 | 19030 | -315 | 18400 – 19030 = 0 | 0 + (-315) = -315 |

| 11 | 19345 | -315 | 18400 – 19345 = 0 | 0 + (-315) = -315 |

| 12 | 19660 | -315 | 18400 – 19660 = 0 | 0 + (-315) = -315 |

Let us make some observations on the behaviour of the P&L (and also make a few P&L generalizations). For the above discussion, set your eyes at row number 8 as your reference point –

- The objective behind buying a put option is to benefit from a falling price. As we can see, the profit increases as and when the price decreases in the spot market (with reference to the strike price of 18400).

- Generalization 1 – Buyers of Put Options are profitable as and when the spot price goes below the strike price. In other words, buy a put option only when you are bearish about the underlying

- As the spot price goes above the strike price (18400) the position starts to make a loss. However, the loss is restricted to the extent of the premium paid, which in this case is Rs.315/-

- Generalization 2 – A put option buyer experiences a loss when the spot price goes higher than the strike price. However, the maximum loss is restricted to the extent of the premium the put option buyer has paid.

Here is a general formula using which you can calculate the P&L from a Put Option position. Do bear in mind this formula is applicable on positions held till expiry.

P&L = [Max (0, Strike Price – Spot Price)] – Premium Paid

Let us pick 2 random values and evaluate if the formula works –

- 16510

- 19660

@16510 (spot below strike, position has to be profitable)

= Max (0, 18400 -16510)] – 315

= 1890 – 315

= + 1575

@19660 (spot above strike, position has to be loss making, restricted to premium paid)

= Max (0, 18400 – 19660) – 315

= Max (0, -1260) – 315

= – 315

Clearly both the results match the expected outcome.

Further, we need to understand the breakeven point calculation for a Put Option buyer. Note, I will take the liberty of skipping the explanation of a breakeven point as we have already dealt with it in the previous chapter; hence I will give you the formula to calculate the same –

Breakeven point = Strike Price – Premium Paid

For the Bank Nifty breakeven point would be

= 18400 – 315

= 18085

So as per this definition of the breakeven point, at 18085 the put option should neither make any money nor lose any money. To validate this let us apply the P&L formula –

= Max (0, 18400 – 18085) – 315

= Max (0, 315) – 315

= 315 – 315

=0

The result obtained is clearly in line with the expectation of the breakeven point.

Important note – The calculation of the intrinsic value, P&L, and Breakeven point is all with respect to the expiry. So far in this module, we have assumed that you as an option buyer or seller would set up the option trade with an intention to hold the same till expiry.

But soon you will realize that more often than not, you will initiate an options trade only to close it much earlier than expiry. Under such a situation the calculations of breakeven point may not matter much, however, the calculation of the P&L and intrinsic value does matter and there is a different formula to do the same.

To put this more clearly let me assume two situations on the Bank Nifty Trade, we know the trade has been initiated on 7th April 2015 and the expiry is on 30th April 2015–

- What would be the P&L assuming the spot is at 17000 on 30th April 2015?

- What would be the P&L assuming the spot is at 17000 on 15th April 2015 (or for that matter any other date apart from the expiry date)

Answer to the first question is fairly simple, we can straightway apply the P&L formula –

= Max (0, 18400 – 17000) – 315

= Max (0, 1400) – 315

= 1400 – 315

= 1085

Going on to the 2nd question, if the spot is at 17000 on any other date apart from the expiry date, the P&L is not going to be 1085, it will be higher. We will discuss why this will be higher at an appropriate stage, but for now just keep this point in the back of your mind.

5.5 – Put option buyer’s P&L payoff

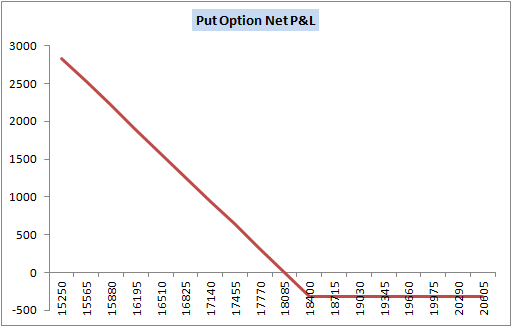

If we connect the P&L points of the Put Option and develop a line chart, we should be able to observe the generalizations we have made on the Put option buyers P&L. Please find below the same –

Here are a few things that you should appreciate from the chart above, remember 18400 is the strike price –

- The Put option buyer experienced a loss only when the spot price goes above the strike price (18400 and above)

- However, this loss is limited to the extent of the premium paid

- The Put Option buyer will experience an exponential gain as and when the spot price trades below the strike price

- The gains can be potentially unlimited

- At the breakeven point (18085) the put option buyer neither makes money nor losses money. You can observe that at the breakeven point, the P&L graph just recovers from a loss-making situation to a neutral situation. It is only above this point the put option buyer would start to make money.

Key takeaways from this chapter

- Buy a Put Option when you are bearish about the prospects of the underlying. In other words, a Put option buyer is profitable only when the underlying declines in value

- The intrinsic value calculation of a Put option is slightly different when compared to the intrinsic value calculation of a call option

- IV (Put Option) = Strike Price – Spot Price

- The P&L of a Put Option buyer can be calculated as P&L = [Max (0, Strike Price – Spot Price)] – Premium Paid

- The breakeven point for the put option buyer is calculated as Strike – Premium Paid

COULD YOU PLEASE EXPLAIN/SIMPLIFY YOU CALCULATION OF CHAPTER 5 (PG. 217-222) BASED ON THE PROFITABILITY. WAS IS BASED ON THE BS FORMULAR? IF SO, ARE THERE VARIABLES NO GIVEN IN THE PROBLEM?

THANKS AND BEST REGARDS,

Its based on the premiums and the difference between buying and selling price of the options.

how does one decide if the view of the underlying is bearish, to buy a put or sell the future.

undoubtedly the premium on the put buy will be larger than the margin on the future sell. Are there any other factors data points which will drive this decision.

Maybe this will help, do check this – https://youtu.be/0CnHdzTE66s?si=fWfAFfj6VG1LMgv2

we cannot execute call option before expiry but we can execute put option before expiry?

When you say \’execute\’, I\’m assuming you mean exercise. There is a difference between execute/exercise and square off. Please do check this – https://youtu.be/Llp4xW2GI4s?si=sZ4ypjwJYqMDyikP

Hi karthik,

If we buy call or put option then our loss is limited to premium that we paid. but to settle the position we will square it off right then losses will be exponenetial?

Think of it this way, the profit or loss you make on the option trade is equal to the difference between the buy and sell price of the option premium.

If i have no underlying stock

Buy a put option, i am in the money after 2 days, what to do in kite to book profit?

YOu can square off the position. On kite, select exit and close the trade.

If I buy one quantity of CE @100 LTP at 22500 strike price. After some time the market fall and LTP dropped to Rs 60. Here I analyse market will further drop.

I have decided to square off this trade and I exercise following two options.

1) I can exit CE and buy PE at current LTP respectively at the same strike 22500.

Or

2) I exercise SELL of two quantity at Same strikes of 22500, (i.e. 1no to exit previous CE trade and 1no for new SELL trade.

Query;

Can I eligible to exercise my suggested above trades options? Also clarify the most beneficial option among two or otherwise another option you suggest.

Thanks,

Hey, suppose i enter a trade in nifty 23800 PE, where nifty currently trading at 24000. and the premium of nifty 23800 PE is 54.90/-, so according to you the breakout point, where i got no profit no loss is (23800-54.90) = 23745.1

But, say when i enter the same trade in zerodha, after entering within a second, i had my PnL flickering with profit and loss, why so .

The breakeven point is applicable only if you hold to expiry. But during the series, the P&L varies depending on the movement in the premium.

Hi kartik

I want you to clarify that the maximum loss of a option (CE or PE) buyer may experience is the premium of the strike or the margin paid (premium * lot size) for the strike.

For buyers, it is to the extent of premium paid.

Hi Karthik

Today in Bank Nifty, even if Bank Nifty is going up the put option premiums are also going up for all the strikes, can you explain the reason?

Option greeks at play 🙂

it would be important to update this in Indian context as now DNE rights of option buyer are taken away. in that sense, call option buyer has to buy the stock and put option buyer has to sell the stock

DNE was not there originally, it was introduced for a bit and then taken away, Pawan.

Hi Karthik,

Please clarify the difference in buying 18000CE & 18000PE same way selling18000PE & 18000 CE its one and the same right ?

Hmm, not the same. Check this – https://www.youtube.com/watch?v=0CnHdzTE66s&list=PLX2SHiKfualEyD05J9JsklEq1JFGbG6qJ&index=1

Hello Kartik Sir,

Good Afternoon,

Thanks for all ur concern knowledge on CALL & PUT option.

Really it helps me a lot.

Now may be i clear on this topic but if i have some quries on this topic then i call u surelly.

Thanks.

Of course, feel free to post your queries here.

Dear Karthik sir,

IV is calculated as Spot-Strike or Strike-Spot on the expiry day. But what is the formula to calculated the IV before expiry day?

For that, you will have to use the B&C calculator Sandeep.

Thank you so much sir.

Sure, happy learning 🙂

Dear Karthik sir,

In the section 5.4 of P&L behavior of Put option buyer example, you have said that if the buyer had closed the trade

before expiry then his P&L would have been higher.

Sir, kindly explain how P&L would be higher before expiry than on the expiry day.

On Expiry, the premium is only equal to the intrinsic value. But Before expiry, the premium is intrensic value plus time value.

Great work by Zerodha Team, I have received lot of suggestions ( different sources of material ) from friends to learn F&O, my instinct suggest varsity over all other sources. your explaination is simply amazing.

I foung this (could be error) in 5.5 – Put option buyer’s P&L payoff, point 5 stating about break even point( It is only above this point the put option buyer would start to make money.)

recommended suggestion: It is only below this point the put option buyer would start to make money. please let me know if i am wrong. i will reread this chapter.

Thanks, Manisha.

Correction noted, will do 🙂

No 18085 is the Profit which I understand. What I am asking is you have said that the Profit would be higher if the option is sold

before expiry. This I want to understand that how will be higher. Sir, kindly explain how is it so.

Dear Karthik sir,

In the section 5.4, you have given an example of Put option where Strike = 18400, Spot = 18085 and the Premium = 315/

The net P&L = 18085. This happens on the day of expiry. Here you say that if the spot is 18400 before the expiry day,

then the profit would be higher. Sir, could you please explain how ? Thanks.

Not sure if I fully understand your query. 18085 is the spot right? P&L is the difference between buy and sell value of the premium.

Oh ok.. Got it now..:-) 😄

Sure, feel free to post all your queries here 🙂

Thanks Karthik but I didn\’t understand the last line in your response above. May be you are asking me to read in between the lines (of your response) which I am not able to do. Frustrated by seeing the far otm options trading at discount on a daily basis these days and not getting the statutory answer. But this motivates me to get to the bottom of this until I am satisfied..

What I mean by that is, if you think there is a very nice and obvious opportunity to trade and profit from, then chances are that its not really an opportunity and our understanding of the market is not complete. Hence if something look too good to be true, that it is 🙂

Thanks Karthik for the explanation. I never thought I will have to get into Black-Scholes formula to understand the option premium pricing but looks like now I have to. As a trader who has bought the monthly PE say for example 17500 PE Mar at the start of the month is getting a raw deal here if they want to square off their position because here it\’s trading at less than the intrinsic value. That\’s actual point when this thing came to my notice. Nevertheless I will explore more in the direction you have provided and try to find the answer that is satisfactory for myself

The theoretical price of an option is based on the B&S calculator, Amit. Btw, one thing in market, if something looks too good to be true, then its not true 🙂

Wow, your explanation came to me as a bummer. Nifty Option Premiums being pegged against the Nifty futures and not the Nifty spot is something new for me. I find this a bit misleading though because on Nifty weekly expiry (Not the monthly expiry) Nifty futures and spot don\’t converge (most of the times) and if one checks the option premiums on the weekly expiry day then at around 3.25 PM they are just near to Nifty spot and not the Nifty futures. Even their final closing prices (not the last traded prices) perfectly match to Nifty spot. For example – on 23-Mar-2023 Nifty weekly expiry Nifty finally closed at 17076 and Nifty 17050-23Mar CE closing price was 26 but Nifty futures closed at 17087, so as per your logic 17050 23-Mar CE final closing price should have been 37 and not 26 isn\’t it?

Please explain if you are not bothered by the flurry of my queries

Thanks in advance

Amit, so its a little tricky and I\’ll try and explain why, if not at least point you in the direction in which you\’ll have to explore more. Options are pegged to the spot itself and not futures (unlike commodities). The risk-free rate is one variable to consider when arriving at the option premium. Riskfree rate is also a common variable for futures pricing. So while calculating the options premium, factoring in the futures instead of the spot implies that you are baking in the risk-free rate as an input into your option pricing.

This should also solve the weekly settlement gap you think exists.

Well, your answer was terse that didn\’t give me any idea about the reason behind the discounted premiums of far otm options. I will keep finding answers myself though and also keep a close watch on when you update the chapters on futures/options pricing

Amit, I was just checking your previous comment.

Strike = 17600 PE

Nifty Fut= 17165

Min price at which 17600 PE should trade = Strike – Spot

i.e. 17600 – 17165

= 435

According to you, the primum is 445, so 10 Rupee higher than the theoretical price. So the additional 10 can be attributed to time value.

Ok. Today\’s situation – Nifty spot 17129, Nifty Mar Fut – 17165 Nifty Mar 17500 PE – 360. Thus it is trading at 10 rupees discount at the moment. Same is the case with 17600 PE trading at 445 thus at discount of 25 INR. How do you explain it? What\’s the relation of Nifty futures price with Nifty option price? And why then ATM or slight otm put options are trading at premium and not at discount. Please care to enlighten people like us..

The reference price for option pricing is option futures (I will have to update the chapters). So please look at the premiums with reference to the futures.

Surprisingly there is a discussion thread on tradingqna.com on this scenario (link below) but no one seems to be having a satisfactory answer.. Can you please shed some light on this Karthik?

https://tradingqna.com/t/why-are-bank-nifty-options-trading-at-discount/42087

I have screenshot of the scenario but no way to attach here.. Monthly put is clearly trading at discount here which is beyond me..

Like I mentioned, also please check the futures price.

Hi Karthik,

See today – 21 Mar 2023 at 1350 hrs. Nifty spot at 17083 and Nifty Mar Put of 17500 trading at 393. Shouldn\’t it be at least 417? Put expiry is more than a week away as you can see. You said that it\’s unlikely scenario but it\’s not. Can you please clarify on this now?

Hey Amit, one thing to note is that the reference should be to future price. Can you check where futures were at that point?

Ok. I will keep an eye on those things in the future because obviously checking it now is not possible. But from the market integrity standpoint I still don\’t understand how it can be trading at discount. I understand that the additional premium could be 0 but 2 days before expiry it should be trading at least at the intrinsic value isn\’t it? I checked in Google and found few links explaining this but nothing specific as such. All I found that this could happen due to market inefficiencies. There is no explanation about what that meant

Amit, its unlikely to trade below the intrinsic value. There must be some mistake. Anyway, keep an eye out and take screenshots the next time you spot such an anomaly 🙂

However shorting futures maybe a bit risky as the overall market is bullish, it is only the banking sector which is lacking lustre. Under circumstances such as these employing an option is best, hence buying a Put Option on the bank Nifty may make sense.

Please explain this. How is shorting futures is risky and Buying Put is not? Not understood.

The only reason to state that is that the loss with a naked put is restricted to the premium paid.

Sorry Karthik, closing price of 18000 put was 324 but it\’s still at 4 INR discount when the expiry is still 2 days away. How come?

Please check the previous comment.

Hi Karthik,

Though i wrote it as ltp it was actually a closing price, you can check this yourself at your end

Thanks

Sure, also, I\’m not sure about the liquidity. The LTP reflects its low intrinsic value, based on a previous trade, but you should also check the bid and ask. This is common with contracts that don\’t have much liquidity.

Hi Karthik,

I observed something strange today. Nifty closed at 17662, weekly expiry still has 2 more days to go and still the 18000 put ltp is 334. Shouldn\’t it be at least 338? More surprisingly 18100 put ltp at close was 410 so it\’s trading at almost 28 rupees discount. Someone who has bought 18100 put few days back is getting a raw deal here. How\’s it even possible that put premium is less than its intrinsic value?

Thanks in advance for clarifying on this

I\’m guessing you are seeing the LTP; please check the close price.

what if I take two puts , both having different expiry ? How will payoff be calculated then ?

You can use Sensibull’s platform to visualize this, Vivek. They give the pay-off plots.

That comes to 9.95x 550(lot size for HDFCBANK) =₹5472.50.

Thanks so much for clarifying that Karthik…you are the best!

Happy to be of help 🙂

Hi,

I am confused by fund requirements for a BUY order for PE of HDFCBank.

How much fund do I need if I buy a PE for strike price of 1460 with premium showing up @9.95?

Can you please clarify?

YOu will have to pay the premium i.e. 9.95*lot size.

Hi Karthik,

I too had a doubt regarding selling call options and buying put options. I went through the comments where you had stated that it is a game of premiums and margins required. Could you explain it in a more elaborate way?

Thanks

You can check this – https://www.youtube.com/watch?v=0CnHdzTE66s&list=PLX2SHiKfualEyD05J9JsklEq1JFGbG6qJ&index=1

Hello,

On option (put bought) expiry date our profit is strike price minus spot price of expiry date if spot price is more. My question is (1) Will we get profit as difference of strike price and spot price of expiry date + any premium left on expiry date of our bought put option. (2) expiry date price means any time price of expiry date or closing price of expiry date.

1) Yes, but only for index options as index options are cash settled. For stock options, the options contracts are physically settled.

2) Its the settlement price on expiry day, which is the average of the last 30 minutes of trading.

How to place a sell order for a put option. How to know the margin requirement for it. How to monitor a executed sell trade of a put option. Do you have a demo video for placing a sell order for a put option ?

Hey, do check our video series on Youtube, we have demonstrated this.

Hello Sir, I am new to options and going through your materials and yet to start its trading……I have one doubt to get clarified…if I buy one Put/Call option as Overnight/NRML, can I square it off the same day if my conditions are meet or is it necessary to hold it for at least a day? Thanks

Yes, you can. No need to wait to expiry.

I had gone through lot of YouTube videos but after going through this.i will rate this one of the best.excellent information.thanks.

Happy learning 🙂

Hi Karthik,

Check Section 5.5-last sentence when you concluded on Break-even Point for a Put option buyer, saying \”It is only above this point the put option buyer would start to make money\”.

I think this has to be corrected as \” It is only below this point the put option buyer would start to make money\” as you meant the strike price going below Break-even point for the put option buyer to start making money.

Is my understanding correct?

Thx,

Gopa.

Ah yes, guess that\’s a typo 🙂

hello Karthik, if I bought a european style put options that expired on 23 july but my otc is 20 july.How can I hedge against for that.

OTC? Which market are you referring to Jiny?

Hii Karthik

Qst.

1) buying a option today will automatically go forward to the next day till expiry?

2) today\’s PE premium has been shrinked from 60 to 20 I think Tommrow will a gap down so i hold it, what if market went opposite to my technicals so is there a chance I would be charge more than my total amount paid for the lot

1) It will get carried through till expiry unless you decide to close it before

2) No, when you buy an option, the maximum you lose is premium paid

hello sir

is it require to have margin amount if we want to sell the put holding

yesterday i traded nifty 15750 put buy option for first time. after getting some profit i place sell but i get error that is \”insufficient funds. Required margin is 72929.96 but available margin is 72026.40.Check the orderbook for open orders\”. can u clarify this sir

thank u

This happens if there are multiple positions. Check this – https://support.zerodha.com/category/trading-and-markets/kite-web-and-mobile/articles/kite-margin-on-exit

Thanks Karthik

Assuming Reliance spot price is 1000/- per share

If I buy reliance 900 strike put @10 rs premium so 250×10=2500

Where my loss is total 2500/- if it’s go higher and I will square off my position on or before expiry

But

On expiry or before expiry it’s turns in the money and spot price is 500

So at this point I am setting on profit assuming x amount

But if I want to square up my position with my X profit amount

I need to sell the put which I bought @10 rs

But what happen if there are no buyers on that day and this strike price become illiquid till on the day of expiry

And I am not able to square off my position

Jigs, yes, you can sell the option anytime before expiry and no need to hold to expiry. If there are no buyers, then you can hold tyo expiry and expect the broker to settle it for you.

Thanks Karthik sir. If you agree with me then kindly change the text in section 5.3. Thanks

Dear Karthik sir

No I just want to say it is the time value which is extracted from Premium, not the IV. IV remains the same in both before/at expiry, i.e. Spot-Strike price. Do you agree?

Yes, I do.

Suppose I bought 2 lots of (x) 1160 CE today i.e, on 23-05-2022 by paying 1 rupee premium. Assuming today is Monday, you said options expire on last Thursday of every month. Then, 1160 CE expires on 26-05-2022.

I will be pocketing the profits if it moves above breakeven point i.e., above 1161 rupees on the last day of expiry.

** My query is: Suppose the stock is trading at 1125 rupees on last day of expiry. Any how I know that I would lose my premium!! But, Assume the premium moved to 1.50 rupees(I paid 1 rupee premium). IS THERE ANY CHANCE ON THE LAST DAY TO EXERCISE THE OPTION AND POCKET THE PREMIUM DIFFERENCE I.E., 1.50-1 = 0.5 RUPEES INSTEAD OF LOSING ENTIRE PREMIUM??

You cant exercise the option since its OTM. But if you get the opportunity, you can sell it before market close and pocket the premium.

Dear Karthik sir

Do you agree with me now that it\’s the time value that is extracted from Premium while IV remains the same in both before/at expiry, i.e. Spot-Strike price? Please clarify sir.

I think the issue you have is that I\’ve used the word, éxtracted.

Zerodha Pi and Kite both same or different

Very different. Pi is discontinued by the way.

It\’s confusing because you say you extract IV from Premium while calculate IV = Spot – Strike.

We know Premium = IV + Time value. Tell me can we calculating time value without calculating IV first, no right ?

So for that

Step 1. IV needs to be calculated. right? (As per you example above, 2247-2220 = 27). Now tell me you are calculating IV as you do before expiry, ie. Spot – Strike. So the formula remains same in both cases before/at expiry. But you say you are extracting IV from Premium.

Step 2. Now after calculating the IV, you deduct it from Premium to get the time value. 102 – 27 = 75.

So my point is that you aren\’t extracting the IV from premium rather extracting the time value from premium. I want you to correct your statement and text in Section 5.3. That\’s all i want sir 🙂

Fine Sandeep.

In your comment above, you calculated IV = 2247-2220 (Spot – Strike) and telling to extract IV from Premium. Is it not confusing.

How is it that confusing Sandeep? First, you need to figure out where you stand in series. At expiry or before expiry. If its before expiry then extract the IV from the premium after deducting time value. If its after expiry, take the difference between spot and strike. That\’s it. Its as simple as that. I\’m explained the same thing many times in my response to your queries 🙂

Dear Karthik sir,

My confusion arises when you say IV is extracted from the Premium after factoring in the time value. In the examples above what you do?

You calculate IV = Spot – Strike price. So tell me where are you extracting the IV from the Premium? Moreover time value can\’t be calculated

before calculating the IV first. Right ?

Sandeep, I explained with the example on how to extract the intrinsic value from premium (before expiry) in my previous comment no. Please check that again.

Therefore I am saying that what you\’ve written in the section 5.3 —> \”However the calculation of intrinsic value of an option is different during the series\”

I believe it should be THE CALCULATION OF P&L OF AN OPTION IS DIFFERENT DURING THE SERIES. Did you get me now sir?

Please clarify if I am wrong.

Please see my previous comment.

Dear Karthik sir

You told in your earlier comment (Please see above) \”Before expiry, the intensive value is extracted from the premium after adjusting for the time value.\”

And in the next comment you have shown Intrinsic Value as = 2247-2220 which is Spot – Strike. So you are not extracting the IV from the premium rather the formula for IV remains the same as is done upon expiry, i.e. Spot – Strike. Did you get my point?

Sandeep, why are you getting confused? Please ignore all comments. Consider this – if you are looking at IV before expiry, then it has be extracted (or adjusted) after factoring in the time value. I have explained this in my earlier comment. If you are trying to find the IV post expiry, then its just the difference between the strike and spot. Thats it.

Hello Karthik,

I\’m struggling with this one issue. In the previous Ch. you mentioned that in India we only use European Call/Put option which means we cannot exercise our right till date of expiry…but all the following lessons indicate that we can exercise the right before dat of expiry. Please explain.

Nikita, these are two different things. Have explained it here – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

But earlier you said that before expiry Premium = IV + Time value. The value above the IV is the time value. As we see, the calculation of

Time value is itself dependent on IV. So as you say extract the IV from Premium.

Kindly explain how to do that.

Its simple. For example, Adani 2220 CE is trading at 102, while the spot is at 2247.

Intresic value = 2247-2220

= 27

Time value = 102 – 27

= 75

So out of the total premium of 102, 75 is attributed to time value and the rest is intrinsic value.

Dear Karthik sir,

Did you get the context of this line in 5.3? —> “However the calculation of intrinsic value of an option is different during the series.”

Its basically what we discussed earlier. At expiry, the intrinsic value is based on the difference between spot and strike. Before expiry, the intensive value is extracted from the premium after adjusting for the time value.

If formula for Intrinsic Value remains the same in both the cases(before/upon expiry), this statement is wrong in Section 5.3 —> \”However the calculation of intrinsic value of an option is different during the series.\”

Do you agree now sir? Please clarify.

Yes, will re-read what Ive written to get the context and change if required.

Thank u Karthik sir, So what I see, before the expiry also, the formula for IV remains the same, i.e, Spot price – Strike price.

Am I right?

Yes, that\’s right.

Dear Karthik sir,

I agree with you that Intrinsic Value is not a part of P&L before expiry.

But since the text is correct, I just want to know the formula to calculate IV before expiry even though it doesn\’t matter.

Kindly let me know this much.

Here you go –

Assume a 200 CE is trading at 25, which the spot is 220. Here the intrinsic value is 20 because we are dealing with a 200CE and spot us at 220. The excess premium overand and above the IV is time value i.e. 5.

So Premium = IV + Time value.

Hello Karthik sir,

I agree with you that before expiry, the P&L = Premium(sell) – Premium(buy).

And the Intinsic Value (IV) of the option does not apply there.

My question is that why have you written in the section 5.3 —>

“The calculation of the P&L and intrinsic value does MATTER and there is a different formula to do the same”

If the Intinsic Value (IV) does not apply, why does it\’s calculation MATTER?

The text is wrong? Kindly tell me Yes or No.

Sandeep, text is not wrong. So there are only two situations here – YOu hold to expiry or you sell before expiry. If you hold to expiry, the intrinsic value approach for P&L kicks in. If you sell before expiry, the difference in premium kicks in. Thats about it.

Hi! Is PE buyer for stocks required to maintain delivery margin on expiry in Indian Markets.?

Yes, thats right.

The chapter says —> \”The calculation of the P&L and intrinsic value does MATTER and there is a different formula to do the same\”

If there is no IV , then why does it matter?

I\’d suggest you check this – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

Dear Karthik sir,

Sorry for the repost.

I was asking about the Intrinsic Value not the Intrinsic Volatility.

Section 5.3 says —-> \”The calculation of INTRINSIC VALUE of an option is different during the series\”

I want to know what is the formula of Intrinsic value during the expiry series (before expiry)?

Kindly let me know.

Thanks

There is no intrinsic value before the expiry. The value of the option (premium) is essentially the difference between the buy and sell price of the premium. So if you buy an option at 25 and sell at 30, the P&L is 5.

That’s the P&L calculation upon expiry. But what about the IV calculation during the series?

You have mentioned in the section 5.3 —-> “However, the calculation of the intrinsic value of an option

is different during the series. Of course, we will understand how to calculate (and the need to calculate)

the intrinsic value of an option during the expiry.”

My questions are :

1. What is the formula to calculate the IV during the series?

2. You said need. So what’s the need to calculate the IV during the series?

Sandeep, please check the previous reply.

That\’s the P&L calculation upon expiry. But what about the IV calculation during the series?

You have mentioned in the section 5.3 —-> \”However, the calculation of the intrinsic value of an option

is different during the series. Of course, we will understand how to calculate (and the need to calculate)

the intrinsic value of an option during the expiry.\”

My questions are :

1. What is the formula to calculate the IV during expiry?

2. You said need. So what\’s the need to calculate the IV during the series?

1) There are mathematical models to forecast volatility. A few models are GARCH (1,1) GARCH (1,2) etc.

2) To take positions, especially options based on your expectations of volatility.

Dear Karhik sir,

We know that IV = Spot-Strike for CE buyer and Strike – Spot for PE buyer And P&L = IV-Premium. But

in section 5.4 you have mentioned that the calculation of IV and P&L is done using a different formula

when you close the option trade before expiry. What are those formulae? Please let me know.

Thanks

If you close the trade before expiry, then its the difference between the buy and sell price of the premium.

If i sell a put option and its ITM on expiry do i need to purchase the stock or it will be automatically assigned to me….also if i sell call option and its ITM on money on expiry do i need to give the stock or it will be deducted from my demat account automatically …

The settlement will happen automatically provided you have the necessary cash and stock in your account.

I BOUGHT put options at Strike price of 16300 in Nifty. Nifty closed at 16209. My premium was 9.35 rupees, it is now at Rs. 60 at close. But when I tried to sell, I was required to add 97000 rupees to my demat. Why is that?

You must have other open F&O positions (maybe long futures) which would have got hedged with your puts. When you close your puts the other F&O position will need full margins, hence 97K.

Hello sir

Thank u bcoz of ur clear explanation I got knowledge regarding to options but I have some doubts

1 if any one who is bearish view on market can they will go for call option sell then what is neseccary for put option buy

2 if I take any option sell position I get the premium amount . immediately we receive premium amount or on expiry

1) Call option sell requires margins

2) You get it immediately.

The PUT buyer makes the highest profit when the spot price is zero on the day of expiry, which means that the maximum profit the put buyer can make is=Strike Price – premium and rather not unlimited.

Yes, but think about the stock price going to 0 and its impact on your margins.

Sir can we sell the put option only when the spot price is below the strike price.

As we can buy the put option of strike price 500 at a premium of rs-5 and the on the day of expiry the spot price of share is 600.then can\’t we sell it for 600.

bcz it will also be profitable if we can.

Or maybe I am little bit confused.

Will you tell me one thing that:

1.Buying an put option gives us right to sell the underlying. Or

2.Buying an option gives us right to sell the underlying at defined strike price.

Buying the put option gives you the right to sell the underlying at the strike price. Also, you can buy and sell options anytime, no need to wait till expiry.

First of all, thanks a lot for this content sir.

Today motherson sumi fell about 20% because of demerger & some of put option were up by almost 40000%.

Sir if everybody knew it is going to fall today this huge, then why the put options became rockets.

I am very curious to know the reason. Please reply as soon as possible.

The contracts would be adjusted accordingly, Anupam. There is no free money in the markets 🙂

Check this – https://zerodha.com/marketintel/bulletin/313884/adjustment-of-futures-and-options-contracts-of-mothersumi

Yes, there will be liquidity problem. If you do not have sufficient balance, auto-exit will take place at any time. However, if you have sufficient balance and call/put ended out of the money i.e zero and you did not execute exit order, no problem will be there.

Suppose I have sold the option it can be call/put, and at the time of expiry day, suppose I didn\’t execute the exit order, then what will happen, also suppose I am profit and premium is very near to 0, then who will execute that order, will there be liquidity problem?

There is nothing to worry about if the option is OTM. But if the option is ITM, then it will be physically settled.

Sir please immediately contact please

Hi great learnings.

One question on this chapter , infact prior one also – why have you called put shorting future more risky compared to buying PUTS ? After all arent both leveraged instruments ? Infact ‘I can still see some merit here because shorting can theoretically lead to unlimited losses(i.e till underlying reaches zero from CMP). But how is buying CALL option in any way less riskier than buying the future ? Only drawback I can see with Future is high margin requirement

Hmm, its not just about margins Himanshu. With futures, the only thing that impacts the price is the directional movement. But in Options, it is a lot more variables. Also, panic spreads faster than greed in the markets. So when you write a put, the chances of it going haywire is higher.

What if we buy a call option of Strike Price less than Spot Price?

YOu can, that would be ITM if its a call option.

Hi ,

I needed a more clarity in case of OTM Put buying of some stock like HUL or TCS ….weather it\’s necessary to take the delivery if the PUT becomes ITM at the day of expiry,

Regards

Anupam Pandey

Necessity depends on your intent right? If you feel you dont need the stock in your DEMAT, then square off the position before expiry.

Can you please cover Put selling and taking stock delivery

There is nothing much to cover there. Its the physical delivery of options, we have discussed that in the last chapter.

Hi Sir,

First of all thank you so much for this teaching. I tried many times before to understand options but never understood it enough to start trading. So, continued traditional stock trading. Now, I started to understand a bit.

Above, you mentioned that, we are buying put instead of shorting future –

\”9.However shorting futures maybe a bit risky as the overall market is bullish, it is only the banking sector which is lacking lustre\”

I understand that you mean to keep limited risk while shorting, buying put is better than shorting future. Is that correct? as if price do go down then will make money on shorting future as well but in case it goes up then there is limited risk with buying put.

Thanks.

Jay, thanks for the kind words. Each of these financial instruments have its own risk and reward profile and its not like one is better than the other. While both are risky, you need to figure the which one is a better bet given the situation in the market. For example, if volatility is very high and I expect volatility to increase, then I\’m rather comfortable selling options.

Mr. Karthik,

Enjoying your wonderful explanation on the different aspects of options trading, and I emphasise here that it is a must read for a person planning to enter this territory. Thanks a lot!

Regards

Sunil Arab

Glad you liked it, Yeshwant! Happy reading 🙂

For example I buy nifty call CE15000 strike price 1 lot at premium 100rs ( 1 lot is 50 quantity which is 50×100 = 5000 i pay 5000 premium to buy CE15000 strike price ) so according to P&L(iv+premimum) stock price is to move 5000 point higher to gain profit. Which is P&L= Max (0, 15000 – 16000) – 5000 = 0 now stock price is 100 point high which is 5000+100 =5100 so P&L= Max (0, 15000 – 16100) -5000 = 100 now i gain profit, in that term if to gain profit we need higher point then premium price which is 5000 point. Am i right these assumption act on real stock market.

Miraz, the profit or loss that you make when you buy an option is the difference between the buy and sell price of the premium, multiplied by its lot size. For example, if you buy an option at 100, sell it at 110, then you make 10 points multiplied by its lot size.

Hi..I have one doubt. If i have put option let say @310 strike price and on expiry CMP of share is 300 then

1. whether I will get exactly 10 rupee without selling put option on expiry.

2. It will settled by delivery. For example if I have shares in my demat account then sell transaction will initiate automatically or I have to inform to broker for initiating a transaction.

Thanks

1) Yes

2) It will be settled physically provided your option is ITM

In the BANKNIFTY example above you said, \”However shorting futures maybe a bit risky as the overall market is bullish, it is only the banking sector which is lacking lustre\”. Can you please tell the rational behind that as this index is also only of banks so how futures are riskier than options.

The overall market sentiment has an impact on your positions. Hence.

Hello sir…

Just wanted a clarification regarding new amendments in Investment Advisor qualifications. If one has a post graduate degree in finance then 5 years of experience certificate is needed or not. And if needed then what type of experience certificate is considered valid? Please advise.

I\’d suggest you check with SEBI directly for this, I\’d not be the right person to advice on this 🙂

Thanks.

Thank you so much karthik

Good luck, Dinesh.

Hi karthik

first of all thank you for the kind reply

my doubt is

well as you said exercising the option happens only on the expiry, but while reading i came across this line \’\’Of course the P&L formula is applicable only if the trader intends to hold the

position till expiry\’\’

Does this mean he can square off the position even before expiry if he intends to (which is opposed to European model).

please clear my doubt

Thank you

Yes, Dinesh. A trader can sell the position anytime he/she wants before the expiry.

Hi Karthik,

You have mentioned that indian derivatives market follows european model so that buyer of the call option can exercise the right to buy only at expiry and not before the expiry day

I am clear with this

But when I continue further i can also see that \”suppose in morning if i bought call option at a premium of 6 rs and after sometime if premium is trading at 9 rs one can sell it\’\’

My doubt is \’\’is it compulsory for the the call/put option buyer to exercise their right only at expiry day or they can do it on any day before the expiry day

That is if am buying call/put options on 9/6/2021 which expires on 24/6/2021. can i exercise my right to buy even before expiry(say 16/6/21) if the situation is in my favour.

please do clear my doubt

correct me if i am wrong

Thank you.

Dinesh, yes, exercising the option happens only on the expiry day, however, if you wish to buy and sell the option premium, you can do that anything you wish and need not wait till expiry.

hey Kartik,

Im a newbie to options and just loving the way you have made these concepts easily understandable. Have been able to understand the concepts of call and put well so far. Hopefully will start trading in options in few months time.

Thanks for the great content. appreciate your efforts

Happy to note that, and I\’m glad you liked the content. Good luck, Lakshmi 🙂

Hello Sir , i was just wondering how are the volume data generated on indices in chartink.com and not on other platforms bcoz indices are not traded directly.

Ah, you need to check with them. I\’m not sure what they are using.

I am planning to place an AMO for nifty 14400 put option but its showing that this option is BLOCKED with a message displayed as (Buy Orders in the following strikes may not go through due to restrictions from the exchange. These do not apply if you are exiting your existing positions.)

what does this mean and what should I do and the msg is showing only for 14400 put option and for all the OTM strikes below it

Strange, its going through for me. Do check this https://support.zerodha.com/category/trading-and-markets/kite-web-and-mobile/holdings/articles/index-options-amo-rejection#:~:text=Your%20index%20option%20AMO%20will,option%20in%20index%20option%20AMOs.

Hi Karthik,

Is exiting the put and selling a put same thing?

I mean, suppose I buy a put at X premium and exit it at a higher Y premium, is it exiting the option (no obligation like selling the option) or it is considered as selling the option (with obligation)?

To exit a position means that you are closing that position. For a long position, exit implies sell. For a short position, exit implies buying back. Selling a put means you are creating a new short position.

If you buy at put at X, its exit position is to sell the same option at Y.

Hi,

I had bought the 7 lot nifty 14900pe Apr monthly series. Nifty closed at the 14894. So how charges and settlement will be calculated?

The Option has a very little intrinsic value i.e. 6 Rupees. Not sure if exercising this will be of any use, hence mostly the strike is considered worthless.

Hello Karthik sir,

I really appreciate your consistent and prompt response to all the queries and admire it.

My question is what is the purpose of one buying a put option of higher strike price ?

There could be many reasons, really depends on the market condition right?

Hello!

Love the content. It was mentioned in Futures lesson that if a portfolio(the example given was Rane Holdings I think) is worth less than one nifty futures contract, it can\’t be hedged using futures but there is another way which will be explained in the options module. I didn\’t come across such explanation in the options module. I\’m guessing that long nifty puts or short nifty calls might have something to do with that but can you please explain EXACTLY how it\’s done in your way – i.e. using examples and payoff charts etc? Thank you

Its essentially boils down to buying puts, that\’s it 🙂

Thank you so much Karthik….

Good luck!

Hello Karthik, Assuming I have bought a call or put option..I have sold the option on the expiry day which has an intrinsic value by booking the profit…… After selling the option ., Suppose if the intrinsic value increase.Will there be any loss…??? ..

Below is what I have understood …

As I have paid the premium I have the right to sell the options at anytime., The maximum loss after selling the options is restricted to my premium ..

Plz do reply… THANK YOU.

Once you sold the option, it does not matter where the option goes. You are out of the market anyway.

Point noted Sir. Also thank you very much for what you\’ve done for me as well as countless other people by teaching us the method in this madness called the stock market. Take a bow.

Happy learning, Prashant.

Sir! In the aforementioned Bank Nifty example, you\’ve said (in points 9 & 10) that shorting Futures maybe a bit risky as the overall market is bullish. It is only the banking sector which is lacking lustre. Hence buying a Put Option on the Bank Nifty may make sense.

One buys a Put option when one is outright bearish on an underlying and buying a Put option is akin to shorting Futures. If you aren\’t shorting Bank Nifty Futures here because the overall market is bullish, then it means you think that Bank Nifty might either stay flat or go down. In such a scenario wouldn\’t selling a Call option be a more prudent choice than buying a Put option?

The decision to buy Put or sell call depends on the volatility and the associated premium, Prashant.

thanks got it.

Good luck!

Karthik Am repeating the question since you have missed answering earlier although It may sound stupid . On the nifty option page there are both on the call side and the put side there are Bid Price and Qty and also Ask Price and Qty .and also the Last traded price . How do we know what is lot size for call and put Options as the Trade page seems confusing

Chacko, the page you are looking at is the Options chain of a contract. But you need to look at the contract page, for example, here is the contract page of Infy, which has all details including the lot size information – https://www.nseindia.com/get-quotes/derivatives?symbol=INFY

Can i buy put options one day before ex dividend date and close with a profit on the ex dividend date?? Does it work?

Please check this – https://www.instagram.com/p/CLqi2XdHvvc/?igshid=opbzeklkza6y

A very basic question . Both on the call side and the put side there are Bid price and qty and Ask price and Qty . Also the the Last traded price . How do we know the lot size for for call and put as it seems confusing.

Ok got it sir Thanks for the quick response sir

Good luck!

Hello kartik you mentioned that an option seller is exposed to an unlimited risk but i think it is true only for a call option seller as the trade goes against him on expiry and the underlying can move to infinity(theoretically) resulting in an infinite loss for the call option seller however for a put option seller the risk is limited to an extent where the underlying reaches zero theoretically. Am i right?

Thats right, Krishna. But last year around April, crude oil traded at -ve prices, wherein Put sellers lost a lot more.

Thank you

Hi Kartik,

Awesome content and explanation.

I am very confused with shorting options.

When some one says he is shorting option, is he shorting for the difference in premium or the difference in value of underlying asset?

When you are shorting you are selling first and buying later. So I am expecting that the value of whatever I am shorting is going to go down. If I am shorting option, today\’s premium will be high and when I am closing my position I expect the premium has gone down.

Please clarify with respect to both Call and Put and if possible in both buy and sell cases.

Thanks in advance. You are doing amazing work Kartik.

Deepak, shorting is essentially that, i.e. sell first and buy back later. YOu will make a profit if the asset price that you shorting goes lower than your short price. Else you will make a loss. When someone shorts an option, then they expect the premium to go lower, and they will make a profit if the buy back the option at that lower price.

I have bought put nifty 50 @11.15 with expiry on 4 th February (14000PE) and I have paid premium amount of rs 826.25…now the nifty50is at 14800 …what will be the maximum loss of me on the expiry day ..

The maximum loss is restricted to the extent of the premium you\’ve paid.

Thank you sir.

Good luck!

Dear sir,

I have a simple query.

As per the new rule, we have to take the physical delivery or exercise the FNO trade of the stock if we hold the trade until expiry. My question is what will happen if we buy or sell option of Index like Nifty 50 and hold it till Expiry?

Please clarify.

Index contracts are cash-settled, Ankit.

what will happen if banknifty trades @18415

Are you serious ? I am C.A by profession. I have never seen this detailed and so easy with full heartedly explanation of options understanding anywhere. This is a true treasure . I am very thankful for this beautiful understanding.

Thanks a lot!

Thanks for the kind words, Nidhi. Happy learning 🙂

Good morning sir.

Sir i bought put option of one stock when premium @ rs. 1.50 but before expiry it becomes zero. What will happend at the time expiry.

That means to say that option expired worthless.

Dear Karthik,

I have read the call option buying and selling part of the module. It was easy to understand because you have given the example of land between Ajay and Venu, which helped to understand the call option very well. I did not understand why you have not given the real time or real life example in the put option. I am requesting you to give the real life example for put option to understand the concept pretty well.

Thanking You,

The problem is drawing an analogy with PUT options to real life is very difficult because these are transactions that we don\’t really carry outside the market 🙂

1) The thought process is to trade the underlying. For example, RIL is at 2000, I expect it to go down to 1825, so I buy the 1900 PE at whatever price. I will cut the losses if RIL hits 2100 at whatever premium.

ALSO IN THE ABOVE SCENARIO I WOULD BE ABLE TO EXIT ONLY IF I HAVE ENOUGH MARGIN THOUGH DELIVERY OR INTRADAY………WHAT IF DONT HAVE ENOUGH MARGIN…FOR INTRADAY IT WILL SQUARE OFF………………………WHAT IF I BUY SOME XYZ OPTION 3RS PREMIUM 1000 QUANTITY (3000) RS AS DELIVERY AND MY ACCOUNT FUNDS ARE 10000………………….WHAT HAPPENS IN BOTH PROFIT AND LOSS CASE………..WHAT MY UNDERSTANDING…IF IN DELIVERY I CAN TAKE MY PROFITS AND EXIT IT BEFORE EXPIRY ALSO…. FUNDS OF 10K WONT BE ISSUE …. WHAT HAPPENS IF IN LOSS?

Your trade won\’t go through if you don\’t have sufficient margins, Mosmi.

HELLO KARTHIK SIR,

I HAVE THIS QUESTION RECENTLY I TOOK A OPTION CALL OF HDFC @ 23 WHICH WAS 550 QUANTITY REQUIRED 12650 BUT I TOOK IT AS INTRADAY(WHICH WAS MY MISTAKE AS I WANTED TO TAKE IT FOR DELIVERY) WHEN IT STARTED GOIN IN LOSS I TRIED EXITING BUT COULDNT AS IT DEMAND MARGIN OF 66K MA ACCONT HAD AROUND 30K…..(As and when the stock starts moving in the opposite direction of the seller, the broker would demand more margins from the seller.)>>>>SECONDLY WAT IF I WOULD HAVE TAKEN IT IN DELIVERY N EXIT WITH PROFIT… IT WOULDNT HAVE REQUIRED EXTRA MARGIN AS I WAS IN PROFIT N I COULD HAVE EXITED IT WITH WATEVER FUND I HAD IN MA ACCOUNT. RIGHT??????

Yes, margin requirements go up if the position moves against you. There is no concept of delivery in options right?

Follow up question,

In NSE website, where we have option chain I can see a legend which says \’highlighted options are in-the-money\’. The chart is divided into 2 parts horizontally i.e. white background data and yellow background data.

From what I understand yellow background data options already surpassed the current market price but still I could buy those options, how does it make sense to buy?

Same Reliance eg. where CMP is 1993.25 so why will someone buy Nov 1980 CE when CMP is already above that price?

I\’ve explained this in the moneyness of options chapter.

Hi Karthik,

1. In many comments I read you are suggesting to place SL for the underlying instead of option premium. But when I try to buy the option premium let\’s suppose Reliance Nov 2000 CE, I can only place a SL for premium price. How can we relate that spot market price as SL in trading terminal?

2. You mentioned shorting futures is risky since only bank sector is effected whereas remaining sectors are good, in that case we can short bank nifty also right? So buying option put or shorting bank nifty futures both are good options is what I feel?

3. One important observation I made and need your inputs. Why would anyone short either call option or put option where risk is higher, returns are less and premium is higher?

For eg. consider Reliance – 1993.25 (CMP)

Suppose I have bullish view then

RELIANCE NOV 2000 CE has premium 54.65 and lot size is 505 so total = 27,598.25

Same can be done by shorting RELIANCE NOV 1980 PE which has premium 46 and lot size is 505 but total margin required is 78K

Same goes for bearish view as well, so my point is why would anyone short the option call or put? I don\’t understand the advantage here.

1) The thought process is to trade the underlying. For example, RIL is at 2000, I expect it to go down to 1825, so I buy the 1900 PE at whatever price. I will cut the losses if RIL hits 2100 at whatever premium.

2) Yes, but please see the context in which I\’ve mentioned this

3) The decision to short comes from how expensive the option is compared to its real value

Hi

Can I buy PE NRML option today and sell it today, rather than waiting till expiry.

Yup, you can.

Sir,

I want to ask here very egarly that i have bought a call option before expire it is profitable and i sell that call it is well settled there or as you said before …..call option buyer risk limited and sell risk unlimited formula applying till expiry.

Hopefully u understand.

Not sure if I fully understand your query, but yes, you can sell the profitable call before expiry, no need to wait for expiry.

First of all, that was some great explanation, now what if I buy the BANKNIFTY 17500 PUT 30 April Expiry, could you share a chart as you shared in the end to understand that scenario, it will be a great help to understand the concept further.

I\’d suggest you use the pay off from Sensibull – https://sensibull.com/

Hi

I took Muthootfin 29 Oct PE 1000 as per angel broking recommendation in research window in the app. now I have doubts, please clarify.

As per the recommendation given \”short term stock option buy Muthootfin OCT PE 1000 @ 56-58 SL 44 target 80\”.

I bought on 24 sep2020 @ 29 rupees. Now the share is only 14+ , what will be the scenario now.

Suppose it goes still less (eg: 2 rupees at 2nd Oct. What will be my loss….how to overcome this situation. Please explain.

Still I m holding the stock, is there any major loss ahead or shall I keep continue till the expiry. Please help in this regard.

I am new to derivatives section, few I bought, I lost it because of unawareness. Please help me or can you share any information about these NSE derivatives. Any contact person no. Or any youtube or by any means.

Since I have plenty of questions to ask about derivatives. I like derivatives but it is risky unless if I don\’t understand properly, please help me in this regard.

Regards

Saravanan

The recommendation was given with an expectation that the stock price will fall, but that has not happened. Hence you are likely to lose the premium you\’ve paid. If you square off the position @ 14, then your loss will be the 56-14*lot size.

Please don\’t fall for stock tips and recommendations. Instead, try to learn and do your research on your own.

then why was CE not expensive sir

why only PE.

thank u sir

Volatility plays a part right?

Hello Sir,

On 24th September ( Expiry Day )

I just checked the price of following strike price ( for study purpose )

BAJFINANCE 3200 CE = 0.05 Rs

BAJFINANCE 3800 PE = 115 Rs

Spot was around 3050 Rs

Lot size is 250.

Now, when I clicked on Buy for CE, amount required was 12.5 Rs (250*0.05) fair enough,

but when I clicked on Buy for PE, amount required was something around 4.3 lakhs.

and we have learned contract value is lot size * premium , which I think should be around ( 250*115 ) =28750 Rs.

why buying PE was so expensive sir.

Thanks.

Regards

Thats because you are trying to buy close to expiry, at which point the margin requirements go significantly up owing to physical settlement.

Hello sir,

My question:

If I have a directional bullish view towards Nifty for tomorrow. Assuming Nifty is trading at 11500. What strike call option should I go for? (ITM,OTM OR ATM, please give me eg wrt the strike price). For intraday.

Ryan

Considering you are bullish and there is ample time to expiry, you can look at slightly OTM options.

Sir, If I buy put(PE) option at a particular strike price and sell it immediately at a price which is below the strike price,

1)Then be the p/l = difference between the buy/sale premium ?

2) Or will I lose the whole premium (bought) ?

1) Yes, that is correct

2) You would, if this was the case on expiry day.

Sorry to bother further. Can you pls elucidate a bit with an example ?

For example, let\’s say you hold a 100 strike CE and the spot expires at 110. On expiry, the premium\’s LTP would be 11.50/-. Now since the option has expired, your P&L is the intrinsic value of the option i.e 10 and not the LTP which is 11.5/-.

Hi ! I have a doubt reg Expiry of Put Option.

Suppose I bought a Put option for Strike Price of 100 at a premium of Rs. 5 and on the day of expiry the Spot price is 120. So, obviously, I will NOT sell the underlying to the Seller of the Opotion. In that case how will be the transaction settled ? (Drawing a parallel to Buying of Call option, the shares will be sold in open market and the transaction is settled. How will this be done in case of a Put option)

On expiry, all options have to be settled at the prevailing settlement price. So there is no other way 🙂

Okay Karthik ji thank you 🙂 …I think I need to read and learn more to clear the doubt.

Happy reading, Atul!

…now I got it this logic.

But my confusion is still in 6th Aug expiry, it should start from 17th July, but in chart we can see the price movement from 13th Aug itself ! can you please explain how and when this 6th one started ? And why chart showing prices before 17th ?

These are weekly contracts Atul, they get introduced the same way as the monthly do.

Karthik ji,

1. Some confusion in index option contract expiry (NIFTY and BankNify), like in both index, weekly expiry happens every Thursday, so I want to know when a new contract starts ? on every Friday (after expiry of current on Thursday) ? or before Friday also ? how it works ?

Right now I am checking \”NIFTY 6th AUG 11000 CE\”… 6th Aug is expiry, but on chart its price movement started on 13 July itself ! so quite confusing! please let me know. Thank you.

So we are in Aug 2020 now. At this point, you will have Aug, Sept, Oct contracts available to trade. When Aug contracts expire, November contracts are introduced. So at any point, you have 3 contracts available to trade. So when Aug expires, the immediate next day Nov contracts are introduced.

Hi Karthik ji … please accept my appreciation and BIG thank You!!! …you are replying everyone\’s query and helping them and guiding, almost without fail ! this is really really very helpful for learners!

We are very much thank full to you 🙂 Great Job ! keep it up ! 🙂

Thanks for the kind words, Atul! Happy reading 🙂

Karthik – Thank you for reverting so quickly. I have certain Questions, kindly help me understand and I hope you help me understand on below.

1. So, if the Postion moves from 7 to 9, i take profit of 2400, I understand that if it moves against(my price @7) eg5, I will loose 2400. What about my premium which paid in both the cases. Do i get my premium back along with profit in 1st case.

2. What happens if i hold it till expiry in this case if the position pricing @ 13 as an example. kindly hep me understand.

1) Yes, you get back the premium. The worth of the premium is dependent on the price of the premium

2) If you hold to expiry, what matters is the intrinsic value of the option. Which I\’ve explained across the module.

Dear Karthik,

One Query, i\’m new to options, Ive bought a Infy AUG 850 PE put @7 with premium 8400 (1200 Units). If my order moves higher than my strike price eg @9, I Sell it and pocket 1200*2=2400, Do i get my Complete premium+2400 profit or I\’ll be at loss as the price must move about 14 to start my profits..I still have a doubt that I would be in profit @break even 14 + above price. Kindly Answer..

Nageshwar, you will get Rs.2400/- as profit.

Hello sir,

Firstly many thanks for the beautiful content you have put up here; trying to explain the most complex topics in a very lucid manner. Amazing effort!

Sir actually i wanted to know in the example of 18400Bank Nifty PE, if upon expiry the underlying is trading @18300 then will trade still get executed(trader minimises loss to 215)?

Thanks.

Yes, upon expiry this trade will get settled and the P&L will get attributed to the trader.

It means that I will lose money if it expires itm? Right?

Also is it a rule that indices are cash settled of the exchange or its a Zerodha policy?

Brokers cant come out with these policies, we have to follow rules set by the exchanges. Yes, indices are cash-settled.

Sir my question is regarding Nifty…. Suppose I sell 10500 and 21000 put option in nifty and Bank Nifty and both of them expire in the money… how will the options be settled? I read somewhere on zerodha that it will be cash settled but I also so read somewhere that we can buy the Nifty shares if the options expire in the money…. Please provide an accurate answer

No, indices are cash settled. Physical delivery is only for stock options.

yes, got it sir.

Seem that is weekly option contract sir, but we\’ve discussed only monthly expiry 🤔

The working of the option remains the same, Mano. Nothing changes.

https://imgur.com/a/WRTsePp

Kindly refer this image sir,

how come the put option premium varies from the option chain and the order window?

Am I missing anything, sir?

Buyer need to pay only the (premium*lot size), am I right sir?

You may be seeing two different expiries.

Hello sir, am a newbie who has been quite intrigued by the course content and your method of explanation(phenomenal to say the least). I just had one doubt, what i have seen so far in the options module is that the P&L formulated is based on the assumption that investors are loss averse. So you mention that a put buyer will not exercise the put option in case the value of the underlying asset is above the strike price. However, he may as well exercise such a loss making deal if he immediately needs some bit of loss elsewhere(where windfall gains have taken place-again the rationality of this could be countered-but let\’s just assume he wants to avoid some sort of tax scrutiny), so he\’s ready to sell the underlying at the strike price(way below the spot price) and incur a loss, instead of simply letting the put option lapse. So essentially something like this is allowed, right? Or he would be barred.

I get your point of carrying forward a loss to offset the gains in equity. However, a PUT option (or even a call option), does not really get exercised if it has no intrinsic value, it is technically not possible.