12.1 – Overnight Fund

We are in living in strange times, as I write this, the market is down nearly 30% from its peak. I’ve seen markets get hammered for a variety of reasons – recessions, business cyclicality, fraud, political unrest, civil unrest, geopolitical tensions, wars, and heck even family feuds. But never in my wildest dreams could I imagine the markets getting trashed owing to a virus of an unknown origin.

I guess with COVID 19, we have seen it all. At least, I hope so :).

Nevertheless, we have to do what we have to do. So let us get back to the debt funds.

In the previous chapter, we introduced the concept of a bond or a debt structure and discussed the first debt mutual fund, i.e. the liquid fund. Do recall; the liquid fund is not risk-free as most people assume, it is susceptible to both default and credit rating risk. The Taurus MF and Ballarpur example highlighted this credit risk in liquid funds.

Both these risk types are significantly reduced (not eliminated) in an overnight debt fund. Remember, a liquid fund invests in papers maturing up to 91 days, this typically includes both the corporate commercial papers and the Govt’s treasury bills.

An overnight fund, on the other hand, invests in securities which have one-day maturity. Think of this as lending money to someone for one day only. So at the start of the day, the Fund manager of an overnight Fund lends to ‘someone’ which is recovered back in 24 hours.

This is precisely what happens in an ‘overnight debt mutual fund’.

Given the fact that the overnight fund invests (or lends) to 1-day debt obligation, the chance of a change in credit rating risk is low. The default risk still exists, although it is small.

The next obvious question is – who are these overnight fund lending to? Well, the overnight loan happens to an RBI regulated money market instrument called ‘Tri party Repo’ or the ‘TREPS’.

I’ll not get into the details of what a TREP is and its purpose, I think that will stray us from the main focus of this chapter. All you need to know is that a TREP is a relatively safe instrument wherein the act of lending and borrowing happens over a 24hr window. You can read more about TREPs here – https://www.ccilindia.com/FAQ/Pages/TREPS.aspx#1

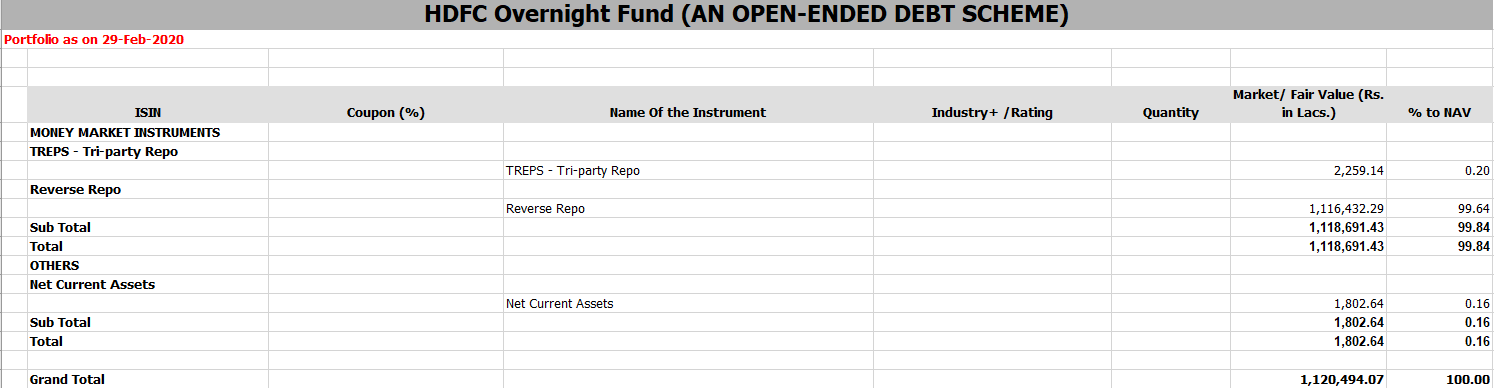

I want you to look at the portfolio of HDFC Overnight Fund –

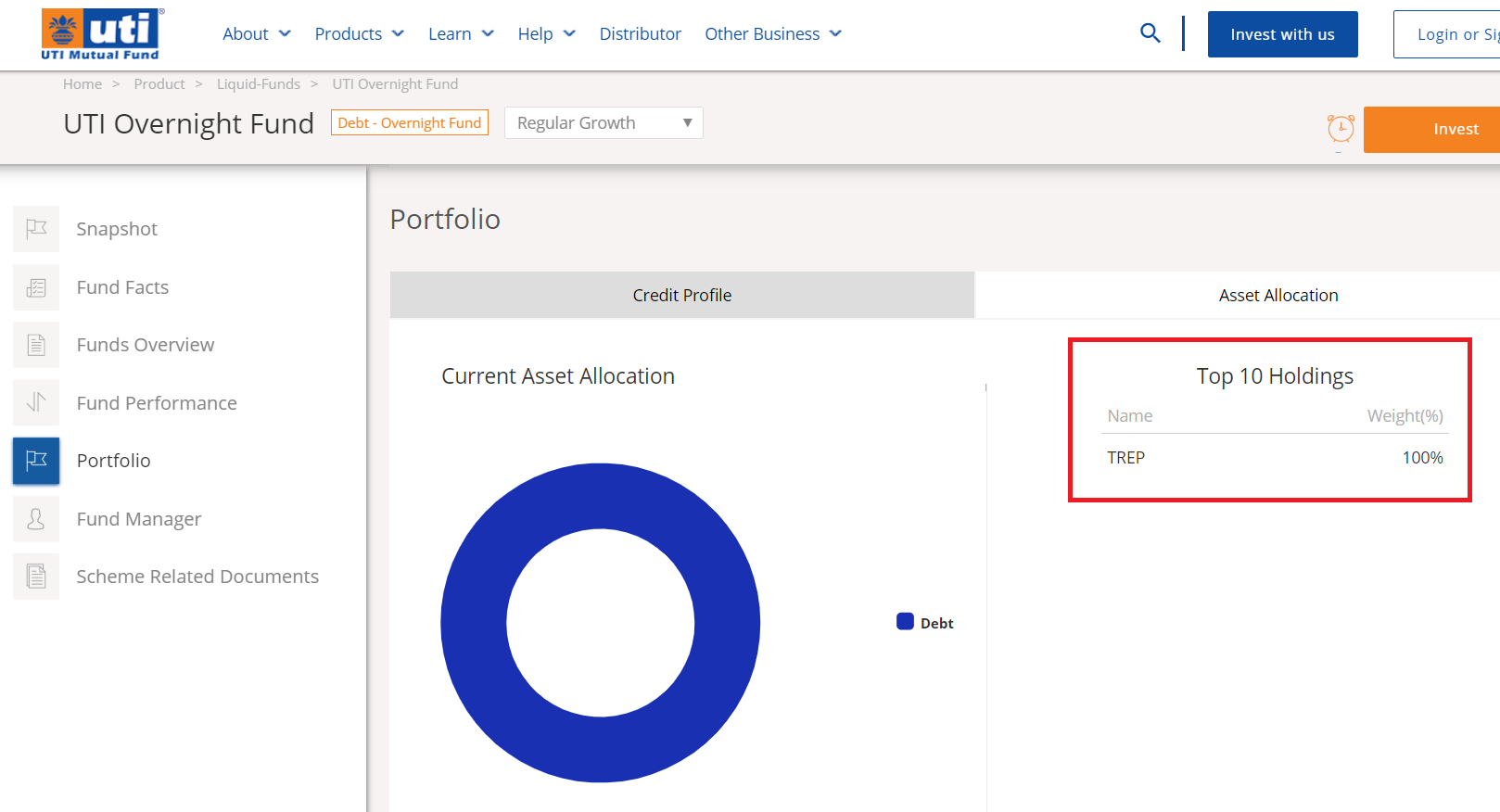

As you can see, the entire portfolio consists of only one instrument, i.e. the TREP. Have a look at the portfolio of the UTI’s overnight fund –

Again, 100% of the fund invests in TREP only.

This leads us to an important conclusion – as every overnight fund invests in TREP instrument, there is no difference between the overnight fund A and overnight Fund B. They all tend to put up the same performance. The only difference is because of the difference in the expense ratio.

Of course, we have not discussed the expense ratio, yet in this module, we will in the coming chapter.

So who would want to invest in an overnight fund? Well, this is an ideal fund for anyone looking at parking funds for a short term duration. By short term, I mean for less than three months. Remember, if you want to park funds for more than three months or 90 days, you are better off looking at a liquid fund.

It is futile to look at the return aspect of an overnight fund. It does not make sense, because you don’t invest in an overnight fund to chase ‘returns’, you do for the sake of convenience.

However, if you are interested, as of today, overnight funds yield around 4-5% annualized. So you can do the math on a pro-rata basis.

12.2 – Ultra-short duration Fund

Next up is the ultra short term debt mutual fund. Things in the debt mutual fund start getting interesting from now.

Think of yourself as a debt mutual fund manager. Your job as a fund manager is to find investments opportunities in the debt market. You can do so by investing the scheme’s corpus in new bond/CP issues, or you can choose to buy these bonds from the secondary bond market.

Think of this as buying a stock at the IPO or buying it post the IPO from the stock exchanges. Now, the moment you buy it from the secondary market, the price of the bond will (may) differ from the first issue price.

Why would the price vary? Well, for a host of reasons including the demand and supply dynamics of the bond.

Each time a bond is purchased, the bond manager expects a periodic coupon (interest) payment during the tenure of the bond and at the end of the tenure, the principal to be repaid.

Let us hold on to this thought for a moment. We will get back to this thread in a bit.

Think of another case. Your best friend needs Rs.10,000/-. He approaches you for it and promises to repay within a year. You decide to give him this money, interest-free.

Now, how long does it take for you to recover back your money? The time taken to get back your money is a year. It was easy to evaluate the time taken because there is no other cash flow in the form of interest repayment.

On the other hand, if there was an additional cash flow in terms of a coupon payment, paid every three months, then what do you think would be the time taken to recover the money?

While pinpointing to the exact number can be a bit tricky, intuition says that the time taken to recover the money is little lower than a full year, because there is cash flow. Do note; you can do some math and get the exact time to recover the money, but let’s not get there.

The point to note is – in the presence of cash flow, the time to recover the principal is lesser.

With this point, let’s go back to the previous thread.

Fund manager A subscribes to a bond at issuance. The specifications are as follows –

- Face value = Rs.1000

- Coupon = 8%

- Coupon payment frequency = Semi-annual

- Maturity = 3 years

Question – How long will the fund manager A take to recover the money invested in this bond?

Answer – Intuition says that it could be a little lesser than three years.

Fund manager B buys the same bond from the secondary market. Now, we know that the bond prices fluctuate in the market. Assume the fund manager B pays Rs.1020 for the same bond.

Question – How long will the fund manager take to recover the money invested in this bond?

Answer – Intuition says Fund manager B will take slightly higher time to recover the price paid for the bond when compared to fund manager A.

Fund manager C buys the same bond from the secondary market. Assume the fund manager pays Rs.980 for the same bond.

Question – How long will the fund manager take to recover the money invested in this bond?

Answer – Intuition says Fund manager C will take lesser time to recover the price paid for the bond when compared to Fund manager A.

I’m trying to make two points here –

- Bond price fluctuates

- Based on the price paid, the time to recover the invested amount varies.

There is an exact science to estimate the time to recover, that is an integral part of the bond math. The metric, ‘time to recover’, is called ‘Macaulay’s Duration of a Bond’.

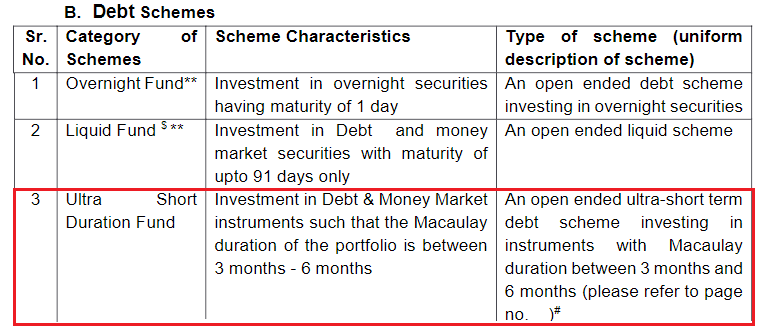

Why is ‘Macaulay Duration’ essential and why are we discussing that? Well, have a look at how SEBI defines the characteristics of an ultra-short duration fund –

According to this definition, an Ultra Short duration fund can invest in short maturity bills and CPs, which has a maturity between 3 month and six months (90 to 180 days).

An important point to note here is that SEBI later specified that this is at a portfolio level and not restricted to an individual bill or CP. What this means is that the fund can buy CPs with a maturity of fewer than 90 days or maybe more than 180 days, they can even invest in TREPS, but at an overall portfolio level, the fund has to ensure that the Macaulay duration of the entire portfolio falls within 3 to 6 months.

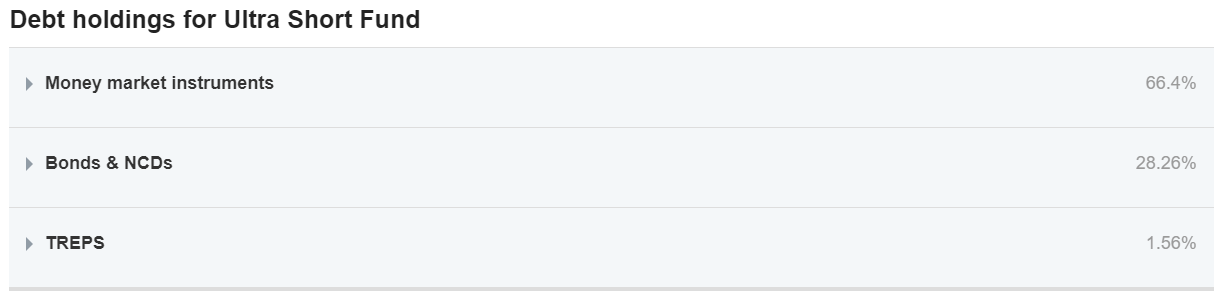

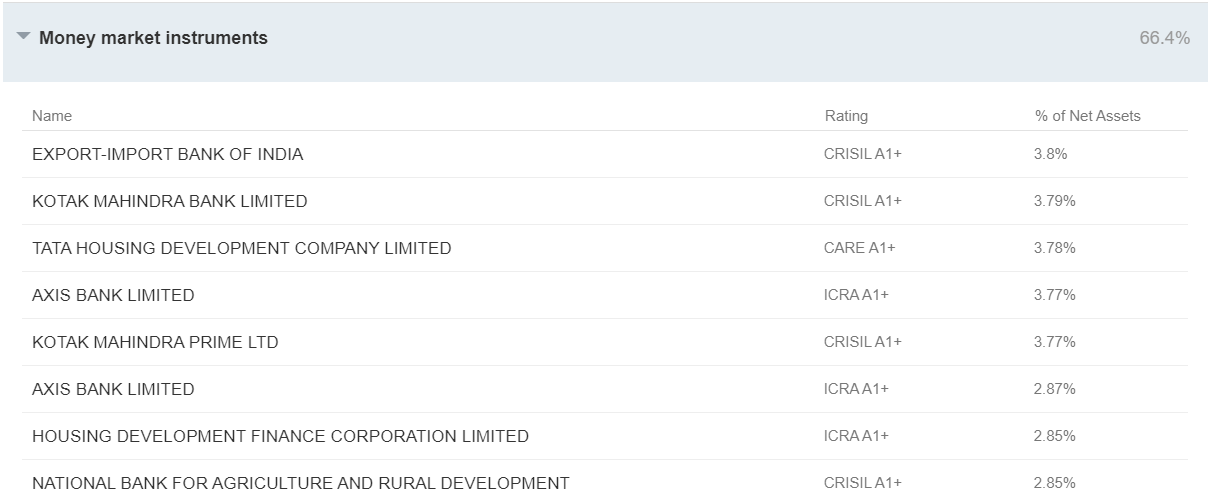

To give you a perspective, have a look at the portfolio of DSP’s Ultra-short duration fund –

The bulk of the ultra-short duration fund is invested in money market instruments; the maturity ranges anywhere between 1 day to 365 days. Mostly these are CPs belonging to various corporate entities, here is a snapshot of their money market portfolio –

They also hold NCDs and Bonds (NCDs and bonds are the same), which have a maturity of at least a year –

The job of the fund manager is to ensure that they not only manage the returns but also manage the Macaulay duration of the entire portfolio such that they adhere to the SEBI specified norm.

There is another interesting point to note here – while the ratings of CPs kind of vary for the money market instruments, they are all triple-A for Bonds and NCDs. Triple AAA ratings imply that the probability of default is lower.

As the maturity of the bond increases, the bond manager is more worried about possible default in the bond. Hence, they tend to stick AAA rate bonds.

However, this leads us to a critical point concerning ultra-short duration funds – they are not risk-free. These funds too, have the risk of credit default and rating downgrade.

Given this, who should invest in an ultra-short duration fund?

I think that this is a good fund for anyone looking to park money for 1-2 years, plus they are ok to take a wee bit of risk on the parked capital. If you can make peace with the fact that on the downside your money can go down by a few percentage points, then go ahead and park your funds in this ultra short term funds.

If you are looking at parking money for lesser than a year, stick to a liquid fund instead.

On the return side, I think it is reasonable to expect a return close to the bank’s fixed deposit.

12.3 – Franklin and Vodafone saga

Since we are talking about Ultra-short duration bonds, I guess it makes sense to quickly discuss the Franklin – Vodafone drama that unfolded earlier this year.

Franklin India had invested in Vodafone India Limited (VIL)’s debt papers across six different debt schemes, including its Ultra short-duration bond fund.

In Oct 2019, the Supreme Court of India passed a judgement in favour of the Dept of Telecom (Dot), in a case against DoT and the telecom operators. As a result of the Supreme Court’s judgement, the operators were asked to pay the licence fee and the spectrum usage charge based on the Adjusted Gross Revenue (AGR).

If you are not familiar with this, then I’d suggest you read this short note from the good folks at Finshots, they have done a great job at explaining the AGR episode – https://finshots.in/archive/the-final-verdict-on-agr-2/

Anyway, to cut a long story short, post this judgement, VIL was now expected to pay Rs.27,000 Crs to DoT towards unpaid dues.

This means VIL would be cash squeezed; hence they are likely to default on their debt obligations.

As a smart money manager, after all, sorts of ramification of this judgement, Franklin India took a proactive step, and they themself internally downgraded the VIL’s papers to junk status and wrote off that investment.

To give you a perspective, Franklin India’s Ultra-short bond fund had 4.2% of its portfolio invested in VIL’s paper. Now, what do you think happens when 4.2% of your portfolio is rendered useless?

Obviously, the NAV of the fund falls. Check this –

In my view, Franklin may take at least a year or year and a half to get back to the previous NAV levels. The only reason I’m discussing the Franklin and Vodafone issue is to make you understand that debt funds too are risky, invest in them only after you fully understand the risk involved.

I’ll stop this chapter at this stage. Before I wrap this up, I’d like to give you a quick insight into the direction we are heading with this module.

So far, we have discussed Equity mutual and few debt funds. The discussion is restricted mainly to a brief introduction to these funds and what happens within these funds. In the next chapter, we will continue this and introduce a few other debt funds and probably wind up the introduction bit.

Once we are through with that, we will start with the fund analysis bit and figure how to select mutual funds, both debt and equity and slowly steer our way in building a goal-based mutual fund portfolio.

So, we have a long way to go. Stay tuned and stay safe!

Key takeaways from this chapter

- Overnight funds invest in debt instruments with a 24hr settlement cycle

- Almost all overnight funds invest in Tri party repo

- The performance across overnight funds is similar

- Macaulay Duration of a fund gives us a sense of how long it takes for the fund to get back its invested amount

- Ultra-short duration fund has a Macaulay duration between 3 to 6 months

- Ultrashort duration funds are also risky

So who would want to invest in an overnight fund? Well, this is an ideal fund for anyone looking at parking funds for a short term duration. By short term, I mean for less than three months. Remember, if you want to park funds for more than three months or 90 days, you are better off looking at a liquid fund.

In the above line you told short term mean less than three month in overnight fund. But overnight fund is applicable for only one day . So why you told for less than three month in overnight month .

Overnight fund, you can invest for however long you want. But the fund itself invests in overnight instruments. So two different things 🙂

The link https://www.ccilindia.com/FAQ/Pages/TREPS.aspx#1 for reading more about TREPS is broken. It would be helpful to have another source of reference here to read about TREPS.

Check this – https://www.nseindia.com/products-services/about-tri-party-repo-intro

Remember, if you want to park funds for more than three months or 90 days, you are better off looking at a liquid fund.

Can you please tell me the reason for the same?

Tbills have a maturity of 90 to 180 days. Thats one of the reason.

Beautifully explained.

Happy learning!

Karthik just wanted to know, how to ensure that someone with restrictions on investing in alcoholic, bond, or bank-related companies avoids such investments.

How can we track and prevent our manager from investing in these types of companies?

Amir, there are funds with specific mandates to invested in companies which comply to these investing rules. They are called the Ethical funds, I\’d suggest you check that.

Hi Karthik

I am a bit confused about the difference between Macaulay’s Duration and maturity . can you please share few more examples or some additional resource that help me to understand the difference?

Maturity = Actual date on which the bond matures and ceases to exist.

Macaulay duration = Figures the payback time of the invested amount in a bond by factoring in coupon payments.

Is Tri Party Repo and TREPS same? I am asking because above you have mentioned \’or\’ between them but as I checked on web, they are completely different concepts. Please correct me if I am wrong. Moreover, by TREPS you mean Treasury Bills Repurchase?

They are same, Kanishk.

Thank you for writing this chapter, Kartik. Two questions:

1) What\’s an ideal debt fund to park your cash for 15-20 days?

2) Why should one park it in debt fund rather than simply keeping it around in your brokerage/ bank account for 15 days?

1) Liquid funds

2) To earn an interest 🙂

Sir,

I have a doubt in Franklin Vodafone saga After VIL paid 27,000 crores it might be cash squeezed but as the Franklin was holding debt papers of the VIL it could have liquidated the assets of VIL had it not paid the debt obligations, hence there are no worries. With this thinking Franklin should not had downgrade the VIL\’s papers thereby the NAV wouldn\’t have fallen.

Why didn\’t this happened?

sir good afternoon

for example ;- sir if we invest in directly liquid fund than its maturity 91 days and if we invest in through mutual fund in liquid fund so its depend their statergy ya as u says that 1 year hold it i am wrong ya right sir please tell and i am confused ya right sir

If you invest in a liquid fund, the fund manager keeps a tab of these maturities and keeps rolling over the position. So you as an investor need not worry about the 91 day maturity.

Sir please do explain about Money market instruments (The names that are given below). Like do they invest in TREPS or treasury bill??

They do, Anshul. I\’ve explained all that there is to it here 🙂

\”While pinpointing to the exact number can be a bit tricky, intuition says that the time taken to recover the money is little lower than a full year, because there is cash flow.\”

Could you please elaborate on this? I am unable to read between the lines.How do you know that the amount can b recovered in less than a year?

So if you spend 1Cr in buying an apartement, and if you expect Rs.x as rent, then you can approximate how many years it will take to recover the investment right? Approximate I\’m saying since there is also capital appreciation on your investment. Its the same way in bonds.

Hi Karthik Sir,

These modules are extremely enlightening and interesting. Thank you so much for it. I have one question related to Macaulay Duration, how can we recover our debt investment before we receive the principal? For example, if our 1 year bond has coupon rate 8% and we receive interest twice in year, we will still need to wait for full year to receive our original principal right? So, didn\’t it take full year to receive our investment wholly?

Glad you liked the content. Its a theoretical concept to establish how quickly you will recover your investment given the coupon cash flow rate.

Question – How long will the fund manager A take to recover the money invested in this bond?

Answer – Intuition says that it could be a little lesser than three years.

Hello, I didn\’t understand the meaning of \”How long will the fund manager A take to recover the money invested in this bond?\”

Why will it take less than 3 years?. What is the meaning of \”recover the money\” ?

Recover is probably not the right word to use here, it is probably more like extracting full value 🙂

Assuming you get back the principal invested, you also get regular coupons. So adding the coupons to the principal, how much time does it take for the investment to return full invested amount is roughly how duration is defined. Think of it in lines of internal accruals.

Hi Karthik, firstly, thanks for all this education. With regard to the Ultra Short Duration Funds, you noted that SEBI explains it like this: \”…the fund has to ensure that the Macaulay duration of the entire portfolio falls within 3 to 6 months.\” Q: Does this mean this is on an everyday rolling basis, or only at the time of rebalancing? Do the fund managers have to actively rebalance everyday depending on the Macaulay duration change at the individual asset level? Thanks.

I\’m not sure how frequently they have to rebalance, but I guess this could be monthly once, especially around the time they have to report/disclose their portfolios to the public and regulators.

Are Debt funds suitable choice for save money for emergency?

Yes, but it depends on which one.

This paragraph

—

Fund manager A subscribes to a bond at issuance. The specifications are as follows –

Face value = Rs.1000

Coupon = 8%

Coupon payment frequency = Semi-annual

Maturity = 3 years

Question – How long will the fund manager A take to recover the money invested in this bond?

Answer – Intuition says that it could be a little lesser than three years.

—

I did not get how it could be lesser than 3 years, considering the coupon rate, it would 80 per year, that would amount to only 240 in interest at the end of 3

years and then they would repay the rest of the principal, hasn\’t the time elapsed till then? How could it take < 3 years, could you clarify thanks

At 3rd year (on maturity), FM gets back the principal. So factoring in the coupon, it will be just short of 3 years.

Hi kartik

u mentioned one statement

\”I think that this is a good fund for anyone looking to park money for 1-2 years, plus they are ok to take a wee bit of risk on the parked capital\”

But if Macaulay\’s duration is 3 to 6 months then how it is relevant for 1 or 2 year

Sarvesh, I think you are getting confused with macaulay\’s duration and your holding period. Both are different. Macaulay\’s duration just highlights the risk of the fund in proportion to the fund\’s assets.

Why did Franklin write off Vodafone bonds as junk instead of trying to recover it or at least wait for them to actually default? At least they would have a chance to get some debt back. Now they lost 4.2% of their portfolio for sure. Maybe they wouldn’t lost the capital if they have waited.

Q1 – Asset classification norms require AMCs to classify and write off if necessary. Hence they would have written this off.

I assume it was just a classification. They didn\’t actually burn those bond papers. So in case if Vodafone tries to repay its bond, Franklin AMC will also recover its NAV?

Yup, it was a classification and they carved out the Vodafone investment and created something called as a \’Segregated Portfolio\’.

Then CDs means Fund Manager gives loans to Bank as Deposits and earn some interest on top of it (Like in Savings Bank Account). Am i Correct ??

Somewhat like that 🙂

One Doubt, In Commercial Papers(CP) fund manager subscribe to the paper issued by Companies and at last they get interest, so its the profit. How do Certificate of Deposit (CDs) work or generate profit in this context ??

They don\’t work to generate profits, they have raised the funds to meet a certain financial obligation for which they have to pay interest. This is just like a loan you\’d take from a bank.

Hello Karthik,

Sorry, I seem to have too many questions with bonds. Here are two more if you don\’t mind.

1. Why did Franklin write off Vodafone bonds as junk instead of trying to recover it or at least wait for them to actually default? At least they would have a chance to get some debt back. Now they lost 4.2% of their portfolio for sure. Maybe they wouldn\’t lost the capital if they have waited.

Question 2:

Face value = Rs.1000

Coupon = 8%

Coupon payment frequency = Semi-annual

Maturity = 3 years

I think it should translate to roughly 240 INR as interest over 3 years. And the final amount to 1240 INR.

Let\’s assume someone pay 1240 for it in the secondary market on the listing date. I think \”Macaulay’s Duration of a Bond\” for it will be exact 3 years?

What if they paid 1500 INR for it which is more than the cost of the principal+interest itself. What will be the \”Macaulay’s Duration of a Bond\”. I heard govt bonds in some countries are in big demand and investors are willing to pay a premium to buy them to safeguard their money.

Question 3:

I assume you also get part of your principal back on \”Coupon payment frequency\” date. Otherwise your money is not safe until maturity since interest is just a small part of the capital.

Q1 – Asset classification norms require AMCs to classify and write off if necessary. Hence they would have written this off.

Q2 – The numbers that you stated are not intuitive, but the higher the price, the longer it takes to recover and hence higher Macaulay

Q3 – Yes, but the price of the bond can also fall right?

Sir can you include investment of REITS in mutual fund section

Maybe in Part 2, Rajiv.

Hi Karthik,

Great resource for beginners like me. Thank you.

Just a small clarification, if overnight funds are settled within 24 hours, why is it mentioned overnight fund is ideal for parking money for less than 3 months. Can you elaborate a little bit please?

It should be treated as cash in bank, Malavika. Plus these are taxes slightly differently giving you an advantage over other debt products.

Hello sir, investing in T-bills still make sense as it is risk free, but why invest in funds containing risk and giving a similar return as FD\’s. So isn\’t FD a better option to choose? Or is it that the future FD & Saving\’s account interest in going to be very low so it would be necessary for us to learn about bonds and invest in it?

Mohit, the advantage is the way debt funds are taxed.

Yes sir,I was little confused why interest rates and bond prices are inversely proportional I got it sir

Thank you for this amazing modules

Happy reading, Avi!

Sir when there is more demand for a bond usually the bond price increases,then interest rate should also rise

Then why it is inversely proportional

Coupon rate you mean?

Sir does Macaulay’s Duration of a Bond says the The AMC should get back the invested amount within 6 months

Thats right. It is an approximation.

Sir why it become late to get the principal amount when cash flow is not involved as in case of lending money to friend example

So Franklin India can do nothing if VI ran out of money? I mean the bond should\’ve had a collateral right? Can\’t Franklin India ask VI to sell some of their property to avoid reduction in their NAV?

These are unsecured bonds, Vinay.

Hello Sir,

These are wonderful article with lots of information. I normally allocate a small percentage of investment in debt funds. Since you have mentioned debt fund are used for short term parking. Do you recommend moving those investment to other types?

Also can we directly invest in NCD and bonds from zerodha?

Debt funds/liquid are still good for short term parking. No issues with that. Yes, you can invest in NCD, check this – https://coin.zerodha.com/bonds

Macaulay Duration of a fund gives us a sense of how long it takes for the fund to get back its invested amount.

You mean to say that the Macaulay Duration of a fund gives us a sense of how long it takes for the fund to get back its principal amount?

Like if the fund manager puts 1lakh in an USMF, then it is the time taken to get the 1lakh back?

Thats right.

Hi Karthik, in deb funds #1 you had mentioned Liquid funds invest only in CPs and T bills with a maximum maturity of 91 days, but in this chapter you\’ve mentioned if you want to park funds for more than three months or 90 days, you are better off looking at a liquid fund. Can you please help clarify ?

These are two different things, Aaditya. What the fund invests in, is a matter of their portfolio. You opting to invest in these funds is a different thing entirely.

Hi Karthik!!

Ultra-short duration fund has a Macaulay duration between 3 to 6 months- does this means the fund manager will withdraw funds from one bond and re invest in another bond or fund manager will close the fund and distribute the funds to the investors?

Will the investors notified if the fund manager withdraws from one bond and re invest in another bond?

They usually hold to maturity and rollover to similar bonds and bills upon maturity.

Hi karthik!

\”Ultra-short duration fund has a Macaulay duration between 3 to 6 months\” – does this means the fund manager will withdraw the money from one bond and invest in another bond by the end of the time period or fund manager will close the fund and distribute the money?

Will the investors(us) be notified if the fund manager transfer fund from one bond to another?

I think these modules are unique and you are doing great by educating the society. Specially, when financial literacy is lacking in India.

I have one question, when the VIL papers written of (Sold), who buys?. What happens if VIL pays off in future.

Thanks, Tejas.

By written off, I mean, its just assumed as a bad bet and let go. No one really buys them. Like a scrap car, it sits in the side. If VIL pays off, then that\’s a different thing. Investor gets back some money.

What does it mean to \”wrote off that investment.\” line franklin and vodafone saga? Also what ts a secondary market?

You basically forget about it and conclude that it was a bad investment 🙂

Hi, after introduction of stamp duty on mutual funds do you think overnight, liquid, ultra short term MF makes any sense?

You mentioned overnight MF are ideal to park money for less than 30 months. After stamp duty isn\’t it close to bank\’s return?

Hi Karthik,

What if I stay invested in overnight funds for around 1 year if I am content with 4-5% interest it offer at almost zero risk. Thanks!!

Its absolutely ok to do that, no issues.

Sir,

I would like to inform you, the explanation part done by you with the help of examples is simply the best.

One more thing sir is there anything more that is covered by you or your team except this series. If yes, please do tell. I would be grateful to you.

Thank you.

Glad you liked the content 🙂 Btw,there is a lot of content here Ayush – https://zerodha.com/varsity/

Hi karthik,

One section/lesson is needed on REITs and Foreign Funds. Cut off timings of foreign funds. etc.

Thanks

Sure, will make a note on this.

how can we download module 11 and 12 pdf?

11 will be available once the module is completed. No PDF for 12.

Hey karthik

You mentioned \”Remember, if you want to park funds for more than three months or 90 days, you are better off looking at a liquid fund.\” but in the previous section you said the maximum duration of liquid fund is 91 days …gives some light here

Thanks

ARUN

91 days is for the t bills itself, but the funds keep rolling over their positions so at any point they will have a portfolio of tbills.

Sir, I have read that bond price is inversely proportional to interest rates. Why is it so?can you please explain with an example.

Here is a nice link which explains this – https://www.investopedia.com/ask/answers/why-interest-rates-have-inverse-relationship-bond-prices/

Hi Sir,

I am first time investor. And my pan is not KYC verified. Can you help with these initial setups.

Your help would be greatly appreciated.

This is easy, please do follow the onscreen account opening instruction and follow-through, and you will be done.

Hi Karthik,

You have seen many situations in the market life cycle- such as- recessions, fraud, political unrest, geopolitical tensions, wars. And now COVID- 19 market has already in crashed and we are again going into recession.If we consider longterm picture( 10-15 yrs) will the always be market be bullish or will it be generate good returns. How much it takes for the market to recover from any situation like this.

Markets tend to go up in the long term, that\’s what markets have taught us so far. I\’m of the belief the same will happen in the coming years as well 🙂

Hi Karthik,

Hope the lockdown is treating you well!

I checked for UTI MFs on Coin but don\’t seem to find them, any specific reason why UTI isn\’t listed there? And can we expect it to be listed on Coin? Also, is UTI a trustable brand when it comes to investing in MFs as compared with other bigs AMCs (HDFC, ICICI etc.)

I understand things been difficult, but when can we expect the module on \’How to chose MFs\’?

Thanks!

Rohit, all fund from UTI and other AMCs are available on Coin. AMCs are highly regulated, they are all trustable brands.

Yes. I get your point.

I\’m trying to understand it from the fund\’s perspective. Doesn\’t the fund that buys the debt papers wait till maturity? Or do they keep trading them in the secondary market which affects the NAV? Ideally, they should just hold on to the debt if the interest rates have gone up to secure at least the predecided coupon price.

Most often they hold to maturity, few trade the papers and it really depends on the scheme.

Hi Karthik,

Shouldn\’t the \’Modified Duration\’ parameter be of concern only when one plans to sell off the fund before the maturity since the interest rates would impact the fund\’s NAV only if one plans to sell his funds?

So if the investor holds till maturity, he would ideally get \’Principle + (pre-decided)Interest\’ as the final amount if there are no defaults irrespective of the change in interest. Is that right?

From the investor\’s perspective, there is no concept of \’wait till maturity\’ in a mutual fund, Rohit. You have to look at it as a fund, however if you were to invest in a debt paper directly, then yes, this is a matter of concern.

Hi Karthik,

Since overnight funds give you returns close to the returns offered by a savings account, then isn\’t it better to keep them parked in the SA to avoid the hassle of investing and also paying any fees associated with it?

Yup, it does. Use overnight funds only for the ease of moving funds between different schemes.

I am investing in MFs since last 3 years but never had any detailed information like you gave here. after reading this, my perspective changed a lot. I still don\’t know why I invested in regular plans without going deeper into that. but now I want to correct that.

Please do, Siddhesh and good luck with that 🙂

till now whatever I have invested in MFs are all regular plans. should I convert them to direct plans?

Better for you right? So why now 🙂

Sir, above you mentioned that rating for Bonds & NCDs are all \”AAA\”, so chances of default is low. But what\’s the credibility of those ratings. Afterall, companies pay the credit rating agencies themselves to obtain the \”AAA\” rating. If Agency A doesn\’t give a company AAA rating, then that company can always just go to Agency B or C. So, this more or less compels them to give AAA rating.

You cant just pay and purchase AAA. Companies pay to get their papers rated…but what rating they get, its beyond the company\’s control, at least to a large extent.

hi karthik,

plz add more funds in overnight as collateral.as it is risky to concentrate large sum of money in one fund .

thnks

Thank Ankit, will look into this.

hi karthik.

Given the fact that the overnight fund invests (or lends) to 1-day debt obligation, the chance of a change in credit rating risk is low. The default risk still exists, although it is small.

plz explain risk here (credit risk and default risk)

Thats true Ankit. Default, rating, and interest rate risk is low. However, liquidity risk still exists and we saw this in the case of Franklin funds.

hi karthik .

1.what are the risk involved in overnight funds if we deploy large sum of money .

2.u have only icici overnight fund in collateral as cash component .

3 capital is preserved (not looking for returns ) in overnight funds as i will do option selling for more than 5 years

1) Overnight funds are relatively safer

2) Yes

3) Yes

You got one more Franklin drama to give us as learning. I am very much relieved that I redeemed all my units before 23rd and yes, I suffered that VodaI dea credit risk too. Investors please don\’t run before more return. Happy Investing!!

You bet! We discuss a bit here – https://zerodha.com/varsity/chapter/the-debt-funds-part-3/

hi karthik ,

u have taken 2 default examples of taurus fund and franklin fund .u have said that nav got a hit and then it recovered .

my qs is that when nav got a hit it is a realised loss or unrealised loss even if we are invested in the fund for long term .

i mean to say after nav hit our return are hit at the current moment as nav is down .but after holding it for long term cagr will be affected on our fund in the long term

It is unrealised since you\’ve not redeemed your units.

Yes, I had checked.

a) Is it better to invest in overnight instead of liquid funds during these circumstances (for pledging)?

b) While most liquid funds are generally same, surely a fund with more AUM is considered more \’safe\’?

Thanks!

1) Yes, overnight is the safest

2) Yes, that is the general perception

Hey Karthik, well written as always!

I\’m primarily an option seller, so the liquid funds would be the obvious choice for me. But under these circumstances, is it better to invest in overnight fund instead? I\’ve been tracking the AUM of liquid funds the past 2 months & all of them have reduced (some quite considerably). Also, Coin has only one option when it comes to overnight funds, so putting all that amount in one place carries institutional risk. Could divide the amount between overnight & liquid fund too I guess.

This might create a bias, but any of the Liquid Funds you can recommend? I don\’t have the best judgement in selecting stocks/funds, so any inputs/advice for this situation would be appreciated.

Sachin, all liquid funds are available on Coin – https://coin.zerodha.com/ , search for the word liquid and you find them all. Like I\’ve explained, almost all liquid funds are the same. Go for the one which has a low expense ratio.

Hi Karthik,

You are one of the best teachers I have come across. I don\’t think thanking you will be enough for all the content provided in such an easy language. God bless you 🙂

Hope will see the next chapter soon as I\’m very excited to build my finanicial profile.

Stay Safe.

Regards,

Pratibha

Thanks for the kind words, Prathiba 🙂

I\’m working on it, will update the next chapter in few days 🙂

Hi Karthik,

Can you suggest some reputable and detailed source of how to make an optimum MF portfolio? I know you plan to cover that topic here but still, I want to invest asap with the current market downfall.

Thanks

Hmm, I\’m also looking for one to cross-reference my thoughts 🙂

chapter 1

1.2 – the investment plan of 12% per annum table has a value drop from 14th year. The value show of the cash retained and retained cash invested @12% is same but the final is 4.2 Cr

please clarify the doubt and calculation. how did it end up changing the final amount???

Need to check. Why don\’t you post this query in chapter 1 itself, may help others.

Sir I am new to trading and I just finished reading Futures and Options module. In it you say Nifty has only 3 months contracts (and only monthly contracts) however I go to NSE and I see Nifty Futures Weekly contracts and also contracts extending up to 28/06/2023 which is two years away from now. Can you please explain? Thank you.

Yes, the weekly was introduced much later. For now only bank nifty weekly is active. Not much trading in weekly Nifty.

Hello, I am a college student and is looking to invest 3-5k per month in MF. What kind of MF will you suggest?

Thank you

Either an index fund or a multi-cap fund.

Just want to say Thanks for all your efforts to put down such a knowledgable writeup.

Thanks, Rajeev. Happy reading 🙂

Hi Karthik ,

Not yet, I was going through personal finance first. Are the concepts on fundamental analysis or technical analysis works same in MF?

Regards

Kartik Soni

No, not at all. None of that is required for MF investing 🙂

Hi,

First of all a big thank you for you work. May god give more power to you.Your articles are exceptional.I have recently started looking into personal finance and have developed a keen interest in MF and stocks. I have completed all the 12 articles and waiting for others.

Meanwhile can you guide us what else we can follow to develop our niche skills in Financial literacy. Still i didn\’t feel confident enough to start investing my money.

Regards

Happy to note that. Have you read the other modules on Varsity? Especially the one on Fundamental analysis?

I loved reading your articles, @Karthik. I\’m totally new to this world and your content made it really easy for me to build a strong foundation. I couldn\’t wait more for your next chapter, when can we expect it here?

By next weekend for sure 🙂

I\’m new to the world of trading and these articles have been extremely helpful in understanding the world of trading..keep it up!!

Good luck, Kishore!

Sir, your content is very useful for me. I just want to invest in MF; I have a sum of 2.75 lakh and I want this total after 6 months. So, What I can do with this fund? Which MF is best for me to invest this total?

Vishal, since you need this money in 6 months, its best if you can invest this in a liquid fund.

The content varsity has I am gonna stick for sure sir.

Sir here are some doubts please clarify it,

1.While investing in any of the funds should we consider the past returns or not to consider the past returns before doing any investment.

2.Instead of investing only in a single fund like Franklin India can we divide our capital and invest in multiple funds like hdfc,axis because every funds will have different portfolio holdings and allocations.

3.When there is a interest rate cut by RBI why the bond price becomes higher,with increase in bond price will we get higher returns.

4.Should every portfolio have the index fund of debt along with our equity investments.

1) You look at it once just to get a perspective. Your decision should not be based on that though

2) You can. The reason to do this not because different asset allocation, but rather to mitigate the institutional risk

3) Bond prices are inversely related to the interest rate. Yes, an increase in bond price is good for existing investor

4) Yes, that would be a good asset allocation strategy.

Sir could you estimate the number of chapters this module would consist of, I mean when its all done?

Sir, there is quite a bit of work left in this module, sometime I feel we are not even 30-40% through. Its hard for me to estimate now. Also, the fact that we are juggling between app content and web, kind of takes away the bandwidth. So request you to kindly bear with us. Thanks.

Franklin India fund which you have discussed in the module what does 27.33 signifies here if I have invested 100 rupees in this fund does it signifies now it is at 27.33 nav.

Ah, that would depends on the price at which you\’ve invested i.e. the invested NAV. 27.33 is the NAV.

Sir the nav here is it the current value of the fund if we have invested 100 rupees in this fund now it is trading at 27.33. I feel it is not like that what does 27.33 signifies here.

Which fund are you talking about, Srinath?

Sir

Please what is \”SORTINO RATIO\” in mutual funds ?

Thanks

I will do that in the coming chapters.

Karthik,

I have been reading all your material since last 2 weeks regarding technical, fundamental analysis and personal finance and it has been really very helpful. Thank you for the same. As you have mentioned in your lecture; ultra short term funds are quite risky as they are exposed to defaults etc. During black swan events like covid-19, how are the debt funds exposed and in what way? Is it recommended to transfer the funds in FD for short-time till we get more clarity in events as such ?

Thank you in advance for your reply. Appreciate your efforts.

Smeet, this is a very tricky situation. This is when you will have to look into the portfolio and see what the fund manager is holding. For example, I\’d be a bit hesitant to park funds in a fund which has papers from airline company or an ancillary services company to this industry. Check this btw – https://www.rupeevest.com/Mutual-Fund-Debt-Holdings

Hello Karthik,

Considering requirement of funds after a year, I had invested surplus funds (around Rs 10 lacs which I received after sale of property) in Short Term Debt Funds. However, the requirement of funds is now deferred by 5 years.

Can you please guide me if I need to stay invested in these debt funds (current appreciation is around 8.5% p.a.) or you suggest to invest in some other schemes / asset classes.

Thanks a lot.

If you have a 5 year period, I\’d suggest you look at a blend of funds – 30% – 40% in Equity funds, some in ultra short term, and bulk in the medium-term bond fund. Do remember they are all subjected to risk, so if you want your capital to be 100% intact, then maybe a 5 year FD is the best. Do check with your financial advisor once.

Karthik,

If you could brief bit about NCD that would be great. I understand commercial paper and t-bill (corporate, government respectively) as per your write-up. Is \”CP\” and NCD are the same?

Thanks,

Harikumar J.

CPs have a maturity of less than a year while an NCD has longer-term maturity. NCDs and bonds are the same.

Hi Karthik,

Once again great Job. I have a question, tell me what is the difference between top performing and top ranked mutual funds?

Desh, over the next few chapters, I\’ll write about selecting MFs, will discuss this there.

Karthik,

As per your write-up on ultra short term debt fund, \”On the return side, I think it is reasonable to expect a return close to the bank’s fixed deposit.\”, wouldn\’t be simpler to go for fixed deposit? Other than \”hoping\” to get slightly better returns is there any other advantage?

Regards,

Harikumar J.

Yes, it does. It is just that the ultra-short duration bond has a potential for a slightly higher return plus the liquidity. Which is not possible with a fixed deposit.

Great study material from Zerodha !!!!

Kindly explain what exactly MONEY MARKET means? How MONEY MARKET differs from STOCK MARKET?

In debt MF, there is a concept called SIDE POCKETING. Please clear this concept also.

Thanks a lot.

The money market is essentially a market to trade/invest in short term debt instruments like the treasury bills, TREP, and CPs. This is an institutional market, not for retail.

I will write about the side pocket concept in one of the upcoming chapters.

Hello sir. Its been a long time since I spoke to you. I had long back asked you what your portfolio looks like and you said that you would not disclose it because it would create a bias that will work against investors and that in the future date you\’d disclose it. My request again is, would you be comfortable in disclosing just two or three holdings? As you know, I\’m still a student and it would very much help my on my learning curve. Also, the new module on mfs are excellent. I\’ve introduced to some of the earnings members of my family and they were thankful for it.

Sudeep, I\’ve invested in few MF\’s – UTI Index funds both Nifty and next 50 🙂

Sir if the returns are same or close to bank returns means then are these funds are just used to park the money for sometime,and Franklin wroteoff that investment means have they sold 4.2% of holdings in vil papers.

Thats right, Srinath. You park your money and hope to get slightly higher returns.

Hi Karthik Sir,

I have read 2 modules in this series over this weekend, and looking forward to reading the entire book!!! Thank you so much for consolidating this information.

Meanwhile, there are some things which I would like to let you know about the content; I\’ve sent you an invite over LinkedIn for the same.

Thanks, Tushar. I\’m not very active on Linkedin, but I do check once a week or so. I\’ll respond soon. Thanks.

Hi,

I am 24 yo and just started my Personal Finance journey. I am more than glad to have found this resource. I started and completed all the 12 articles today and am waiting eagerly for the MF portfolio management stuff. Can you tell me your frequency of article uploads monthly here? Once again, thanks a ton for this! 🙂

Happy to note that, Raunak. There is no set frequency, it really depends on how quickly I can write the next one. Usually takes about 1.5-2 weeks for me 🙂