7.1 – Remember these graphs

Over the last few chapters, we have looked at two basic option type’s, i.e. the ‘Call Option’ and the ‘Put Option’. Further, we looked at four different variants originating from these 2 options –

- Buying a Call Option

- Selling a Call Option

- Buying a Put Option

- Selling a Put Option

With these 4 variants, a trader can create numerous different combinations and venture into some really efficient strategies, generally referred to as ‘Option Strategies’. Think of it this way – if you give a good artist a colour palette and canvas he can create some fascinating paintings, similarly a good trader can use these four option variants to create some outstanding trades. Imagination and intellect is the only requirement for creating these option trades. Hence before we get deeper into options, it is important to have a strong foundation on these four variants of options. For this reason, we will quickly summarize what we have learnt so far in this module.

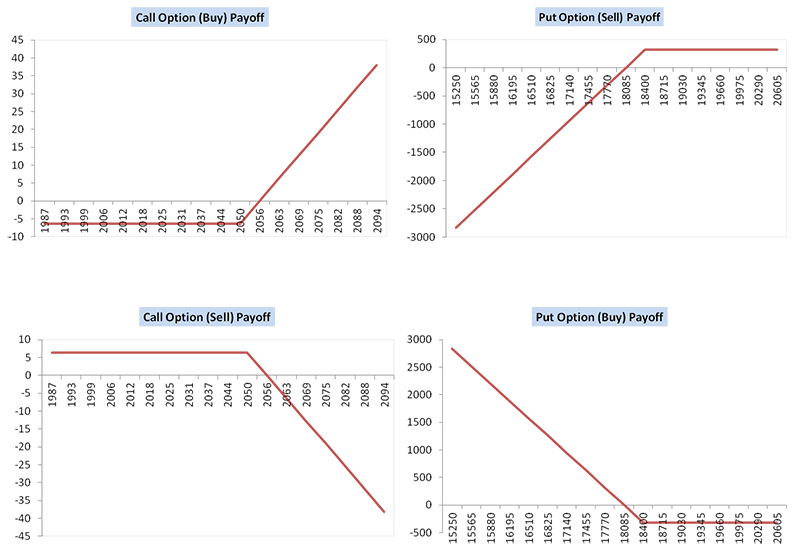

Please find below the pay off diagrams for the four different option variants –

Arranging the Payoff diagrams in the above fashion helps us understand a few things better. Let me list them for you –

- Let us start from the left side – if you notice we have stacked the pay off diagram of Call Option (buy) and Call option (sell) one below the other. If you look at the payoff diagram carefully, they both look like a mirror image. The mirror image of the payoff emphasis the fact that the risk-reward characteristics of an option buyer and seller are opposite. The maximum loss of the call option buyer is the maximum profit of the call option seller. Likewise, the call option buyer has unlimited profit potential, mirroring this the call option seller has maximum loss potential.

- We have placed the payoff of Call Option (buy) and Put Option (sell) next to each other. This is to emphasize that both these option variants make money only when the market is expected to go higher. In other words, do not buy a call option or do not sell a put option when you sense there is a chance for the markets to go down. You will not make money doing so, or in other words, you will certainly lose money in such circumstances. Of course, there is an angle of volatility here which we have not discussed yet; we will discuss the same going forward. The reason why I’m talking about volatility is that volatility has an impact on option premiums.

- Finally, on the right, the pay off diagram of Put Option (sell) and the Put Option (buy) are stacked one below the other. Clearly, the pay off diagrams looks like the mirror image of one another. The mirror image of the payoff emphasizes the fact that the maximum loss of the put option buyer is the maximum profit of the put option seller. Likewise, the put option buyer has unlimited profit potential, mirroring this the put option seller has maximum loss potential.

Further, here is a table where the option positions are summarized.

| Your Market View | Option Type | Position also called | Other Alternatives | Premium |

|---|---|---|---|---|

| Bullish | Call Option (Buy) | Long Call | Buy Futures or Buy Spot | Pay |

| Flat or Bullish | Put Option (Sell) | Short Put | Buy Futures or Buy Spot | Receive |

| Flat or Bearish | Call Option (Sell) | Short Call | Sell Futures | Receive |

| Bearish | Put Option (Buy) | Long Put | Sell Futures | Pay |

It would help if you remembered that when you buy an option, it is also called a ‘Long’ position. Going by that, buying a call option and buying a put option is called Long Call and Long Put position respectively.

Likewise, whenever you sell an option, it is called a ‘Short’ position. Going by that, selling a call option and selling a put option is also called Short Call and Short Put position respectively.

Now here is another important thing to note, you can buy an option under 2 circumstances –

- You buy to create a fresh option position.

- You buy intending to close an existing short position.

The position is called ‘Long Option’ only if you are creating a fresh buy position. If you are buying with and intention of closing an existing short position, then it is merely called a ‘square off’ position.

Similarly, you can sell an option under 2 circumstances –

- You sell intending to create a fresh short position.

- You sell intending to close an existing long position.

The position is called ‘Short Option’ only if you are creating a fresh sell (writing an option) position. If you are selling with and intention of closing an existing long position, then it is merely called a ‘square off’ position.

7.2 – Option Buyer in a nutshell

By now, I’m certain you would have a basic understanding of the call and put option both from the buyer’s and seller’s perspective. However, I think it is best to reiterate a few key points before we make further progress in this module.

Buying an option (call or put) makes sense only when we expect the market to move strongly in a certain direction. If fact, for the option buyer to be profitable, the market should move away from the selected strike price. Selecting the right strike price to trade is a major task; we will learn this at a later stage. For now, here are a few key points that you should remember –

- P&L (Long call) upon expiry is calculated as P&L = Max [0, (Spot Price – Strike Price)] – Premium Paid

- P&L (Long Put) upon expiry is calculated as P&L = [Max (0, Strike Price – Spot Price)] – Premium Paid

- The above formula is applicable only when the trader intends to hold the long option till expiry

- The intrinsic value calculation we have looked at in the previous chapters is only applicable on the expiry day. We CANNOT use the same formula during the series

- The P&L calculation changes when the trader intends to square off the position well before the expiry

- The buyer of an option has limited risk, to the extent of the premium paid. However, he enjoys an unlimited profit potential

7.2 – Option seller in a nutshell

The option sellers (call or put) are also called the option writers. The buyers and sellers have the exact opposite P&L experience. Selling an option makes sense when you expect the market to remain flat or below the strike price (in case of calls) or above strike price (in case of put option).

I want you to appreciate the fact that all else equal, markets are slightly favourable to option sellers. This is because, for the option sellers to be profitable the market has to be either flat or move in a certain direction (based on the type of option). However for the option buyer to be profitable, the market has to move in a certain direction. Clearly there are two favorable market conditions for the option seller versus one favorable condition for the option buyer. But of course, this in itself should not be a reason to sell options.

Here are a few key points you need to remember when it comes to selling options –

- P&L for a short call option upon expiry is calculated as P&L = Premium Received – Max [0, (Spot Price – Strike Price)]

- P&L for a short put option upon expiry is calculated as P&L = Premium Received – Max (0, Strike Price – Spot Price)

- Of course the P&L formula is applicable only if the trader intends to hold the position till expiry

- When you write options, margins are blocked in your trading account

- The seller of the option has unlimited risk but minimal profit potential (to the extent of the premium received)

Perhaps this is the reason why Nassim Nicholas Taleb in his book “Fooled by Randomness” says “Option writers eat like a chicken but shit like an elephant”. This means to say that the option writers earn small and steady returns by selling options, but when a disaster happens, they tend to lose a fortune.

Well, with this I hope you have developed a strong foundation on how a Call and Put option behaves. To give you a heads up, the focus going forward in this module will be on moneyness of an option, premiums, option pricing, option Greeks, and strike selection. Once we understand these topics, we will revisit the call and put option all over again. When we do so, I’m certain you will see the calls and puts in a new light and perhaps develop a vision to trade options professionally.

7.3 – A quick note on Premiums

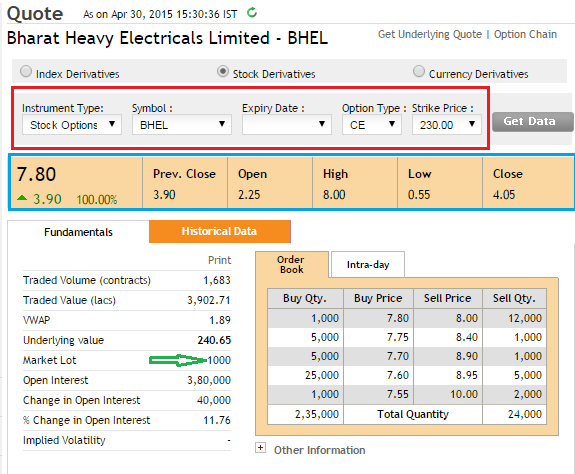

Have a look at the snapshot below –

This is the snapshot of how the premium has behaved on an intraday basis (30th April 2015) for BHEL. The strike under consideration is 230, and the option type is a European Call Option (CE). This information is highlighted in the red box. Below the red box, I have highlighted the price information of the premium. If you notice, the premium of the 230 CE opened at Rs.2.25, shot up to make a high of Rs.8/- and closed the day at Rs.4.05/-.

Think about it; the premium has gyrated over 350% intraday! i.e. from Rs.2.25/- to Rs.8/-, and it roughly closed up 180% for the day, i.e. from Rs.2.25/- to Rs.4.05/-. Moves like this should not surprise you. These are fairly common to expect in the options world.

Assume in this massive swing you managed to capture just 2 points while trading this particular option intraday. This translates to a sweet Rs.2000/- in profits considering the lot size is 1000 (highlighted in green arrow). In fact this is exactly what happens in the real world. Traders trade premiums. Hardly any traders hold option contracts until expiry. Most of the traders are interested in initiating a trade now and squaring it off in a short while (intraday or maybe for a few days) and capturing the movements in the premium. They do not really wait for the options to expire.

In fact, you might be interested to know that a return of 100% or so while trading options is not really a thing of surprise. But please don’t just get carried away with what I just said; to enjoy such returns consistently you need to develop a deep insight into options.

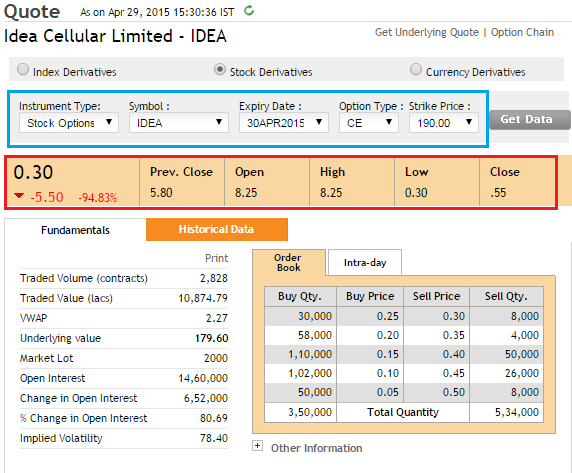

Have a look at this snapshot –

This is the option contract of IDEA Cellular Limited, strike price is 190, expiry is on 30th April 2015 and the option type is a European Call Option . These details are marked in the blue box. Below this we can notice the OHLC data, which quite obviously is very interesting.

The 190CE premium opened the day at Rs.8.25/- and made a low of Rs.0.30/-. I will skip the % calculation simply because it is a ridiculous figure for intraday. However assume you were a seller of the 190 call option intraday and you managed to capture just 2 points again, considering the lot size is 2000, the 2 point capture on the premium translates to Rs.4000/- in profits intraday, good enough for that nice dinner at Marriot with your better half J.

The point that I’m trying to make is that, traders (most of them) trade options only to capture the variations in premium. They don’t really bother to hold till expiry. However by no means I am suggesting that you need not hold until expiry, in fact I do hold options till expiry in certain cases. Generally, speaking option sellers tend to hold contracts till expiry rather than option buyers. This is because if you have written an option for Rs.8/- you will enjoy the full premium received, i.e. Rs.8/- only on expiry.

So having said that the traders prefer to trade just the premiums, you may have a few fundamental questions cropping up in your mind. Why do premiums vary? What is the basis for the change in premium? How can I predict the change in premiums? Who decides what should be the premium price of a particular option?

Well, these questions and therefore, the answers to these form the crux of option trading. If you can master these aspects of an option, let me assure you that you would set yourself on a professional path to trade options.

To give you a heads up – the answers to all these questions lies in understanding the 4 forces that simultaneously exerts its influence on options premiums, as a result of which the premiums vary. Think of this as a ship sailing in the sea. The speed at which the ship sails (assume its equivalent to the option premium) depends on various forces such as wind speed, sea water density, sea pressure, and the power of the ship. Some forces tend to increase the speed of the ship, while some tend to decrease the speed of the ship. The ship battles these forces and finally arrives at an optimal sailing speed.

Likewise the premium of the option depends on certain forces called as the ‘Option Greeks’. Crudely put, some Option Greeks tends to increase the premium, while some try to reduce the premium. A formula called the ‘Black & Scholes Option Pricing Formula’ employs these forces and translates the forces into a number, which is the premium of the option.

Try and imagine this – the Option Greeks influence the option premium; however, the Option Greeks itself are controlled by the markets. As the markets change on a minute by minute basis, therefore the Option Greeks change and therefore the option premiums!

In the future, in this module, we will understand each of these forces and their characteristics. We will understand how the force gets influenced by the markets and how the Option Greeks further influence the premium.

So the end objective here would be to be –

- To get a sense of how the Option Greeks influence premiums

- To figure out how the premiums are priced considering Option Greeks and their influence

- Finally keeping the Greeks and pricing in perspective, we need to smartly select strike prices to trade

One of the key things we need to know before we attempt to learn the option Greeks is to learn about the ‘Moneyness of an Option’. We will do the same in the next chapter.

A quick note here – the topics in the future will get a little complex, although we will try our best to simplify it. While we do that, we would request you to please be thorough with all the concepts we have learnt so far.

Key takeaways from this chapter

- Buy a call option or sell a put option only when you expect the market to go up

- Buy a put option or sell a call option only when you expect the market to go down

- The buyer of an option has unlimited profit potential and limited risk (to the extent of the premium paid)

- The seller of an option has an unlimited risk potential and limited reward (to the extent of the premium received)

- Majority of options traders prefer to trade options only to capture the variation in premiums

- Option premiums tend to gyrate drastically – as an options trader, and you can expect this to happen quite frequently.

- Premiums vary as a function of 4 forces called the Option Greeks

- Black & Sholes option pricing formula employs four forces as inputs to give out a price for the premium

- Markets control the Option Greeks and the Greek’s variation itself

“I have an objection to this statement: ‘The put option buyer has unlimited profit potential.’

The put option buyer’s profit potential exists only until the spot price on expiry falls from the strike price down to zero. The maximum profit is capped because the underlying price cannot fall below zero.”

With respect to the above explanation: the put option seller has limited loss potential, limited to the point where the spot price can fall only to zero.

Only the call option buyer has unlimited profit potential, and only the call option seller has unlimited loss potential.

Sure, thats another way to look at it.

Option trading put and call advisory

Sorry, we dont provide it here on Varsity.

Hi Karthik,

Always grateful to Zerodha varsity content, thanks a ton.

I had a question regarding short covering in stock options.

Usually price action in the underlying stock in the cash market (spot) decides the premium of its derivatives (f & o). If stock price goes up then option premium goes up or vice versa.

But how come when traders cover their shorts in derivatives, the price of stock in the cash market goes up? It appears as if the spot and derivatives have reversed their roles.

Not really, the underlying is closely tracing the spot. However there could be instances where the F&O can do their own thing, but that does not last for long. Maybe few minutes, maybe just intrday.

Sir as option buyers after capturing moment they sold premium in market.but as a option seller if written contract for one month.how it can be square off before expiry.so after getting few premium if there is chance market gaining momentum I have to become option buyers.

The same rules applies for both buyer and sellers in-terms of transactional abilities. So yes, the sellers can square off the positions, anytime they wish.

As premium=intrinsic value + Time value

So on 05 September nifty options expired,Nifty closed 25234 on expiry but nifty CE 25200 05 September option closed at 0.As intrinsic value is left as option expired why premium where not 34(25234-25200)?

You cant look at the close price, you need to look at the settlement price. Check this – https://www.youtube.com/watch?v=eJiouVUWEb0

As you said for the seller he need to hold the option till expiry for the sake of premiums, but what is the buyer buys it before the expiry from the seller?

Your position will stay open for as long as you wisk to keep it, Prem.

Sir, somewhere in these capters you said it\’s very rare for traders to exercise their option rather they trade on premium. What I understood is, if premium increases from what you have paid,( say I am an option call buyer) then you can sell it and pocket the difference. Right?

But my question is, why don\’t traders wait till expiry, because if the trade is indeed going in your direction then the profit grows exponentially. If the premium is increasing, then it means the trade is going bullish. So why pocket the small difference in premium raher than waiting to exercise the option on expiry? Is it because the risk is very high and the probability is only 33%?

Thats right, most traders prefer to exit trades before expiry, and by that I mean you can exit the trade on the day of expiry also and not necessary to wait till the close of the market (and expiry). You can check this as well – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

I’m in college, know very little about trading and have an exam on various scenarios to buy/sell corn futures. In doing so, I need to understand and explain my approach as to why I may be buying calls/puts, setting my max price vs actual price etc. is there a tutor out there who I can speak with who’d be willing to work with me on understanding the concepts.

You can read through the contents here, I\’ll be happy to answer if you have any specific questions.

Hi, so the option price is determined by the BS formula u say and market makers and market participants are the ones that trade contracts in the market. And they are the ones that quote the prices and the LTP becomes the price of the given contract. Where does the BS formula price comes here?

The prices traders quote is based on the fair value, as determined by B&S formula. For example, if a fair value of option is Rs.25, the trades would be in and around 25 and would not vary much.

Sir, thank you for sharing your knowledge on Option trading.

Sir, you said Premiums = f (Option Greeks), Option Greeks = f (market conditions) & Market conditions change every minute.

Sir, will I be right in saying that market conditions are shown by \”Change in Open Interest\” in the open chain.

Open interest = f (trader\’s sentiment). So its all interconnected to one another 🙂

Hi

Thanks Karthik

Kalyan

Happy learning!

Thanks a lot for the fantastic inputs. This is truly unbeatable.

I have a question on the screenshots. Why is the close price not matching the price displayed in bold? the screenshot is take at 15;30 hrs which means the end of the day price

For BHEL , it shows close as Rs 4.05 and current price as Rs 7.05

For Idea , it shows close as Rs 0.55 and current price as Rs 0.30

I read an z-connect article on a possible small difference. But that happens late in the evening much after market close and the difference is normally small.

The close price is the average of the last 30 minutes trading, Kalyan. So the close price will always be different from the last traded price.

Respected Sir,

uptill this level, learning was smooth

now at this point chapter 7.3 of module 5 (OPTIONS)

There is a snapshot of BHEL

Underlying value 240.65

Strike Price 230 CE

Exp. Date NIL

Premium Price Close 7.80

Here I am stuck, to my understanding so far

Intrinsic Value should have been at least 10.65

Hence Closing Price of the Premium should have been at least 10.65

But here it is only 7.80

Kindly explain where I am going wrong or where to rectify the understanding.

I shall be grateful for your response.

Regards

Sagromoy, so the premium also depends on many other factors apart from direction. So you will also have to consider that 🙂

So much information…than watching videos on YouTube… content is top notch and most important thing is you are learning by your broker… ☺️

Happy learning, Gaurav 🙂

Even in Selling call/put, the obligation is on seller and right is with buyer. Correct?

For example person A sells a Put option, it is still up to Buyer of put option whether or not to exersice the right to buy upon expiry. Right Sir?

Yes, sellers are always obligated to the buyers.

but seller can also square off the position at any time, how come sellers are obligated

What if we

1.Buy option 100 CE when market price was 90 and market reached @a. 100 b. Reached @95 c. Reached @105

2.Buy 100 PE when market is at 110 and hold it until expiry with market at a. @100 b. Reached @95 c. reached @105 hold it till expiry.

Another query as said premium going to reduce each day then why should we hold option till expiry date. In which case should we hold it till expiry what the parameters to check this.

For 1 & 2, check this – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

That depends on many factors, suggest you read the next set of chapter 🙂

Excellent course. Had a doubt though.

If I buy a call option of strike price 100 rs from an option writer (Mr. X) at say Rs 5. Now I sell this option contract itself for Rs 6 to Mr. Y (suppose). If Mr. Y exercises the option and CMP of underlying is 105. Now Mr. Y gets to buy the underlying at Rs 100 from the option writer(Mr. X) or myself (because I sold the contract to Y)?

In other words if a contract travels like X->Y->Z->A. And A is exercising, the liability or contract of A is with whom?

Since you have squared off the contract/position, you a no longer in the market. The trade is with the latest buyer and seller.

As an option seller, do we get freedom to decide on (a) Strike Price (b) Premium Amount (c) No. of Shares in a lot.

Please clarify.

Thanks.

You get to choose the strike. But lot size is standardized..and the option premium is market driven.

Hi dear sir, thank you for these valuable articles, I got very much good understanding, please make these more aspects or topics for option trading and candle chart etc.

Happy learning, Harpreet 🙂

Hi Karthik, I have a very basic question, I don\’t know how to think about it. Here it goes – if option prices are determined by a formula, then how does one trade in it? I mean when we see the market depth of a stock/index option for example, we see multiple prices being quoted by different traders, but if the price being quoted is purely the trader\’s price, then how does the price get determined by the option pricing model. I mean how does the option price adjust itself based on the factors if people are quoting it. Is it that option pricing formula is merely quantifying what the traders are likely to do in a given situation?

Dave, so it is like this. We all know what the manufacturing and marketing cost of a Rolex is. But why does it still trade at a serious premium in the market? Because that\’s how people perceive it. So options to are dictated by a theoretical price, but the market demand and supply situation rule over the theoretical price.

SIR I AM DOING NIFTY/BANK NIFTY OPTIONS SELLING … ON THURSDAY EXPIRY DAY I SELL A CALL/UPT OF RS 50 60 70 ANY MY FUND WILL BE USE AROUND 115000 RS … SIR IF BY MIKTAKE I FORGET OR BUY ON EXPIRY DAY HOW MY FUND WILL SETTLE.

The option contract will be cash settled, Ravi.

Dear Karthik,

Excellent effort on Explaining this complex subject!

I have a query.. Could pls clarify this?

Example: (Ref.08/12/22 Expiry).

On 02/12 friday close, Nifty Spot at 18696. (18700).

NIFTY 18900 PUT CLOSES AT 213. (ITM worth 204)

NIFTY 18500 CALL CLOSES AT 251. (ITM worth 196).

My QUery is: When We take these Two pairs, Same Distance (200 Pts) from the SPOT on both sides, PUT Options at almost zero premium (Just 10 pts)… But on Call Side it Trades at nearly 60 Pts Premium… (SOmetimes, its 75 pts premium on same situations)..

I request you to Explain, What such scenario Indicates? Why there is almost no premium on one side (Here PUT Side), eventhough its just 1% distance Strike from Nifty Spot, that too on first day of the fresh weekly expiry?

Pls clarify on this case, as this would help us a lot..

Eswaran, so the premium is a function of many factors. One of the explanations for this disparity is that the sellers maybe expect the market to break 18500 during the series, hence more activity/premium to this particular strike.

Good explanation to boost the confidence of a nascent options trader.

Happy with the concepts being explained in a layman\’s terms

Happy learning 🙂

How can I buy stocks myself on expiry for- a written put option (in the money) ? or I need to wait for settlement ?

You need to wait for settlement.

I am new to zerodha option trading. In a week how many times we are allowed to buy option & exit. For example I buy option 17000PE and exit. Later same week shall I buy same 17000 PE multiple times

Sir kindly suggest me how many times I can do call or put option in a day?

As many times as you want, but that said, excessive trading usually does more harm to you than it benefits you.

want open demat

sumit

8000556439

9950119876

https://support.zerodha.com/category/trading-and-markets/kite-web-and-mobile/articles/why-did-my-bank-nifty-option-order-get-rejected

Sir in this above link,

It has been told that sometimes DEEP OTM OPTIONS can’t be brought

But such SAME DEEP OTM OPTIONS can be sold.

How Sir???

Selling requires margins, Muthu, which is several times over the premium you\’d pay as a buyer.

Sir due to SEBI\’s open interest regulation, SOME OTM OPTIONS cannot be BROUGHT

But such SAME OTM OPTONS can be SOLD

https://support.zerodha.com/category/trading-and-markets/kite-web-and-mobile/articles/why-did-my-bank-nifty-option-order-get-rejected

I think the persons who SOLD earlier would be buying (and)

and the NEW SELLERS can SELL to them – will it work like this sir?

To sell you need margins, and when you square off the position, you are not creating a new position, rather just closing an existing one.

Hi Karthik,

Thank you for the wonderful study material. Just a quick one here.

If only European options are allowed in India how come one has the option to exercise while he is still bounded by the contract? Please throw some light on that

I\’ve actually discussed that in this chapter – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

Basically, they are two different things, I\’ve discussed the difference between the two in the chapter.

Hi,

I need to understand if the following examples are right with regards to square-off

I bought Call option for XYZ stock, lot size = 100, strike price = 200 and spot price = 210.

to square-off the above trade I should \”Sell Put\” for XYZ stock, lot size = 100, strike price = 200

I bought Put option for XYZ stock, lot size = 100, strike price = 200 and spot price = 190.

to square-off the above trade I should \”Sell Call\” for XYZ stock, lot size = 100, strike price = 200

I couldn\’t find any detailed explanation regarding the square-off process until now, if the square-off process has been detailed in this series, please redirect me to that part I need to understand it thoroughly.

Nathan, to square off you need to reverse the position you originally initiated. For example, if I buy 1 share of Reliance, to square off I need to sell 1 share of Reliance. Likewise, if I buy 1 lot of Call option, to square off I need to sell 1 lot of the same call option (cant be a different strike).

If a call option meets the strike price n in profit say, how to exercise. So also, put option

You cannot exercise the option, you can sell the option though.

In Option CE – if i exit less than my premium amount, whether capital will be Zero ?

Example:

Contract 17600CE

Bought Premium at Avg 277

If i sell at LTP 260 whether my captial will be zero or only will lose part of capital.

If you sell it at 260, then your loss is difference between the buy and sell value of the premium i.e. 277-260 = 17.

You should use the \”Water image\” instead of \”Mirror image\” in the pay off chart and previous chapter also when you are comparing charts side by side and up and down.

That\’s new, I\’ll check this Deedy.

Maine Manappuram jan172.5CE buy kiya tha Premium Rs 4 par. Abhi uska premium Rs 0.05 hai jo lower circuit hai. Current market price of share is Rs 153. This is ITM or OTM? Agar weekly expiry ke din koi buyer nahi mila aur main contract square off nahi kar paya to kya hoga in present situation.

Kya mujhe physical delivery Leni paregi as per sebi new rule ya zerodha already square off kar dega. Kindly reply.

I appreciate your suggestion on forex .. so a doubt what do we trade and basically what\’s the difference between USDINR and INRUSD

USD INR is what we trade. The easiest way to remember is – what does $1 cost in INR? This is USDINR. If you are looking at INR USD then you need to ask what does Rs.1 cost in USD? which as you can imagine is a tiny fractional number.

Before continuing ahead … Is data on premium and options Available in form of charts say candlestick..?

Yeah, you can look at the charts of options.

Hello again sir the chapters are on fire honestly never felt more motivated to continue 😁🙏

I\’m 17 right now and want plenty of information and practice (dummy trading) before actually starting with real money when I get 18 and these modules contribute like 99.99% to it 🙂

Hey Chetan, I\’m glad you liked the content here on Varsity. To practise, stick to USD INR, it\’s not volatile, less risky, and you can learn all the nuances of placing an order easily with USDINR. Much better than paper trading I think 🙂

मुझे इस सम्बन्ध मे एक्सपर्ट का सुझाव और मार्गदर्शन चाहिए। कम जोखिम अधिक लाभ फुल प्रूफ के साथ लाइव ट्रेडिंग।

Mobile No-. 09125325672

In Hindi Language.

I have a doubt in the table of Options positions. What is the difference between the two views? \”Bullish\” and \”Flat or Bullish\”?

Flat to bullish is that you expect the price to either stay neutral or increase, but not fall 🙂

Sir,

Can you explain me what is shot covering.

Eg. Nifty close at 16900

At 17000 1 CR call writers are their.

Then if the next day open above 17200, then some analysts say huge short covering will happen and nifty will go high. But how i it happens?

Kiran, short covering is basically traders closing out their short position, which means they have to buy back their positions. Because traders are buying (to close their open position), markets tend to go up for a bit.

How long does it take for option scripts to react to changes in the underlying asset prices. When I see out of the call options of BANKNIFTY I see that the OTC options have there own price discovering mechanisms. Would anyone like to comment upon it.

It reacts instantly, Jay. When you look at options, don\’t just look at the premium, look at the changes in bid and ask.

Hi Karthik- one ws please.

If I\’m bullish on a stock which is currently beaten down to go up in one month\’s time.

Can i buy the dec call option sitting in November?

In the that case, will the time expiry make the premium worthless even if the stock prices reached strike point?

Yes, you can choose to buy either Dec or Jan call in Nov, but make sure they are liquid and tradable. Time value is something you need to take care off. Usually these options carry a huge amount of time value.

Awesome, thank you so much for the knowledge you share. I can not thank you enough…cheers!

Happy learning!

Hi Karthik, I didn\’t get \” Generally, speaking option sellers tend to hold contracts till expiry rather than option buyers. This is because if you have written an option for Rs.8/- you will enjoy the full premium received, i.e. Rs.8/- only on expiry.\”

So lets say you write an option at 8. After some time, you decide to square off at 5. The profit you make here is 3. Now, if you want to make the entire 8 as profit, you will have to buy back at 0 or say 0.1. You can do that (i.e. buy at 0 or 0.1), only on expiry.

thanks to zeridha varsity..spreading knowledge..

Happy learning!

Hi Karthik, your modules are very good and give a lot of clarity. I have a few question since I am very new to this aspect of trading.

Hypothetical example:

I write a call option with the below assumptions:

Nifty @18000 for a premium of Rs.100. Validity is till the last Thursday of the month.

Buyer pays premium of Rs.100 and buys.

Questions:

1. Premium goes down to Rs.50. As a buyer I make a loss if I want to sell the brought option, right?

2. Premium goes up to Rs.125. As a buyer I make a profit of Rs.25 if I want to sell the brought option, right?

3. If Nifty goes to 18200, and premium goes to 125, as a writer I am staring at a loss. Can I close/square off the call option mid term?

Thanks

1) Yes, thats right

2) Yes

3) Yes, you can. No need to wait till expiry.

Hi sir

I have two queries

1)can we do intraday options on nifty and shares

2)let me know if yes I apply short straddle on share or nifty can

I square off immediately

As it is risk in my range bound (ie risk neutral)

1) Yes, you can.

2) Yes, you can.

Dear Sir,

Below are the details of option I am analysing .

My question is Target p&l show 915 does this mean this position is in profit of 915 if I exit this position now?

Premium paid is 9750.

QNIFTY 18151.85 +0.2%

B 1x 28 OCT 18300 Pe

Target price 10618

LTP: 10500

Entry Px: 9703

Target P&L: 915

Max Profit At Expiry

9.05L

Max Loss At Expiry

-9,703

Reward/Risk ratio

93

Breakeven at expiry Ⓒ

18105.95

Not sure where you are seeing the target P&L, but to identify the P&L, all you need to do is consider the difference between the purchase price of premium and sell price of premium and multiply by the lot size.

Dear sir if have

ICall sell position and I hedge the position by call buy at different strike price, same lot size both position.

What will happened during settlement Whether I need take delivery of stock?

That depends, if both options are ITM, then no physical delivery. The position will be net off against each other. If both are OTM, then both expire worthlessly. Otherwise, whichever option is ITM, that will be settled physically.

Is it possible

If yes then how??

Suppose PE of a Stock XYZ is sold at ₹ 10 @ strike price ₹ 100/-

After a week It is reduced to ₹2 and spot price increases to ₹ 180.

Then profit booking took place in market and spot price reduces to

₹ 120. But now the premium is increased to ₹20.

Expiry is short of one week.

Do the premium keep changing and adjusted like this .

This is possible, Ritu. Time to expiry plays an important role here.

Thanks a lot sir for explaining in such a easy way.

Good luck, Deepak!

Good Article for beginners to understand options trading .

Happy reading, Abhishek.

I sold a Put Options of a stock, and at the moment it is showing \’Out of Money\’. My question is on the day of expiry in case it remains \’Out of Money\’, do I need to square-off, or maintain margin in my trading account? Or in this situation I have to do nothing, it will automatically settle, and I will receive the premium at which I sold the Put? Thank you.

No need, since the OTM option will expire worthless anyway.

Hello Sir,

In stock options I don\’t know which order to use and how to put stoploss for that trade. I did put a stoploss in trade but price fell below it and still stoploss didn\’t trigger. I seek for your help and guidance on this. Thanking you in anticipation 😊

Latesh, this is can happen when stock prices move quickly. I\’d suggest you use a stoploss limit, and put the trigger price lower than the current price, so that your SL gets triggered as a market order but with protection.

Very useful information.

Thank you !

Happy reading!

Sir, If I am trading in options and suppose market is trading on 15,513. I\’ve put a call option on 15550 CE. And the market goes upto 15,538. Then I\’d sell my lot! Now market goes down again at 15,520.. can I again buy the same trade i.e, 15550 CE on the same day??? To make extra profit?

Yes, you can intrday trade options.

What if sold option becomes in the money on expiry?

Do I have to pay difference as loss or I can also pick delivery of shares at sold strike price?

All ITM stock options will be physically settled.

If on day of expiry, if my call option (long) is in the money, what happens if I don\’t (or am not able to) square it off. Will it be settled in my favor?

2 scenarios:

1. Spot of ABC closes at 204 at the end of the day. I had bought a lot of 1000 of 200 call at RS. 10. If I don\’t square off, I will receive 4000 whereas will pay 10000. Net out 6000.

2. I had bought a lot of Rs. 2. I will receive net income 2000.

Is my understanding correct?

It wont be squared off or settled till expiry. Alternatively, if you sell it, the difference between the buy and sell price of the premium will be settled.

1) What matters before expiry is the price at which you buy and sell the premium

2) Same as above

How to see number of contracts on nse official website..?

Please check the Open interest.

I have a one confusion please clear it by given example suppose i am buying call option of 10 june 21 at the strike of 15750, of 1 lot, and at same time i am also buying another 1 lot of call at strike of 15550 and same time i am selling 2 lot at the srike of 15650 .

Means same time in a morning i am taking position with 3 trades

15750 CE BUY 1 LOT OF NIFTY

15650 CE SELL 2 LOT OF NIFTY

15559 CE BUY 1 LOT OF NIFTY

NOW position are opened but after few hours i want to take exit at spot of 15670

So i calculated i am making profit of 80 points its correct or not ?

As per my calculations :-

15670 – 15750 = -80 or loss in buying

15670 – 15650 = -20×2 lots = -40 for selling

In last 15550 – 15670 = 120 point

So 120-40 = 80

Is it correct ?

Please answer

Not really, it depends on what price you bought the option and the price at which you sold. Suppose you bought an option at 10 and sold the same at 13 on the same day, then the profit is Rs.3 in this case.

Hi karthik brother. Really amazing. Kindly send me your whatsapp number 9037022131

If I buy nifty CE date 03/06/21 @ Rs. 60/- . On due date it will become zero / Rs.0 05 ?

Or I buy PE , on due date it will become zero / Rs. 0.05 ?

It depends on the market movement, right?

Hi Karthik, Kindly clarify these doubts of mine, I\’m very confused with how premium\’s works for \’Seller\’ and what happens when Seller Exits!!

Day1, 9:30AM : Assume a contract occurred between A(buyer) and Z(seller). \’A\’ bought the option at 80 premium.

Sam Day(Day1), 9:45AM: Premium increased to 100. Seller \’Z\’ exits the position, where \’Y\’ has comes in to place. Now the Contract is between \’A\’ (Buyer) and \’Y\’ (Seller).

Question1: In the above case, what\’s the Premium that Seller(\’Y\’) gets ? Is it 100 or the 80 ? Since originally the agreed contract was at premium 80 between \’A\’ and \’Z\’ !!

Question2: When the premium increased to 100. The first seller \’Z\’ got panicked and exited immediately. Now, will there be any Loss/Profit for \’Z\’?

The contract is a floating rate…keeps changing every minute. When A and Z struck a deal, the premium was 80. Now both of them can exit anytime they wish. When Z decided to close the position, Z has to buy back. That means, he will be buying at 100 (at a loss) and the new seller selling at 100 is Y.

I\’d suggest you read this chapter to understand this better – https://zerodha.com/varsity/chapter/open-interest/ , I\’ve used a similar example that you\’ve quoted.

How to decide a Strike Price.

Please Enlighten me

This entire module is for that, please do check 🙂

Dear Sir,

Thank You for providing such beneficial information to all pupil who wants to learn the stock market from scratch before entering the real game.

I\’d like to inform you about the data which the site provides whereas the data which the app provides have a huge difference and also there\’s no update regarding Module 12 in the app which shows \’Coming Soon\’ for the last 2 years. Can you provide an update on these queries?

Also, I\’ve noticed some issues with Varsity App Qualification Test and Certification Test wherein some answers I selected were changed unanimously and due to which scores during those tests were affected. Please provide the updates regarding the issue ASAP.

Thank You for your humble efforts.

Module 12 – which is inner worth is available on the app Sanskar. Check the home page in the app. About the questions, can you please tell me what issues you\’ve noticed.

Hi Karthik, Could you kindly help me understand this scenario. Assume Day 5 is expiry.

Day1: Person A and Person Z has entered in to the contract. A is buyer and Z is seller. Strike price for PVR is 1200, premium paid by buyer is 80. At this point, all that Seller(Z) gets is limited to 80(at the expiry), if his prediction turns out to be true.

Day2: Premium went upto 100. Buyer(A) exits his position @100 which was then bought by someone called C. Now a new buyer came into place called \’C\’. My 1st question is, As the A exits and C comes in place, does the contract now lies between C and Z ? If yes, then Is the premium that Seller(Z) gets is now changed to 100 ?

On the Same Day(Day2) or Day3: Can the seller now exit his position by taking away the increased premium ?

Yes, the new agreement is between C & Z. However, the premium you paid is to A, so A get to make a quick buck here i.e 100-80 = 20. C and Z can exit their positions anytime, no need to wait till expiry.

If I short 33200 put @400

And at expiry market closes at 33100

What will be my profit and loss.

The option will have an intrinsic value of 100, but since you\’ve received 400, you will get to keep 300 as profits here.

The seller of the option has unlimited risk but minimal profit potential (to the extent of the premium received)

Assuming you put an appropriate stop loss, say stop loss=premium received.

Then unlimited risk no longer exists right?

Yes, thats always possible.

Sir, in zerodha varsity there is no chapter for NSE option chain learnig. Please see that.

You can check this – https://zerodha.com/varsity/chapter/moneyness-of-an-option-contract/

In intraday, if one is an option buyer, can he trade in any strike price provided that he buy that premium at low and exit at high even though spot price does not reach that strike price.

Ex. Spot Price of BankNifty 31900 at 10:00 am,

Strike Price selected: 32300

Premium: 320 (during buy)

If the market is bullish and the Spot Price of BankNifty is 32200 at 12:00 am and Premium of 32300 reaches from 320 to 520 and we exit.

Will I be profitable?

Yes, you can exit at any given point, Saurabh. No need to hold to expiry.

Is positional and intraday/scalping option different or same?

Both are very different. Positional trading = you expect to capture a large move with positions held over few trading sessions. Intraday is exact opposite i.e. small profits, held for a short span.

on the last day of settlement i.e 15th April what would be the premium on call and put of strike rate of 14950 nifty when the current mkt rate is say 15000 and starts moving above the strike rate of 14950.

It depends on the exact spot price. CE will have an intrinsic value if the spot is higher than the strike and put will have an intrinsic value if the spot is lower than the strike. I\’ve given the exact formula in the chapter.

Available hai sir abhi aap ke paas

Hi Karthik,

I have some queries related to the premium received or pay by an option holder/writer.

1. You have mentioned that the option writer only gets the premium on the day of expiry, but if I want to square off my position, I can buy an option. Will I not receive the difference in the premium amount on the day of squaring off, or I have to wait till expiry?

2. Selling a future or an option both require margins. But for the futures, if I ignore MTM Losses and look only at the big picture, will it be good to go for shorting futures only as options have higher margins? Also, buying futures require margin but buying options- that will direct me to buy options only and overlook the alternatives. Please correct me if I am wrong in my predictions.

Anyway, I love Zerodha, and a great thumbs up to you and the varsity team for making my life in stock trading very easy.

1) Yes you will be settled on T+1 basis if you were to close out the position. Btw, if you are to hold to expiry, then you will get the full premium assuming the option is worthless.

2) The margins are similar, not different. Option buying has limited risk, hence there is no margin

Thanks, and happy learning!

Hi, I have a doubt. Suppose I have bought a PUT option at 10rs then I exit at 12rs. Exiting means that I have now become a seller and may face unlimited loss on the expiry?

No, exit means that you are out of the market and any further movement in the market has no consequences to you.

Karthik . Great and extremely understandable learning modules.

Can you suggest any site where demo trading can be practiced from live Data for Indai.

Maybe you should check Sensibull website.

Under fund tab my option premium is showing in negative , what is the meaning of that.

The total amount you have paid to purchase options. This value will be negative if you have received funds for shorting/writing options.

Check this Haarish – https://support.zerodha.com/category/trading-and-markets/margin-leverage-and-product-and-order-types/articles/kite-dashboard-and-fund-values-calculation

Thank You so much sir for your effort. I was able to atleast begin my first trade in options after this chapter, i think my basics of options were cleared to some extent and these articles also drive away the fear of the unknown.

Thanks once again 🙂

Happy to note that, Divya! Keep learning 🙂

If I get gain from change in prices of premium how is it considered in return filling ?

Considered as business income, assuming you are a regular trader.

when there is a buyer for each seller in derivative trading then why I could not find buyer for my call option on Expiry day..

The availability of the buyer and seller depends on that particular moment in the market 🙂

Can we have more examples for this kind of topics?

There are quite a few after this chapter, Kavita.

Got it. Thank you, Karthik.

Good luck, Rohit!

Thank you, Karthik. But isn\’t the seller Obligated to sell the shares to the buyer at expiry? If the spot price is moving up sharply well and above the strike price and if the Buyer hasn\’t exited yet (Possibly because he prefers physical settlement and is hoping to get the shares from the seller at the agreed upon strike price since it looks like the spot will be way higher than the strike at expiry) and is holding on to the contract, can the seller still Exit before expiry? If that is the case, then can\’t all Sellers just pocket the premium and exit the position immediately thereby guaranteeing confirmed profits?

Apologies if my question is based on a wrong assumption.

Rohit, that\’s the advantage of a \’tradable asset\’. At any point, the buyer or the seller can simply choose to exit their position. When they exit, the same position is held by a new buyer or seller. Like this, the contract will continue to exist, until it expires on the expiry day.

This is a very helpful module. Thank you.

My query is of a very beginner level.

For a call option buyer, he/she can make profits by trading on the Premium instead of waiting till expiry. But what about a call option seller? A seller receives premium from the buyer. So can you please explain what happens if a seller exits before expiry?

Its the same for both buyer and seller, Rohit. The seller too can exit whenever he/she desires.

If I sold Call Option, and on the day of expiry the spot price is below strike price then do I need to do anything to exit the trade or it will automatically get squared-off at premium of Rs 0?

You need not have to do anything, it will be automatically squared off to 0.

Hi Kartik,

Will it not be prudent for the initial trader to buy Option Calls or puts rather than be a seller of either.

Atleast initially till one gets a feel of the trades before venturing into selling

Yes, at least in the initial stages.

Hi karthik,

Thank you for the module as I have learnt from your module better than anuone yet.

therefore I have doubts for you to assist me with:-

1:- Explain ITM and OTM elaborately as got confused that spot price is above strike price or vice versa. hope you will assist.

2:- Explain margins

To understand the concept of ITM and OTM, you need to understand the concept of time value and intrinsic value. I\’ve explained that in the moneyness of the options chapter. Basically, ITM = In the money, these are options which have intrinsic value OTM options don\’t have intrinsic value and has only time value.

Sir,

I am very new to F&0 segment.

I have sold ITC JAN 190 PUT OPTION ie PE for Rs 1.15 premium.

Plz guide me what to do..

Whether to wait till expiry or shall I square off. If I square off, how much premium will I get?

If I hold till monthly expiry how much capital shall I need to buy ITC at Rs 190, Is that Rs 190*3200.

Plz help me.

Obliged,

I got the answer for last question sir.. I was just little confused

Good 🙂

Hi sir..

Call Option (buy) and Put Option (sell) next to each other. This is to emphasize that both these option variants make money only when the market is expected to go higher

Sir we put sell only make money when spot price is below strike price and you have mentioned the market should be bullish.. Please clarify this..

Thats right Chandu, to profit out of a short PUT position, you expect the market to go higher.

sir can we sell call or put option on expiry day and square off our position by buying them again at low price and till what time i have to buy them again on expiry day and what will happen if forget to square off my position

Yes, you can.

Hello sir, you have been doing a great job with these modules which are really helping us a lot. I only had one question in mind that are these modules on options sufficient for a person to learn about this if he is planning to become a full time trader or does he have to do an additional online course and if so which course would you recommend?

I\’d believe so, this module along with the next has everything you need to know about options trading.

The content is excellent, especially for layman understanding. Can we get access to these chapters in some form? Paid subscription or can we buy these modules for academic interest and learning? Thanks a lot for sharing on online platform.

YOu have free access to it here itself, right?

Hi,

I am Getting error in zerodha while buying fresh call option of \’bank nifty\’ today for 01st Oct expiry with strike price as 22500 and its present spot value is 21100. Error is;

\”Fresh buy orders are not allowed for this strike due to OI restrictions.Buy for range 21000-21500 only\”. What does it mean?

This means that the strike that you are trying to buy is not permitted due to restrictions.

Thanks sir for reply.

But, on expiray day its not guranteed that some buyer will available. Many times squaring call on expiry day becomes diffcult due to no buyer, so in such case , for OTM , loss is restricted to primium paid only but big risk on ITM , as in case of \’no buyer\’ in ITM, you need to take physical delivery of all stocks i.e. you should have that much money in pocket, so always better to square off positions before 1-2 days before expiry day irrespective of OTM/ITM calls and OTM have low risk compared to ITM , does this understandinh is correct ?

Jaggi, there is no concern of settlement from the exchange as the contracts will get settled even if there are no sellers available. However, you need to go through the physical settlement process. If you don\’t want to take these chances, then yes, its better if you sell before expiry. Ensure you deal with liquid contracts so that you avoid getting stuck in illiquid contracts.

Yes sir,

But we need to have that much money to take delivery. For e.g. in case of IDEA , slot is of 45,000 stocks, and in case of ITM if we do not exercise call option on expiry day , we need to invest said money to take delivery (e.g. if stock price is 10/- INR, we need to have 4.5 Lacs to take this delivery), is this understanding correct?

Thats right. But you can always square off the position before expiry too.

Hi Sir,

Thanks for your guidance , i made 45 K in less than 2 weeks via call options only (out of money call only). Still I am beginner , some basic fundas wants to clear.

Advantage of out of money call is , you don\’t need to bother to exercise it till expiry day , max loss is your premium and no limit for max profit.However catch here is if it hits/crosses strike price then it got converted into \’in the money\’ call option. For e.g. I bought IDEA OCT CE 12 and on expiry day only if it hits 12.50/- and if i do not exercise my call till eod on expiry day , I need to buy entire lot i.e. 45,000 stocks in case of IDEA, is this correct? As \’in the money\’ options needs to exercise at any cost before expiry and even-though it was purchased/bought as out of money , it got converted into \’in the money\’ due to rice in stock price , then \’In the money\’ is huge risky than \’out of money\’ and what is point on going for \’in the money\’ call option?

Jaggi, yes, you will have to take delivery of ITM options. Taking delivery is not really a huge risk, you can still take delivery of stocks and sell it in markets for a higher rate right?

Hello Sir,

I am new to options. I have some basic query.

Suppose I bought call options in OCT of a stock say RELIANCE NOV CE 2500 , current price of stock (spot value) is 2200/- and premium is 8/- , lot size is 505 , so I invested 505*8= 4040/- , now on same day or next day only (in OCT only) RELIANCE stock price becomes 2300/- (it still did not hit strike price of 2500/-), and my premium prize becomes 20/- and total value of my lot becomes 505*20=10,100/- , so my profit is 10100-4040=6060/- , so what is use of strike price then? It anyways grows till it hits strike price?

Rajesh, strike price matters a lot. Especially when it comes to taking delivery on expiry days.

Thanks sir.

One more thing,

Suppose i buy one call option of XYZ trade having spot price as 2000/- and strike price as 2050/- , primum is 8/- and lot size is 500 ,so I invested 500*8=4000/- , on same day or on next day , spot price becomes 2035 and primum also moves to 12/- , now still it did not hit strike price , but still i am in profit i.e. 12-8*500=2000/-, so here , i will sell said option and gain profit , will not wait to hit for strike price , so any harm in this process ? Or we cannot sell option call like stocks ?

Yes, you can do this, no need to wait till expiry.

Hello,

I have one question , I buy option call when infosys stock price was at 1030/- INR , with premium as 7/- INR (1 lot of 1200 stocks) for 1050 as strike price , so I pay premium as 1200*7= 8400/- INR, now on expiry day, market crashes and infosys share price becomes 975/- INR and OTM call option primum price becomes 0.5 (5 paisa), and there was no buyer for the same (unable to sell said call option ), so here I will loose 8400/- or more?

That\’s right, you lose the premium money in case the option expires out of the money.

Hi Karthik,

If we use naked sell option ( for call or put)with stop loss , it is risk free. The loss is restricted to the stop loss. Am i correct?

Yeah, but it is not \’ risk-free\’, its \’risk contained\’ 🙂

Now suddenly in 2nd week, the stock spot value jumps backs to sat 990 Rs….. my losses from futures stock are getting less… but 1000CE call sell will definitely go towards losses AM I CORRECT ?????????

Excerpt From Vikas Rana\’s question,

Pl answer what to do, Exit or else?

There nothing like \’definite\’ in the market, Shankar.

Hi karthik sir,

Can you please clarify something for me,

Lets say I\’m Bearish on a share and in the beginning of the month I sold its call option with a premium of 10/- per share. Let\’s say the lot size was 1000.

The next day premium reduces to 6/- per share. Now i want to book profit so,

1) I\’ll have to buy the call option to exit the position and book profit on premium, right?

If I\’m correct then,

2) when I buy the call option I\’ll have to pay premium @6/- per share, right?

3)Then the difference between the premium I received and the premium I paid(i.e. 10000-6000=4000) will be my profit, is that right?

Thats absolutely correct, Rishabh.

Dear sir, I am beginner in options trading and doing studies of different different option strategies , I would like to know if I am using STRADDLE + BUTTERFLY strategy example sbi is having strike price of 200, then I am USING STRATEGY

BUY 210 CE

SELL 200 CE

SELL 200 PE

BUY 190 PE

In this case I can receive a good premium against sold 200 CE and PE , but I would like to know if I want to exit from strategy before expiry then in this case it will deduct my recieved premium amount ?

Yes, if you exit out of the positions, then the P&L will be based on the premium value at exit.

Karthik, could you please explain this?

\’Generally speaking option sellers tend to hold contracts till expiry rather than option buyers. This is because if you have written an option for Rs.8/- you will enjoy the full premium received i.e. Rs.8/- only on expiry.\’

I did not understand this. What are the scenarios in which a seller may sell/square it off? Is there a loss due to squaring off both ITM and OTM?

You sell for Rs.8, you will get to retain this amount only if you buy it back at 0. It will goto 0 on expiry, provided the option is worthless (OTM). Have explained this in the module.

Sir ,I have a positional trade which I have taken one week ago in options .Can I convert that trade into MIS today? If yes then can that be done in both long and short positions? Thank you sir.

Sir, Can I convert NRML positional trade into MIS after a week on expiry day? THANKS.

Meaning?

THANK YOU FOR THE PROMPT REPLY.

But i did not understand about margin benefit.

Which part of the margin benefit, Narasimha?

Please clarify if I can write/sell a covered call option and collect premium on HDFC securities platform.

I have one lot of ITC shares in my dmat account with them.

I am willing to deliver the shares if the price goes beyond the srike price.

Other wise I will keep the premium

Yes, you can. However, you will not get any margin benefit for this.

can i buy an option call with strike price lower than the spot price? If yes, the spot price is already higher than the spot price, then will i make a profit or when is the loss?

Yes, you can buy any strike you wish. When you buy, you have to pay for the premium. So there is a cost. You will make money only if the price of the premium increases.

Ok sir got your point. My bad. But what you said matters only when we try to square off our position anytime before expiry, right? At the date of expiry the value at which premium trades is irrelevant. Only the Premium fixed as Payable/receivable(at the time of buying and selling respectively) is considered. Isn\’t it?

Yes, at expiry, what matters is the intrinsic value of the option.

Sir I understand that Option greeks are going to play a role in determining the appropriate Premium, but i am still a little curious to know one thing,

If RIL is trading @1997.7Rs and someone sells a 1800RIL PE @Premium of 5.9Rs then from that Put option seller\’s perspective the premium should go higher as RIL\’s share price goes over 2000Rs, but from a Put option buyer\’s perspective the premium should go lower. So then how is a an adept Premium value fixed?

Thanks.

Arti, irrespective of call or Put, the option seller wants the premium to go lower to the price which she has sold and the buyer wants the price to go higher from the price she has bought at.

Also Sir I want to start with rs 3000 (savings) as I am a student now so no active income. What would you suggest where should I start trading from equity or currency trading or something else. Asking this because I read on quora that with little amount one can start trading in currency. Please tell me which should be best for a begginer.

Thank you very much.

I\’d suggest you get used to the act of buying and holding stock in the initial days. Once you get used to it, you can to explore trading.Straight away starting to trade can be a daunting affair.

Sir, I am a complete newbie into trading along with technical analysis should one watch news also. Please tell me from where one can get news is it sites like monecontrol.

Also sir what should be minimum amount to start trading?

There is no minimum amount to start. You can start with as low as 500 also. Yes, news helps in building a view. You can check out https://pulse.zerodha.com/ to get a clutter-free news aggregation experience.

Sir,

The options premiums that change every second when we trade in zerodha are all driven by supply/ demand market forces or automatically calculated backend based on Black Scholes formula by the exchange ?

Thanks in Advance

Supply-demand, guided by a fair price as derived from a B&S calculator.

Hi

I am a newbie to option

I would like no know that in a Call option trade on expiry date if trade becomes ITM in intraday , but on closing share price will below the stike price. In such condition contract will expired or excuted.

Thank you

No, in that case, the option is still OTM. The point is that the option should be OTM upon expiry, during the day is ok.

very well explained, looking forward to learn more

Happy learning.

Thank you so much Sir.

u taught me a lot of things in very simple language.

Honestly i would not have lost so much money if i would have studied this.

definitely would recommend any beginner to go through all the topics.

Thank you .

Happy reading, Siddharth 🙂

sir what happen when we buy a call option of a strike price which is below the spot price ?

That will be an ITM option, premium will be higher.

sir one more doubt ,

i go through the NSE website and kite chart for the paticular share ( RELIANCE) today , dated 6 july

sir there were difference of 0.05 – 0.1 in certain figures when i compared the figures of open high low close from NSE website to that of KITE chart directly

Is it because of round figures or something else?

That\’s possible, do check this – https://tradingqna.com/t/why-does-two-charts-of-the-same-timeframe-look-different-on-the-same-platform/4715

sorry sir , but i am still confused .The example above stated of BHEL shows LTP at market close differ from that of CLOSE price .LTP at market close become closing price then why there is a difference in the figures in the example mentioned above

Rajat, that is the closing price. I took this screenshot a few minutes after the market closing. There is no difference of any sort.

hello sir,

one basis concept is drilling me , as per the screenshot shared above of BHEL , Open low close high , all figures are stated but beside them a figure on the left side is there of 7.8 showing a increase of 100 % from 3.9 . I though it was current market price but market was close while taking screenshot of this stock so what does this price reflect ?

It was the LTP at market close.

Hi All,

If I have buy some call option for a particular month. If strike price is not achieved. So can I move this to another months. Paying some more premium. Once month end all money is gone when strike price is not hit.

That\’s right, Vivek. If by expiry the stock does not move higher than the strike price, you will lose all money.

Thanks for reply.

Are both situations beneficial?

Depends on the market circumstances.

If I already have 20 shares of XYZ stock in my portfolio @Rs.80/share then

Kindly resolve the query: Suppose, I sell a call Option on 3 JUN for monthly expiry of any stock XYZ of 20 shares/lot @100 price.

Current market price of stock is Rs.80/share.

First Condition is, on expiry if stock goes to Rs. 110 then I have to sell all my holding shares @Rs. 110 per share.

Second Condition is, on expiry if stock goes to Rs. 50 then I got premium amount as profit.

Am I right?

Kindly ignore previous post.

1) Yes, in this case, you will have to bring stock, which you already have in your DEMAT

2) Yes, in this case, you can retain the entire premium

Kindly resolve one query

Query 1: Suppose, we sell a call Option of any stock XYX of 20 shares/lot @110 price. So, margin will be something in thousands.

Now, First Condition is, he buys it @90 during intraday. What will be the profit? 400 INR?

Second Condition is, if he buys next day @90, will the profit be the same? i.e., 400 INR?

Am I right?

1) You make a profit of 30 here, multiplied by lot size

2) Same as above.

Hi Karthik,

Thanks for the wonderful explanation. Per you explanation, traders can create different combination of call and put options to make profit.

Lets Say Nifty is at 10000 and I am bullish on the market, So

1) Buying the nifty in call options by paying the premium

Also thinking that market would go down and also would like to make profit if the market goes down

2) Buying the put option by paying the premium

In both the cases, My maximum lose is premium but if market goes in either of the direction I can make profits in any one of my trades right? Did I understand this correctly?

Thank you!

Yes, whenever you buy options, the max loss is restricted to the extent of the premium paid.

Understand, helpful… thanx a ton !

Goodluck!

Understand, but then what about a stock like reliance, I see there is an option at 1307.60. How is that decided. My question at what point and who is the first initiator of a particular option.

So as an individual can i write an option like 1308 ? or does the exchange define an option and then buyers and sellers work basis that?

Like I said, the strike price intervals depend on the price of the underlying. For example, if a stock is priced at 75, there is no point having 50 Rupee strikes. The strikes will be around 2.50 here. For any stock, look at the option chain and you\’ll know which strikes are available.

ok, with regards

\”3. How does one write a new option, when i look at the nifty option chain I dont see an option like 10105, or 11025 or 11075 etc. How are such options written for trade ? can i as individual do it or is it made available by the exchange.\”

So for example when i search for say a reliance Jun 1308 pe, it doesnt show up that value. Even if i search for a 10105 CE it adds the 10100 option? so how do this.

Nifty strikes are available 50 point interval, so odd lots like 11025/75 etc are not available. The strikes depend on the underlying asset.

Hi Karthik,

So i have being reading the chapters trying to understand options. Please check if my understanding is right and if you can help me solve the doubts

Say i am a option seller and say spot nifty is 9500 and I have sold 1 lot call for NIFTY CE 10500 Jun 25 @ Rupees 10

Question 1:

1. If I have sold the call today at 10 rupee premium, the premium fluctuates through the day so say by 3 pm the premium is at 8. How does one unwind this position ? I purchase the same call at 8 and the position closes and i make 2 rupees on the position and similarly for put If i have sold the put at 10 and intraday it falls to 8 I purchase the put and close the position with 2 rupee profit ?is this understanding correct ?

2. If I were to hold the above position for say 10 – 15 days or even till expiry, in the interim when the call/put premium fluctuates. Or even an increase in the premium on intra day basis, Does it have an impact on my margin ? Say if the premium were to jump to say 12

3. How does one write a new option, when i look at the nifty option chain I dont see an option like 10105, or 11025 or 11075 etc. How are such options written for trade ? can i as individual do it or is it made available by the exchange.

4. Why are time value and intrinsic values not specified as a value on say the nifty option chain ?

1) Yes, the option premium trades just like a stock

2) There will be, but at 12 it won\’t be much and nothing to do from your end

3) You load that strike on the MarketWatch and click sell, thats it:)

Hello sir..

I have a doubt regarding premium.

Example, buy BANKNIFTY xxxxx CE at ₹45 and sell Same at ₹60. I am making +15.

now, will I get only 15 or premium+15 as return?

In short, will I get my premium back if i sell before expiry?

You will get 60, which means a 15/- profit over your investment.

Thanks again Mr. Karthik for giving prompt response to my query.

So, if we sum up all asked doubts in an example-

Buying Reliance Jun 1500 CE @34 for the shares of 505 per lot, it will cost the premium of 17170 INR and no matter whether I will sell it today or any other day, in case it rises above 34, that will be the complete profit despite paying 17170 INR as premium. Right?

Yes, for example, if it goes to 40, you will make 6 * lot size as profit.

Hello Mr. Karthik, Thanks for responding to my query.

If in case of monthly or weekly expiry, then will the premium or margin also be paid? if we get in the trade in the morning and square off the trade before day closing?

Yes, the premium for long and margin for short will be applicable.

First of all I would like to thank you for sharing such a beautifully explained article.

I have a little confusion in my mind. I beg your pardon if in case it sounds silly as I am newbie. 🙂

Query 1: Suppose, we buy an Option of any stock XYX of 20 shares/lot @110 price. So, premium will be 110×20=2200 INR.

Now, First Condition is, he sells it @130 during intraday. What will be the profit? 400 INR or 2600 INR?

Second Condition is, if he sells next day @130, will the profit be, 400 INR or loss of 1800 INR? As premium gets deducted from the profit.

Query 2: Suppose, we sell an Option of any stock XYX of 20 shares/lot @110 price. So, margin will be something in thousands.

Now, First Condition is, he buys it @90 during intraday. What will be the profit? 400 INR?

Second Condition is, if he buys next day @90, will the profit be the same? i.e., 400 INR?

Query 3: It actually linked to above two, i.e., during intraday option trading, we don\’t have to pay premium or margin, right? we only have to pay premium or margin if we keep the trade for next day, right?

I would be really obliged if you clear this confusion, Thank you!

1) Yes, that is correct. The premium paid is premium * lot size. If you bought and 110 and sold at 130, your profit is 20*lot size. The same holds true irrespective of which day you sell.

2) Yes, margins will be applicable for selling an option. In this case, your profit will be 110-90 = 20, so 20*lot size. The same holds true irrespective of which day you buy.

3) You need to pay the premium or margin for intraday as well. However, if you are using MIS, the margin gets reduced.

Thnak you sir. That I understand. What I wanted to understand is how sudden change in premium can affect my PL. Is it possible that premium values appreciate and my oerall PL turn negative? Since I am selling an ITM put and if it remains or ITM, won\’t premium increase day by day?

Yes, premium changes every instance, so will your P&L.

Hi Sir!

Say I sell a NIFTY [email protected] with NIFTY spot as 9031. This means till 8966 I am profitable below which my loss start. Say tomorrow is expiry and due to some reason option prices rise to 200 for same 9150 strike and market starts falling but still remained at 8970. Here will I make profit of 183.8 premium I receive or loss of (200 – 183.8) = 16.2 due to increase in premium now?

Thanks and Regards

Saurav

When you write a put, you will make a profit upon expiry as long as the spot is at or above the strike, in which case you get to retain the entire premium. You make a loss if the spot moves below the strike.

Thanks for your kind words, Karthik!

I hope you recover your losses quickly. Good luck.

Karthik,

Both expire on 28 May 2020.

Hi Karthik….

M in a deep mess and need your help…. I purchased 2 lots of Nifty May 8900 PE @CMP 196.5 and 6 lots of BANKNIFTY May 17000 PE @ CMP 480 on 20th May.. Both these options are OTM as of today and are trading at much lower rates… My P&L shows around -40,000…😢…

Please guide me on what can I do to get out of this put problem..

Sorry to hear this. Unfortunately, there is nothing much that can be done. You either have to take this hit or hope that the market moves in your favour and you get an exit.

How much is the leverage I get in mis

You can check that here – https://zerodha.com/margin-calculator/SPAN/

Sir, I am new to options and I have account in zerotha

I have doubt regarding buying and selling options.

Sir ,my question is can I do trade in (for say: Banknifty options or any stocks options) same as like stocks but I want to ask can I do trade in premiums.

Let\’s say I want to trade in Banknifty 21st may 16000 PE and I buy trade with premium 11 rupees and after few minutes when it reaches 15 and I sell it and when it again comes down and I short sell when it goes down at rupee 14 premium and again after few minutes I buy it at 12 premium. Can I do like that trade and what will be my profit if I take quantity lot size of Banknifty is 20 and I take 2000 quantity means 100 lot.

And same question is for call side means let\’s say if I take trade in Banknifty 21st may 22000 CE in intraday and I buy their premium at rupee 13 and after few minutes sell it goes to 22 and vice versa . Can I do trade like that in intraday and what will be my profit if I take quantity 2000 means 100 lots in bank nifty.

And can I take margin in zerotha for intraday in options in this strategy,. How much is that margin ?

I am new to options trading and I am confused to buy and selling call and put .I only want to do trade in intraday ,not hold until expiry because I was already doing trading in intraday in stocks and now I want to apply same strategy in options in this way in intraday, please help us?

Is this possible in options in intraday?

Yes, Vikrant. You can trade-in options premium, just like the way you would with the stocks. No problem with this. While placing the order, choose MIS product type for additional leverage.

No need to hold till expiry.

Thank You Karthik Rangappa Sir for sharing the point wise query reply……and that too very fast within the same day …………. Can you able to give me link of some video learning lesson on SHORT SELL / write of any stock cash market , stock & indices in options market (not future market) , hedging…….because though we read articles , but video with live exapmles are easy to catch

Let me look for these Jatin. I\’m sure there are many on youtube.

Today 14 May 2020 Indigo was trading at Rs.971 , when i done far out of the money (OTM) call CE1160 at 14.80

I\’m not sure if I get your query fully, can you please share more context? Thanks.

Sir,

I am new to option short sell