3.1 – Buying call option

In the previous chapters we looked at the basic structure of a call option and understood the broad context under which it makes sense to buy a call option. In this chapter, we will formally structure our thoughts on the call option and get a firm understanding on both buying and selling of the call option. Before we move ahead any further in this chapter, here is a quick recap of what we learnt in the first chapter –

- It makes sense to be a buyer of a call option when you expect the underlying price to increase

- If the underlying price remains flat or goes down then the buyer of the call option loses money

- The money the buyer of the call option would lose is equivalent to the premium (agreement fees) the buyer pays to the seller/writer of the call option

We will keep the above three points in perspective (which serves as basic guidelines) and understand the call option to a greater extent.

3.2 – Building a case for a call option

There are many situations in the market that warrants the purchase of a call option. Here is one that I just discovered while writing this chapter, thought the example would fit well in the context of our discussions. Have a look at the chart below –

The stock in consideration is Bajaj Auto Limited. As you may know, they are one of the biggest manufacturers of two wheelers in India. For various reasons the stock has been beaten down in the market, so much so that the stock is trading at its 52 week low price. I believe there could be an opportunity to initiate a trade here. Here are my thoughts with respect to this trade –

- Bajaj Auto is a quality fundamental stock, there is no denying this.

- The stock has been beaten down so heavily, makes me believe this could be the market’s over reaction to volatility in Bajaj Auto’s business cycle.

- I expect the stock price to stop falling sometime soon and eventually rise.

- However I do not want to buy the stock for delivery (yet) as I’m worried about a further decline of the stock.

- Extending the above point, the worry of M2M losses prevents me from buying Bajaj Auto’s futures as well.

- At the same time I don’t want to miss an opportunity of a sharp reversal in the stock price.

To sum up, I’m optimistic on the stock price of Bajaj Auto (the stock price to eventually increase) but I’m kind of uncertain about the immediate outlook on the stock. The uncertainty is mainly due the fact that my losses in the short term could be intense if the weakness in the stock persists. However as per my estimate the probability of the loss is low, but nevertheless the probability still exists. So what should I do?

Now, if you realize I’m in a similar dilemma that was Ajay was in (recall the Ajay – Venu example from chapter 1). A circumstance such as this, builds up for a classic case of an options trade.

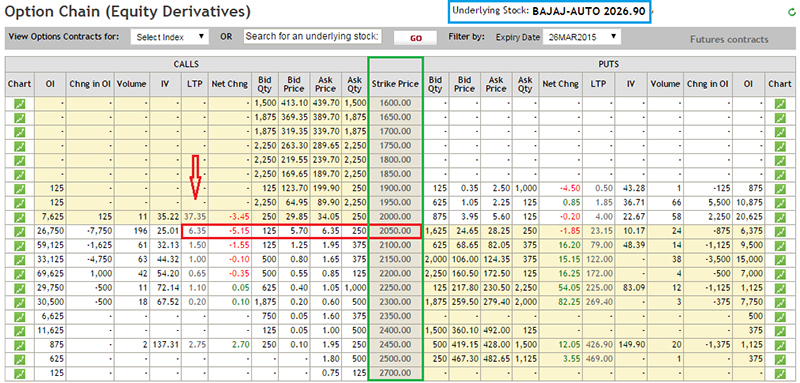

In the context of my dilemma, clearly buying a call option on Bajaj Auto makes sense for reasons I will explain shortly. Here is a snapshot of Bajaj Auto’s option chain –

As we can see the stock is trading at Rs.2026.9 (highlighted in blue). I will choose to buy 2050 strike call option by paying a premium of Rs.6.35/- (highlighted in red box and red arrow). You may be wondering on what basis I choose the 2050 strike price when in fact there are so many different strike prices available (highlighted in green)?. Well, the process of strike price selection is a vast topic on its own, we will eventually get there in this module, but for now let us just believe 2050 is the right strike price to trade.

3.3 – Intrinsic value of a call option (upon expiry)

So what happens to the call option now considering the expiry is 15 days away? Well, broadly speaking there are three possible scenarios which I suppose you are familiar with by now –

Scenario 1 – The stock price goes above the strike price, say 2080

Scenario 2 – The stock price goes below the strike price, say 2030

Scenario 3 – The stock price stays at 2050

The above 3 scenarios are very similar to the ones we had looked at in chapter 1, hence I will also assume that you are familiar with the P&L calculation at the specific value of the spot in the given scenarios above (if not, I would suggest you read through Chapter 1 again).

The idea I’m interested in exploring now is this –

- You will agree there are only 3 broad scenarios under which the price movement of Bajaj Auto can be classified (upon expiry) i.e. the price either increases, decreases, or stays flat

- But what about all the different prices in between? For example if as per Scenario 1 the price is considered to be at 2080 which is above the strike of 2050. What about other strike prices such as 2055, 2060, 2065, 2070 etc? Can we generalize anything here with respect to the P&L?

- In scenario 2, the price is considered to be at 2030 which is below the strike of 2050. What about other strike prices such as 2045, 2040, 2035 etc? Can we generalize anything here with respect to the P&L?

What would happen to the P&L at various possible prices of spot (upon expiry) – I would like to call these points as the “Possible values of the spot on expiry” and sort of generalize the P&L understanding of the call option.

In order to do this, I would like to first talk about (in part and not the full concept) the idea of the ‘intrinsic value of the option upon expiry’.

The intrinsic value (IV) of the option upon expiry (specifically a call option for now) is defined as the non – negative value which the option buyer is entitled to if he were to exercise the call option. In simple words ask yourself (assuming you are the buyer of a call option) how much money you would receive upon expiry, if the call option you hold is profitable. Mathematically it is defined as –

IV = Spot Price – Strike Price

So if Bajaj Auto on the day of expiry is trading at 2068 (in the spot market) the 2050 Call option’s intrinsic value would be –

= 2068 – 2050

= 18

Likewise, if Bajaj Auto is trading at 2025 on the expiry day the intrinsic value of the option would be –

= 2025 – 2050

= -25

But remember, IV of an option (irrespective of a call or put) is a non negative number; hence we leave the IV at 2025

= 0

Now our objective is to keep the idea of intrinsic value of the option in perspective, and to identify how much money I will make at every possible expiry value of Bajaj Auto and in the process make some generalizations on the call option buyer’s P&L.

3.4 – Generalizing the P&L for a call option buyer

Now keeping the concept of intrinsic value of an option at the back of our mind, let us work towards building a table which would help us identify how much money, I as the buyer of Bajaj Auto’s 2050 call option would make under the various possible spot value changes of Bajaj Auto (in spot market) on expiry. Do remember the premium paid for this option is Rs 6.35/–. Irrespective of how the spot value changes, the fact that I have paid Rs.6.35/- remains unchanged. This is the cost that I have incurred in order to buy the 2050 Call Option. Let us keep this in perspective and work out the P&L table –

Please note – the negative sign before the premium paid represents a cash out flow from my trading account.

| Serial No. | Possible values of spot | Premium Paid | Intrinsic Value (IV) | P&L (IV + Premium) |

|---|---|---|---|---|

| 01 | 1990 | (-) 6.35 | 1990 – 2050 = 0 | = 0 + (– 6.35) = – 6.35 |

| 02 | 2000 | (-) 6.35 | 2000 – 2050 = 0 | = 0 + (– 6.35) = – 6.35 |

| 03 | 2010 | (-) 6.35 | 2010 – 2050 = 0 | = 0 + (– 6.35) = – 6.35 |

| 04 | 2020 | (-) 6.35 | 2020 – 2050 = 0 | = 0 + (– 6.35) = – 6.35 |

| 05 | 2030 | (-) 6.35 | 2030 – 2050 = 0 | = 0 + (– 6.35) = – 6.35 |

| 06 | 2040 | (-) 6.35 | 2040 – 2050 = 0 | = 0 + (– 6.35) = – 6.35 |

| 07 | 2050 | (-) 6.35 | 2050 – 2050 = 0 | = 0 + (– 6.35) = – 6.35 |

| 08 | 2060 | (-) 6.35 | 2060 – 2050 = 10 | = 10 +(-6.35) = + 3.65 |

| 09 | 2070 | (-) 6.35 | 2070 – 2050 = 20 | = 20 +(-6.35) = + 13.65 |

| 10 | 2080 | (-) 6.35 | 2080 – 2050 = 30 | = 30 +(-6.35) = + 23.65 |

| 11 | 2090 | (-) 6.35 | 2090 – 2050 = 40 | = 40 +(-6.35) = + 33.65 |

| 12 | 2100 | (-) 6.35 | 2100 – 2050 = 50 | = 50 +(-6.35) = + 43.65 |

So what do you observe? The table above throws out 2 strong observations –

- Even if the price of Bajaj Auto goes down (below the strike price of 2050), the maximum loss seems to be just Rs.6.35/-

- Generalization 1 – For a call option buyer a loss occurs when the spot price moves below the strike price. However the loss to the call option buyer is restricted to the extent of the premium he has paid

- The profit from this call option seems to increase exponentially as and when Bajaj Auto starts to move above the strike price of 2050

- Generalization 2 – The call option becomes profitable as and when the spot price moves over and above the strike price. The higher the spot price goes from the strike price, the higher the profit.

- From the above 2 generalizations it is fair for us to say that the buyer of the call option has a limited risk and a potential to make an unlimited profit.

Here is a general formula that tells you the Call option P&L for a given spot price –

P&L = Max [0, (Spot Price – Strike Price)] – Premium Paid

Going by the above formula, let’s evaluate the P&L for a few possible spot values on expiry –

- 2023

- 2072

- 2055

The solution is as follows –

@2023

= Max [0, (2023 – 2050)] – 6.35

= Max [0, (-27)] – 6.35

= 0 – 6.35

= – 6.35

The answer is in line with Generalization 1 (loss restricted to the extent of premium paid).

@2072

= Max [0, (2072 – 2050)] – 6.35

= Max [0, (+22)] – 6.35

= 22 – 6.35

= +15.65

The answer is in line with Generalization 2 (Call option gets profitable as and when the spot price moves over and above the strike price).

@2055

= Max [0, (2055 – 2050)] – 6.35

= Max [0, (+5)] – 6.35

= 5 – 6.35

= -1.35

So, here is a tricky situation, the result what we obtained here is against the 2nd generalization. Despite the spot price being above the strike price, the trade is resulting in a loss! Why is this so? Also if you observe the loss is much lesser than the maximum loss of Rs.6.35/-, it is in fact just Rs.1.35/-. To understand why this is happening we should diligently inspect the P&L behavior around the spot value which is slightly above the strike price (2050 in this case).

| Serial No. | Possible values of spot | Premium Paid | Intrinsic Value (IV) | P&L (IV + Premium) |

|---|---|---|---|---|

| 01 | 2050 | (-) 6.35 | 2050 – 2050 = 0 | = 0 + (– 6.35) = – 6.35 |

| 02 | 2051 | (-) 6.35 | 2051 – 2050 = 1 | = 1 + (– 6.35) = – 5.35 |

| 03 | 2052 | (-) 6.35 | 2052 – 2050 = 2 | = 2 + (– 6.35) = – 4.35 |

| 04 | 2053 | (-) 6.35 | 2053 – 2050 = 3 | = 3 + (– 6.35) = – 3.35 |

| 05 | 2054 | (-) 6.35 | 2054 – 2050 = 4 | = 4 + (– 6.35) = – 2.35 |

| 06 | 2055 | (-) 6.35 | 2055 – 2050 = 5 | = 5 + (– 6.35) = – 1.35 |

| 07 | 2056 | (-) 6.35 | 2056 – 2050 = 6 | = 6 + (– 6.35) = – 0.35 |

| 08 | 2057 | (-) 6.35 | 2057 – 2050 = 7 | = 7 +(- 6.35) = + 0.65 |

| 09 | 2058 | (-) 6.35 | 2058 – 2050 = 8 | = 8 +(- 6.35) = + 1.65 |

| 10 | 2059 | (-) 6.35 | 2059 – 2050 = 9 | = 9 +(- 6.35) = + 2.65 |

As you notice from the table above, the buyer suffers a maximum loss (Rs. 6.35 in this case) till the spot price is equal to the strike price. However, when the spot price starts to move above the strike price, the loss starts to minimize. The losses keep getting minimized till a point where the trade neither results in a profit or a loss. This is called the breakeven point.

The formula to identify the breakeven point for any call option is –

B.E = Strike Price + Premium Paid

For the Bajaj Auto example, the ‘Break Even’ point is –

= 2050 + 6.35

= 2056.35

In fact let us find out find out the P&L at the breakeven point

= Max [0, (2056.35 – 2050)] – 6.35

= Max [0, (+6.35)] – 6.35

= +6.35 – 6.35

= 0

As you can see, at the breakeven point we neither make money nor lose money. In other words, if the call option has to be profitable it not only has to move above the strike price but it has to move above the breakeven point.

3.5 – Call option buyer’s payoff

So far we have understood a few very important features with respect to a call option buyer’s payoff; I will reiterate the same –

- The maximum loss the buyer of a call option experiences is, to the extent of the premium paid. The buyer experiences a loss as long as the spot price is below the strike price

- The call option buyer has the potential to realize unlimited profits provided the spot price moves higher than the strike price

- Though the call option is supposed to make a profit when the spot price moves above the strike price, the call option buyer first needs to recover the premium he has paid

- The point at which the call option buyer completely recovers the premium he has paid is called the breakeven point

- The call option buyer truly starts making a profit only beyond the breakeven point (which naturally is above the strike price)

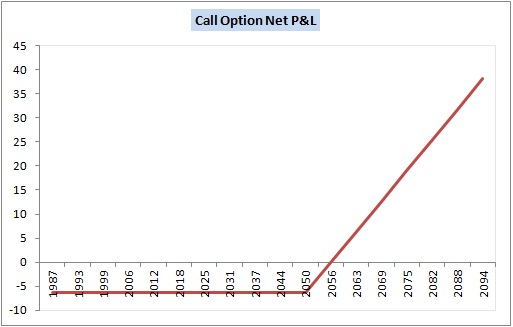

Interestingly, all these points can be visualized if we plot the chart of the P&L. Here is the P&L chart of Bajaj Auto’s Call Option trade –

From the chart above you can notice the following points which are in line with the discussion we have just had –

- The loss is restricted to Rs.6.35/- as long as the spot price is trading at any price below the strike of 2050

- From 2050 to 2056.35 (breakeven price) we can see the losses getting minimized

- At 2056.35 we can see that there is neither a profit nor a loss

- Above 2056.35 the call option starts making money. In fact the slope of the P&L line clearly indicates that the profits start increasing exponentially as and when the spot value moves away from the strike

Again, from the graph one thing is very evident – A call option buyer has a limited risk but unlimited profit potential. And with this I hope you are now clear with the call option from the buyer’s perspective. In the next chapter we will look into the Call Option from the seller’s perspective.

Key takeaways from this chapter

- It makes sense to be a buyer of a call option when you expect the underlying price to increase

- If the underlying price remains flat or goes down then the buyer of the call option loses money

- The money the buyer of the call option would lose is equivalent to the premium (agreement fees) the buyer pays to the seller/writer of the call option

- Intrinsic value (IV) of a call option is a non negative number

- IV = Max[0, (spot price – strike price)]

- The maximum loss the buyer of a call option experiences is to the extent of the premium paid. The loss is experienced as long as the spot price is below the strike price

- The call option buyer has the potential to make unlimited profits provided the spot price moves higher than the strike price

- Though the call option is supposed to make a profit when the spot price moves above the strike price, the call option buyer first needs to recover the premium he has paid

- The point at which the call option buyer completely recovers the premium he has paid is called the breakeven point

- The call option buyer truly starts making a profit only beyond the breakeven point (which naturally is above the strike price).

what happens if we buy same strike call option at different price during same say and sell also at different price during the same day? how to adjust this dilemma about final Profit and loss decision

Its like buying stocks at different prices, its all gets averaged out.

How to select the buy call and put call in the availability of various option premium….. ex. if I select buy call at ATM , but so many ATM options available .. how could I chose and relate to main chart.. kindly explain

There will be many OTM and ITM options (both call and puts), but ATM is only one. I think you need to spend somemore time on option analysis to get this. Alternatively, you can attend a live class on Option – https://varsitylive.zerodha.com/programmes/40a39a1b-bda0-4d54-82f8-2d453ad3187f

MY POSITION IS NOT SELL.

MY POSITION iS LOCK

KINDLY REMOVE MY POSITION .

IF NOT POSITION REMOVE , THEN BIG LOSS RESPONSIBBLE YOUR COMPANY ZERODHA >

Thans

saroj

Please contact the helpdesk for this. I wont be able to help you here.

Help me to understand

For example

scenario 1 – Bought Nifty 24000 CE @ 10 rs. and sold @12 rs. before expiry where Nifty was at 23950…..in this case will i make profit or loss ?

Scenario 2 – Bought Nifty 24000 CE @ 10 rs. and sold @12 rs. on the day of expiry where Nifty was at 23950…in this case will i make profit or loss ?

Scenario 3 – Bought Nifty 24000 CE @ 10 rs. SL was 8, once the SL hit, my order will execute and there will be a loss of Rs.2 …is this correct?

> Scenario 1 – Depends on the spot value on day of expiry

> Scenario 2 – You will lose 10 CE bought, make 12 on short call

> Scenario 3 – Yes

And to make profit the spot price have to be above breakeven point?

Thats correct, Niraj.

Sir the premium that we pay that we get back on the day of expiry then why we minus (-) from p&l ?

No, you only minus the charges that are applicable.

For ex :

On 25 dec to enter a contract with spot price of 100(1lot) i have to pay premium of 5rs set strike price is 110.

Now,On 10 jan

Spot price = 120

So my profit on 10 jan is 10rs.

The premium that i pay(5rs)i will get that premium back(like in futures the margin are release on the day of expiry) or its cover in 10 rs profit.

And if yes , so the breakeven point will be 110 right or wrong?

The easiest way to remember this – The P&L is equal to what you pay as premium minus what you get back when you square off your position minus all the charges.

If the premium that we pay will get back. so the breakeven point should be 2050.

You will get back the premium, only if you square off…and the fact that the premium at the time of square off should be higher than what you\’ve paid.

the premium that we pay we\”ll get back that premium or not when we square off the position .

Yes, you will get back whatever is the value of the premium at the time of you closing your position.

as you have mentioned exponential profit if price increases from strike price, isnt that linear growth?

Can I buy a call option which has already crossed the strike price, and still the expiry is there for 15 days.

say for ex

CMP 780 current Premium: 18/unit

Strike price 750 (premium : 11/unit)

I am new to this field, kindly apologize if it is a wrong question.

Yes, you can. When you buy option, you need to justify as to which strike, what price, and what outcome you expect. As long as these are taken care off, it does not matter which strike you are buying.

hello sir,

suppose any call option has been buyed on thursday for next week at premium of 10 rs and on the expiry thursday due to market volatility its price 20 rs, but till 3.25 pm i could not sell it, will it be exercised automatically and the profit be credited to account or entire premium which i paid will be lost during squareoff time..

Depends, if its stock option then there is a physical delivery and its cash settled if its an index option.

Hii,

I have read this module carefully and as you mentioned above that IV in case of CALL option can be defined as Spot Price – Strike Price. But while building my option strategy i saw that IV value is showing different. It was not as per the above formula.

The Spot – Strike formula is as on expiry, not during the series. During the series, it will be [Spot-Strike]+Time value.

Sir if BN 51500ce trading at 500.now i want to buy that option at 550 then simultaneously place the traget at 600 and stoploss at 500.is it possible to place these three orders at same time?

You can do it via SL by setting target and SL%. See in the GTT section.

Thank you for your response sir.

In that case, I see in option chain the price of premium is went down by -19.92%. can you please clarify what this implies?

It just means the premium for that particular option is down by 19.92%. Thats it.

Sir,

Please clarify my doubt.

Now bank nifty at 51295.

The premium for bank nifty 48400 CE is at Rs.2350.

In this case IV value is 51295-48400 = 2895

So I buy this option and sell it instantly assuming no change in underlying bank nifty, then am I entitled to receive profit of Rs.2895-2350 = 545.

After deducting brokerage charges I will receive balance amount.

Am I right or missing anything here? Please clarify.

Yes, thats right Vignesh. Your profit or loss is the difference between the buy price and sell price minus the charges applicable.

Sir, I am planning to buy SBIN JUL 870 CE 1 LOT(750) @ 24. I understand that I need to pay the premium amount to enter into the trade. But I am confused about how much I need to pay while exiting the trade? Do I need to pay 870 (strike price) x 750 (qty of 1 lot) if I decide to go ahead with the buying?

Can you please explain with following example?

Considering that the stock price has gone to 900 and the trade is ITM and inside expiry. While exiting the trade how much will I need to pay?

Paresh, you only need to pay Premium * lot size, in this case 24*750 = 18000.

Hello Sir, if I make a profit of say Rs.1000 by squaring off my option before expiry, what would be the applicable charges to be paid and the net amount to me?

You can simulate all charges from here and figure how much exactly you will be charged – https://zerodha.com/brokerage-calculator/#tab-equities

if i buy delivery option of nifty 23000 of 6 june expiry at 1st june can i hold it till 6th june till it\’s expiry ?

There is no physical delivery from Nifty. All index options are physically settled.

Hi,

If we are settling the differential amount only, neither the seller nor buyer owns the underlying asset, then how does it work?

like in the case of a property seller owns the property till the buyer buys it and the ownership gets transferred, but here the same is not happening. What is the underlying mechanism here? As in the equity market when I buy a share I own it. It\’s confusing me to my core.

regards

vaibhav

The way settlement works has changed. Share move from sellers to buyer\’s demat account. Check this – https://zerodha.com/varsity/chapter/quick-note-on-physical-settlement-2/

I want to buy Kotak bank mar 1950 CE at 1.85 whose 1 lot size is 400 how do I buy more than one lot of above ?

You just increase the quantity to two lots, thats it 🙂

If I feel that Nifty will rise in next 2 months. Should I focus on premium or spot price ?

Will i benefit if spot price and premium value both increase?

You can buy in the spot, Darshan.

Edit requested: The profits after breakeven point increase linearly not exponentially.

Makes sense 🙂

If I buy 45900 PE at 225 and stock price is 45825 …and next day stock goes up …can 45900 PE price rise …?

Yes, the price will fluctuate based on the movement in the underlying.

Sir here it is written you start making profit when the spot price is above breakeven point but I have recently made profit in oil 155ce Jan expiry and I have seen the spot price is lower than breakeven point can you explain where I am not understanding the things clearly

The Profit or Loss situation I\’ve explained is assuming you hold the position to expiry. The P&L could be different based on when you sell before expiry.

One question sir

if I buy a call option of a particular stock and the price of that stock goes up after a while and then if I decide to exit before expiry will I have to pay the complete premium even then

Sir,

I am new to options…i uderstood that buying and selling options all are based on the premium only and trading options also based on premium only just like equities at market price, these strike prices and expiry dates are just factors effecting the premium….Please do correct me if I\’m wrong

They are not just factors, but rather they are key parts of an options contract.

First of all thank You so much for reply Sir ❤️💕

P&L = Max [0, (Spot Price – Strike Price)] – Premium Paid

I bUY 1 lot of NIFTY 50 PUT @40rs premium Paid

Spot price is 19000

Strike Price is 19050

As per Formula P&L = Max [0, (19000 – 19050)] – 40

[0, (-50)] – 40

What happened further idk please explain

Ahmad, here goes –

P&L = Max [0, 50]-40

= 50-40

=10.

Mistake is you are considering spot – strike, which is for call options. For put it is Strike – Spot.

P&L = Max [0, (Spot Price – Strike Price)] – Premium Paid

Can You please Give an example on Nifty 50 using this formula,

I was calculating it but my answer were not satisfied

plz help me

Give me your example, will try and help you with that only. Also note, this formula is applicable for contracts upon expiry and not when its during the series.

Hi,

How to map Nifty Fut price with CALL Options premium price on respective ATM Strike price? Is there any formula? Is there any way to correlate that day current Nifty Future Opening price with its ATM or ITM Strike price to map?

Ah, you will have to get the time series and plot it using some program. Or you can do a side by side comparision on chart layout. I\’d suggest you call the support desk, our agent can explain this.

If you were to buy call european of ashok leyland you\’re certain that you\’ll make a max loss of x amount if the market didn\’t go up upon the expiry(last thursday of month).

But for sure you would have made profit if you bought stock and took long position as you\’re certain it is a fundamentally strong company and any decline after your stock purchase would cancel out when market starts to rally(go up)?

So I was wondering why didn\’t you buy stock delivery from that perspective?🤔

There is nothing called as certainty or for sure in market, they are all odds at play 😉

Thank you Karthik Sir

Happy learning 🙂

Can I buy one option with two different premiums separately?

Like ITC jul410 CE one lot at 22 and one lot at 18.5

Yes, you can. Your average cost will come down to the average of 22 and 18.5.

After reading this chapter numerous times and going through the comments. I am most likely to understand the concept of Stock options buying (choosing to buy at a specified price of yours ranging with the strike price, and taking delivery on expiry or let it go). But most traders I think they trade stock option premiums (Buy premium at low and sell it at high) , not stock options until expiry and taking delivery of it . If I am wrong with my thinking , please rectify me sir.

Thats right, most people end up trading options just for premium differentials.

Hi Karthik sir,

First of all thank you for Responding to the query that I had in Technical Analysis on Twitter , few days back.

I have just completed reading Futures module on Varsity, now I am diving towards options.

I am currently reading the 2nd chapter (Basic Option Jargons).

In that section I found the sub topic \”Exercising of an option contract\”

I am having little confusion in that topic,

You wrote \”Here is an important point to note – you can exercise the option only on the day of the expiry and not anytime before the expiry\”

Here exercising refers to as an option buyer claiming my right to buy the asset at that price as per contract on expiry.

so if I buy a call option of Hindalco JUL 440 CE today by paying premium 12.70 rs with a lot size 1400 and the expiry is on 27th July. That means my break even price is 452.70 Rs. Now hindalco\’s underlying price is 446.95. So if the underlying price increases , the premium for that will also increase.

My question is that :

If I purchase that Hindalco JUL 440 CE AT PREMIUM 12.70 Rs and next day Hindalco opens gap up at 449 rs. The premium will also increase , let\’s say the premium becomes 14.70rs.

1) Can I square off that 440 CE position and book the profits, (14.70-12.70) = 2 Rs *1400 qty = 2800rs and The premium that I have paid 17,780 rs , will that be added with 2800rs (2800rs + 17,780)= 20,580(14.70*1400) Or I have the only option to square off the trade on the expiry day only if the price gets above the Break even.

Yes, you can square off the position anytime you wish 🙂

Do check this – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

Hi Karthik,

I just started reading about \”Options\” on Varsity and the concepts are explained so wonderfully that I want to follow them as practice. However I read through an article in ET today and it seems the companies are slowing moving away from F&O. What are your thoughts please?

The article is – Exit from F&O segment could mean more upside for stocks

Read more at:

https://economictimes.indiatimes.com/markets/stocks/news/exit-from-fo-segment-could-mean-more-upside-for-stocks/articleshow/100950013.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

Kamal, that article talks about a stock being listed under F&O segment and then exit from there. Nothing much from a trader\’s point of view.

Dear Sir,

P. clarify:

Example: I buy Nifty 18700 call for premium Rs 200 monthly expiry, when Nifty is at 18680 level. Is the latter is what is called as spot price at that time? Secondly, if Nifty goes up to 18720 and then premium goes up to Rs 220, am I not making Rs 20 profit X 50 (one lot) = Rs 1000? Or, is profit available only after Nifty spot prices goes up to the strike price of 18700 + 200 (premium paid) that is, 18900? If this is the case, then don\’t you think chances of making profit are very less. Is it not better to sell for a small profit like mentioned above where premium goes up by Rs 20 and even though spot price is below the total of spot price + premium?

Yes, that is the spot price (18680). Yes, you can profit that 20 gain, provided you sell at 18720. Do check this chapter – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

what happened before expiry my premium went 0 then strike price increase after 0 , will I get benifit?

No, the strike price won\’t increase. Zero implies that the option has 0 intrinsic value.

After going long on a call option, can I put a target and stop loss at the same time, the way we do it in intraday…?

Hi sir,

My question is I want to buy a script which is 17300 PE at market price which is 57.05 for which I required a margin approx 2875(50 lot size ) But when I am goin to sell that same script at same price it\’s showing 98221 rupees. My question is why it\’s showing such a big amount while sailing and why small amount while buying ? Kindly replay to this question sir .

I guess you have another position already?

Ohhhhkay, I\’m so sorry for that I didn\’t knew, I thought both were same, but anyway, Thank you a LOT sir for explaining all this Technical Analysis and this Option series beautifully 🙂🙏

Happy learning, Rohan 🙂

Yeah I got that the IV cant be negative, my question is how that \”25.1\” is derived in that strike price of 2050 in Option Chain pic you have shared

Ah, ROhan, that IV in option chain refers to Implied Volatility. The IV we are talking about is intrinsic value 🙂

Sr in the above Option Chain that you have posted, how the Intrinsic Value of 25.1 is derived, one with the strike price of 2050 ?

As you said IV = Spot price(2026.90)-Strike Price(2050) so the value is coming in Negative.

Rohan, IV is either a positive value or 0. It cant be -ve.

So,

IV = Spot Price – Strike Price

If we put values in that formula for:-

Spot Price= 2026.90 (highlighted in blue)

Strike Price= 2050.00 (highlighted in Red) then,

IV = 2026.90 – 2050.00

= -23.1

So, the answer is -23.1 as you said IV is non – negative number.

But in the Image it says IV is 25.01.

Please Explain it, how did happen?

IV is either a positive value of 0, as I;ve explained in the chapter. There cant be -ve IVs.

Hi Karthik,

I am really so confused about calculation of P&L of an option. what you have explained even everywhere I see same calculation i.e.

P&L = Max [0, (Spot Price – Strike Price)] – Premium Paid

but my experience in option buying is different, means that is not actual P&L i get when I trade in options.

for example-: I traded BANKNIFTY call option of Strike price of 42000

Buy BANKNIFTY CE 42000 at premium of 1123.50 on 1\’st Feb during 12:45 candle (considering 5 mins chart). at this moment BANKNIFTY was trading at 41590.30.

In next 2 candles of 5 mins chart, BANKNIFTY was reached at 42011, but at the same time my options was reached at 1350.

So according to Formula P&L = Max [0, (Spot Price – Strike Price)] – Premium Paid my P&L should be as below,

Expected P&L = Max [0, (42011-42000)] – 1123.50…..-1112.5, which is actually loss.

but my P&L was in very good profit as below,

Actual P&L = 1350 (Option price at 1 PM) – 1123.50 (Buy price at 12:45 PM)……226.50, which is around 20% of profit.

So please clarify my this doubt, why option calculation is different in theory when actual movement is completely different.

Thanks,

Gaurav

Gaurav, please check this, hopefully it should address most of your concerns – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

sir,

I have a question, that if a person bought the call option at the extreme \’In the money\’ end with the highest premium and stock price does not fall below to that price, can he loss the money.

Yeah, the ITM option also has time value baked in, which the trader will lose on.

Yes sir, suppose Bank nifty spot is at 42250, and i am planning a call buy of 42200CE or 42100CE (slight ITM , delta 50-55%), Target is 42350 and SL of 42150 which i marked on index chart or fut. Now that we know if the market goes up by 100 points the call premium will increase by 50(50% delta) and vice versa. So let\’s say i had bought the call option at 100 rupees, should i keep SL at 50 and target at 150?

Yes, it\’s good to have a SL. But the exact level you need to place a SL depends on your risk appetite.

sir how to decide stop loss and target in option buying, as we have to keep in delta, theta & volatility. Its easy to mark levels but how to figure out SL n target for option contracts.

For stoploss and target, I\’d suggest you take the help of tools like Support & Resistance to identify these levels. Do apply these on the spot market and see what levels you get. Use that to setup trades in options.

Hi

I buy a call

To exit the call

What is the margin

The amount required in the account

Example

I have 10k

I buy call ce

using 5k

Now I want to exit

More money is to be added to account.

There is no margin required to buy a call option, Rama. You only have to pay a premium for it.

I have made 4 Bank Nifty 43200 CE of 1 lot each at varying intervals during intraday trading sessions by first buying and then selling. Even though I have sold each one at a higher market price, I have eventually ended up in loss. Please explain?

I\’m not sure about the details, but going by what you say, it could be the charges. Do check the charge list here – https://zerodha.com/charges/#tab-equities. Maybe you should call the support desk and enquire.

In which case premiums price up and down?

Is Premiums prices changes or it will fixed?

Premiums changes as and when the market condition changes.

Suppose Yesterday ( Monday ) I have bought 1 Nifty CE / PE Lot

now ledger balance is NIL

Next day ( Tuesday ) I sell it out

Now Can I Buy back that Particular Nifty CE/ PE On The Same Day ( Tuesday )

OR

Any Other CE / PE Against The Square off trade Value ( Tuesday )

Yes, you can Nilay.

Thanks for the insight. I want to understand how to calculate the open price of an option stike at 9:15AM. For e.g. if previous day Bank nifty (BNF) closed at 42500 and suppose the call option price of strike 42600 closed at 150. The other day in the morning, at close of pre market at 9:07 AM, BNF opens at 42600, then what will be the opening price of 42600 strike call option? How do we calculate this?

The opening price, and for that matter all prices in markets, are driven by the supply-demand factors. While you can predict if the opening will be positive or negative, it will be nearly impossible to predict the open price. Think about it, if you can predict the opening price, then you can predict pretty much every other price in the market right?

What if i bought a call option and there is no call option seller till the expiry date then what will happen to my order??? will i be in loss or it will be rejected by the system stating that no seller available.

The exchange will settle the contract for you.

if on 17th Nov 2022 i bought BAJAJ AUTO CMP 3647 call option at the strike price of 3600 @0.35/. for a lot size of 250, expiry date is 24th Nov 2022. if closing price on 24th Nov 2022 is 3900 then what will be my profit??

1.) is it Max[0, (3900-3600)]*250 = 75000( incl. premium paid)???

2.) If there is change in IV = 0 and premium charges are unchanged on expiry date then what will be the P&L?

1) Yes

2) 0

How do I calculate total payoff & breakeven in case I have two legs both with different expiry ?

Nikunj, please check Sensibull platform, they will give you the splitup.

How do I calculate payoff diagram for two calls if both has different expiry ? is BS formula used in it ?

You can use Sensibull\’s platform to visualize this, Bruce.

Can I buy VEDL DEC 300 CE at different time points …to average out the premium paid…just we do to average with stocks?

Yes, you can.

hlo sir

my doubt is can the spot price decrease to any level till the risk is limited that is the premium.

example – strike price is at 8500 the spot decreases to 8000 till my risk is only the premium which i paid multiply by share lot.

Yes, thats how it works for call option buyers.

so sir you are saying that stock options the buyers loss is limited only up to premium price. but index options loss will include diff between underlying price and strike price along with premium loss, if underlying price is below the strike price

No, it is the same for all option buying. But I\’m not sure if I understand your query fully.

Sir, you have said that options contracts are cash settled in India. so when the spot price is at 1990. the option buyer will suffer a loss of 60+6.35 premium paid right? so how is it only limited to the premium paid? clarify this

Krishan, please check the chpater on the physical settlement. Now only index options are cash settled, stock options are physically settled.

Sir

Wow..! Just marvellous..!!

Appreciate. Not bothering for space you let us make understand these complexities as smoothly as possible.

Thank you Gentleman. May God bless you.

I cannot break mathematical barriers, you get 10 on 10.

Accept my regards please.

Thanks so much for the kind words, happy learning 🙂

As per the chart of Bajaj Auto in Chapter 3.2, I understood that the striking price should be Rs. 2026.90 and the chosen option price at Rs. 2050 by paying a premium of Rs. 6.35/=.

but you have mentioned the striking price of Rs. 2050 in all the calculations, which gets me confused.

Please clarify.

The strike price is 2050. 2062.9 must be the spot price.

Hi,

I have 2 query:

1. I have buy a put of 40500 with a premium of 380 on friday and sell the same at 425 with 45 Rs profit on premium. Can i gets profit or loss if the strike price even not touched break even point.

2. I have bought call of 40400 with a premium of 475 and sell it at 550 with a profit of 75 rs on premium. Can I get the profit or loss if the strike price even not touched break even point.

3. If we buy any ITM option call or put amd sell it at profit on premium on the same day can I get the profit or loss.

1) Yes, you can.

2) Yes, you can.

3) Yes, you can.

Please check this chapter – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

I bought NIFTY17900. CE . weekly options on Friday at a cost of Rs. 108 . On Monday can I sell on Rs. 120 even if NIFTY is rallying around 17800- 17850 .

Will I get back my premium amount that I paid or it’s not refundable.

Yes, you can square off your position, no need to wait to expiry.

This gold was here in my backyard to learn options and i was roaming around 100s of YouTube videos and many paid tutorials 🙂

Thank you !

There is more on Youtube as well – https://www.youtube.com/playlist?list=PLX2SHiKfualFiusiT9G5uE9jU3vetvW2x

Happy learning 🙂

I bought any option and sold it at higher price.

Again when I want to buy at lower price it gets averaged buying Why.

That is because you are buying the same instrument multiple times. The buy average will change.

What if I buy a call option and couldn\’t sell it on the day of expiry, what would be my max loss in the case that the premium amount has goes down from x to 0.

In that case, you will lose the money paid as a premium, Sumit.

Thanks for ur help Sir..🙂

Happy learning 🙂

Sir If I bought Nifty50 at a strike price of 17300CE(50Lot) premium of ₹200 but stock goes against me and fall upto 16800,premium became ₹80.At that point i.e before expiry if I Exit this contract then what loss incurred? The whole premium or just (200-80)*50?

You will lose (200-80)*50, assuming you square off your position at 80.

Sir, If i bought any stock at a strike price of 100 CE with a premium of Rs.10. The stock traded at 85 and the spot price goes upto 95, premium also increased to 12. If I exit the contract before expiry what will be the profit or loss?

You will be in profit. In this case, a profit of Rs.2.

Hey! I\’m not sure if you meant it technically or figuratively but you might want to correct the line where you say that the profits increase \”exponentially\”. P&L is a linear plot and varies \”linearly\”.

Thanks, Anurag. I will fix that.

Sir, if I buy call of Same strike Price of 1 lot(50qty)for 6 times will my p&l multiply on the 6 th trade ie I mean to say on the 6 th trade will I face big loss of around 500 to 600 just after opening the trade. By multiply I mean will i face loss for 300 qty(1 lot bought 6 times). It happened to me in an app.. Does it happen in zerodha too

Loss happens only when the price moves against your expected direction, Arindam. The number of lots wont increase.

Sir, Simply amazing and really appreciate the efforts you are putting in. Really getting to understand the concept of Option unlike seeing numerous youtubers. I feel like I am gaining the content which is priceless. Your explanation and specially question and answer section really provides better clarity regarding concept discussing in the theory, open new horizons of knowledge regarding the topic and real life example is a gem.

Thanks for the kind words, Ajay. I hope you continue learning on Varsity 🙂

Means Thursday of last week of June.

Should be ok.

For ex . If I bought reliance option in the first week of June in respect that price will rise but it reverse price get down .

So here I want to know that till what period I can hold option of reliance ?

You can hold till June expiry.

Sir kindly tell me simple calculation for profit or loss when I buy a nifty call option or put option and sell before expiry and before it reaches strike price

Exp.

1) buy nifty 16000 call option at premium 80 (1 lot of 50 )and sell when spot price is 15900 and premium price is 85 before expiry day

Think of it as buying and selling a stock. So the P&L is the difference between the buy and sell price of the option premium. In this case, it is 5.

Hello sir,

What happens if I bought a stock call option and next day it gets split?

The option gets adjusted so you wont have any drastic P&L.

Just to be mathematically correct, profits start to increase linearly after spot price moves above strike price – not exponentially

Thats right, Prashanth.

If i buy call option in normal order can i sell on dame day if

Yes, you can.

Hello Karthik,

If we buy call option higher than the spot price. Then what would be my profit

case 1 :- before expiry :

if the spot price is more than strike price as well as premium also increased by certain amount, after selling the call option?

case 2 :- after expiry

again, if the spot price is more than strike price as well as premium also increased by certain amount?

case 3 :- after expiry

if the spot price is less than strike price and premium increased by certain amount?

Anupam, the easiest way to think about it is by calculating the intrinsic value of an option. After expiry, in the option has an intrinsic value, then the premium = intrinsic value. Else it will be zero.

Sir, can option buyer (both call & put buyer) exit their positions before expiry date (in case of intraday, weekly & monthly)?

Yes, they can.

sir i want to ask that if the CMP is 2030 and we bought the call option of the strike price of 2050. if CMP goes to 2040 we still can make profit? as options premium increases with the respect of CMP.

Yes, you will most likely make a profit, but not guaranteed. For example, if its too close to expiry then you wont.

If suppose i paid a premium for a particular stock for a particular strike price as 20 and if the premium goes to 16 and I excerised the option , so will my loss be 20(the premium paid)+4(loss)=24 ?

You will lose the difference between the buy and sell premium i.e.20-16 = 4.

Thanks a lot

So I am confused a bit here, as a option buyer is my profit calculated on increase and decrease of my premium prices or increase and decrease of actual underlying stock.

Its the increase/decrease in premium. But the premium itself changes based on the changes in the spot.

Sir i want count our profit and lose how

Hi I wanted to know if we buy 8600 PE at 15 ,75 quantity is the minimum required so how much I have to pay to get those shares and what ij case if it goes down to 5 rupees what will be the total loss .. can u pls reply on this as it will be really helpful

Its simple, the amount you have to pay while buying is lot size * premium, and while selling its again lot size * premium. YOu make a profit if you buy at low premium and sell at high premium, loss otherwise.

Let\’s keep Strike price and spot aside and also the expiry.

I bought a call option @rs10 premium, lot size is 100, i paid 1000rs.

Now the premium is @ 12rs and I want to sell @12 what will be the profit?

You bought at 10 and sold at 12, so you make a profit of 2.

Hi,

Can I buy and sell call option many times a day?

Thanks.

Yes, you can.

Dear Karthick, First thanks a lot this excellent blog and illustration, really enjoying learning about options and thanks a lot for this amazing work .

I\’ve the below silly question help me that my understanding is correct or not

For example Assume TCS Spot at Rs.1000 and I\’m buying the call option 1500 CE at the premium of Rs.10

Its is 500 point away from the spot price and Also, I\’m buying and squaring off on the same day

say I bought at morning at the premium of Rs.10 and on afternoon the premium was Rs.15 and I squared of that position

So, my profit would be the premium difference

And also breakeven point is not considered if we are selling on the same day right ?

My doubt is how we are getting the profit here, I\’m betting that stock will move above Rs.1500 but say as for today it moved Rs.1100

so I\’ll get the profit for that 100 points as a premium difference ?

Thanks for your time.

Prabhu, in this case, you are only buying and selling the premium. As good as buying a stock at 10 and selling at 15.

Hi sir, can a option buyer and seller can close their position before expiry date. their is any obligation.

Yes, they can. No need to wait for expiry.

Hi Karthik, Thank you for helping me with my previous query dated 23rd-Jan-2022.

I need your help and expertise to understand something related to trade execution, large quantity option buying of near atm strikes(+/- 3 atm strikes with good volume) and associated slippages.

1. Assuming on 14th-Feb-2022 @ 11.15 am I had a speculative bias towards the downside in Bank Nifty- BNF Spot-37456 @ 11.15 am.

Around 11.21 if I had decided to Buy 37500 PE @ 490 \”with the volume for that particular strike at the particular time being 5Lakh+\”

trades then would I be able to punch an order of 6000 quantity (1200*5) and be sure of getting my PE BUY Order filled instantly with

the least slippage since the overall traded volume stands quite high. (6000 Buy Order < 5 Lakh Traded Volume so order fill at the

desired price should perhaps not be a problem right?)

What would be the average slippage in this situation and in general while trading a near atm strike or +/- 3 atm strikes in Bank Nifty.

2. Assume my plan was to enter 37500 PE BUY @ 490 around 11.21 am-hold for 20/30points i.e. 510/520 and square it off. This particular

trade closed @ 530 around 11.30. So what are my chances of punching a 6000 quantity size and making a 20+ points profit

minus the slippage and all the other charges combined.

Is it possible or will the cost and slippage eat away the 20 points gain more or less. (i.e. will the cost of trades like these in general

outweigh the profits made?)

2. Since Nifty and Bank Nifty are quite liquid and the near atm strikes carry decent trading volumes then does an order size of

6000-12000 quantity in Bank Nifty and 18000+ quantity in Nifty be filled instantly and not incur vast slippages that I may have

otherwise not factored in or misunderstood.

Please do provide your insights into this as it is much needed and kindly do correct me if I am misunderstanding or missing something.

Best Regards,

Siddharth

1) There are quantity restrictions on a per order basis. But I\’d suggest you use this instead – https://support.zerodha.com/category/console/portfolio/holdings/articles/what-is-a-sticky-order-window-in-kite-and-how-can-i-use-it

2) Its possible to lose 20 points via slippage, you need to be careful with order execution. You can easily overcome this by placing sticky window + limit orders. Check this – https://support.zerodha.com/category/trading-and-markets/margin-leverage-and-product-and-order-types/articles/what-are-limit-and-market-orders (the last part of the article).

3) Both these contracts are liquid, you may get fills soon.

What if I have bought a call option of certain stock at any target price (suppose 100) and during the expiry day I\’ve to sell my call and stock hasn\’t reach 100 (as I assumed) also no buyer is available then what should I do? How can I sell my options call ?

Please suggest.

In that case, the option is considered worthless and hence no physical settlement.

I would like to understand the procedure of selecting the strike price for ce & pe in regards to nifty and bank nifty, how does one determine which price should be selected

Mansoor, I\’ve discussed this in the chapter itself, right? Request you to please check the chapter again.

Hi Sir,

If I brought Bank Nifty or Nifty or WIPRO CE contract with Overnight (NRML), Options Intraday will close at 3-25PM Right?

Can I sell options contract on same day between 3-25PM to 3-30PM which took as Overnight? or I must close before 3-25PM?

Thanks

Venu

You can, but I don\’t think you\’ll make anything at that point.

Sir please guide me in option Buying and selling of stock on expiry day

E.g if on expiry day(as premiums low on expiry day) I bought SBIN CE strike price of 520 at premium of Rs 2(CMP is 510) so as day goes the when premium goes to 8 as stock price increases to 522. So my question is Can I exit the position at anytime before market close and book profit or I can\’t as option is ITM? Please guide. Same applicable in case of loss?

Yes Satish, you can book profits (or losses) anytime during the expiry. No need to wait till expiry.

Superb….. Excellent examples for easily understanding…. Thank you thank you so much

Happy learning!

does the concept of breakeven point apply if you don\’t hold the option till the expiry date? if you sell your option before the expiry do you get your premium back?

No, it does not. When you trade before expiry, what matters is the difference between the buy and sell price of the premium.

Thank you for your reply to my previous querry.

would like to have you view on whether it is good to buy same strike price contract when premium reduces instead of raise after some time lapse to average out. that is to reduce average premium paid for two contracts so that chance of going to profit increases

You can, as long as you are convinced about the direction. I\’d personally prefer to trade another strike, maybe closer to the ATM.

I bought Nifty CE 18000 @ 150/- premium. on expiry nifty was 18300. but due some problem i could not sell the contract before expiry. now will i loose all premium paid or i get automatically 300 X lot into my account so that i get profit of 150x lot. will the exchange close automaticaly and credit the amount

Thanks in advance

Regards

That\’s right. This option is worth 300 upon expiry, so you will get 300xlotsize.

Sir,

I took one Lot Nifty options at 200 Rupees and now it is trading at 350 Rupees.

1) Can I create GTT with Stop loss 360 Rupees (more than bought price ) and target Price 500 Rupees?

2) Second question is can I change stop loss always more than bought price and more than present trading price?

Thanks

Venkat

1) Yes, but please make sure the price is within the price range – https://support.zerodha.com/category/trading-and-markets/trading-faqs/f-otrading/articles/what-is-f-o-execution-range-and-why-do-some-open-orders-outside-f-o-execution-range-get-cancelled

2) Yup

Hi Sir,

1) if I buy Nifty Feb or March CE or PE contracts in This month January, then expiry is feb last Thursday (for Feb) and march last Thursday (for March) only right, Those Feb and march Nifty options will not expiry in January and continue in respective month and expiry in that month only right? I am I correct

2) If I buy Nifty Jan 17400 CE at 100 for 1 Lot (that is 50*100=5000) and not closed this Thursday, so it will settled on last traded price on Thursday (Loss or Profit) and no need to pay anything again right?

Thanks

Venu

1) Thats correct Venu, the expiry of the series is always in that month only.

2) It will be settled on the basis of the settlement price on the expiry day. The settlement price is the average of the last 30 mins of trading on the expiry day.

Hi Karthik, I was hoping you could help me with a few silly questions and am thanking you beforehand for taking up your time on a Sunday Night.

1. Reliance Spot closing @2478-21stJan(Friday)_Expiry27thJan. Assuming my speculative view is Bearish:

2500PE BuyRate@51 (250qty) should be 51*250=12750 but the premium calculated in KITE terminal says 37290 as Margin Required for

the given strike.

(Also, In the Buy Order window-2500PE \”Margin Required\” here implies Premium to be paid since it is an Option Buy correct and not an

Option Sell?)

2.Physical Settlement applies only for stocks and not indices UPON EXPIRY of an ITM Call/Put (Option Buy/Sell) and Stock Futures.

Now UPON EXPIRY here \”PRECISELY\” means @ 3.30pm on Thursday27thJan or is it 3.20pm, since Thursday27th is an Expiry Day from

9.15am to 3.30pm market time.

3.What I mean to understand is,

Assumption – If I trade the premiums of the current expiry Intraday on either Monday24/Tuesday25/Thursday27-Expiry day itself,

then even though if I choose to trade the premium of an ITM Strike and close the trade before 3pm or 3.20pm on either of the days

including the ExpiryDay27thJAN mentioned above before 3.20pm then will that lead me to a physical delivery obligation since the strike

being chosen to trade is ITM.

4.In layman\’s term Trading the Premium means buying @50 and selling @60 and profiting the 10 points difference on either Call/Put

Option Buy be it 15 seconds from placing a Buy Trade or 15 minutes or even after a day.

So in Trading the Premium, the concept of Strike+PremiumPaid for a Call Buy and Stike-PremiumPaid for a Put Buy to arrive at profit or

loss scenario does not apply as that is true if the bet is held till the contract expires on the last minute of the Expiry day. But if I am

Trading the Premium then immediately(say right after 5 seconds of placing an Option Buy Order I can exit it even at a 1-2 point

profit/loss. Please help me in understanding this part if I misunderstood the concept.

Best Regards,

Siddharth

1) That\’s right Siddharth. The additional margins is for physical delivery. You must have got a nudge saying so right? More on that here – https://zerodha.com/varsity/chapter/quick-note-on-physical-settlement/. Yes, the margin required means the premium payable to the seller.

2) It means the settlement price on the expiry day. The settlement price is the weighted average of the last 30 mins price. Yes, physical settlement is only for stocks, not indices

3) No, physical delivery is applicable only if you hold the position to expiry. Not if you close before that. Even if you close at 3:25PM on expiry day, no physical settlement for you.

4) That is right. More on this, in this chapter – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

Hello Karthik sir, Thank You for this great content.!!

Happy learning!

At two places in the article, you mention that the profit increases exponentially. The profit actually increases linearly.

Yup, \’exponentially\’ is the wrong choice of word I suppose.

If I am in the money on expiry day for a call option I bought and I don\’t close my position with a profit, will I be forced to buy the whole of the underlying stick which can run into lakhs. Or zerodha automatically squares it before the eod?

Yes, if it\’s a stock option then your position will have to go through the physical settlement. Check this – https://zerodha.com/varsity/chapter/quick-note-on-physical-settlement-2/

I took NIIT Share 10 days back with price 490 and to day I sell it for 507 in the morning, later that share went 489 or 491 range, in this case what is the steps need to follow to close the positions?

1) Is it just exit from position with giving desired price to buy?

or

2) do i need to convert position or any other steps need to follow?

Nikhil, yes when you click on exit, your position will be closed (provided the order has gone through the exchange).

Only if the option is in the money.then need to take physical delivery?

When I took it is otm, but came in itm category, in this case I sell my position, so no physical delivery?

If i didn\’t sell since it is zero, still need to take physical delivery even though I took otm and closednin itm?

Kavitha, upon expiry, if the option is ITM, then it attracts physical delivery. Not otherwise.

Hi Sir,

If I bought IEX Jan 320CE and before expiry it become 0.05

1) In this case I will loose all the money right?

2) In which case it will become zero? Please suggest all the scenarios, so that many traders will get the benfit.

3) when we need to take physicals delivery?

Please can you help on these queries in detail,

Thank you so much you help always

Kavitha

1) Yes, since the option is worthless

2) The option is worthless, so you lose the entire premium paid

3) Only if the option is in the money.

Hi Karthik

I bought a lot (25 ) banknifty strike price is 38300 at premium 237.5 and sell at spot price 38440 at premium 350 .

how much profit I have made & it\’s right thing to do can i sell when my premium price is up from my brought price.

Anshu, the profit is the difference between the buy and sell premium price multiplied by lot size minus charges applicable.

For buying nifty50 option, how the expiry date and strike price to be determined? Also how to determined the price at which it is to be sold. I am new to trading and also to zerodha and will appreciate it very much if you kindly advice in detail through my mail id.

Swarnali, this depends on your expectation. Based on your view of the market you can select the strike and expiry series.

Exercising an option is only on the day of expiry. What does it mean. Suppose we bought and sold any CE before expiry then what does it mean exercising an option is only on the day of expiry. Is any thing us required to do on expiry date if option already bought and sold before this expiry date.

Exercising the option is different from selling the option. I\’d suggest you read this – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

Sir, I wanted to buy a call option for intraday how should I buy and sell in a day

And is there any call options within 10k rupees

Buying and selling is easy. Click and buy/sell just like the way you trade stocks. Which option etc, I won\’t be able to help 🙂

i buyed call option for nifty 17200 dec 2021 on expiry of 2 lots at 6.20 but as badluck it went to 3.5 and when i was trying to exit it was asking their should be margin of 180000 in account that i didnt got can anyone please explain me

I guess you had a few other open positions Sushant, that\’s why.

Hi sir,

I have question regarding options buying. I am bullish on nifty, if I buy 17200CE @ 154rs. Theoretically my breakeven point is 17354, if nifty went above of 17354 then only I make profit but practically when we buy option and in few minutes if nifty move to 17250 then after also I started making profit. Why this happens??

There is any differences in theory and practical??

It depends on how long you keep a trade. Check this chapter – https://zerodha.com/varsity/chapter/options-m2m-and-pl/

Hello sir, hope you\’re doing well. I am an options beginner with zerodha and my query is regarding placing orders. When I place market orders, it tends to get filled away from my desired price and when the difference gets multiplied by the lot size, we lose a significant amount just getting in and out of the trade. To help this I use limit orders but during gap ups or gap down openings, my orders usually don\’t go through. Are there any alternatives to this or a better solution to my problem? Your two cents about the same would really be appreciated.

Thanks and regards,

Sharon.

Limit order helps you with slippage, but there is nothing much you can do to prevent from gap opening risk. One thing that helps is having a spread position instead of naked positions.

How can we match the nifty strike price chart with nifty chart?

Sorry, dint get that query. Can you add more context, please?

I have Infosys shares at 2300 per share, and I sell it 2400 for 100 rupees profit , and same day it went to 2350 again, so can I buy again using position tab to get the 50 rupees profit instead of 100 and keep the same shares? if yes, so i Need to maintain any money in my account to close the position in that scenario?

The sell and buy trade that you do will be treated as an intraday trade. The shares will remain intact in your demat. No need for extra money.

I would like to know how to trade in F&O on Zerodha platform (laptop or mobile). What is the step to invest. I don\’t find any option of doing that

Sitesh, I\’d suggest you call the support desk, they will guide you with this.

Hi Sir, you\’d mentioned that the Profits rise exponentially above the BE point. However, it seems to be a linear increase as seen in the graph.

Is \’exponentially\’ just a phrase to indicate rising profits or do profits actually rise exponentially (y=a^x)?

I think the word exponential should not have been used. You are right 🙂

Hi Karthik, Please can you clarify,

1) When Physical delivery is mandatory in options? Is there any details in Zerodha?

2) Bank Nifty and Nifty has Physical delivery after expiry?

Thanks

1) You can check this – https://zerodha.com/varsity/chapter/quick-note-on-physical-settlement/

2) No, indices are cash settled.

if I buy CE or PE contract overnight position and want to sell on same day?

1) Do I need to convert to Intraday?

2) or directly click exit and give sell price?

3) What is the process to convert intraday to overnight? Is there any varsity material links on this?

1) No

2) Click exit and square off

3) YOu can check this – https://support.zerodha.com/category/trading-and-markets/margin-leverage-and-product-and-order-types/articles/how-to-convert-mis-to-cnc-nrml-and-vice-versa

If I buy nifty Nov 18000 CE or PE, Overnight position?

1) What will happen if I didn\’t close the position before month expiry?

2) What will happen it goes zero or minus? my liability only that amount which initially paid for that Lot?

1) The position will be settled by the broker upon expiry at the settlement price

2) Minus won\’t happen as option prices cant go below 0. But if its zero, then the option is worthless and you will lose the premium paid.

Hello

Is it possible in Nifty option with zerodha

If Nifty 18000 CE is trading at say 120rs and it\’s going side ways ,so I have to buy this call option at 135rs ,how to place order in that case , please help

A regular limit buy order, right?

in that above case: If I squared of before 28th Oct (month Expiry) may be around 26th with loss of 1 rupee, then I will born only that loss , so no other physical delivery on expiry right?

Thats right, no physical delivery.

This contract will be physically settled on expiry if it turns ITM and requires additional physical delivery margins. You can trade the next expiry if you wish to avoid this.

When I am buying WIPRO OCT 700CE @2 Rs of 1 lot (1600), I am getting above message, but maximum my loss will only 1600*2 =3200 even it go zero or 28th Oct month expiry day if I am not squared of right? what is that mean physically settled means, do i need to purchase 1600 shares at 700 rupees?

When you are long CE, physical delivery obligation mandates you to take delivery of the stock. This means you need to have sufficient margins in the account to buy the stock.

Can I buy November 2021 CE or PE Option in October and sell in October itself if I get profit, so in this case no obligation to me after selling in October itself?

Yes, you can do that. No obligation after you square off the position.

If I buy WIPRO NOV 800CE on Today (Any date in October), Is it valid until November 25th(Next month) last week Thursday?

Yes, provided you buy the November series expiry.

The rate of increase of premium will be same for both 2850CE and 2900CE???

Again, that depends on the time to expiry.

Current HDFC spot price in market is 2814. I think the stock price will go up and want to buy a call option.

What is better/difference between the below two options.

1) 2850 CE at a premium price of 37.75

2)2900 CE at a premium price of 24.6

So if the stock price goes up as i expected the premiums also goes up in above two CE option.

So taking 2900 CE option is better as the premium is less than taking a 2850 CE?

please confirm if my understanding is correct.

Yes, usually the call option premium increases when the stock price increases. The extent to which the premium will move up depends on the extent to which the stock price moves.

Hello Karthik,

I bought 1 lot of HDFC 740 ce at 20.15 ,lot size 1100.Currently the spot price is 709 and the value of my call is now 8.90.

i have a few questions:-

1.what if the spot stays at the same place at the time of expiry,will i lose my total capital of 20.15×1100?

2. In order to get breakeven,how much should my spot price of the stock move now so that i breakeven at 20.15?

3.when i bought the call at 20.15 ,the spot price was 735.so will it mean that if the spot price right now goes to 735,i will break even again?

sir,i find it confusing to understand how premiums behave and what value will they be later.how understand what their value will remain?

1) Yes, assuming you hold the position to expiry

2) Strike + premium

3) Yes, that\’s possible considering there is enough time to expiry

Premiums are a function of many things, Ajit. You need to spend time observing the markets and eventually, you will figure this out 🙂

If I took overnight position : Ex: WIPRO OCT 640 CE for 1 lot, I can sell before oct 28th ? or after also?

Is this monthly one, how to identify weekly one?

Yes, you can sell anytime on or before the expiry.

If I buy WIPRO OCT 640 CE @29 (1 Lot 1600)Today and sell @30 on today or Tomorrow, so my profit is 1600

Q1) Here I will get 1600 profit and there is no obligation before expiry of Oct month cycle right?

Q2) My amount will reflect after T+2 right?

Q3) Can I sell option first and buy later in intraday?

Q4) Is there any other obligation in that question scenario?

1) Yes, thats right

2) On T+1

3) Yes, you can

4) No obligation.

i wanted to ask how can i buy next week\’s option on the present day, like i know the literal way of doing it, wanted to know which options among overnight or nrml , ioc etc to choose.

Thanks Karthik, for making it clear.

Happy trading, Rupali.

THANKS Karthik for such details document with example.

I have a query-

If Bank Nifty\’s sopt price 37000 and I buy call @ strike price 36500 and on expiry spot price goes to 36700 then what will be the P&L?

Then the option is ITM with 200 intrinsic value. Your profit will be 200 * number of lots * lot size.

For a retail investors buying CE or PE is better than selling because in Selling option he may lose all the money.

Question no 1 : if somebody incurred a loss of 1 lakh in selling options but he has only 2000 Rs in Zerodha account so how Zerodha will recover the money from customer.

Question no 2 In option trading which one is better intradey or delivery.

Question no 3 why 90% retails investor (including myself) regularly incurring loss in trading. I am alive in market because 90% of total amount I have invested in top 6 companies of NIFTY 50 with BUY on Dip strategy.

Question no 4

Why it is too much complicated that a science doctorate with mathematics background is unable to snatch profits. It means it is only an organized loot by big investors.

1) The max loss allowed from the risk management system will be 2000. But there will be situations (when markets move rapidly) where the loss will be higher than the margins, this is the risk that the broker will have to manage. Eventually, the client is liable to pay the broker.

2) I personally prefer delivery

3) Most option traders enter the market without fully understanding the risk, hence.

4) Human emotions is beyond a science doctorate 🙂

Sir if I buy Nifty sep 18000 CE at 15 and hold it

1.When will it expire?

3. Do I have to pay premium everyday till the expiry?

3. If I make a profit on or before expiry will my profit include all my premium I had paid?

1) On the expiry date i.e. the last Thursday of the month

2) No, the premium is paid only once, i.e. at the time of buying

3) Yes.For example, you can buy an option at 20 and sell it at 25 before expiry.

how to buy 16700 ce 30 sep expiry

Please check the marketwatch, load the scrip, and hit the buy button.

Karthik Sir, Good morning. Need a clarification.

1. There is lot of confusion among option traders regarding whether we have to consider the spot price or future price while calculating the Intrinsic value. Suppose I want to check the time value for a given strike say 16700 of Nifty fifty which is ITM for PUT. I am considering Nifty 50 Spot. This helps me to check whether the time value on 16700PE ITM PUT is more or Time value on 16700CE OTM Call is more. Using this info I will decide whether to write call or put. Requesting you to kindly clarify please sir. In your write up you have mentioned that to calculate Intrinsic value we have to consider Sot price.

Warm regards.

Premakumar Kootagal Sanjeevaiah

Since index spot is not traded, you can consider Index futures as reference. For stocks, you can consider the spot.

I have a doubt regarding trading options intraday.If I have 50k rupees in my trading account,how many times can I trade nifty options of the same and different strike prices with the same amount.Will there be any margin penalty for the above situations?

You can trade the strikes as many times as you wish. No restriction on that.

can the premium increase for the same strike price, after i have brot it ?

Yes, it can.

How many times can i buy a call option for one strike price in a day

As many times as you\’d want.

Sir,

I brought 4000 lot of usdinr 73.5pe 6th August at 0.0025 on 3rd August what happens if I failed to sell those before expiry and is it in the money or out of the money how much I can get back

It depends on the settlement price of USDINR. If its OTM, the option will expire worthless.

Hi,

I had bought a lalpath labs 2700ce(itm) at 190 of 250 quantity. Cmp was at 2800 levels. A friend had bought 2900ce at premium 97. I calculated breakeven to be 2700+190. Friend\’s breakeven should be 2900+97. Cmp at 2888. He claims to have made a profit by selling at 147 bought at 97.

So breakeven doesn\’t matter? What am I missing?

You would be relieving me off a tremendous headache if you could answer.

Thank you.

There are two things, Thulasi –

1) Holding on to the options till expiry and exercising it

2) Trading the premiums actively

Breakeven comes to the picture when you intend to hold the option expiry. But before expiry, you can actively buy and sell the options. Your P&L depends on what price you buy and sell the option (like your friend did).

I know that karthik.

I am looking for the probability of increase in premium if NAM INDIA stock moves up.

What if it reaches the level 415 rs, 420 rs, And even 425 rs (Which is my strike price) ???

Can i calculate or atleast estimate the increase in premium with increase in Stock price(Spot price) to above mentioned different levels ???

I am a beginner in options trading. In my first 2 trade i made handsome profit just on the basis of checking VOLUME, VOLATALITY, O.I, AND, 20 DEPTH.

I have been reading your articles for past few days after checking and searching through many other sources available online.

Your way of explaining things is awesome. Its very simple and at the time Very Unique. I am making hand written notes of some important topics.

Thanks.

Kaushal, the stock is OTM. YOu can do a few things if you still feel bullish about the stock –

1) Sell OTM Puts (although I\’m not a fan of selling puts)

2) Sell 425 CE and buy 400 CE

3) Buy futures

Dear bro.

I purchased NAM INDIA 425 C.E july expiry at price 8.5 rs.

2 times i missed to book profit as i forgot to place GTT SELL ORDER.

Now the stock is moving somewhere 398 rs and my premium has gone down to 2.15 rs from 8.50 rs.

9 days lefts for expiry.

Should i wait till expiry.

Or what?

Thanks.

Its simple Kaushal, if you are still bullish and expect NAM to move higher than 425, over the next 5 days, then stay put, else there is no need to hold the option.

Sir, If I buy suppose irctc 2000 ce and sell after half n hour and I want to buy it again on same day after 1 hour, is it possible?

Yes, that\’s possible Yogesh.

In one word ,simply outstanding clarification of the Call by Karthik.I personally want to meet him and want to request him to be my teacher for option and sharemarket understanding because his knowledge is very high and i am a big fan of it.

Karthik sir,if you have your email id please share with me so that i can be in touch with you for my queries regarding option jargons.

The service provided by varsity and especially by Karthik sir is simply outstanding. Five Star rating from me.

Thanks for the kind words, Rupesh. I\’m glad you liked the content. I\’m fairly active on Varsity. So whatever your queries, please post here. I will try and resolve it here itself. Thanks.

Dear Sir

I bought Jindal Steel CE 430 of 29 July expiry at a premium of 4 and sell it if it reaches 5, am I making a profit of 1*2500=2500 or losing RS 10000 I,e 4*2500 as the said stock is trading at 397

You bought at 4 and sold at 5, so you make a profit of 1.

I appreciate the effort that\’s put into creating this good tutorial. However repetitive reference to Futures (some other tutorial) sticks out like a sore thumb. Why do you have to do that? This reference has zero value actually, doesn\’t add anything to the current tutorial, instead only confuses someone who hasn\’t gone through that tutorial yet.