It’s the economy, stupid! Of dollars and disinflation

We love India Data Hub’s weekly newsletter, ‘This Week in Data’, which neatly wraps up all major macroeconomic data stories for the week. We love it so much, in fact, that we’ve taken it upon ourselves to create a simple, digestible version of their newsletter for those of you that don’t like econ-speak. Think of us as a cover band, reproducing their ideas in our own style. Attribute all insights, here, to India Data Hub. All mistakes, of course, are our own.

We’re bringing inflation under control!

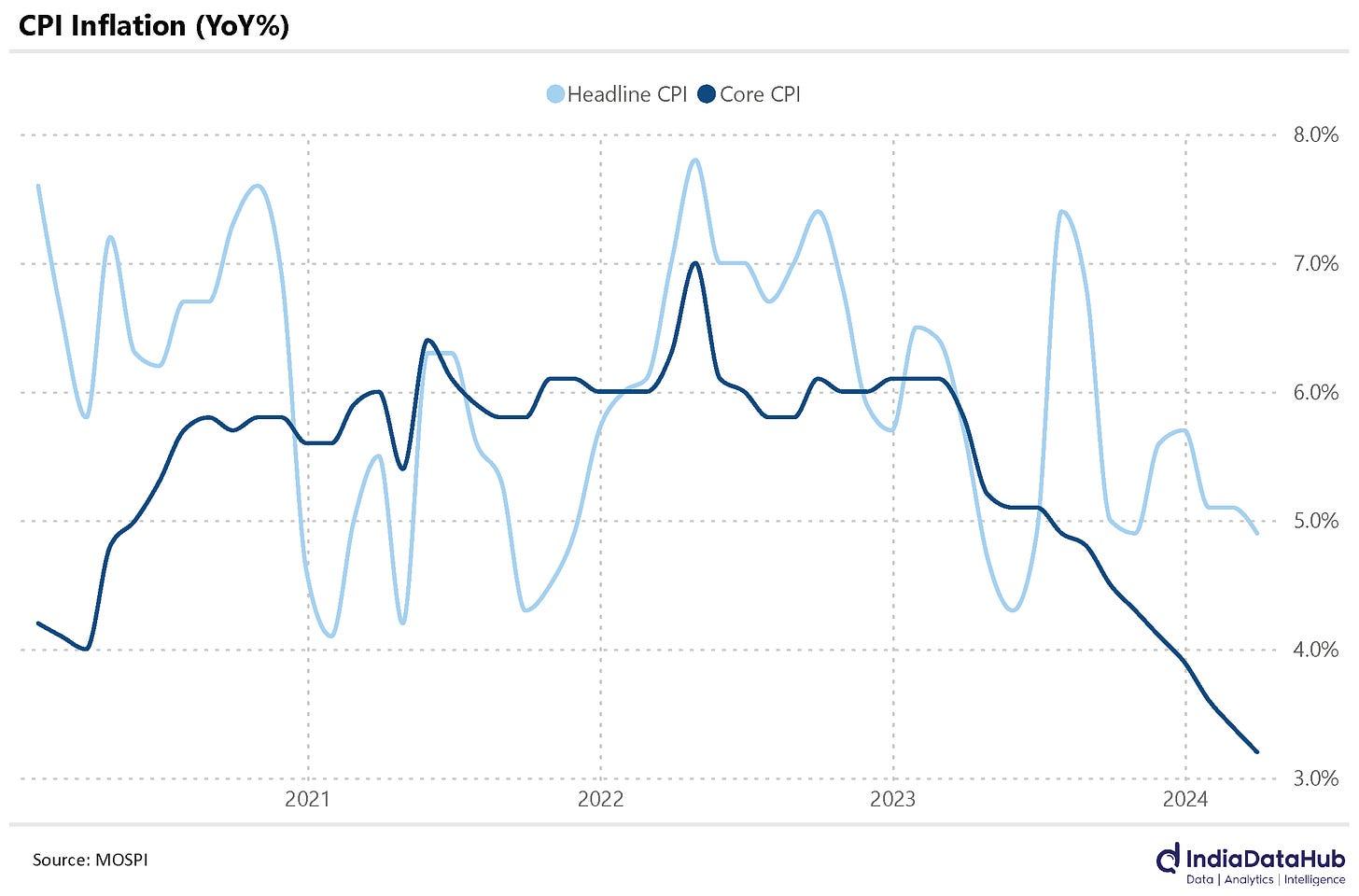

India’s inflation fell to 4.85% in March. This is well below the 5.1% inflation reading from the previous two months, and the lowest it has been since May last year.

That’s just the headline, however. Inflation measures rising prices in general. But the price of everything doesn’t rise together – some prices, naturally, grow faster than others. There’s more to learn if you look at the fineprint.

India’s ‘core inflation’ – inflation in everything other than food and energy – is at a record low of 3.25%. Indian policymakers have little control over how expensive food and energy are: we import most of our energy from abroad, while the business of growing food is literally as unpredictable as the weather. We have more control over core inflation, however, and it looks like we’re doing a decent job of it.

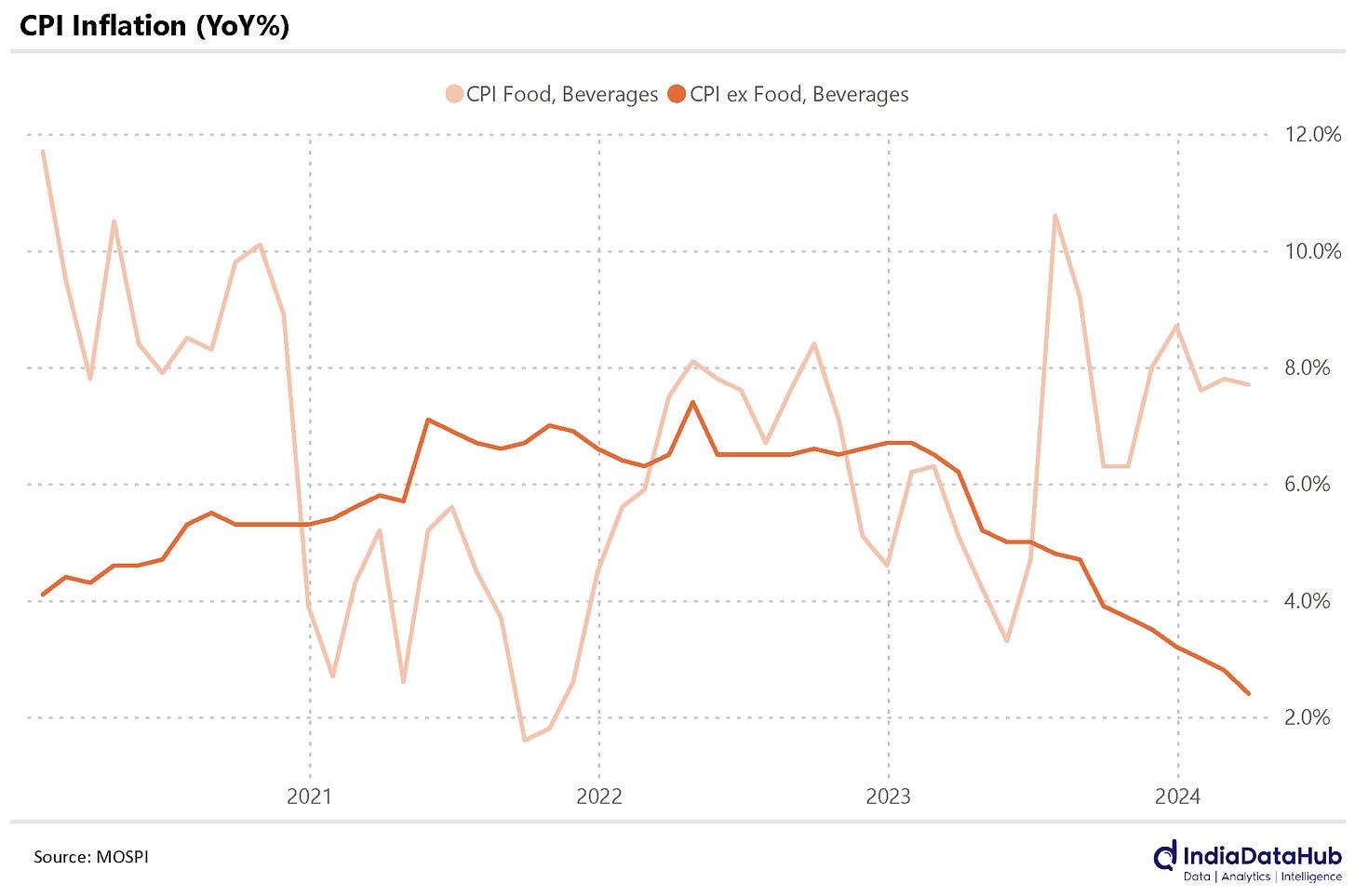

A lot of our inflation comes from the high, and growing, prices of food and beverages. In March, food and beverage inflation was at 7.7% over the previous year – a level it has been at for the two preceding months. Unlike what this high figure would suggest, interesting, the prices of many types of food are actually stabilising. The prices of milk, pulses, fruits and vegetables, for instance, are growing slower than they previously were. The prices of cereals and meat, alas, have spiked up, keeping overall inflation high.

If you could only ignore food, somehow, our inflation for the month would fall below 3%.

Dealing with inflation, as we’ve mentioned before, is among the RBI’s primary jobs. Now that inflation is coming under control, it might consider pulling down its ‘policy repo rate’. This rate determines how expensive it is for a bank to take loans, and by extension, how easy it is for new money to enter the economy.

Having completed a meeting of its ‘monetary policy committee’ (which decides the repo rate) only a couple of weeks ago, however, the RBI will probably not take such a call anytime soon. In the meanwhile, it has enough to occupy its attention. The Middle East threatens to break into all-out conflict. Unfortunately, that happens to be where we import most of our oil from. If our import bills balloon and start eat into our foreign exchange reserves, the RBI will have its hands full – with little time to think about interest rates.

A strong Rupee and a stronger Dollar

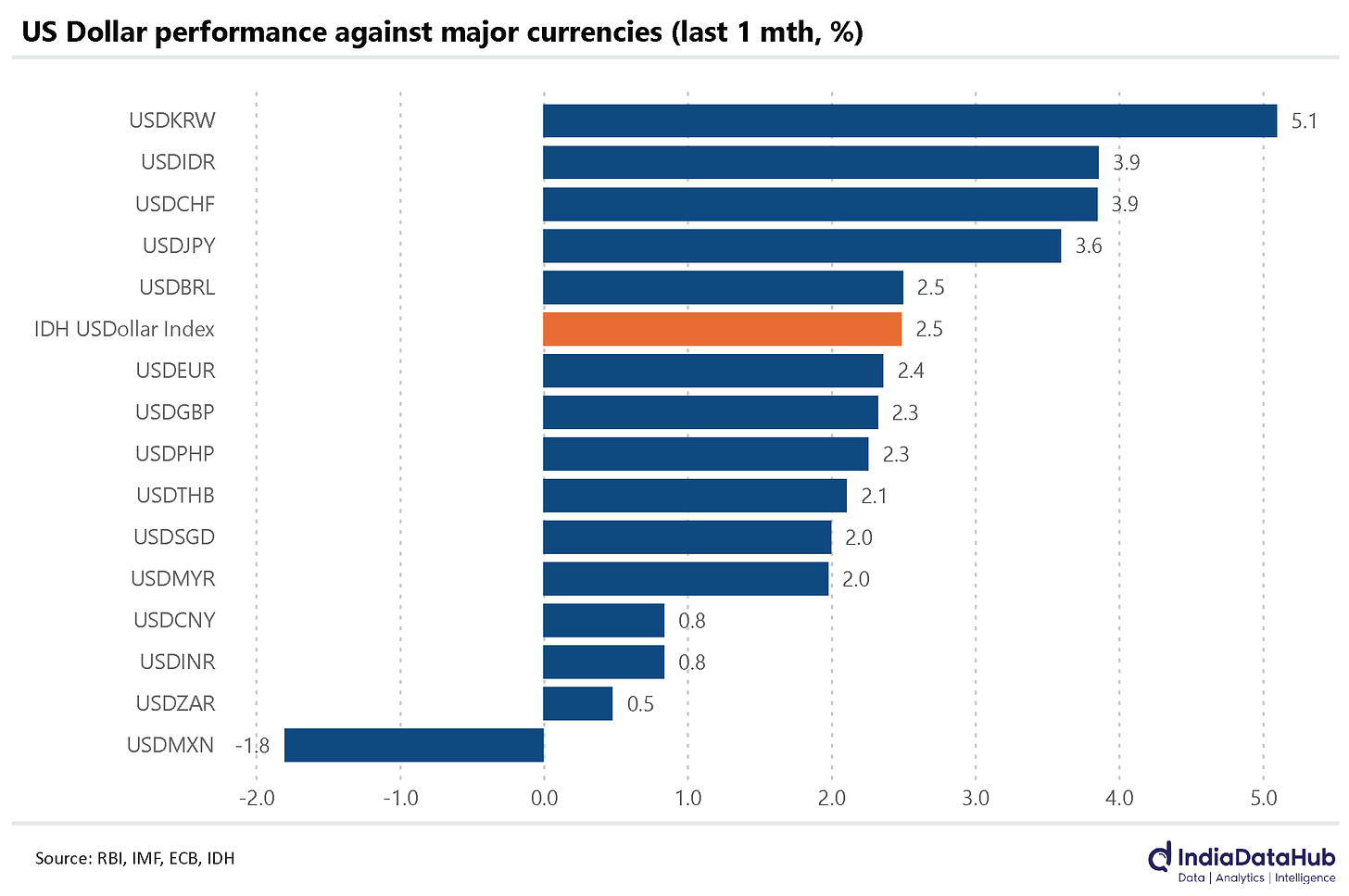

As rising tensions in the Middle East spook the world, people are rushing to secure their money. How can they best do that? By buying the world’s safest currency – the US Dollar – and other assets that are priced in US Dollars. The demand for the Dollar has spiked. As per India Data Hub’s proprietary US Dollar Index, the dollar has appreciated by 2.5% in just the last month.

Naturally, compared to a more expensive Dollar, most world currencies have dropped in value.

Asian currencies have been hit the hardest. The Korean Won dropped by ~5% over the last month. The Japanese Yen and the Indonesian Rupiah both fell by ~4%. In comparison, the Indian Rupee’s ~1% decline – to 83.5 Rupees to the Dollar – makes it look quite robust.

The Chinese Yuan, too, has also shown a similar, limited decline of ~1%.

Money pours into India

So why is the Rupee doing well, as world currencies go?

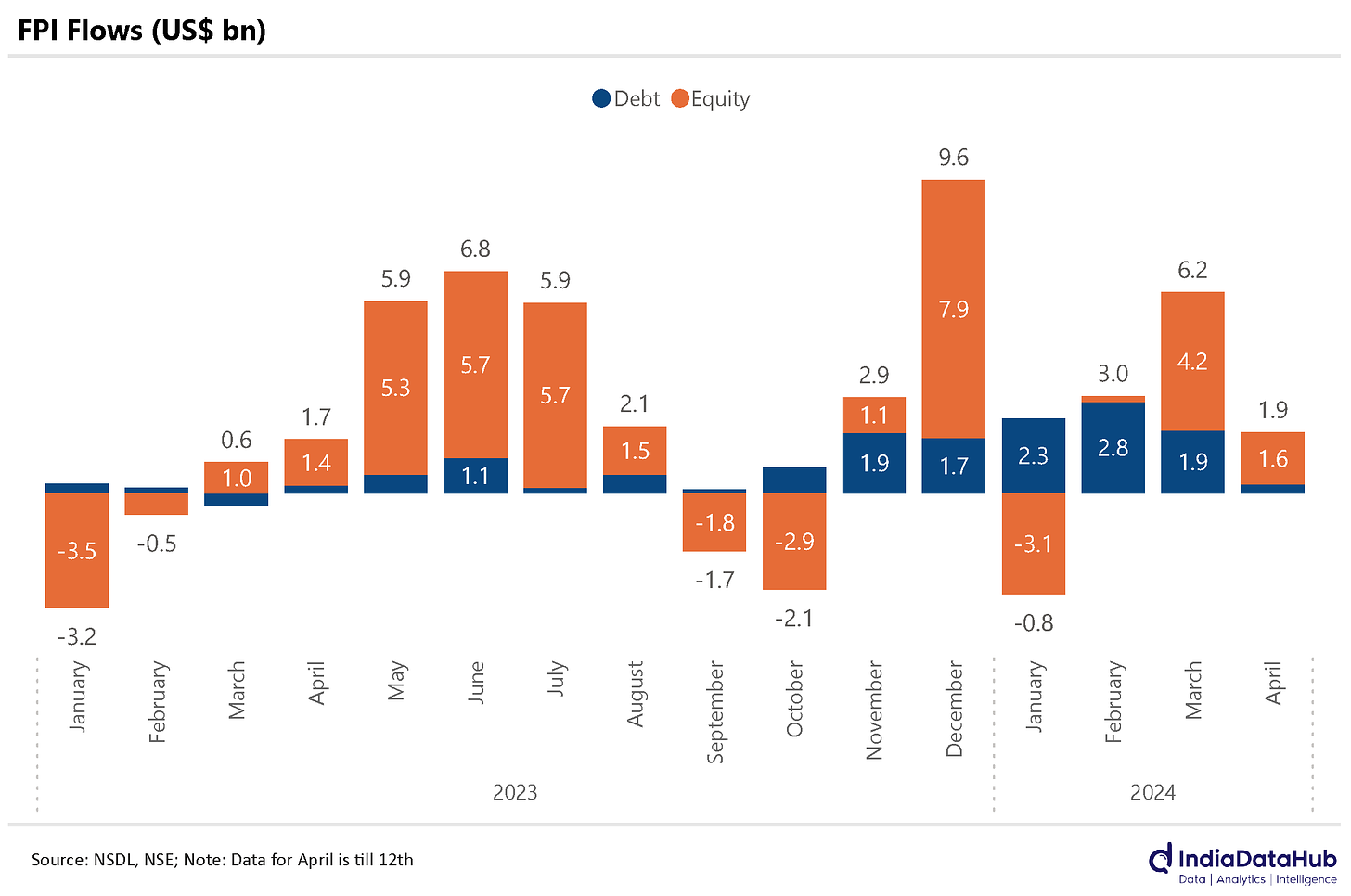

Here’s one reason: a lot of investment is flowing into the country. India’s debt markets have seen heavy foreign portfolio investment since November last year: averaging at US$ 2 billion every month. A total of almost US$ 11 billion in foreign portfolio investment entered Indian debt markets through this time.

If you’re wondering what foreign portfolio investment even is, by the way, we’ve gone into it before:

“…you take a punt on [another country’s] capital markets. You buy stocks, bonds, or something similar, and see where they go. You aren’t trying to get your hands dirty or make something – you’re just along for the ride. Much like you might be in the capital markets of your own country. This is called ‘foreign portfolio investment’ (FPI).”

Indian equity markets saw a lot of foreign money come in as well through this time, even though it came in irregular bursts unlike the steady hum of debt investment. In total, Indian equity markets saw an additional US$ 10 billion enter India as foreign portfolio investment since November.

In all, these five months have seen an incredible US$ 20 billion enter the country as foreign portfolio investment. And this same frenetic pace has continued into April: with US$ 2 billion having come in, even though half a month still lies ahead.

A wealth of foreign exchange

With all this money flowing in, India’s foreign exchange reserves have been growing. If you’re not quite sure what that means, don’t worry. We have you covered – we’ve done this before:

“A country’s ‘foreign exchange reserves’ work a little like its savings. Like your personal savings, these reserves can have many uses.

The country can use them to buy its own currency in international markets, to make its value go up. It can use them to pay off debts. If things go seriously wrong, it can use them to import essentials. They don’t have a single, defined purpose – they help a country ride out any monetary shocks it would otherwise face.”

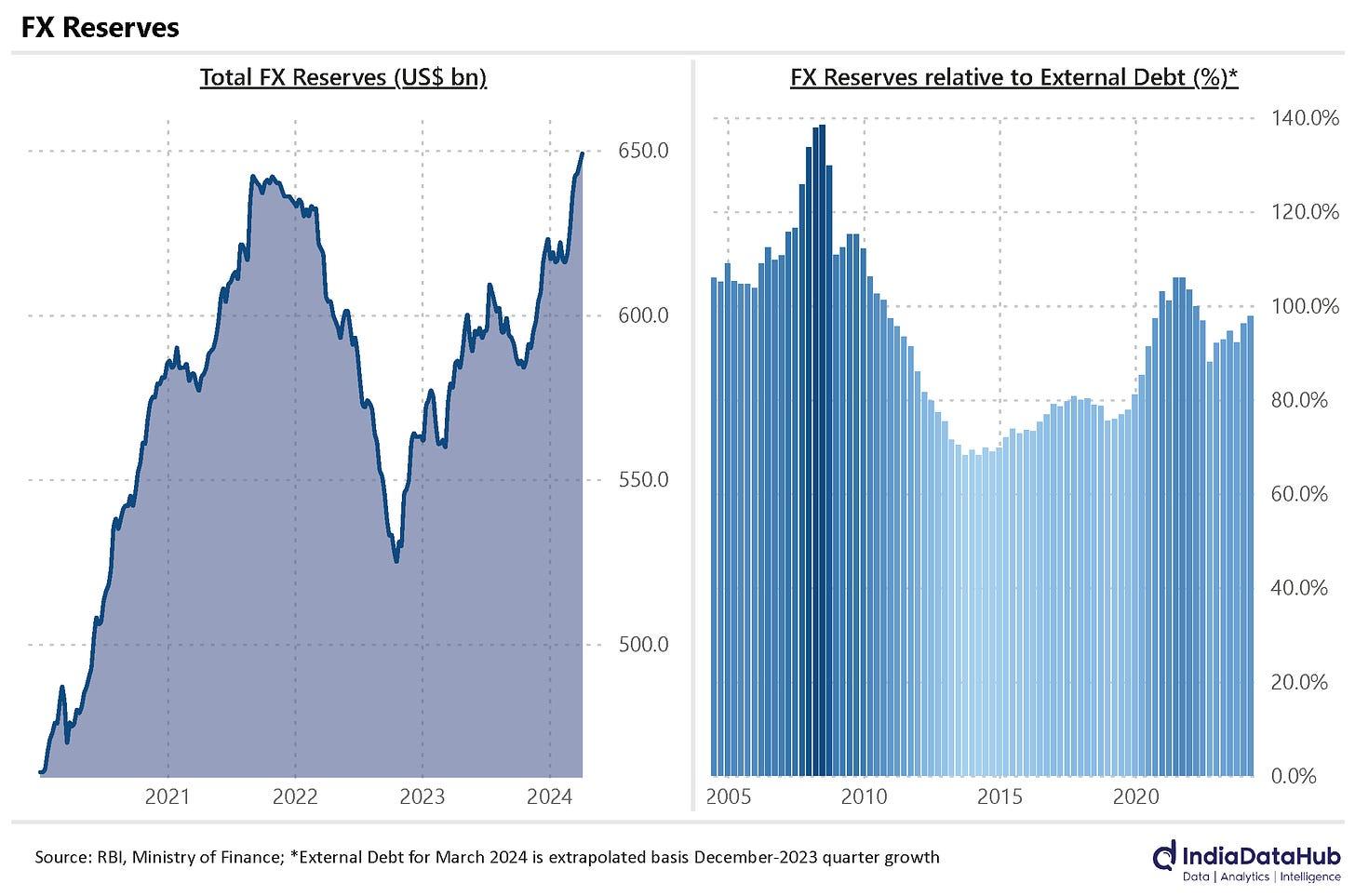

In early April, they had zoomed up to US$ 650 billion – the highest they’ve ever been. For some context, until last year, their highest ever peak was ~US$ 60 billion below this. Our foreign exchange reserves have swollen by US$ 30 billion in the two months since mid-February alone.

Having US$ 650 billion in the bank buys us a lot of mental peace. For one, India’s total external debt, as of December 2023, was at US$ 648 billion. This might have jumped up to somewhere around ~US$ 660 billion in March, but the point remains. If the Indian economy went into some sort of sudden free fall, we’d still have enough money to pay off almost all our debt in one go.

It’s not as though we actually have to pay our debts any time soon. But if we can pay off all our foreign debts, there are a lot of other things we can do. For instance, if we took a sharp economic hit in the Middle East conflict and started bleeding money, we’d still be able to sustain ourselves for a while. Our treasury gives us some much-needed resilience in these tense times.

American prices go up

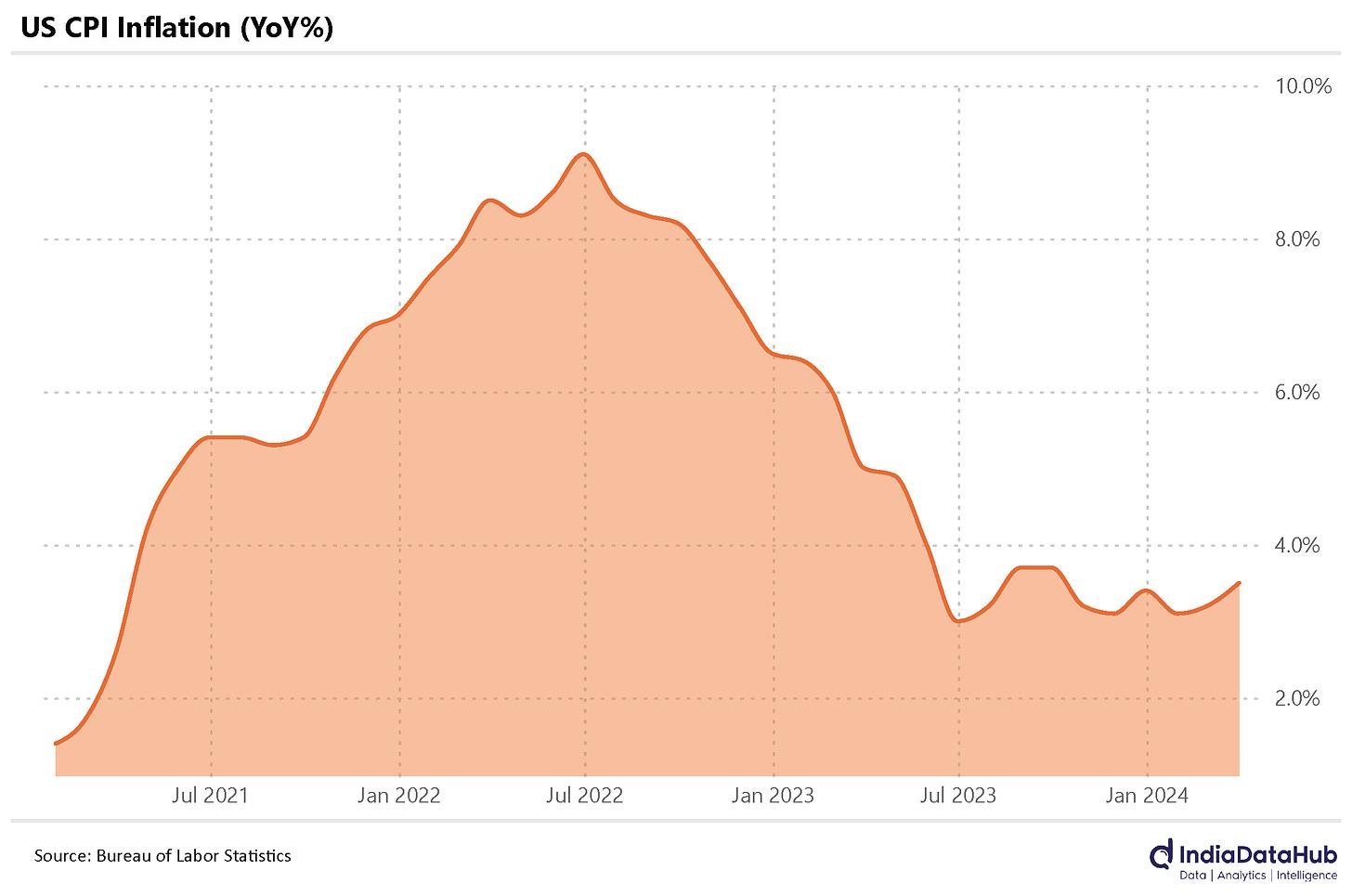

After hovering around 3% for a while, inflation in the United States shot up to 3.5% this March. A big departure from the last few months came in energy prices – which rose by 2.1% in March, compared to a year ago, after declining for twelve months on the trot. Food was 2.2% more expensive than last March, and energy was 5.7% more expensive – which was around how things were in February.

If the US Fed was considering cutting interest rates any time soon, well, it’s certainly not doing so any more. The markets too have come to terms with this reality. At the earliest, the markets are hoping for a rate cut in July. And this, too, is touch-and-go; they aren’t attributing a rate cut any higher a chance than 55%.

If the US Fed was considering cutting interest rates any time soon, well, it’s certainly not doing so any more. The markets too have come to terms with this reality. At the earliest, the markets are hoping for a rate cut in July. And this, too, is touch-and-go; they aren’t attributing a rate cut any higher a chance than 55%.

Meanwhile, the European Central Bank has kept rates exactly where they were: at 4.5%.

That’s all for the week, folks. Thanks for reading!

Your insights are impressive. Looking forward to more content like this. Visit us