9.1 – Overview

Yesterday I watched the latest bollywood flick ‘Piku’. Quite nice I must say. After watching the movie I was casually pondering over what really made me like Piku – was it the overall storyline, or Amitabh Bachchan’s brilliant acting, or Deepika Padukone’s charming screen presence, or Shoojit Sircar’s brilliant direction? Well, I suppose it was a mix of all these factors that made the movie enjoyable.

This also made me realize, there is a remarkable similarity between a bollywood movie and an options trade. Similar to a bollywood movie, for an options trade to be successful in the market there are several forces which need to work in the option trader’s favor. These forces are collectively called ‘The Option Greeks’. These forces influence an option contract in real time, affecting the premium to either increase or decrease on a minute by minute basis. To make matters complicated, these forces not only influence the premiums directly but also influence each another.

To put this in perspective think about these two bollywood actors – Aamir Khan and Salman Khan. Movie buffs would recognize them as two independent acting forces (similar to option Greeks) of Bollywood. They can independently influence the outcome of the movie they act in (think of the movie as an options premium). However if you put both these guys in a single flick, chances are that they will try to pull one another down while at the same time push themselves up and at the same time try to make the movie a success. Do you see the juggling around here? This may not be a perfect analogy, but I hope it gives you a sense of what I’m trying to convey.

Options Premiums, options Greeks, and the natural demand supply situation of the markets influence each other. Though all these factors work as independent agents, yet they are all intervened with one another. The final outcome of this mixture can be assessed in the option’s premium. For an options trader, assessing the variation in premium is most important. He needs to develop a sense for how these factors play out before setting up an option trade.

So without much ado, let me introduce the Greeks to you –

So without much ado, let me introduce the Greeks to you –

- Delta – Measures the rate of change of options premium based on the directional movement of the underlying

- Gamma – Rate of change of delta itself

- Vega – Rate of change of premium based on change in volatility

- Theta – Measures the impact on premium based on time left for expiry

We will discuss these Greeks over the next few chapters. The focus of this chapter is to understand the Delta.

9.2 – Delta of an Option

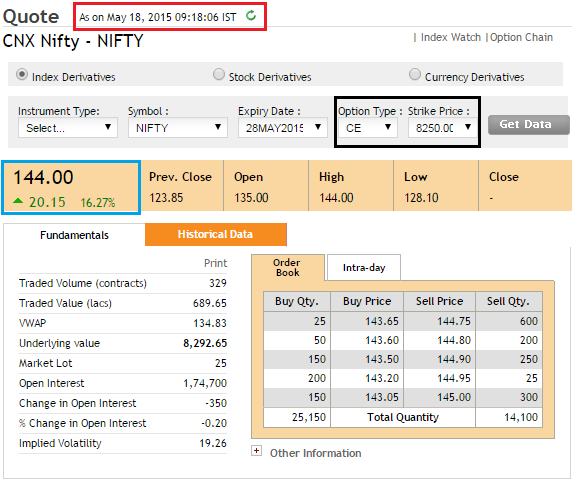

Notice the following two snapshots here – they belong to Nifty’s 8250 CE option. The first snapshot was taken at 09:18 AM when Nifty spot was at 8292.

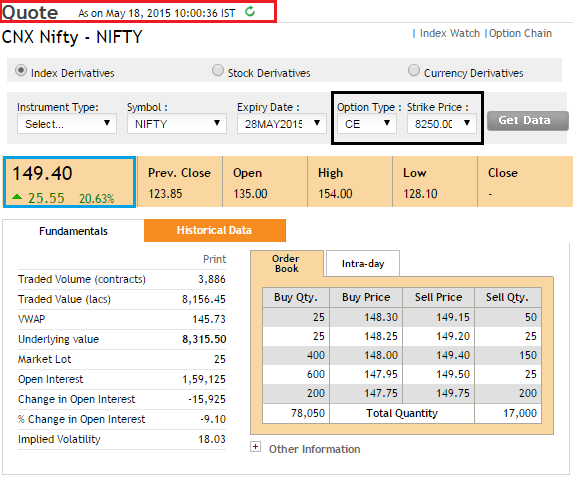

Now notice the change in premium – at 09:18 AM when Nifty was at 8292 the call option was trading at 144, however at 10:00 AM Nifty moved to 8315 and the same call option was trading at 150.

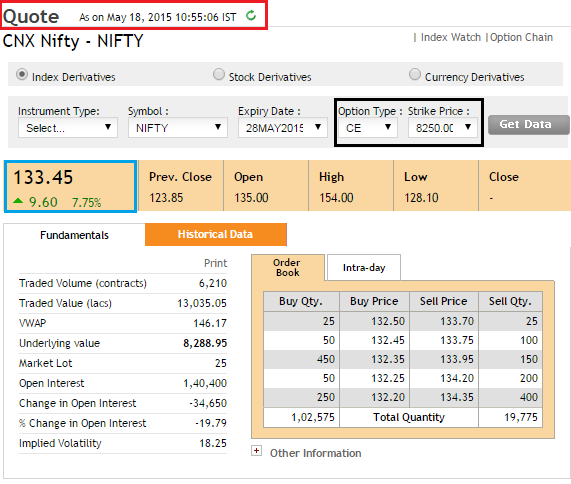

In fact here is another snapshot at 10:55 AM – Nifty declined to 8288 and so did the option premium (declined to 133).

From the above observations one thing stands out very clear – as and when the value of the spot changes, so does the option premium. More precisely as we already know – the call option premium increases with the increase in the spot value and vice versa.

Keeping this in perspective, imagine this – you have predicted that Nifty will reach 8355 by 3:00 PM today. From the snapshots above we know that the premium will certainly change – but by how much? What is the likely value of the 8250 CE premium if Nifty reaches 8355?

Well, this is exactly where the ‘Delta of an Option’ comes handy. The Delta measures how an options value changes with respect to the change in the underlying. In simpler terms, the Delta of an option helps us answer questions of this sort – “By how many points will the option premium change for every 1 point change in the underlying?”

Therefore the Option Greek’s ‘Delta’ captures the effect of the directional movement of the market on the Option’s premium.

The delta is a number which varies –

- Between 0 and 1 for a call option, some traders prefer to use the 0 to 100 scale. So the delta value of 0.55 on 0 to 1 scale is equivalent to 55 on the 0 to 100 scale.

- Between -1 and 0 (-100 to 0) for a put option. So the delta value of -0.4 on the -1 to 0 scale is equivalent to -40 on the -100 to 0 scale

- We will soon understand why the put option’s delta has a negative value associated with it

At this stage I want to give you an orientation of how this chapter will shape up, please do keep this at the back of your mind as I believe it will help you join the dots better –

- We will understand how we can use the Delta value for Call Options

- A quick note on how the Delta values are arrived at

- Understand how we can use the Delta value for Put Options

- Delta Characteristics – Delta vs. Spot, Delta Acceleration (continued in next chapter)

- Option positions in terms of Delta (continued in next chapter)

So let’s hit the road!

9.3 – Delta for a Call Option

We know the delta is a number that ranges between 0 and 1. Assume a call option has a delta of 0.3 or 30 – what does this mean?

Well, as we know the delta measures the rate of change of premium for every unit change in the underlying. So a delta of 0.3 indicates that for every 1 point change in the underlying, the premium is likely change by 0.3 units, or for every 100 point change in the underlying the premium is likely to change by 30 points.

The following example should help you understand this better –

Nifty @ 10:55 AM is at 8288

Option Strike = 8250 Call Option

Premium = 133

Delta of the option = + 0.55

Nifty @ 3:15 PM is expected to reach 8310

What is the likely option premium value at 3:15 PM?

Well, this is fairly easy to calculate. We know the Delta of the option is 0.55, which means for every 1 point change in the underlying the premium is expected to change by 0.55 points.

We are expecting the underlying to change by 22 points (8310 – 8288), hence the premium is supposed to increase by

= 22*0.55

= 12.1

Therefore the new option premium is expected to trade around 145.1 (133+12.1)

Which is the sum of old premium + expected change in premium

Let us pick another case – what if one anticipates a drop in Nifty? What will happen to the premium? Let us figure that out –

Nifty @ 10:55 AM is at 8288

Option Strike = 8250 Call Option

Premium = 133

Delta of the option = 0.55

Nifty @ 3:15 PM is expected to reach 8200

What is the likely premium value at 3:15 PM?

We are expecting Nifty to decline by – 88 points (8200 – 8288), hence the change in premium will be –

= – 88 * 0.55

= – 48.4

Therefore the premium is expected to trade around

= 133 – 48.4

= 84.6 (new premium value)

As you can see from the above two examples, the delta helps us evaluate the premium value based on the directional move in the underlying. This is extremely useful information to have while trading options. For example assume you expect a massive 100 point up move on Nifty, and based on this expectation you decide to buy an option. There are two Call options and you need to decide which one to buy.

Call Option 1 has a delta of 0.05

Call Option 2 has a delta of 0.2

Now the question is, which option will you buy?

Let us do some math to answer this –

Change in underlying = 100 points

Call option 1 Delta = 0.05

Change in premium for call option 1 = 100 * 0.05

= 5

Call option 2 Delta = 0.2

Change in premium for call option 2 = 100 * 0.2

= 20

As you can see the same 100 point move in the underlying has different effects on different options. In this case clearly the trader would be better off buying Call Option 2. This should give you a hint – the delta helps you select the right option strike to trade. But of course there are more dimensions to this, which we will explore soon.

At this stage let me post a very important question – Why is the delta value for a call option bound by 0 and 1? Why can’t the call option’s delta go beyond 0 and 1?

To help understand this, let us look at 2 scenarios wherein I will purposely keep the delta value above 1 and below 0.

Scenario 1: Delta greater than 1 for a call option

Nifty @ 10:55 AM at 8268

Option Strike = 8250 Call Option

Premium = 133

Delta of the option = 1.5 (purposely keeping it above 1)

Nifty @ 3:15 PM is expected to reach 8310

What is the likely premium value at 3:15 PM?

Change in Nifty = 42 points

Therefore the change in premium (considering the delta is 1.5)

= 1.5*42

= 63

Do you notice that? The answer suggests that for a 42 point change in the underlying, the value of premium is increasing by 63 points! In other words, the option is gaining more value than the underlying itself. Remember the option is a derivative contract, it derives its value from its respective underlying, hence it can never move faster than the underlying.

If the delta is 1 (which is the maximum delta value) it signifies that the option is moving in line with the underlying which is acceptable, but a value higher than 1 does not make sense. For this reason the delta of an option is fixed to a maximum value of 1 or 100.

Let us extend the same logic to figure out why the delta of a call option is lower bound to 0.

Scenario 2: Delta lesser than 0 for a call option

Nifty @ 10:55 AM at 8288

Option Strike = 8300 Call Option

Premium = 9

Delta of the option = – 0.2 (have purposely changed the value to below 0, hence negative delta)

Nifty @ 3:15 PM is expected to reach 8200

What is the likely premium value at 3:15 PM?

Change in Nifty = 88 points (8288 -8200)

Therefore the change in premium (considering the delta is -0.2)

= -0.2*88

= -17.6

For a moment we will assume this is true, therefore new premium will be

= -17.6 + 9

= – 8.6

As you can see in this case, when the delta of a call option goes below 0, there is a possibility for the premium to go below 0, which is impossible. At this point do recollect the premium irrespective of a call or put can never be negative. Hence for this reason, the delta of a call option is lower bound to zero.

9.4 – Who decides the value of the Delta?

The value of the delta is one of the many outputs from the Black & Scholes option pricing formula. As I have mentioned earlier in this module, the B&S formula takes in a bunch of inputs and gives out a few key outputs. The output includes the option’s delta value and other Greeks. After discussing all the Greeks, we will also go through the B&S formula to strengthen our understanding on options. However for now, you need to be aware that the delta and other Greeks are market driven values and are computed by the B&S formula.

However here is a table which will help you identify the approximate delta value for a given option –

| Option Type | Approx Delta value (CE) | Approx Delta value (PE) |

|---|---|---|

| Deep ITM | Between + 0.8 to + 1 | Between – 0.8 to – 1 |

| Slightly ITM | Between + 0.6 to + 1 | Between – 0.6 to – 1 |

| ATM | Between + 0.45 to + 0.55 | Between – 0.45 to – 0.55 |

| Slightly OTM | Between + 0.45 to + 0.3 | Between – 0.45 to -0.3 |

| Deep OTM | Between + 0.3 to + 0 | Between – 0.3 to – 0 |

Of course you can always find out the exact delta of an option by using a B&S option pricing calculator.

9.5 – Delta for a Put Option

Do recollect the Delta of a Put Option ranges from -1 to 0. The negative sign is just to illustrate the fact that when the underlying gains in value, the value of premium goes down. Keeping this in mind, consider the following details –

| Parameters | Values |

|---|---|

| Underlying | Nifty |

| Strike | 8300 |

| Spot value | 8268 |

| Premium | 128 |

| Delta | -0.55 |

| Expected Nifty Value (Case 1) | 8310 |

| Expected Nifty Value (Case 2) | 8230 |

Note – 8268 is a slightly ITM option, hence the delta is around -0.55 (as indicated from the table above).

The objective is to evaluate the new premium value considering the delta value to be -0.55. Do pay attention to the calculations made below.

Case 1: Nifty is expected to move to 8310

Expected change = 8310 – 8268

= 42

Delta = – 0.55

= -0.55*42

= -23.1

Current Premium = 128

New Premium = 128 -23.1

= 104.9

Here I’m subtracting the value of delta since I know that the value of a Put option declines when the underlying value increases.

Case 2: Nifty is expected to move to 8230

Expected change = 8268 – 8230

= 38

Delta = – 0.55

= -0.55*38

= -20.9

Current Premium = 128

New Premium = 128 + 20.9

= 148.9

Here I’m adding the value of delta since I know that the value of a Put option gains when the underlying value decreases.

I hope with the above two Illustrations you are now clear on how to use the Put Option’s delta value to evaluate the new premium value. Also, I will take the liberty to skip explaining why the Put Option’s delta is bound between -1 and 0.

In fact I would encourage the readers to apply the same logic we used while understanding why the call option’s delta is bound between 0 and 1, to understand why Put option’s delta is bound between -1 and 0.

In the next chapter we will dig deeper into Delta and understand some of its characteristics.

Key takeaways from this chapter

- Option Greeks are forces that influence the premium of an option

- Delta is an Option Greek that captures the effect of the direction of the market

- Call option delta varies between 0 and 1, some traders prefer to use 0 to 100.

- Put option delta varies between -1 and 0 (-100 to 0)

- The negative delta value for a Put Option indicates that the option premium and underlying value moves in the opposite direction

- ATM options have a delta of 0.5

- ITM option have a delta of close to 1

- OTM options have a delta of close to 0.

Hi Karthik, in one of our example:-

There are two Call options and you need to decide which one to buy.

Call Option 1 has a delta of 0.05

Call Option 2 has a delta of 0.2

Now the question is, which option will you buy?

Let us do some math to answer this –

Change in underlying = 100 points

Call option 1 Delta = 0.05

Change in premium for call option 1 = 100 * 0.05

= 5

Call option 2 Delta = 0.2

Change in premium for call option 2 = 100 * 0.2

= 20

As you can see the same 100 point move in the underlying has different effects on different options. In this case clearly the trader would be better off buying Call Option 2.

Why call option 2 is better ? For the same change in the underlying if we pay less premium thats more better na ?

Yes, there are trade offs, you need to decide what you prefer – higher magnitude of premium movement or lower premium outlay.

Thanks for responding sir. But it still doesnt answer the question. Call option we buy the premium and when the premium is lower we make higher profits? Could you pls explain? Why 0.2 delta he would choose?

You can buy either call or Put option by paying a premium. You make money when the premium increases from whatever price you have paid.

\”You can buy either call or Put option by paying a premium. You make money when the premium increases from whatever price you have paid.\”

But if you hold till expiry(which is what we are considering till now in all examples), the premium change is irrelevant as the P&L is determined by the spot price, strike price and the *premium paid* and not the current premium right? So the less premium paid initially the better the profits

Thats right. Its like buying a stock, the lower the price, the better it is, assuming you get to sell for higher 🙂

Hi Sir,

How can we choose delta here. For example .2 delta, .3 delta, .4 delta how can we choose the exact one. Is there any ways..

Divya, not sure if I fully understand the query. But we dont choose the delta, the delta of an option depends on the moneyness of the option.

Hi Kartik

In the last example, In case of put option, since spot – 8268 is less than strike – 8300, it is slightly OTM right instead of slightly ITM?

Please help me understand this

Yes, its slightly ITM.

Hi Karthick,

Not sure if i\’ll get a response since this article has been published long back. But i was wondering about the approximate delta values which was given. The Deep OTM delta values ranged from 0 to 0.3 (i.e. 0.3 difference) whereas the Deep ITM delta values ranged from 0.8 to 1 (i.e only a 0.2 difference). Can you give some insight as to why this is the case (is there some particular reason behind it?).

I was expecting the Deep OTM to be from 0 to 0.2 delta in order to maintain the symmetry. Please help on this. 🙂

Ram, the actual values can change, the range is more like a rough guide to basically figure where the delta is likely to be given the moneyness of the option 🙂

Okay Great👍 Thanks for the reply Karthik🙂

Happy learning, Ram 🙂

Hi Karthik,

For ce delta will be +ve ,say 0.4 delta means for every 1 point upwards move in the underlying premium increase by 0.4 likewise for every 1 point decrease premium can go down by 0.4

For pe, delta of -0.4 premium increases for by 0.4 for every point decrease in underlying !! So far it’s clear what if we enter an iron condor trade involving ce and pe how would positional delta impact with respect to the movement of the stock price

So if you know how the deltas work for CE and PE, both long and short, then you pretty much know the basics and the underlying working of the delta. Consider a bull call spread with long call, delta of 0.4, and short call with delta of -0.2. Now since the deltas are additive in nature, we can add up both the deltas and say that the bull call spread, as a position has a delta of 0.2.

Hi,

In the numericals involving calculation of new option premium when the underlying price increased or decreased, we have taken the delta to be a fixed value. But in reality delta of an option also changes when the option transitions from OTM – ATM – ITM. Could you please help in understanding this part?

Have explained this in the next chapter on Gamma, please do check that 🙂

Hi Karthik, I have one question about section 9.3. You first explained the call option premium changes if the underlying goes down. Below is the exact reading:

\”Nifty @ 10:55 AM is at 8288

Option Strike = 8250 Call Option

Premium = 133

Delta of the option = 0.55

Nifty @ 3:15 PM is expected to reach 8200

What is the likely premium value at 3:15 PM?

We are expecting Nifty to decline by – 88 points (8200 – 8288), hence the change in premium will be –

= – 88 * 0.55

= – 48.4\”

Here you are calculating the decline with a negative (-ve) sign. However, in scenario 2, you are just doing the opposite while explaining why Delta can not be negative (-ve). Below is the exact reading:

\”Scenario 2: Delta lesser than 0 for a call option

Nifty @ 10:55 AM at 8288

Option Strike = 8300 Call Option

Premium = 9

Delta of the option = – 0.2 (have purposely changed the value to below 0, hence negative delta)

Nifty @ 3:15 PM is expected to reach 8200

What is the likely premium value at 3:15 PM?

Change in Nifty = 88 points (8288 -8200)

Therefore the change in premium (considering the delta is -0.2)

= -0.2*88

= -17.6

For a moment we will assume this is true, therefore new premium will be

= -17.6 + 9

= – 8.6\”

How do we decide the sign while calculating the difference?

For CE = +ve if the market moves up, -ve otherwise

For PE = +ve if the market goes down, -ve otherwise.

Hi Karthik, As a thumb rule, we can follow the mentioned convention. I got confused from the mathematical perspective as I find the below explanation a little contradictory:

\”As you can see in this case, when the delta of a call option goes below 0, there is a possibility for the premium to go below 0, which is impossible. At this point do recollect the premium irrespective of a call or put can never be negative. Hence for this reason, the delta of a call option is lower bound to zero.\”

In many scenarios, there\’s the possibility of the premium going below zero if we calculate it in a similar manner, where delta is not below zero. We already know that premium can not go below zero, so we consider it to be zero in all such cases. That\’s the convention that we are following, but it can not be a justification for the delta to be non-negative.

However, if we follow the same convention of using a negative (-ve) sign in calculating the change (decline) in Nifty and calculate the change in premium, it would be +17.6 + 9 = 26.6 i.e. premium for the call option is increasing. However, underlying is declining.

Now we can easily deduce that the underlying is going down for a call option, and ideally, the derivative value should follow the direction of the underlying. A negative delta is not possible as it will result in the underlying and derivatives following different directions.

\’and ideally, the derivative value should follow the direction of the underlying\’ – how would this fit into a Put option? For example if underlying value increases, the value of PUT option decreases.

Hi, Why we are not doing spot-strike in the a case of CE and why we are doing previous spot – new spot, What is role of strike price in this concept

The formula changes based on the option type.

1) For CE, it is = Spot-Strike

2) For PE, it is = Strike – Spot

You mean to say 0.05 is higher number than 0.2?

Sorry, dint see that number properly. Missed it, but in general, higher the delta value, higher is the sensitivity to change in underlying price.

In the example of 2 different deltas, one having0.05 & other 0.2, with change of 100 points in underlying, the change in premium will be 5 in first case 20 in second case.That means addition of 20 points will make the second premium costlier than the one in which only 5 points are getting added,isn\’t it?

Yes, that is because the delta is higher in the first place.

Hi, I was a bit confused with this as well. not sure if you would get a chance to reply, but you said in the example of the change in the premium by 20 & 5 in the 2 cases, it would be better to go with the one changing by 20. With the premiums increasing, why would it be better to go with that option for a call option?

Hey Nishanth, its the absolute change, which will have a bigger impact on your P&L.

Okay sir i have a question. In the module you have mentioned that Delta of the option = 0.55. So you are considering the delta of the strike price (8250) or delta of current strike price i.e(8288) or delta of the future strike price that is 8310

Hi!!!

There was a little confusion regarding the example discussed.

Call option 1 Delta = 0.05

Change in premium for call option 1 = 100 * 0.05

= 5

Call option 2 Delta = 0.2

Change in premium for call option 2 = 100 * 0.2

= 20

As you can see the same 100 point move in the underlying has different effects on different options. In this case clearly the trader would be better off buying Call Option 2.

In the above example, if the trader is buying a call option 1, and suppose the old call premium is Rs.20 then new call premium will be Rs.25. Thus, the trader will end up paying Rs.25.

Whereas if the trader is buying a call option 2, and suppose the old call premium is Rs.20 then the new call premium will be Rs.40. Thus, the trader will end up paying Rs.40.

If we compare the premium of Call Option 1 it is Rs.25, and that of Call Option 2 is Rs.40. So as a trader, who is a buyer of the Call option, won\’t he benefit by paying less premium and choosing Call option 1 instead of Call option 2. Please explain, whether the choice made by the trader for the Call Option 1 is better or not when compared to Call Option 2. Reply awaited.

One way to evaluate this is in the percentage terms and the return on premium paid basis.

Hi Karthik Sir,

I have a doubt regarding the call option.

For Example – When the nifty spot is 8100 then i have a bullish view then bought call option of 8150 CE. so now nifty went up to say 8250. Now I have a 100 points on my side. Apart from the premium aspects. Already nifty went upto 8250 even now will i be able to buy the 8150 CE again.

Like what i dont get is when the strike price is passed still we can buy the option?

The premium increases and therefore the value of the option that you bought increases. Thats how you gain while trading options.

Happy Teacher\’s say, Karthik sir:)

Thanks so much 🙂

In the example for delta-call option, the delta value is 0.55 where the strike is 8250 and spot is 8288, so it comes under slightly ITM right? So the delta value falls under 0.6-1 right?

Thats right, its slightly ITM.

Before my query would like to thanks for explaining the delta and all the previous modules in a lucid manner.

The query was regarding the 100 point move in the underlying and impact on option premium.

You have compared

case-1: Increase in premium by 5

case-2 : Increase in premium by 20

You have recommended that case-2 would be better to be chosen. i do not understand the fact that why 20/- which is higher premium than 5/- is more beneficial ? Is it not that for case 2 i as an call option buyer paying more premium ? Little confused now

Thanks Anand.

This is basically evaluating which option is better assuming you are buyer in both. Clearly, 20 point increase in premium is better than 5.

Hello Karthik,

Which means logically we cannot apply the two different Delta values to the same \”Change in underlying\”. Because we know Change in Delta directly proportional to Change in Premium. So each Changes in underlying has each delta.

Please confirm If my understanding is correct?

I\’m not able to understand this statement you made – So each Changes in underlying has each delta.

Can you share more context?

I have tried the applying delta of -1.5 and +0.2 for put option which should not be possible values.

strike = 8300 PE, premium 128, initial morning spot price=8268

case 1: NIFTY increases @ afternoon to 8310

change in underlying = 42 points. Therefore, 42*-1.5=-63

So, like we had a change in call option, the above put option changes -63 points for 42 point underlying which is not possible. Similarly, applying the concept to below example(delta=+0.2), validation of answer is not happening.

Case 2: NIFTY decreases @ afternoon to 8230

change in underlying = 38 points. Therefore, 0.2*38=7.6

change in premium = 128+7.6= implies new premium is 135.6. We observed a premium increase. But delta of put option cannot be +0.2. Explain please

Premium cant be -ve. Please ensure you are assigning the right sign (+ve and -ve) while doing the math.

how do we ensure that?

what if delta of an call option is 1 and the underlying price goes down by 30 points does the option premium also down by 30 points?

Yes, if the delta is 1, then this is the expected behavior.

in the examples of call and put you have subtracted spot from expected underlying value except for the case 2 of put. you can simply subtract the spot from expected value, and it will give negative value if the expected value if the value is to be expected to go down and multiplying it will negative delta value gonna give positive value and you can simply add it to the premium . why you have to confuse the case 2 of put.

you can simply do like this

Nifty is expected to move to 8230

Expected change = 8230 – 8268

= -38

Delta = – 0.55

= -0.55*-38

= +20.9

Current Premium = 128

New Premium = 128 + 20.9

= 148.9

why are you complicating the simplest thing

Ok.

Is it true if any future stock oi is Maximum changes for big movement expected

Not necessary, Mihir. But whenever there are big changes in OI, volatility is quite high.

Can you pls explain intuitively why the delta of ITMs and Deep ITMs are higher than that for OTMS ?

The higher the moneyness, higher is the delta. Deep ITMs have a lot of moneyness, hence higher delta.

Hi

When we look at CRUDEOIL24MAY6550PE the moment of option price does not match the moment in the Crude future contract, the proportion of movement here does not match as compared to Bank nifty or Nifty option trade, any reason?

Why do you think so? Is there any specific example you\’d like to quote?

Hello Kartik,

Is there any merit in conducting technical analysis on a strike price chart, considering that option premiums are primarily influenced by options Greeks rather than supply and demand?\”

I\’d not suggest that, rather look at the spot price and analyse that.

I am a bit confuse. I watched the videos carefully still premium dint rise till the estimated value as per Delta. I calculated both strike n spot price still there was huge difference between the premium. Can you guide me?

The premium is not just a function of delta, it has other factors impacting too. Hence the difference 🙂

VERY SIMPLE LANGUAGE IN EXPLAIN AND UNDESATAND DELTA GREEK TOPIC.

Happy learning 🙂

PLEASE DO CORRECTION AT CHAPTOR 9.5 CASE 2 NIFTY EXPACTED TO MOVE 8230

AS PER YOUR

EXPACTED CHANGE=8268-8230 CORRECTION SHOULD BE =8230-8268

=38 =(-)38

DELTA =(-)0.55 DELTA =(-)0.55

PRICE CHANGE =38*(-)0.55 PRICE CHANGE =(-)38*(-)0.55

=(-)20.9 =20.9

Sure, checking this.

Please advise on US Stock, where and when should i invest? I am originally from Nepal and been in US for work.

What are the stocks where i should invest, NASDAQ or S&P 500 ?

I think both these are good options – S&P 500 and NASDAQ. You can invest in ETFs directly, check with your broker for that.

ITM has highest delta is a fact, but slots of ITM are also expensive wrt to OTM. What\’s the best option to trade if I have limited capital of say ₹1,00,000, then what should i prefer, ITM or OTM.

There is no straightforward answer to this, Aayush. It really depends on many other factors – time to expiry, volatility, speed at which the market is moving etc.

i intend to learn DELTA AND OTHER FACTORS IMPACTING option INDEX (NIFTY) premium. Regards

We have discussed quite a few details here, Bina. Request you to go through the same.

Hello sir, if I may ask a question

Suppose I think Bnf will go down till 42500 today (just for example )and rise from there. And I want to buy at the money call option when the prices go to 42500. Now how can calculate what the premium will be for that strike price when the price goes to 42500 so that I can place a limit order for what the premium would be when bnf hits 42500?

Earlier I used the option calculator in sensibull but they have discontinued that.

That will be hard as the premium value is not just dependent on the price movement, but also on time and volatility. But over time, you will know the approximate value at which these options will trade, so you can use your experience to arrive at that 🙂

Thanks Sir

For explaining the delta in such a simple way.

Happy learning, Manoj!

Rs 5 is premium that you booked as a profit

Thank you for the beautiful explanation.

Happy learning, Devang!

Thank you so much sir, concepts are very well explained.

Happy learning 🙂

Hi thank you so much for your lesson on delta, I have one question, For simplicity i will assume nifty as 100, so spot price currently of nifty is 100, at 9:15, Nifty was trading at 90, the value of call option is 2, I am expecting an upward trend and i buy a call option but at 3:15, there was no movement at all, assuming, but at 3:15 despite nifty being at 90 the value of call option dips to 1.5, I have noticed this quite a few times, and this isnt the expiry day… can u help me with this

This is because the option premium is a function of factors including delta and theta. While one force tends to increase the value of the premium, others kind of drag it down. So you need to look at it in totality 🙂

Hey Karthik,

Slightly ITM Between + 0.6 to + 1 Between – 0.6 to – 1

This should be

Slightly ITM Between + 0.6 to + 0.8 Between – 0.6 to – 0.8

Right?

The idea was to say its closer to 1 🙂

Hello Karthik Rangappa,

since i started my trading journey i was really confuse about call and put option premium.. in face, i didn\’t know what is premium then i started finding about premium and greeks. Today i reached this page and everything is crystal clear about how to what to trade and when to trade according to Delta..

I want one more favor from you. Where can i find live greek chart of call options or anything like that.

Thank you so much…

Happy to note that Ashish. For live greek, you can check the Sensibull platform.

Splendid..

Instead having moderate knowledge of Greek,this article has given so much insight about Greeks

Glad you liked it Ramendra. Happy learning 🙂

I never imagined I could understand Delta so easily. Have been super intimidated by options. Thanks a ton for simplifying!

Happy learning, Anaida!

is all chapter in hindi avalabile sir

Yes, click on Hindi module.

Hi Karthik,

In case 2 of the put option, the expected change should be -38 (8230 – 8268). And therefore the change in premium should automatically be +20.9 (-0.55 * -38). This way, one does not have to remember when to add and when to substract the change in premium. You followed the same method when explaining the call option, but not sure why not for the put option.

Checking on this, Vishal.

When I buy the call option where the delta was 0.65 (2 lots *50)=0.65*100 => 65

But unfortunately market goes down , on the second day

When I see the same strike price now the new delta is 0.27 which means for 100 is equal to 27 premium.

Now my doubt is which delta will be applied to me 65 or 27?

If 27 why

Because I buy the option with delta 65 means its the contract while buying the strike .

(I\’m not buying on the second day I\’m just going through delta values by holding my option)

You must always take the current delta value to estimate the overall delta.

Correction: Just wanted to highlight as how 8268 would be ITM for 8300 considering PUT options?

Its actually both ATM and ITM, given that it a strike which is so close to spot. But more ITM than ATM 🙂

In the \’Delta for a Put Option\’, table values for Spot & Strike might have got interchanged which is somehow causing the confusion in the explanation below regarding the delta calculation.

Just wanted to highlight as how 8268 would be ITM for 2300 considering PUT options?

In this example, spot is 8300, so 8268, which is close to the spot becomes ITM, right?

Thank you sir for explaining.

I request you to please elaborate on up delta ,Down delta, delta contraction

Abhijith, I\’ve explained all that\’s there to Delta in this and the next few chapters 🙂

At least, the ones that i think are important to know about.

Enjoyed

Happy learning!

Hey Karthik, I hope you are doing well.

(9.3)

For example assume you expect a massive 100 point up move on Nifty, and based on this expectation you decide to buy an option. There are two Call options and you need to decide which one to buy.

Call Option 1 has a delta of 0.05

Call Option 2 has a delta of 0.2

Now the question is, which option will you buy?

Let us do some math to answer this –

Change in underlying = 100 points

Call option 1 Delta = 0.05

Change in premium for call option 1 = 100 * 0.05

= 5

Call option 2 Delta = 0.2

Change in premium for call option 2 = 100 * 0.2

= 20

Why 2nd option is suitable for a call buyer? It makes sense for me to buy a call for a lower premium right? How does probability plan in this?

Thank you 🙂

From an absolute change in premium perspective, option 2 makes sense. But if the expected move is significant and there is enough time to expiry, then maybe you should consider the first option 🙂

Rangappa sir,

Slightly ITM Between + 0.6 to + 1 Between – 0.6 to – 1 confused with this.

is it Slightly ITM Between + 0.6 to + 8 Between – 0.6 to – 8?

These are just reference delta values based on the moneyness of the option, Shashwath.

Hi Karthik,

Its really very interesting going through the chapters, Kudos to you for bringing us these wonderful training material and that too at no additional cost. God bless you for being the person you are.

I posted another query in Moneyness chapter, please ignore it if you haven\’t gone through it, I felt it is not a question you can spend your precious time on, and I didn\’t find a way to delete that question.

However, I have a question in this chapter 😅.

Delta is an option Greek that captures the effect of the direction of the market. So wanted to understand how the different movements of price within this direction effect the strike Price.

I didn\’t know if I put my question as I wanted to convey, so explained my question below a bit longer so that you understand what I am trying to ask. Please pardon my writing communication skills, I wish there is a feature for audio comments 😀

In the first example of this chapter:

At 09:18am, Nifty Spot = 8292, Strike = 8250, Premium = 144

At 10:00am, Nifty moved to = 8315, Premium now trading at = 150

My doubt here is, I do not know how (pattern) the Nifty moved between 09:18am to 10:00am before it ended at 8315 at 10:00am, would have the premium moved to same Rs.150, irrespective of how the movement was in this 1 hour?

Like, if in this time 09:18am to 10:00am:

1) Nifty has slowly moved up, without any much down fall and finally ended at 8315 (or)

2) Nifty drastically fell to 8100 and then suddenly moved up to 8315 by 10:00am (or)

3) Nifty surged up to 8400 and then fell to 8315 by 10:00am

4) Nifty moved sideways and then right at 10:00am moved to 8315

Nifty would have behaved in many ways in that 1 hour before coming to 8315, will in either of the above cases the premium would have been Rs.150 at 10:00am?

Another query, if I may ask:

I went through the comments and understood that Delta values are not available real time and we would need an options calculator, but, when we are doing live trading and we do not see Delta values in Real time, isn\’t it difficult to trade in options? as we have to go somewhere else to calculate the delta and by that time, the numbers would have changed. Can you help us how to tackle such things.

Can I ask how you work on with Greeks when live trading in Options when markets are open?

Is there any platform that offers live delta values?

Thank you for taking the stress to go trough my loooong query.

Thanks for the kind words, Sai. I may have answered your previous question also 🙂

You are right. Nifty can move between two values in multiple ways. In this explanation, I\’m only considering two end point values here and calculating the change in delta, this is mainly to explain the concept of how delta changes.. In reality, delta and, therefore the premiums change continuously. So if nifty shoots up and comes back to a certain value, so would the premium. But then it can also get a little complex, as the change in delta is also ascribed to other greek changes. For instance, if volatility increases, so would the premium. With expiry close, the theta delcay is higher.

So the way to look at greeks is to get a holistic view and not isolate the greeks and evaluate its impact on silo\’d basis. Hope this helps 🙂

9.5 – Delta for a Put Option

Note – 8268 is a slightly ITM option, hence the delta is around -0.55 (as indicated from the table above).

I think number 8268 above is wrong here, instead it should be 8300 because in table we have strike as 8300 and spot price is 8268 so 8300 can be considered as slightly ITM option.

please correct me if I am wrong.

Ah, need to check. In general, if the spot is below the strike, then the option is considered ITM for puts.

Hello Sir. Please would you kindly explain what do you mean by deep ITM and Slight ITM.

Ritu, please check the earlier chapter on moneyness of options. Have explained this there.

No compalints about the article but how can you forget the brilliant acting of Irrfan in the intro.

Of course 🙂 I should have mentioned that as well.

\”In this case clearly the trader would be better off buying Call Option 2\” – Can you explain this little more, i believe in the option 2 the premium will increase by 20 for the buyer so it is better to buy call option 1 right? in which option premium will increase only by 5 ?

Also at the time 3:15 if the NIFTY closes at 8310 in the very first example according to the delta of +0.55 it increases the premium to 145.1, if i decide to come out of the contract do i have to pay the difference in the premium (145.1-133(original premium)) ? Please help to elaborate

Can you check the previous comments, I remember discussing this in detail.

\’\’\’As you can see the same 100 point move in the underlying has different effects on different options. In this case clearly the trader would be better off buying Call Option 2. \’\’\’

Why is this?

is not paying lesser premium better?

Yeah, but you also need to worry about the probability of the option moving in your favor after buying right?

Hii kartik

I need to know that as you have told earlier that if delta of a call option is .2 it means there\’s only 20%chances that this option will expire ITM.

So if we formulate a selling strategy based on that view how can we succeed in our strategy if there\’s a change in underlying and it becomes a otm due a sharp rise/fall in the market.

How can we save ourselves in that situation.

The odds of the position moving against you is only 20%, but if you are selling, you want the position to go OTM right?

Ok sir thanks for your answer.

Happy learning 🙂

Hello Karthik sir,

How are you? I have a doubt.. I have this situation.

Nifty spot = 8600 (let\’s assume for the sake of example). I expect it to become 8500 and took a put option.

Premium = 70. Delta = -0.5. I want to calculate how much premium will become when Nifty becomes 8500.

Here\’s how I calculate..

Expected change in spot = 100.

Change in the premium will be 100*-0.5 = -50.

Now since this is a put option, premium will increase when underlying goes down. (other factors being same).

So my premium will become 70 + (-50) = 20. Whereas the premium should become 70+50 = 120.

This is where I am wondering where I went wrong. Kindly correct me.

Sandeep, you can consider the change in spot as -100. So, -100*(-)0.5 = 50.

How option prices are influenced by option greeks? When we buy a call / put option, a buyer and seller needs to agree on the price right ? How the prices are influenced by greeks when the price needs to be matched b/w seller and buyer?

The price you buy and sell at is decided by how prices move, time to expiry, and volatility. These are essentially captured by the greeks, and that\’s how the option premiums are decided.

sir, I have doubts..my doubt is regarding Rahul Chaudhary saying:

related to adding deltas; if there any formulas to add up deltas …. how it works sir pls explain to me …

Rahul Chaudhary says:

November 11, 2022 at 9:44 am

Hi, when we buy 1 CE (Delta-0.6) and PE (Delta -0.4) of the same strike it becomes Delta 1 (0.6-(-0.4)=1). Pl confirm if the same concept applied in the below situations is ok –

1. Buy 1 CE (0.6), Write 1 PE (-0.4)= 0.6+(-0.4)= 0.2

2. Write 1 CE (0.6), Buy 1 PE (-0.4)= -0.6-(-0.4)= -0.2

3. Write 1 CE (0.6), Write 1 PE (-0.4)= -0.6+(-0.4)= -1.0

Here is an easy way to remember this –

1) Calls and +ve delta to indicate that the strike gains value with an increase in spot

2) Puts have a -ve delta to indicate that the strike loses value with an increase in spot

When adding delta –

Long CE = +(+Delta)

Short CE = -(+Delta)

Long PE = +(-Delta)

SHort PE = -(-Delta)

So Write CE (0.6) and Buy PE (-0.4)

= 0.6 +(-0.4)

=0.6-0.4

=0.2

Thats how you can add the deltas.

one of the best teacher i have ever come across. Happy teacher\’s day sir…

I am a new bee here…my doubt is…

sir when the strike price 18300CE LONG spot price is below the strike price if the market move above the strike price we will be in profit right?

sir what if we chose 18300CE long when already spot price is above the strike price how do we profit how it works sir pls explain.

Yes Arpitha. The call option will be profitable if the spot is above the strike. If you choose, a strike that is already above the strike (also called ITM), then premium you\’d pay would be very high. For you to profit, the spot price has to move even higher.

Hi, when we buy 1 CE (Delta-0.6) and PE (Delta -0.4) of same strike it becomes Delta 1 (0.6-(-0.4)=1). Pl confirm if the same concept is applied in below situations is ok –

1. Buy 1 CE (0.6), Write 1 PE (-0.4)= 0.6+(-0.4)= 0.2

2. Write 1 CE (0.6), Buy 1 PE (-0.4)= -0.6-(-0.4)= -0.2

3. Write 1 CE (0.6), Write 1 PE (-0.4)= -0.6+(-0.4)= -1.0

This is the correct way to add up the deltas, Rahul.

hlo sir

my question is Case 2: Nifty is expected to move to 8230 and spot is 8268 can we subtract like this 8230-8268 = -38

then delta = -0.55*(-38) = +20.9

now the new premium is 128+20.9 = 148.9

is this right ?

Yup, it is.

strike price = 8500 PE and spot Price is 8550 and premium value is 100, ith delta value of – 0.55. Suppose if price increased from 8550 to 8750, then there is 200 points increase in underlying, this ill result in 110 points decrease in premium right? which attributes to premium value to ZERO(100-110 pts= -10 = 0),so now the premium value will be zero. but if the spot price falls from 8750 to 8510(240),with delta value = 0.55, premium change is 132, so does this means that the new premium value will be 132, or it should stay at zero itself?

These are approximate values. Remember, the premium is a function of both delta (intrinsic value) and time value.

Sir at the end of the day, option premiums move according to demand/supply, and greeks are tools with which we can better analyse/forecast them.

Is my understanding correct?

Also sir as you said \”Option Greeks are forces that influence the premium of an option\”, is this like a cause effect thing ; i mean do greeks \”control\” premium or rather greeks get their values from the premium\’s movement?

Thank you for providing us with such lucid learning material…

Absolutely, Yash. Thats the way it works 🙂

Hi Karthik,

Thank you for Varsity and all the educational contents.

In section \”9.5 – Delta for a Put Option\”, in the note below the table it is mentioned that \”8268 is a slightly ITM option\”, shouldn\’t it be \”8300 is a slightly ITM option\” as it is the strike value and in the money put option with respect to the spot value of 8268.

Ah yes, I guess 8300 is the strike under consideration.

BEAUTIFULLY AND INFORMATIVE EXPLAINED. THANK YOU SIR

Glad you liked it, happy learning 🙂

In 9.5 delta for put option case 2:

Below correction required pls check

Expected change = 8230 -8268

= -38

Delta = – 0.55

= -0.55*-38

= 20.9

Than only new premium will be

128+20.9 = 148.9

There are a few comments regarding this, Holas. Please do check that for clarity.

Hi Karthik,

First of all thanks for the reply.

My question is when I calculate the delta value that time I am confused when you calculate DELTA FOR A PUT OPTION in Scenario –

1. Subtract the SPOT VALUE (8268) from EXPECTED NIFTY VALUE (8310)

So, 8310 – 8268 = 42

But in Scenario –

2. Subtract the EXPECTED NIFTY VALUE (8230) from SPOT VALUE (8268)

Like, 8268 – 8230 = 38

But as I learned in previous chapter that PUT OPTION = STRIKE PRICE – SPOT PRICE. This is little confusing to me . Please help me to understand the difference.

The expected nifty value is replacing the sport price on expiry. SO here you are trying to figure out what will be the intrinsic value if Nifty on expiry is at a certain value. That certain value is called \’expected value\’.

Hi Karthik ,

I am confused when you calculate DELTA FOR A PUT OPTION in Scenario –

1. Subtract the SPOT VALUE (8268) from EXPECTED NIFTY VALUE (8310)

So, 8310 – 8268 = 42

But in Scenario –

2. Subtract the EXPECTED NIFTY VALUE (8230) from SPOT VALUE (8268)

Like, 8268 – 8230 = 38

But as I learned in previous chapter that PUT OPTION = STRIKE PRICE – SPOT PRICE. This is little confusing to me . Please help me to understand the difference.

Strike Price – Spot price, if its a positive number, is the put option\’s intrinsic value. I\’m not sure about the delta value thing you are talking about. Can you share more context?

Superb learning.

One of my Mentor and GooD Motivating friend Guru told me about this.

This theory is fantastic.

Thanks Guru Bhai Thanks Team Zerodha.

Happy learning 🙂

Hey kartik, In delta for a put option strike price written as 8300 and spot price as 8268 then it should be slightly out of the money option ?

8300 PE strike is ITM if spot 8268 right?

Sir Can you please give an example with Explantion that in case of Put Option Why Delta cannot be above 0.?

For the same reason why PE and CE are upper and lower bound.

Where can I find option geeks ?

Try Sensibull.

Hi

You mentioned that delta can not be more than one as the option can not gain more value than the underlying itself. But if we see real trading cases, when some stocks trades at 10% sometimes their derivatives trade more than 50%, specially OTM contracts. (I am just giving an example here). In that case options price moves faster than the underlying.

Yeah, thats possible. I\’ve explained this case as well where the option strikes especially OTMs have a higher % change and this is because of the delta acceleration part (refer to the delta curve). That said, if you look at these options purely from delta perspective, then you will realize that the delta cannot move beyond the upper and lower bound.

TODAY IS Wednesday,

Today\’s bank nifty CMP: 35000

A) I bought a bank nifty call option strike price of 34900 (ITM)which going to expire tomorrow

If I failed to square off that what will happen

B)I SOLD A BANK NIFTY OF CALL OPTION OF A STRIKE PRICE OF 40000(OTM) WHICH GOING TO EXPIRE ON TOMORROW

If I failed to square off what will happen

How many days I can hold the short selling position of the option contract

On Thursday evening bank nifty CMP is 35600

On Thursday evening, what will happen to OTM & ATM contract

1) It will be settled by the broker

2) Same as above, provided its ITM

YOu can hold the short to expiry.

Here we see delta is between +1 to -1 is in rs or in decimal?

I mean is Greeks are in rs or in decimal?

They are considered in units, usually translating to Rupees. For example, if the delta of a call is 0.45, for every 1 point (or Rupees) change in underlying, the delta is expected to by 0.45 points (or Rupees).

Hi …

Regarding the explanation for why Delta cant be negative, I felt the more logical explanation could be that the direction of change of premium cant be in the opposite to the direction of change of underlying. Please correct me if I am wrong

Thats also true, Chandana.

i think in the below sentence that\’s written, 8300 should have been mentioned as it is the strike price.

8268 is the spot price right in that example right?

Note – 8268 is a slightly ITM option, hence the delta is around -0.55 (as indicated from the table above).

Ah, yes. Let me try and fix it.

Right!😊

Happy learning!

Karthik Rangappa says:

May 28, 2015 at 9:15 am

You are absolutely right – when it comes to option trading you should be using Option Greeks and other parameters to trade and not really Technical Analysis.

Here,we can say that look first at greeks and then consider TA. For example, we choose a proper strike say for CE and we expect Nifty to move up. Now we look at TA and find out that the candle formed is bearish; we further look at other indicators,EMA,RSI,MACD,BB and conclude that instead of moving up,Nifty may come down.

There must be a correlation between greeks and TA indicators. Please enlighten us.

Regards. ETU737

Yes, but like you mentioned take your cues, especially for designing the trade from Greeks and maybe use TA to time our entry and exit.

Recently i bought axis bank 850 CE option…My Question is Today Morning (28-Apr-22) axisbank opened at 776.90 same 850Call option opened at 9.20 later axis bank share price went to 785 but option call is not moved that much…bit option contract price should be moved above 9.20

Can anyone clarify?

That\’s because today was expiry and therefore zero time value. Hence the option won\’t move much unless the stock itself moves closer to the strike.

In 9.3 – Delta for a Call Option , you have written \” As you can see the same 100 point move in the underlying has different effects on different options. In this case clearly the trader would be better off buying Call Option 2. \” Why would trader choose call option 2? Can someone please explain?

How is the value of delta for different strikes derived?

It is based on the Black & Scholes model.

sir in the above section 9.5 delta for a put option

the value 8268 can be slightly OTM because in the put side of option chain the 8268 will be in the white section not in the pale yellow section.

please explain

thanks

regards

Yes, it is slightly OTM, Yash.

How is it seen , the call option premium increases with the increase in the spot value and vice versa ? Pls explain

Hmm, I\’ve explained this right in the first chapter Mayank. Request you to read that again. Thanks.

Hello sir,

For the call option delta case where the delta can not be less than 0, the following was the scenario mentioned.

Scenario 2: Delta lesser than 0 for a call option

Nifty @ 10:55 AM at 8288

Option Strike = 8300 Call Option

Premium = 9

Delta of the option = – 0.2 (have purposely changed the value to below 0, hence negative delta)

Nifty @ 3:15 PM is expected to reach 8200

What is the likely premium value at 3:15 PM?

Change in Nifty = 88 points (8288 -8200)

Therefore the change in premium (considering the delta is -0.2)

= -0.2*88

= -17.6

For a moment we will assume this is true, therefore new premium will be

= -17.6 + 9

= – 8.6

But, shouldnt the change in premium value be = -0.2*(8200-8288) = +17.6 ?

I am not able to understand clearly from the comments part for this query.

I\’m taking the absolute change in Nifty here, Parth. The directional movement is captured by the delta sign.

Hi,

How frequently Value of the Delta changes? The Value of Delta is counted same for all the strike prices while calculating even of Deep OTM Options

Delta changes as and when the value of the underlying value changes, so it is on a continuous basis.

In your example \”what if one anticipates a drop in Nifty? What will happen to the premium?\” you have shown the decline in NIFTY to be -88.

However, in your example \”Delta lesser than 0 for a call option\” when the decline in NIFTY is 88, you have shown the figure as 88. So when the stock declines, do we take the difference as negative or take the absolute value?

Another student brought this up and your response which I did not understand was

Thats because the delta is lower bound to 0…it cannot go lesser than 0. If it was lesser than 0, it means the option is moving faster than the underlying, which is counter intuitive.

In summary, if the stock declines by 88, do we use +88 or -88

Kalika, you will have to use -88.

I feel the reason for delta value of Call not to be below 0 would have been explained better by using -88 (8200-8288) as the difference in the drop in value of underlying. In which case delta of -0.2 and the change in price would be -88 would give a change in premium of +17.6. hence the premium would keep rising even when the underlying is dropping which cannot be the case for Calls.

I am new to derivatives and still learning. So pls excuse me if I am wrong. Logically I felt this would serve a better explanation while working it out for my better understanding.

Perhaps, and I need to check that again. But the idea of explaining it this way is to ensure that the concept of delta increase/decrease with the change in market direction is clear. Let me re-look at this.

Case 2: Nifty is expected to move to 8230

Expected change = 8268 – 8230

= 38

Delta = – 0.55

= -0.55*38

= -20.9

Current Premium = 128

New Premium = 128 + 20.9

= 148.9

Here I’m adding the value of delta since I know that the value of a Put option gains when the underlying value decreases.

shouldn\’t this be

Expected change = 8230 – 8268

= -38

Delta = – 0.55

= -0.55 * -38 (- – = +)

= 20.9

Current Premium = 128

New Premium = 128 + 20.9

= 148.9

The above explanation is confusing, it coveys that even if the result of delta is negative we are required to senselessly add it to current premium to get the new premium…

Hey Nathan, I agree with you and few others who have pointed this out (please see the comments). The idea was to emphasize how the deltas add up and subtract out wrt to the movement in spot.

Thank you sir… 😊

Hoping I can clear all my doubts in coming days if a mentor is like you..!!!

Have a great day ahead sir🙏

Happy learning!

So there is difference between selling and exercising one\’s position?

Yes, there is. You can sq off your position anytime you wish, but exercising is only on the expiry day.

Sir I have a queries….

If I buy call option 17000 today with expiry date 17th March that is last week of a month, then can I exercise my contact tomorrow or next week? Or should I have to wait for the last week of that month that is 17th March expiry…

Please sir clear my doubts, it\’s really very confusing for me.

YOu can sell the position anytime you wish, but exercise is only on the expiry day.

I understood very well in quick

Thank you so much ZERODHA

Happy learning, Rohit!

Hello sir

I have one simple question as you mentioned earlier that we get full IV on exercising our right on expiry. Sir if we are sure about upcoming trend like if am sure that XYZ option will close many points up on expiry than I would exercise my right on expiry and will not bother about to trade premiums . Then sir would i still worry about all option greaks if I will only exercise my right and can wait for expiry and is there any sense that i am seeing all these option greaks if were to only exercise right and not to trade premiums.

For this to play out, you need to be 100% sure about the directional move of the stock. Which in my experience is very tough to estimate 🙂

Karthik Sir, did you left discussion RHO intentionally or by mistake sir?

Intentionally Muthu, Rho is not actively used, so took the liberty to skip it.

How do we get the entry and exit?

Chitra, you can look at TA for identifying entry and exits.

Below statement is wrong. Please correct:

Case 2: Nifty is expected to move to 8230

Expected change = 8268 – 8230

= 38

Delta = – 0.55

= -0.55*38

= -20.9

Current Premium = 128

New Premium = 128 + 20.9

= 148.9

——————————-

It should be as below:

Expected change = 8230 – 8268

= -38

Delta = – 0.55

= -0.55*-38

= +20.9

Current Premium = 128

New Premium = 128 + 20.9

= 148.9

Yup, Praveen. Idea was to illustrate the fact that PUTS gains premium when the spot price decreases.

Hi karthik,

One doubt, please refer section 9.3 example for call option Delta

@9.15am spot price 8288

I am @3.15pm expecting nifty at 8000

So

8000-8288=-288

=-288*0.55

=-158.4

So premium 133-158.4=-25.4

Premium is minus 25.4.

I am expecting @3.15pm nifty at 8093

So 8093-8288= -195

=-195*.55

=-107.25

So premium 133-107.25=25.75

Here premium is +25.75

In these two nifty , premium value is same but in negative and positive sign.. how to calculate… Pls help..

Premium cannot go -ve, it will be a non-zero positive number. Since the intrinsic value is near zero, whatever value remains is due to the time value only.

Greeks

Hi Karthik

I think in the second example of Put option premium change you have deducted spot value minus current value while it should’ve been the other way round as in the first option the difference multiplied by a negative delta value gives reduction in premium and a negative reduction in spot value multiplied by a negative delta will give a positive change in premium of put option because a reduction in spot increases the premium of put option.

Let me recheck this, Ansul.

Sir Namaste,

I couldn\’t understand the very first para of the module. How 0.55 came the Delta? I am a late student of varsity.

Ramesh, if the option is ATM, then the delta will be around 0.55.

Sir , option premium is the same for option seller as well as the seller buyer , so why do we add the new premium in one case and subtract in the other case. For instance if there is a call option , the premium would be the same for buyer as well as writer , so why the delta is positive in case of buyers and negative in case of writers?

Sanvi, yes the premium is the same, but the sign difference is to indicate the directional difference. +ve indicate long position, -ve for short position.

Sir can you please explain why the value of a Put Option can never go above 0? I am unable to calculate it myself.

Options don\’t have -ve value, neither calls or Puts.

Thanks for the quick response Karthik

1. in this case the New Premium will be = 5-(-4) = 9 right?

2. I\’ve another question same was asked in tradingqna

As the option moves out of the money (OTM) the delta will start reducing

so the rate of Delta wont be 0.5 % throughout

Yet it is an interesting question

Lets take a real example – say ITC (Share value at Rs 227 at the end of the trading session on 24th Nov 2021)

And the premium value of the ATM Put Option (with Strike Price of Rs 227) is Rs 1.15

What if the value of ITC share price increases by Rs 20 in the first five minutes of trade the next day , then what happens to the value of the Put option ?

Even if Delta value falls rapidly, say it becomes 0.02 by the time ITC share price reaches 247 and the average change in Delta is 0.25, that would still mean that it would reduce the Option price by Rs 20 X 0.25 (Average Delta) – which is Rs 5 .

So the new value of the Put Option should be

Rs 1.15 – Rs 5 = (-) Rs 3.85

But we cant have Premium values in the negative

So what am I missing ?

What exactly happens ?

Thanks

Option premium cannot be -ve, it\’s capped to zero. In this case, the premium will rapidly decline very close to 0.

Hi Karthik, How the expected premium is calculated for option writers? As we know CALL option writer delta will be negative. When underlying increases the CALL premium should increase but in math calculation it is not. How exactly do we need to calculate?

Values

Current Underlying Price @ 100

CALL Option Premium = 5

Delta of the option = + 0.50

Assuming Underlying Price will rise to 108

CALL Option Buyer

Change in Underlying = 108-100 = +8 Points

Change in Premium = 8*(+0.5) = 4

New Premium = 5+4 = 9

CALL Option Seller

Change in Underlying = 108-100 = +8 Points

Change in Premium = 8*(-0.5) = -4

CALL Option seller Delta value taken as negative (-0.5)

New Premium = 5-4 = 1 ???

Can you help me??

The premium remains the same for both buyers and sellers, so does the delta. The position sign changes though, its + for long and -ve for option writers/sellers.

Sir u tell me that, if I have deep otm option and it became atm on the same day then delta value of my option will be remaining same or it will change? If it will change than how we can calculate?

It will change, Sandeep. Delta will be close to 0.5 for ATM options.

hello sir,

in the above example of put option you have said

Note – 8268 is a slightly ITM option, hence the delta is around -0.55 (as indicated from the table above).

but in the table its written that , Slightly ITM Between + 0.6 to + 1(CE) Between – 0.6 to – 1(PE)

Then according to the table it should be ATM option.

Anything above 0.55 is assumed to be ITM, Yakshdeep.

Hi Karthik,

I have a query. Here is the example you mentioned.

Nifty @ 10:55 AM is at 8288

Option Strike = 8250 Call Option

Premium = 133

Delta of the option = + 0.55

Nifty @ 3:15 PM is expected to reach 8310

and then calculated the new premium as 133 + (8310-8288)*0.55 = 145.1

What this means is that @10:55AM, the nifty spot price is 8288 and to buy the 8250 Call option, one has to pay 133 rupees as premium so that at the end of contract expiry, buyer can get nifty at 8250 rupees irrespective of spot price of nifty in market.

If suppose, the nifty spot price increased by 300 points by @3:00PM

Nifty spot price: 8288 + 300 => 8588

New Premium: 133 + 300*0.55 => 298

So now, to purchase nifty at the end of contract at 8250 rupees, one has to pay 298 rupees of premium. If you see here, current spot price (8588) > new premimum (298) + strike price (8250).

Is it possible to have this type of situation in market where the current spot price is greater than premium + strike price?

If yes, then won\’t the buyer have higher chance of getting profits? He makes profit if nifty stays at same price (or) moves up.

which is a contradiction to what we learned in call options theory where seller have more chance of getting profits than the buyer.

I know these numbers are used as an example, but point that I want to ask is \”Is it possible in market where the current spot price is greater than premimum + strike price\”?

Thanks,

Anil

Yes, its very possible for the spot to be higher than strike + premium. But remember, there is also a time component that keeps eating away the premium with the passage of time, so all else equal the premium will come down.

I\’d suggest you take a look at the option chain to see how the premiums are behaving wrt to spot price, you will understand this better.

Hello Nikhil,

First of all thank you for such useful contents to understand options. I have query on the following sample scenario (in quotes below) discussed under the heading \”Delta for call option\”.

\”For example assume you expect a massive 100 point up move on Nifty, and based on this expectation you decide to buy an option. There are two Call options and you need to decide which one to buy.

Call Option 1 has a delta of 0.05

Call Option 2 has a delta of 0.2

Now the question is, which option will you buy?

Let us do some math to answer this –

Change in underlying = 100 points

Call option 1 Delta = 0.05

Change in premium for call option 1 = 100 * 0.05 = 5

Call option 2 Delta = 0.2

Change in premium for call option 2 = 100 * 0.2= 20\”

As you can see the same 100 point move in the underlying has different effects on different options. In this case clearly the trader would be better off buying Call Option 2.\”

Since the payoff for call option buyer is max (0, spot – strike) – premium, wouldn\’t it be helpful for the trader to opt for low change in premium (i.e. 5) as premium reduces the payoff overall? Please help on this as I have hit a roadblock here.

Premium once paid is a constant. But the larger the \’Spot-strike\’, the bigger the payoff right?

Hello nikhil, I wanted to know that how can we know (Volatility% and interest%) when we calculating Delta value by using B&S calculator

FOr volatility, you can consider the implied volatility of the index.

where can we see the Delta value of option of a underlying stock

I\’d suggest you look at Sensibull website for this.

Best explanation #tradingwithbooks

Happy reading!

Thanks for sharing valuable information sir

Good luck, Anil. Happy learning 🙂

* Call Option 1 has a delta of 0.05

* Call Option 2 has a delta of 0.2

Now the question is, which option will you buy?

* Change in underlying = 100 points

– Call option 1 Delta = 0.05

Change in premium for call option 1 = 100 * 0.05 = 5

– Call option 2 Delta = 0.2

Change in premium for call option 2 = 100 * 0.2 = 20

Could you please explain how option 2 is better?

Prerana, the decision to buy or sell an option should not be dependent on the delta, rather should be dependent on what you expect from the market.

sir so can we conclude that buying an deep itm option is better than buying future (considering intraday), even i will need less amount to get equal benefit. and even the loss will be same in both the scenario.

Not always true, very dependent on the market and its context 🙂

How you came up with delta 0.55 in the example of Nifty you gave ? how to find that or calculate that ?

I\’ve explained how delta varies based on the moneyness of the option. Request you to kindly check that. Thanks.

😂😂I was reading so deeply when I red keytakways from this i was like 😔ohhhh this end here

We\’ll take that as a compliment 🙂

Hi Karthik

Well explained. This so much for your efforts

Happy learning!

Sir where can i get delta, iv, theta of an option strike price

Pinaki Nandy

Please do check the Sensibull site for this.

I have a similar question, \” WHO DECIDES VALUE OF OPTION PREMIUMS? which came into my mind when I read this\” Who decides the value of the Delta?\”

Rishabh, these are all market-driven. Its collectively driven by the market. Very similar to vegetable prices. For example who decides the prices of onions? Its market-driven right?

option 1 delta 0.05 , change in premium for every 100 points in underlying = 5

option 2 delta .2 , change in premium for every 100 points in underlying = 20

we have to pay more for buying call option 2,

why it is better to buy 2 as given in example

Which option is better depends on the market situation. If there is more time to expiry and you are bullish, then option 1. If there is not so much time to expiry and you are bulish, then maybe option 2.

As per understanding section 9.5 correction require

Case 2: Nifty is expected to move to 8230, spot price is 8268

Expected change = 8230 – 8268 = -38

Delta = – 0.55

Premium expected to change by = -0.55*-38 = 20.9

Current Premium = 128

New Premium = 128 + 20.9 = 148.9

Checking this, btw, I think this was discussed and clarified in the comments above. Can you please check?

I have found the pdf\’s.

But there is no pdf for modules12 and 13

How do we get excess to it??

Sir where?

Sir can u plse provide us pdf of each modules

It\’s already there no?

Hi, is it possible to cover Credit default swap in detail? It\’s a request.

It is not an instrument that can be traded in India, Daksha.

Excellent explanation. Thx.

Hello, It is mention here that value option can\’t change more than value of underlying, i.e. delta value can\’t be more than 1.

But on 28.05.21

change in Havells spot price is -1.7 rs ( change from 1019.8 to 1018.1)

But change in Havells jun ce 1060 is -3.35 rs( change from 27 to 23.65)

Avinash, you need to compare the delta of the option, not the absolute price change of spot and the premium.

In the example given for delta of 0.05 and 0.2, I assume the call buyer will take the one with lower premium. However the example mentions that the user will buy call for costlier delta 0.2.. Could you please explain

This depends on the larger context of the market and expectations right? I\’ve tried to explain this in the chapter itself.

Hi Karthik, I had one query. In the first example of this chapter of Nifty, 8250 CE is ATM considering Spot price 8292. So, the Delta should be around 0.5. Now, if the underlying moves to 8315, it\’s a (8315-8292)=23 point upward move, so the premium should also move (144*0.5)= 72 points up, right! Whereas, the new premium is just 149.40. Why is that?

It\’s middle of the month and I understand that other greeks are effecting the price too. Can you elaborate what is happening here like what other greeks are effecting the price and how? That would be a great help. Thanks.

That is true assuming only delta moves and all other greeks are constant. In reality, all greeks exert a force on the premiums which you need to factor in.

Yes, it\’s clear. Got confused in that bit. Thanks 🙂

Good luck, Robin. Happy learning.

Note – 8268 is a slightly ITM option, hence the delta is around -0.55 (as indicated from the table above) : From the module

If 8300 is the strike of the PUT OPTION, then won\’t 8268 be slightly OTM option?

If 8300 is the strike, and spot is 8268, then 8300 is ITM right?

Hello kartik, Can I buy a call option at 9:20 Am and sell it on the same day (3:20pm)?

Yes, you can Jaydeep.

Why would he be better off buying call Option2 is my question.

Please check my previous response. Thanks.

Could you elaborate on

`As you can see the same 100 point move in the underlying has different effects on different options. In this case clearly the trader would be better off buying Call Option 2.`

This means, based on the moneyness of the option, the premium may vary for the very same movement in the underlying.

Hey Kartik, how to login to Varsity(on a PC or through browser), do you need a Zerodha account for logging in? Also, why don\’t comments work on the app? I didn\’t even know that comments were an option until I started using Varsity on my PC.

Thanks a lot

No need to log in for VArsity web, you can comment without one. however, we need login for the app to ensure we maintain your progress.

Why the delta in Put Option is between -1 and 0? While I understand the it cannot go lesser than -1, what if I take the delta say 0.55 (greater than 0)?

The calculation is as below

Nifty Spot – 8268

Expected – 8310

Expected change – 42

Delta value = 0.55*42 = 23.1

Ideally we should subtract the value from the premium as the underlying is increasing in a put option. If we do that, we get 104.9 (which was like the first case).

There\’s a confusion here.

Can you please clarify?

With Puts, as the spot moves higher, you reduce the delta from the premium right?

Expiry day what I am doing?

How to exit?

If exit what is happening?

If not Exit what is happening?

What you will do, depends on what you want to do. To exit, you can press the exit position button on the terminal. If you don\’t exit, it will be settled by the broker.

Nifty is expected to move to 8230

Expected change = 8268 – 8230

= 38

Delta = – 0.55

= -0.55*38

= -20.9

Current Premium = 128

New Premium = 128 + 20.9

= 148.9

Sir in above Ex shouldn\’t we do 8230-8268

-38*-0.55=+21.9

and than 128+21.9 = 148.9

Not really, Utsav, we just take the difference in the spot change. The delta indicates the sign anyway.

I have a trading account with Zerodha. Please inform from which website can I get the Delta for Different strike prices for Call and Put

Please do check https://sensibull.com/, they have all metric that you are looking for, put in a very user-friendly way.

Refer to 9.5 – Delta for a Put Option

\”Note – 8268 is a slightly ITM option\”

You mentioned that Strike is 8300. If so, will 8268 be slightly ITM or slightly OTM? Please clarify.

Slightly ITM.

Dear Kartik Sir,

Let’s take one example

Friday Reliance closed at 2080.30 (cash)

25.02.21 expiry PE at Strike price 1,600 (Deep OTM) premium was Rs 0.20

Today Reliance drop by Rs 50 and presently trading at 2,030 and premium dropped to Rs 0.15

This drop of 0.05 is due to time decay but my question is here delta ( say at leat at 0.05 ) did not work. I mean at 0.05 delta with price drop of Rs 50, premium should have been increase by around Rs 2.50 but that did not happen.

Does it mean, delta worked at 0 and is this because it is near expiry?

If this price drop happened 10 days before , the effects of Rs 2.50 would have worked?

Is delta and Theta have co relation?

I mean, delta drops as time decay and over the price VS delta proportion?

I will appreciate, if you answer