13.1 – The Curvature

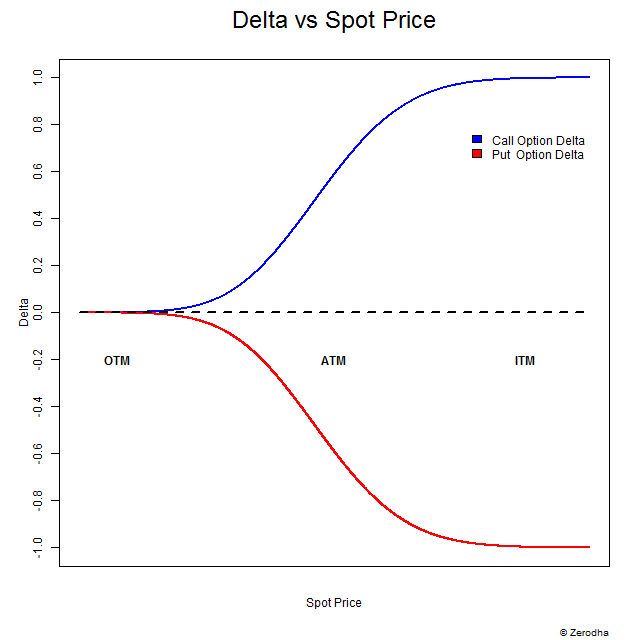

We now know for a fact that the Delta of an option is a variable, as it constantly changes its value relative to the change in the underlying. Let me repost the graph of the delta’s movement here –

If you look at the blue line representing the delta of a call option, it is quite clear that it traverses between 0 and 1 or maybe from 1 to 0 as the situation would demand. Similar observations can be made on the red line representing the put option’s delta (except the value changes between 0 to -1). This graph reemphasizes what we already know, i.e. the delta is a variable, and it changes all the time. Given this, the question that one needs to answer is –

- I know the delta changes, but why should I care about it?

- If the change in delta really matters, how do I estimate the likely change in the delta?

We will talk about the 2nd question first as I’m reasonably certain the answer to the first question will reveal itself as we progress through this chapter.

As introduced in the previous chapter, ‘The Gamma’ (2nd order derivative of premium) also referred to as the curvature of the option gives the rate at which the option’s delta changes as the underlying changes. The gamma is usually expressed in deltas gained or lost per one-point change in the underlying – with the delta increasing by the amount of the gamma when the underlying rises and falls by the amount of the gamma when the underlying falls.

For example consider this –

- Nifty Spot = 8326

- Strike = 8400

- Option type = CE

- Moneyness of Option = Slightly OTM

- Premium = Rs.26/-

- Delta = 0.3

- Gamma = 0.0025

- Change in Spot = 70 points

- New Spot price = 8326 + 70 = 8396

- New Premium =??

- New Delta =??

- New moneyness =??

Let’s figure this out –

- Change in Premium = Delta * change in spot i.e 0.3 * 70 = 21

- New premium = 21 + 26 = 47

- Rate of change of delta = 0.0025 units for every 1 point change in underlying

- Change in delta = Gamma * Change in underlying i.e 0.0025*70 = 0.175

- New Delta = Old Delta + Change in Delta i.e 0.3 + 0.175 = 0.475

- New Moneyness = ATM

When Nifty moves from 8326 to 8396, the 8400 CE premium changed from Rs.26 to Rs.47, and along with this the Delta changed from 0.3 to 0.475.

Notice with the change of 70 points, the option transitions from slightly OTM to ATM option. Which means the option’s delta has to change from 0.3 to somewhere close to 0.5. This is exactly what’s happening here.

Further, let us assume Nifty moves up another 70 points from 8396; let us see what happens with the 8400 CE option –

- Old spot = 8396

- New spot value = 8396 + 70 = 8466

- Old Premium = 47

- Old Delta = 0.475

- Change in Premium = 0.475 * 70 = 33.25

- New Premium = 47 + 33.25 = 80.25

- New moneyness = ITM (hence delta should be higher than 0.5)

- Change in delta =0.0025 * 70 = 0.175

- New Delta = 0.475 + 0.175 = 0.65

Let’s take this forward a little further, now assume Nifty falls by 50 points, let us see what happens with the 8400 CE option –

- Old spot = 8466

- New spot value = 8466 – 50 = 8416

- Old Premium = 80.25

- Old Delta = 0.65

- Change in Premium = 0.65 *(50) = – 32.5

- New Premium = 80.25 – 32. 5 = 47.75

- New moneyness = slightly ITM (hence delta should be higher than 0.5)

- Change in delta = 0.0025 * (50) = – 0.125

- New Delta = 0.65 – 0.125 = 0.525

Notice how well the delta transitions and adheres to the delta value rules we discussed in the earlier chapters. Also, you may wonder why the Gamma value is kept constant in the above examples. Well, in reality, the Gamma also changes with the change in the underlying. This change in Gamma due to changes in underlying is captured by 3rd derivative of underlying called “Speed” or “Gamma of Gamma” or “DgammaDspot”. For all practical purposes, it is not necessary to get into the discussion of Speed, unless you are mathematically inclined or you work for an Investment Bank where the trading book risk can run into several $ Millions.

Unlike the delta, the Gamma is always a positive number for both Call and Put Option. Therefore when a trader is long options (both Calls and Puts), the trader is considered ‘Long Gamma’, and when he is short options (both calls and puts) he is considered ‘Short Gamma’.

For example, consider this – The Gamma of an ATM Put option is 0.004, if the underlying moves 10 points, what do you think the new delta is?

Before you proceed, I would suggest you spend a few minutes to think about the solution for the above.

Here is the solution – Since we are talking about an ATM Put option, the Delta must be around – 0.5. Remember Put options have a –ve Delta. Gamma, as you notice, is a positive number, i.e. +0.004. The underlying moves by 10 points without specifying the direction, so let us figure out what happens in both cases.

Case 1 – Underlying moves up by 10 points

- Delta = – 0.5

- Gamma = 0.004

- Change in underlying = 10 points

- Change in Delta = Gamma * Change in underlying = 0.004 * 10 = 0.04

- New Delta = We know the Put option loses delta when underlying increases, hence – 0.5 + 0.04 = – 0.46

Case 2 – Underlying goes down by 10 points

- Delta = – 0.5

- Gamma = 0.004

- Change in underlying = – 10 points

- Change in Delta = Gamma * Change in underlying = 0.004 * – 10 = – 0.04

- New Delta = We know the Put option gains delta when underlying goes down, hence – 0.5 + (-0.04) = – 0.54

Now, here is a trick question for you – In the earlier chapters, we had discussed that the Delta of the Futures contract is always 1, so what do you think the gamma of the Futures contract is? Please leave your answers in the comment box below :).

13.2 – Estimating Risk using Gamma

I know many traders define their risk limits while trading. Here is what I mean by a risk limit – for example, the trader may have a capital of Rs.300,000/- in his trading account. Margin required for each Nifty Futures is approximately Rs.16,500/-. Do note you can use Zerodha’s SPAN calculator to figure out the margin required for any F&O contract. So considering the margin and the M2M margin required, the trader may decide at any point he may not want to exceed holding more than 5 Nifty Futures contracts, thus defining his risk limits, this seems fair enough and works really well while trading futures.

But does the same logic work while trading options? Let’s figure out if it is the right way to think about risk while trading options.

Here is a situation –

- Number of lots traded = 10 lots (Note – 10 lots of ATM contracts with a delta of 0.5 each is equivalent to 5 Futures contract)

- Option = 8400 CE

- Spot = 8405

- Delta = 0.5

- Gamma = 0.005

- Position = Short

The trader is short 10 lots of Nifty 8400 Call Option; this means the trader is within his risk boundary. Recall the discussion we had in the Delta chapter about adding up the delta. We can essentially add up the deltas to get the overall delta of the position. Also, each delta of 1 represents 1 lot of the underlying. So we will keep this in perspective, and we can figure out the overall position’s delta.

- Delta = 0.5

- Number of lots = 10

- Position Delta = 10 * 0.5 = 5

So from the overall delta perspective, the trader is within his risk boundary of trading not more than 5 Futures lots. Also, do note since the trader is short options, he is essentially short gamma.

The position’s delta of 5 indicates that the trader’s position will move 5 points for every 1 point movement in the underlying.

Now, assume Nifty moves 70 points against him, and the trader continues to hold his position, hoping for a recovery. The trader is obviously under the impression that he is holding 10 lots of options which is within his risk appetite…

Let’s do some forensics to figure out behind the scenes changes –

- Delta = 0.5

- Gamma = 0.005

- Change in underlying = 70 points

- Change in Delta = Gamma * change in underlying = 0.005 * 70 = 0.35

- New Delta = 0.5 + 0.35 = 0.85

- New Position Delta = 0.85*10 = 8.5

Do you see the problem here? Although the trader has defined his risk limit of 5 lots, thanks to a high Gamma value, he has overshot his risk limit and now holds positions equivalent to 8.5 lots, way beyond his perceived risk limit. An inexperienced trader can be caught unaware of this and still be under the impression that he is well under his risk radar. But in reality, his risk exposure is getting higher.

Now since the delta is 8.5, his overall position is expected to move 8.5 points for every 1 point change in the underlying. For a moment, assume the trader is long on the call option instead of being short – obviously, he would enjoy the situation here as the market is moving in his favour. Besides the favourable movement in the market, his positions are getting ‘Longer’ since the ‘long gamma’ tends to add up the deltas. Therefore the delta tends to get bigger, which means the rate of change on premium concerning the change in underlying is faster.

Suggest you read that again in small bits if you found it confusing.

But since the trader is short, he is essentially short gamma…this means when the position moves against him (as in the market moves up while he is short) the deltas add up (thanks to gamma) and therefore at every stage of market increase, the delta and gamma gang up against the short option trader, making his position riskier way beyond what the plain eyes can see. Perhaps this is the reason why they say – shorting options carry a huge amount of risk. In fact, you can be more precise and say “shorting options carry the risk of being short gamma”.

Note – By no means I’m suggesting that you should not short options. In fact, a successful trader employs both short and long positions as the situation demands. I’m only suggesting that when you short options, you need to be aware of the Greeks and what they can do to your positions.

Also, I’d strongly suggest you avoid shorting option contracts which has a large Gamma.

This leads us to another interesting topic – what is considered as ‘large gamma’.

13.3 – Gamma movement

Earlier in the chapter, we briefly discussed that the Gamma changes concerning the change in the underlying. This change in Gamma is captured by the 3rd order derivative called ‘Speed’. I won’t get into discussing ‘Speed’ for reasons stated earlier. However, we need to know the behaviour of Gamma movement so that we can avoid initiating trades with high Gamma. Of course, there are other advantages of knowing the behaviour of Gamma, and we will talk about this at a later stage in this module. But for now, we will look into how the Gamma behaves concerning changes in the underlying.

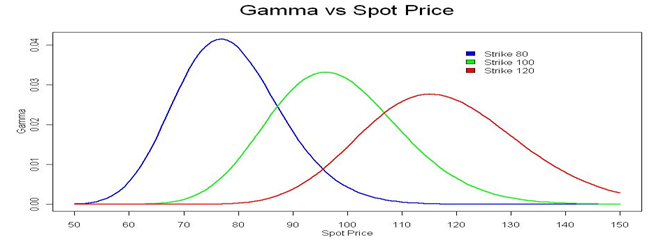

Have a look at the chart below,

The chart above has 3 different CE strike prices – 80, 100, and 120 and their respective Gamma movement. For example, the blue line represents the Gamma of the 80 CE strike price. I would suggest you look at each graph individually to avoid confusion. In fact, for the sake of simplicity, I will only talk about the 80 CE strike option, represented by the blue line.

Let us assume the spot price is at 80, thus making the 80 strike ATM. Keeping this in perspective we can observe the following from the above chart –

- Since the strike under consideration is 80 CE, the option attains ATM status when the spot price equals 80

- Strike values below 80 (65, 70, 75 etc) are ITM and values above 80 (85, 90, 95 etx) are OTM options.

- Notice the gamma value is low for OTM Options (80 and above). This explains why the premium for OTM options doesn’t change much in terms of absolute point terms; however, in % terms, the change is bigger. For example – the premium of an OTM option can change from Rs.2 to Rs.2.5, while the absolute change in is just 50 paisa, the % change is 25%.

- The gamma peaks when the option hits ATM status. This implies that the rate of change of delta is highest when the option is ATM. In other words, ATM options are most sensitive to the changes in the underlying.

- Also, since ATM options have the highest Gamma – avoid shorting ATM options.

- The gamma value is also low for ITM options (80 and below). Hence for a certain change in the underlying, the rate of change of delta for an ITM option is much lesser compared to ATM option. However, do remember the ITM option inherently has a high delta. So while ITM delta reacts slowly to the change in underlying (due to low gamma) the change in premium is big (due to high base value of delta).

- You can observe similar Gamma behaviour for other strikes, i.e. 100, and 120. In fact, the reason to show different strikes is to showcase the fact that the gamma behaves in the same way for all options strikes

Just in case you found the above discussion bit overwhelming, here are 3 simple points that you can take home –

- Delta changes rapidly for ATM option.

- Delta changes slowly for OTM and ITM options.

- Never short ATM or ITM option with a hope that they will expire worthless upon expiry

- OTM options are great candidates for short trades assuming you intend to hold these short trades upto expiry wherein you expect the option to expire worthlessly

13.4 – Quick note on Greek interactions

One of the keys to successful options trading is to understand how the individual option Greeks behave under various circumstances. Now besides understanding the individual Greek behaviour, one also needs to understand how these individual option Greeks react with each other.

So far, we have considered only the premium change concerning the changes in the spot price. We have not yet discussed time and volatility. Think about the markets and the real-time changes that happen. Everything changes – time, volatility, and the underlying price. So an options trader should be in a position to understand these changes and its overall impact on the option premium.

You will fully appreciate this only when you understand the cross interactions of the option Greeks. Typical Greek cross interactions would be – gamma versus time, gamma versus volatility, volatility vs time, time vs delta etc.

Finally, all your understanding of the Greeks boils down to a few critical decision making factors such as –

- For the given market circumstances, which is the best strike to trade?

- What is your expectation of the premium of that particular strike – would it increase or decrease? Hence would you be a buyer or a seller in that option?

- If you plan to buy an option – is there a realistic chance for the premium to increase?

- If you plan to short an option – is it really safe to do so? Are you able to see risk beyond what the naked eyes can spot?

The answers to all these questions will evolve once you fully understand individual Greeks and their cross interactions.

Given this, here is how this module will develop going further –

- So far, we have understood Delta and Gamma.

- Over the next few chapters, we will understand Theta and Vega.

- When we introduce Vega (change in premium concerning the change in volatility) – we will digress slightly to understand volatility based stoploss

- Introduce Greek cross interactions – Gamma vs time, Gamma vs spot, Theta vs Vega, Vega vs Spot etc

- Overview of Black and Scholes option pricing formula

- Option calculator

So as you see, we have miles to walk before we sleep :-).

Key takeaways from this chapter

- Gamma measures the rate of change of delta.

- Gamma is always a positive number for both Calls and Puts.

- Large Gamma can translate to large gamma risk (directional risk)

- When you buy options (Calls or Puts) you are long Gamma.

- When you short options (Calls or Puts) you are short Gamma

- Avoid shorting options which have a large gamma.

- Delta changes rapidly for ATM option.

- Delta changes slowly for OTM and ITM options.

Special thanks to our good friend Prakash Lekkala for providing the Greek graphs in this and other chapters.

The change in Gamma due to changes in underlying is captured by 3rd derivative of underlying called “Speed” or “Gamma of Gamma” or “DgammaDspot”.

I think there is a small correction in this sentence,

The change in Gamma due to changes in underlying is captured by 3rd derivative of PREMIUM called “Speed” or “Gamma of Gamma” or “DgammaDspot”.

As, The underlying price is just a variable — we don’t take “Greeks” of the underlying itself.

All Greeks (Delta, Gamma, Speed, etc.) are derivatives of the option price (premium) with respect to underlying or other factors.

I would like to take a moment to sincerely thank you for sharing such valuable knowledge about trading. Your guidance has not only helped me understand the market better but has also given me clarity and confidence in my learning journey. What once felt confusing now feels structured and achievable because of your insights. I truly appreciate the effort, consistency, and dedication you put into helping others grow. Your work is making a real difference.One day, I hope to meet you in person and personally convey my gratitude.

Thanks for the kind words, Venu, and also thanks for pointing out the error 🙂

Hi Karthik Sir,

You gave this example in this lesson.

For example consider this –

Nifty Spot = 8326

Strike = 8400

Option type = CE

Moneyness of Option = Slightly OTM

Premium = Rs.26/-

Delta = 0.3

Gamma = 0.0025

Change in Spot = 70 points

New Spot price = 8326 + 70 = 8396

New Premium =??

New Delta =??

New moneyness =??

Let’s figure this out –

Change in Premium = Delta * change in spot i.e 0.3 * 70 = 21

New premium = 21 + 26 = 47

I have small doubt here, here you calculated the change in premium using this formula

Change in Premium = Delta * change in spot i.e 0.3 * 70 = 21

For all 70 points move the delta will not be same as 0.3, so the calculation 0.3*70 =21. Is this correct ? Every point change the underlying, the delta also changes because of Gamma. Please let me know if my understanding is right ?

Yes, technically no, there will be minor variations in delta. That said, its a good approximation.

Never short ATM or ITM option with a hope that they will expire worthless upon expiry

OTM options are great candidates for short trades assuming you intend to hold these short trades upto expiry wherein you expect the option to expire worthlessly

Can you little elaborate what worthless & worthlessly here mean.

By worthless I mean they will expire without any value attributed to the option. Basically expire as out of the money option.

When would it make sense to buy an option in the hopes that it will expire?

GAMMA FOR FUTURES IS ZERO

Gamma captures convexity. Options have curvature in their payoff (non-linear), but futures don’t.

Therefore, futures lack gamma risk — delta doesn\’t change with the underlying price.

HELLO, KARTHIK SIR

STARTED VARSITY TOUR JUST FOR SOME EXTRA KNOWLEDGE AND TO MAKE SOME BUCKS OTHER THAN REGULAR INCOME. BUT KNOW SPENDING MOST OF MY TIME ON VARSITY DUE TO ITS EASY AND CLEAN EXPLAINATION OF TOPICS.

WANT TO JOIN THE TEAM OF GREAT MINDS LIKE IN ZERODHA, SO THAT I CAN ALSO MAKE MY DREAMS TRUE.

Thats right, Futures dont have Gamma. Happy learning 🙂

Namaste sir,

Under the 13.1 heading in example

Change in premium= old delta*(underlying movement)

But if gamma is there so delta must change continuously so it must follow S= ut+ (1/2)at^2.

where S is change in premium.

please guide

Thank you.

Sorry, dint really get your query. But in general – with change in underlying, gamma changes, and hence the delta changes, and hence the premium also changes.

S= ut+ (1/2)at^2.

where S is change in premium.

To answer your question, first need to clarify on following

what is u, t, a?

Hi @karthik, thanks for all the wonderful articles, it\’s gold mine and would love to meet you one day.

Just one understanding here, so in order for us to make money , the default assumption is we need to predict the market, be it in equity trading or in derivates. Can we infer this ?

Thanks, Rohit. Yes, that is the underlying fact. Basically, be in a position to either predict direction or volatility 🙂

Answer is Zero for Future. Karthik you are awesome. The way you explain the things is really very remarkable and simple way. Thanks for preparing study materials for us. Sinc I am beginner I was not looking into this deltas, gamma and other Greeks. but now chapter by chapter its increasing my excitement and looking for what a good strategy considering DELTA where few traders do follow for neutral strategy like short iron condor or short iron butterfly.

Happy to know Poonam. I have shared the link to the videos in the previous comment you posted; I hope you find that useful. Happy learning 🙂

gamma of a futures contract would be 0

Yes, thats right.

So basically, if a trade is favouring you, then gamma shoots up

If a trade is against you, then gamma shoots down.. Does it make sense?

In a sense yes and you can extend this to all greeks 🙂

As you said that shorting ITM & OTM are risky as the gamma is high and also with the hope that they\’ll expire worthless. So what are the chances that this is true? Also does it mean one should never short ATM and ITM?

You can use the delta as a proxy for the probability of the option expiring ITM. So if the delta of an option is 0.6, then you can think that the probability of that particular option/strike expiring ITM is 60%.

so if the underlying goes up/down, the new delta value will be negative? since shown in the example below.

Yes, the delta changes based on the changes in the underlying value.

I am following the Option Greek series and I am very happy that I started learning from zerodha verasity platform, Slowly I am getting insights about many things like movement of premium and how to deal with premium while trading. Everything has been explained in a very lucid manner. Thank you

Thanks Vivek, I\’m glad you liked it. Happy learning 🙂

Hello Karthik,

had doubt in example mentioned above. here gamma should be negative since it is a short position right?

Let’s do some forensics to figure out behind the scenes changes –

Delta = 0.5

Gamma = 0.005

Change in underlying = 70 points

Change in Delta = Gamma * change in underlying = 0.005 * 70 = 0.35

New Delta = 0.5 + 0.35 = 0.85

New Position Delta = 0.85*10 = 8.5

therefore actual gamma = -0.005

new position delta = -8.5

is this error or maybe I am wrong somewhere. please help me understand this.

I think its short put right?

Hello Karthik,

have doubt in following:

The trader is short 10 lots of Nifty 8400 Call Option; this means the trader is within his risk boundary. Recall the discussion we had in the Delta chapter about adding up the delta. We can essentially add up the deltas to get the overall delta of the position. Also, each delta of 1 represents 1 lot of the underlying. So we will keep this in perspective, and we can figure out the overall position’s delta.

Delta = 0.5

Number of lots = 10

Position Delta = 10 * 0.5 = 5

Shouldn\’t the delta of position = -5 since it is short call?

Puts have -ve delta, so short put becomes positive.

very interesting and very difficult to understand.In fact, options trading is not easy, which is why 9 out of 10 traders make losses here.ufffff….😐

Yes, options are complex, and takes time to figure 🙂

then what about the premium, will it depend on new delta or the old delta

Yes, the premiums too change with the change in the underlying.

Hi Karthik, could you please explain this statement,

\”Never short ATM or ITM option with a hope that they will expire worthless upon expiry\”

And also in the first example,

\”\”Change in Premium = Delta * change in spot i.e 0.3 * 70 = 21

New premium = 21 + 26 = 47

Rate of change of delta = 0.0025 units for every 1 point change in underlying

Change in delta = Gamma * Change in underlying i.e 0.0025*70 = 0.175

New Delta = Old Delta + Change in Delta i.e 0.3 + 0.175 = 0.475

New Moneyness = ATM\”\”

Does the new premium depend on old delta value(0.3) or the new one(0.475)

Thats right, old delta changes with the change in underlying and that is dependent on the gamma of the option.

Hi Karthik,

The old delta changes with underlying but when calculating the new premium we use the old delta itself and then calculate the new delta?

Or do we first calculate new delta and then use the new delta value to calculate new premium?

We use the old delta to get the new premiun, and then the new delta for subsequent calculation.

where to get the real time chart for values of Gamma of nifty options during live trading hours..

waiting for reply..

No, this is not possible. But do check once with Sensibull.

Thank you for detailed explain about gamma, what is the reason to change the gamma value

The change happens due to the change in the underlying price change.

hello sir

in the example given below u have told that we have shorted the call option taking 10 lots into consideration then how come delta value will be 0.85 if the situation goes 70 points against our favour which is 70 points increase

So from the overall delta perspective, the trader is within his risk boundary of trading not more than 5 Futures lots. Also, do note since the trader is short options, he is essentially short gamma.

since we are shorting new delta should be -0.5 + 0.35

Now, assume Nifty moves 70 points against him, and the trader continues to hold his position, hoping for a recovery. The trader is obviously under the impression that he is holding 10 lots of options which is within his risk appetite…

Let’s do some forensics to figure out behind the scenes changes –

Delta = 0.5

Gamma = 0.005

Change in underlying = 70 points

Change in Delta = Gamma * change in underlying = 0.005 * 70 = 0.35

New Delta = 0.5 + 0.35 = 0.85

New Position Delta = 0.85*10 = 8.5

The easier way to think about it is that the underlying is gaining in value, which means the stike is getting closer to or more in the money, which means the delta should increase. Therefore the delta gains.

Thanks Sir, You have written everything over here, We don\’t need any paid course at all.

Thanks, yes, you dont really need a paid course 🙂

Happy learning!

Sir, I think the Gamma of the Futures contract is Zero.

Thats right.

The reply section ain\’t working. Anyway my question was-

Nifty at 20070

strike price 20250CE OTM

Premium 5.2 Gamma 0.0012 Delta 0.09

if we expect the market to move till 20250 that is 180 pts then the delta should be at 0.5 but if we calculate the gamma then 0.012*180= 0.216

Add delta- 0.09+0.216= 0.3

if 20250 becomes ATM when nifty moves from 20070 to 20250 then why is the delta at 0.3? which should be at 0.5

For which u said to confirm the value, as i have a pic of that values which i had taken from sensibull.

let me know if possible to send you that pic for confirmation.

thankyou !

Gamma for the future contracts must be 0 so it won\’t affect its delta from 1. 🙂

Thats right, Ajay. Futures does not have any gamma.

Sir how can I find the Value of gamma for ex delta for ATM is 0.5 to 1 like what about gamma

There are no ranges like that for Gamma, Limith.

Nifty at 20070

strike price 20250CE OTM

Premium 5.2 Gamma 0.0012 Delta 0.09

if we expect the market to move till 20250 that is 180 pts then the delta should be at 0.5 but if we calculate the gamma then 0.012*180= 0.216

Add delta- 0.09+0.216= 0.3

if 20250 becomes ATM when nifty moves from 20070 to 20250 then why is the delta at 0.3? which should be at 0.5?

Where did you get the values of Delta and gamma? Anyway, delta will be ard 0.5, may not be exact 0.5. But that said, it wont be 0.3 as well. Please double check your values once.

Hi

I believe there is some confusion in the graph of delta versus spot for put option. I think it must be as follows.

Delta curve for put option in in the above graph delta vs spot must start raising from -1 delta to 0 with a positive slope representing +Gamma. That means for put options delta -1, option is in full ITM, -0.5 is ATM and 0 is OTM. If the graph is modified that way it represents Gamma is is positive either for PUT or CALL option.

with best regards

Eleswara Rao Mylangam

Thank you, let me review this again.

Gama is zero in future trade

Because underline valu increase future increase but not more thane delta are not change 1 to 0.5 and 0.5 to 0 so gama value is zero i think

Thats right.

Hi karthik, My question is how to factor in the gamma on expiry day for ATM options, is there any basic roundoff formula to calculate. Let me give you an example, let us say that around 10am on expiry nifty atm is worth 40(delta close to 0.45) and my spot Sl is 30 points, how can i factor in gamma to find how much premium would move when 30 points SL is reached within 5-10 min(Consider zero to none theta decay, as Spot SL is hit within no time). Also do i need to worry about vega while calculating the risk??

As far as I understand, you only need to factor in Vega on expiry day. You would not have to worry about gamma to play out. Otherwise also, no round off formula for this.

Sir,

If my nifty expiry is on 3rd august,

The nifty spot price is 19600,

the atm call option 19600 CE price is 5500RS Per lot. 110 rs is the premium

Delta is 0.5

and gamma is 0.0016

my position delta is 0.5*2 =1

I expect nifty spot to go up by 50 points

so the premium change will be:- (DELTA*EXPECTED CHANGE IN UNDERLYING) 0.5*50 =25 points

for my position delta will be :- 25 points *2 = 50 points

the total delta change will be:- (GAMMA*EXPECTED CHANGE IN UNDERLYING) 0.0016*50 = 0.08

new delta will be = 0.5+0.08 = 0.58

positional new delta = 0.58*2= 1.16

for every 1 point change in my underlying, my premium will be changing by 1.16 points.

I paid the premium of 220 rs(for 2 lots) and the return I got is 50 rs (for 2 lots). = 220+50= 270, (270/220)-1*100 = 22.72% ROI. 🙂

is it correct ? 🙂

I understood the gamma in respective of Call and Put option longs, but how does the gamma move react in shorting options , if you can explain it to me with an example of nifty options that I given above, it will be helpful. 🙂

The easiest way to understand the gamma movement is to imagine it to be on a slider, the movement is similar for CE and PE.

In my opinion, the gamma of a futures contract should be zero. This is because changes in the price of a futures contract do not affect the Delta, which remains equal to one.

I derived this logic by equating futures contracts with Deep ITM CE. As a CE gets deeper into ITM, the delta becomes quite close to 1. So, when the delta becomes equal to 1, it cannot increase further, and hence, the gamma gets closer to 0 when a call option gets deeper ITM.

Sir, please tell me whether my answer & logic is right or wrong.

Yes, thats right. We have discussed this in comments as well 🙂

I think I got it. We are talking about strike price here and not spot price and hence the confusion

Cool 🙂

May be it\’s too late to point out error in the article, but just want to clear out in case I have misunderstood while interpreting.

13.3 – Gamma movement – Gamma vs Spot price chart

It says – The chart above has 3 different CE strike prices – 80, 100, and 120 and their respective Gamma movement

So we are talking about call options over here, is that correct ? If it is then next statements in subsequent explanation contradicts with it and explains OTM, ATM, ITM as if its put option

2. Strike values below 80 (65, 70, 75 etc) are ITM and values above 80 (85, 90, 95 etx) are OTM options.

Am I missing something here ?

Devendra, I just read the explanation. It looks alright to me, not sure if I\’m missing something here 🙂

Volatility can have varying effects on different strike prices in options trading. The impact of volatility on different strike prices is often analyzed through the use of the Vega Greek, which measures an option\’s sensitivity to changes in implied volatility. Here are some general observations regarding the relationship between volatility and different strike prices:

1. At-the-money (ATM) options: ATM options, where the strike price is close to the current market price of the underlying asset, tend to be most sensitive to changes in volatility. As volatility increases, the prices of ATM options typically rise, and as volatility decreases, their prices tend to fall. The Vega value for ATM options is usually the highest.

2. In-the-money (ITM) options: ITM options have strike prices below the current market price (for calls) or above the current market price (for puts) of the underlying asset. These options have built-in intrinsic value. The impact of volatility on ITM options is generally less pronounced compared to ATM options. While higher volatility may still increase ITM option prices and lower volatility may decrease them, the effect is typically not as significant as with ATM options.

3. Out-of-the-money (OTM) options: OTM options have strike prices above the current market price (for calls) or below the current market price (for puts) of the underlying asset. These options rely solely on extrinsic value, as they lack intrinsic value. The impact of volatility on OTM options is usually lower compared to ATM options. Higher volatility can potentially increase the prices of OTM options, and lower volatility can decrease them, but the effect is generally less pronounced.

It\’s important to note that the relationship between volatility and different strike prices can vary depending on market conditions, supply and demand dynamics, and other factors. Additionally, the specific characteristics of each options contract, such as time to expiration, can also influence the impact of volatility on different strike prices.

Analyzing the Vega values of options at various strike prices can provide a more detailed understanding of the relationship between volatility and option prices. Options trading platforms or software often provide access to these values and can assist in evaluating the impact of volatility on different strike prices more precisely.

This is correct, but I dint really find a query 🙂

I read the volatility topic, but in all 3 chapters in varsity, it\’s not explained how this happens in each strike. Can you please help me a little more?

My exact question is \” Volatility is highest for ATM and lower as we go OTM or ITM. Also, it decreases in a linear fashion. How are some options behaving in the opposite way of gaining premium while the whole chain is losing premium? \”

Any kind of help to understand this deeper would be so much more meaningful. Thank you.

There are multiple factors at play Hesham. Premium is a function of all these factors at play. Some of these factors are –

1) Volatility

2) Theta decay

3) Directional movement of the underlying

4) Individual strike\’s demand and supply

So the premium for that particular strike which you are referring to would have baked all these factors into its premium. While volatility is one aspect, do pay attention to the particular strike\’s demand and supply. That too have a role to play in determining the premium.

Why is this nature of one PE premium decreasing while another PE is increasing, I am aware that it may decay less as it goes away from ATM due to decreasing theta value but why will it increase?? Please refer where I can read or know more about this kind of behaviour or imbalance in behaviour based on strikes

Each strike has volatility which impacts the premium, Hesham. So this is a function of that.

I have observed that the option price of say PE near the ATM is 50 rupees, a few more strikes away i.e. OTM is 20 rupees. In a sideways Market, 50 Drops to say 40 rupees, while 20 sometimes increases to say 22. Is this due to Gamma? Please help me understand

Its due to how volatility affects the individual strikes.

This is Really Rocket Science. One hell of a ride but worth pursuing.

Its fairly simple if you give it a couple of reads. Let me know if you have any queries, will be happy to help.

hi if nifty is at 17000 and i buy 1 lot of 18000 ce and i sell 16000 pe of 1 lot so where should the market move to make profit can you explain it in detail

What you have initiated here is a spread strategy, and each spread has its own set of P&L attributes, as I\’ve explained here – https://zerodha.com/varsity/module/option-strategies/.

To know the exact points at which you profit or loss, you can enter these values on Sensibull\’s platform and figure.

Dear Sir,

I am a Zerodha client and a big fan! I have been consistently profitable in Nifty Bank Nifty trading Options. I do directional trading. I only wirte ATM options. I have a concern. My ROI is very low. Margin blocked is too high. So I cannot increase position size since I have limited capital. I was thinking about two things on which I need your guidance- 1 To shift to ITM option buying with delta close 1, in which case will they be liquid enough to exit position and how to manage spread? 2 I shift to monthly ATM option buying where theta won\’t be much of a problem, but again how about liquidity and spread?

Please guide me here as I am a profitable trader looking to improve ROI as my skills far exceed my capital now.

Anand, writing ITM options itself is a bit scary thing and add to the liquidity issues, and it just does not make sense. ATMs are better that way. This is the trade-off Anand, if you want to push ROI, you will have to take a higher risk. You need to figure what keeps you comfortable and allows you a good night sleep 🙂

Many thanks for this and previous articles. this has really helped in clearing my concepts about options

Happy learning!

GAMMA of the Futures should be 1

Yeah, since Delta of Futures is 1.

Sir, in section 13.2, if nifty moves 70 points against ATM put, then the delta should decrease i.e new delta 0.5-.35= .15

And total delta for 10 lots= .15*10 = 1.5

Am I correct or should I revisit the calculations

Yup, for a call, if the spot falls, so does the delta.

I think gamma for future contracts is 0 as the delta is constant.

Yeah.

Hey Karthik!

I think you have made some serious mistake, while calculating the price of new premium, let\’s take the example you have mentioned:

Where: ->

Nifty Spot = 8326

Option = Nifty 8400 CE

Moneyness = Slightly OTM

Current Premium = 26

Current Delta = 0.3

Gamma = 0.0025

New Premium = ?

New Delta = ?

New Moneyness = ?

We know,

change in delta = gamma * change in spot

In our case, new delta = old delta + change in delta

New delta = 0.3 + 0.0025 * 70 = 0.475 (This part you have calculated correct)

Change in premium = delta * change in spot

But, here delta is not constant, which you have assumed, this is wrong.

So, dP = (OldDelta + Gamma*S)*dS, because delta is a function of Gamma and Spot

where dP = Change in premium and dS = Change in Spot price

And hence, change in premium comes out to be = (oldDelta + 1/2(Gamma * change in Spot) ) * change in spot

And so new premium = old premium + change in premium

New Premium = (0.3 + 1/2(0.0025 * 70) ) * 70 = 27.125, although the contribution with change in gamma currently seems less, but if the change in spot will be higher, the change in premium will differ a lot with your forumla.

Also, I have assumed the Gamma as constant, just to solve the problem, which is clearly not possible in real life. Correct me if I am wrong somewhere.

Rishabh, thanks. Let me check. In reality, neither gamma or delta are constant; they change continuously. I assumed a constant delta to convey the topic, like the way you assumed constant gamma for simplicity.

But I do get your point 🙂

Hi Karthik,

Thank you for all these wonderful learnings.

I have a query if I may –

Is the classification of option as OTM ATM ITM from option buyers perspective alone?

Say for a CE, if an option is OTM for buyer, it would obviously be ITM for seller right?

Example-

Option Type = CE (Buyer)

Strike Price = 100

Spot Price = 90

Moneyness = OTM

If you look at the above example from sellers perspective it would be ITM for him isn\’t it?

I think I am confusing myself. Appreciate if you can help me connect the dots where I am missing.

Thank You

The moneyness of an option is the same for both buyers and sellers. In the above case, 100 CE is OTM for both buyers and sellers.

Never short ATM or ITM option with a hope that they will expire worthless upon expiry

(please help me to understand the meaning of this line )

Thank you.

The probability of ATM and ITM expiring as an ITM option is quite high. Hence you don\’t want to risk it.

It is really commendable work that you are doing.

My doubt is how is the gamma value arrived at? As we can calculate delta, given gamma, but how the gamma is derived?

Thanks, Pariskhit. Gamma, and all the other greeks, are an output of B&S calculator.

Hello,

My question is regarding the value of delta taken as positive 0.5 in the example where we are shorting 10 calls. Why is the delta positive when we short/ sell calls? Shouldn\’t it be -0.5 and consequently the delta of the portfolio be -5 (since -0.5*10 = -5)? And then wouldn\’t a change in underlying of +70 points result in +0.35 gamma and then, a net portfolio delta of -5+3.5 = -1.5 ? Please let me know if there is some error in my understanding.

Thank you.

+ve for Delta, and -ve for the direction of trade.

Hi Karthik,

The gamma of a futures contract should be zero.

Any suggestive material to read more about the quantitative side of options theory? I want to dig deeper into the math.

Love the way you explain such complex topics in a simplistic manner.

Thanks.

Rahul, there are multiple books. I\’d suggest you check out the book reco on CQF forums.

Also you cannot simply calculate the change in premium as delta*(change in spot). At ATM there is significant gamma which you cannot ignore.

So the correct approach should be.

Change in premium = delta*(change in spot) + 1/2*gamma*(change in spot)^2

Your explanation and coverage is quiet good but I found a lot errors on Gamma topic. Please review and correct.

1. Gamma is not always positive. Its positive for all long position. A put option is a bearish position and will have negative gamma. Because as the underline increase the PE will move towards OTM resulting decrease in premium, delta and hence gamma is negative.

2. Even you wrongly tried to prove in examples, that Put options will have positive gamma.

1. Case 1 – Underlying moves up by 10 points

* Delta = – 0.5

* Gamma = 0.004

* Change in underlying = 10 points

* Change in Delta = Gamma * Change in underlying = 0.004 * 10 = 0.04

* New Delta = We know the Put option loses delta when underlying increases, hence – 0.5 + 0.04 = – 0.46

Put option loses delta when underlying increases – this is correct but -0.46 > -0.5. So by your calculation its not losing delta.

Correct approach is Gamma = -0.004

Then ->

* Change in Delta = Gamma * Change in underlying = -0.004 * 10 = – 0.04

* New Delta = We know the Put option loses delta when underlying increases, hence – 0.5 + -0.04 = -0.54

Thanks Anshu, I need to double-check this. I have started updating the content starting from the first module, will try and fix this bit soon.

Hi Karthik,

I like your literature on stock market.

In this chapter, you have concluded that \”Never short ATM or ITM option with a hope that they will expire worthless upon expiry\”.

From this chapter i understood that, as gamma is high for ATM options we should avoid shorting as there is high risk.

My doubt is how did you conclude that ITM options are not great for shorting, as gamma is lesser for both ITM and OTM compared to ATM options.

Regards.

Ah, Raju…I\’ve explained the logic in the chapter itself.

Number of lots traded = 10 lots (Note – 10 lots of ATM contracts with a delta of 0.5 each is equivalent to 5 Futures contract)

Option = 8400 CE

Spot = 8405

Delta = 0.5

Gamma = 0.005

Position = Short

The trader is short 10 lots of Nifty 8400 Call Option; this means the trader is within his risk boundary.

Sir the above extract is taken from chap 13.2

sir can you please explain how the trader is within his risk boundary.

Thank you sir.

Paul, can you please check the above comments one, we have discussed this specifically 🙂

note ;- revised question

sir i have some confusions in this chapter Gamma part 2 , going back to the lesson page 124

senario 1 of the lesson

o Number of lots traded = 10 lots

o Option = 8400 CE

o Spot = 8405

o Delta = 0.5

o Gamma = 0.005

o Position = Short

(Now, assume Nifty moves 70 points against him and the trader continues to hold

his position, hoping for a recovery. The trader is obviously under the impression

that he is holding 10 lots of options which is within his risk appetite…

Let’s do some forensics to figure out behind the scenes changes –

o Delta = 0.5

o Gamma = 0.005

o Change in underlying = 70 points

o Change in Delta = Gamma * change in underlying = 0.005 * 70 = 0.35

o New Delta = 0.5 + 0.35 = 0.85124

o New Position Delta = 0.85*10 = 8.5

correct me if i am wrong ,as short

o Delta = 0.5

o Gamma = 0.005

o Change in underlying = -70 points

o Change in Delta = Gamma * change in underlying = 0.005 * -70 = -0.35

o New Delta = 0.5 – 0.35 = 0.15

o New Position Delta = 0.15 *10 = 1.5

so this is what what needed to be written over there ?

as 70 points went against him so change in underlying will be -70 points

so Change in Delta = Gamma * change in underlying = 0.005 * -70 = -0.35

o New Delta = 0.5 +(-0.35) =0.15

o New Position Delta =0.15*10 =1.5

this is what i have assumed please correct if i have assumed wrong

You can take the absolute change in Nifty as 70. But if you want to consider the -ve sign to indicate the short position, then you will also have to consider a -ve sign with Delta since its a short position.

1. sir i have some confusions in this chapter , going back to the lesson page 124

senario 1 of the lesson

o Number of lots traded = 10 lots

o Option = 8400 CE

o Spot = 8405

o Delta = 0.5

o Gamma = 0.005

o Position = Short

(Now, assume Nifty moves 70 points against him and the trader continues to hold

his position, hoping for a recovery. The trader is obviously under the impression

that he is holding 10 lots of options which is within his risk appetite…

Let’s do some forensics to figure out behind the scenes changes –

o Delta = 0.5

o Gamma = 0.005

o Change in underlying = 70 points

o Change in Delta = Gamma * change in underlying = 0.005 * 70 = 0.35

o New Delta = 0.5 + 0.35 = 0.85124

o New Position Delta = 0.85*10 = 8.5

correct me if i am wrong ,as short

o Delta = -0.5

o Gamma = 0.005

o Change in underlying = 70 points

o Change in Delta = Gamma * change in underlying = 0.005 * -70 = -0.35

o New Delta = 0.005 -0.35 = 0.345

o New Position Delta =0.15*10 = 1.5

so this is what what needed to be written over there ?

i assumed as its short delta =-0.5 and

as 70 points went against him so change in underlying will be -70 points

so Change in Delta = Gamma * change in underlying = 0.005 * -70 = -0.35

o New Delta = 0.005 +(-0.35) = -0.345

o New Position Delta =-0.345*10 = -3.45

this is what i have assumed please correct if i have assumed wrong .

For example consider this –

Nifty Spot = 8326

Strike = 8400

Option type = CE

Moneyness of Option = Slightly OTM

Premium = Rs.26/-

Delta = 0.3

Gamma = 0.0025

Change in Spot = 70 points

New Spot price = 8326 + 70 = 8396

New Premium =??

New Delta =??

New moneyness =??

Let’s figure this out –

Change in Premium = Delta * change in spot i.e 0.3 * 70 = 21

New premium = 21 + 26 = 47

Rate of change of delta = 0.0025 units for every 1 point change in underlying

Change in delta = Gamma * Change in underlying i.e 0.0025*70 = 0.175

New Delta = Old Delta + Change in Delta i.e 0.3 + 0.175 = 0.475

New Moneyness = ATM

MY QUESTION:

when 70 points move upside then you mentioned change in Delta is=0.3*70=21,But for every one point gamma also adds value to Delta but you are not including the gamma value in calculating the NEW Premium.

According to my understanding NEW PREMIUM=old premium+[(Delta+gamma)*70]

=26+33.25

New Premium =59.25

Yup. We\’ve had this discussion earlier in the comments as well. In reality, both delta and gamma change in real-time. Gamma does not change after the delta changes.

But sir,in case of going long,in chapter 10,you have stated slightly OTM can be very impressive,so likewise in case of going short, actually itm options can be a good try, isn\’t it so?

But here why is it told OTM options are better than itm options in case of shorting

Why,sir?

No, in fact, you should never look at shorting an ITM option unless it\’s part of a strategy.

Sir,I read it in one of the questions that deep itm options have very less volume.

Is it so?

Sir if yes

why is it so?

Yes, usually the liquidity is quite low for these options.

Sir,one doubt

Why is it told \”Never short ATM or ITM option with a hope that they will expire worthless upon expiry\”

That\’s because ATM and ITM options have very high probability of expiring ITM. You want to short options which can expire OTM, hence.

Delta changes rapidly for ATM option- Why sir?

Because the gamma to is at the peak for ATM. So when gamma changes are high, so will the delta.

Hi Kartik,

Thanks for laying this down so well!

Continuing with your example:

Option = 8400 CE

Spot = 8405

Delta = 0.5

Gamma = 0.005

Position = Short

My question is that –

If the underlying moves by 70 against me -> 8405-70

New gamma = -70*0.005 = -0.35

New delta = 0.5-0.35 = 0.15

Shouldn\’t 0.15 be the new delta for me rather than 0.85 mentioned in your example?

That means if I was initially carrying a delta of 5 (10 lots * 0.5 delta) , my new position delta position becomes 1.5 (10 lots * 0.15). Which means I\’m carrying lesser risk now?

This might be way of if I\’m missing something. Can you please help me out?

YOu are short on CE, and the move against you means the underlying price has increased and therefore the delta too should increase. Keep the greeks apart and think just from your position perspective and then overlay how the greeks should behave. Hopefully that will clear things up 🙂

Hello Karthik,

Thank you detail explanation.

One query.

OTM options are great candidates for short trades assuming you intend to hold these short trades up to expiries wherein you expect the option to expire worthlessly Can you please elaborate more on this regards to Delta & Gamma.

Thanks in advance.

Simplistically, OTM options have the highest probability to expire worthless thereby the odds of you retaining the premium are high.

So gamma value can actually be negative based on my position ?

https://www.projectfinance.com/long-gamma-short-gamma/

Hi, everywhere they say long gamma is positive and short gamma is -ve but you said , Gamma is always positive number..Which one is correct

Gamma is dependent on the position you take, Bruce. Hence that statement.

where we can see gamma value of particular option strike price ?

any application?

Yes, check sensibull – https://sensibull.com/

Very very Helpful

Happy learning!

Sir, (this is about estimating risk using gamma) As i saw one of your comment u said that option transition from atm to itm so delta should gain but earlier in this chapter we learn that if position delta is -ve then underlying and options move in opposite direction so underlying gain options lose so do delta and premium right sir?

Hi sir, in estimating risk using gamma there we are shorting 10 lots of call options, delta is 0.5 then position delta should be -5 right sir?

And as underlying is against means market moving up delta should go down then how delta is 0.85 instead 0.15

I\’m confused in this section please answer my confusion.

Sir What do u mean by theata is 0.65 when the value of premium itself is Rs.25???

And How does theta decays in Weekly expiry

It means that the option premium will lose 0.65 points is all else equal. Theta decay works the same way with weekly expiry as well.

Gamma आणखी सोप्या पद्धतींमध्ये होऊ शकतो का ,समजण्यासाठी जास्त किचकट होत आहे.

कृपया याबद्दल मार्गदर्शन करावे

I think the gamma for future will be 0. The delta don\’t change with the change in underlying price value.

Please let me if i am right ?

Yes, thats right.

hi!

went through this chapter, on page number 121, i.e in first equation after the curvature :in there u explained \’rate of change of delta=\’ and \’change in delta=\’ in those two formula u told \”change in spot\” once and \”change in underlying\” once both are same or different?

The spot is the underlying, Anuj. Both are the same.

GAMMA IS A MEASURE OF RATE OF CHANGE OF DELTA. SINCE DELTA DOES NOT CHANGE FOR FUTURE, GAMMA IS NOT REQUIRED.

Thats right.

hello karthik sir , first of all thanks for such execellent yet simple and free classes , i have a querry that you mentioned \’ Never short ATM or ITM option with a hope that they will expire worthless upon expiry\’ . What does this mean by expire worthless upon expiry ,like what i m expecting to happen with delta and premium values if am shorting an ATM and ITM and what will actually going to happen with these upon expiry

Worthless options are those which have zero intrinsic value upon expiry. If you write an option, it\’s good to see the option go worthless upon expiry as you can retain the premium received. The chances of an ATM or ITM option being worthless upon expiry is low, hence you should try and avoid writing these options.

Thanks sir for all your efforts 😊

Good luck and happy learning 🙂

Does option contract have expiry on the last Thursday of every month or every Thursday??

Every Thursday is for weekly options, last Thursday is for Monthly contracts.

Sir what\’s the meaning of a contract expiring worthless?? As in when you said OTM is great candidate for shorting wherein we expect it to expire worthless… What\’s the meaning of worthless here ?

If an option contract does not have any intrinsic value upon expiry, then that option is said to be worthless.

Sir was there a set calculation when you\’d say that the trader would define his risk limits to 5 Nifty futures contracts ?? I mean why \”5\” …As a capital of Rs.300,000 he could obviously go for more contacts than just 5

Or is the number purely imaginary and only for the example ….

10 lots of ATM option, each with a delta of 0.5, so 10*0.5 = 5 lots futures equivalent.

since trader has short 10 lots of Nifty 8400 Call Option, Initial Delta of position should be -5, instead of +5

and after market moves 70 pts up against the trader, new delta should be -5+0.35= 4.65

pl clarify where am I wrong

Varun, its the delta of the option we are talking about. So an option transitioning from ATM to ITM will gain delta right?

Sir can volatility alone can increase the premium of an option if market movement direction is not supportive

Yes, volatility can play an important role in determining the price of an option premium.

Ok Karthik.Got confused by the graph of PE option.

Delta calculation is correct.But graph is wrong.

Red graph should be horizontally reversed(as Spot increases PE delta should go from ITM(-1) to OTM(0), but here it is going from OTM(0) to ITM(-1) .. Pls change graph if possible

Thanks a lot

Let me relook at this, thanks 🙂

Thanks for response Karthik.

No, Hence from -0.54 from -0.5

-0.54 is more negative than -0.5..pls see the red graph of Put option delta

Sreekanth, -0.5 to -1 indicates that the option is transitioning from ATM to ITM, and from ATM to OTM the delta moves from -0.5 to near 0. The graph and the math indicate the same. Look at the graph from the ATM point of view.

Hi Karthik,

Firstly thanks for your awsome learning articles. I am a big fan of your way of writing.

I have a query in below calculation of Delta for PE option:

Case 1 – Underlying moves up by 10 points

Delta = – 0.5

Gamma = 0.004

Change in underlying = 10 points

Change in Delta = Gamma * Change in underlying = 0.004 * 10 = 0.04

New Delta = We know the Put option loses delta when underlying increases, hence – 0.5 + 0.04 = – 0.46

Case 2 – Underlying goes down by 10 points

===> Here new Delta should be -0.54 beacuse PE Delta loses value(becomes more negative) as Underlying increases. Even from graph, we can infer, red line moves towards more negative value as underlying price increases.

Delta = – 0.5

Gamma = 0.004

Change in underlying = – 10 points

Change in Delta = Gamma * Change in underlying = 0.004 * – 10 = – 0.04

New Delta = We know the Put option gains delta when underlying goes down, hence – 0.5 + (-0.04) = – 0.54

===> Here new Delta should be -0.46 beacuse PE Delta gains value(becomes less negative) as Underlying decreases. Even from graph, we can infer, red line moves towards less negative value as underlying price decreases(moves to left on X-axis).

Here new Delta should be -0.54 because PE Delta loses value(becomes more negative) as Underlying increases —–> hence -0.46 from -0.5 right?

Sir I have read almost all Modules they are amazing. Thank you For that. Can you please Provide a module regarding Algo trading too??? That would be really helpful because zerodha is providing algo trading through STREAK but its still confusing.

Algo trading is simply packaging a bunch of rules which gets validated systematically. Check this – https://zerodha.com/z-connect/queries/general-queries/the-rise-of-algo-trading-platforms-everything-you-need-to-know

If you are long options then you are long gamma

If you are short options then you are short gamma

I am not able to understand this properly. Kindly elaborate sir

Thank you

Jitesh, have explained this in the module and comment section. Request you to check this again.

Hello sir,

Great work, you just put this confusing concept in such a way with an simple example that any one can understand this concept.(*with little brain work 😅).

Gamma value of future- 0.

Happy learning, Vishad!

Gamma will be somewhere near to zero but never be zero such value of gamma could be 0.000000001

Yeah, as long as there is time to expiry, greeks will have a value, however small they are.

Calculation mistake in 13.2 where delta should be -0.5+0.35=-.15

Hmm, I need to check again.

hi karthik

as price action, zones work on naked charts of stocks, indices, does price action works on candle stick charts of options, in the same way it works on charts of stocks and indices?

can i apply same patterns, doji, stars and other indicators, to know the movement of options?

regards

I\’m not a big fan of applying CS patterns on the option charts, because there are lot more factors at play wrt options.

Hi Karthik,

A critique on chapter 13.2. The point on \”gammas getting added up\” and making shorting options riskier than long options would have been easier to understand with an example. In my opinion your point is a VERY IMPORTANT one and I humbly submit that one can get the wrong picture here. This can be explained as below with data from your own example where delta = 0.5; gamma = 0.005 and underlying moves by 70 points:

Case 1: Underlying moves up by 70 points for a person shorting options (market moves against the person\’s position):

– New delta = old delta + (gamma x change in underlying)

– New delta = 0.5 + (0.005 x +70) = 0.85

Case 2: Underlying moving down by 70 points for a person buying options (market moves against the person\’s position)

– New delta = 0.5 + (0.005 x -70) = 0.15

So in both the above cases, market has moved against the person\’s positional view by the same 70 points. But the person holding short position will likely lose more because of higher delta. The person holding long position will also lose but lesser because of lower delta.

1) Is my understanding correct?

2) Leaving the mathematics aside, why do you think is the reason for this phenomenon?

Regards

Sathya

Sathya, this is correct and I also realised that I gave a rather simplified example here. Will try and add more details to strengthen this.

constant

Hi karthik,

These topics are amazing and very lucid.

can u suggest me where can i find value of delta and gamma of stock.

in some exmples you have taken 0.005. How do u know

Is there any website?

Thanks Pavan. I\’d suggest you look at Sensibull\’s website for this.

Then , you supposed to be correct in above example under the \’Risk in Gamma\’.

You took + 5 in the example

Your multiplication are 10 *0.5 = 5

Even you are short on call option and don\’t you think the whole scenario will change as you has put your thought according to +5 delta .

That\’s right -5 lots * -(underlying change) gives a positive output.

Hi,

Option = 8400 CE

Spot = 8405

Delta = 0.5

Gamma = 0.005

Position = Short

Number of lots = 10

Position Delta = 10 * 0.5 = 5

These values are updated by you .

But when we are short on call . The value of delta comes in negative .

Like you told in previous module that when we are short on call we use ( – ve ) sign .

So , delta position should be –

-10 *0.5 = -5

I put negative sign next to next because we are short on call as you said in previous module .

Thats right, Shubhika 🙂

Hi,

I Went through some of the comments and You mentioned some Values of Delta

– Delta of Call ATM = +0.5

– Delta of Put ATM = -0.5

But when You are Short

– Delta of Call ATM = -0.5

– Delta of Put ATM = +0.5

In the Above example Under gamma Risk

You took 10 lots and delta = 0.5

You were short on Call Option

So, don\’t You think delta of short Call = – 0.5

You can think about it from this perspective. Its a CE we are talking about, ATM becomes ITM if the spot moves up. So the example we have quoted is correct. Short CE is = -ve, change in underlying wrt to the position is also -ve. So both together is +ve.

Hi,

In the previous chapter we calculated the delta values . If you see last case in previous chapter you sold the 1 lot and you put (- ve) sign before 1 and above example under risk you were short on 10 lots.

so, why didn\’t you put – ve sign before 10 .

Sort call or PUt?

Hi Karthik,

Thanks for these wonderful lessons. I am finding them so interesting and able to understand as the flow is very simple and step by step. Although I am excited to enter Options\’ world but holding my resistance for now as I know that until I know full alphabets of Options it is asking for trouble. Every chapter I go through, makes me feel more confident on my understanding of Options. Continuing with next chapters on theta and Vega.

Thanks for the awesome job!

Happy learning, Neeraj! I hope you find the rest of the chapters interesting as well 🙂

Hello Karthik.

I must say, all these modules have helped me a great deal in understanding the basics of options trading.

Now, I have a confusion regarding the Gamma value for Calls and Puts. We know premiums tend to fall faster than they rise. Although this is a qualitative factor, shouldn\’t this mean the gamma of a Put and a Call option at the same strike would be different.

Umm…going by your analogy, if the acceleration of a car is at lesser speed than its braking, the velocity of a car going in reverse should be different than the velocity at which it advances, isn\’t it?

Keshav, prices tend to fall faster than they raise —> as you said, this is sentiment-driven and not really quantified.

Hi Karthik,

You\’ve mentioned – \”Avoid shorting options which have a large gamma\”

Why did you specify only shorting, isn\’t the risk same for shorting or buying an option for a particular gamma?

I mean – \”Avoid shorting/buying options which have a large gamma\” – Is this wrong?

SHort positions requires margins, and with the price drop, margins increase and therefore your capital deployed increases.

Hello Mr. Karthik,

On May 29, avinash singh also asked same thing, there is something wrong as compared to old chapter & this chapter explination, as in previous chapter negative sign considered in calculation. but in this case section 13.2 negative sign should consider. can please explain in more detail.

Vishwajeet.

Let me check this again, Vishwajeet.

Hello Mr. Karthik,

In estimating risk by gamma, The trader is short 10 lots of Nifty 8400 Call Option, but while calulation no where minus sign is considered, while review of adding up deltas(Previous chapter) we have seen in case no 5 that for sell(Short) we are considering (-1* 0.5)= -0.5 but here in this case +0.5 considered. what is the logic behind this? if am wrong please correct me.

-ve sign indicates the direction of the trade, Vishwajeet.

in 13.2 – since the nifty has moved 70 points against the 8400ce seller this means the spot now is 8475. this means option has become OTM from ATM. and for OTM delta should decrease from 0.5. but why are we adding 0.35 to 0.5? as mentioned before delta above 0.5 is ITM in case of call options..plz explain this..

We are not adding, I guess the new delta is less than 0.5, hence around 0.35.

Change in delta = gamma * change in underlying

So in futures

Change in delta is 1

Gamma is ?

Changes in underlying if 1

Put this in equ

1=gamma * 1

So gamma = 1/1

Ans for future in gamma is zero

Yes sir.

gamma of the future will be zero because the future delta is constant to 1 which doesn\’t change. gamma is the rate at which delta changes. if delta is not changing then why gamma? so gamma will be zero.

Thats right.

Hi Karthik,

When I use the Black and School Greek calculator from Zerodha, I get (in addition to others) delta and gamma values. For that day, can I add delta and gamma and then multiply the sum with unit change in spot price to get unit change in premium?

You cant add delta and gamma, Sathya.

Hello Sir ,

Very beautifully explained gamma especially the 3D graph was very helpful.

I have understood the gamma relation with moneyness and expiry.

Is there any other factor gamma related to ?

( i heard someone saying gamma shoots up with the increase in volatility )

Is this correct sir?

Thank U for always guiding us.

Gamma is more related to the change in the price. Yes, volatility too has an impact on Gamma, Abdul.

Sir I have a doubt

At sr 13.3 graph has drawn with spot price on X axis but while discussing the same strike price has been considered which is little bit difficult to understand. Correlating the two graph and the discussion is cumbersome. Can you please explain the same.

Thanks in advance.

Hmm, but these are used in different context, Anurag.

I believe gamma is 0 for future contracts.

Right.

Answer to your futures gamma question.

Zero, why because, gamma is change in delta value, but futures, delta is constant and so gamma is zero. Am I right Mr. Karthik?

Yup.

I think the gamma of a futures contract will be 0.

Yup.

In Section 13.2, example is considered for Short CE means delta must be negative means -5 for 10 lot, if spot price moves 70 point then it is moving is OTM zone for CE shorter & delta should decrease so new delta should be -5+3.5 = -1.5

Yes, the delta increases if the spot increases, but it has an opposite effect on short CE, hence the -ve sign.

I am confused about this part –

Since the strike under consideration is 80 CE, the option attains ATM status when the spot price equals 80

Strike values below 80 (65, 70, 75 etc) are ITM and values above 80 (85, 90, 95 etx) are OTM options.

For call options, isn\’t that price higher than strike should be called ITM and lower are OTM? What am I missing here.

Strike higher than spot will be ATM for CE (ITM for PUT), and OTM otherwise.

Sir

Please tell me or suggest which chapter read again.

The module on options, especially the ones dealing with the greeks.

For example consider this –

Nifty Spot = 8326

Strike = 8400

Option type = CE

Moneyness of Option = Slightly OTM

Premium = Rs.26/-

Delta = 0.3

Gamma = 0.0025

Change in Spot = 70 points

New Spot price = 8326 + 70 = 8396

Above example premium Rs 26 /- .

This 26 /-₹ how to calculate or where from came.

You have explained it yourself 🙂

Hey you Teach us how to calculate Premium after changing underlying points, delta or gamma. But can you tell us how this premium decided what calculate required for set premium.

Sorry, dint get that. Can you please share more context?

For delta calculation, we have taken an updated delta.

But, for gamma why always (0.0025), why now updated gamma?

thank u sir

The change in gamma is very small.

Hello sir,

This is paragraph from above .

\”Option = 8400 CE

Spot = 8405

Delta = 0.5

Gamma = 0.005

Position = Short

Delta = 0.5

Number of lots = 10

Position Delta = 10 * 0.5 = 5\”

Shouldnt the position delta be -5 as the position is selling as we took negative in case of selling in delta part 3.

Ty

We took the difference in the spot as -ve, right? That takes care of the delta movement.

Gamma of future contracts = 0

Gamma = Change in delta / Change in underlying asset

Hence, Since the delta of future contracts doesn\’t change, hence Change in delta = 0

Hence, Gamma of future contracts = 0

Thats right, Eesha.

HI.. Sir

Thank you for such a valuable information. i have one doubt

in this

Case 1 – Underlying moves up by 10 points

Delta = – 0.5

Gamma = 0.004

Change in underlying = 10 points

Change in Delta = Gamma * Change in underlying = 0.004 * 10 = 0.04

New Delta = We know the Put option loses data when underlying increases, hence – 0.5 + 0.04 = – 0.46

Case 2 – Underlying goes down by 10 points

For PE option when the underlying moves up by 10 from ATM it becomes ITM and ITM data should increase OR i misunderstood somthing

and when ATM becomes ITM

When underlying moves up, the PE loses money right?

Hi Karthik sir, gamma is slightly difficult to understand because it\’s contain lot of calculus. And also I\’m unable to integrate and interpret the delta and gamma together. In fact I\’m poor in mathematics from school days. My questions are…

1. Is it really important to understand the calculation? Is it not enough if I understand only the behaviour of the Greeks? (i.e. gamma value is high in ATM, and low in ITM and OTM,etc)

2. Should options trader need to calculate all the Greeks before enter into it?? Is it not enough only directional view (i.e. underlying is going to raise or fall)

3. You have explained what is naked options. Can you please interpret it more clearly?

Thank you.

I understand Sathish. Eventually, all you need is a working knowledge of Greeks, no need to understand the exact calculations and values 🙂

Dear Sir,

What exactly do you consider to be a large gamma?

So ideally one should short mainly OTM options that have low Gamma correct?

Thats right, Litesh. While putting a number is difficult, its good to be aware that ITM/ATM tends to have higher gamma.

Can you suggest some books to get hold of these concepts or the overall F&O market?

You have Varsity for this 🙂

Hi Sir,

I am new to options and I have a basic question.

If I short a call, but don\’t square off till the expiry date, and if the spot is below my strike, what will happen to my lot?

Will the system auto-square off with a value of 0.05?

Yes, the option will be settled by the broker at 0.

Hello sir,

I m new to options, Just to understand, people always say not to do naked options. Naked means position without hedge, right??

But, in case of naked options we can use stop loss, right??

I just want to understand difference between stop loss and hedge?

stop loss is used to exit the trade which doesn\’t work as per our view or setup. Then again we can take fresh entry.

What happens in case of hedge??

Hope I asked right question..

That\’s right, Pravin. Naked means its unhedged. Yes, you can use SL to naked positions.

When you hedge, you have no exposure to the market. You are completely insulated to the movements in the market.

When you place an SL, you are willing to take a loss, in the event the market moves in the opposite direction of your trade.

got it.

so can we say, when delta is 1(DEEP ITMs), gamma will be zero.

Gamma is a non zero value. But yes, near 0.

Thank you again. Understood the calculation.

Good luck!

Thank you so much for this well elaborative write up. Have derived a lot of clarity on the options. Just for the sake of clarification, the calculation of new premium over is done based on the spot price and delta while the table shown in the previous topic (delta) has calculated the new premium based on the old premium with the delta value.

Would appreciate your clarification.

That right Gresha. In this chapter, we consider the rate of change of delta as well. We discuss that since we introduced the concept only in this chapter 🙂

Dear Sir,

I think there is a mistake in the above chapter. I sorry in advance if I am wrong.

Case 1 – When underlying moves up by 10 points.

So new delta for PE should decrease with the increase in underlying.

So as per me, the new delta should be = -0.5-0.04=-.54

Hence Old delta -.05>New delta -.54

Case 2 – When underlying goes down by 10 points.

So new delts should increase for PE

So new delta should be = -.5+0.04=-0.46

Hence Old Delta-0.5<New delta -0.46.

Please clarify

Ankit, I guess we have discussed this in the thread, can you please check the query section once?

after digestion roughly this topic ,i gain some ideas from this module, thank you karthik. but if you give link for download of worksheet then it must be more pleasure to the zerodha customer.

We have the PDFs at the end of the module page, which you can download and use. Happy learning!

Alright Karthik. So somewhere closer to 1 near ATM and closer to zero for OTM and ITM if we are to make a guess.

Yeah, that is right. Remember, these are just quick reference numbers.

Hello Karthik

Once again, these modules are extremely helpful and also thank you for responding to our queries even now.

In case of a Delta\’s value, we can kind of predict what it will be based on the type of option we are holding (0 to 0.3 for Deep OTM, 0.6 to 1 for Slightly ITM) and so on without having to depend on the Black and Scholes model. Similarly, is there any way to roughly predict what the value of Gamma will be without using the Black and Scholes method? While we know the Gamma value will be positive and that it will be between 0 and 1, is there some way to make a slightly more precise guess like in the case of Deltas?

YOu can estimate the rough gamma based on the delta itself 🙂 It will be max for ATM, slightly lower for OTM and ITM.

Hi Karthik,

New option premium should be by considering Delta and Gamma only

.: Option premium at the time of executing order +/- [ Difference in underlying value * New Delta taking Gamma effect at the latest spot price of underlying where the new option premium would be calculated] and not the old Delta as stated above module.

Thank You

Thanks for pointing this, Satyajit. I need to validate this, will do.

What is maximum value of gamma? Is it 0.5? In real world is it possible such gamma value?

Yes and yes 🙂

Gamma of Futures is zero, as there is no change in it\’s delta.

In calculus, Derivative of a constant quantity is zero.

True.

Hi Karthik,

Few questions, please clear my understanding. I tried to progress through this chapter slowly as per your suggestion, if you feel I missed anything let me know.