5.1 – Assumptions

We are at an exciting point now. The previous chapter helped us estimate (roughly) the corpus required for one to retire comfortably, without drastically changing the post-retirement lifestyle.

One can argue that certain aspects were overlooked while estimating the post-retirement corpus, which is ok for now because this helps us determine the retirement corpus on a conservative basis.

The idea, of course, is to understand personal finance so well that we can plugin things as we progress and eventually get the corpus number right.

In the previous chapter, we figured that we need roughly 7Cr by retirement; in this chapter, we address the technique to generate the same. It must be quite evident to you by now that to create the retirement corpus by the target retirement year; we need to make investments starting today.

The investments that we make today should ideally spread across multiple assets. This is called the multi-asset portfolio, which includes – fixed deposits, gold, real estate, equities, cash, and cash equivalents. The overall growth that you experience will then be an aggregate across all these assets.

Let me explain a bit more before we get back to the retirement problem. Assume your net worth is distributed across multiple assets –

- 50% of your net worth is invested in real estate

- 10% of your net worth is in the fixed deposit

- 10% of your net worth is from gold

- 15% of your net worth is in equities

- Cash is 15%

The numbers assigned are all arbitrary, to drive the concept, so don’t sweat over it 🙂

Now, each of these assets grows at a specific rate. Needless to say that the growth rates differ for each of these assets. The question is, what is the overall growth given this portfolio of assets?

To answer this, we need to have an expected growth rate for each of these assets.

My long term (10 plus years) growth expectation (CAGR) from these assets are as follows –

- Real estate – 8-10%

- Fixed Deposit – 6-7%

- Gold – 8-9%

- Equities – 10-11%

- Cash – 0% (in fact cash de grows if you consider inflation)

You can develop your own opinion on the growth rates for these assets by looking at the long-term trends and by developing an idea on their future performance. But here is an advise, when you work with predictions/projections of any sort in personal finance, always keep the number on a conservative basis.

For example, frankly, I know equities, in the long run, will do much better than 11% CAGR, but I’ll work with a 10-11% range. The advantage here is that you build a future based on conservative assumption, anything better is only a bonus.

Anyway, the overall portfolio growth in the sum product of the weight of each asset and the expected return. Therefore –

= (50% * 10% + 10% * 7% + 10% * 9% + 15% * 11% + 15% * 0) * 100

= 8.25%

So as you can see, the combined (diversified) portfolio with multi-assets, generates an overall return of 8.25%.

Of course, change in asset allocation has an impact on portfolio growth. We have discussed this multiple times, won’t get into that discussion now.

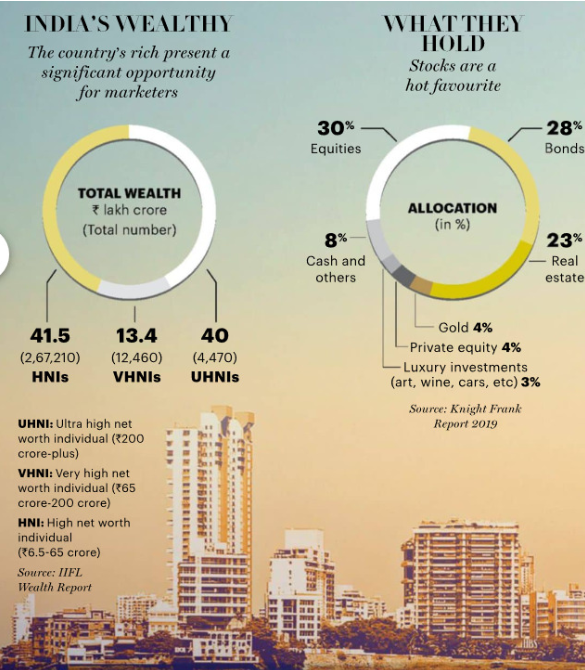

By the way, check this to know how people generally divide their net worth across a diverse set of assets –

The infographic above mainly talks about the HNI and above category; however, if you walk into any financial planning firm, you are likely to get a somewhat similar diversification plan.

While a multi-asset portfolio is highly desirable, we won’t get into that discussion just yet. This is slightly complex, and we are too early in this module to talk about it.

For the retirement problem, we will make one fundamental assumption. The assumption is that we will look at only equity for building the retirement corpus. The exposure to equity is in the form of making systematic investments in a growth-oriented equity mutual fund.

If you do not understand ‘systematic investments in a growth-oriented equity mutual fund’, then do not worry. Going forward in this module, we will discuss this in detail.

Since equity is the only asset we are dealing with in this retirement problem, we need to assign an expected growth rate to this asset. I think a 10-11% CAGR is a fair expectation, especially when the holding period is long, i.e. more than ten plus years.

So let’s work with this number for now.

5.2 – The setup

A quick recap of the retirement problem, before we proceed. In the previous chapter, we figured that we need funds to the tune of 7Crs to lead a comfortable retired life. We call this a retirement corpus. We defied ‘comfortable’ by ensuring we have at least Rs.50,000/- per month for the 20 years post-retirement.

The next step is to figure out how one can generate a retirement corpus. Remember, we are starting our journey to save for retirement today, and we have 25 years to build this corpus. Twenty-five years is 300 months.

For now, we will rely upon investing in an equity mutual fund, in a systematic way to generate this retirement corpus. To solve this problem, we need to make a few assumptions. They are –

- We have a steady job which pays us a salary every month

- We are employed until the year of our retirement

- Our primary savings vehicle is regular investments in equity mutual funds

- We get yearly hikes in our pay

- Every year we will increase the investments in equity mutual funds by 10%

- The increase in savings happens every January

I know many of you may be concerned with these assumptions here, especially about the job and the hikes, but then, that’s an underlying assumption, without which we cannot proceed 🙂

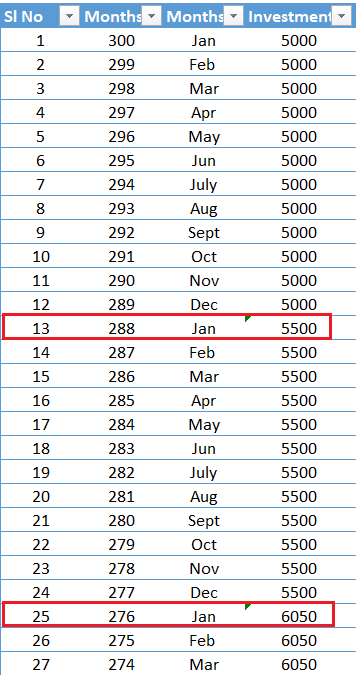

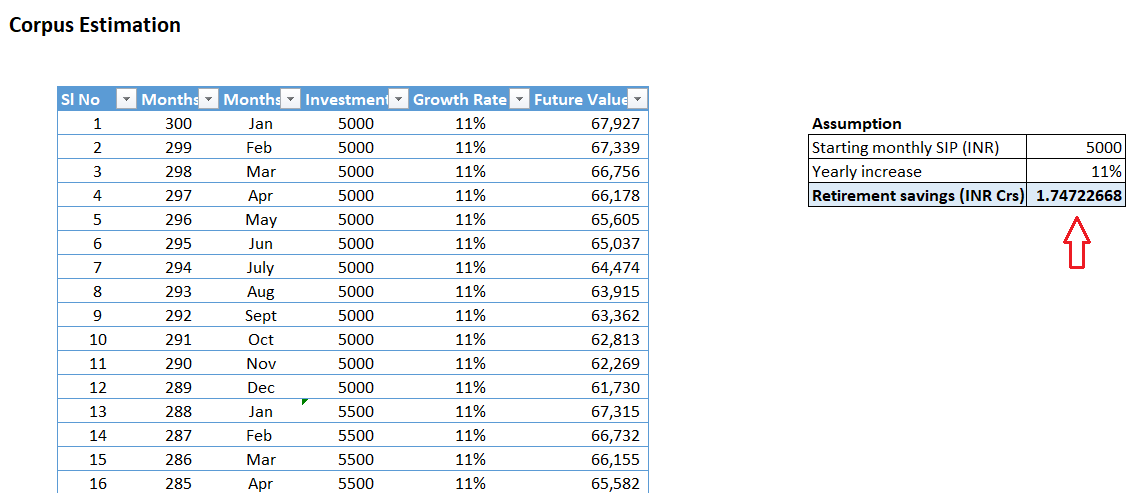

So how do these assumptions translate to action? Here is how it looks –

Let me explain this table. The very first row reads like this –

It is January, and I’m making my very first investment of Rs.5000/- today. I won’t be touching this investment until I retire, which is 25 years away or about 300 months away.

The 2nd row reads similar – Its February, I’m making the 2nd savings installment for the year, i.e. Rs.5000/-. Retirement is now 299 months away.

I want you to recognize the fact that the ‘months away’ can be looked at from a different perspective. If you realize, these are the number of months during which your money can grow. For example, the very first installment you make has the luxury to build (or compound) for 300 full months. The next month’s savings can grow only for 299 months, 3rd installment has only 298 months to grow. So on and so forth.

Now, the 5th and 6th assumptions state that we are increasing the savings rate by 10% every January. This means, if we are starting with Rs.5000/- for year 1, the 2nd year we bump this up by 10%, hence for the 2nd year we invest Rs.5,500/-.

This is how it looks –

The month counting continues the same way. For example, the Rs.5,500/- investment we make in the 2nd year January has only 288 months to grow or compound.

I hope you get this flow for now.

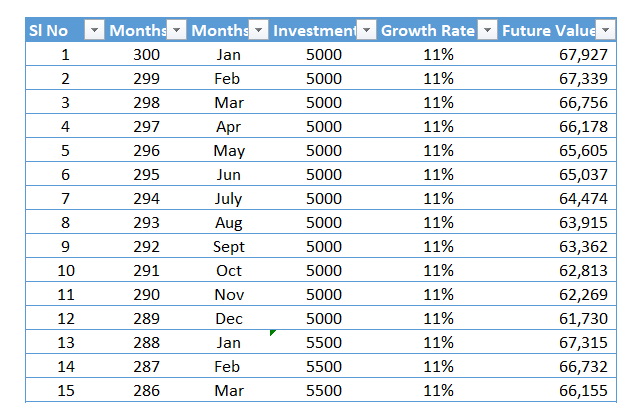

So what happens after you make these investments? Well, as per the assumption, each of these monthly investments we make, grows at 11% CAGR (compounded annual growth rate), for the respective months.

For example, the very first investment that we make, i.e. Rs.5000/- gets to grow at the rate of 11%, for 300 months. So what would be the value of this investment at the end of 300 months?

Well, by now, you should recognize that we can apply the concept of the future value of money and get the answer. The future value of money formula is –

Future value = P*(1+R)^(n)

Where,

Principal (P) = Rs.5000

Growth rate (R) = 11% per annum

Time (n) = 300 months. However, this formula considers time in years. Hence we need to express 300 months in years, therefore 300/12 = 25

= 5000*(1+11%)^(300/12)

=Rs.67,927/-

Let us do this for the 2nd installment as well; everything stays the same except for the time component –

= 5000*(1+11%)^(299/12)

=Rs.67,339/-

This is how the table looks –

Now, if you add up all the future values, you get the corpus accumulated for your retirement. Before I show you the number, what is your guess? Does Rs.5000/- as the starting amount make the cut? Do you think it gives you the target corpus of Rs.7Crs?

If you are doubtful, then you are right. It does not cut the mark. It’s way off the mark –

So what should we do? How do we ensure we reach the target retirement corpus? Well, we can do three things –

- We save for a much longer period, say 30 or 35 years. However, this may not be viable as we won’t have a sustainable source of income for these many years

- Increase the rate of return, maybe from 11% to 14%, but then is like robbing yourself of your future. So we won’t commit this sin

- Increase savings, this means a frugal life today for a comfortable and financially independent life tomorrow. This is an option we can work with this.

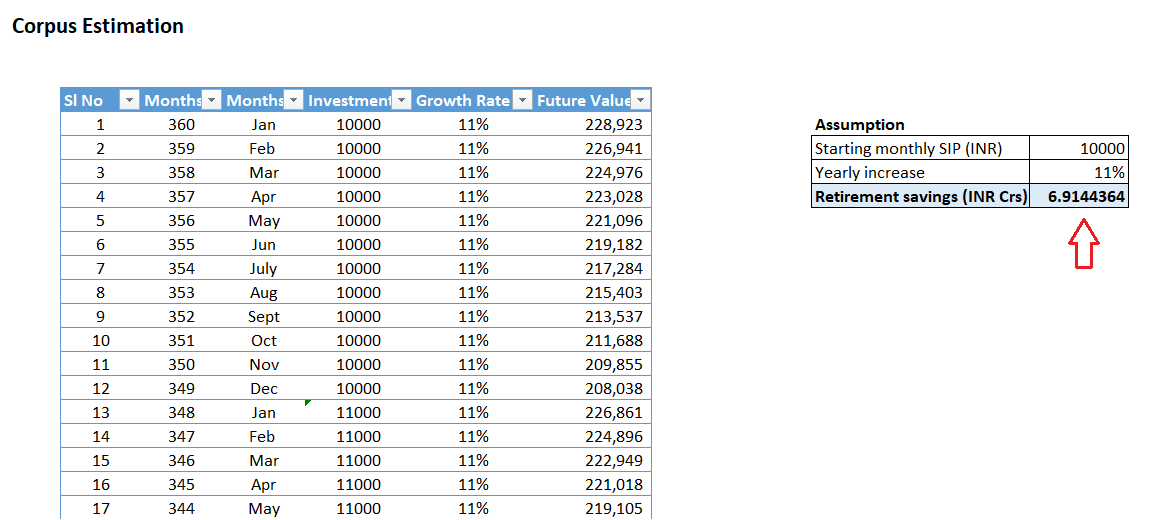

So from saving Rs.5000 per month, let us bump this up to say Rs.15,000/- per month. Here is how the numbers stack up –

There is a significant improvement, but still not close to the 7Cr mark. We can try this with Rs.20,000/-

As you can see, starting at Rs.20,000/- per month, we get close to the 7 Cr mark, which upon retirement will yield us Rs.50,000/- per month for 20 years.

5.3 – Are you serious?

Saving Rs.20,000/- a month, that too as a starting amount may sound crazy to many, especially for people who are just starting their careers. After all, you’ve just started your career, started seeing a steady cash flow, and you are expected to park the bulk of it for retirement?

How fair is that?

Before it demotivates you any further, let me tell you. It is not all that lousy 🙂

Let me make an assumption here; if you are starting your career now, then probably you are 24 or 25 years old. This means you have a long runway before you retire. Even if you retire by 60, you mostly have 35 years to retire.

Out of these 35 years of service, even if you invest for 30 years, you will be placed much better. You can choose to start with Rs.10,000/- per month. Check the snapshot –

Starting your career early, gives you two powerful levers to operate – time and money. You can start with a small amount and build on it, eventually, it will yield you a similar result.

What if you are in the middle of your career and you are looking at retirement sometime over the next 10 or 15 years? Well, unfortunately, you do not have many options except to save large chunks of your cash flow.

But remember, this entire conversation is an oversimplification to help us get started. There are many angles to this story. For example, you may acquire property by inheritance, which earns you a rental income for the rest of your life or you can get a huge lump sum amount at retirement, thanks to PF and stuff. This retirement amount gets parked in a savings account or a fixed deposit, which gives you yearly cash flow.

The objective of this module is to help you solve this puzzle so that you can plan your financials efficiently for yourself and your family.

5.4 –Next step

Irrespective of the lump sum cash or a yielding rental property landing up in your lap by retirement, investing in equity is something that you cannot miss. I firmly believe that ‘equity’ as an asset class will outperform all other assets and shine through. Equity has to be a part of your long term portfolio.

The best way to gain exposure to equity is by investing in mutual funds via a systematic investment plan. Of course, there are many other variants and techniques for this.

Given this, over the next few chapters, we will deep dive into mutual funds and get a thorough understanding of mutual fund investing. This discussion will include things like developing a mindset for mutual fund investment, building a mutual fund portfolio, goal-based portfolio, fund analysis, direct vs regular, growth vs dividends, etc.

Once we understand mutual funds, we will steer our way to learn other critical components of personal finance such as life insurance, health insurance, pension funds, EPF, ETFs etc.

So as you can imagine, we have a long learning path ahead 🙂

Key takeaways from this chapter

- In a multi-asset portfolio, the aggregate portfolio return is the sum product of the asset weight and the asset’s expected returns

- Equity exposure is a critical component in long term wealth creation

- Investing small amounts of money regularly leads to a massive retirement corpus

I have 40L in my savings account and 30L in FD (maturing sometime next year (2027)).

I want to start investing in market. Can you guide how to do it.

I have a government job. OPS Scheme.

Monthly expenses are around 30k, and salary after deduction (this expense of 30k and accommodation) is 1.2 L.

I want to put this 40L to work and to decide if 30L in FD (annual interest around 5.5-6%) is safe or should I invest in market.

Also, about SIP, how a person with govt. should invest in market.

Hi Mr Karthik

when everone says, 15% of your net worth should go into this asset or that, what is the net worth value actually. how does one calculate the networth ?

An individual\’s networth is basically all the investments (stocks, bonds, FDs, real estate, gold) minus all the liabilities.

Hi Karthik. First of all thank you for sharing the knowledge. It\’s been very helpful.

My doubt is, let\’s say we invested for 15 years and as you mentioned that the 1 Lakh per year is tax exempted, then in that case even if we invest 20k per month, it will be 2.4 Lakh per year. And I\’m sure there is no good chance we are going to get 1 Lakh returns per year for a long time(it may take more than 10 years). So, in this case the only tax that gets calculated when the money is withdrawn when the investment period is over. Is this correct? Or we will get that situation somewhere?

Gawtham, you are always taxed on the money you realize. This means you have to sell, and then on the profits, the tax will be calculated based on the tax rate prevailing at that time.

If I invest 5000 Rs in Jan 2025 and then invest every month and increase my investment by 10% annually for next 22 years what will be by corpus after 22 years with 11% growth rate?

After 22 years, with a starting investment of ₹5000 in January 2025, increasing by 10% annually, and growing at an 11% annual return (compounded monthly), your corpus will be approximately ₹1.21 crore (₹12,085,220). Why does your Excel calculation show 1.139 Cr?

Prajwal, you can check this – https://zerodha.com/calculators/

Please upload excel sheet used in this chapter.

Checking, not sure why we dont have it yet 🙂

The 11% CAGR that you mentioned it is the for the annual but why it is applied on the monthly value of 5000?

Its on a pro rata basis right?

HI Sir, I would like to ask a major doubt i could\’nt get the answer anywhere. I am 28 years old planning to invest for my retirement. In order to have a good asset diversification i have 15% allocated to debt for 25 years . Then slowly increasing to 100% for my retirement . My question here is in which debt fund should i invest at my starting stage(for that 15%) for long term debt investment.

is PPF good option? How should i park my retirement money?

Oh yes, PPF and NPS are good options too 🙂

Loved how you explained a real life problem in such an easy way….. Thanks a lot sir. I just have one doubt what did you mean when you said-

\”Increase the rate of return, maybe from 11% to 14%, but then is like robbing yourself of your future. So we won’t commit this sin\”

Thanks Chirag. So when you increase the rate, you achieve savings faster. However, my take on personal finance is that it is always better to be conservative than be aggressive with your assumptions.

Hi.

I am already a retired person since 2019. I have a penny pension amount which is not sufficient for my day to day expenditure. I have some FDs through which I am getting some monthly interest to cop-up my daily needs.

My question is how much amount should I invest in MF, lumpsum, so that I can get atleast Rs.20000 – 25000 per month. I mean to say what type of funds it should be Debt funds, hybrid funds, ELSS funds, Aggressive funds or what else? So that I may get regular income plus my hard earned money should also be safe and growth

None of the funds really offer any guaranteed returns, they all have market risk. I\’d suggest you speak to a professional financial advisor once.

There should be a \’Go to Next Chapter\’ button at the bottom of the page after \’Key Takeaways\’ so that after finishing this page we can go to the next.

Noted, Amit. We will fix it sometime soon.

Hi Karthik,

Thank you very much for making complex money matters simpler to understand. I particularly liked this bit below:

\”My long term (10 plus years) growth expectation (CAGR) from these assets are as follows –

Real estate – 8-10%

Fixed Deposit – 6-7%

Gold – 8-9%

Equities – 10-11%\”

Considering the pandemic and current market situation in 2023, curious to know what might be your updated long term growth expectations from these assets? Would be great if it seems possible to share. Thanks!

That\’s true but this is just for easier calculation i have taken the monthly amount of 5000 INR and multiplied by 12 months and tried to establish a formula.

Will that work and does it have to always be months only.

P*(1+R)^n

where n could be anything can be months, years right?

Please correct me if am wrong

N can be anytime period. But if you are taking months, rates too should be proportionately adjusted. But, the problem with what you are doing is that you are missing out the compounding for many months, which is very crucial.

Hello Karthik,

Can we use this formula for a year instead of calculating monthly. The below example is for 1st year

=60000*(1+11%)^25

Please advise if it\’s wrong can you please help me changing it.

Thankyou in advance

But investments are made monthly which needs to be accounted for right?

I was just thinking it will do wonders if somehow we can increase our investments in the earlier years rather than increasing in the later years. Karthik Sir what are your views?

Yes, but most of us have higher incomes as we head closer to retirement 🙂

Dear Karthik sir,

I came across Varsity a few weeks back, and until now I\’ve read 3 modules and I loved it. Thanks for sharing your knowledge.

I request you to make this excel file available, so that we can change the figures, and see the results as per our suitability.

Thanks a lot.

Glad you liked it, Bhargav. Will try and upload it.

Can you post the excel sheet

Will try and do that sometime soon.

This is what, I were looking for long time.

Very important topic and knowledge you covered here in simple and concise way.

Actually helpful content on personal Finance, which is now basic needs of everyone to survive happily. Thanks

Happy learning, Kanchan!

Hi Kathik,

Could you share the excel sheet used for the calculations in this chapter?

Hari, not sure why I\’ve not shared it (are you sure?), I\’m afraid I may have lost it 🙁

Looking forward to the excel sheet used in the current module. Great content 🙂

Happy learning!

I can\’t able to find the excel sheet😪

Sir There is time when Equity has given negative return for almost 10 year. Is it true

Yes, that\’s possible.

Hey,

Does this module not assume that we will stop investing our money after retirement?

It does right?

That makes sense. Also, that money doesn\’t necessarily needs to be in SB accounts. With that thought in mind I wanted to ask if you plan to cover investment options for retirees. (Sorry if you have already covered and I may have missed it.) I know a lot of people who may benefit from that and it would also give me an idea of what could be done with the corpus that has been accumulated.

I\’d probably do that in the 2nd half of personal finance, Anurag.

I tried to play around with the sheet and let\’s say for a hypothetical retirement amount the total corpus required at the end of the retirement year is 24 crores. Now wouldn\’t this amount be invested in somewhere and would be providing a reasonable return (even in let\’s say a safe investment). So for such a large corpus the return on the investment would be sizeable and help in the yearly amount required, right?

Thats right. But I\’ve not factored that in considering SB accounts in future will yield next to 0 plus to add some conservatism to our calculation.

Is there a downloadable corpus estimation excel sheet where we can play around with the numbers?

I think the excel sheet is put up for download.

Wonderful content sir…please upload the Excel sheets u used to explain the contents if u have uploaded already pls provide the link to download

I\’ve uploaded I guess.

The requirement of about Rs 7 Cr has been estimated to be in hand in the year 2044 , ie the year of retirement by investing Rs 20000 as monthly SIP in equity (with 10 percent increase in SIP every year) from year 2019 for 25 years. It is noted that Rs 7 Cr for post retirement life is not required in the single year 2044 itself , rather it is required over a long period of 20 years from 2044 to 2063. No doubt Rs 7 Cr estimated in year 2044 will not be parked as cash for next 20 years but definitely the entire amount or major part of it will be invested in suitable instrument or financial institutions to fetch interest or the value to grow . So with this , the person retiring will be leading more comfortable life meaning by he will be getting per month an amount more than present value of Rs 50000 as assumed.

Thats right, Anita.

Hello Sir,

In your opinion, do bank fixed deposits still have a place in an investment portfolio, given the very low interest rates? Do they have any real merit except for the psychological security of a conservative investor? Are they not fully replaceable by Liquid funds?

Thanks in advance

Not really. If your time horizon is 1-2 years and want capital safety, the FDs is still a good option.

Hi Karthik,

Please can you verify the equation.

I have gone through the comments and saw a few others also asking this

= 30% * 10% + 8% * 7% + 8% * 9% + 13% * 11% + 4%* 0

= 8.3%

If you calculate this, the answer is 5.7 %.

Would really appreciate if you can confirm or am i missing something

Thats right. Btw, I realised another mistake while checking this. I\’ll try and fix both, thanks for pointing 🙂

if we are considering that we have 360 weeks instead of 300, then corpos required will be more then 7cr.

Perhaps, I\’ve not checked that.

A small typo, I like to report \” I think a 10-11% CARG is a fair expectation\”. I think it should be CAGR, not CARG. Sorry if I am being grammar nazi.

Fixing this, Varun. Thanks for pointing 🙂

Got it. Just read your replies. You kind of overly simplified it.

Yes, with the intention of getting started, Gagan.

Sir, are we assuming that from the time of retirement, we are going to keep 7cr in form of cash. Won\’t it still remain invested. Its still gonna generate something for next 20 years. We would just stop adding to it.

Yes, it will be invested in a return generating instrument. But for simplicity in our understanding, we are going with the total corpus required.

Hello Karthik, First of all, brilliant and easy explanations. Thank you very much for that.

I was just doing the math and found that , if we start saving 20k Per month with a 10% increment every year, by the time we are saving on 24th year, we are required to save close to 2Lakh per month, am I getting this right? which means saving 24 Lcs to get 50K per month from next year onwards? And also, the returns which we are expecting from the next year, is that not taxed at 10% too? ( with the current tax rules?)

Regards

Keerthi

It works out to 1.79L per month or about 21L per year.

Its 50K for the next several years right? About the tax part, yes there would be 10% capital gains going by current rules.

still dont see those excel files 😛

Would love pdf version of this module please 🙂

Working on PDFs.

Hi Karthik,

I am about to retire in 10 years time. I would like to have some fixed-income (pension) after my retirement. I have looked around all the Annuity plans (HDFC, SBI, ICICI and other financial houses) and found that all of them charges a hefty fees (often 5 to 8% yearly). I have heard that Mr. Nithin (zerodha founder) is about to come up with pension and annuity plans that would charge far less %. Is it really so! Also heard that he has applied to SEBI and other regulatory bodies for permission.

If it is so Iwould like to put some hefty amount for the annuity plan. Please convey him to pursue the matter faster. I shall be waiting out for his annuity scheme to invest.

Thanks

Are you sure its 5-8%? That is quite a bit. Our AMC plans will take some time, it\’s at the hands of the regulators. We are yet to get the licence.

Hi Karthik sir,

I have a piece of land 2400 square feet in outskirts of Chennai and cash on hand around 25 lakhs. Is it okay to build house in that land using the cash and get then rental income ? Say like constructing 6 one bhk house and get the rental income. I already have one home to live. Also have sip in mutual fund for 10k going on around past 6 years. Have some money into direct stocks. Some money going into retirement account monthly. Is it okay to put money into constructing house for rental income ?

Ashok, I\’m not a real estate expert and I really don\’t know much about it. Not sure if I\’m the right person to take this advice from. If I were you, I\’d talk to a good RE expert in the Chennai area and take a call on this.

Good luck, Ashok.

Hi,

In Chapter 5 you have mentioned that you will discuss about – Life insurance, health insurance, pension funds, EPF, etc. Can you refer me to the chapter number where you have covered them as it is not clear from the Index items.

That will come up in Part 2 🙂

\”but then is like robbing yourself of your future. So we won’t commit this sin\” I didn\’t get that point. Can anybody help : )

The higher the return expectation, the lower is the investment required per month. But it does not make sense to increase the return as we are better off taking a conservative approch.

https://docs.google.com/spreadsheets/d/1PELKcsCPUk8X7dxsm3gBG8RRjGfhMuuv/edit#gid=1352582989

The excel file for the corpus calculator is shared in the link above.

Regards,

Dhairya.

Thanks, I hope ppl find it beneficial.

Hi Karthik,

I have made the excel sheet for the corpus calculator in the above example.

If you can give me your email id, I can mail it across to you and you can include it in the module for everyone\’s benefit( i see a lot of questions asking for the same)

Or else, my email id is mentioned along with this message, you can send me a mail and I\’ll be happy to send you the sheet.

Thanks,

Dhairya Trivedi.

Thanks Dhairya. That helps me save some time 🙂

Maybe you can upload the file on Google drive and share the link for everybody\’s benefit? Thanks.

Will be glad if you could do the same. Waiting.

Thanks.

Hi Karthik,

Many thanks for the excellent initiatives you have been taking to empower people towards meeting their financial goals.

Can you please share the downloadable excel sheet used in the corpus estimation?

Regards,

Dhairya Trivedi.

I\’ll try and upload the same.

Oh first cell write 500, in cell below that write 499, you may add one more entry below that for 498. Select all two or three cells depending on how many you wrote. Now with your mouse, clink and hold bottom right corner of your selection.while holding drag your mouse down to cells, your series will be filled up.

Sir what is the function in Excel for months

Starting from 500 to 1 month

If I use autofill function it comes like this 500,501,502………..

Can you guide me in this step

Maybe you should check out the date function? =date ()

Hi sir

Sir excel sheet for this chapter

Ah, I seem to have missed it. But its a fairly straightforward sheet, have explained the steps in the chapter itself.

What about the tax on retirement corpus?

As per tax bracket.

Can you please upload the excel sheet of above explanation. Thanks !

Will try and do that, Naveen.

Sir I\’m now student can I start investing as low as 100-200 every month or 1k for year

Yes, you can. Anything is a good start, as long as you can start 🙂

Sir I\’m undergraduate student if I get into work my starting salary would be 15000 I will follow 50% for basic needs, 20% for luxury and 30% of 15000 for savings which is 4500 will it help me starting my investment journey

Sure, you can. Maybe compromise a bit on luxury 🙂

One of the problems about being conservative at every step of the calculation means that we may make major errors due to the effects of compounding. For example, the retirement problem above assumes a 100% cash holding at the start of the retirement period: that is you hold cash for 20 years between retirement and death thereby giving up the benefits of compounding for 10-20 years. This makes the savings numbers look larger than they need to be, and may frighten some young savers!

I agree. The idea was to reintroduce this concept after discussing a few other financial products.

Hi Karthik ji

At the outstet thank you for sharing this valuable knowledge on personal finance, MF and other market instruments. I wanted to know your view on rate of return to expect if one invests in value stocks and leave it for 10 plus year horizon. I presume it to be similar as any equity MF (11-12% on conservative basis). Do you agree or have some other perspective which I am missing.

I\’d peg the expected returns from value stocks to much higher, but so would the risk 🙂

Can you pls publish the excel referred to in the above write-up?

Will do that.

Hello Karthik, Great going with this article and it\’s need of the hour as well –

Just one request, I see that this topic is yet to be available of Varsity mobile app.

Do we know on when it would be updated on the app as well?

This will be updated once this module is completed. This is still work in progress 🙂

Please share the Excel sheet.

Did we take 5000 pmt or PV? ( as we calculated Sip amt after 25 years?)

As we calculated by CAGR the answer for 5000 sip would be 5647652 ( as 5000 is in monthly )

Apurva, the excel is towards the bottom of the page. Search for \’download\’, and you will get it.

Hi Karthik,

The whole series of personal finance is just awesome. Eye opener.

Very well explained.

One question, where can I get this calculation excel sheet?

Thanks, Ashish. The excel sheet is available in the chapter itself, just search for the word, \’download\’.

What is the difference between Equities and private equity (ref. image shown of ideal distribution of investment)

Equity is listed stocks in the secondary market, Private Eq is investing in unlisted companies.

Hi Sir, great articles about financial education. Can you also cover the topics like how to identify a good IPO.

Will do that, Anish.

Hi,

Can you cover expense ratio. And how it will be charged annually with example?

Thanks

I\’ve done that later in this module.

Hi ,

In section 5.1, the overall portfolio growth as per the assumed allocation comes to 5.71% instead of 8.3%, can you please verify?

Regards,

I will, thanks. Btw, I will revisit this problem later in the module.

Thanks for the reply karthik.

Alternatives I meant, there are options like PPF, VPF, NPS also (of course with limitations like lock-in period, liquidity, less returns compared to equities etc) Let\’s assume am not going to touch the money until it\’s maturity. So now, what % of investment should I have in these instruments vs equities? For the sake of stability.

Hard to give a generic number, but I\’d say about 40% in such instruments, rest in equity.

Hello Karthik,

I am 25 now. Provided I decide to invest 20,000 every month (with 10% increase every year) for next 25-30yrs, where should I predominantly invest for building this retirement corpus? I understand investing in equity over long term will be beneficial.. But because of this covid situation, aren\’t the past 10 year returns for some have been negative? And retirement corpus is a huge sum of money. I am skeptical to invest my hard earned money in something which will eventually eat up everything at last. Can you suggest best investment options for building this retirement corpus?

What are the alternatives, Janani? When you talk about 10 plus year time frame, your best bet is Equities.

sir, will you be uploading the calculator sheet ?

will you be uploading the calculator sheet? is there a place i can find it. i tried to make my own and i think i\’ve really messed up on a few formulas (or it\’s just a frightening amount…)

Search for \’download\’ in the page, and if the sheet is put up, you\’ll get find it.

sir, can you mail us/ upload this calculator sheet?

I will reintroduce this concept a little later in the module.

This is a very informative and helpful piece on personal finance in the internet. it addresses the much-confused issue on how to save for retirement. Thanks Varsity for putting up such info.

Additionally, I have a question on equity growth rate assumed in this article. The 11% p.a. growth assumed for regular MF investments, means by compounding at the end of 300 months it will be giving an absolute return of 1258% {i.e (1+11%)^(300/12)-1}. Similarly, 183% for 10 yr & 68% for 5yr. But, historically such high returns have not been observed and once invested, the amount gets the benefit of time while the returns are unrealised and not reinvested .So, do you think for equities we should go for \’per annum\’ growth assumption or \’overall/absolute\’ historical return rate?

Hello Mr. Karthik, I searched for the download link. It\’s not available.

I have a question: you\’ve advised us to increase the investments by 10% every year.

This will increase our investment from – Year 1 = 20,000

To –

Year 10 – 51,875

Year 17 – 1,01,090

Won\’t it be challenging to save upwards of 1,00,000 for 3-4 years consecutively? Even after taking the hike in salary into consideration.

Thank you.

It is, Akshay. I\’ll revisit this chapter again when we have introduced more concepts and notes, request you to wait till then 🙂

Very Nice Article . Thanks

Not able to find Download option

The download option will be available once the module is complete, Mohit. This is work in progress still.

Karthik,

Thanks, it was wonderful article. is it possible to share the excel sheet which you have used in this article or share the path, so I can download?

Thanks,

Rakshith

Can you search for \’download\’ option, it should lead you to the excel.

Awesome article,I will try to follow…Thx

Good luck!

I do not get it how did you calculate the total growth rate to be 8.3% ?

It happens to be 5.71% ?

You should take the sum-product of each the asset weight and returns.

Hello Sir,

Heartfelt appreciation your superb initiative for spreading financial literacy.

AS we are talking about retirement problem, what do you think about NPS. NPS also gives 50k additional limit under 80C and can have equity portion upto 75 %.

Isn\’t it must to have in portfolio?

Are there any drawbacks to it.

NPS is a great addition to the portfolio. I will discuss it in the coming few chapters.

Although, I already know what are these things mentioned in this chapter but i just loved the way you have explained it in so simple language.

Happy to note that, Shubham!

I did not get this —-

= 30% * 10% + 8% * 7% + 8% * 9% + 13% * 11% + 4%* 0

= 8.3%

How you got it..Please explain..

Still the excel sheets used in above chapter are missing…Kindly upload those excel sheets for easy reference…

It is a \’Sumproduct\’ of the investment weight and returns.

Sir,but asa rule we should never extrapolate the past to the future.There has to be independent reasoning to predict future trends?

Divyam, we will revisit this model again later in the module. The idea is to lay down the foundation.

1)why do u believe equity as a class will outperform all others?I have seen lot of graphs which say the gsec bonds have over 25 years done almost as well or better then nifty?

2)dor retirement calculation,we should convert all our calculation to money we will require to earn by end of working life-because in 20 years to retirement it can still give significant interest?

1) Over a long period, equities have always outperformed. Of course, this was challenged in recent times when even the 10-year SIPs went -ve.

2) Yes, but we have no insights into the interest rates, right?

Thanks for the advise. I may start with a small capital of 15Lacs for 1 year and then see how it goes.

Good luck, Narana! Hope this works well for you. Let me know if you have any questions with regard to options trading.

Hi Karthik,

Most of the expenses (school fees, clothes, shoes, electronics, restaurants, vacations, fuel) go down after retirement. Also inflation is not applicable for every product. If we closely observe, mobile phones, TVs, Laptops, clothing, shoes, cars and for many things , prices have not increased since 2005. Rather reduced. I agree on food inflation but that\’s not more than 10%-15% of total costs. So, will it not make sense to calculate retirement requirements taking a inflation of not more than 1%-2%. Even if we are at par with USA in next 20 years, just look at the cost of things in USA. Its not that expensive. If some one is able to buy a house for retirement in 30s and 40s, shouldn\’t such retirement targets scare him than help him…..My question is should we reduce the targets for retirement?

I am in mid 40s and would like to start trading in options . I want to become more of an option writer. Just finished 4 modules on Analysis, Futures and Options . Tonnes of thanks to you. Taking full advantage of COVID situation. I am NIT passout ECE, working in Sales and Marketing. A doubt keeps coming in my mind , whether its a right age to start Option Trading ? Even if I am able to make 1Lacs/month , that would not be able to replace my current income. Suppose I religiously trade in options for next 2-3 years, is it possible to generate a net income of 2L-3L/month after few years? How much investment is needed to generate this level of income ? Will it make sense to sell a flat and plot ( which is any way seems to be dead investment) and put it into options ?

rgds/Narana

Narana, of course, it makes sense to factor in inflation and a lot of other parameters before factoring in retirement. The one that I\’ve put up here is to help start the train of thoughts. We will revisit this topic when we have sufficient knowledge of various components that make up a retirement plan, guess I\’ve mentioned it towards the end of the chapter as well.

As far as options writing is concerned, all one needs is a month like April to wipe out all gains made along the year. Its very tricky and can be really hard to replace your main source of income unless you do it with a ton of capital and have a significant amount of risk management. Selling your property for this is a really bad idea. Even if its a dead investment, your capital is safe, with options, that can also get wiped out in a month 🙂

Hi Karthik,

Thank you for the clarification. Look forward to understand the other angles and concepts

Hopefully soon 🙂

Hi,

Don\’t you think that the corpus of 7Cr will also keep growing year over year? And considering the growth rate of 8.3% illustrated in this chapter (with the asset allocation) will generate 58L annually. Whereas the requirement at the first year of retirement is barely 20L. So, the return of 38L is added back to the corpus of 7Cr. Isn\’t it a very conservative (or safe) approach to build such a huge retirement corpus which also seems to be impractical? In my opinion, 3Cr corpus is good enough to generate 25L returns and after expenses of 20L still has a surplus of 5L which goes back to the corpus. Am I wrong in my assumption?

Sumanth, yes, that matters and there are other angles to this as well. I\’ve kept it straight forward for now, as we develop more and introduce more concepts, we will reintroduce the retirement problem and rework on it. This chapter is to just kick start the thought process.

Thanks for your response. I\’m looking for the excel file to check the accumulated corpus values with different initial conditions. I understand the PDF will only be published after the completion of the module.

Ah, Vivek not sure if I had saved the excel, looks like I only too screenshots 🙁

Hi Karthik,

Great work with all the modules. I couldn\’t find the link to download the corpus estimation excel sheet. Can you please share the link here.

Thanks

This module is work in progress. The PDF will be available once the module is complete.

* Karthik

Thanks Karthok. I understand & appreciate your point.

Welcome!

Hi Sir.

Can we trust mutual funds for such a long time and put big chunk of our income in such schemes for this long?

Yes, they are all highly regulated entities. So far there have been no bad incidents in the MF industry, so we all hope for the best 🙂

Your retirement corpus calculation is not correct. You have not escalated current monthly expenditure 50k with inflation rate to get expected monthly expenditure when person retires. You assumed same expenditure at retirement age and then taken inflation rate for post retirement period. Secondly, post retirement if one invest the retirement corpus in bank @7% then inflation at that bulk amount will be taken care by this bank interest. Thirdly, you are expecting that after life span is over the person will leave a big amount to his nominees. Whereas the value of retirement corpus will be reduce drastically from 7 Cr, if you consider as diminishing balance and will become zero after his demise. For safety life span can be taken 5 year more if felt by anybody.

Kumar, I\’m aware of all these points. It is just that I dint want to complicate the retirement problem at the start of the module. The idea is to introduce different concepts and then revisit the problem again for better understanding. For this reason, in the chapter, I\’ve mentioned that the solution is an oversimplification.

Hi Sir,

Any reason on why to increase sip by specifically 10% every year or was it just an example?

No specific reason, it can be any %. Needless to say, the higher the better.

Hi

Similar to other modules, can we also have a downloadable pdf available for \’Personal Finance\’ module ?

Thanks

PDF will be ready when the module gets completed, right now this is work in progress.

Is there a way to label my mutual fund investments with goals? For e.g. Aditya Birla Sun Life Frontline Equity Fund – Direct Plan – Growth—> House, Nippon India Low Duration Fund–> Vacation etc. This would really help track our investments based on different goals

For now you cant, but I\’ll pass this feedback to Coin team.

May i know how many lessonns there are going to be in this module , also the number of modules you are going to make ?

I\’m really not sure about that, but the idea is to cover as many topics as possible.

Hi Karthik thanks for all the knowledge and wisdom that you are sharing with us.But I would like to ask a naive question With SIPs we are building our retirement corpus or some goal purchase like luxury car after 20 years.But our investments will be attracting LTCG @10% suppose my goal amount is 1Cr in 20 years I can build that at nearly 7K per month at 15% CAGR my total investment will be 16 lakhs which means I will gain 84 lakhs so how is tax calculated on such investment is it calculated yearly or only when I have to do redemption does it mean that at 10% I will be paying 8.4 lakhs on the wealth that I built slowly and working very hard or is there any smart way around.Also how is indexation benefit availed is it applicable for all investments or only selected types of investment??

And last but not the least thank you team Zerodha you have amazing apps and services varsity,kite,coin and many more😍😍😍

Pritesh, that\’s right. As of today, the investment in any non ELSS equity-based MF is taxed at 10% with indexation benefit. By the way, the first 1 Lakh is exempted from taxation. You can check this chapter for how indexation works – https://zerodha.com/varsity/chapter/taxation-for-investors/

Agreed with Govil, Karthik its like I get up everyday with the expectation that you will upload a new chapter but I have to go with despair every day. Karthik please………….! 🙂

Will try and upload soon, Ram 🙂

Thanks Sir, for sharing these insightful information. You are doing a great job. Keep going..

Happy reading, Satyam!

Sir, Thanks a lot for nice explanation.

There are 2 sheets are already available , however rest are not.

With Regards,

Ah, I may have forgotten to upload this. I\’ll do it right away. Thanks.

Personal Finance is a much needed subject on wealth creation. Zerodha understood the need for such module and presented it in a simplied manner. Hope this module will covers all the relevant asset classes. Keep going Zerodha.

Yes, sir. We will 🙂

The only drawback of Varsity is that you have to wait eagerly for the next chapter. I wish you can start like Binge reading in varsity!! 🙂

Great content Sir!!

Govil, I\’ll take that as a compliment 🙂

Hi Karthik,

You have listed the importance of savings and investing your savings in a very effectively manner, The point I wanted to add was we even have PF\’s which will also add a significant contribution to our final corpus – Do you like to and any points on the same.

Yes Punith, that makes a difference. I will include that in later topics.

I have read all of your varsity modules!

I\’m eagerly waiting for the mutual fund education. There are a lot of mutual funds out there and which makes it confusing to know where to park our money into. And how much tax do we have to pay for the interest we receive every year.

Glad to note that, Kunal. I will try and put up clear and non-confusing articles on MFs 🙂