4.1 – Defining the problem

If you think about it, success in personal finance boils down to three things –

- Your ability to see through the numbers

- Your risk-taking ability, and

- Common sense

I hope that the previous two chapters have laid down a foundation, which will help you look through the numbers.

The risk-taking ability is merely a function of your knowledge and the way you continuously expand it. The more you read and understand, the more you get familiar with risk and the better equipped you are to handle risk. The extent of risk you assume can make or break your financial fortunes. Of course, we will discuss more as we proceed through this module.

Common sense is something applicable to all aspect of life and not just finance; we will leave it at that 🙂

So, given these three key points, we will now steer our way into learning the vast set of things that make up personal finance, and hopefully, this will help us develop our instincts on all the three counts required for success in personal finance.

Finding a starting point to start this journey is a challenge given that the vastness of this topic. Hence, in my opinion, the best way to proceed is by identifying a real-life financial problem and then finding a solution for it.

The process of finding the solution will open up many different learning windows, which will help us understand the core concepts of personal finance.

So let’s get started.

I’m assuming most of you would be in different stages of your working life, some would be starting (or about to begin your careers), some may be few years into work life, and others probably halfway through your work life.

Regardless of where you are, one of the common goals in life is to ensure that you retire into a happy and content life. The fact that you have retired should not stop you from leading a particular desired lifestyle. You should continue to lead a lifestyle that you think you deserve.

If the above is true, then it implies that you need the same amount of disposable income, as you would have when while you were working. Lesser disposable income wants a compromised post-retirement lifestyle, which none of us wants.

Let us put this in context and assign numbers to it, and elaborate this a bit further.

Assume you will work for the next 25 years (these are your income-generating years), post which you will retire. After you retire, you expect to live for say 20 more years. Assume, the cash required today to lead your lifestyle is Rs.50,000/- per month. This is cash post taxes, fixed expenses, utility bills, etc. This is your disposable income per month.

The idea is that after 25 years, for the next 20 years of your post-retirement life, you’ll need the same Rs.50,000/- every month, this is about Rs.600,000/- per year.

Some of you may disagree or may have a different opinion on how much you need post-retirement; I understand that but stick with for now, please.

Let me put this tabular format for you to understand this better –

| Current year | 2019 |

| Number of working years | 25 |

| Year of retirement | 2044 |

| Number of years post-retirement | 20 |

| Final year | 2063 (including 2044) |

| Monthly cash requirement | Rs.50,000/- |

| Yearly cash requirement | Rs.600,000/- |

I’m sure all of you reading would agree that this is a real-life problem and we all need to address this.

If you think about this, there are two parts to this real-life problem –

- How much retirement corpus one needs to have accumulated by the time of retirement, i.e. the beginning of the year 2044?

- How does one accumulate the required money?

Some of you may be tempted to answer the first part straight away –

It is Rs.600,000/- per year (50,000 per month for 12 months) and for 20 year it is Rs.12,000,000/- (600,000 * 20) or 1.2Cr. So if we were to accumulate a retirement corpus of 1.2Cr by the year 2044, we could easily sail through the next 20 years of post-retirement life by burning Rs.50,000/- per month, all the way to 2063.

Well, if only life was that simple 🙂

Given the above, the question is, how much cash reserves you’d need at the end of 25 years, i.e. in the year 2044, such that you can have Rs.50,000/- every month till the year 2064.

In this chapter, we will address the required corpus bit and figure out the amount needed at the start of the retirement year. In the next section, we will figure out how this corpus gets generated.

4.2 – Inflation and other realities of life

In the absence of inflation, the math above would work like a charm, i.e. in the year 2044, a sum of Rs.12,000,000/- would help us sail through our retirement years at ease, i.e. at the rate of Rs.50,000/- per month up to 2064.

However, inflation is real, and this makes life complicated in multiple ways. Inflation is the phenomenon, which makes things expensive. For example, a plate of pav bhaji at a restaurant may cost Rs.50/- today, but the same may cost Rs.55/- at the very same restaurant the next year. This marginal increase in cost is attributed to inflation. In other words, the purchasing power of money has reduced over one year.

This is true, all else equal, money today will always be less valuable at a future date. For this same reason, all the stories of our parents and grandparents enjoying a full meal for less than Rs.2/- exists 🙂

This implies, today’s Rs.50,000/- will not be Rs.50,000/- tomorrow. It will naturally reduce owing to inflation. For this exact reason, we cannot only multiply the amount required with the number of years and arrive at a figure.

4.3 – The Future value

To find a solution, we need to find out the Rs.50,000/- equivalent 25 years from now. This is what we learned in the previous chapter.

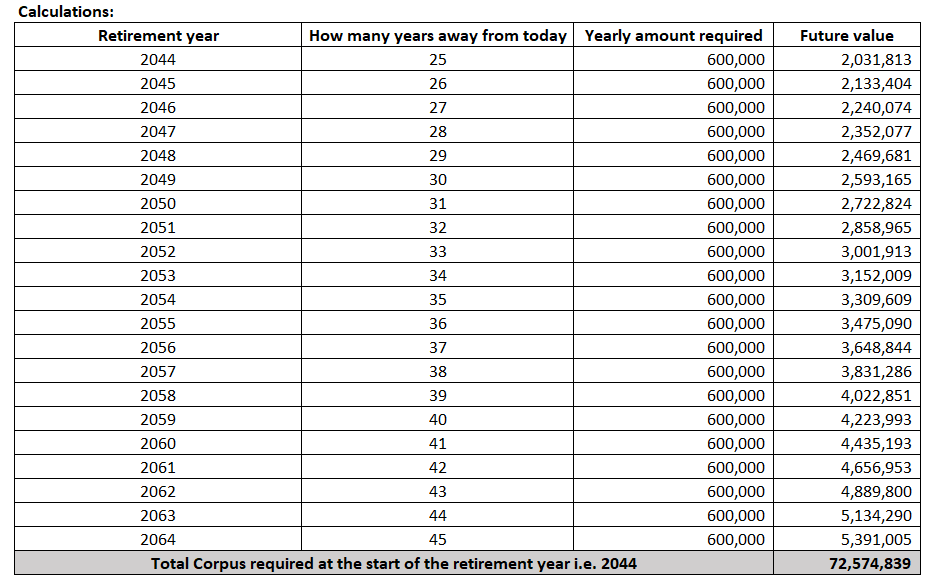

The expected cash requirement is as shown below –

| Year of retirement | Year | How many years away | Corpus required as per today’s value |

| 01 | 2044 | 25 | Rs.600,000/- |

| 02 | 2045 | 26 | Rs.600,000/- |

| 03 | 2046 | 27 | Rs.600,000/- |

| 04 | 2047 | 28 | Rs.600,000/- |

| 05 | 2048 | 29 | Rs.600,000/- |

| 06 | 2049 | 30 | Rs.600,000/- |

| 07 | 2050 | 31 | Rs.600,000/- |

| 08 | 2051 | 32 | Rs.600,000/- |

| 09 | 2052 | 33 | Rs.600,000/- |

| 10 | 2053 | 34 | Rs.600,000/- |

| 11 | 2054 | 36 | Rs.600,000/- |

| 12 | 2055 | 37 | Rs.600,000/- |

| 13 | 2056 | 38 | Rs.600,000/- |

| 14 | 2057 | 39 | Rs.600,000/- |

| 15 | 2058 | 40 | Rs.600,000/- |

| 16 | 2059 | 41 | Rs.600,000/- |

| 17 | 2060 | 42 | Rs.600,000/- |

| 18 | 2061 | 43 | Rs.600,000/- |

| 19 | 2062 | 44 | Rs.600,000/- |

| 20 | 2063 | 45 | Rs.600,000/- |

The table is quite easy to understand. Look at the first row, it says, the 1st retirement year is 2044, and it is 25 years from the current year i.e.2019. The corpus required for 2044 is Rs.600,000/-. This is a constant amount needed for all the retirement years.

The 2nd retirement year is 2045, which is 26 years away from the current year (2019). So on and so forth.

Now the task at hand is to estimate the value of Rs.600,000/- 25 years later, 26 years later, 27 years later, and for each year up to the final year, given a certain level of inflation. Remember, these are all the future value of money.

4.4 – Estimating the future value of the corpus

To proceed further from this point and estimate the corpus required at the start of the retirement year, i.e. 2044, we need to have a view on the long-term inflation.

I would be comfortable pegging the long-term average inflation value between 4-5%. Now, the question to answer is – given 5% inflation, what would be the value of Rs.600,000/- 25 years from now.

Similarly, given 5% inflation, what would be the value of Rs.600,000/-, 26 years from now, so on and so forth, all the way to the 20 years of retirement.

If you recollect from the previous chapter, we are talking about the future value calculation here. Once we have all the future values, we need to sum them up to get the total corpus required at the start of the retirement year.

Let us do this for the initial 2-3 years and then take the help of MS Excel to figure the rest.

From the previous chapter, the future value formula is –

Future value = P*(1+R)^(n)

Where,

- P= Principal i.e. Rs.600,000/-

- R = opportunity cost, in this context it is the inflation rate, so 5%

- n = Period, 25 in this case

Plugging in these value –

600,000*(1+5%)^(25)

= Rs.2,031,813/-

So, in 25 years, if you have Rs.2,031,813/-, then it is as good as having Rs.600,000/- today.

For the 2nd year –

600,000*(1+5%)^(26)

= Rs.2,133,404/-

So, in 26 years, if you have Rs.2,133,404/-, then it is as good as having Rs.600,000/- today.

So on and so forth.

Here is an excel snapshot that shows how the numbers stack up for all the other years, but before you look at it, can you guess how much this amount can be?

For most people I’ve asked this question, they get the value way off the mark, this is because they cannot comprehend the fact there is inflation and compounding (future value) at play here.

So go ahead and give it a shot, take a guess on how much the retirement corpus should be, once you’ve answered this, then take a look at the actual number; hopefully, it should match, if not, don’t worry, we all have some learning to do.

As you can see, the corpus required at the start of the retirement year is a staggering 7.2Crs!

The numbers drastically change if we change the inflation assumption and of course the actual amount of our lifestyle demands.

4.5 – Oversimplification

Some of the things are oversimplified and exaggerated here. For instance, having a constant monthly requirement of 50k may not be accurate. As we age, we would prefer to sit at home and sip a drink as opposed to hanging out in the coolest and trendiest bar in town. Or we may cut down on all the outside eating, watching movies, etc. We may not want to buy the latest denim from Levis or the newest pair of sneakers from Nike. Who knows?

Our requirements could be very different, and from whatever I’ve read, observed, and understood, the money required for older people is lesser than the younger ones. So we may not need 50K per month when we retire.

But here is the thing with personal finance, it is best to take a conservative approach and figure out the outcome. If we manage to lead a comfortable but yet frugal life at a later point, it’s great, else we would have anyway budgeted for it.

In the next chapter, we will understand ways to generate this income.

Download the excel sheet used in this chapter here.

Key takeaways from this chapter

- Retirement is a real-life financial problem that we all need to address

- Inflation complicates things. Money today is not the same as tomorrow

- Inflation diminishes the purchasing power of money

- Use the future value of money to estimate the worth of money today, ‘n’, many years later.

I tried calculating using simple arithmetic progressions and got 7.72 Cr, too bad considering it was an approximation. Might as well live an year longer to spend the extra

I hope many more years with good income and corpus 🙂

pranam karthik sir,

total corpus required at the start of the retirement year is a staggering 7.2 crores. the calculation is fine. but the corpus amount 7.2 crores in 2044 can be invested in a risk free instrument for next 20 years with systematic withdrawal plan. if considered this, the corpus required in 2044 can be reduced.

This is correct, this calculation is actually is incorrect.

The calculation is not incorrect. Considering the next 20 years we have in hands to invest the retirement corpus, the original corpus required can be reduced.

Madhav, why dont you attend this session 🙂

https://varsitylive.zerodha.com/programmes/a7a4a539-7c51-4895-8e9c-edfd3e5fd1a7

Pranam Sir,

sir sir I am already retired bank official long 6 years back.

thanks a lot.

Sure. Good luck, and happy learning and investing, Madhav.

Yes. By the please do check this and encourage you to attend if this is of interest – https://varsitylive.zerodha.com/programmes/a7a4a539-7c51-4895-8e9c-edfd3e5fd1a7

Hello Karthik,

It’s very encouraging to learn about investing from you. However, my problem is a bit personal. Investing wasn’t even in my dictionary until I accidentally bumped into it recently. In all your examples, the person who starts investing is usually 20-25 years old.

But I’m 35. Since I’m reading all this in 2025, is it too late for me to start now? Please guide me — is investing still for me? I’m really enthusiastic to learn.

As cliched as it may sound, it is never too late. The only way to offset the time lost till now is to save slightly higher amounts. But please get started as soon as possible 🙂

Please use Indian number format. Commas. This is harder to understand.

Ok. Noted.

Thanks Karthik,

I shall do that.

Good luck!

Excellent article. I am already retired and so late to consider these points you mentioned. I should have read this long time back. I need your advice on good mutual fund schemes for people like me. Thanks Karthik

Its never too late Vinod. I\’d suggest you speak to a good finacial advisor to figure what best approach you can take, do ensure you pay adequate attention to risk 🙂

karthikjii the retirement table above there is missing 35:).

Let me check this 🙂

Hii Karthik,

I have one question: whatever money we save will definitely earn some interest afterwards for the remaining 20 years, so considering this, how much Money Need for the future?

So if we go with considering this way, then your 7.2 cr requirements may change.

Yes, but I\’ve not factored that in to add some conservative approch to planning. But you can factor in the interest as well 🙂

Hi,

Thanks for simplified explanation.

I think 7.22 cr is less as it is also going to depriciate (due to inflation) after 2044 subsequently.

What do you think?

End of the day this is a model, you can plug in numbers that works best for you.

Hi Karthik,

Thanks for this wonderful article . I can see some issues with the calculation, Kindly have a look .

we are calculating the future value of Rs 6 lac at the years 25, 26 ,27 and so on till 45 years . Since this future value is at different time frames(25 yrs , 26 yrs , ….. to 45 years) the addition is not right in my understanding.

Now if you are talking about future value at 2044 which is 25 later from our start date ,which is also our retirement date , we need to discount values from what we have calculated for 26 , 27 28,….45 years to 25th year.

Which if we add all the values we get around 4 crores at the 25th year or our retirement year.

Thats right, hence the time is a variable here right? And this gets factored in the formula as well.

Please add a next page option at the bottom of every chapter.

Noted, we will do that. Thanks.

Hi Kartik,

I was just skimming through the content and I noticed something which I thought I should bring to your notice…

I guess, you may have to review the calculation for \”Corpus required at retirement\”… The corpus requirement cannot be that high given the assumptions made….

According to me, the corpus required at retirement should be the present value of the future outflows(expenses post retirement) – 20 years ahead – discounted at the rate of inflation or a rate marginally higher than inflation, assuming that my corpus will be invested in the most conservative instrument post retirement… Even If I discount it at the rate of inflation assuming ZERO real returns post retirement, I still get a corpus figure that\’s just a little above 4 crore, and not 7.2Cr. So naturally the amount required to be saved per month to reach the corpus would be significantly lower and thus manageable.

In the illustration given, you have added up the inflation adjusted expenses to arrive at a figure. However this figure is the future value…All you need to do is just discount it back 20 years using an appropriate discount rate, which will give you the corpus required at retirement.

In case my point isn\’t clear enough, you may contact me by e-mail, I\’ll be glad to share more details.

I hope my assessment is correct… However do let me know If you think I\’m wrong…

Regards

Deepak Rameshan

Sure, let me review this. But the overall idea is to stay on the conservative side when dealing with personal finance 🙂

Karthik, is the certificate granted for completing Varsity on web through laptop as well? or is it limited to the phone app only?

Yes, you can check this – https://zerodha.com/varsity/certified/

I think here is a point that we have missed out. The entire 7.2 cr amount is assumed thinking that the entire corpus would get used and would get exhausted in 20 years. But in real life the 7.2 cr corpus will also remain invested for the entire period at least in risk free instruments or others as the case may be. So while 7.2 cr is calculated thinking that i gets used over lifetime but the corpus will also fetch interest which gets accumulated.

At 2044 year 7.2cr will fetch @ 6% ~ Rs 44lacs. whereas the requirement at year 2044 is only 21 lacs. so the entire corpus of money will actually increase over time.

The real value for retirement would be much less than 7.2crs

I agree, but as a thumb rule while planning for retirement, its always good to assume things on the conservative side. Here the assumption is that interest rates will be near zero like in the developed nations like US and Japan. If it is not, good for you and me. But if it turns out true, then we are safe. So the question is how do you want to plan for it?

If one starts with a corpus of 7.2 Cr, your sheet misses out on the money it will earns every year!

Sorry, dint get that. Can you elaborate on the query?

I guess, he meant if someone will start with 7.2 Cr corpus then it doesn\’t mean that money remaining after pulling 50K every time the remaining money is lying down there. It\’ll remain invested somewhere and will earn interest over time.

Sorry, missed the context. But yes, what you are saying makes sense 🙂

Prev and next lesson button in end of the lesson, will be helpful a lot in means of reader\’s perspective.

Anyways kudos to the team for making good financial content, Happy to explore more content from zerodha.

Thanks for the feedback, Manik. Glad you liked the content on Varsity 🙂

Hey guys, no pdf availability for this lesson?

https://docs.google.com/spreadsheets/d/1I_-OUTuShScybKd16L7SGr-AOI1sDpp2OShg6EGY2-o/edit#gid=597060860

Scenario: I have put two MFs. 1 index fund, 1 PPFAS. I am planning to invest 10000 in the beginning stages and increase the SIP percentage by 10% every year as mentioned in the example.

After few years (especially after 181 months) we can see that the investment per month is around 41k per month and increases very much quickly in the coming year. Hence, as a retail investor, this would be a huge amount to invest on a monthly basis.

I am planning to increase my wealth apart from SIPs too. Any advice on this would be really grateful.

Also, It would be really great if you could make a module on Swing Trading (if possible). The reason for this suggestion is because a common man just depends on his salary (which won\’t make us wealthy in the long term) and is looking to increase their source of income through additional means. Hence they can deploy certain swing trading on the equity market (only in cash no margin). I believe it would be a really helpful module to people who are looking to build a secondary source of income.

I totally understand you would be juggling with multiple works at hand. I loved reading all your modules. I am starting to read the Financial Modelling module which you have put across recently.

Thank you very much in advance.

I understand your point of view. I think you\’d be better off by increasing your SIPs over time rather than attempting to create wealth from trading. Trading is a really tough business to be in. SIPs over the long term is a much better bet. Once you increase your SIPs to a reasonable extent, then start looking at trading and other avenues.

I couldn\’t find the excel sheet so I manually created the SIP calculation by referring to the pic. However, my one doubt is.. Suppose when we come near 24th year of our working year. During that time the SIP monthly amount increases exponentially if we increase by 10% every year (98k per month). But realistically, I don\’t think a normal person can invest 98k per month. I am not sure if my calcualtion is correct. Is there a way where I can share the excel sheet?

Maybe you can upload it on Google sheets and share the link?

What does J stand for in the above content sir?

Supposed to be a smiley, sometimes it does not render properly 🙂

Hello Sir,

I hope you are doing well.

Is there a way you can show us your edit history or let us know the changes you make to each chapter so one can go over them while re reading the chapter?

Maybe make the edits in Red?

So atleast one knows what you have changed.

Ah, that is tricky. Not sure if wordpress supports that. Need to check.

Why can\’t we just have 4 kids who will take care of us instead of solving the retirement problem mathematically? 😉 (joking)

You\’ll have other problems then 🙂

what is the difference in taking FV either by just taking interest rates or inflation rate..?

i mean unable to understand that shud i take inflation as \’R\’ or that govt. bonds return number 7.5% or similar as \’R\’..?

u took out FV from both perspective..which one is right used and for which reason..?

Consider the inflation in most cases.

Hi Kartik.. I am reading this chapter \”The retirement Probem\”. I am not able to find the excel sheet to download that you are referring to. Please help.

Let me check this again.

Great Articles…. In the excel file there is a problem in formula.. The retirement year column not populating according to Year of retirement cell. Please change that.

Once again thank you so much for this great article.

Thanks, Vamsi. Let me check this out.

When will the PDF document be available for last 2 modules ?

It becomes very handy & can read whenever one has time & without internet.

Once the module is complete. 2-3 more chapters left.

how did we decide that we should be taking inflation rate as 4-5% ?

Long term average.

HI ,

Why we need to take it from principle, ok i accept the fact of inflation.

On your say , we are dividing the entire money for 20 years after retirement. If a person stay alive after 20 years and the amount accumulated is only 7 crs . It will get expired ryt.

So why cant one put in a FD and survive on the interest of FD.

What if the interest you earn is lesser than inflation?

Not able to find the downloadable excel.

Its just above the Key takeaway section.

Thanks for your reply. Eagerly waiting for the other chapters in this module. Keep up the amazing work.

Hopefully soon 🙂

Karthik,

Thanks for covering the retirement problem. Is 5% inflation pessimistic or optimistic? I\’ve heard that a reasonable(pessimistic) side will be 8% inflation though my friends mentioned 10% is reasonable given that even government milk price has increased at the rate of 8% for the past 20 yrs in India. Of-course most USA based blogs mention it around 2-3% but that in India is not possible I guess.

Another question on corpus required. Given that tax on gains is high in India(both equity and debt are taxed) and given that income tax slab change is much slower than inflation the interest generated on the corpus(of 7 Cr) on yr 2044 may well attract 30% tax. So the amount left for our living might well be less.

I think 5-6% is a reasonable long term expectation of inflation. By long term, I mean = 20+ years. About the corpus, true, hence we need to consider inflation-adjusted and tax-adjusted returns. I intend to revisit this chapter again, waiting to cover a few more topics in this module.

Hi Karthik,

First of all, thanks to you and the varsity team for this initiative and much needed module for every one who wants to manage their personal finance themselves. After going through the PV and FV concept now I am better equipped to decide if an investment proposal makes sense in the first place.

I have a little problem in understanding the below:

We calculated the FV of 600,000 for each year from the present year at the inflation rate. But how can we add all these values and say that we need so much at the start of retirement(2044 in the example) ?

Is the assumption here that from 2044 onwards, our money only loses value every year ? We do not invest that amount anywhere else post 2044 ? We just keep on spending out of the corpus accumulated by 2044 ?

Please help me understand this.

Thanks again for the wonderful chapter and module.

That\’s because we are moving forward the value of money in today\’s terms to a point in the futures by keeping the inflation in perspective. Yes, we can invest the money in 2044, I will discuss that part again later in this module 🙂

Excel download link not enabled

Need to check.

Suppose instead of 7 crore, we have 5 crore at retirement. We will not keep the cash at home. We invest it at 8% per annum. That generates 40 lacs per annum. Even after taxes, we will be left with much more than 22-23 lacs required. We can further reinvest the remaining amount and keep enjoying. This way may be even 4 crore will suffice.

Yup, as I have mentioned in earlier comments, we will revisit this at a later point.

Hi Kartik,

Can you tell how to calculate step up SIP (growing annuity) in Excel. I require it for my son\’s retirement corpus calculation.

Regards.

I will do that shortly in the upcoming chapter, Kumar.

Hi sir,

Thank you for this fantastic article. Pls can you clarify the doubt that I have?

As I have understood from the example, we have found the FV of our expense today, for the different years from 2044-2064. But the column \’Future Value\’ only refers to the amount that will be needed for that particular year mentioned in the First Column.

If that is the case how can we sum these amounts at different timelines (FVs) to come up with the Corpus reqd at the start of 2044?

Please help me understand where my understanding is wrong.

Vicky, these are summed and discounted back to the present year right? So we are not mixing up the cashflows across timelines.

Hi kathik sir ,

In the above scenario ; Can we solve using PV ?? Because I\’m little confused by going through the example ; since the ask is we need 6L every year from 2044-2064 to manage ; so we are calculating FV of 6L from now (i-e) If we have 6L now ; this amount will be equal to 2 Cr in the yr 2044 – which in turn will be equal is it what it implies? ?

We are moving along the timeline here, Aditya. We are calculating the present value of the future cash flow required. So yes, we are essentially calculating the future value of 6L 25 years later given a certain rate of inflation.

Sir kindly add a chapter regarding health insurances ,how to choose best insurance for our family, what parameters to consider ?

Yes sir, will certainly add that.

Let me know if I am wrong in my calculations, I will retire on 2044 with corpus 3.2 Cr and put it in fixed deposits and spend interest . My principal will remain same…

why we calculating in a way where I am taking 50,000/month from principal.

Vivek, you also need to account for inflation and the interest rate in 2044 🙂

Sir I consider myself a very disciplined learner and all thanks to you I\’ve been able to learn a lot about investing. However, there\’s a lot of things regarding economics and other things that you haven\’t covered here, I\’m having a hard time understanding. How would you suggest I go about learning this? I read business newspapers and I see a lot of stuff that I have no idea about. Thank you.

I\’m glad you liked reading up on Varsity 🙂

Macroeconomics is a huge topic, I\’m not sure if I\’m the right person to discuss the same. However, I\’ll try and put some material on this topic.

Query

Query on compounding, I had bought 100 shares of X company based on fundamental and after 4 months l I see profit is around 30% hence I sold 50 shares and booked the profit.

After few weeks, share price came down so I bought again.

In above example how compounding effect is taken into consideration for new bought 50 shares and 50 existing shares of same company?

Regards,

Yuvraj

Yuvraj, there is compounding here 🙂

Compounding occurs when you hold positions for multi-years. In your case, it is a simple \’absolute return\’.

Hi Karthik,

Another excellent chapter. Although i think this is a vast topic and probably nothing can be a complete guide for this. But I would suggest to add details on below things also

1. On things like Insurance (Life, Medical) also, as i have seen and heard personally lot of stories where people\’s savings have been wiped out by such things.

2. Utilizing Tax Saving instruments properly (80C, NPS, PF etc) as that automtically accumulates a lot of money for you while providing you tax benefits also.

3. Your thoughts on buying property, car etc. How to plan these things.

Some other things which may be useful.

Sunny, yes all these things and more will be added to this module 🙂

I do have another question too. Although you have done an excellent job of demystifying FA on stocks, I do feel each sector needs to be analysed with separate set of tools.

1.Can you let me know a book which deals with sectoral analysis?

2. How do we develop a framework for each sector? Please point me toward a resource or something. Thank you.

Karthik I read an article saying the promoters of JSW Steel has released the pledged shares worth 1150 crs. From my understanding, shares are pledged by owners to lenders, so only the lenders have the power to release it after the payment is made, right? Please help me understand this article. I\’m posting the link below. Thank you.

https://www.business-standard.com/article/companies/jsw-steel-promoter-companies-release-pledged-shares-worth-rs-1-150-crore-119091901010_1.html

Thats right. When the promoters bring back to the principal and accrued interest, the pledge is released and the shares are given back to the promoters.

Sir

This article is good for the young generation to let them know how much is required as retirement corpus. Could you please (if possible) write about what should a retiree do on the assumption that he toiled and saved and created the corpus of 7.22 cr. Then what? How do a retiree manage his corpus. The evil inflation, medical expenses etc are all real. What should a retiree do.

I did an extensive search (cannot call it research – as it is for the PHDs) for how to manage a corpus on retirement and beat inflation.

All the good writers have written upto the corpus creation and not what happens next.

Regards

Ninan

That\’s an excellent point. I\’ll try and include this in this module.

Sir,

Please post the second part quickly very scared after looking at the Retirement Amount

I will, Siddharth 🙂

Hi

A good article that brings out the effect of inflation and the need to save more.

Can you also advise on the ways of saving with better returns especially for those who do not have pension

Also some comparison of options (like ETF, MF, ULIP, Insurance…etc) would help

Thanks

Glad you liked it 🙂

We will include all those topics and more!

Sir,

i have a problem in excuting bo (bracket order) in nifty oct fut, it rejecting last 3 day last friday i complaint about this to zerodh team but no use , with the any desk platform they try to help me they failed..but same bo for nifty sep fut they working well, in my dad accout also nifty oct fut bo not working, rejection reson is showing that insufficient balance, but i have 2 lac , please help me…. Thank you

Suggest you reach out to the support team for this, Avinash.

I think you should be front loading all the FV calculations going into the retirement to the year 2044, which means a PV calculation of all these FV calculations to come to the exact value req. as of 2044( As the money saved till this point will keep on earning interest for next 20 years of retired life).

A couple of things, Prateek – (1) Even if you front load, how do you work yourself up to ensure you save enough? That this point that I\’m trying to make, and hopefully will in the next chapter (2) The trick with personal finance is to ensure we take a conservative approach and be prepared for a worst-case scenario. This will give us enough margin of safety.