26.1 – Assumptions

We have reached a stage where we have discussed almost everything related to Mutual funds, leaving us with the last crucial bit, i.e. the mutual fund portfolio construction. I’ve spent last several days to think through the best possible way to explain this, and finally concluded that this is a herculean task 😊

I’ll explain why in a bit, but don’t worry, I will attempt to explain it 😊

Before we proceed, I need to address a few assumptions I’ve made.

When we talk about constructing a mutual fund portfolio or for that matter an equity portfolio to solve for a financial goal, we make two assumption –

-

- We are covered for the risk

- We are covered for emergency

Before a person can have a portfolio of any sort, these two things should be in place.

Let me explain what I mean.

Cover for the risk – An individual faces many different kinds of risk in his/her lifetime. Risk across multiples areas of life – physical health, mental health, permanent disabilities, a prolonged state of joblessness, broken relationships, and whatnot.

While it is impossible to anticipate everything and get a cover, an individual should get a cover for two things in life – loss of life and hospitalization.

Of course, the cover comes in the form of insurance. Term insurance will ensure that your near and dear ones, your dependents are not financially burdened after your passing away.

Health insurance will ensure you don’t spend your life’s earnings to pay for hospital bills while getting treated for chronic illness.

Given this, you need to estimate the extent your family will be paid off if unfortunately, you pass away. Similarly, you need to figure out the extent of health insurance cover you need to get. Topics related to insurance are vast and have many technicalities. I won’t get into this at this point. But I want you to be aware that as an individual, the very first step in your ‘personal finance’ journey is to ensure you get cover for these two types of risks.

I want to stress that don’t buy insurance products linked to investment plans. These are not worth it.

Cover for an emergency – I’m referring to an emergency corpus here, an emergency corpus to help you navigate your tough times. Tough time could be a job loss, or it could be as simple as having enough money to replace a piece of electronic equipment at home or a medical emergency.

I understand medical emergencies are covered by health insurance but don’t take that for granted. To give you an example, in September 2020, both my parents were hit by Covid 19. When I took them to the hospital, the hospital made me pay a certain amount of money for admission and cover the initial expenses. Of course, I had an insurance cover for both of them, which later came in handy, but at that moment, I needed ready cash and needed a fairly large amount.

Or take this, for example – thanks to Covid 19, schools went online, and I suddenly had to equip the house with a printer and a laptop for my 10-year-old daughter. That was an unplanned financial expense but had to be done.

Emergencies can come in any form and can come at any time. One has to have sufficient funds, which is easily available to you when the emergency strikes. Given this, at the very initial stages of your ‘personal finance’ journey, I’d advise you to build this emergency corpus.

The question is, how much money is good enough for the emergency corpus? Different people have different opinions, but I see most of them agree to have an emergency corpus equivalent to 6 months of expense. For example, if your monthly expense is 40K, then the emergency corpus should be at least 2.4L.

But I don’t subscribe to the 6-month emergency corpus template.

Each person is different; each family is different. It would help if you sat with your family, go through different scenarios and identify a corpus amount good enough to sail your family through these tough times.

Anyway, I will make these two assumptions – that you have the basic insurance cover and have built an emergency corpus. With these things taken care of, we will now understand how to build a mutual fund portfolio.

26.2 – Financial Goal

Imagine a newly married couple. Both the husband and wife are young, say in the late ’20s, and both are working professionals. The couple aspires to buy a house of their own. Their idea of the home is a 2BHK apartment downtown, costing roughly 1.5Cr, and they give themselves a ten-year window to achieve this goal.

Or think of this situation – A 40-year-old working woman wants to accumulate money to upgrade her car over the next five years. The estimated cost of the car is 55L.

Or imagine this situation (last one, I promise) – A 21-year-old has just started working for an MNC. Wants to accumulate 20L in 8 years to fund his/her post-graduate degree in the UK.

These are all examples of a ‘financial goal’. A financial goal has three specific attributes –

-

- The quantum of funds required

- The estimated time over which these funds need to be accumulated

- The current age of the person

Without these three attributes, a financial goal is incomplete.

For instance, a young working professional intends to accumulate ‘enough money’ to go to the UK for post-graduate studies in a couple of years down the line, is not a reasonable financial goal.

With the three random scenarios that I have quoted, you can imagine how diverse each person’s financial aspirations are. No two families or humans will have the same requirement (apart from retirement maybe). Financial goals are extremely diverse and very personal to your situation.

However diverse the situation is, the good thing is that you eventually have to look at mutual funds to help you solve for the situation, well, at least in most cases.

Of course, there are other financial instruments, but nothing as versatile as mutual funds (or ETFs).

Given this, there are two ways in which I can help you understand how to build a mutual fund portfolio to solve for your financial goals –

-

- Consider all sorts of life scenarios, build case studies around it, and stitch together a mutual fund portfolio to solve the given scenarios. You can then look at these scenarios, identify the one closest to your situation, and build a similar portfolio for yourself.

or

-

- Help you understand the different attributes of funds from a portfolio perspective so that you can identify what sort of funds to pick given the situation.

The difference between the two approaches is like this – assume you like savoury dishes, so I give you 20 different dishes to try. You taste each one of these and dishes and finally figure which one to eat fully.

Alternatively, I familiarize you with ten basic savoury ingredients. Once familiar, you can use these ingredients in the right measure to quickly prepare a savoury dish to satisfy your taste buds.

I will take the second approach to build a mutual fund portfolio, and I hope this works out better.

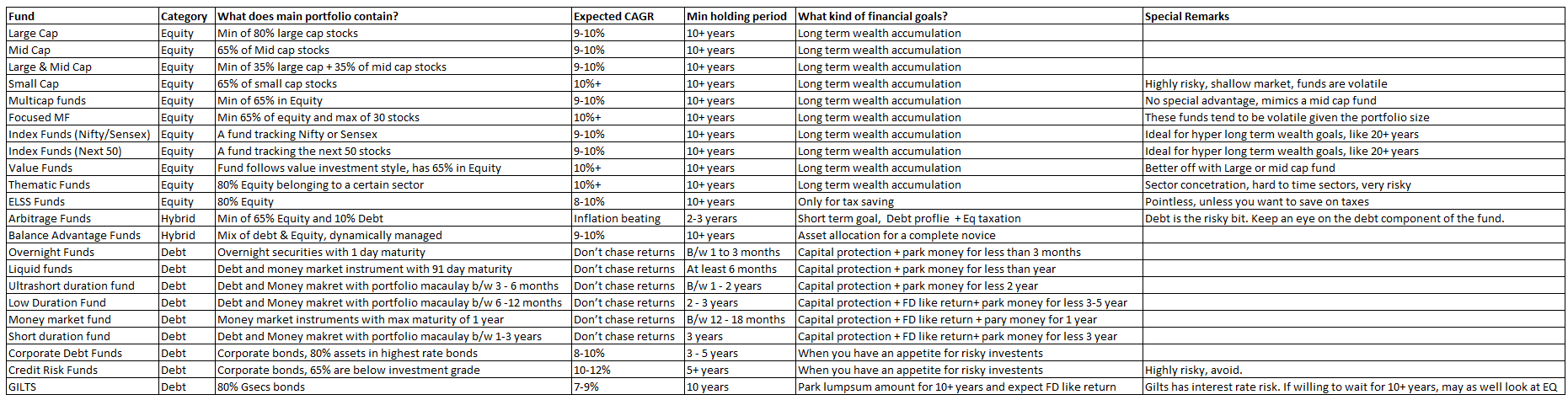

26.3 – Mutual Fund cheat sheet

I’ve prepared this Mutual fund cheat sheet for you. The sheet summarizes all the key attributes of the different mutual funds we have discussed. Please click on the image to enlarge and get a better view.

The table is simple, has few basic information –

-

- Fund type

- Category

- The main constituents of the fund

- Expected CAGR – as much as I hate it, I’ve included this 😊

- The minimum holding period – the minimum holding period for the fund if you were to invest in it. Not that you cannot invest in the fund and hold it for lesser than the minimum holding period, it is just that if you do so, recovering from a drawdown could be difficult.

- Financial Goal – The kind of financial goal the fund can be used for, more on this later.

- ‘Special remark’ – Things you need to be aware.

I’d suggest you keep this table handy. This table will help you craft a mutual fund portfolio for most of the financial goals.

Before we proceed further, we need to understand an important aspect of the number of funds one should have in a portfolio.

I’ve seen investors with 10-12 mutual funds in their portfolio for a single financial goal. Usually, their portfolio will contain 3-4 large-cap fund, another 3-4 mid-cap funds, few random debt funds, and perhaps a hybrid fund tucked in.

This is a classic example of a messy, directionless, and a pointless portfolio.

Ideally, you need to have non-overlapping mutual funds to avoid redundancy.

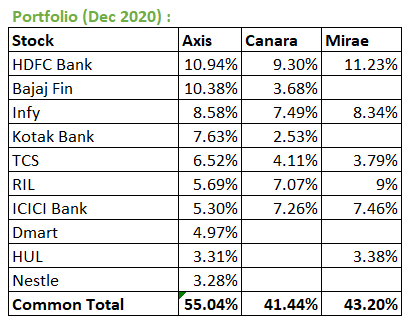

Let me explain, assume you have the following three large-cap funds in your portfolio –

-

- Axis Bluechip fund

- Mirae Asset Large cap fund

- Canara Rob Blue chip Equity.

All three funds are good, but does that mean all the three funds should belong in your portfolio. Take a look at the top 10 holdings across all the three funds –

As you can see, nearly half the portfolio across all these funds are similar. All funds hold HDFC Bank to the extent of 10%. If you extend this across all the portfolio holdings, I’m sure the common overlap would be a much bigger number. Given this, the performance across these funds also tend to be similar. The economic/market factors that impact these funds will be similar, and the volatility will be similar.

Hence, as an investor, if you buy multiple funds of the same type across different AMCs, then you need to realize that there is no significant advantage in you doing so.

Of course, the only argument for having two funds of the same type is AMC diversification, where you split your money across two different AMCs. You can probably do this if you worry that one of the AMCs may fold during the tenure of your investment.

The better way to do this is to see if you can include funds from different AMC, such as a large-cap fund from HDFC and a mid-cap fund from DSP, where you diversify across AMCs and market capitalizations.

As an investor, build your portfolio so that the overlap between funds is minimum. Eliminating overlap is very tough; the idea is to ensure its minimum. Otherwise, you just end up paying just to get the same exposure and costs can eat into your returns significantly.

26.4 – Portfolio, by the method of elimination

Let us revisit the scenarios we looked at earlier and see how the table can craft a mutual fund portfolio.

Case 1 – A newly married couple, aspires to buy an apartment, estimated at 1.5Cr in 10 years. Both of them work, hence can save 30K each, every month.

We have the following data –

-

- Savings per month – 30K each

- Target corpus – 1.5Cr

- Time available – 10 Years

- Age – Young can afford to take financial risks in life.

Given this, let us try and arrive at the portfolio by the method of elimination. I find the elimination technique quite powerful; if not for anything, the technique helps us avoid the wrong fund for the given financial goal.

Alright, with ten years’ time frame, we know that investing in debt is not required, so let us eliminate the debt category.

When I say debt is not required, I mean not required as the main investment fund. Let me get back to this in a bit. Debt has another role to play here.

The focus is clearly on Equity as the category. Within Equity as a category, we have a list of schemes available, which we need to start eliminating –

-

- Large & Midcap – may not work, since most of these ‘Large & Midcap funds’ are mid-cap stocks anyway.

- Small-cap funds – These are risky, volatile. Of course, ten years is a good enough period for this fund, but I’d personally avoid given the quantum of volatility involved in these funds.

- Multi cap funds – These are again qazi mid, and small-cap stocks, may as well stick to a straight forward mid-cap fund.

- Focused fund – Concentrated bets. Highly dependent on fund manager skills. If the fund’s investment turns out to be a mistake, the realization may come in a bit too late.

- Thematic funds are sector dependent; if the call on sector goes wrong, the fund will take forever to recover.

- ELSS funds – Useless one needs to save on taxes as well.

- Index funds – While this is a great option, somehow, a strict 10-year period may not do justice for these funds. These funds are best used for hyper long-term financial goals like retirement.

Given the rationale, we can eliminate all the above funds, which leaves us with the following options –

-

- Large-cap fund

- Mid-cap fund

- Value fund

I’d further eliminate the value fund due to the uncertainties involved in unlocking value stocks. Hence, the best option for the couple is to invest in a large-cap and mid-cap stock.

They both can choose a fund each across both these categories and start their investment journey. Do recall we have discussed how to select an equity mutual fund in the previous chapters.

The easiest way to invest the funds would be a systematic investment plan (SIP) in the selected mutual funds every month.

So how do the numbers stack up assuming a CAGR of 10%? Take a look at the calculation table below. Note, this is a not the entire table, it is just a part for you to get the idea –

I’ve assumed a CAGR of 10% for both large-cap fund and mid-cap fund, of course, we can argue endlessly on how conservative/aggressive this return percentage is, but it would be a waste of time for both of us.

As you can see, the couple accumulates 1.21Crs, which is quite close to the target funds over the 10-year window. A bank loan can plug in the deficit (which is not much).

Now, here is another aspect to consider. What if, as an when you approach the target year, the market starts to fall and you lose the accumulated wealth? This is a possibility; after all, no one can time the market.

One way to deal with this is to start to shift the corpus funds to a debt fund as and when you start approaching the target year. For example, from the 8th year onwards, they can withdraw the accumulated funds and park it in a debt fund. There are many different ways to do this –

-

- Withdrawl can be made on a monthly/quarterly/semi-annual basis.

- The funds withdrawn, can go into an ultra short term fund since we only hold the funds for 3 years.

The idea here is to protect the corpus from a sequence risk, where in the market takes a hit as and when the target year approaches.

Of course, this is a rather simplified approach, but I’d like to keep it simple and not over complicate it.

You may ask if this is a ‘fill it, shut it’ approach with no intervention during the investment tenure. Yes, this is largely a fill it and shut it approach. But once in a way (like once a year), one should track the fund’s performance and take a call on continuity.

Apart from that, you need to keep these two points in mind –

-

- Use conservative estimates when dealing with returns in personal finance. If in the end, the returns turn out better, then it is good for you. Consider yourself lucky.

- You need to understand that the equity returns are lumpy and not smooth and steady like a bank FD returns. You may have no returns for a long time, but the bulk of the returns will come in a short burst of times. Unfortunately, no one can time this short burst, hence the need to SIP and give it adequate time.

Let us look at another case and see how elimination would help us build a Mutual fund portfolio.

Case 2 – A 40-year-old person wants to save 25L over the next eight years for the kids’ overseas post-graduate degree. Monthly savings available for this goal is Rs.20,000/-

Since the period is less than ten years, there is no point looking at 100% equity investment. The plan would largely involve debt, maybe a small equity portion.

Ok, to begin with, let us keep Equity aside for now and look at the rest of the funds.

Hybrid funds like the Arbitrage fund may be a decent option, but something like a balanced fund may not be.

Debt funds are a good option –

-

- Liquid funds and overnight funds won’t fit the bill since we are talking about eight-plus years

- All funds with Macaulay duration of fewer than two years can be ignored since these are relatively shorter maturity funds.

- Money market funds too can be ignored since the investor can take on a slightly higher degree of risk

- A short-duration fund is an option

- Credit risk is risky so that they can be avoided.

- Corporate bonds fund is an option

- GILTS won’t fit the bill either.

This leaves us with three good options –

-

- Arbitrage Funds

- Short duration funds

- Corporate bond funds.

Investment in corporate bond fund requires a greater degree of involvement from the investor. If one decides to invest in it, then a regular review the scheme’s portfolio is mandatory. If this is not possible, then the only two options to invest in the short duration fund and the arbitrage fund. Probably the person can split the investment equally in both these funds.

One thing to note, just because the investment is in a short duration fund and arbitrage fund, it does not mean that a period review of the fund’s portfolio is not necessary. Yes, the short duration fund may not need as much scrutiny as a corporate bond fund, but it does require you to look at, at least once a quarter. The arbitrage fund too as the portfolio contains a debt portion.

I’ll spare you the maths here, but if you assume a 7% CAGR, the target funds can be accumulated over the given timeframe.

Since this is anyway a longish tenure, i.e. 8 years, one can also consider a little equity exposure. Maybe 20-25% of the monthly SIP can go into a large-cap fund.

Let us take up one last case – You’ve received a lump sum amount, say Rs.50L from the sale of an asset, maybe real estate. You want to use this amount and start a retirement corpus. However, you are worried about the current state of markets and fear that the current market level is unstainable.

Retirement is a hyper long-term financial goal. By hyper long term, I mean 20 plus years but may vary based on your current age.

Here is a plan assuming you are not comfortable investing the lump sum right away.

-

- Invest the lump sum in a fund which offers capital protection (to the best possible extent)

- Withdraw chunks of it every month and invest that into the designated fund for retirement

- Continue doing do so till you deploy the entire capital

In this case, you can decide to invest 50L over 3/6/12 months, based on your comfort.

Assuming, six months, then every month you will invest –

5,000,000/6

= 8.3L.

The question is, what is the choice of funds for such a plan of action.

-

- We need a carrier fund, which will hold the capital, provide adequate capital protection over the next six months.

- The only funds which fulfil the purpose of the carrier funds are – the overnight or liquid fund.

- Identify a target fund for retirement. Recall, retirement is a hyper long-term financial goal so the funds you pick for this purpose should fit this bill

- The best funds for retirement (in my opinion) are Index funds, large-cap funds, or just a balanced fund.

So the set up here would look like this –

-

- Park the entire 50L in a liquid fund to redeem the entire amount over six months

- Redeem 8.3L every month from the liquid fund over the next six months

- Invest the funds redeemed funds into the retirement fund – say a Balanced Fund and a Midcap fund. Or an Index fund and a mid-cap fund.

- If you are choosing two funds, the funds can be split equally.

Do remember, once you invest in these funds, this is largely on autopilot mode with no frequent intervention required from your end. However, you may need to look at the following –

-

- Yearly review of performance – ensure your fund is not lagging its peers and behaving more volatile compared to the rest of the category

- You may want to rebalance based on your risk appetite, wherein you book some profits from the equity funds and deploy the same in debt funds.

Apart from the above two, you are fairly set. Please don’t attempt anything else, and let the market do what it is supposed to do.

I’ll stop the case studies here since it is impossible to cover all sorts of cases. But I hope this chapter has given you a good starting point for designing your mutual fund portfolio.

I’d love to dig deeper on this topic of goal-based investing, but at this stage, I’m not sure if I will take that route. If you do want me to do that, share your comments below.

Over the next 2 or 3 chapters, I’d like to discuss the Sovereign gold bonds (SGB), NPS, and perhaps a bit about asset allocation, and wrap up this module.

Key takeaways from this chapter

-

- The first step in personal finance is to ensure you have health and term insurance

- 2nd most important aspect is to ensure you have an emergency corpus

- The financial goal is defined by the amount of corpus required and the time frame available to accumulate the corpus

- One of the easier ways to build a mutual fund portfolio is by using the method of elimination

- Always use a conservative approach and tone down your return expectations

- Try and avoid having multiple funds of the same subcategory, have a minimum non-overlapping portfolio instead

- A common goal for all us to have a retirement corpus

- Once a portfolio is set, a yearly review of the funds is more than sufficient

- Do not over complicate mutual fund portfolio construct

Hi Sir,

I have already invested in three mutual funds: a Large Cap Fund, a Flexi Cap Fund, and a Small Cap Fund in the ratio of 40% : 40% : 20%.

I learned that there may be an overlap between the Large Cap and Flexi Cap funds, as Flexi Cap funds often have a significant allocation to large-cap companies. Should I consider replacing one of these funds with another category of mutual fund?

Could you please suggest a good mutual fund combination for a long-term investment horizon of 15+ years?

Thank you.

Dear Sir,

My SIP investment horizon is 20 years.

Based on the insights you have shared, I understand that investing in a single Large & Mid Cap 250 Index Fund could be a suitable option, as it provides approximately 50% exposure to large-cap stocks and 50% exposure to mid-cap stocks, along with automatic rebalancing.

Alternatively, would it be better to invest in actively managed funds by selecting one large-cap fund and one mid-cap fund?

I would appreciate your guidance on which approach would be more suitable for a long-term investment horizon like mine.

Regards,

Nikita

Sure, only if you believe the active funds can beat passive over the 20 year period 🙂

Dear Sir,

I have very impressed with your valuable teaching on risk management.

Though i work as an accountant and i have family and does not get time to see the share market. So i always look on risk first.

So, now i have decided a mutual fund portfolio for SIP till for long run without changing or switching to any other active funds in future.

My new tension free monthly SIP portfolio:

SBI nifty 50 index fund : Rs.1,000

SBI nifty next 50 index fund : Rs.1,000

Again Thanks You Sir for valuable teaching on risk management.

Thanks for letting me know, and happy learning!

Happy investing for long term 🙂

Respected Sir,

Please guide if my current portfolio is good or need improvement.

my monthly saving is 10,000, from which 5,000 goes to Recurring deposit in bank and 5,000 goes to Tata Midcap fund.

I think it would be very hard to advice without full context. Why dont you speak to a financial advisor for this?

Hi,

Current i have mutual fund port folio:

SBI Nifty 50 index fund : 70%

SBI Midcap fund : 30%

yearly re balanced to same ratio.

Can you guide on ratio size or should i move to 50% & 50% in both fund.

Anil, I think it make sense to speak to a speak to a financial advisor for this.

Hi Karthik,

Although I am not very confident in making financial decisions like investments, reading these chapters has helped me a lot—especially the examples. I still have a few doubts, and I would really appreciate your help in understanding the following:

1. Since Nifty 50 index funds primarily consist of large-cap companies, should I invest in a large-cap mutual fund, a Nifty 50 index fund, or both equally?

2. I am confused between flexi-cap and multi-cap funds. Since fund managers in both categories can invest across different market capitalizations, how should I decide which one offers better returns relative to the risk involved?

Happy to note that, Lavish. Sharing a personal preference here –

1) I prefer just the low cost index as a proxy for large cap.

2) You can look at risk metric – standard deviation, downside capture ratio etc.

Understood, Thanks

Happy learning 🙂

Sir, I have only one fund that is SBI large and midcap fund

Please guide is this ok, or should I go with one large cap fund and one midcap fund from different AMC

Soumya, while I think its ok, maybe you should speak to a qualified financial advisor about this.

Sir, I need your view only as i also work under financial advisor.

Sir,

We know that to diversify in equity, we should invest across largecap, midcap, small cap. Likewise, in bond, is there any particular protocol, which we can follow like diversify across GILT, corporate bond etc. Time horizon to consider: 20 years.

Yeah, it depends on the goal of you portfolio. But diversification within bonds MFs largely means having a bunch – short duration, GILTS, Bank bonds etc. But bond MFs are not as straight forward as EQ, so you need to be sure on why and what 🙂

Hi Karthick,

I have 200000 corpus,

so I decided to invest 50000 in Large cap

50000 in balance advantage fund,50000 BSE Sensex

Index Fund and 25000 in Mid cap and 25000 in small cap.Is it a good mutual fund portfolio?

May be due to high work load, you or your team missed this comment, still waiting for the answer as soon as you guys got some time to answer this question.

Can you post the question once again? Sorry, it may have slipped through and I\’d have lost the context of your question.

You will have to check with an advisor to help you map your financial goal and allocation. That said, I think there is a bit of an overlap with a large cap fund and index fund 🙂

Hi karthik,

Thank you for curating zerodha varsity content. It has helped me learn about personal finance in a structured manner.

I have a couple of queries.

I am planning to create a 3 – fund portfolio for my equity investments. I have a long term view of 15 to 20 years.

I have curated two options –

Nifty 50 index + (one of Next50 or midcap 150) index + (flexi cap / multicap) active fund with a ratio of 60:20:20 for a total sip of 50k (25k each for me and my spouse)

Q1: Between nifty next 50 and midcap 150, which is a better index fundamentally to invest long term ? Similarly between multicap and flexi cap which is better?

Q2: What can be the optimal ratio between these three funds ? Is the active fund redundant unless it is as significant as passive in contribution ?

1) For long term, both are decent. Although with Nifty 50, you know you are following the index and have clarity on what to expect.

2) The ratio you have suggested is fair. Although I like passive, there are still a few active ones that tend to outperform. So it all depends on which fund 🙂

Thanks for the reply, Karthik.

I’m not sure if I fully understood your point. Could you please clarify the part about Nifty Next 50 (not Nifty 50) vs Midcap 150, and why one may be preferable? Are you saying both are equally decent?

Also, on flexi vs multicap — many proven flexicaps seem tilted toward large caps lately. I’m not sure if that’s by choice or due to their AUM. Given that, which category is a better bet?

About whats better, not sure if I can give an opinion. But I personally prefer Next 50.

Flexicap being tilted towards largecap, thats right. Thats also due to bloated AUMs in this segment.

Hi Karthik,

The content is quite useful in building a healthy money mindset. Cheers to your work!

Question- many times in the module you have mentioned \”Capital protection\”, what does it mean? As per my understanding \”Capital protection\” means your investment vehicle should give at least 6% return to beat inflation (assuming 6%) otherwise the money is losing its value over time because of inflation. When you say capital protection without looking at returns, I am bit confused here?

Thanks Ashish. Yes, capital protection means no erosion of the purchasing power of money. When you look at it this way, it factors in inflation.

In that sense, should we look at debt funds with at least 6% past returns (considering risk metrics and portfolio composition), so that in reality our capital is protected?

Yeah, which means your holding tenure should also increase.

Hi Karthik Sir,

I’m 35 years old with a corpus of around ₹50 L in PF and one year of emergency funds; 6 months’ expenses parked in an FD and the remaining 6 months in a Post Office account.

As I fall under the 30% tax bracket, I’m planning to restructure my emergency fund allocation. The idea is to:

Retain six months of expenses in an FD for immediate liquidity,

Move the next six months into a liquid fund

Park an additional one year’s worth of expenses in a short-term debt fund or an arbitrage fund.

I intend to diversify across different AMCs for risk mitigation. The broader goal is to maintain a total of two years’ worth of expenses as an emergency corpus.

Since taxation applies only upon redemption for mutual funds (unlike FDs that are taxed yearly), this structure might also be more tax-efficient.

Could you please share your thoughts, is this the right strategy for parking emergency funds or is there something I could do it better?

Regards,

Pavan

2 years seems like an overkill at glance, but I wont dispute that since each family circumstances is different. This if fine if it gives you the confidence, but somehow feels over engineered for an emergency fund. The main risk of emergency fund is not AMC risk, but rather liquidity, meaning the funds not being available when you need it the most.

Also since this is a lot of money being parked as emergency, please make sure its not costing you much in terms of opportunity cost. Meaning, the useage of this fund to build long term wealth.

I am just starting my career, and I have no particular financial goal in mind, but I want to start investing my money. So, I am thinking of investing in equity through SIP.

Is it ok to park savings for each month in only equity? if not, how can I do my asset allocation?

Yes, assuming you are young, you can start investing in Equity. You can start with asset allocation once you gain some foothold.

Downpayment Goal

Hi Karthik, three years ago, I started my investment journey with a SIP of ₹20,000 in the Navi Nifty 50 Index Fund. Every year, I increased my SIP by 10%, without having a defined goal in mind—my primary focus was just to build the habit of investing. Around one and a half years back, I also started adding some lumpsum amounts aggressively, and over time, the corpus grew to about ₹17 lakhs with an XIRR of 11%.

Now, I need this money for a home loan down payment. Looking back, I realize that since my requirement was within 2–3 years, investing in an index fund was not the right approach. Ideally, I should have chosen safer avenues aligned with the short-term horizon. With that realization, I have withdrawn everything from the fund and moved it into a fixed deposit at 6.5% for one year.

At present, I’m in a dilemma—should I just keep this in an FD, or consider moving it to a debt mutual fund? On one hand, I know FD interest will be taxed at 30% given my tax slab. On the other hand, I’m not feeling confident enough about debt funds considering the risks involved. My home purchase is likely within the next 1–2 years, so capital safety is my top priority.

I would say I am lucky that the market has given me an XIRR of 11%, otherwise I would have been in trouble as I did not understand the risk properly.

Am I being too conservative by sticking fully to FD for such a short-term goal, or is this the right approach given the circumstances?

By the way, this series on personal finance has been amazing, and I’ve learned a lot from it.

Hi Raj, I\’m glad you liked the content here.

1) Yes, ideally EQ investment for under 5 years is not a good thing. We do get lucky at times (like how you did), but thats just luck. Could have been anything.

2) FD is fine if its just 1-2 years. Your other option for 1-2 years is a short term debt fund, which gives you similar returns as FD. However, since its just 2 years, you may not get tax benefit.

By the way, we are working on something interesting, and your case seems to fit some of the criteria we are looking at. Can I ask my colleague to email you?

Thank you, Karthik, for the reply. Yes, I’m interested—please go ahead and ask your colleague to email me.

Thanks, will do 🙂

Thank you so much for this tremendous work you have put into this for us. Read many times and keep visiting time and again for doubts. Most consider the scenario of young people to build the case studies while explaining the MF investment which is understandable. But in our case, we are in 50s, post is little long..sorry

1. Started building MF portfolio with RIA almost 9 yrs ago and on my own for many yrs now.

2. Didn’t strictly follow 50:50 suggested, portfolio is 75:25(Eq:Dt)now…have Lcap(predominantly), ValDiscovery, and savings fund.

3. Elder son’s education at present – taken care of by present debt portfolio

4. Younger son’s education – 50% of accumulated current Eq portfolio plus SIP in ST debt fund over next 5 years should meet the requirement.

5. Bought house for retirement living.

6. Will be getting pension enough to take care of two of us. My big Question is : DO I REALLY NEED RETIREMENT plan?

7. In this scenario, my future investments (apart from debt sip for education ) will be basically wealth creation, wealth preservation though timeline is not there. Remaining 50% of Eq portfolio to meet any obligation for next 10year or so.

With these scenario, I was planning to direct my future investments(5-6years till retirement) to Nifty 50, NNext50 and conservative hybrid(debt component), ST Debt fund which may be needed after 10years.

Am I fine with this thinking process? Or should I go with active funds as time period to retire is 5 yrs?

Note: approximately 50% of Eq portfolio(large amount)is in ICICI large cap fund. So don’t want to shift to avoid paying LTCG tax.

If you could find time to go through, I would be grateful.

Thank you

Yavika, you seem to be largely sorted. But let me share some risk concerns –

1) At age 50+, sequence-of-returns risk is significant: if markets correct sharply in the next 5–7 years, a 75% equity allocation could hurt retirement corpus just when withdrawals are about to start.

2) Since pension covers day-to-day expenses, the equity tilt is less threatening, but education and other big goals in the next 5–10 years are still market-linked. If a downturn coincides, equity redemption might force a loss booking

3) ~50% of equity corpus in ICICI Large Cap Fund.

4) Tax concerns (LTCG) are valid, but diversification can still be built through new SIPs in other funds

5) Pension covers both lives today, but question is whether it’s inflation-indexed. If pension is fixed, real value erodes in 15–20 years. Medical inflation (12–15% annually) is a particular risk.

I\’m not a professional financial advisor, I\’d suggest you think through these, sit with your RIA and figure what could go wrong. Take a risk first approach to plan further.

Thank you very much for your time and explanation sir.

1. Understood the sequence of return risks, would be bringing down the Eq ratio down. While rebalancing is it always necessary to sell the profit in Eq portfolio and invest it in debt? Or it would just be fine if I keep adding lumpsum(like bonus) into debt portion and balance it?

2. Planning to divert new SIPs in Flexicap or NNext50 to reduce dependence on on AMC.

3. Pension is inflation adjusted (6-7%) annually, but didn’t think of medical inflation to be 12-15%…scary. Thank you, shall plan.

🙏 warm regards

1) Adding more to debt is also as good as re balancing. But yes, the idea is to reduce EQ portion and move assets to debt.

2) Sure, I hope you\’ve done the needed due diligence.

3) Yeah, thats unfortunately true 🙁

In an 80-20 equity-debt portfolio allocation, I am planning to put the 20% in arbitrage, gilt, and low-duration funds in a 50:25:25 ratio. Is that a good strategy for the long term (around 5 years)? Or what would be the ideal debt allocation for balancing a long-term portfolio?

I\’m assuming you are young, so 80-20 split seems fine to me. The split is also fine, but have a longer duration that 5 yrs for debt 🙂

Hi Karthik,

I had a question about parking emergency funds. I currently have 6-7 months of expenses (single income) saved in a liquid fund. I just received a lump sum amount that I am looking to add to my emergency fund because I know that my expenses will increase in the next 3-4 years. What are your thoughts on starting a secondary emergency fund in a conservative hybrid fund?

Thanks for all you do to further financial education!

Emergency fund is supposed to be parked in non volatile instruments. I\’d suggest you look at simple FDs or an arbitrage fund 🙂

Hi Karthik. I started the modules today and am already loving them. Can you please take up one last case – How to build a retirement portfolio with SIPs? I am confused as to which funds (equity/debt/gold) to park my money in. Thanks in advance..

Sagnik, thanks for sharing this concern. Please start with an index fund – maybe one large cap and a mid cap. Unfortunately I wont be able to help you with specific fund name, for that you will have to speak to an advisor 🙂

Thanks for the reply. So, should I start with 100% equity in the initial years and as I progress towards my retirement, I rebalance my portfolio?

I do not need the fund names. I will do my research. I require your guidance in choosing the categories and want to know what you would pick in such case.

Thats a reasonable approach, but I should also warn you that I\’m biased towards Equity 🙂

Best wishes!

Hi Karthik sir

So ive decided to invest in around 7 mutual funds. i wanted to explain my rationale and see if it makes sense.

1 Large cap fund

2 mid cap fund (for divesrification and hopefully better returns)

2 short term funds (for diversification)

1 flexi cap fund

1 index fund

does this make sense? Or should i specify the fund that ive picked as well

I\’d consider the index fund and large cap fund to be similar. Everything else is ok, but please do speak to a professional advisor once 🙂

Hi Karthik Sir

is there much of a difference between investing in a large cap and an index fund? they seem to be fairly overlapping.

Also sir While I was trying to gauge index funds I couldnt find much data apart from the expense ratio and initial investment amount. Should I base my investment into index funds (for the long term) based off of these criterias?

lastly, if for my retirement I was to divide my investments into say a balanced advantage and index fund or a balanced advantage and flexi cap fund, would that make sense?

Yes, they are similar. The biggest data point for index fund is the index itself 🙂

By the way, you can track the tracking error for the Index fund. Lower the better.

Yes, either of the combination is good, but do consider index as a common denominator.

Hi Karthik

So im a bit confused about the downward capture ratio. Youve mentioned that its good if its capture ratio is high. However, doesnt it mean that it captures most of the losses? Which isnt a good thing right? So is it that if a MFs downward capture ratio is higher than the benchmark (say 84 against 76) then its good or bad? and if so why?

Sanjay you want the downside capture ratio to be a small number—ideally below 100%.

What it means –

> Downside Capture Ratio measures how much a fund falls in comparison to a benchmark during market downturns.

> A ratio of 100% means the fund falls just as much as the benchmark.

> A ratio below 100% means the fund loses less than the benchmark (which is good).

> A ratio above 100% means the fund loses more than the benchmark during down markets (which is bad).

Have I said otherwise in the chapter, if yes, my bad, clearly a typo 🙂

alright thank you!

Sure, good luck!

hi so i was trying to figure out the rate for my retirement corpus. Id used inflation rate as 7%, amount needed every year as 3.6L and the year starting from 2065 till 2095 (who knows if ill live that long but its this is just for practice). Im getting the corpus as an insanely huge amount! iVE probably done something wrong in my calculation or in my understanding of future value so I wanted to know as to what could I have done wrong considering these figures.

Also, thank you so much for constantly replying to my queries.

It is usually a shocking number 🙂

Maybe you can reduce 7% to 6.5%, but then when it comes to retirement planning, its always good to be conservative.

Hi Karthik,

Why are you completely ignoring flexi cap funds?

Not really ignoring, including funds based on portfolio needs 🙂

Hi

I also did not understand how do i Integrate the future value in the whole MF portfolio. I also couldnt digure out how much SIP I should put. How do I get the excel sheet like you got it, which integrated the SIP and the future value

Future value? Not sure if I fully understand this query.

ok im sorry for that confusing message. I was having confusion with figuring out an adequate discounted rate to select for deriving the future value formula. How do I go about doing that?

Ah, you mean to say the rate of return? You can assume a return between 9-11% for this pre tax.

Hi Karthik sir

thank you so much for these modules. I wanted to express my gratitude on this because I couldnt find a comprehensive coverage, with a few directives, towards understanding personal finance.

Albeit im not an employee, I wanted to know if lumpsum investments can make a dent if I were to say invest them and keep it running over a period of a year. Id follow all the steps of analysis, except that I wouldnt be able to SIP it. Does it make sense to do that or should I consider doing an SIP based off of the amount that I hold?

additionally, I checked coin and found a huge number of equity and debt funds. Is there maybe, idk a short hand way of discerning through the many funds or is it the whole process of checking each and every one along the various steps youd recommended and then coming to a conclusion?

Thanks Sanjay.

The only issue with lumpsum is that your timing matters, but with SIP that is not an issue. Why not do something like this – Lets say you have 1L to invest as lumpsum, park that money in a bank or liquid fund, pull 5 or 10k of it everymonth and invest it like SIP?

If you are fully new, then look for Index fund.

alright ill look at the SIP idea that you had suggested. Thank you!

ok I had a question: why not keep the money in my bank account itself instead of a liquid debt fund? it might be a stupid question but is it because liquid funds would give some better returns than the bank?

You can do that as well, but as long as you ensure that you dont utilize that money towards other things. Parking it in a liquid fund is more of a mental setup, where in you tell yourself that the money is for investment and not for other things in life 🙂

Sure, wishing you the best!

Hi Karthik, what should one do after Yearly performance review of the fund? Let\’s say the fund is not performing well compared to competitors. So we should look out to exit from that fund and invest that sum in another fund?

In that case, there is actually no guarantee of the new fund being performant when do the review of it a year later. And another assumption might be is that, the existing fund might be performing not well at that particular time but it can take momentum at any point in time, correct?

So, how should one look at this. Please kindly elaborate.

As always, thank you for this valuable lesson.

Firstly, there are no guarantees that a particular fund will perform 🙂

I\’d suggest a yearly review to get started. Ideally, the fund should be better than, if not equal to, the category average returns. If not, consider an exit. But that said, there could be periods where a fund may not deliver for a bit before it can take off, but to identify such reasons, you really have to dig deep into the fund\’s portfolio etc.

Hi Karthik. How do you feel about flexi cap funds? Do they deserve a place in our portfolio?

No feelings for any particular kind of MF 🙂….it really depends on your financial goals, and if that fund serves you in achieving your financial goal.- From Karthik 🙂

Flexi cap funds is a must have in the portfolio. There is no need to think or calculate so much while investing in mutual funds as most of the good funds gives returns(between 8 to 15%) above inflation(except situation like covid).

Hmm, must have? It would depend on the portfolio goals right?

If we withdrawn money suppose in 8th Year so, there will be LTCG and we have pay Tax there. So how to deal with it? Please guide Sir.

You will have to pay LTCG, no escape there 🙂

Hi, thanks for the tutorial.

I have two questions:

1. When I try to invest in large-cap funds on Zerodha, it recommends I invest in index funds instead. My investment term is around 10 years, and in general, index funds have been seen to outperform actively managed large-cap funds, due to lower management costs. So, I am not sure why you say that for a strict ten year term, index funds may not be ideal, and they are good for \”hyper long term\” goals. Could you please define \”hyper-long term\”, and also clarify why an index fund is not ideal for a 10-year period?

2. You have recommended that it\’s best for people to have a small number of funds in each category, because these fund holdings often mimic each other. I can imagine this happening for large-cap funds, because the total number of large-cap stocks is low. But in mid-cap funds, I find a lot of variation in stock holding. So, do you still recommend your strategy of holding only one of every type of fund in mid-cap and small-cap too?

Thanks, and look forward to your response.

1) I think anything around 15 plus years in my view is hyper long term 🙂

2) I get your point, but fund managers all chase returns, so they tend to cluster around the similar set of stocks.

I’m 27 year old, considering to invest in 3 safe funds. I’m a beginner! I have considered nifty 50, icici gold etf and Parag Parikh flexicap. One of my trusted agent is saying to invest through them. And as well the ICICI.

I want to invest and forget about it for 3-5 years. So is lump sum a good option?

I’m very confused as I’m moving to US in a month. I want to do it beforehand

If you have a trusted agent, who will hand hold you, then fine, please go ahead. Lumpsum is good, but I\’m assuming you are aware that you will not benefit from averaging. Also, if the market stays muted for these 5 years then so would be your returns.

What is the advantage of debt fund over an FD? I feel FDs are much better since we don\’t have to worry about the debt fund portfolio of it is holding AA or AAA rated papers.The only advantage of debt fund I can think is withdrawal of funds anytime(that to hoping investment is not dented due to default).

The big difference is the fund structure and the fact that a debt fund is a market linked instrument, unlike a FD which is not.

Plz help me out of hand to make portfolio in mutual fund with my retirement benefits which I will about to receive.

I want one to one discussion

Regds

D. K. Kanjilal

Kolkata

9830078574

My ph. No is 9830078574

D. K. Kanjilal

Plz help me out of hand to make portfolio in mutual fund with my retirement benefits which I will about to receive.

I want one to one discussion

Regds

D. K. Kanjilal

Kolkata

I\’d suggest you speak to a good financial advisor in your circle.

Sir,

With regards to retirement planning, as you suggest that GILT debt fund could be an option. In between, which one could be a better choice- The gilt fund itself or with constant duration?

For longer term, maybe GILT itself. I\’d suggest you speak to a proper financial advisor for this 🙂

Sir,

Do gold ETFs has things like dividend/coupon? If yes, who is responsible for that funding?

Ah, no, they dont.

Sir,

Do you personally invest in outside country? Zerodha has taught us to diversify outside India. However, in coin, I could find the S&P 500 index fund, however, the expense ratio is on high side, considering an index investment.

What should be the approach? Can I still consider buying or any suggestion?

No, I dont have any MF investments outside India. Yes, these expense ratios tend to be high because of the intermediaries involved.

Sir,

I am a little confused taking debt funds. Looking for long term retirement planning, could you Please suggest me a possible type of debt fund which could be invested in?

A fund protection will suffice my requirement in debt fund category.

If its long term, maybe you can consider GILT funds, Anirban.

Sir,

(i)In case of Growth Debt fund, do the coupons automatically get reinvested in the fund?

(ii)For a long term investor (20+), as growth fund is suitable in case of equity, which fund (growth/IDCW) is suited in case of Debt fund?

1) Yes

2) Growth, always.

Sir,

(i) In case of IDCW-Interim gold FoF, do we used to receive payments? If yes, which entity is funding here with the payment?

(ii) For a long term investor (20+), as growth fund is suitable in case of equity, which fund (growth/IDCW) is suited in case of gold FoF?

1) I think you do, even I\’m not sure about this. Have never invested in one.

2) I\’d suggest a simple Gold ETF.

Sir,

(i)If I want to protect my capital with less headache and not chase returns, what according to you would be the best possible type of debt fund to invest? Will it be the Banking and PSU fund?

(ii)Also, Regarding PPF, can it satisfy to give capital protection?

1) Short term debt funds maybe? But for what purpose are you using this?

2) Yes, it can.

Sir,

Regarding investment in Gold, instead of MF, can investment in \”goldbees\” serve the same purpose?

Sir,

Debt funds, as to me, is not straight forward as equity. Just to ask- Can I substitute debt funds with \”PPF\” in terms of fund protection?

Sir,

As we know, for equity, SIP holds good whether the markets are up/down for long term investment. Also, during low market, we can do some lumpsum.

(i)Now, in case of debt MFs, do the same principle holds good i.e, SIP whether the bond price is at a cheaper or dearer?

(ii) Also, when the interest rates are high, can we do some lumpsum investment? Please suggest.

1) Yes

2) You can, but this assumes you know how to time the debt market.

Sir,

I am looking a long horizon for investment. With this view, which one will be better- Banking and PSU debt fund or Gilt fund?

Either, I\’d say. Also, when investing in debt funds, know what and why you are investing. You need to be clear about your investment obective

Sir,

I have a newbie to MF investment. I want 20% allocation to Debt instruments. In this perspective, I would like to know that is it wise to diversify in Debt instruments also like , Short term, Mid term and Banking & PSU? Or taking one from the list will suffice?

That depends on what exactly you want to do with Debt funds, you need to define your objective.

Sir,

I wanted 10% investment in Gold. Kindly confirm if the below fund could be intended for my purpose:

ICICI Prudential Regular Gold Savings Fund (FOF)

Direct

Growth

Others – Fund of Funds

Sure, I guess so. But do double check again with a financial planner if you know one. Other alternative is to just go for an ETF.

Sir,

I could find two types of investments in real estate- REIT & REMF. Which one will be best suited for long term? Any advice on it?

I\’d suggest a REIT directly, you don\’t need a REMF.

Sir,

Regarding diversification, is it advisable to invest in REIT MF? May be 10%?

Meanwhile, I have no idea of this REIT investment and come across below 4 REITs:

1. Kotak International REIT FOF (Growth & IDCW-Interim)

2. Mahindra Manulife Asia Pacific REITs FOF(Growth & IDCW-Interim).

Could you kindly suggest which one to take for and how these two funds from two houses differ? Also, I believe growth will be more prominent to take for?

Request your kind inputs.

Anirban, you can check this video, it will help you understand how to analyze an REIT – https://www.youtube.com/watch?v=XhCeX98vY28&list=PLX2SHiKfualEyD05J9JsklEq1JFGbG6qJ&index=13

Sir,

Although I had asked in the previous query, I would like you to specifically guide me (considering hyper long term investment ,25+ yrs):

(i) Whether to go for both index and MF for midcap/smallcap? If it is yes, pls help with a generic proportion to invest for index and MF for mid and small cap.

(ii) There is an index fund for micro fund also. Is it advisable to keep that in portfolio?

1) I\’d say avoid smallcap, but maybe large and mid cap. Assuming you are young, you can do 60 large and 40 mid. But please double check with a qualified advisor once for this.

2) I personally prefer index.

3) Not sure, but even if its there, I\’d hesitate to include that in my portfolio.

Sir,

I want to park some money in gold, however, confused on mode to invest. Could you kindly suggest the mode- MF/ETF?

If MF, I am seeing all such MFs to be FoF? I request you to please help/guide me take decision.

Thats right, most of these funds are FoF, which invest back in an ETF of sorts. Thats ok, but be aware of the expense ratio.

Sir,

Regarding a hyper long term investment, I have decided to park money in only growth Index funds.

However, for investment in midcap & small cap, should I park money in both index funds and MF? Or only MF will be suggestable in this segment? Please advise.

There are mid cap index funds too, that are good. You can check that as well.

Hi Karthik,

Thanks for the great article! I had a query regarding the cost aspect when investing in multiple funds of the same type. To quote the article,

\”As an investor, build your portfolio so that the overlap between funds is minimum. Eliminating overlap is very tough; the idea is to ensure its minimum. Otherwise, you just end up paying just to get the same exposure and costs can eat into your returns significantly.\”

My doubt is, irrespective of whether I invest INR 10k in one fund or INR 5k each in two funds, wouldn\’t the cost be the same? (Assuming both have similar expense ratios).

While I completely agree that there is no point in having multiple funds with overlap, there is often variation in some of the fund returns even though they belong to the same category, so wouldn\’t it be a good idea to spread our money across a few different promising funds of the category we are interested in (to smooth out the variation/volatility in the various fund returns). Once again, thanks for the insightful information!

Ayushman, most people wont split their investments the way you suggest. More often than not, its random. Yes, if you split this the way you suggested then it adds AMC diversification. You can do this if you fear one of the AMC can go kaput.

Dear Karthik Sir,

Please mention which index fund.

Nifty 50

Next 50

Nifty 500

Nifty 150

Nifty 250

It depends on your risk profile.

Dear Karthik Sir,

I want to invest 5,000 monthly sip for life time till my retirement. My current age is 36.

Can you guide which fund will be suitable for me.

Ah, I cant help you pin point to a fund. But if I were you, I\’d pick and index fund 🙂

Yes sir

Can i rebalance this? Need your strong advise.

1. Kotak Bluechip – 1,000

2. Nifty 50 Index fund – 1,000

Total Large cap – 2,000

3. Tata Midcap – 2,000

Total Midcap – 2000

This seems ok, but why two large cap MFs? Is that to diversify b/w AMCs?

Sir,

i have three mf sip

1. Kotak Bluechip – 1,000

2. Tata Midcap – 1,000

3. SBI Multicap – 1,000

I need your guidance on this as i need only two SIP to continue only. OR should i continue with these three.

Please guide as per your experience.

I think there could be overlaps b/w Kotak and SBI. If I were you\’s I\’d probably stick to Kotak and Tata, but then its based on what I think. Your situation could be different, so I\’d suggest you speak to some good RIA to figure this 🙂

Dear Karthik Sir,

Should I go for large cap and midcap fund OR multicap fund.

I am little confused on this.

Please help on this

This depends on your portfolio goals, right?

Hi Karthik Sir,

I have a doubt again…. like I started to figure out my goals and trying to find the fund categories as you taught in this module.

For the goal to have a retirement fund and taught of investing in index funds… While analysing these funds does not have any major difference with AMC as this is a passive and Tracking index. So do this hold any major difference between other AMC\’s funds than TER and Allocation Category.

Do we need to focus more on finding the best index fund?

Yeah, keep an eye on the TER, that is one of the most important aspects.

Hello Karthik, great set of lessons i feel im late to learn all this but i know its never too late. In most of the chapters you are discussing about returns in debt and equity in various time periods. But the returns are not the take home money right, there is some important tax component like STCG and LTCG it would be best to include the tax component and let the readers know the modified returns like you explained the expense ratio.

Glad you liked the content here, Abhimanyu. CAGR is not the return you take home, but rather the growth rate you experience. The return you take home is absolute return on which taxes are applicable.

CAGR is crucial when making investment decisions.

Hi Karthik Sir,

Hope everything is good…

We have heard of SIP and Lumpsum but what about SWP? Since it has been a trendy topic in these recent days. Is it more powerful than SIP rather than Withdrawal of money at a single shot why not withdraw from the middle as the remaining corpus will accumulate the withdrawal Money.

I would like to hear about this because i\’m not fully known about this….

SWP is the opposite of SIP, where in you systematically withdraw funds over time. Will probably write about it in detail in Varsity blog.

Thank you for writing this informative chapter. Can you please help me understand this part?

\”As an investor, build your portfolio so that the overlap between funds is minimum. Eliminating overlap is very tough; the idea is to ensure its minimum. Otherwise, you just end up paying just to get the same exposure and costs can eat into your returns significantly\”

If I invest say 10000 in two funds each in the same category with the same expense ratio, or 20000 in one of them, I will end up paying the same amount. How do I save on cost by minimizing overlap?

Thanks

Here you will be investing in two funds, which in turn has same set of stocks. Your returns will be similar. So the idea is to minimize such overlaps.

I am recently retired and want to invest in Mutual Fund. Can you suggest few portfolios either for lumpsum or SIP. Let us also assume, I may need systematic withdrawal from 2028. You may pl consider, I have one crore in my hand.

Ah Ashok, I\’m not sure if I can suggest funds. I\’d suggest you speak to a Registered Investment Advisor for this, they can help you plan the portfolio better.

Hii Karthik

Thanks for amazing articles

Few queries

1.can you suggest good MF category for 1 to 2 year for good return

2.best mf category or combination for retirement planning i e for 20+ year

3.Can we use suggest best mf category combination

For 5 years 10 year 15 ,20 and 25 year

Unfortunately I cant as I\’m not a certified advisor. But this also depends on your goals. Please do take help of a professional advisor for this.

Thanks Karthik for your response. Now I can able to get it that it entirely depends on how much risk we are willing to take.

Please let me know what will you choose if you are in my shoes.

1. Large cap active funds vs nifty 50 + nifty next 50 index funds

2. Midcap active funds vs midcap index funds

1) Nifty 50

2) Active

Hi Karthik,

To add more to my point,

lets consider 2 scenarios.

scenario 1 : opting for large cap fund

My pick was ICICI prudential bluechip fund. Lets consider 11 years of investment. The SIP amount is 10000 per month. The annualised return of this fund is 17.57%. This would have generated a sum of Rs. 37,60,511.

Scenario 2 : opting for index fund

My pick was Bandhan nifty 50 index fund and ICICI prudential nifty next 50 index fund. Lets consider the same 11 years of investment. The SIP amount invested is 5000 per month in each of these funds. The annualised return of these funds are 14.27% and 17.8% respectively. This would have generated Rs. 15,82,547 and Rs. 19,64,178 respectively (Total 35,46,725)

By looking at the above scenarios, large cap fund tend to beat the index fund right? what am I missing here? Also, I didn\’t pick any star active fund here.

My investment horizon is for at least 20 years. But I considered 11 years because the funds that i considered is 11 years old.

Please enlighten me on this. I\’m so confused to choose between large cap active fund and index funds.

And for midcap category, I\’m convinced to go for index funds to avoid risks as this category is highliy volatile. Am I right here? or considering the 20 year investment period should I take risk and go for active mid cap fund?

If you have any other suggestions apart from these are much welcome.

Sridhar, I think in India, there is still scope for an active fund to beat the market. At least thats how it has been for so long. But since we are forward looking 20 years, the question you need to as is – will this out performance continue during your period of investment? If yes, then yes, an active fund makes sense. If no, then you are better off with an index fund.

Hi Karthik,

1. As per the reports published last year, more than 80% of large cap funds beat their benchmark and gave good returns whereas on the other hand 48 out of 52 nifty 50 index funds failed to beat their benchmark. Should this be a concern? the large cap active funds were struggling since the time Sebi introduced the total return index (TRI). Have they finally find a way to beat their benchmark? what is the reason behind the index funds failure?

2. Please help me on this as I have finalised my list of mutual funds. three index funds (nifty 50, nifty next 50 and nifty midcap 150) and one flexi cap fund.

Now I\’m just confused whether to go for large cap active fund rather than nifty 50 index fund.

3. Also I could see few index funds like midcap 150 momentum 50, midcap 150 quality 50, nifty 50 value 20. how these funds differ from their traditional index funds? are these better option to invest rather than midcap 150 & nifty 50?

Your insights on this will be really helpful.

1) With index funds, the idea is not to beat the benchmark but to match the returns of the benchmark. The reason is tracking error. There will be some difference between actual index return and the return you\’d experience as an index fund investor, but that difference will be small.

2) For this, I\’d suggest you speak to a good financial advisor, dont think I can advice 🙂

3) Again, this depends on what your financial goal is and how much time you are willing to give your goal. There are plenty of index funds and varieties. You need to understand what works for you 🙂

Hi Karthik,

Thanks for simplifying the mutual funds for common people like me. After reading through it I started investing.

I am 25 years old and below is my investment plan for a goal for a monthly SIP of Rs 5000.

1. Large & Mid Cap Fund (50%)

2. Flexi Cap Fund (50%)

Now, I want to increase my monthly SIP to Rs 10000.

Should I continue with the above funds with the same allocation percentage? Or, do you suggest to add another fund? If yes, which one and what will be the allocation percentage overall then?

Yes, if I were you, I;d invest more in both these funds instead of adding new funds.

Also, I have one question about lumpsum amount investing. Let\’s say I have 20 Lakhs of corpus which I want to deploy as lumpsum (it can be one-shot or staggered way too).

Given that below are the 2 goals of mine, the respective funds and its splits, how would you suggest to split and invest those 20 Lakhs across these funds?

Goal 1: Retirement Planning (1 Lakh)

1. Index (Nifty 50) Fund (40%, 40,000)

2. Large & Mid Cap Fund (60%, 60000)

Goal 2: Returns Making (1 Lakh)

1. Flexi Cap Fund (50%, 50,000)

2. Multi Cap Fund Fund (20%, 20,000)

3. Multi-Asset Allocation Fund (30%, 30,000)

One easy way to think about this is to split the funds equally and spread it across all funds.

The thought about keeping a multi-asset allocation hybrid fund (ICICI Multi-Asset Fund) is that it invests in at least 10% in 3 different asset classes such as Equity, Gold and Debt. Also, the other 2 funds in that particular goal are Flexi Cap & Multi Cap which fall into comparatively highly volatile zone. So, this Multi-Asset fund will provide some cushion to the portfolio.

Also, when I grow old (let\’s say 10-20 years later), I would need to reduce equity exposure. Then, I will have to look for another fund. I think Hybrid fund would be okay in that case. So, instead of starting then, to maintain discipline and not getting into headache of switching funds then, I am continuing with one hybrid (multi-asset) fund from now itself (of course with a small percentage). And when I keep getting older, I will reduce equity exposure and increase hybrid fund exposure accordingly.

Well, that\’s my thinking after learning so much from varsity. What are your thoughts about my thought Karthik?

Makes sense Amit, I just wanted to understand your opinon on why multi asset funds. Also, please do double check once from a professional investment advisor. Wishing you the best.

I am 30 years old and I have the flexibility to invest 2 Lakhs per month into Mutual Funds.

After reading this chapter, here is something I am thinking to distribute 2 Lakhs across 2 different goals:

Goal 1: Retirement Planning (1 Lakh)

1. Index (Nifty 50) Fund (40%, 40,000)

2. Large & Mid Cap Fund (60%, 60000) – thinking of keeping this instead of a pure Mid Cap Fund to be a bit safe.

Goal 2: Returns Making (1 Lakh)

1. Flexi Cap Fund (50%, 50,000) – since this is majorly Large cap stocks

2. Multi Cap Fund Fund (20%, 20,000) – thinking of keeping this a pure Mid cap or Small Cap to be less volatile

3. Multi-Asset Allocation Fund (30%, 30,000) – to maintain balance in the portfolio for safety

How does this look Karthik?

Thats a sizable amount to invest. I hope that grows over the years and creates lot of wealth to you and your family 🙂

The split sounds ok, except I\’m unsure about the multi asset allocation and its purpose.

Hi Karthik

Big fan of your work.

After going through your modules I have done some research for the 2 months and identified funds for my portfolio. If you could share your insight on this it will be really helpful.

1. ICICI prudential bluechip fund (investment time : 15 years. financial goal : Child education) (reason for picking : more number of holdings, less risk ratios, good rolling returns)

2. Zerodha large mid cap 250 index fund (investment time : 20 years. financial goal : child\’s marriage) (reason for picking : liked the concept of this index. upon my research, found that its lesser risk compared to mid cap index and better returns when compared to large cap index. Also, Edelweiss offers lesser expense ratio than zerodha but my bias towards zerodha made me to choose this. Hope zerodha reduces the expense ratio in the future)

3. Parag Parikh flexi cap fund (investment time : 25 years. financial goal : Retirement) (reason for picking : considering the duration, I thought I would take bit more risk)

4. Nippon India Nifty smallcap 250 index fund (investment time : 25 years. financial goal : Retirement) (reason for picking : considering the duration, I thought I would take bit more risk)

1. Also, I would like to know when it comes to mid cap & small cap funds, is it advisable to invest in active funds rather than index funds? why because, all the index funds that I see under midcap 150 and small cap 250 are newly started ones and I don\’t have any historical data to research.

2. what would be your combination of funds (like large cap, mid cap etc) if you are to invest in 4 funds for duration of 20 years.

3. I chose active funds in nifty 50 category over index funds because I expect large cap active funds to perform well over index funds for a 20 year span. Am I right here or should I invest that also in nifty 50 or nifty next 50 index funds?

4. Is investing in large mid cap category a good option or its better to take some risk and invest in mid cap funds?

5. Am I taking too much risk in adding flexi cap and small cap index funds to my portfolio?

I\’m sorry to shoot these many questions at you. Its just that even after doing these many researches for over 2 months also, I\’m stuck to choose between the funds as there are numerous funds under different categories.

I would just need your insight like what will you do if you are in my position.

Many thanks to you for your work on these modules.

Thanks Rohit. All the 4 funds are good, although the Zerodha fund is relatively younger. And I\’m obviously biased given my close association with the fund. I\’m glad you\’ve identified that these funds need a lot of investment time and are willing to give that. Its ok to stick with a avg fund for a long time versus a star fund for a short duration. Time heals all investment mistakes 🙂

1) Yes, I guess that is ok, although I personally invest in Nifty Next 50 Index fund.

2) An equal split is fine too. Or maybe a slight bias towards retirement.

3) SPIVA data suggests otherwise, where over 10+ years, index funds tend to outperform active funds.

4) Its ok, dont hesitate to invest. Give it time though.

5) I\’m not a fan of small cap fund at this stage in my life 🙂

Good luck!

Hi Karthik, I am 40 years old and have mostly invested in Mutual Funds via research and advice from helpful articles like yours. If I share my current mutual fund portfolio, are you able to provide your feedback?

While I did consider stocks as well, did not proceed due to lack of clear understanding about the process and which ones to opt for.

Thank you for your great advice and insight.

I\’m glad the articles help 🙂

Unfortunately, I wont be able to do that. I\’m not a registered advisor 🙂

Hi Karthik,

Appreciate you for awesome content !!

I am new to the investment world. I have the flexibility to invest Rs 1 lakh per month in MFs. I will turn 30 this May. I’m unmarried, have no debt/loans and my planned investment horizon is 15+ years.

Considering moderate risk profile for me, would you mind suggesting a sample MF portfolio for me that includes number of funds, their respective category, the percentage allocation, etc.

Thank you in advance!!

Priyanshu, please talk to a professional RIA for this, they will be he happy to help you with this 🙂

Any specific reason for not having the Multi Asset Fund and having a Mid cap fund?

Reasons to include or not include a fund depends on portfolio goals, AMit. I\’m not sure if I cant talk more about fund specifc things, I\’m not a RIA 🙂

Which Mid-Cap Fund would you prefer, HDFC Mid-Cap Opportunities Fund OR Kotak Emerging Equity Fund?

Or may be a Mid-Cap Index Fund instead?

Amit, there are many factors based on which you can select a fund, I\’ve discussed that in the previous chapter on how to pick an EQ fund, request you to watch that 🙂

Dear Karthik,

Just a suggestion request from me. And I’m absolutely fine to take your suggestion with a pinch of salt 😊.

1. UTI Nifty 50 Index Fund (Index Fund)

2. ICICI Prudential Bluechip Fund (Large Cap)

3. HDFC Large & Mid Cap Fund (Large & Mid Cap Fund)

4. ICICI Prudential Multi Asset Fund (Hybrid Fund)

5. Parag Parikh Flexi Cap Fund (Flexi Cap)

Considering the above MFs in a portfolio, which option would you think would be better and would optimize the portfolio in, from the below two options? Option 1 OR Option 2?

Options:

1. Remove the ICICI Prudential Bluechip Fund (Large Cap)

OR

2. Replace the HDFC Large & Mid Cap Fund with a pure Mid Cap Fund i.e. HDFC Mid-Cap Opportunities Fund.

Any 3rd option is also welcomed. 😊

If I were you, I\’d consider –

1) UTI Nifty 50 Index Fund (Index Fund)

2) ICICI Prudential Multi Asset Fund (Hybrid Fund)

3) Parag Parikh Flexi Cap Fund (Flexi Cap)

In fact, I\’d even think about not having Multi Asset Fund, and having a mid cap fund 🙂

Hi Karthik,

The modules have been very helpful for learning.

One question here – when you said \”I/d consider-\” ; do you mean that you would consider to continue holding the fund? OR do you mean that you would consider discontinuing the investment in those funds?

Ah, sorry, I\’m unable to get the full context.

Hi i want to start SIP please give me good funds allocation wise for 20+ years ( i.e. midcap percentage, small cap percentage etc )

Also can we consider GOLD ETF in SIP?

My age in 27

I\’m not really qualified to suggest funds, but if I were you, I\’d start with simple index funds.

1) The thought behind UTI Nifty 50 and ICICI Pru Blue chip was to keep one active and one passive fund in Large Cap category. At the same time, the amount I was planning to invest in Large Cap as a whole is basically distributed between these 2 funds.

At the same time, I completely understand the point after reading through the varsity.

So, what / which one do you suggest to keep in my portfolio considering I am planning for long term investing of 10+ years?

2) My thought behind keeping HDFC Large and Mid cap was to have some exposure to Mid Cap too, without having a pure Mid Cap fund.

For this one, what do you suggest? should I keep it or replace it with a pure Mid Cap fund?

Ultimately, how would rebalance and replan my portfolio for a monthly outflow of Rs 60000 in mutual funds after mentioning that the 3rd and 4th in the below list is fine as per your thoughts:

A. Current Portfolio – Rs 60000 per month

1. UTI Nifty 50 Index Fund (Index Fund) – 10000

2. ICICI Prudential Bluechip Fund (Large Cap) – 10000

3. HDFC Large & Mid Cap Fund (Large & Mid Cap Fund) – 12500

4. ICICI Prudential Multi Asset Fund (Hybrid Fund) – 12500

5. Parag Parikh Flexi Cap Fund (Flexi Cap) – 15000

B. New/Properly Diversified Portfolio – Rs 60000 per month

?????

—————————————–

Reply: Karthik Rangappa says: March 1, 2024 at 6:04 am

I’m not a professional advisor, so do take my advice with a pinch of salt.

1) UTI Nifty 50 and ICICI Pru Blue chip is an overlap, why would you need two of these?

2) Why do you need HDFC Large and Mid cap when you have large cap exposure already?

The rest seem ok. But do ensure you have a proper reason for holding these funds in your portfolio. I’ve shared my thoughts here, please do check this once – https://www.youtube.com/watch?v=6Zrl3ZeqqsE

————————————–

Amit Kumar says: March 1, 2024 at 1:40 am

I am investing Rs 60000 per month in SIP through Coin App spread across as below:

1. UTI Nifty 50 Index Fund (Index Fund) – 10000

2. ICICI Prudential Bluechip Fund (Large Cap) – 10000

3. HDFC Large & Mid Cap Fund (Large & Mid Cap Fund) – 12500

4. ICICI Prudential Multi Asset Fund (Hybrid Fund) – 12500

5. Parag Parikh Flexi Cap Fund (Flexi Cap) – 15000

Is it properly diversified? Is it okay to continue with the above combination?

I am a new investor. So, any suggestion would be highly appreciated.

I still feel there is a bit of optimization possible, best to speak to a good financial advisor (RIA) 🙂