16.1 Overview

In chapter 6 & 7, we discussed the basics of a mutual fund and how a fund works. Just to recap, a mutual fund is a pooled investment vehicle that takes your money, invests and manages it on your behalf. What distinguishes one fund from another is the management part. There are 100s of strategies that AMCs employ but broadly speaking, you can categorize them as:

- Active

- Passive

In an active mutual fund, the fund manager tries to beat a benchmark or deliver alpha. In simple terms, alpha is the excess return above a benchmark.

Before we go further, it’s important to understand what a benchmark is and why do you need a benchmark. A benchmark serves as a point of reference for measuring performance because you cannot look at the performance of a mutual fund in isolation. Every mutual fund benchmarks itself to an index like the Nifty 100, Nifty Midcap 150, Nifty Smallcap 100, etc depending on the category it operates in. Benchmarks also give you an idea of the returns you would’ve made if you had done nothing and just bought the index.

Now, the job of the active manager is to deliver returns over and above the benchmark. He does this by actively picking stocks or based on various strategies and by deviating from the benchmark to various degrees. For example, one of the most widely used strategies among mutual funds is Value investing. Here a manager tries to pick stocks that are cheaper than their intrinsic value. On the other end of the spectrum, there’s growth investing where a manager invests in companies, as the name implies that is growing at a faster rate than their peers/industry and also invest most of the earnings back in the business to fuel the growth. Similarly, there are hundreds and thousands of approaches and strategies used by managers, which is outside the scope of this chapter, but I hope you got the idea. The job of an active manager is to beat the benchmark.

A passive fund or an index fund, on the other hand, simply tracks the performance of a benchmark as closely as possible. It does not try to outperform or underperform the benchmark, but just match the returns before costs (expense ratio). Mutual funds have costs, so the return of an index fund, broadly speaking, will be the benchmark returns minus costs.

So, when you invest in a Nifty 50 index fund, all you are getting is Nifty 50 returns. If Nifty 50 returns 10% this year, your return will be 10% minus the expense ratio. It’s as simple as that.

16.2 History

Before we look at the performance of active funds, why index funds make sense etc, I think it’s important to know a little history about how index funds came to be.

The story of how the first index fund came to be is quite fascinating. John C. Bogle, also known as Jack Bogle, the founder Vanguard, launched the first index fund in 1976. The fund was called the First Index Investment and tracked the S&P 500 Index. The fund was later renamed as the Vanguard 500 Index Fund. For context, the S&P 500 consists of the 500 biggest US companies, and the index is a market capitalization-weighted. Meaning, the total free float outstanding shares of a company are multiplied by its price and higher the value, higher the weight of that stock in the index, and it’s that simple. Nifty and Sensex follow the same methodology as well minus a few technicalities.

The crazy thing about the first index fund is that the launch was an abject failure. Vanguard led by Jack Bogle was hoping to raise $150 million during the underwriting process but managed to raise just $11.3 million. They didn’t even have enough money to buy all the shares in the index. What they ended up doing is they sampled the index, they just bought enough stocks across sectors to broadly resemble an index, and it worked out well in the end. If Jack Bogle had given up, we probably would have had to wait longer for an index fund and history would have been much different.

Even though it was launched in 1976, the Vanguard 500 Index Fund didn’t reach the $1 billion mark until 1990. As of writing this chapter, however, the fund has $500 billion in assets and is the largest mutual fund on the planet. This fund alone is bigger than the entire Indian mutual fund industry, which has about $350 billion in assets. As for Vanguard, it is the second-largest AMC in the world with over $6 trillion in assets, next only to Blackrock, which has close to $7 trillion in assets.

India

IDBI Principal was the first AMC to launch an index mutual fund tracking Nifty in India. The scheme later became the Principal Nifty 100 Equal-Weight fund. Benchmark AMC was the first to launch Niftybees – an index exchange-traded fund (ETF) tracking the Nifty 50. Benchmark was later acquired by Goldman Sachs India which was acquired by Reliance mutual fund which was acquired by Nippon.

Today, the biggest mutual fund in India is an Index fund – the SBI Nifty 50 ETF with over Rs 60,000 crores in AUM. Before you start thinking when did index funds become so popular in India, they aren’t 🙂 Pretty much all of the money in this ETF is from The Employees’ Provident Fund Organisation (EPFO). It started investing in equities since 2015 and Nifty, and Sensex ETFs were the chosen routes. The AUM of Index mutual funds is a better proxy of the popularity of these funds and as of April 2020, they just had Rs 8,800 crores in AUM.

This is nothing compared to the Rs 119,861 crores in active large-cap mutual funds, for example.

16.3 Definition of an index fund

The active vs passive debate is one of the longest-running, loudest, and one the most controversial debates in finance, I’ll get to that later. But even when it comes to the definition of an index fund, there are widely different thoughts. Today, any fund that tracks an index is called an index fund. You can technically create an index of companies whose name starts with the letter G and then launch a fund tracking that index. But the very first index fund was tracked the S&P 500 which is a market capitalization-weighted index. But according to the hardcore finance guys and academics, a true index fund is one that tracks a broad cap-weighted index like the Nifty 50, S&P 500 etc.

16.4 Do index funds work?

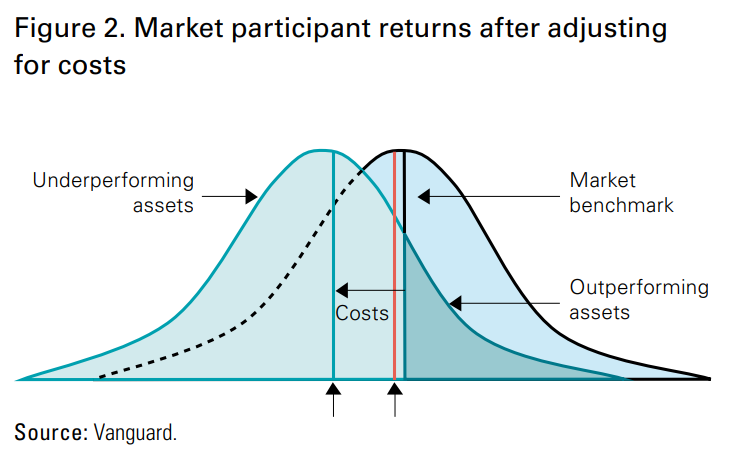

You may be wondering given that index funds just track a benchmark and not seek to outperform, how do they even make sense, it’s a fair question. Outperformance is always better than just benchmark returns, right? Let’s unwrap this. There are a bunch of complicated ways this can be answered, but here’s the gist. If you think about it, markets are a zero-sum game, meaning for every person making money, somebody has to lose money. Here’s an illustration to explain that:

This means that all active managers collectively cannot beat the market. The reason is cost, and they are the biggest drag on the performance.

Now forget that you read the previous paragraph for a minute and let’s look at costs. An active mutual fund seeks to outperform any index, which means it needs the resources to do so. This involves hiring a bunch of analysts, getting the best Chief Investment Officer(s), the best research, the best tools – your Bloomberg Terminals what have you and other things. All this doesn’t come cheap, and there are costs involved.

How much? Let’s compare the expense ratios of active large-cap mutual funds and index mutual funds. Moneycontrol shows the category average expense ratios, which allows you to quickly get a sense. The category average expense ratio of active mutual large-cap mutual funds (direct plans) is 1.28%

The category average for index funds, on the other hand, is 0.31%.

Note: the average expense ratios will be far higher for regular plans of mutual funds.

That’s almost a 1% difference. Though this might seem small, costs compound over a long period and significantly eat into your returns. If you are investing on Coin, you’d have already realized this and made the smart choice. But just to reiterate, you can use the savings calculator on Coin to calculate the impact of costs. Here’s the difference between paying .6% and 1.6% on a Rs 10,000 SIP over 20 years. That tiny 1% difference will cost you Rs 12.8 lakhs.

Assuming that an active mutual fund is charging 1.5% is benchmarked to Nifty 50 for example and let’s assume that the Nifty Index fund charges 0.10%. Right out of the gate, the active fund is at a disadvantage and has to generate 1.4% just to keep up with the benchmark, and I am not even talking about outperforming the benchmark.

Index funds, on the other hand, are extremely cheap. The SBI Nifty ETF charges 0.07% for comparison. The reason why index funds and ETFs are cheap is that they don’t need highly paid star fund managers, research teams etc. All they have to do is copy an index, and that’s it.

16.5 Historical Performance

Let’s look at the historical performance of active funds and index funds. I know at this point, you are thinking about those huge past returns displayed prominently on AMC sites, Value research and elsewhere. S&P – the world’s largest index provider publishes a semi-annual report called the S&P Indices Versus Active (SPIVA®) scorecard. This report looks at the performance of active funds versus a standardized benchmark period for 1,3,5,10 years. Here’s how the Indian active mutual funds have fared as of the end of 2019.

On 5 years, 82% of active large-cap funds have underperformed the S&P BSE 100 index, which consists of the 100 largest Indian companies by market cap.

Although the performance of mid and small-caps looks promising, things seem to be changing. With the recategorization exercise, SEBI has clearly defined the universe of stocks fund managers can invest in which will make outperformance harder. Up until last year, we didn’t have mid-cap index mutual funds, we had ETFs, but they were illiquid. Several AMCs have started launching them over the past year or so.

As for small-caps, active or passive, I don’t think investors should invest in these funds at all. They seem to fall as fast as they go up, which makes it frustrating for investors to hold on to. That gut-wrenching volatility also increasing the chances of investors buying high and selling low.

16.6 Bottomline

Based on the numbers at any given point, your chances of picking a consistently performing active fund is worse than 50:50. In the case of large-caps, it’s consistently worse. And it’s going to get worse as the Indian capital markets deepen. Let’s take the case of large-caps, and there are 40 AMCs and 40 large-cap funds. Broadly speaking everybody pretty much has access to the same information and everybody can only invest in the top 100 stocks, outperforming the benchmark isn’t easy, not to mention the cost disadvantage they have vs index funds.

And there’s also the issue of funds just hugging benchmarks which is quite common – this is also referred to as closet indexing. Most funds don’t deviate significantly from the benchmarks, and after expenses, they are guaranteed to underperform the index.

There’s another way of looking at this. Famed researcher Michael Mauboussin, in this paper, termed this the paradox of skill:

“In cases where two or more players have the same level of skill—whether that skill is high or low doesn’t matter—the skills of the players offset one another and luck becomes the primary determinant of the outcome. “Players” can be athletes, investors, or business executives. In many competitive realms, including investing, the skills of the participants have improved on an absolute basis but have shrunk on a relative basis. Today’s investor has vastly more resources and training than his or her predecessor from years past. The problem is that investors, broadly speaking, have gotten much better which means that the difference between the skill of the best and the average participant isn’t as great as it used to be”

16.7 Fixed income (Debt)

So far, when I say an index fund, I’ve meant equity index funds. Globally in the last 5-10 years index funds including debt index funds, have experienced phenomenal growth. Bond ETFs recently crossed the $1 trillion mark in the US. In case you are wondering if there are any debt index funds in India, these are very early days for equity index funds, let alone debt index funds. Except for the recently launched Bharat Bond ETF and fund of fund, we don’t have any debt index funds.

The Indian debt markets are very tiny and notoriously illiquid. Except for G-Secs and the best AAA-rated bonds, most other bonds trade sparingly. And unlike equities which trade on the exchanges and there’s transparent price discovery, most of the trading activity in bonds happens over the counter (OTC) or off-market. It’s the same even in the US, where the debt market is bigger than the equity market.

This, among many other things, makes indexing debt very hard, but maybe as the markets evolve, things should change. There are companies like Tradeweb trying to bring electronic trading to the bond markets.

16.8 Active or passive (Conclusion)

After reading all this, you might be wondering if you should choose active or index funds. It’s not active or passive but active and passive. You can mix both in your portfolio and have allocation based on your risk tolerance. But always pick a fund that has a long track record and sticks it’s stated mandate. Before the SEBI scheme recategorization exercise, funds didn’t have any restrictions on how they could invest. Some funds used to be labelled large-cap and used to invest in mid-cap and small-caps to juice returns. So, picking a fund where the manager does what he says is important. Funds with cowboy managers pretty much always end up as disasters.

I have also mention exchange-traded funds (ETFs) in the chapter, although they are similar to index funds, there are some important differences. In the next chapter, we’ll discuss ETFs. Similar to index funds, there’s a category of funds called smart-beta funds, which have grown increasingly popular over the past decade. The term “smart beta” is meaningless, at the core these are rules-based funds, and we’ll also briefly understand the basics.

Hi Karthik, thanks for the varsity lessons, I loved the way you explain. I want to invest in index mutual fund, could you please suggest me which index fund I have to select and how to invest via zerodha.

Thanks

Sunil

\”As for small-caps, active or passive, I don’t think investors should invest in these funds at all. They seem to fall as fast as they go up, which makes it frustrating for investors to hold on to.\”

A few chapters back, you told that time is the antidote for high risk opportunities. Are you contradicting that fact here or are you just saying that high risk opportunities are bad for people looking for short term gains?

Time is Shubham. I\’m not denying that. But this is about the level of risk you are willing to take 🙂

Hello Mr Karthik,

Thank you very much for posting yet another important lesson on Investments.

In this module

The statement regarding expenses due to which the cost one may occur says

\”Here’s the difference between paying .6% and 1.6% on a Rs 10,000 SIP over 20 years. That tiny 1% difference will cost you Rs 12.8 lakhs.\”

How was the cost of 12.8 lakh calculated?

The SIP of Rs 10000 for 20 years, i.e., 10000X20X12 = Rs 2400000

The Expense ratio being 1.6 % so 2400000X0.016 = Rs 38400 is the cost I will bear individually is what is my understanding

Am I missing something here?

YOu can calculate the SIP returns with two different expense ratio and figure what the difference is. Assume your return is 10% and TER is 0.6% and 1.6%. So post TER returns are 8.4% and 9.4%.

I am 21, just starting my investing journey. I am planning to invest in the below 3 equities-

1. 1 large and mid cap fund (for goals between 5-10 years)

2. either a multi cap/ELSS (for 10-15 year goals)

3. index fund or ETF or small cap (for retirement/15+ year goals)

Is there anything else I can invest in? or anything I can replace with some other kindof equity? Would be grateful if you can share you personal suggestions.

Also, Your work is very insightful!Love it! Would be very useful if you can incorporate some lessons specifically for early investors like me 😉

Hi Sridhar, glad you are starting your investment journey soon. These ETF/Funds look good from a long term portfolio building perspective. But please double check once by talking to a professional advisor once 🙂

Have you explored VArsity Live? We have all sorts of programs there 🙂

https://varsitylive.zerodha.com/home

I think you should put this in the above document. There is a general perception that nifty 50 represents the top 50 company of India. It is not so.

Brodersen said that in the Indian context, passive funds are like buying a quantitative fund where the portfolio is created based on tradable market capitalisation of a company. He added that it is not based on the actual size of the company, but how much shares are freely trading in the market.

hmm, but that said, the trading activity is highest in these companies itself.

Yes okay. Thank you for the prompt reply!

Sure, happy learning.

Hi.

I want to start investing with index funds as a base. I have seen recommendations to Nifty 50, Nifty Next 50 and Nifty midcap 150 as more reliable of the indices/mutual funds over a long period.

I am conflicted between choosing index funds and ETFs. The tracking error and expense ratio are low in ETFs(and for popular ones like niftybees liquidity doesn\’t seem to be an issue). Is it cumbersome to having to match the iNAV everytime before investing or ETF SIPs work well too over a long time; especially if we have to invest for a friend or a family member? Or does convenience of mutual fund SIPs, not having to constantly check the NAVs outweigh whatever loss there is to relatively higher TER?

Also, while choosing index funds, is it better to stick to a reputed and established fund but with higher expense ratio and AUM or newer index fund offering an lower expense ratio (0.06) which is closer to an ETF (for the time being till it gathers more AUM i think)?

Would be really helpful if you could provide clarity on both the thought processes.

Thanks

Hi Mansi, I think ETFs are getting a lot better in India now. YOu can simulate a SIP on ETFs on your broker platform. The only issue is to evelaute the iNAV and all that. If you can manage this, then ETF is the answer, else its Index fund 🙂

Yeah, stick to big names, that should be alright.

Thanks Karthik for your prompt response. That really helps.

I\’m investing in Nifty 50 and Nifty next 50 index funds. These are popular indices and liquidity shouldn\’t be an issue in this case. Am I right here?

If above statement is right, I can stop the SIP mutual fund, withdraw the money and put it in ETFs instead and I can create SIP for those ETFs right?

I\’m so confused here. Please enlighten me on this Karthik. Thanks!

You can do that. Yes, broad indices should have better liquidity. Btw, do check this as well – https://youtu.be/DeGzj9BJmcY?si=IyYeF20shLi6ZPkO

Hi again Karthik,

I would like to know whether similar option (creating SIP for stocks / ETFs) is available in Zerodha app too.

Yes, you can. Check this – https://support.zerodha.com/category/trading-and-markets/kite-web-and-mobile/others/articles/kite-sip-order

Hi Karthik,

I have gonethrough your modules and sort out the list of funds that im going to invest successfully and i started my investment journey 6 months ago.

My portfolio includes 2 index mutual funds. Im using Groww app to handle my investment. I noticed that there is an option to create SIP for stocks in Groww app.

AMCs have index ETFs and index mutual funds. If I can create SIP for index ETFs, that would be more beneficial than investing in index mutual funds right? because the expense ratio for ETFs are less compared to their mutual funds.

if we have an option like this, then everyone can just skip mutual fund and just create ETF SIP right? what is stopping everyone to do this? Am I missing something here?

Also, I need your guidance on whether to stop index mutual fund investment and start SIP for index ETFs instead (I have invested for the past 6 months till now).

Hi Gautam, yes, you can create SIPs and invest in it with the same discipline. Nothing wrong with it. Yes, the expense ratio is lower with the ETF. Few reasons why people dont invest in ETFs much –

1) Awareness

2) Liquidity issue

3) Tracking error.

Otherwise, ETF is a good choice.

That definitely makes sense, thank you for your prompt reply!

Cheers, good luck!

Hey Karthik,

I want to invest (over a long horizon) in an instrument that tracks the Nifty 50 index, and I\’m really struggling to understand why one would ever choose a Nifty 50 Index Fund over something like the Nifty Bees ETF.

Nifty Bees has much lower TER (as opposed to common/popular Nifty 50 Index Funds)

Due to its popularity, Liquidity does not seem to be an issue with Nifty Bees, unlike some other less common ETFs

The tracking error is pretty good, especially considering a long investment horizon.

I get to invest at a price close to the live price, i.e. iNAV unlike an Index Fund where I get assigned the end of day NAV

I have seen a few arguments in favor of Index Funds like redemption of units not being an issue since the AMC maintains a reserve (unlike ETFs where we need to find a seller). However for a popular ETF like Nifty Bees I doubt that selling units at a fair price(or close to the fair price) would be an issue.

Could you please help me understand what I might be missing here?

For someone starting new, ETF makes sense. In most cases, ppl would have started SIPs in Index fund long back, shifting to ETF will be a pain, hence they continue in MFs only 🙂

Hi Karthik Sir,

Thanks for your courses. I would like to know your opinion on \’Equal weighted\’ vs \’Market cap weighted\’ index funds for long term investment goals like retirement.

If its in India, it is market cap weighted anyway 🙂

Thanks, this is helpful – I greatly appreciate your time in clarifying the questions.

Cheers, good luck!

Could you please clarify this point on your last comment: If the NAV goes to 10, the number of units remain the same, but the value of each asset increases.

From my understanding, when I buy a fund, the total no. of units in the fund should also increase because I am adding additional money to the fund for buying more securities, thus new units shall get created. Considering the opposite, if the total number of units in the fund remains constant, it will imply that I am investing in the units of the fund and there is someone willing to sell the units of the fund.

Hey wait, I thought your question was – what happens if NAV goes up after you purchase units. So naturally, your investment value increases.

Yes, when you buy or add more to an existing mutual fund, the NAVs increase. Unlike in stocks, the NAV wont decrease if someone sells.

Hi Karthik, can you explain why the NAV won\’t decrease if someone sells?

The investor\’s purchase or redemption does not control NAV, but rather the movement of the underlying stocks.

I am trying to understand index funds and I have outlined my reasoning here is a series of questions and answers. Could you please confirm that my understanding is right?

How is the index computed?

Index computation is based on giving weightage to various securities by market-cap.

For example, there is a stock A with a market cap of Rs. 60 and stock B with a market cap of Rs. 40. Let\’s assume that the index contains only these two stocks. Then, the weightage of stock A in the index will be 60 / (60 + 40) = 0.6 and the weightage of stock B in the index will be 40 / (40 + 60) = 0.4.

Now, what is the value of the index as per the above example?

Assuming that the LTP of stock A is Rs. 1 and that of stock B is Rs. 2, then the value of index will be 1 * 0.6 + 2 * 0.4 = 1.4.

Let\’s say I invest Rs. 100 into the above index fund containing of stock A and B.

How will the Rs. 100 be allocated across the securities A and B?

Weightage of stock A in index is 60% and weightage of stock B in index is 40%.

With Rs. 100, Rs. 60 will be invested in stock A and Rs. 40 will be invested in stock B.

This will result in 60 securities of stock A (LTP of stock A is Rs. 1) and 20 securities of stock B (LTP of stock B is Rs. 2)

Now, let\’s assume the NAV of the fund is 10. Since, I have invested Rs. 100, I will get 10 units. That means, the total number of outstanding units in the fund will increase. Am I right in the above understanding?

Yes, higher the market, more weightage. If the NAV goes to 10, the number of units remain the same, but the value of each asset increases.

Hi Karthik

I have the below queries where I need your inputs:

1. I think Midcap equity funds should be avoided since if a Midcap stock does well, it will ultimately move to large cap and churn out of the Midcap fund leaving nothing as return for me. Is this reasoning correct as per you? Similar reasoning may hold for Smallcaps moving into Midcap.

2. From the above perspective is it better to have multicap or Large&Midcap funds only?

1) No, I\’d not avoid mid caps. After SEBI\’s re categorization effort, this overlap is taken care.

2) All are ok, but fit them to your purpose and financial goal.

Whether index funds are good or any other MF are good to invest for a longer period of time. Because as explianed other MFs have high expense ratio compared to index funds and they may or may not outperform.

Index fund or any large cap fund, either is good, Purva. My preference is the Index fund 🙂

Thank you for the reply. Great job on the Personal Finance Module on Varsity. It was a big help for a novice like me.

Thanks, Arjun!

All index funds have a very poor alpha (negative alpha), beta of 0.99 and returns are same for the similar index. So how to choose a fund apart from expense ratios. Does AUM of an index funds matter as the returns are more or less similar across funds.

Second point, why is a index fund better for ultra long term (retirement) goals than an active fund like large cap fund?

Arjun, index by design contains only the winners and large companies which is crucial for ultra long term goals. Also, data suggests that over long term (10years +), index funds beat the actively managed funds.

Also, index funds are not designed to give an alpha, you only expect the market returns, i.e beta.

So many index funds are tracking the same indices, let\’s say Nifty50. How can any investor find the benchmark indices tracking error of index funds? Is the expense ratio the only quantitative criterion to differentiate between index fund ?

Yes, expense ratio is one indicator of tracking error. But if your question is how to find the tracking error, then its published by the fund house right?

Is good to have both an active (Large Cap) and a passive (Index Large Cap) fund in our MF portfolio?

Let\’s say I plan to invest 30% of my overall MF portfolio in Large Cap MFs for long term.

Is it fine to distribute this 30% across both an active & a passive fund (i.e. 15% in active large cap fund and the other 15% in a large cap index fund)?

But why would you want to do that? The stocks are the same, may as well get a cheaper exposure via a passive fund?

Hi Karthik,

First thanks for the all the great information you put out here. Super grateful for that.

Can you explain the difference between the expense ratio of ETF like SBI Nifty 50 ETF which has expense ration of \”0.07%\” (as of 03/03/24) whereas mutual fund like \”SBI Nifty Index Fund\” has \”0.18%\” (as of 03/03/24). Wanted to understand the difference here.

Thanks again!!

ETFs are stock like stucture, easily managed. So the expense ratio is much lower for them, unless Index funds. The expense ratio will be much higher for an actively managed fund.

Do index fund offer Dividend ? Consisting companies of the fund certainly pays dividends then the funds

also may pay it.

No, they don\’t. Gets reinvested in the fund.

Thanks, Kartik for answering my question. I have few follow up questions:

1) For instance, NIFTY 50 ETF A has turnover ratio of 0.32% while the turnover ratio of NIFTY 50 ETF B is 0.17%?

Furthermore, NIFTY 50 Index Fund A has turnover ratio of 0.04%? Where is this huge difference coming from?

2) Does this mean NIFTY 50 ETF A would eat up my returns most followed by ETF B and then by Index Fund A?

3) I am currently evaluating costs of these funds as Total Expense Ratio + Turnover Ratio. Would you agree with this

formula? (Formula Source: Common Sense Investing by John Bogle).

1) Ideally they should all have similar turnover ratios, but I think the difference is also in terms of the fund flows to these accounts.

2) For that, you need to check the expense ratio and look at turnover ratio in the backdrop of expense ratio.

3) Yes, that would be fair.

Thanks for writing this chapter, Kartik. Could you please explain the importance of turnover ratio and how does it end up eating your returns in an index and active funds? Please elaborate.

For instance, if Fund A has an expense ratio of 0.50% and turnover ratio of 2.50% vs. Fund B whose expense ratio is 0.50% and turnover ratio is 0.30%. Would the investor selecting Fund B will have higher returns compared to Fund A?

Turnover is basically indicative of how frequently the portfolio constituents are bought and sold. Higher the turnover, higher is the expense ratio, which of course eats into your returns.

Kartik one thing is clear ki I want to increase sip amount to 4000 every month but I\’m also thinking ki ye jo 4000 every month ka amount h ye hm hr saal increase krte rhe..like for example agr abhi hm 4000 every month ki sip kr dete h then next year se iss 4000 every month ko hm 5000 ya may be 6000 every month krne ka soch rhe h so this is what I\’m asking ki hm hr saal apni sip amount ko kitna increase kre ?

On what basis should I do this ?

You can keep a thumb rule of 10% increment every year. Check this – https://zerodha.com/varsity/do-you-know-how-much-you-need-for-your-retirement/

First of all big thank you kartik for all these modules.

I have one question

I\’m invested in nifty 50 index fund for the past 3 years with sip of 2000 every month and now I want to increase the sip amount to 4000 every month but I\’m confused about by how much should I increase my sip amount every year ?

I mean how should I decide this ?

But you seem to be clear about it – right now its 2000 but want to increase it to 4000. Thats realy good 🙂

Thanks for writing this chapter, Kartik. Few questions on new indexes being developed by NSE:

1) NSE recently launched NIFTY MidCap 150 Quality 50 and NIFTY MidCap 150 Momemtum 50 which derives it\’s constituents of companies from NIFTY MidCap 150. Few of them have higher rolling returns compared to NIFTY MidCap 150/ NIFTY 50. What are your thoughts on investing in these new Indexes developed by NSE?

2) Who should invest in these indexes and under what circumstances does it make sense to invest in these indexes?

1) Higher returns also imply higher risk. Higher risk can be offset to some extent by giving it a lot of time. So you should be ok investing in these funds as long as you give your investments multi year time period.

2) The decision to invest should depend on your portfolio requirements.

Thanks, Kartik for writing this chapter. Couple of questions:

1) If 70% of the large cap funds under-performs NIFTY 50, then would it not make sense to invest in Index fund for the period of 10 years or above? Source: SPIVA

2) Under what circumstances does it makes sense to invest in NIFTY MidCap 150 Index? What would be exemplary scenario look like? What should be the key things to keep in mind while investing in this Index?

1) Yes, it does.

2) When you need exposure to mid cap stocks, thats when you opt for Midcap 150 fund. The decision to invest in this fund should be driven by your portfolio needs.

Thank you, Kartik for your prompt response. But the NAV will take into account both expense ratio & tracking difference right? If I go with example above, my NAV should be ~14.29% of the original returns (i.e., 15%), correct?

In addition, if you had Lumpsum of INR 50L. how would you go about investing these amount in Index Fund at this point in time?

Yes, the NAV factors in all expenses. If I had lumpsum, I\’d probably split that across a few months and make SIPs in a fund of my choice.

Thanks, Kartik for writing this guide. I am trying to understand how to calculate returns on investing in Motilal Oswal NIFTY MidCap 150 Index Fund. My question is \”Do I need to take into account tracking difference while calculating the returns\”? You did not seem to mention it in this chapter.

Let us take following exemplary scenario:

NIFTY MidCap 150 TRI Returns (Last 1 Year): ~15%

Motilal Oswal NIFTY MidCap 150 Index Fund Returns (Last 1 Year): 15% – 0.30% (Expense Ratio) – 0.41% (Tracking difference) = ~14.29%

Is this the correct way to analyze the Motilal Oswal MidCap 150 Index Fund Returns?

The NAV that is published by the AMC is post all the expense adjustment, no need to separately deduct it.

Sir,

For Large caps investment for hyper long term, I thought of considering direct stock investment (Market cap positioning 1-10) and some portion to index fund. Tried to avoid mutual funds of large cap. Is this okay with large cap for long term?

Now, regarding midcap and since I have not gained that expertise to pick direct stocks in mid caps, I thought to invest in index/mutual fund. As per study from zerodha, understood to invest in proportion to both mutual and index funds for midcap. Now, can you suggest the proportion to which funds should be allocated between mutual fund and index fund for midcap?

Similarly, I want to know the proportion to follow between investment in mutual fund and index fund for small cap.

N.B: Please advise noting- I can digest large volatility and can keep the investment alive for a hyper long term.

Why not fully mutual funds and leave the headache of picking stocks and managing money to a professional fund manager?

Hi Karthik

Should one consider the inception date of an index fund before deciding to invest in it? Navi Nifty 50 for example has a decent AUM size (~1000Cr) and very low TER(0.06%) but has only been running since 2021. What problems (if at all) can arise for newly launched index funds?

Thanks

It does not really matter, Atharva. It would if it was a regular EQ fund as it would give us an idea of the fund manager\’s perspective, but not for any index fund.

Sir , I intend to invest in index mutual funds for 25 to 30 years but after reading this chapter mind has changed . I sense you are indirectly saying that index mutual index fund are not good to invested .

Not at all, which part make you imply that 🙂

Sir,

I want to invest in index fund as a lumpsum amount. Could you kindly help provide me the path to do the same?I could not find the path. Please help.

You can search for Index funds here – https://coin.zerodha.com/mf/invest

A great article sir. It takes great commitment and conviction to reply to each and every comment posted across many years. Hats off to you!

I have read a lot about mutual funds by Vanguard. Many people in America swear by the index funds offered by this behemoth, because of the simplicity and low expense ratio. Based on my readings, I think Vanguard focuses predominantly on index funds and works from the angle of investor instead of working from the angle of the fund house manager or the shareholders of the AMC.

My question to you would be if India can get any fund house like that focuses majorly only on index funds that work in the favour of the average retail investor? Can we get any funds similar to vanguard total stock market index fund in India? If this is not possible, can we directly invest in Vanguard from India any time soon (currently we only have mutual funds that invest in Vanguard but not directly, I believe)?

Thats right, Siva. Vanguard has done amazingly well. Cant think of any fund as such, but I hope Zerodha AMC turns into that 🙂

Hello Karthik,

Good day

1. While choosing An Index fund what is more important

1. The AUM of the company or

2. Expense ratio

2. What AUM is considered to be an healthy one for a company to be choosen

Thankyou in Advance

Both are important, I\’d suggest you take a look at the expense ratio closely. AUM, there is no set number as such. But beyond 20 – 30K cr, it may start getting bloated.

how to invest in index fund nifty50,

Please login to Coin and look for the fund you wish to invest in, as simple as that 🙂

Hello Karthik,

https://www.spglobal.com/spdji/en/research-insights/spiva/#india

According to the above link you shared, as a reply to @Pranjal, I understand that:

1) 1 year: only 9.09% of active funds outperformed S&P BSE 100

2) 3 years: 16.13% of active funds outperformed S&P BSE 100

3) 5 years: 10.94% of active funds outperformed S&P BSE 100

4) 10 years: 32.64% of active funds outperformed S&P BSE 100

So, it means if I invest for 10 years, there are only 32.64% chances that the selected active fund will give returns over the benchmark. Whereas, there is 67.36% chances of getting returns below the benchmark. Is this understanding correct?

Thats right, Virendra. Hence most ppl stick to index funds.

How does investing in an index fund actually differ from investing in the index shares if the fund were to track the index, e.g difference between investing 10k in Nifty 50 vs 10k in UTI Nifty 50 index fund for a 10 year term? Thank you

I\’m assuming you are talking about investing in individual shares, right? So the costs will be very high in buying shares as each share is treated as a transaction. Its much cheaper as a fund.

Hello Karthik

Thank you very much for all the content on Varsity. This is exceptional stuff.

Same thing as Mihir, I couldn\’t understand the graph and what can be inferred from it. Specifically the labels of underperforming or out perfoming.

Thanks, Vinay. Maybe I\’ll try and update the graphs. But let me know if you are stuck with something else, I\’ll be happy to help.

Hi, I did not understand the market participant graph(Figure 2). Can you please share resources explaining the same in detail?

Which bit in particular, Mihir?

How can I buy an index fund SBI Nifty 50 ETF.

Look for it on Kite market watch, Neelesh… and buy/sell just like how you\’d buy/sell stocks.

Hi Kartik, I have a question in one of your lessons https://zerodha.com/varsity/chapter/the-mutual-fund-portfolio/ here you have recommended index fund as investment vehicle for long term investments 20Y+. Basically ideal for building retirement corpus. I am also in the middle of building my retirement corpus. And I have stumbled upon these solution oriented equity funds for retirement:

https://groww.in/mutual-funds/filter?q=&fundSize=&investType=%5B%22SIP%22%5D&categories=%7B%22Other%22%3Afalse%2C%22Solution%20Oriented%22%3A%7B%22type%22%3A%22category%22%2C%22parent%22%3A%22Solution%20Oriented%22%2C%22subCategories%22%3A%5B%22Retirement%22%5D%7D%7D&sortBy=0

I suppose these are \”actively managed\” counter part of index funds. What do you make of these are they better compared to index funds for long term investment?

It depends on multiple things, Hardik. If you feel active fund managers won\’t outperform the index in the long term, then maybe an index fund is a better choice.

Sorry, do you mean the percentage of active funds overperforming index funds has dropped over the years? Or Active funds are actually doing better now?

Yes, I mean the % of active funds underperforming the index. YOu can check this for more details – https://www.spglobal.com/spdji/en/research-insights/spiva/#india

Hey Karthik,

Thanks for all the info, really helpful.

By the article above, what I understand is that since the expense ratio of Index funds is much lower compared to Active MFs, and that chances of finding the right Active MF to beat the index fund are lower than 50% (or might get lower as we move ahead) then the best bet is to use Index funds?

For a long term portfolio (10 / 20 -yrs) then, does it make sense to keep about 60% in Index and 40% in Equity MF? How about 90% in Index?

Absolutely. We have seen this happen in the west as well. The percentage of active funds underperforming index funds has dropped over the years. Assuming something like that will happen here, maybe you can invest a larger portion to index funds.

I want to invest in IT INDEX FUND. How can I invest. What is the best IT INDEX FUND.

PLease do look up online. We have shared all the information here using which you can figure whats good 🙂

Axis CRISIL SDL 2027 Debt Index Fund – Regular Plan – Growth. Is this a Debt Index fund ? My research says it is but nothing beats an experts opinion 🙂

Yup, it is like a target maturity fund. Check this – https://tradingqna.com/t/should-you-invest-in-bharat-bond-etf/123159

Thanks Karthik for your suggestion. I have enjoyed a lot reading all the modules. Thank you so much for sharing all this wonderful info!!

Keep up the great work!!

Happy learning, Arup!

Hi Karthik, it was a tweet. Below link explains about it –

https://www.bloombergquint.com/markets/michael-burry-explains-why-index-funds-are-like-subprime-cdos

I am worried about nifty small cap 250 index. Is there a chance of liquidity crunch in future in case of sudden mass exit?

Arup, if you indexing, I\’d suggest you stick to Nifty 50.

Hi Karthik, thanks for the awesome content. Michael burry commented that index funds are like CDOs and are in bubble. What is your take on that? Please explain your ideas in detail.

Did he justify why its a bubble?

Hello,

Very grateful and appreciative of the content your team produces- great stuff!

I have a question regarding the initial pricing of an index fund product – If two different banks/AMCs initiate or commence an Index fund product on the same date, will the issue price be the same? In other words, I understand that the price of Index Fund units fluctuate over time in line with the underlying NAV (ETFs see greater fluctuations intra-day due to demand-supply on the open exchange, but long term they too move in sync with underlying NAV) but could you shed some light on how the initial pricing or price-setting is determined for an Index Fund product by an issuer? Any additional reading links would be greatly appreciated! Thank you in advance

Rohan, most NFOs are offered at Rs 10. The AMCs collect funds during the NFO period and deploy them at the end of the NFO, post which the normal NAV calculation happens. This 10 is a reference number, it could be anything.

Hi Sir,

We are seeing a trend where new companies are emerging with bloated valuations. Even loss making or low profit companies are having so much market cap. Will this lead into a situation where many of these kind of companies will be in Nifty 50 (within next 5-10 years). In that case, relying on Nifty 50 index fund will be more volatile situation than today with more stable companies?

Thanks,

Kiran.

Bloated valuations do not necessarily mean volatile index right?

Thanks for the great contents from Zerodha,

I have questions in index funds, it would be great support if you can answer these.

As far as I heard, the index funds tracks the stocks listed in that particular index,

1. Suppose if I invest in NIFTY SMLCAP 250 index fund for long term, what happens if some companies in this index becomes listed in Large or Mid CAP indexes.?

2. How exit of stocks in a particular index affects the NAV.?

1) Any index is supposed to contain \’n\’ number of stocks, be it 30,50, or 250. The job of the index provider is to ensure that the number is maintained. If any company in the index gets booted out, it gets replaced by another company, ensuring the number remains constant in the index.

2) It wont have an impact. For example, if the fund has invested 30K in one company, and that company gets out of the list and replaced by another, then the MF sells 30K worth in company A and buys 30K in Company B.

Between Nifty 50 and Nifty small cap 50…which is better on the long term to invest?

I\’d prefer the large-cap 🙂

Where can i find the tracking error value of an index fund in coin app?

I\’m not sure if this is available on Coin.

I want to invest commodities cash into index fund from commodities account can it be done ???

and then pledge that fund for trading???

if yes then how, if not then make a common account.

Hi Kartik, Which are the Lowest cost index funds in India currently? also eagerly waiting for zerodha to enter into passive funds 🙂

I think UTI is one of the lowest, I heard Navi funds will launch low costs funds as well.

Love the article but the Vanguard graph shown was so confusing. What\’s on the x-axis and y?

Bhavana, its the number of funds on X axis. Y- axis is fund returns.

Hey Karthik,

I\’m pretty much new to investing in mutual funds. So, in order to kickstart things, I started doing monthly SIP from last month in index funds nifty 50 & nifty next 50. Now that nifty & sensex are all time high, should I continue doing SIP in these index funds on a regular basis or should I wait as market is very high?

The idea with SIPs is to continue doing it for however long you can. None of us can really time the market, so no point attempting it.

Hey Karthik,

When choosing index fund of a specific type (say, nifty50), apart from the expense ratio should we also have a check on the fund size?

On mint platform, I came across this statement, \”When choosing an index fund, make sure you go for the one with higher assets under management (AUMs). Higher AUM is better in case there is redemption pressure on the fund.\”

Currently, I understand that expense ratio is the only factor which needs to be checked when comparing index funds of a type. So, do we really need to consider the fund size?

Yes, the expense ratio matters but do keep an eye on the fund size as well, not that it\’s a game-changer, but it is a good to know metric.

Does zerodha providing sip ln index founds

Yup, you can do this on Coin.

If I can make a simple suggestion, can the most recent comments be shown first rather than old ones?? This would help us to have a go on the updated Q&A..(rather than of 2015 which i could see in some section).. thanks

There is very little that can be done about this. The only option is to move it to a different platform. We are thinking about it.

Thank you sir this reassures my conviction. 🙏

Happy learning, Udit!

Sir I’m studying for my CFA level 1 and am moving to London for my masters in finance. Along with my studies I thoroughly studied the material on varsity.

Now it’s time to implement theory into practice and I wanted some advise as if you were advising your own.

1) people say that every single trader leaves the market making a loss or barely breaks even. Is this true?

2) is stock trading really a sustainable way to create a passive/portfolio income? And by trading I mean futures and options too.

3) if the success ratio was SO low wouldn’t this be illegal like gambling?

And wouldn’t all hedge funds be out of business?

4) Do Fund managers do short term trading (such as swing or intraday), along with the use of derivates, for return maximisation?

5) In your personal journey, have you made more wealth through trading or by long term investing?

6) When you say long term investing through fundamental analysis, does that mean value investing (buying cheap stocks with potential) or do you do growth investing?

7) I was reading about your life’s journey of how you studied at EDHEC Paris, then traded, experienced the crash, saw the bullish run, basically seen it all done it all, what would be some golden advise from you at this point for us?

Something we should focus on more selectively in our journey further?

Some of these questions may seem very vague and naive but I wanted your perspective on the following.

Unfortunately the stock market has a very negative impression and I am facing a lot of discouragement for taking this route and so I thought there can’t be someone better to ask than you! 🙂

1) While this is true, there are exceptions to this. There are traders who have made it really big.

2) No straightforward answer to this. There are ppl who depend purely on trading but like I mentioned above, not everyone cuts it. Trading like swing trading is a much better form compared to F&O intraday

3) No, that\’s in fact the difference. Educated ppl trade, and ppl with no knowledge speculate. This is true in any market

4) Yes

5) I was never a great trader, just about average. However, I\’ve had better luck with investing

6) Yes, plus even simple things like staying invested in mutual funds

7) Chase what you are passionate about, and at some point, the dots will connect

Good luck, and I hope London favours you well.

Dear Kartik Sir,

Firstly thank you so much for all this life changing information free of cost. I am almost done reading every module from Varsity except G-Sec, it is phenomenally well made.

Sir may I have your personal email ID, or your company mail ID, I would like to ask you a few detailed questions which unfortunately are too long and detailed for this comment section. I would be very grateful if you can take out some time and go through what I have to ask.

Yours respectfully,

Udit

Udit, unfortunately, I cannot share. Please do ask here itself, maybe you can break it down into a few small questions and ask. Thanks.

Hi sir,

I am a resident doc, still very very fresh and new to the investing arena. Out of my monthly salary of 60k-ish, I invest 40k monthly in various equity funds. I have savings of about 2 months\’ salary. I\’ve been reading multiple sources which advise I should put at least 20% into debt/FDs but would it be wiser to invest in index funds?

Thank you for all your help sir!

If you are starting your career now, I\’d suggest you invest in Equities (like the Index funds), you can think about debt funds a bit down the land. Or if you are uncomfortable with 100% equity, then maybe 10 – 15% exposure to debt is good as well.

If 2 index index funds track the same index on what basis are different AMCs setting different expense ratios ?

How does one decide whic index fund to choose ?

Yup, just the expense ratio. You can also keep track of the tracking error which indicates how closely the fund is tracking the index.

Hi sir , I invested in ICICI Pru Nifty 50 Index fund as a retirement plan . I am planning to invest the same index fund in either UTI or Motilal just to prevent any risk if ICICI defaults in future( hopefully not) . But , as I researched more on this topic, I am thinking how would it be if I invest in Nifty Next 50 fund from UTI or Motilal because my portfolio already consists of ICICI Pru Nifty 50 Index fund and it invests majorly in IT and Financials .Whereas Nifty Next 50 is consisting more of Health Care and Consumer Staples. It would be a perfect balance in this way instead of having both Nifty 50 Index funds in my portfolio. Please let me know your thoughts on this . Thank you for the wonderful content !!

Nifty 50 plus Nifty next 50 is a good combination, Yash.

How to invest directly in Nifty 50 instead of Nifty 50 mutual fund?

You will have to create and buy the index yourself, it is a difficult task. Better to buy the Index fund.

Hello Sir,

What are the differences between the several nifty 50 index funds available??

All of them have their basis based on the Nifty 50 but are offered by different companies, so what makes them unique??

Hi. Can someone guide me as to how can I invest in Index funds from Zerodha App. I am a beginner in investing. TIA.

Goto coin.zerodha.com and search for the index fund of your choice. Click on it invest the amount you wish to invest in.

Personally, 10-15% loss will be fine if leverage is 2-2.5x which I am intending to maintain

10% loss in that example will be 50K which the exposure funds will cover easily.

I am not saying I will invest 100% of my capital on 2x leverage on Nifty. But I am talking about investing let say 25-40% of my capital on Nifty futures contracts. I feel it will give a better than any index mutual fund.

Return wise there is no doubt, leverage enhances your returns. It\’s the risk bit I\’m worried about. Technically there is nothing wrong with it as long as you can manage the daily M2M, volatility, and the associated anxiety 🙂

Hello Karthik,

I have a question. Why should we invest in an index fund rather than future contracts which have leverage with a cheap interest rate (T-Bill rate) if we want to do it for the long term? Here is an example. For the example, I am assuming a constant CAGR of 10%

Suppose we have 2L money.

A) We bought 1 contract of Nifty worth 5L and paid 1L as margin. We also deposited 1L as exposure.

Profit after 1 year = (10% of 5L) – (3.5% T-Bill interest on 4L) = 50K – 14K = 36K

B) We invested 2L in an index fund without leverage

Profit after 1 year = 10% of 2L = 20K

As you can see, on a future contract we have 80% more profit even paying the interest. So why shouldn\’t we use that instead?

Varun, futures are a leveraged instrument. How will you cope up with the M2M loss in a situation where Nifty cracks 1% on a daily basis for say 8-10 days?

Hi Karthik,

I have checked in my end as well that uti nifty direct fund is having 0.1% expense ratio which is lowest amount other funds in same category and also this fund exists for almost two decades. But why do index funds have standard deviation as different between funds, for example uti nifty fund is having SD as 23% and Taurus nifty 50 fund is having 19% , shouldn’t be the same or very little difference in SD between these funds since they track same index ?

It should be similar, but there are multiple factors at play – fund\’s demand and supply, rate at which stocks get bought for the fund etc.

Hi Karthik,

Good Day. I have few questions regarding index fund and other general doubt

1) When picking nifty 50 index fund, can we look at only factor of which index fund is charging lowest expense ratio ? Will that be enough or do we need to focus on any other parameter because all nifty 50 index is going to track the same index ?

2) Even with index fund do you suggest to diversify between two fund houses say like sip of 15k in uti nifty index fund and sip of 15k in icici nifty 50 fund for next 10 years ? or if i pick only uti nifty fund for sip of 30k for next 10 years will that be good too ? Please let me know your thoughts

3) Will there any drawback if i choose to go with folio mode than demat mode ? Can you help me with any major drawback with folio mode over demat mode of holding mutual fund units as you know please ?

1) Yeah, go for the one with the lowest expense ratio. Maybe its the UTI one, pls check again and don\’t take my word for it 🙂

2) Tricky, but yeah, why not. Just to hedge yourself against an institutional risk

3) Not really. I like it the DEMAT way because of the convenience of no paper work. Also, worst case I can borrow easily against it.

Sir if I put one order of 5000 rupees

Or 5 orders of 1000 rupees each for uti index fund units make any difference on charges . Like does it cost more charges in latter case or doesn\’t matter .

It makes a difference based on when you place the order. If on different days, then you will get different NAVs.

Yeah, I understand. But overall, can it perform better than just simply holding index fund? This strategy will outperform the index when index goes down, stays flat, or moves up but stays below our call strike price. Only in months, when index rallies above strike price, then it will underperform. Even then, we will not lose money because the amount lost on short call will be offest by gains on our index fund holdings.

Option P&L is non-linear, you can\’t really assume a 1 is to 1 pay off between the index fund and short CE.

Thank you so much Sir for your explanation.

If you dont mind I have a couple of questions more.

1- What is your recommendation to someone like me who wants to make career in the market? Please dont recommend getting CFA certification as it is not my cup of tea:)

2- I have a strategy in my mind. Please tell your views on it whether it is viable or not. Basically, the strategy is like doing Covered call with index fund. We invest sufficient amount of money in Nifty 50 index fund and sell equivalent Otm nifty50 calls so that apart from index returns, we can generate some extra returns from writing calls. Does it sound practical? If yes, how much extra return should we expect or aim for?

1) CFA is great if you want to target \’fund manager\’ kind of roles. Else you can always look at FRM, CAIA, or CFP.

2) Yeah, lots of ppl do this. The problem is when it blows, it will eat away all the premium you\’ve earned.

Thanks Sir for replying.

I have a few questions.

1- I think those people who know it\’s difficult to beat the markets and they\’ll be better off to invest in index funds still invest (or trade) directly in stocks just because of their passion and thrill. Just like gambling in casino when we know odds are against us, but we still play for fun and if we get lucky we will get some extra money. What\’s your view on this?

2- What percentage of your overall portfolio goes in direct stocks? And what has been your experience of direct investing and trading? Were you able to outperform the markets?

3- It amazes me how big of financial ecosystem exists to try to beat markets. Advisors, analysts, PMS, catchy softwares, etc. Are they all pointless when in the end they can\’t help you make extra money?

4- I am a student of B.com Final and I am very much interested in markets and want to make them my profession. But this theory that it is extremely difficult to outperform the markets puts me in doubt. Because again all these advisors, analysts, etc., seems pointless if we believe in this theory. Then what should one do who wants to make career in markets?

Sorry for so many questions but I will be grateful if you help me clear my doubts.

Thanks.

1) This is true to some extent. However, there are people who are passionate about fining multi-baggers and investing the long term as well. Of course, there are good traders as well

2) At least 30-40% is in direct stocks. I\’m fairly decent with investing, but I was an average trader, neither made or lost money, I just survived

3) No, there are many folks who need help with investing, retirement, and other goals. Beating markets is the cherry on top

4) Market exists because the profile of each investor is very different, cant have a single product and expect everyone to just lap that up. Bigger the market, diverse is the set of offerings, and hence the opportunity to create stuff.

Thanks sir for this amazing work.

My question is when even professional fund managers with so much resources and experience can\’t beat the market, then where do retailer investors stand? Why people spend so much time, energy and money to try to beat markets by investing directly in stocks? Shouldn\’t everyone just stop all trading and investing directly in stocks and just invest their money in index fund?

That makes sense to a large extent. I do that myself. However, apart from investing in Index funds, I also have a small portfolio of stocks and at times take up positional trades in stocks.

How to purchase indexes like S&P BSE SmallCap, S&P BSE – 200 index and S&P BSE – 100 index. Which ticker symbols we need to use?

Is it possible to invest in mutual funds (both active and passive) from our Zerodha account?

Yes, please do check – https://coin.zerodha.com/

Dear Sir,

1. Which is best Index fund for Long run like (10 or more years)…to get good benefit and which have lower Expense ratio?

2. If I buy index fund for weekly basis instead of one time, is there any advantage over single buying, your views please.

Regards

Asit Rathod

1) Have laid out the entire analysis toolkit for you, you will have to figure what works for you :). I\’d suggest you pick the one with the lowest expense ratio

2) On a weekly basis, you get to average out more. Thats it.

hello sir

\’\’You can technically create an index of companies whose name starts with the letter G \’\’ what does G means here ?

It is just an example, Rajat 🙂

Sir,

Is it better to purchase directly Nifty ETF stock in place of Index Fund ?

Yes, you can.

Thanks.

I am a doctor and I am still understanding all the concepts. Hats off to you for such lucid and crisp description of each financial concept.

I will surely ask all my colleagues to go through this educational platform.

Happy to note that, Doctor!

Can you please explain ETF concept and benefits of it.

Will try and add a chapter on it soon.

What is the difference between buying an ETF directly through a trading account and buying an index fund from platforms like Coin?

The difference is the way in which both are managed. An index ETF is traded on the exchange and can be bought and sold like a stock, an Index fund, on the other hand, is managed by an active fund manager.

Usually, I find it quite baffling to understand finance and related subject. I was trying to understand on how to plan for my retirement via investing options. These articles are quite simple and the narrative style is easy to understand and accidentally I ended up enjoying the read. 🙂

Thanks for the kind words, happy learning 🙂

What are a few of the good Index funds that I start SIP of 5000 rs for the period of 15 years?

Do check out the UTI Index funds.

Kartik sir

Wishing you a belated happy New Year…

1. Thanks for introducing us to world of finance /capital markets.

I just wish I had some one like u to guide when I was young.. Though it\’s not late now… Thanks to varsity.😁

2. These topics should be introduced for mid level schools and colleges. It\’s shocking to know that many ppl have zero knowledge about MF and finance

3. Any way I am planning to book partial profits from my existing mutual funds and investing this profit in index and small cap funds? I have been thinking about this for quite some time and I have not been able to come to a decision.

I know mutual funds are beneficial for longer duration, power of compounding etc

As you know no one knows when this bull run will subside… I just wanted to know if this is advisable?

1) Thanks so much for the kind words, Shyam 🙂

2) I completely agree with you

3) Please do check this chapter – https://zerodha.com/varsity/chapter/the-mutual-fund-portfolio/ 🙂

what do you mean by instituitional risk?

The risk of one institution going down 🙂

Thanks for very good material. I am a regular investor in MF using Coin Platform.

Between Index Fund and Index ETF – which one we should consider?

I know the advantages (Low cost, Slightly High Return, Can be bought at market price) and disadvantages (No SIP) of ETF. What you think should be a better choice for long term corpus building?

I also see more innovations in ETF (like with different themes) – though not sure whether they are successful.

What you suggest Index Fund (Hassle free) or Index ETF (for lower cost and slightly better return)?

I prefer ETFs, but unfortunately, ETFs are not very liquid, hence Funds are the next best bet.

Thanks Karthik! How do you feel about having the NASDAQ 100 index fund in the portfolio?

Will reserve my thoughts as I\’m yet to look at it in detail. But I think that should be ok, end of the day it is a thematic index with a focus on tech business.

Hello Karthik,

What is the pros & cons if we buy an Index Funds from a trading account instead of investing through MF since we don\’t want any kind of analysis, so by doing this we can save the expense ratio cost right,

What is your viewpoint?

Direct funds are always cheaper in terms of expense ratio. I\’d suggest you buy the index fund from Coin.

How can i buy Index fund through Zerodha. Not an ETF only Nifty Index find

Check for the fund you are looking for in Coin and you should get it. https://coin.zerodha.com/

Thanks Karthik. Index funds seems to be a good choice for conservative investors. However, I see that the Motilal Oswal NASDAQ 100 fund has a high risk in the riskometer. I\’m not sure why is that.

https://www.motilaloswalmf.com/mf/nasdaq100fof/

Because these are equity investment right? Equity is the highest risky asset.

Hi

First of all, I want to thank you for sharing such invaluable information all in one place.

I am always interested in Index funds and wanted to invest in them but I have a few questions regarding Index funds. Hope you will help me with this. 🙂

1. I can see the maximum period to invest is 25 years. Can\’t I leave it for 30 years or more?

2. Are the returns of all the index funds offered by many issuers the same?

3. Is there a possibility to check the returns offered by each issuer or an option to compare between issuers?

1) Of course, you can 🙂

2) Yes, may vary by a small %

3) Yes, you can use the compare feature – https://coin.zerodha.com/compare/14058300.00206600

This entire series is fuelling the paradox of skill XD

🙂 Do I take that as a positive comment?

Why there is no pdf for module 11 and module 12

Module 11 is work in progress, PDF will be done once its completed. We don\’t intend to put up the PDF for 12.

Sir,it would be very helpful if you could give much more details on the ETF market and how does it function which is much more prevalent in today\’s scenario ?

Noted, will do that.

Sir,

Do you suggest Parag Parikh Long Term Equity Fund?

I like that fund. You need to include the fund in your portfolio after a thorough due diligence.

When we invest in Nifty 50 companies we receive dividends. So when we invest in index funds do we receive dividends?

The fund does, which gets reinvested back to the fund.

Considering the sheer market voilatility specially in the current scenario(global pandemic etc.), isn\’t SIP in a Large Cap MF a better deal than in an Index fund. Ofcourse one could say that it\’s a long term horizon, but still what\’s your opinion on this?

You need to have a much larger time frame when doing SIPs, don\’t have short term market volatility/gains in perspective when starting SIPs.

When I buy a SIP of MF through Coin(Zerodha) at 10AM, what time\’s NAV is considered? As it shows as \”processing\” even till 3PM.

If the order is placed before 11:30 AM, you get the same-day NAV.

1. Since Nifty is under 11000 mark now, would it be a wise decision to buy Nifty Index Mutual Fund now

2. Which Index MF has least Expense Ratio

3. Should I put a lumpsum amount (considering the market crash), or still SIP is recommended?

1) YOur call is as good as mine. For this reason, I always prefer a classic SIP 🙂

2) I think UTI has the lowest expense ratio

3) SIP

Karthik sir, first of all Thank you for doing such a tremendous job! I have probably learnt more valuable things from Zerodha varsity in past few weeks than I\’ve learnt my whole life. Keep up the good work. ❤️❤️

Coming to my question, can you tell me whether a Nifty 50 index fund comprises of THE TOP 50 COMPANIES of Indian economy irrespective of their sectors, or a few representations from all the sectors is mandatory? (eg: top 5 from Banking, top 5 from Pharma etc)

Soumik, thanks for the kind words. I\’m glad you liked Varsity. Yes, Nifty 50 consists of the top 50 stocks in the economy.

Thank you, This was very informative.

The entire series on Debt funds and index funds.

Have you somewhere explained the differences between liquid funds and LiquidBees. When would somebody choose one over the other.

I dont think I\’ve done that yet, Vikas. Will try and do that soon.

Sir what is tracking error in mutual fund? And how it is calculated on the basis of different parameters??

Will discuss this in the next chapter i.e. chapter 22.

Hi Karthik,

How does dividend payouts differ between a Nifty 50 index ETF and Nifty 50 Index Growth Mutual fund?

My aim is long term investment, with my dividends reinvested to back into the ETF/Mutual Fund. Which one is better for me?

In both these, the dividend is reinvested.

Yes sir.

Hi,

You quoted \” On 5 years, 82% of active large-cap funds have underperformed the S&P BSE 100 index, which consists of the 100 largest Indian companies by market cap.\”,

-> Is there any data by comparing with Nifty Index 50, it might have performed even better, do you have any such data.

Index fund is wrt to Nifty 50 no?

Hi i have a query if i want to trade on etf then do i need margins to buy and sell them ?? is trading ETF and options are same ?

You will have to buy ETFs with 100% cash. No margins here. No, ETFs and Options are very different instruments.

I have seen most of the large-cap funds hold the same kind of stocks from the top 100 companies. You are right they don\’t have much to choose just the holding percentage to adjust. Should we keep more than 1 large-cap MF in our SIP portfolio or just keep 1 largecap fund with 1 index fund and other midcap multicap funds.

The only risk you need to worry about is the institutional risk. 2 large caps are required to hedge away the institutional risk, else there is no real need to have multiple large cap funds.

Hi

You mentioned that index funds just follow the benchmark they have like Nifty 50 or 100.

Here what actually mean by just follow the index. (Like index will go up and down so they do with their finds)

Follow means the returns are identical across Nifty and the Nifty Index funds.

hi sir i have a doubt which is better to invest in gold ETF (equity) or in gold ETF mutual fund

Gold ETF, but I\’m not sure about its liquidity. Please do check that bit, else you can even look at the SGB.

Thanks a lot for your advise Mr karthik. When is the next chapter on MF coming?

Maybe end of next week, Doc.

Hi

Hey!

Dear Karthik,

Many thanks for your kind words and your advise for my portfolio.

I am planning to give about Rs.10,000 / month to my son to start investing. He is 19 year old, doing his medical school.

I did\’t want him to do the same mistake I did!!!

Kindly advise what he should do for investing in what kind of mutual funds ?

He is doing some research as well and waiting. to read your future articles on MF portfolio construction

With regards

One thing that can do considering his age, I\’d suggest to experiments with a long term buy and hold stock portfolio. He can create a portfolio of top 20 stocks and keep investing in the same portfolio every month.

I\’ll try and put up the material soon 🙂

HI karthik, It was wonderful to read all your articles on personal finance.

Great way to educate in a simple terms and excellent example.

Some one rightly said that doctors know only know how to earn. Being a doctors in 50+ hardly had any knowledge about the investment till recently.

Being in the middle class Indian family I was are always kept away from investment opportunities and discussions.

Now I told my son to read about Zeroda varsity and to start investments.

I have recently started few mutual funds and stocks.

Since I have started (last 1-2 mo) quite late and have only about 8 years for retirement from a teaching at University hospital,

So to have a decent retirement life ( current monthly expenses about Rs 50000), kindly advise how much should I invest in MF and stocks. Also kindly advice on kinds of mutual funds to invest in.

Looking forward to read future articles. Thanks

Doctor, thanks for your message. I have massive respect to all the doctors and other Govt officials for relentlessly working during these testing times. So thank you so much for that! I echo your thoughts, I too come from a middle-class family and my mother is a Doctor as well 🙂

Since you are starting late, I\’d suggest you don\’t keep 8 years as a target. You need to have a longer time frame. Avoid direct stocks, this can be very risky for you, but do encourage your son to figure this out with small amounts.

Stick to Mutual funds, maybe about 60% Equity and 40% in the long term GILT Fund. Wishing you all the very best!

WHAT HAPPENS TO DIVIDENDS PAID TO STOCKS WHICH ARE HELD BY MUTUAL FUNDS? ARE THOSE DISTRIBUTED AMONGST MUTUAL FUND INVESTORS?

No, these are ploughed back and gets reinvested (growth funds).

Well written chapter.

Should i invest in Niftybee or Index Mutual Fund? It hasn\’t been explained, and i see varied views of expert on it.

I\’d prefer a low-cost index fund, Monal, simply because the funds don\’t have liquidity issues.

Delta neutral (market neutral)means almost same delta for both options,ignore delta positive ,i was mentioning option buying

First two weeks of the month time (theta) is not very effective in the market for monthly options.During these times hedge by buying options wait for a 30% return and square off both. worked perfectly on june because of the bull run in the first week.call option outperformed put Option on the first week itself and got 40% profit .strikes were 19500 ce and 18500 pe.I bought both on may 28 at market open , end of the june expiry (june 25th).If you got time please check the graphs

Straddle or strangle with option buying.

I am not waiting for expiry but a target of 30% investment return .i got it on june but have to clarify for coming months

Sure, but do ensure you paper trade this and ensure you are comfortable with all the expected behaviour.

Sir please hear out my strategy

I will buy nearest otm strike of highest OI put and highest oi call option , mainly a perfect even number strike on the beginning of the month.Expiry is at the end of the same month.A delta neutral,delta positive strategy. since it got good OI any movement will give me profits because i am delta positive (gamma will help me),time is with me because of the one month expiry(theta is small ) i am not interested in buying vix suggested option strike because vix also changes hence the nearest with best oi or perfect even number.I will not hold on till expiry, my target is 30% investment return,I will square off my trade and do same in the next month.A simple straddle or strangle

Since its a monthly trade it will take me years to backtest .please verify my strategy and point out the mistake.Do share your strategy aswell ,i know its not fair to ask a hedging strategy but still

You need to post this question in the relevant section of Varsity, this is a topic on Index fund 🙂

Anyway, what do you mean by delta neutral, delta positive strategy? I\’m not sure if I understand this completely.

hi karthik .

where can i compare funds .(index funds).do u have this features in coin .or any other source

Yes, you can compare funds on Coin – https://coin.zerodha.com/compare/14058300.00206600

Just Gold(SGB, ETF, DIGITAL) & ETF left.

Can you explain Why gold ETF & digital gold price difference is so high currently ?

ETFs are not so liquid Kunal, hence the pricing difference. Btw, digital gold, if I\’m not wrong, has a high markup. I think SBG is the best way to invest in Gold.

Hey karthik

From June 1 Nse brought new margin framework, Nitin send us the circular but there it\’s mentioned \”Price scan range which is used to determine F&O margins is now changed to 6 sigma from 3.5 sigma\” . Can you tell me how prie scan range works and what is sigma hear and how is 6 sigma batter then 3.5 sigma . (Am i right the sigma what we read in varsity it is the same one)

Thanks

Arun

Price scans and sigma are different from what we have learnt here. These are technical terms, mainly applicable to the exchanges and brokers. You need not have to worry about this.

Hi Karthik,

What happens in the scenario when a Nifty-50 company gets delisted from the index. Does the index investment change or anything? Needed some clarification on this please.

Regards,

Vivek P

Yes, the index fund manager will have to make the necessary changes in the index fund.

Is this a good time to be investing in any Index or Equity based Mutual funds?

Yes, as long as you\’ve committed enough time for such investments. Don\’t look at it from a short term perspective.

Hi Karthik,

You have written,\” As for small-caps, active or passive, I don’t think investors should invest in these funds at all.\”

This means we shouldn\’t invest in small caps at all? I was in impression small funds are good as returns are going to be higher(with high risk) due to unexausted growth opportunities.

Regards,

Jalpa Jain

Ah, I will have to reword this 🙂

Karthik I am a little confused with the concept of \’Clean EOD Data\’. Three questions

1. What does the term clean data imply? How is this different from the free data we download from NSE website?