13.1 – Debt jargons

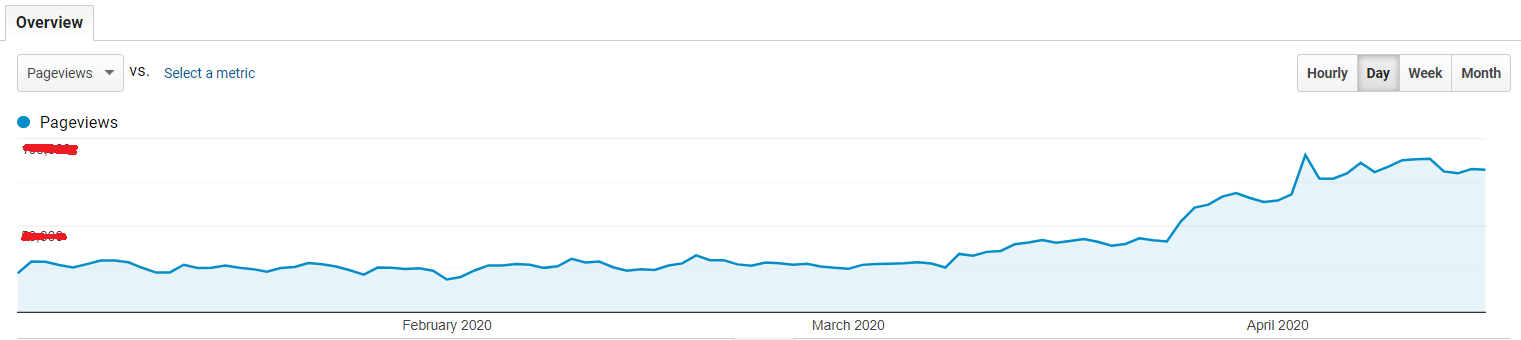

As we enter the 27th day of the nationwide lockdown, I hope you and your loved ones are staying home, staying safe. The number of COVID19 cases in India has crossed 17,000 with Maharashtra topping the charts with over 3,500 cases. I hope all of this ends soon and we can all get back to our normal lives, until then the only mantra is ‘social distancing’, I hope you are following this diligently.

I think many people across the country are using the lockdown opportunity to learn something new and educated themselves. The traffic on Varsity has shot up quite a bit, here is the pageview snapshot from Google Analytics –

Along with the pageview, the number of queries pouring in has also shot up. We spend several hours every day to answer your questions.

So if you find the new chapter update a bit slow, then please do understand its because of the increased load 🙂

In the previous chapter, we introduced a term called ‘Macaulay Duration’. If you recollect, Macaulay duration measure in years, the time required for the bondholder to recover the price paid for the bond by the bond’s cash flow. We did not discuss the math behind Macaulay duration because that’s outside the scope, but as I hinted in the previous chapter, the next module is on fixed income security (mini-series) where I’ll try and take this up in detail.

However, while we cruise along, there are few bond relationships that you need to know –

- The yield of a bond and the price of the bond are inversely proportional. If the price of the bond increases, the yield of the bond decreases and vice versa

- Interest rates and bond price are inversely proportional. If the interest rates increase, the bond price reduces and vice versa.

While we are at it, let me introduce another term – ‘ Modified Duration’, of the bond.

The modified duration (measured in years) of a bond is essentially the sensitivity of the bond’s price to the change in interest rate. So if a bond has a modified duration of 3.2 years, then –

- A 1% increase in interest rate decreases the bond’s price by 3.2%. A 1.5% increase in the interest rate, lower the bond’s price by 4.8%

- A 1% decrease in interest rate increases the bond’s price by 3.2%. A 1.5% decrease in bond price, increases the bond’s price by 4.8%

We can generalize this – Higher duration funds have a higher sensitivity to interest rate changes. So a 1% change in interest rate reduced the price of a longer duration fund in a greater magnitude compared to a low duration fund and vice versa.

In the context of a mutual debt fund, the modified duration is at an aggregate portfolio level. In the example above, say for a 1.5% increase in the interest rate, the debt fund’s NAV is likely to decrease by 4.8%. I hope you get the drift.

As a debt mutual fund investor, you are in the right spot if you are aware of the few points we have discussed so far. Along with these few points, as a bondholder or a debt mutual fund holder, you need to be aware that the mutual fund you are holding is susceptible to –

- Credit risk – The risk that the bond held by the debt fund can get downgraded

- Default risk – The risk that the bond issuer defaults on a coupon or principal repayment

Of course, now you also know that the bond price has an interest rate risk, but at this point, let us just assume the fund manager can hedge the interest rate risk.

Anyway, we will get back to the good old debt mutual funds. In this chapter, we will continue our discussion and take a few more debt (sub) categories. We will start the conversation with the low duration, money market, and short-duration funds.

13.2 – Low duration and Money Market

We looked at the ultra-short duration bond fund in the previous chapter. The defining criterion for the ultra-short duration fund was the Macaulay duration of the portfolio. As per SEBI’s classification, at the aggregate portfolio level, the Macaulay duration of the ultra short term duration fund has to vary between three to six months.

Next up is the low duration fund. The low duration fund is just like the ultra-short duration, only that the low duration fund, the Macaulay duration at the aggregate portfolio level varies between six to twelve months.

The credit risk of the low duration fund is similar to the ultra-short duration fund. Hence it is imperative for the investors to glance through the asset quality (paper quality) of the fund.

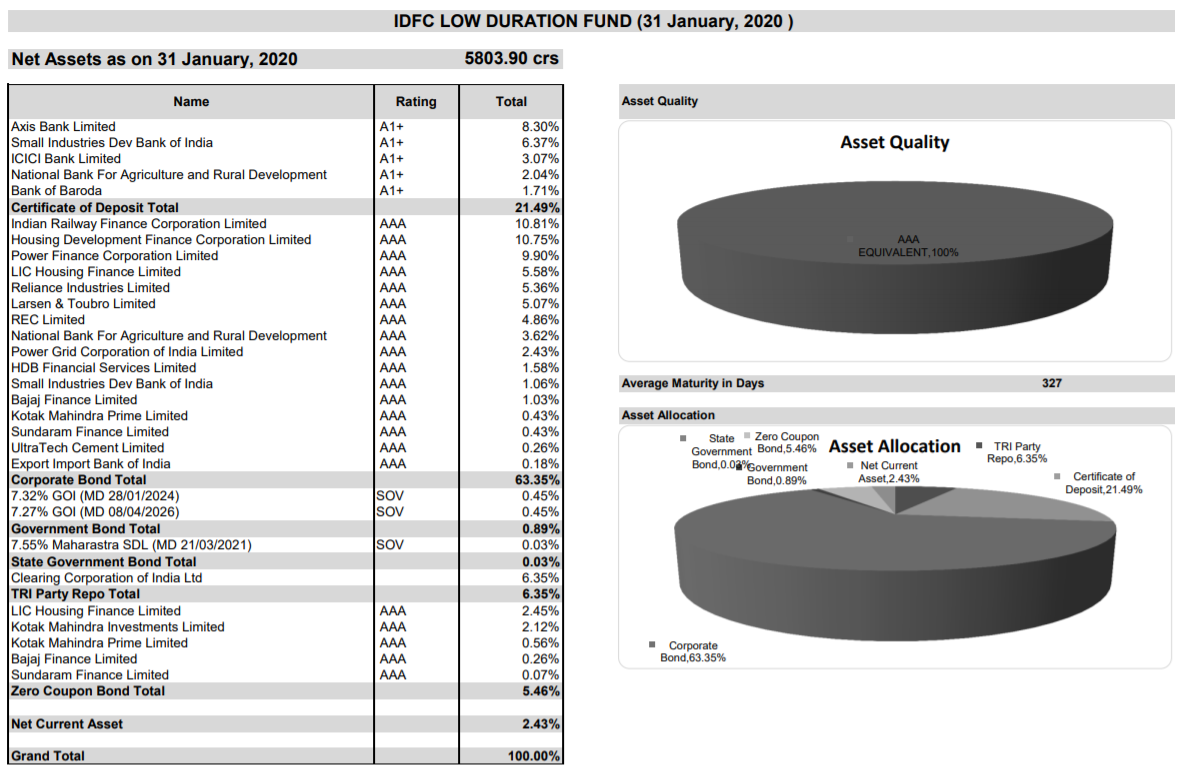

Have a look at the portfolio of the IDFC AMC’s low duration fund –

As you can see, IDFC has 100% of its portfolio invested across various AAA papers. However, just because the fund has only AAA papers, does not imply zero credit risk. Remember, we discussed the Vodafone case in the previous chapter.

While the credit risk exists, the interest rate risk for the low duration fund is low. Have a look at the modified duration of IDFC’s Low duration fund (published in the fund’s factsheet) –

The modified duration is 289 days. I can convert this to years by dividing this by 360 –

= 289/360

= 0.802

This means to say for every 1% increase or decrease in the interest rate, and the NAV is likely to decrease/increase by 0.802%, which as you can imagine is not much.

By the way, not all funds report modified duration in terms of the number of days. Modified duration is expressed in terms of years.

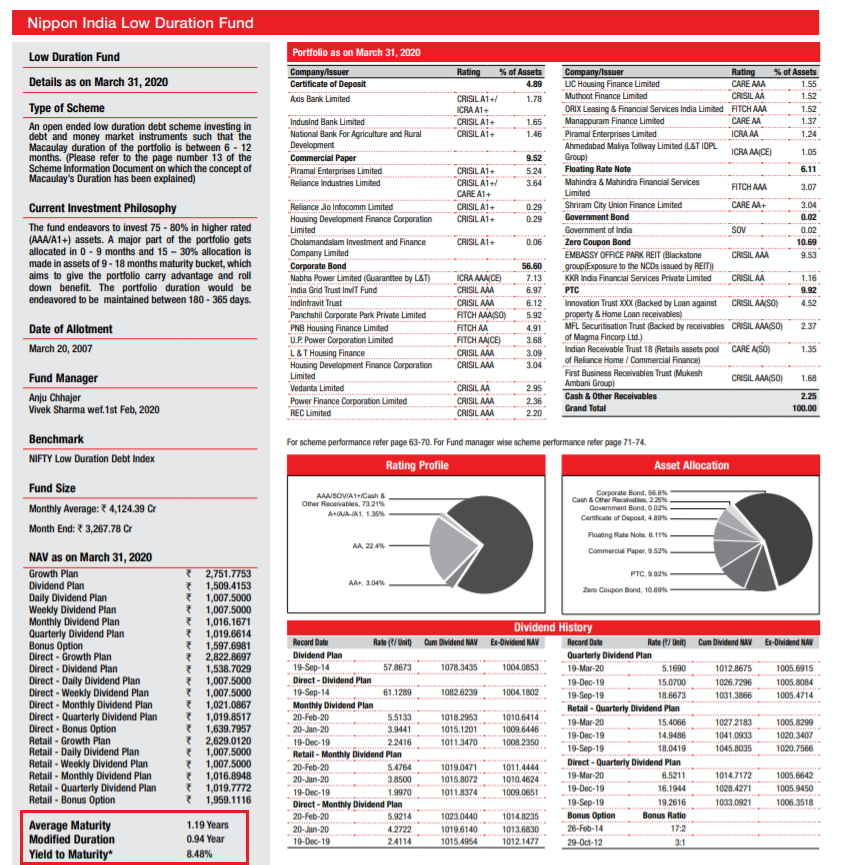

For example, the Nippon India low duration fund expresses the modified duration in years, which is 0.94 yrs.

So when the fund expresses in years, you need not divide by 360. Instead, you can use the number directly.

While we are at it, which of the two low duration funds do you think is risky in terms of modified duration?

IDFC’s Low duration Fund with a modified duration of 0.802 or Nippon India’s low duration fund with a modified duration of 0.94?

Here is a task for you – why do you think Nippon India’s low duration fund has a higher modified duration? Can you look into their portfolio (as of April 2020) and get your answer?

If you can answer these questions with ease, then we are headed on the right track 🙂

Lastly, who should look at investing in a low duration fund? This is best suited under situations where you want to park your money for a short duration and utilize the funds towards a specific goal at a later point.

Next up is the money market fund.

The money market fund is somewhat similar to the low duration fund. Here is SEBI’s classification of the money market fund –

As you can see, the maturity is capped to one year, similar to that of low duration fund; the only difference is in terms of the portfolio constituents.

A low duration fund can invest in both money market instruments and bonds but ensure at the aggregate portfolio level the duration is between 6-12 months. The money market fund, however, can invest only in money market instruments. The money market instruments usually consist –

- ‘Commercial Papers’ or CPs, issued by companies. CPs are unsecured

- ‘Certificate of Deposits’ or CDs. Banks issue CDs to entities depositing money

- T-Bills, issued by the Government, carries a sovereign guarantee.

So just to summarize, the fund manager of a low duration fund can invest in CPs, CDs, and perhaps even in a bond with two years maturity. However, a money market fund manager can only invest in CDs and CPs.

Let me ask you two question –

- What is the risk of investing in a money market fund?

- What do you think will be the modified duration of a money market fund? Will it be 1, greater than one or less than 1.

Do pause here, think about it, try to answer yourself.

Have a look at the factsheet of UTI’s Money market fund –

You will find the answers for both the questions here.

- The money market fund is exposed to credit risk. As you can see, 9.39% of the portfolio is invested in a single company’s CP or CD. Of course, the company’s paper enjoys a high rating, but I want you to remember the fact that these ratings can change. So yeah, credit risk exists in a money market fund.

- As you may have guessed, the modified duration will be under one year for a money market fund, which implies that the interest rate risk for these funds is low.

Investment philosophy in the money market fund is similar to the low duration fund. In fact, many investors often choose between low duration and the money market fund.

13.3 – Short Duration and Medium Duration funds

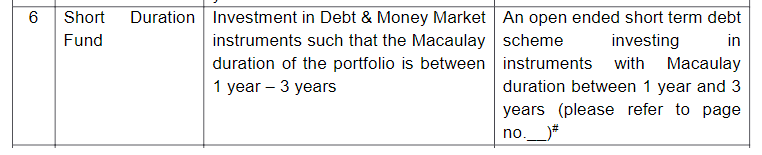

Next up is the short duration fund. Let’s start straight with SEBI’s definition –

The Macaulay’s duration of the short duration fund has to range between 1 and 3 years. After reading the SEBI definition, what is the first thing that comes to your mind?

Well, I hope you think about it from a risk perspective. With an increase in the duration, the modified duration also increases – which means the risk associated with changes in interest rate is higher with a short duration fund (and the medium duration fund). Do note; this was not so much of a concern with the low duration and money market fund (or even the ultra-short duration fund).

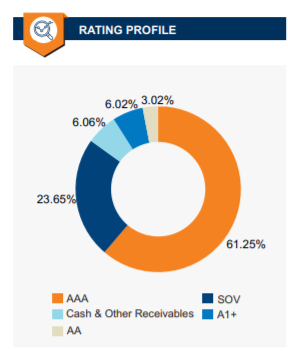

Of course, credit risk continues for short duration fund as well. Have a look at the rating profile of the Mirae Asset Short Term Fund –

As you can see, the fund has a mix of AAA, AA and A1+ debt papers in the portfolio. For the same fund, look at the modified duration –

The modified duration is 2.67 years, which means, for every 1% increase in the interest rate, the fund will drop 2.67% in its NAV. The risk associated with the short-term fund is higher compared to all the other funds we have discussed so far.

Also, do notice the Macaulay duration of the fund, it is below 3, as SEBI has defined.

With a considerable amount of risk, you need to be clear with your investment objective in these funds. Invest in these funds only if you have an investment horizon of at least three years in perspective. Of course, with the increased risk, the return expectation is also higher. I think it is prudent to expect about 7 (ish) % return on these short-duration funds.

I think by now, you must have got the hang of how to understand the basics of debt fund.

Here is the SEBI’s classification of a Medium duration fund –

As a task, why don’t you do look upon a fact sheet belonging to a medium duration fund and answer these questions –

- How is the portfolio composition? What do they hold in the portfolio? How are the papers rated?

- What do you this is the credit risk here?

- What is the Macaulay duration? Does it match SEBI’s mandate?

- What is the modified duration? What do you think is the risk associated with the interest rate change?

- What is your investment horizon if you were to invest in these funds?

I’m reasonably sure that you can carry out the above task with ease. If you find any difficulty of any sort, then please do leave a query at the end of this chapter and I’ll be more than happy to help you with it.

In the next chapter, we will take up the Credit risk, dynamic bonds and the gilts. However, there is one last thing we need to discuss before we end this chapter.

13.4 – The Franklin India debt fund saga

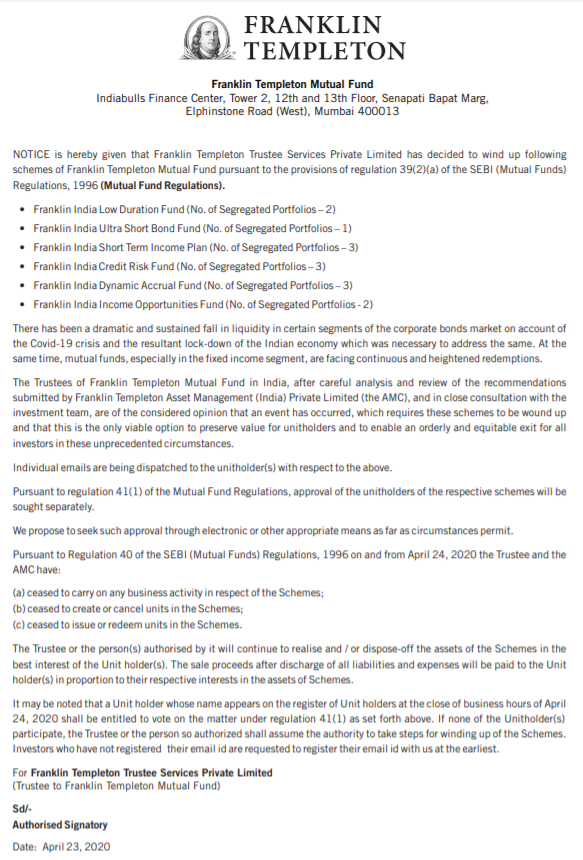

On 23rd April 2020, Franklin Templeton (India) AMC made an announcement that shook the entire debt fund world.

In an unprecedented move, Franklin has decided to close six of its debt funds, which includes their low duration fund and ultra-short duration fund. The AUM across these six funds is roughly Rs.27,000 Crores.

The reason they cite is – because of the current economic situation, there is a surge in redemption, leading to a liquidity crunch within the AMC.

To put this in perspective, Franklin witnessed a surge in redemption to the extent of over Rs.9000 Crores in March 2020, which as you can imagine is one-third of the AUM across these funds.

Unfortunately, the secondary bond market in India is not liquid enough. It is not easy for the fund managers to quickly liquidate the bonds from their portfolio. For this reason, most of the bonds held to maturity. Of course, the AMC plans to have enough cash to meet daily redemptions, they do this in several ways, including a technique called laddering, wherein they have a blend of papers maturing in different timelines. The liquidity arrangements work when business functions as usual. But as we clearly understand now, things go helter-skelter when tables turn.

None of the AMCs would be (at least up until now) prepared for such a steep surge in redemption.

Hence to ease the situation, Franklin has decided to close down the schemes completely and lockdown the funds entirely, which implies that if you are an investor in these funds, then you cannot place a redemption request.

Please note, the AMC is not winding down the scheme because of the credit or interest rate risk. Folks at Franklin are outstanding in the debt fund game, and they have a vast experience in this segment, but unfortunately, they are now threading on a different territory.

Therefore, dear readers, when investing in debt funds, along with the credit and interest rate risk, factor in a new risk – liquidity risk.

But of course, how do you quantify and apply liquidity risk in a real-life scenario? Well, I don’t know that just yet. However, does this mean that you should completely stay away from debt funds?

No, not at all.

Debt funds play an essential role in asset allocation, and it should play its part in your portfolio. The COVID19 situation if not for anything, has yet again highlighted the importance of asset allocation.

More on this as we cruise through this module!

Stay home, stay safe!

Key takeaways from this chapter

- Bond yields and bond prices are inversely proportional

- Interest rate and bond prices are inversely proportional

- Modified duration helps us understand the change in NAV of the fund (in the context of debt fund) for every 1% change in interest rate

- Low duration fund has credit risk, but low-interest rate risk

- Money market fund has credit risk, but low interest rate risk

- Short and medium duration fund has both credit and interest rate risk

- Debt investors have to factor in liquidity risk along with credit and interest rate risk

Guess there is a copy mistake here correct me if I am wrong \”A 1.5% decrease in bond price, increases the bond’s price by 4.8%\”

The 1.5% decrease is in interest not in bond price

Let me check this, thanks for pointing out.

Hi, here you discussed that Franklin closed its two debt fund schemes does that mean people will not get the money forever (meaning money is lost) or whether it will allow for redemption after this uncertainty of covid

If investments were in instruments which are a write off, then its a dead investment as there is nothing much to recover and pay the investors. Thats the reason checking the portfolio of a debt fund is important.

This was a very heavy chapter. Had to go through it twice or thrice. Still getting my head around it. Insightful though!

Glad you found it useful, Yash! Happy learning 🙂

Hey Karthik,

Can you pls help me understand the difference between CP and bond?? (Don\’t they mean the same)

Both represent borrowing obligation. CP = tenure is 1 year and bonds can be more than year.

Hello Sir,

I don\’t know it\’s me understanding it wrong or it is a mistake. In 13.1 in Modified Duration\’s second point it is written (A 1.5% decrease in bond price, increases the bond’s price by 4.8%). So, isn\’t there decrease in interest rate will come in the first sentence..?

Sorry, I\’m unable to understand this. Can you please give more context?

Hey Karthik!. First of all i have to say you are AWESOME!. You make everything easier for people like me who are just starting to enter this new world. You are indeed a great teacher. I have a simple question. Does the yield calculated take into account inflation i mean wouldn\’t inflation affect the purchasing power of my returns ? Also one more thing could you give us some resources that everyone here can use to dig deeper into mutual funds and stocks and stuff. There are a lot of junk out there so i would love if you could point to us out some great reads/books you learned a lot from (like gradually from beginner to more advanced level) if you don\’t mind.

Thanks for the kind words, means a lot 🙂

No yield calculation does not factor inflation. Thats a separate math that you will have to do. As far as the resources, can you tell me what exactly you are looking for beyond whats here in Varsity. It will help me point you to a worthy resource and also help me understand what else we could cover to make our content comprehensive.

It is mentioned that money market instruments are CP, CD and T bill. But why does it say that money market fund managers can only invest in CP and CD.

Basically money market fund managers invest in short term bonds, which is basically CPs and T-bills.

I saw the SBI MAGNUM MEDIUM DURATION FUND and its portfolio consists of investments in two different things one is CP and the rset is all in non convertible debentures. I am not getting how to see for the credit risk. Kindly explain me the answer to this question

Credit risk is basically assessment of the repayment capacity of borrower. For example, if its a T bill of G Sec, I know the borrower is Govt of India, therefore the credit risk is very little to nil. However, if the borrower is a corporate with weak balance sheet, then I know the borrower will have trouble repaying and hence the credit risk is high.

You basically have to check the repayment ability of the borrower to get a sense of credit risk.

Here is a task for you – why do you think Nippon India’s low duration fund has a higher modified duration? Can you look into their portfolio (as of April 2020) and get your answer?

Is it because Nippon has few AA and A bonds which adds to interest rate risk , thus having higher modified duration , where IDFC has 100% AAA bonds thus have low interest risk thus low modified duration.

Am I correct?

Yes, also do check other\’s reply.

Hello sir,

I want to know your thoughts on my answer for the question asked in here:

Here is a task for you – why do you think Nippon India’s low duration fund has a higher modified duration? Can you look into their portfolio (as of April 2020) and get your answer?

I think that the longer the longer a bond takes to mature, the more its price will change when interest rates go up or down. This is because there\’s more time for interest rate changes to impact the overall value of the bond\’s future payments.

So is this reasoning correct or am i missing something.

Thank you for this knowledge that you are providing. 🙂

Thats right Ritwik. In the comments, do check the previous answers as well 🙂

Hello Karthik

In the screenshot of IDFC low duration fund, the last item is Zero coupon bond which is 5.46%. Does this mean they have invested in bonds having 0% interest. If so then what is the benifit of that? Could you please give some input

Its a zero coupon bond, meaning there is no interest, but the bond itself is purchased at a discount to par and you get par value upon maturity.

Hello Karthik,

You asked a question regarding why Nippon has a higher Modified duration compared to IDFC. Why is that so? is it because Nippon invests more percentage of its assets in corporate bonds in comparison to IDFC? Does that mean it carries more risk? Since Modified Duration is a measure of volatility in NAV values based on interest rate changes, I believe Nippon has more volatility and hence higher Modified duration.

IS this logical?

Yup, its linked to the risk 🙂

Q:Here is a task for you – why do you think Nippon India’s low duration fund has a higher modified duration?

My answer: Is it because of the low percentage of government bonds and higher percentage of zero coupon bonds (which results in less cash flow and increased risk ) in Nippon\’s case ?

Yeah, essentially higher risk in the category.

Hello sir,

I am unsure how to assess the riskiness of IDFC\’s low-duration fund and Nippon India\’s low-duration fund. Could you kindly elaborate on this topic? Thank you!

Why this these new features of this page like junior, certified tests, and more is available in the app

We will be updating the app sometime soon, Kumar.

Hi Karthik can you please post the answers with explanations as well. thank you

Can you share the question?

Sir I\’m confused between Bond and Equity markets co-relation

Pls help getting some clarity

As the interest rates go up, cost of borrowing goes up and there will be slowdown in capex which make equity markets unattractive

Agreed

But at the same time as the interest rate goes up, the price of the bonds do decrease right…

so the investors in bond market can get out of the bond market and invest in equity.

And when the interest rates decrease, the price of bond go up

and investors can get out of equity market and invest in bond market

But why would they book loss in bond and invest in equity which is looking weak?

The yield of a bond and the price of the bond are inversely proportional. If the price of the bond increases, the yield of the bond decreases and vice versa.

Sir can you tell the reason??

Sir we generally notice that when interest rates go up, equity market goes down. Similarly when FED increases interest rates, US equity market goes down and at same time Indian markets go down aswell. Why does that happen?? American Investors can invest in Indian equity market but we see the opposite of it. Why

Raising interest rates means that the cost of borrowing for corporate is higher, which means there could be a slow down in capex spend, hence the slow down in growth. Likewise in the US markets.

Dear Sir,

First of all kindly accept my congratulations and thanks for your initiative in the personal finance space. This is indeed a great and valuable source of information and you are explaining each concepts so well that anyone can understand.

You mentioned that \”Interest rate and bond value are inversely propotional to each other\”. Does this mean, if the bond (A) is trading at INR 1000, with an interest rate of 9% and other bond (B) trades at INR 1000 with an interest rate of 10%, then the price of bond (A) with 9% interest rate will go down in the market, as people start preferring Bond (B) over bond (A). Is my understanding correct?

Thank you!

Sort of yes, but all bonds react similarly to rate hike in bonds.

Sir I went through the fact sheet of Aditya Birla Sun life medium term plan and their its mention that they are allocating 0-10% to REITS & inviTS, so how does change in interest rate affects REITS

Not much directly, Anwit. But changes in interest does effect the over all economy and it will have an impact on REITS as well.

Hello Karthik,

Excellent work.

A 1% decrease in interest rate increases the bond’s price by 3.2%. A 1.5% decrease in bond price, increases the bond’s price by 4.8%.

should be replaced by following (1.5% decrease in bond price should be changed to 1.5% decrease in interest rate)

A 1% decrease in interest rate increases the bond’s price by 3.2%. A 1.5% decrease in interest rate, increases the bond’s price by 4.8%.

Saurab, thanks for suggesting it. Let me check this.

Hi Karthik,

When you refer to interest rate in the articles, are you talking about the YTM of the respective mutual funds? or the cagr of the fund?

Its the interest rate in the economy that I\’m referring to, Aditya. The monetary policy set by the Reserve Bank of India.

1)Isn\’t COD issued by Bank\’s and for Corporates it is Commercial Paper?

Guide for the same.

Thanks in Advance!

As far as I know, COD can be issued by any corporate entity.

Do confirm and correct :-

1)Bonds can be issued by both government and corporate\’s who\’s repayment term is generally more than a year.

2)The status Shares have in the Equity Market is same as Bonds in Debt market.

3)Macaulay\’s Duration is applicable for all the debt instruments and not specifically restricted to bonds.It is the time required to recover our principal amount.

4) Modified Duration is the interest rate risk which the debt instrument faces and is specifically high for bonds as the duration of maturity is longer.

5)Nippon has less bond investment but high Cr risk due to ratings then how does it affects the Modified duration? Shouldn\’t it affect the Macaulay\’s duration and not modified duration.

Do guide for the same

Thanks In Advance.

1) Yes, it can be under a year as well and these are called Certificate of deposits (if issued by a corporate) and treasury bills (if issued by the Govt)

2) Not sure if I understand this correctly, can you please elaborate?

3) Thats right

4) Thats right

5) YOu need to check the latest portfolio for this and conclude based on that.

Need some pointers here. While going through the coin app, most of the liquid or overnight debt funds have 4-5% CAGR, Is it good to invest in these debt funds, because nowadays I can see FD offering ~7% returns? Just correct me, if anything is wrong.

I\’d go for the FDs if the rates are better. But do check with your CA for taxation once.

Here from all the examples of modified duration, it looks like interest rates always go up and hence NAV will always fall in accordance to the modified duration of fund.

but is it always this case? or do interest rates go down as well, making NAV go higher??

Not really, the way in which interest rates move depend on the central bank, which further depends on the state of economy in the country.

Why some funds have greater modified duration than the other funds of the same category?

Depends on the portfolio, right?

Thank you Sir 🙂 This makes me so eager to continue reading on varsity

Happy learning, Chetan 🙂

Sir in the chapter you asked…..

1.In the chapter section 13.2 Below the snapshot of Nippon india low duration fund \”here is a task for you…..\” that question

2. What is the significance of Macauly years?

Ah got it, its just that one of the portfolio holdings has a longer maturity, hence the modified duration has increased. Modified duration significance, I have explained in the previous chapter.

I\’m Sorry sir but i could not figure out why is Nippon\’s Fund having higher Macauly Years so would you mind answering the same , but even before that i\’d like to ask you What exactly does Macauly Years Signify?

Can you specify which fund, Chetan?

I invested in short term bond funds about 6 months back with an expectation that I will utilize it between 24-36 months from investment date. I expect around 7% annualized. Given the current conditions that interest rates will start creeping up is this still the best place to leave the funds or should they be moved to low duration funds?

It is best to stick to short-duration funds, these are the least affected in the rate hike cycle.

\”the interest rate risk for the low duration fund is low.\” Why?

Because it\’s a short-term bond and interest rates are not expected to change in a short duration.

Hi, Karthik!

Thanks for the structured modules.

I am a bit confused about Macaulay\’s duration and risks. According to Macaulay\’s duration, one is entitled to receive his funds back by the mandated duration, but suppose during the invested period one of the company\’s ratings downgraded and is in the portfolio, which means the NAV of the fund will automatically fall, what if the duration is about to end? Will investors of the fund bear the loss?

Macaulay\’s duration is averaged out. Yes, if a bond is written off, then that bond will have an impact on the NAV, for this reason, AMCs separate out the investment and create a segregated portfolio to hold just the paper. I guess I\’ve discussed this in the Vodafone paper and Franklin case.

Hi Karthik, why this module is named as \’ Personal Finance (Part 1)\’ ? I couldn\’t find Part 2. Let me know if any Part 2 coming. This chapter is already very fascinating and would really dive deep if any Part 2 is planned.

TIA.

I\’m yet to start work on Part 2, working on Financial modelling for now 🙂

Hi Karthik, enjoying these articles on mutual funds, I looked at the factsheet of ICICI Prudential Medium tern debt scheme. As per that, Macaulay duration is 2.60 years but SEBI has classified that it should be between 3-4 years for medium term debt fund. What is it that I am missing here?

Pranjal, I think on the date of reporting the ratio would have slipped (I\’m not sure as well, taking a guess) , but these funds ensure it is between the stipulated mark for the majority of the time.

Hey Pranjal, SEBI defined Macaulay Duration range for Medium Duration Funds is between 3-4 years. The current Macaulay Duration of ICICI Prudential Medium Term Bond Fund is 3.25 years according to the November factsheet.

ques. you asked why nippon low duration fund had high modified duration as compare to idfc low d. fund

ans-if i am right then it is bcz ….of asset allocation rating

Yup, also please see some of the comments above.

Sir

I am a bit confused about the relationship between interest rates and returns.

As explained in this module, longer-duration funds are negatively affected when interest rates go up, but then why is it different for liquid and overnight funds?

I was checking historic returns and liquid/overnight funds had bigger returns in 2018/19 than in 20/21

So a bit confused.

Think about it, you have a long term fund that pays 6%, but the interest rates go up by 6.75% what would make the 6% bond attractive? Hence it has a negative impact. Liquidfunds/overnight funds are all similar, just like your savings account. Nothing more.

Thanks Karthik. I think the reason why Nippon had higher modified duration than IDFC is because the average maturity date for Nippon is higher. My understanding is that when the maturity date increases, it will automatically increase the macaulay duration (keeping other factors such as interest rates constant). When macaulay duration increases, it will lead to a higher modified duration. Sorry if I\’m not correct here, I looked at the portfolio of Nippon for April 2020, I couldn\’t really find anything that would suggest the reason for a higher modified duration.

Lastly, thank you so much for the content put up on Varsity. This is exactly what I have been looking for. Varsity has made learning so much more insightful because of the way you have written these articles. It\’s just great! Thanks for everything you do. Love to Zerodha!

Thanks for the kind and encouraging words, Pradeep.

You are right about the modified duration bit. Did you also check the weightage assigned to each paper? Sometimes it could be just 1 debt instrument with a heavy weight that could skew the duration.

Why Nippon Low Duration fund has higher modified duration? I\’m having some trouble understanding it. I went to AMFI website and took the April 2020 portfolio disclosure report. In that I see a lot of the underlying bonds are illquid/non traded securities. Does that have something to do with it

Not sure if liquidity has anything to do with that. Please look for the portfolio details along with the weights of the papers.

Hi KR,

I had a question regarding medium term debt fund. As per your article, I analyzed \” Nippon India Strategic Debt Fund (Number of Segregated Portfolios – 2)\”. The link to the portfolio as on 31st July, 2021 can be found https://mf.nipponindiaim.com/InvestorServices/Factsheets/Fundamentals-August-2021.pdf on page number 31.

I had couple of questions here:

1) The fund states that it is a medium term debt fund which means the Macaulay\’s duration should be between 3 to 4 years. However, the portfolio says that it is 2.51 years. Can you explain what is happening here? Am I missing something?

2) What does (Number of Segregated Portfolios – 2) mean here? It seems Yes Bank and Vi Limited has been segregated from the portfolio because of ratings downgrade. I see the fund\’s NAV has also gone down because of the same. Could you throw some additional light on this?

1) 2.51 indicates that there is a short term shift in the maturity of the bond (perhaps due to the segregated portfolio). Please do check the most recent funds update or wait for the fund to update

2) Yes, it means that the fund has carved out the bad apples from the portfolio and treated it as a segregated portfolio.

Hi, Karthik. I understood debt funds should not be looked at as an investment tool for higher returns. However, is it safe to assume that they will beat inflation? I looked at a couple of them which are composed of Goverment and AAA securities and the returns hover at 9-10%. Thanks

I think the returns have dropped significantly Siddhath. I quite doubt its in the 9-10% range. Please double check the same.

Unable to understand the interest rate of a debt mutual fund. When you say NAV will decrease with increase in interest rate, whose interest rate are we talking about?

Talking about the interest rate prevailing in the economy, Vamshi.

\”Please note, the AMC is not winding down the scheme because of the credit or interest rate risk.\” – Looks like SEBI found several irregularities in the debt fund including credit quality issues. I think this should reflect in the chapter for better accuracy. BTW, great module, Karthik!

Yeah, debt funds are always worrying for some reason.

In the beginning, it is mentioned, that \”The modified duration (measured in years) of a bond is essentially the sensitivity of the bond’s price to the change in interest rate.\”

However, while reading up on my own, I came across the statement \”Unlike Macaulay duration, modified duration is not measured in years. Modified duration measures the expected change in a bond\’s price to a 1% change in interest rates.\”

Clarity on this discrepancy would be highly appreciated! ~ Thanks!

Sorry, dint get the discripency. Not sure if I\’m missing anything.

Why Bharatbond is not taken for pledge by Zerodha even though it\’s allowed by the exchange. ?

It should be possible, let me check.

Its possible to pledged Bharathbond, no issues with it.

Hello Karthik,

Another small typo. \”threading on a different territory\”. you probably meant \”treading\”.

Once again, I am just suggesting because Varsity is an excellent resource and I want it to be perfect 🙂

Thanks, Varun. Please keep them coming 🙂

Hi Karthik,

I saw this response from you for someone query in comment section in same article.

If I interest rates drops then bond price should increase right ?

“ If the interest rate drops, then the price can drop to 95.5, and therefore the yield increases to 4.5%. ”

Ah, let me recheck this.

Hi sir,

In section 13.2-You asked – why do you think Nippon India’s low duration fund has a higher modified duration?

I didn\’t get it. I think , assuming statement – Interest rates & Bond prices are inversely proportional & that IDFC Low duration fund has higher (63%) of bonds in portfolio than Nippon\’s low duration fund (56%).So interest rate change will affect IDFC Portfolio most & it will become more risky. So IDFC has to be Higher \’Modified duration\’ than Nippon.

Plz explain this.Thanks.

Yeh, hence the higher modified duration.

why do you think Nippon India’s low duration fund has a higher modified duration?

@Karthik, could you please let us know the answer to the above question ?

I think a few ppl have already answered that in the query section. I\’d request you to please check the comments.

Can you explain the difference between bond yield and interest rates

Hmm, bond yield is the amount of money you will make if you were to hold the bond to its maturity. Interest rate is the money you pay against your borrowings.

As a beginner I have no idea what bond yield is. So I am not sure why that part was relevant to the whole article.

Hmm, its good to know for a well-rounded understanding, right?

Hi,

The simplicity of your concepts is amazing. Really want to understand bond mathematics from varsity. I hope you put up a module on fixed income soon. Thank you.

Regards,

Akshay Jain

Hopefully, one of these days, not anytime soon though 🙂

Sr as you have mentioned Macaulay duration for low duration fund is six to twelve months,then how is it possible in case Nippon india duration fund where it\’s average maturity is 1.19 years

Ah, you need to check the portfolio and see what they are holding to understand this, Aman.

I did not understand below points:

1) The yield of a bond and the price of the bond are inversely proportional. If the price of the bond increases, the yield of the bond decreases and vice versa

2) Interest rates and bond price are inversely proportional. If the interest rates increase, the bond price reduces and vice versa.

1) That\’s right, both yield and price of the bonds move in opposite directions

2) This is right again.

To understand this, you will have to look at the bond mathematics, I thought it would be outside the scope of this content, hence did not include it.

Sir how interest rates increase or decrease

If it even decrease the bond price will increase

If bond price increase they can sell that at higher price in the bond market

The interest rate increases or decreases based on multiple macro factors – inflation, trade deficit, GDP etc. Yes, if the bond price increase you can sell at a higher price, but the overall yield comes down.

Great resource this is. Thank you very much.

Just wanted to point a small typo.

In the second point explaining modified duration time:

\”1.5% decrease in bond price, increases the bond’s price by 4.8%\”

It should be \”decrease in interest rate*, increases the…\”

Thanks again for great resource

Ah, thanks Vinay, will fix this.

Hi karthik,

Thankyou for this module, I have a question here as to convert modified duration from days to years why 360 days are taken into account and not 365.

This depends on the day count convention. Some prefer 30 months and 360 days, while few take 31 days month and 365 days a year.

Hi Karthik,

Thanks for educating us on debt instruments.

Need some clarification here. Which debt instrument would you suggest to park emergency/opportunity fund ? I never know when I would be needing this money, might be within a year or 15 years from now. If this instrument helps achieve near inflation returns that would be great.

Do let us know your thoughts 🙂

Probably an arbitrage fund?

why do you think Nippon India’s low duration fund has a higher modified duration ?

because average maturity of IDFC AMC’s low duration fund is 10 months but average maturity of Nippon fund id 1.19 years .

please correct me if i am wrong 🙂

Shanu, perhaps they have higher maturity papers. That is the only reason.

Thank you for this chapter,

I had gone through Kotak Medium term Debt Fund ( Link – https://www.kotakmf.com/funds/debt-funds/Kotak-Medium-Term-Fund/Reg-%20G ),

It\’s a decent debt fund with moderate risk. However 2 things aren\’t clear for me

1) Their portfolio allocation shows that their Net Current Assets is -2.76%, what does that precisely mean ? I have seen current assets in Balance sheet of companies, but I hope the current asset in this fund is something else.

2) what is Yield till Maturity (YTM)

Great articles, Karthik. Have learnt a ton from you, can\’t thank you enough for that! 🙂

You said \”The modified duration (measured in years) of a bond is essentially the sensitivity of the bond’s price to the change in interest rate.\”

What exactly is the interest rate here? Is it the current repo rate? I also see something called MCLR on RBI\’s website. This question might sound a bit silly, but since am new to finance I\’m confused.

Sriram, for all practical purposes, you can keep the repo rate as the proxy for the interest rate.

Why it is so that nippon india low duration mutual fund has higher modified duration compared to idfc amc low duration fund?

Why it is so that nipppon india low duration mutual fund has higher modified duration compared to idfc low duration fund??

Perhaps because of the quality of the paper they hold?

Hi Karthik,

Tier 1 Scheme G of National Pension Scheme, which invests in government securities, is recommended by Pension Fund Houses to those who have an appetite for “low risk” and want to play it “safe”. But the average modified duration of this scheme is about 8 years. I know there is no Credit risk, however, the mere fluctuations in its returns with a 1% change in interest rate will be too huge.

Then why is it marketed as so “safe”? Should I invest my savings in this scheme G (modified duration 8 years ) or should I choose Scheme C (corporate debt scheme with modified duration of 4.5 years).

P.S. I still have 30 years to go for my retirement and 50% i intend to invest Scheme E (Equity products).

Sharan, interest rate risk is common across all bonds. The safe part is keeping credit risk in perspective.

yours answer for this question ?

IDFC’s Low duration Fund with a modified duration of 0.802 or Nippon India’s low duration fund with a modified duration of 0.94?

Nippon is risky, since it has higher modified duration and high interest rate .

Thats right, Karthick.

How to understand interest rate risk for G-Secs and co-relate modified duration ? Say, investing in 7.16% 2050 G-secs. Typically, G-Secs do not carry credit risk (a rarity) but there is always an interest rate risk ..

Thats right, Tushar. The duration of the bond gives you a perspective of the risk. I\’ve explained this in this (or the previous) chapter.

Thanks Sir.

Hi Sir,

Great Job at publishing so much knowledgable content for dummies like me.

I have read all your material from module 1 and have absolutely loved it.(Except derivates till now, plan to do it next)I know its not enough but a big thank you again.

\”Investment philosophy in the money market fund is similar to the low duration fund. In fact, many investors often choose between low duration and the money market fund.\”

I found the above statement incomplete. Kindly inform me what is preferred between low duration and money market fund?

Thanks Piyush. I\’m glad you liked the content!

Low duration funds and money market fund invest in similar instruments, hence I said the philosophies are similar.

Thanks Karthik. I\’ll check that. Just one thing, when we say the \”yield of the bond\”. We are talking about the returns the bond is generating right?

Yes, thats right. The overall return.

Hi Karthik,

Thank you so much for such wonderful content. Have learned a lot from Varsity and still continuing to do so.

I could not understand this part very clearly. Can you please help and explain a bit more about this?

\”The yield of a bond and the price of the bond are inversely proportional. If the price of the bond increases, the yield of the bond decreases and vice versa

Interest rates and bond price are inversely proportional. If the interest rates increase, the bond price reduces and vice versa.\”

Thanks. 🙂

Chinmay, these are inherent bond properties, very integral to the bond math. I thought the explanation would be a bit too much given the context we are discussing this. Hence posted only the summary. However, if you are interested, I think Investopedia has done a nice job at explaining this. Request you to kindly refer to that.

Hello Karthik,

This is a follow up of a previous question about where to find Macaulay\’s duration if that isn\’t available in the fund factsheet. (the reply button on comment doesn\’t seem to work 🙂 )

I looked up the same on morningstar and valueresearch, as you had said. Couldn\’t find it on either.

In such case, do we assume that the given fund will have Macaulay\’s duration in the range it should be. For example, low duration funds to have it between 6-12m; or it may wary?

Thanks for the reply 🙂

That\’s a fair enough estimate 🙂

One more please

Why bond price decrease with the increase in interest rate and vice versa?

Isn\’t that should be the case that more people will be willing to invest in a fund which is offering more rate of interest so bond price should go up or vice versa.

Thats just that nature of the instrument. You can derive this mathematically as well, but gets a little complicated.

Hey Karthik

Firstly i would say i love the content at varsity, thanks for that.

I have a question that why interest rate are changing in debt fund isn\’t this should remains constant for a bond because that had been promised between issuer and the investor, is it the case that fund manager do not invest in only CPs?

Interest rate is dependent on the economy. The coupon rate is fixed and that does not change.

Hello Karthik,

Some one pagers/fact sheets of funds, such as IDFC and SBI, do not mention the Macaulay\’s duration in quantitative data. How do we find Macaulay\’s duration in such cases?

Can you look for it in morningstar or valueresearch?

Hey Kartik I just had a doubt. when you say \”rise in interest rates results in fall in bond prices\” what is the benchmark for the interest rates here? the repo rate? or the sbi savings rate?

The repo rates are the usual reference.

I am finding it a little difficult to understand why the modified duration increases as the macaulay duration of the fund increases (the fundamental reason). Furthermore, I just wish to get a confirmation on my understanding of the inverse relation between bond prices and interest rates. As interest rates increase, FDs and SAs become more attractive which leads to selling of the bonds in the secondary markets leading to a fall in price. Am I right here?

Thank You for such a great learning opportunity, it let me make good use of my extra time during lockdown.

Do check this Rushriraj – https://www.investopedia.com/ask/answers/why-interest-rates-have-inverse-relationship-bond-prices/

There is some error with the link provided

Which link, Dheeraj?

As the rate of interest of a bond increases, the price of the bond should also increase right?

They have an inverse relationship Dheeraj. Check this – https://www.investopedia.com/ask/answers/why-interest-rates-have-inverse-relationship-bond-price

\’While we are at it, which of the two low duration funds do you think is risky in terms of modified duration?

IDFC’s Low duration Fund with a modified duration of 0.802 or Nippon India’s low duration fund with a modified duration of 0.94?

Here is a task for you – why do you think Nippon India’s low duration fund has a higher modified duration? Can you look into their portfolio (as of April 2020) and get your answer?\’

Hi Karthik,

At the risk of sounding stupid, I wanted to ask – my understanding as per the learning above, that higher the modified duration, higher the sensitivity to rate in interest. So Nippon fund is riskier in terms of modified duration ? (basis march 2020 report) Is that correct? Further you have mentioned to check April 2020 portfolio report, which shows modified duration .82 years, Is this because AA+ % in rating profile increased ? Pls can you explain

Thanks

That\’s absolutely correct, Gautam 🙂

Hi Karthik,

I did not quite understand the below statement from article:

\”Interest rates and bond price are inversely proportional. If the interest rates increase, the bond price reduces and vice versa.\”

Why is this happening exactly? Is it the because of natural market movement?

Like if the interest(repo) rate goes down, then all bonds issued so far were at higher rate than present time so naturally their demand goes up which drives prices? Am I right in this?

Here is a decent explanation for the same – https://www.investopedia.com/ask/answers/why-interest-rates-have-inverse-relationship-bond-prices/

Hi

Great job but i am not getting the confidence in bond market, as the continuity is missing , State wise debt, countries debt, Import export and trade deficit, Debt problem and currency fluctuation, mainly it\’s all together a vast topic several things like RBI\’s e-kuber facility, recently 2029 10 yr bond crashed while 2030 10 yr bond remains there, i analysed and get to know that due to the10 yr bond shift(when it generally happen) and a lot more is missing…

The main problem of retail investors is data and where to get it –

1. MSCI index change and foreign inflow

2. forex Hedging

3. Mutual fund inflow in the quater end

Can you give us site links so that we can get the data ..In bloomberg terminal everything is available ( i Came to know that in bloom berg you can watch the oil tanker position in the sea, from that you can predict the recent oil market crash), From where they get data how mutual fund industry analyse and get data and many more can you bring some light to this…

Thanks

AK

Yeah, Bloomberg is good, but its quite expensive. You can also try Cogencis – http://www.cogencis.com/

A 1.5% increase in bond price, lower the bond’s price by 4.8%..

Kartik sir, how is this possible..?

I think correct line should be \” A 1.5% increase in Intrest rate, lower the bond’s price by 4.8%.\”

That\’s right will make the correction, thanks for pointing 🙂

What the gap between present bond yields of 5.95 and RBI rate 4% tells us? Is it possible that the bond yields will fall to 4% over a period of time?

No, it depends on the bond in reference. Remember, it has to factor in interest rate risk + credit risk and the premium associated.

Hey ,i had searched about the short terms funds of different AMC\’S but in the factsheet or in the portfolio I did not find the modified duration and Macaulay duration, where I can find those in the fund?

Strange, because this is critical info, should be available in the fact sheet of the fund.

Two days ago, I read about the modified duration above & yesterday, RBI cut repo rate by 0.40. So, I thought of testing it.

Fund.Dir-Grth Mod. Dur. Y\’day Gain

ABSL GSF. 7.32. 0.60

DSP GSF. 6.95. 0.69

EDEL GSF. 5.5. 0.68

ICICI 10 Yr. 7. 0.61

IDFC GSF. 6.8. 0.57

NIPP GSF. 6.6. 0.50

It appears that the math is not that simple. Other forces also play. Please explain.

By the way, although I did not know these technicalities, I participated successfully in last 3 gilt rallies, gaining 12%+ for 2/3 years. I get in after couple of rate cuts & get out after first rate hike.

Thanks for your educative lessons.

Nice study material to gain knowledge about personal finance..Thank you

1.Can you please tell how nifty and gold etf are related?

It\’s seen that as market goes up gold price goes down and vice versa..Please explain this

2. Does it necessary for one to have certain amount of index and gold in their portfolio to stabilize profit and loss ratio..

1) Will include that in an ETF section

2) It is good to have these in a portfolio to spread risk and stabilize the portfolio.

sir, isme aur bhi chapter hain kiya ?

Hi Karthik,

I have some lump sum amount that i wanted to invest in index funds (please suggest if anything will be better than index fund at this time).. i was thinking of taking the STP route with first parking money in a liquid fund and then moving the money to index funds in a period of around 6 months.. now my question is given the uncertainty in the market is it advisable to park the money in the liquid fund or i will be good with money in the Bank and taking conventional SIP route to the index funds..

Also any suggestions on which index funds to choose will be welcome, not looking for names, what criteria i should apply or what parameters i should look at . Thanks

Rites, given the environment, you can park the money in your bank SB and then SIP in an index fund. I think UTI has the lowest expense ratio

thank you for your efforts, really great to have simple explanations. please provide mutual fund diversification.i have a query-

for a person in 30% tax slab, what is better- overnight/ liquid debt fund or govt bank FD to safely invest? sip in equity mutual fund are already there.

This should depend on your overall portfolio, I may not be in a position to render a good advice 🙂

Karthik after reading your trading systems module I’m highly motivated to build a trading system of my own. I have seen that you say we’ve to get clean data from nse certified vendors. Now how is that data different from data downloaded from NSE and cleaning it ourselves? Also, if we buy data from vendors is it like a one time purchase where we get historical data? I am asking this from the point of view of constructing a Quant System. Please answer both the questions. Thanks a ton for all your work Karthik. Greatly indebted to you.

1) Yes, you can get data from NSE and clean it up yourself. Its just that it is a daily process. If I were you, I\’d opt for the data from a vendor, where his primary job is to give you clean data

2) It is usually a yearly subscription. You get historical plus the data for the coming year

Karthik after reading your trading systems module I\’m highly motivated to build a trading system of my own. I have seen that you say we\’ve to get clean data from nse certified vendors. Now how is that data different from data downloaded from NSE and cleaning it ourselves? Also, if we buy data from vendors is it like a one time purchase where we get historical data? Please answer both the questions. Thanks a ton for all your work karthik. Greatly indebted to you.

Highly informative content Karthik! Thanks for sharing

When is the next chapter coming?

I\’m 75% done, hopefully in a day or 2 🙂

As you said, there is no liquidity in the long dated options sir. But my question was more geared towards theoretical understanding of Expiry Series. I could not see any noticeable pattern. Can you please shed some light on this? For theoretical understanding.

Apart from the fact that these are long-dated options, everything else remains the same.

Karthik I have a doubt regarding Nifty and Bank Nifty Futures. I know they have recently introduced Weekly options on Nifty but there seems to be no observable pattern if I see the dates of various expiries. It extends to December of 2023, which is 3 years away. Can you explain what are the new expiry series in Nifty and how to make sense of them? It would be of great help. Thank you.

Options expiring in Dec 2023 are called a long-dated option, they are not tradable as there is hardly any liquidity. I\’d suggest you stick to the monthly contracts, this is where all the action lies 🙂

Sir, one suggestion.

In Zerodha Coin, we don\’t have the asset allocation of the mutual funds unlike other brokers (Eg. ICICI). Please try to add this feature in the future if possible, so that the complete information about the mutual fund especially its allocation in sectors & companies can be analysed.

Do you mean the portfolio of the individual funds?

Hi Karthik,

Love your content, kudos to you and your team.

Can you please cover Gold funds in coming modules, how it works and its details.

Happy to note that, Aftab. I will try and do that 🙂

Interest rate predication is complex I know 🙂 , Can you please explain how fund manager hedge interest rate risk ?

They do this with fixed income strategies, check out things like laddering, butterflies, and barbells 🙂

Dear Sir

Really the contents are very useful for investors. As i am risk taker so in general how many nos. of MF/SIP should be in my portfolio

Not more than 3-5 funds in my opinion.

Hi Karthik,

Bond prices are inversely proportional to interest rate. Looking at current scenario repo rate 4.25 now. Do you think it will go further down? If not then do you think it is good to shift low and ultra low duration fund which has modified duration less than 1. (Low interest risk). May be just related question , you said fund manager hedge the interest rate risk. Can you explain how they do it

Thank

Nikhil

Nikhil, I\’m not sure if I\’m capable of predicting interest rates 🙂

Sir

Great study material from Zerodha.

Sir what is SORTINO Ratio and Side Pocketing in MFs ?

Regards

Will be covering these topics in the coming chapters.

Hey , i have a question regarding , Ultra short term , Liquid Funds and debt funds in general . In current situation. Since their is lock down since 1 and half months now ,even the well run Companies are incurring losses ,So what do you think about the Credit risk and Default risk related to it. Do we need to expect a sharp increase in these risk even for the \”AAA\” papers due to current crisis .

Also I have even seen a sharp decline in most of the Debt funds at the end of April , i guess due to panic among investors after \”Franklin India Debt Saga\”.

So i wanted to know your views on it and what should we do , can we invest in a scheme now, having satisfied by its current records or we should wait and watch , as situation may drastically change in coming months.

Debt funds are a scary term now. Your thinking is right, there could be rating cuts and even default, but the problem is timing these events. I\’d suggest you carefully track and take a wait and watch approach.

Its lucky that your friends have not invested in MF. If they have invested in MF last year, they would have lost 30-50 percent today. Nothing is certain.

Yup, nothing is certain in markets 🙂

Hey , loved you\’re explanation on the mutual funds and personal finance in general . I think you are doing a great work by spreading this knowledge to everyone for free and in depth. As i have gone through many investing sites and MF sites and almost 90% of them only talk about the return aspects (1yr,3yr,5yr) but none of them are concerned about telling about the risks or educating us before we put our hard earned money. I don\’t think even a Mutual fund agent selling any scheme would like to explain this stuff in detail obviously because of higher commissions. It is only now in the crisis times that their truth comes in picture.

I also feel that India\’s financial literacy is still very low and it needs to be promoted on wider scale and people like you are at forefront of it. I have shared your article and varsity app to all of my friends but many are still very slow in their efforts as i feel many of them and their parents are not confident about the MF industry i.e due to mainly lac of knowledge and they still keep lakhs of rs. in their bank accounts for long period of time.

Apart from it i wanted to know about gilt funds and index funds. Also i wanted to ask that is it good to rely only on equity mutual funds for now or should i also start directly investing in stock markets, considering i am little new to the markets and i am gradually learning about fundamental analysis and i am from finance background ??

Thanking You!!

Thanks for the kind words and also for spreading the word. Every effort counts 🙂

In the next chapter, I will discuss the GILT fund and few other funds. Of course, I will talk about the Index fund as well. While MF is a good, direct EQ is also a great component of your portfolio, but it depends on how well you are equipped to handle this. The more you learn, the better you get it.

First of all hats off you guyz….means if I have learnt how to swim in ocean of share market….all credit goes to you guyz….may god always bless you guyz….

Now as concern to my query…are you guyz planning for any module on algo trading in future.. because if you are introducing this module in this portal..than anyone can wait for that in coming future…..and if you aren\’t then please guide how to proceed for algo trading learning

Thanks for the kind words Aman 🙂

Currently, there are no plans to introduce that, will certainly keep that in mind.

Karthik – You are doing a great service to the community by writing these awesome articles. They are really helpful. I have recommended these to my family members and they also loved it. I hope this series continues and become a benchmark for not so informed retail investors and public at large.

Just to let you know, these articles on personal finance are not available on varsity app. Was wondering why it is so?

Thanks!

Thanks for the kind words and thanks for helping us spread the word, Sumit. We have a lot more to add here, so this module will continue for a while 🙂

We are adding one module at a time, this will be added to the app when the module is complete.

Thanks for explaining in depth information about mutual debt mutual funds.

It will be great if there can be suggestive debt portfolio, especially for 50+ age group, who wants to park a substantial part of portfolio in debt instruments.

The suggestive portfolio, I meant the type of fund.

Suppose I want to keep my 3 years equivalent expenditure in debt fund.

For Sort team (less than 3 months), I can easily select ultra Short term/Over night fund.but for rest of the period I am little confused with so many type of funds.

Also like technical analysis, if you can suggest a debt fund check list, which a retail investor can easily digest and execute.

Thanks in advance

I will do this, Anup. For 3 years, I\’d suggest a low duration or a money market fund. It is scary to beyond this in the current circumstances 🙂

I am not able to reply to previous answer on index fund . Assume there is some technical errror right now.

Hence, posting saparate que on your answer on index fund.

Your answer is:

\”Jalpa, if you are doing a one-time investment, then maybe you can take the wait and watch approach. If you are doing a SIP in index fund, then go ahead and invest, no need to wait and watch.\”

For index funds , there are different views by different investors. In Intelligent Investor, it says,it is good to do index funds in SIP mode. Others says , it is good to do them in Lumpsum. So,

1) How to decide , What appraoch is right for you?

2) Considering current situation, how should we think of index funds, lumpsum or SIP?

Thanks in advance!

1) I\’d suggest SIP too

2) Start with a lumpsum and then continue SIP on it 🙂

HI.. EXCELLENT FINANCE LITERATURE TO LEARN IN A SIMPLE LANGUAGE!!1

DEBT IS USUALLY INVESTED FOR SECURITY OF OUR INVESTMENT.. SO HOW DOES IT DIFFERS FROM EQUITY MF .. WHEN DURATION IS 2 YEARS OF INVESTMENT ?

THANKS

The nature of the underlying assets is very different, hence the difference.

I want you to please discuss the tax details that needs to be paid while selling different funds.

For now you can refer to this module – https://zerodha.com/varsity/module/markets-and-taxation/

Will try add another chapter on this.

For last 3 months, I have been investing in equity mutual funds.

As stock market is fluctuating these days , I was wondering to invest on index fund as well. I amnot sure , I should start investing them right away or wait for some more days for stock market to come down?

Also , we can\’t thank you enough for the amount of efforts you are putting in these course. Deep gratitude.

Jalpa, if you are doing a one-time investment, then maybe you can take the wait and watch approach. If you are doing a SIP in index fund, then go ahead and invest, no need to wait and watch.

IDFC debt fund is less risky comparing to Nippon debt fund. So if interest rate increase then chance of selling and moving out from this fund would be higher, taken into consideration the risk factor. so bond price / nav would decrease rapidly. Thats why Modified duration is high in the case of Nippon bond fund

Am I right?

Perfect 🙂

Also, look at the rating profile of the papers held by Nippon. Not as good as IDFC.

Can u please include a working guide to understanding credit ratings and how reliable are they?

Yes, we will in the next module (fixed income mini-series).

Hi Karthik,

You have a great knack of explaining things. Keep it up!

I have couple of questions:

1) Now that the government is dropping interest rates (almost every year) to spur growth, would it be advisable to go for higher modified duration funds? Or is there a catch here?

2) Can you please explain the inverse proportionality of the yield and price of the bond?

Thanks,

Jayendra

1) Higher the modified duration, higher the risk. Which implies that you will have to be prepared for long term investment in the debt funds. You have to take that call based on how you plan to structure your portfolio.

2) If the bond price drops, then yield increases. Think about a discounted paper available to you at 96, this means the yield is about 4% (assuming you get 100 on maturity). If the interest rate drops, then the price can drop to 95.5, and therefore the yield increases to 4.5%. This is a crude example, but I hope you get the gist.

Sincerely appreciate the great work Karthik.

Is there a single place where all the parameters of a liquid fund can be compared ? Most of the places like value research provide individual performance etc.. It is difficult to compare asset quality, beta, sharpe rato etc..

Thanks again.

I\’m not sure about that, perhaps there must be some feature in VR online. Need to check that myself.

Sir why sebi is not aware of this Franklin liquidity problem,is it not a bigger scam than PMC was 10k crs franklin is of 28k crs,why they have not disclosed the information of borrowings from banks to pay back investors,what do you say about this do u think they are transparent in this issue.

Its not a scam, Srinath. This is a market-led scenario. AMC was transparent, they conducted in ways prescribed by SEBI, it is just an unfortunate incident.

If the redemption requests and new investments are blocked in Franklin Templton debt funds, then how NAV is expected to change? Is it that the NAVs will change because of the expected defaults made by the company or after the default occurs?

It is based on the assets that they hold.

Hi Karthik,

I have gone through all your chapters and I must say your way of explaining things is simple and easy to understand. Would request you to upload the remaining chapters soon. I am investing in MFs for last 3 years based on self analysis. However I still find it very difficult to find a single source to get all the relevant information. There are multiple sites like moneycontrol, value research, etmoney etc. But I get confused when I see different sites. Also some of the information like Macaulay duration, Modified duration etc. are not readily available. Can u please let me know a SINGLE SOURCE from where i can analyse the MF.?

Thanks, Abhijeet. I need time to prepare the content, so this will take some time 🙂

Btw, I too look at the same sites and get all the info. Sometimes, it is best to visit the AMC website and get all the relevant info from the factsheet.

thanks but sir…is there any risk in terms of AMC prospective….or should i change from niftybees from reliance nippon to say icici nifty bees or kotak nifty bees etf.

You can always split your investment across a few AMCs to hedge institutional risk.

What will happen to etf like niftybees or bankbess… If the AMC closes or go bust like franklin templton…is these etf will track respective benchmark with little tracking error… irrespective of the performance of fund houses …or there is any fund house risk in it…kindly add chapter on etf also.

Franklin was a case of liquidity in debt markets. I\’m assuming ETFs, although not liquid, is still better than DEBT. Also, the segment itself is small compared to the debt funds. Will add a chapter on ETFs.

Sir on what basis will Franklin Templeton investors will get there investments back,is it on nav as of 23/4/2020 is when they announced the shutting down of those 6funds or will it be on the nav on the sale day of those assets.

I think the NAV for the funds will be announced on a daily basis. We are waiting for more details on this, will share as and when we get more info.

Hindi me please

Sir what is redemption?

When a mutual fund investor wishes to take back the invested money, its called a \’redemption\’ request.

Sir, when you mean 1% increase in the interest there will be \”n\” decrease in the NAV, what interest rate does it mean here? Because, all the CDs,CPs or Bonds that are invested have already fixed the coupon rate right? Could you please explain a bit more on this?

I\’m talking about monetary policy rates. Yes, the change in rates have a higher impact on bonds compared to CD and CPs, in fact that is evident with the low modified duration of these funds.

Hi, Question about The Franklin India debt fund saga:

let\’s talk for one particular fund: Franklin India Ultra Short Bond Fund: by definition Macaulay duration is 3-6months

1. So can we assume that the investors money will be returned in 6months at max?

2. I understand that now purchase and redemption is blocked for this, but until money is returned to investors, does the NAV of these funds will be frozen or will it keep on varying?

3. In the situation of COVID-19, let\’s say borrowers are not able to pay the money back to Franklin, it\’s Macaulay duration will be affected? Then usually how does this being managed or it\’s simply not taken care by Fund Manager.

Thanks a lot, hoping for a reply. I\’m one of the investor who has parked a bit sum in this fund and feel really sad now.

1) The weighted average is 6 months, the papers can be longer than that. So no visibility on that just yet

2) It is expected to vary

3) THis will be a case of default and will affect the overall fund. Btw, this wont impact the duration of the fund.

Do check this thread – https://tradingqna.com/t/everything-you-need-to-know-about-whats-happening-with-the-6-debt-schemes-of-franklin-templeton/75781

A 1% increase in interest rate decreases the bond’s price by 3.2%. A 1.5% increase in \”bond price\”, lower the bond’s price by 4.8%

A 1% decrease in interest rate increases the bond’s price by 3.2%. A 1.5% decrease in \”bond price\”, increases the bond’s price by 4.8%

the place where the bond price is written in inverted commas looks like a typing error

it must be the interest rate

Ah, thanks, will check this.

Why you can\’t approve Bank FD, Government Bonds, Gold Bonds and Bharat Bond ETF for margin funding for F&O.

Bharath Bond, you can use, FD is operationally a nightmare. Govt Bonds is work in progress.

Great information in varsity,

Happy to note that, Rajesh. Happy reading 🙂

All these mutual funds are rated by the returns they generate. Rather Rating should be split – Capital Preservation & Returns Generation, from retailers perspective as most wouldn’t know to look at scheme composition & arrive at a decision.

Most of the ratings are flawed Chetan. One should do their analysis without looking at ratings. Will talk more about this as we proceed in this module.

Hey Karthik, great piece, I think the date is wrong here -13.4 – The Franklin India debt fund saga says – \” On 23rd August 2020, Franklin Templeton (India) AMC\” instead it should be \” On 23rd April 2020, Franklin Templeton (India) AMC\”

Thanks, Pulkit. Made the change.

Love to all the Learnapp folks 🙂