8.1 – Overview

The Cash flow statement is a significant financial statement, as it reveals how much cash the company is actually generating. Is this information not revealed in the P&L statement you may think? Well, the answer is both a yes and a no.

Consider the following scenario.

Assume a simple coffee shop selling coffee and short eats. All the shop’s sales are mostly on a cash basis, meaning if a customer wants to have a cup of coffee and a snack, he needs to have enough money to buy what he wants. On a particular day, assume the shop manages to sell Rs.2,500/- worth of coffee and Rs.3,000/- worth of snacks. The shop’s income is Rs.5,500/- for that day. Rs.5,500/- is reported as revenues in P&L, and there is no ambiguity with this.

Now think about another business that sells laptops. For the sake of simplicity, let us assume that the shop sells only 1 type of laptop at a standard fixed rate of Rs.25,000/- per laptop. Assume on a certain day; the shop manages to sell 20 such laptops. Clearly the revenue for the shop would be Rs.25,000 x 20 = Rs.500,000/-. But what if 5 of the 20 laptops were sold on credit? A credit sale is when the customer takes the product today but pays the cash at a later point in time. In this situation here is how the numbers would look:

Cash sale: 15 * 25000 = Rs.375,000/-

Credit sale: 5 * 25000 = Rs.125,000/-

Total sales: Rs.500,000/-

If this shop were to show its total revenue in its P&L statement, you would see revenue of Rs.500,000/- which may seem good on the face of it. However, how much of this Rs.500,000/- is actually present in the company’s bank account is not clear. What if this company had a loan of Rs.400,000/- that had to be repaid urgently? Even though the company has a sale of Rs.500,000, it has only Rs.375,000/- in its account. This means the company has a cash crunch, as it cannot meet its debt obligations.

The cash flow statement captures this information. A statement of cash flows should be presented as an integral part of an entity’s financial statements. Hence in this context evaluation of the cash flow statement is highly critical as it reveals, amongst other things, the true cash position of the company.

To sum up, every company’s financial performance is not so much dependent on the profits earned during a period, but more realistically on liquidity or cash flows.

8.2 – Activities of a company

Before we understand the cash flow statement, it is important to understand ‘the activities’ of a company. If you think about a company and the various business activities, you will realize that the company’s activities can be classified under one of the three standard baskets. We will understand this in terms of an example.

Imagine a business, maybe a very well established fitness centre (Talwalkars, Gold’s Gym etc.) with a sound corporate structure. What are the typical business activities you think a fitness centre would have? Let me go ahead and list a few business activities:

- Display advertisements to attract new customers

- Hire fitness instructors to help clients in their fitness workout

- Buy new fitness types of equipment to replace worn-out equipment.

- Seek short term loan from bankers

- Issue a certificate of deposit for raising funds

- Issue new shares to a few known friends to raise fresh capital for expansion (also called preferential allotment)

- Invest in a startup company working towards innovative fitness regimes

- Park excess money (if any) in fixed deposits

- Invest in a building coming up in the neighbourhood, for opening a new fitness centre sometime in the future

- Upgrade the sound system for a better workout experience

As you can see, the above-listed business activities are quite diverse; however, they are all related to the business. We can classify these activities as:

- Operational activities (OA): Activities related to the daily core business operations are called operational activities. Typical operating activities include sales, marketing, manufacturing, technology upgrade, resource hiring etc.

- Investing activities (IA): Activities about investments that the company makes intending to reap benefits at a later stage. Examples include parking money in interest-bearing instruments, investing in equity shares, investing in land, property, plant and equipment, intangibles and other non-current assets etc.

- Financing activities (FA): Activities about all financial transactions of the company such as distributing dividends, paying interest to service debt, raising fresh debt, issuing corporate bonds etc

All activities a legitimate company performs can be classified under one of the above three mentioned categories.

Keeping the above three activities in perspective, we will now classify each of the above-mentioned activities into three categories /baskets.

- Display advertisements to attract new customers – OA

- Hire fitness instructors to help customers with their fitness workout – OA

- Buy new fitness equipment to replace worn-out equipment – OA.

- Seek a short term loan from bankers – FA

- Issue a certificate of deposit (CD) for raising funds – FA

- Issue new shares to few known friends to raise fresh capital for expansion (also called preferential allotment) – FA

- Invest in a startup company working towards innovative fitness regimes – IA

- Park excess money (if any) in fixed deposit – IA

- Invest in a building coming up in the neighbourhood for opening a new fitness centre sometime in the future – IA

- Upgrade the sound system for better workout experience- OA

Now think about the cash moving in and out of the company and its impact on the cash balance. Each activity that the company undertakes has an impact on cash. For example “Upgrade the sound system for a better workout experience” means the company has to pay money towards purchasing a new sound system. Hence the cash balance decreases. It is also interesting to note that the new sound system itself will be treated as a company asset.

Keeping this in perspective, we will now understand for the example given above how the various activities listed would impact the cash balance and how would it impact the balance sheet.

| Activity No | Activity Type | Rational | Cash Balance | On Balance Sheet |

|---|---|---|---|---|

| 01 | OA | Expenditure on advertisement | Decreases | Treated as an asset as it increases the brand value |

| 02 | OA | Expenditure towards recruits | Decreases | Treated as an asset as it increases the company’s intellectual capital |

| 03 | OA | Expenditure on new equipment | Decreases | Treated as asset |

| 04 | FA | Loan means cash inflow to business | Increases | The loan is a liability |

| 05 | FA | Deposits via CD means cash inflow | Increases | CD is a liability |

| 06 | FA | Issue of fresh capital means cash inflow | Increases | Treated as a liability as share capital increases |

| 07 | IA | Investment in a startup means cash outflow | Decreases | Investment is an asset |

| 08 | IA | Money parked in FD means cash going out of business | Decreases | Equivalent to cash, hence considered an asset |

| 09 | IA | Investment in the building means cash going out of business | Decreases | Gross block considered an asset |

| 10 | OA | Expenditure towards the sound system | Decreases | Treated as an asset |

The table above is colour coded:

- Increase in cash is colour coded in blue

- The decrease in cash is colour coded in red

- Assets are colour coded in green and

- Liabilities are colour coded in purple.

If you look through the table and start correlating the ‘Cash Balance’ and ‘Asset/Liability’ you will observe that:

- Whenever the liabilities of the company increases, the cash balance also increases.

- This means if the liabilities decreases, the cash balance also decreases.

- Whenever the asset of the company increases, the cash balance decreases.

- This means if the assets decreases, the cash balance increases.

The above conclusion is the key concept while constructing a cash flow statement. Also, extending this further, you will realize that each company’s activity is its operating activity, financing activity, or investing activity either produces cash (net increase in cash) or reduces (net decrease in cash)the cash for the company.

Hence the total cash flow for the company will be:-

| Cash Flow of the company = Net cash flow from operating activities + Net Cash flow from investing activities + Net cash flow from financing activities |

8.3 – The Cash Flow Statement

Having some insight into the cash flow statement, you would now appreciate that you need to look into the cash flow statement to review the company from a cash perspective.

Typically when companies present their cash flow statement, they split the statement into three segments to explicitly show how much cash the company has generated across the three business activities. Continuing with our example from the earlier chapters, here is the cash flow statement of Amara Raja Batteries Limited (ARBL):

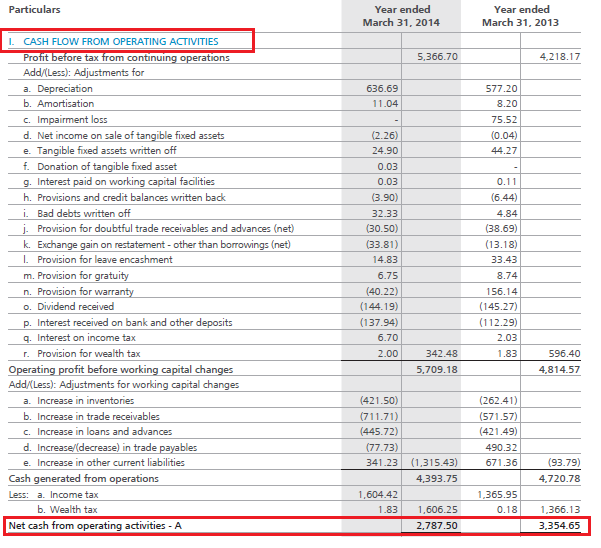

I will skip going through each line item, as most of them are self-explanatory. However, please notice that ARBL has generated Rs.278.7 Crs from operating activities. Note, a company with a positive cash flow from operating activities is always a sign of financial well being.

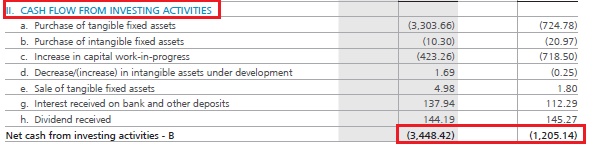

Here is the snapshot of ARBL’s cash flow from investing activities:

As you can see, ARBL has consumed Rs.344.8 Crs in its investing activities. This is quite intuitive as investing activities tend to consume cash. Also, remember healthy investing activities foretells the investor that the company is serious about its business expansion. Of course, how much is considered healthy and how much is not, is something we will understand as we proceed through this module.

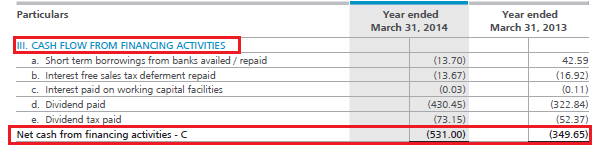

Finally, here is the snapshot of ARBL’s cash balance from financing activities:

ARBL consumed Rs.53.1Crs through its financing activities. If you notice the bulk of the money went in paying dividends. Also, if ARBL takes on new debt in the future, it would increase the cash balance (remember the increase in liabilities, increases cash balance). We know from the balance sheet that ARBL did not undertake any new debt.

Let us summarize the cash flow from all the activities:

| Cash Flow from | Rupees Crores (2013-14) | Rupees Crores (2012-13) |

|---|---|---|

| Operating Activities | 278.7 | 335.4 |

| Investing Activities | (344.8) | (120.05) |

| Financing Activities | (53.1) | (34.96) |

| Total | (119.19) | 179.986 |

This means the company consumed total cash of Rs.119.19 Crs for the financial year 2013 -2014. Fair enough, but what about the cash from the previous year? As we can see, the company generated Rs.179.986 Crs through all its activities from the previous year. Here is an extract from ARBL’s cash flow statement:

Look at the section highlighted in green (for the year 2013-14). It says the opening balance for the year is Rs.409.46Crs. How did they get this? Well, this happens to be the closing balance for the previous year (refer to the arrow marks). Add to this the current year’s cash equivalents (Rs.119.19) Crs along with a minor forex exchange difference of Rs.2.58 Crs we get the company’s total cash position which is Rs.292.86 Crs. This means, while the company guzzled cash every year, they still have adequate cash, thanks to the previous year’s carry forward.

Note, the closing balance of 2013-14 will now be the opening balance for the FY 2014 – 15. You can watch out for this when ARBL provides its cash flow numbers for the year ended 31st March 2015.

At this point, let us run through a few interesting questions and answers:

- What does Rs.292.86 Crs actually state?

- This literally shows how much cash ARBL has in its various bank accounts.

- What is cash?

- Cash comprises cash on hand and demand deposits. Obviously, this is a liquid asset of the company.

- What are liquid assets?

- Liquid assets are assets that can be easily converted to cash or cash equivalents.

- Are liquid assets similar to ‘current items’ that we looked at in the Balance sheet?

- Yes, you can think of it that way.

- If cash is current and cash is an asset, shouldn’t it reflect under the Balance sheet’s current asset?

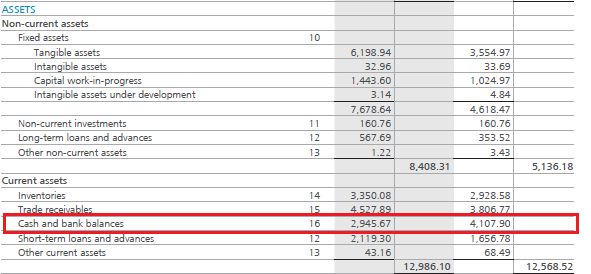

- Exactly and here it is. Look at the balance sheet extract below.

Clearly, we can now infer that the cash flow statement and the balance sheet interact with each other. This is in line with what we had discussed earlier, i.e. all the three financial statements are interconnected.

8.4 – A brief on the financial statements

Over the last few chapters, we have discussed the company’s three important financial statements, i.e. the P&L statement, the Balance Sheet and the Cash Flow statement of the company. While the Cash flow and P&L statement are prepared on a standalone basis (representing the given year’s financial position), the Balance Sheet is prepared on a flow basis.

The P&L statement discusses how much the company earned as revenues versus how much the company expanded in terms of expenses. The company’s retained earnings, also called the surplus of the company, are carried forward to the balance sheet. The P&L also incorporates the depreciation number. The depreciation mentioned in the P&L statement is carried forward to the balance sheet.

The Balance Sheet details the company’s assets and liabilities. On the liabilities side of the Balance sheet, the company represents the shareholders’ funds. The assets should always be equal to the liabilities; only then do we say the balance sheet has balanced. One of the key details on the balance sheet is the cash and cash equivalents of the firm. This number tells us how much money the company has in its bank account. This number comes from the cash flow statement.

The cash flow statement provides information to the users of the financial statements about the entity’s ability to generate cash and cash equivalents and indicates the cash needs of a company. Cash flows are prepared on a historical basis providing information about the cash and cash equivalents, classifying cash flows in to operating, financing and investing activities. The final number of cash flow tells us how much money the company has in its bank account.

We have so far looked into how to read the financial statements and what to expect from each of them. We have not yet ventured into how to analyze these numbers. One of the ways to analyze the financial numbers is by calculating a few important financial ratios. In fact, we will focus on the financial ratios in the next few chapters.

Key takeaways from this chapter

- The Cash flow statement gives us a picture of the true cash position of the company.

- A legitimate company has three main activities – operating activities, investing activities and the financing activities.

- Each activity either generates or drains money for the company.

- The company’s net cash flow is the sum of operating activities, investing activities, and financing activities.

- Investors should specifically look at the cash flow from operating activities of the company.

- When the liabilities increase, cash level increases and vice versa

- When the assets increase, cash level decreases and vice versa.

- The net cash flow number for the year is also reflected in the balance sheet.

- The Statement of Cash flow is a useful addition to a company’s financial statements because it indicates the company’s performance.

Hi Karthik,

I am on FA module-Chapter 8. Do you think I should start trading at this point? If I wait until I complete all the modules, I might forget a few things. Additionally, I do not know how to short hence I thought I will complete all the modules where shorting will also be covered and then start Investing & Trading. Please advise!

I think its ok to take these trades in parallel. Especially if it helps you learn better.

Do you mean I should start trading(off course in very less quantity for now) & parallely learn about FA?

Hello Karthik,

I am seeing that \”Dividend received\” and \”Interest received on banks and other deposits\” and the values for these line items are present under the section \’Profit before tax from continuing operations\’ in \”cash flow from OA\” and \”cash flow from IA\”.

My questions:

(1) How can these came under both of the cash flows from OA and IA?

(2) Shouldn\’t these two should be under FA?

Under the indirect method, you start with PBT and then make adjustments. Since \”Dividend received\” and \”Interest received\” are included in Profit Before Tax (they\’re income in the P&L), they show up in the OA section..but only to be subtracted/reversed out, because they don\’t belong there.They then reappear under Investing Activities (IA) as the actual cash inflow, which is their correct home.

Hello Sir,

This is Sohan. I hope you have looked into the error I posted before.

I had one more question in the same module,

In the list of business activities it is said that issuing a certificate of deposits (CD) is regarded as financing activity.

My question is who is issuing a CD here, the bank or the business? Since businesses are not allowed to issue CD, and if banks are issuing CD then it must go under investing activity right?

Or did I misunderstood something here?

Sohan, private companies can issue CDs and NCDs to raise capital. Thats absolutely ok.

Hello Sir,

There is a slight correction on Page 86 of the PDF of Fundamental Analysis.

It is mentioned that the Net Profit Margin for ARBL is the same as PAT wiz calculated as 10.5 % on Page 83.

Bit on Pg 86 it is highlighted as 9.2%.

Subsequently this number is used in calculating RoE on Page 88 due to which the ROE has also been miscalculated.

Kindly Acknowledge the same.

On same note I am very thankful for the modules that has been provided here. The precision and simplicity has made the complex concept easy to learn. The way of explanation is also pretty on point and no room for confusion.

Thank you very much!

I hope to take a test soon after completion of the course.

Sohan, thanks so much the kind words, glad you liked the content. About the error, I\’ll look into it, thanks for pointing it out.

When the company is parking its excess cash in a cash deposit, its cash balance decreases but I don\’t get how it is a liability(with reference to the table given)?

Never mind, I misread

Sure, happy learning 🙂

Cash and cash equivalent remains same right?

Hi Karthik, I am a bit confused. how is issue of fresh capital treated as a liability as share capital increases? won\’t it be like the proceeds from the issuance of new shares increase the shareholders\’ equity section of the balance sheet?

as it increases the share capital account by the par value (or stated value) of the newly issued shares.

And any amount received above the par value is recorded as additional paid-in capital (also called share premium) within the shareholders\’ equity section? please clarify, I have got confused.

I dont know if this really makes sense, but perhaps it helps in a quick understanding. Think of the company as a person, and the balance sheet as a statement of funds the company is presenting to its shareholders. From the company’s perspective, share capital is a liability as it belongs to shareholders.

Hey, thanks for sharing that — I get what you mean now. Thinking of it like the company \”owes\” something to shareholders does help conceptually.

But yeah, just to clarify, in actual accounting terms, share capital isn’t treated as a liability. It’s part of shareholders’ equity on the balance sheet — the money from issuing shares goes into share capital and share premium (if any), all under equity.

Still, your perspective gave me a different way to look at it, so I appreciate that!

Thanks, happy learning 🙂

Hello Karthik. Thank you for the amazing module. It would be great if you could provide explanation of all the items in cash flow from operating activities.

I\’ve tried to do that to an extent. Will do this via a video maybe.

Thank you. That would be great

Sure. Happy learning, Rishabh 🙂

ARBL\’s Closing Cash and Cash Equivalent for FY14 was reported as 292.8 CR in the Cash Flow Statement. In the balance sheet, Cash and Bank Balances is reported as 294.5 Cr. Could you explain why there is a difference? Shouldn\’t these two entries match exactly, as you mentioned as three financial statements are interlinked?

It should, please do check the associated notes for this once.

As I was reading i got the same problem and i cross check the balance sheet also IN Asset section Cash and bank balance is 294.5 Cr but in the same FY14 closing Cash and cash equivalent was reported as 292.8 Cr. Why is miss calculation is arise?

hasn\’t it needed to be same sir?

Not really a miss calculation, but companies do restate their numbers by making minor adjustments. In this case its hardly 2cr, so it can be ignored. Only if the difference is large, then you will have to evaluate why and how.

Cash Flow from Rupees Crores (2013-14) Rupees Crores (2012-13)

Operating Activities 278.7 335.4

Investing Activities (344.8) (120.05)

Financing Activities (53.1) (34.96)

Total (119.19) 179.986

This table above is a bit confusing to me that you have provide

As Financing activity increase cash balance why is it negative and OA decreases the cash so why is it positive in this table to calculate total cashbalance

Finance activity can be -ve too, especially if there is dividend payout or debt repayment.

Thank you, Sir.

Happy learning!

In 8.2 the table you created there is activity type and cash balance status of that activity.

In Sr. no.: 1,2,3 & 10 the activity type is operational meaning \”Activities related to the daily core business operations are called operational activities. Typical operating activities include sales, marketing, manufacturing, technology upgrade, resource hiring etc.\”

due to which there is decrease in Cash balance because the company has to pay for these activities to be done.

Till this everything is right.

Problem arises here in 8.3 where you said that \”However, please notice that ARBL has generated Rs.278.7 Crs from operating activities.\”

my question is that how someone can generate cash from operational activities when one has to pay for doing operational activities.

Maybe I am missing something which I didn\’t understand if you find my mistake, please tell me.

Ah, because right at the top is the PAT, which is cash inflow. For other activities, cash is taken out from PAT. So you need to see this on an overall basis.

Well sir,

we saw that after operational activity the cash balance decreases so how it can be possible that the cash flow from operational activity is positive.

Need explanation where you showed \”ARBL has generated Rs.278.7 Crs from operating activities\”.

Decrease if ok, as long as the numbers are positive right? Sorry, I may not be getting the full context.

In Intermediate level quiz.. Question:9 regarding two parameters require to calculate EPS of share,the option seems wrong..it PAT/No of shares and it quiz correct option showing as Share price and No of outstanding shares

Ah, ok Biju. Need to double check this. Thanks for pointing out.

Cash Flow from Rupees Crores (2013-14) Rupees Crores (2012-13)

Operating Activities 278.7 335.4

Investing Activities (344.8) (120.05)

Financing Activities (53.1) (34.96)

Total (119.19) 179.986

could not understand the Total figures. i.e 119.19

Does the total mean the amount the company has in cash, after deducting cash outflows.

Thats right. Total cash flow is the sum of cash flows from all 3 activities.

Hi Karthik,

Thanks again for this wonderful work that you have done. Im slightly confused looking at this cashflow statement. How can a depreciation/amortization can be positive for a company?

As i would recall, the depreciation is nothing but the expenses splitted across its lifetime in P/L statement.

For example, buying a machinery for 5,00,000 whose expected lifetime is 5 years,

1. in P&L statement, under expenses, the depreciation would be 1,00,000.

2. In balance sheet, it would be 4,00,000 under assets (5,00,000-1,00,000(accumulated depreciation))

3. In cashflow statement, it should be total 5,00,000 under depreciation right? Since this amount went out of the company\’s pocket.

I\’m confused here. Please help me get clarified on this. Thanks.

Without depreciation, you\’d have to show the entire 5L as an expense in 1 shot. Now you can split this expense over the life of the asset, hence your bottom line improves.

How certificate of deposit id increasing cash and how can a gym lend CD?

Hi Karthik

While Cash flow from Investing and Financing activities are clear, I needed your help on the below:

1. Dividend received is subtracted from PBT. It should be a part of cash received (as it is cash inflow) so it should not be removed from PBT. But I guess it is removed from Operating activity and added under Investing activity as the dividend received is part of the company\’s investments. Is this correct?

2. Similar explanation can hold for Interest received on bank deposits.

3. Why do we need to subtract increase in inventory? It is already baked in the PBT in the form of various expenses like raw materials, WIP, etc. It need not be subtracted.

I understand items like recievables, loans and advances need to be subtracted to give the correct cash position but why inventory?

1) Yes, as in operating activity, the idea is to check for the cash flow situation purely from an operating activity perspective.

2) Yes, it can.

3) Increase in inventory is a cash drain, if the inventory increases, then it means the company is unable to offload it and convert the inventory to revenue. So in a sense its draining cash out of the company.

Hello Sir as you say every company has a three activities operating,investing and financing it\’s apply in bank also but when I see Banks cash flow statement the numbers are abnormal.

So I\’m confuse when applying in Banks cash flow statement.

You can largely apply that to banks as well. The numbers are abnormal becuase their operating activities is lending which involves lot of cash inflow and outflow.

In cash flow from OA why is the O-Dividend received and P-interest received negative? Please reply on email.

Think about it from cash received to bank and cash outflow from bank perspective. All receipts are +ve and all outflow is -ve.

gross profit margin and operating profit margin are same?

No, operating profits is income minus expenses. Gross profits include other expenses.

Amazing,need elaboration

Regards

Hi Karthick,

I agree what if a company capitalising the interest cost, how to find that in cashflow can you please help with that detailed information

Ram, for this you will have to go through the balance sheet, see the quantum of borrowing, maybe see the associated notes for additional details, and then check the P&L for finance charges. That should give you a perspective on interest rate capitalization.

Thank you Sir for your Great Information.

Reserves in Balance sheet, is it Cash and Cash equivalents or it is just an addition of PAT from PnL statement

Because some companies manipulating PAT with out real Cash

Can we consider Reserves as real Cash and Cash equivalents

Not really, these two are different. Do check the notes on how these two statements are related.

Thank you for your information.

Some companies Cash Flow Statement shows Profit from operations=100cr and Cash from OA is 10cr

Remaining 90cr they are showing as Receivables

How we can know whether this Receivables are received in future or not

Do they reflect in next year balance sheet

You need yo keep track of it in company;s statements. Make sure receivables dont slide into provisions 🙂

Yes sir. I did check again in the corresponding line item in balance sheet in the notes section.(Consolidated Cash flow statements didn\’t have any notes section) It clearly says \’Bank Deposits with original maturity of more than 12 months\’ in the other financial assets section. The huge number also coincides approximately.

I should also mention that the company had news regarding IT raid after Q4. That quarter\’s concall was not conducted. (The company used to conduct concalls regularly). The latest concall also doesn\’t say anything clearly about the raid except that it was a routine procedure. Something isn\’t adding up or I\’m looking this in the wrong way. But your explanation seems so good.

(Watched your full latest interview with your team. Was good. Please do more of those)

Thanks Sathish.

So these are all red flags that you need to watch out for. If something is not adding up even after through inspection and study, then the other option is to talk the company\’s investor desk.

Also, one good idea is to see the peer company\’s AR to check if such issue are there. If yes, maybe its an industry related?

1. I was analysing the cash flow statement of this company called Sharda Motors. The CFO was negative despite good profits. CFO was mainly negative due to a huge change in this line item called \’Decrease/(increase) in other financial asset\’. When I dug the AR further, I realised that it was due to huge FD investments.

What I don\’t understand is that shouldn\’t these type of investments be reported under cash flow from investing? Why is it reported under cash flow from operations?

2. If you observe the paper sector, it has already given a big run. Margins and Realisation per Metric Ton are all at its peak. But the valuation for certain stocks seems to be super cheap. I would like to know how would you look at this. Being a cyclical commodity sector, will you be cautious, since the important metrics are at its peak, or wouldn\’t worry much since valuations are reasonable. Because I\’m thinking, if even a small U turn happens in the business, our cash flow assumptions can itself go wrong and mess with our valuations right? I would like to know your view on this in relation to any cyclical sector(Not just paper).

Thank You.

1) I\’m not sure why its in OA, but sometimes it can so happen that the company is forced to deposit bank guarantees or book FDs in the name of its customers to show financial stability. For example, assume there is a small cable manufacturing company supplying to Hyundai. Now, Hyundai may insist that this company does a bank guarantee, just so that they don\’t dissapper overnight. So maybe this is the reason, please double check.

2) Most paper companies or packaging companies dont have a pricing power, hence their valuations are always on the lower side.

Sir does we have to see the cash flow statement of minimum 5 years to decide whether to invest or not.cause seeing one cash flow statement makes it hard to decide as in the example mentioned for two years their having negative cash flow but thanks to previous year they have positive flow

Ideally, it is good to evaluate the cash flow for a minimum of 3-5 years, it gives you a sense of any hidden business cycles and its impact on financials.

Karthik, what a thorough job! you\’ve been replying for last many many years. Awesome!!

I have a very rudimentary question here, in 8.3) from where the top line – \”Profit before tax from continuing Operations\” taken.

Is it bottom line from P&L statement (of course before taxes)?

If yes, in P&L Statements this value \”after\” Depr and Amort are netted out? If yes, It makes sense to add that back, as there is never \”real\” cash loss due to depreciation for correct reflection of actual cash from Operations.

Second question is : As I am referring to screener for doing analysis, and since they are taking top line as Profit from Operations(while calculating Cash flow from Operations). This top line seems to be Before depreciation adjustment, therefore there\’s no netting of dep and amort underneath.

is my understanding correct, or I am the one adding more to the rayeta in the conversation 🙂

Best Regards

Thanks, Rajneesh.

1) Yes, the opening line on CF is from the bottom line of P&L. We also add back D&A in cashflow to account for it.

2) So in cashflow operating activities, you have to add back D&A. Do check this – https://zerodha.com/varsity/chapter/cash-flow-statement-2/

Whenever I analyze financial statements, I have this question. Why is there a discrepancy between capex(PPP + CWIP) in cash flow statements and the capex change(PPP + CWIP) between current and previous year in the balance sheet? It doesn\’t even tally even if I take current year\’s depreciation into account. Shouldn\’t it be the same? Or Am I missing something here? Thanks Sir.

This is common, Sathish. This happens whenever there is a balance sheet issue and the numbers get restated.

Hello sir, please show how all three statements are interlinked. You have shown first two statements interlinking but cash flow statement is not shown when interlinked with profit and loss and balance sheet.

Hi Karthik, I am a little confused about the above example of the Gym business the 3rd point \”Buy new fitness equipment to replace worn-out equipment\”. Will this not be an example of Investing Activity, as the Gym is buying equipment which is an investment into the business?

At the stage where I\’ve mentioned this, I\’ve classified this as a business activity, which is generic. But yes, you can classify this as a capex spend and therefore investing activity.

February 23, 2023 at 10:18 am

1)As per Ind AS-7(Preparation of cash flow statement) states that companies can either prepare cash flow statement in:-

Direct Method or Indirect Method.

However we see most of the companies follow Indirect Methord.So,is there any Indian company following Direct method and what are the effects of the same.

2)In the above example isn’t the net increase/decrease in cash computed by adding=operating+investing+financing+effect of exchange rate changes?

3)Can you brief about the Effect of exchange rate changes??

Thanks in Advance.

Paras, can you double-check that? Companies/CFOs prefer the direct method as they can access bills, vouchers, spends, etc.

2) Yes, but we do not consider the effect of Fx at this stage

3) Depends on which context. I suggest you look at the FX hedge positions and the associated notes in the annual report.

Can you guide me with my previous doubt?

Which doubt, Paras?

I think there is a typing error in the Financial activity Cash flow:

Total Cash flow from financial activity is written as 53.1.cr instead of 531 cr.

But the content is very good,

thanks for your education

Thanks for pointing that out, Kuldeep. Let me check this again.

1)As per Ind AS-7(Preparation of cash flow statement) states that companies can either prepare cash flow statement in:-

Direct Method or Indirect Method.

However we see most of the companies follow Indirect Methord.So,is there any Indian company following Direct method and what are the effects of the same.

2)In the above example isn\’t the net increase/decrease in cash computed by adding=operating+investing+financing+effect of exchange rate changes?

3)Can you brief about the Effect of exchange rate changes??

Thanks in Advance.

got your point 👍

Happy learning!

Sir nothing in badway but just asking.

These much deep knowledge(assuming from the concept of varsity is only one in stock market history) and understanding you have of investing.

Why your name is not in list of top 10 investor?

Niraj, by that measure, all teachers at business schools should have been millionaires right 🙂

Sir I only like fundamental analysis(to read and understand companys) is it enough to become successful in stock market or technical analysis is important?

Yes, thats all you need 🙂

Oh ok

Ok thanks sir. Wish there was a feature on Varsity Web version so that users are alerted every time you reply to their comments

We had that initially, Mrinal, but it end up spamming people quite a bit.

Karthik sir, if the closing balance for the previous year got carried forward to the current year, how can we say the Cash Flow statement is prepared on a standalone Basis?

What is carried forward is the cash balance, the net cash flow is the sum of the cash flow from OA + IA + FA, which are all calculated on a stand alone basis.

yes sir, that is cash balance but cash balance also comes from cash sale or from comapany doing business which is already part of profits whatever in shareholders equity->surplus funds.Then i am unable to understand its an current asset.kindly help me?

Cash is a current asset, Srikanth. But I\’m not sure if I fully understand your query.

Hello sir

Actually in balance we were discussing whatever profit company making in terms credit+cash sale is in shareholders funds->surplus and it is a liability. But while we are calculating cash flow statement wahtever cash we have come PBT operating activities and we are considering it an current asset. We have alredy included profits in liability side of shareholders then how same profit we considering current asset in assets side of BS.

That is cash balance which is in asset side right?

Good morning sir,

I have doubt about cash flow statement

1. Sometimes I found operating cash flow positive for eg (100) I.A negative (-150), FA is also negative (instead of positive) how could it possible?

2. Many times I found op cash flow – ve, how could it would be negative it max it should be 0 .

Thanks

Each activity either consumes cash or generates cash. If OA is positive, then it means the business is generating cash. If IA is -ve, it means cash is going for investment. FA positive means, the company is taking on debt.

When businesses burn more money than they generate, then OA will be -ve.

How do we calculate the Direct Tax/Tax Amount in Cash Flow From Operating Activities?

Logically, It should be equal to the (PBT – PAT) of the previous year as the tax incurred in the previous year will be paid in the current year itself. But I see that the numbers vary by some margin although very small.

What can be the reasons for that?

Yup, you can do that. But why do you need to calculate from cashflow itself?

Hi, I had tried to analyze the AR\’s of Maruti Suzuki, so like you had mentioned to always start with cash flow statement before diving into P/L, and Balance sheet of the company. So here is the summarized numbers of Maruti from 2010 till 2020, So from Operations = +64924, from Investing = -49740, and from Financing = -14884 they have secured and spent till date, can you please validate the numbers so I can rely upon my data in future? I would also like to know what could be the reason for a negative financing, what that could mean for an analyst?

I hope you will find time from your busy schedule to answer them.

Thank you.

Adarsh, financing can be -ve if there is repayment of funds, which is either repayment of debt or it could be payment of dividends. You need to dig deeper into their balance sheet to see these numbers.

Thank you Sir, for enlightening us with your superb explanation of CFS preparation. I am so ever grateful to you for your kind efforts in this regard

Glad you liked the content. Happy learning 🙂

Sir, how to calculate free cash flow?

Have explained that in the subsequent chapters.

Good morning sir,

I have doubt about cash flow statement

1. Sometimes I found operating cash flow positive for eg (100) I.A negative (-150), FA is also negative (instead of positive) how could it possible?

2. Many times I found op cash flow – ve, how could it would be negative it max it should be 0 .

Thanks

Hi Karthik,

In some cash flow statement,under the net cash from operations \”Interest Reversal\” is mentioned as extraordinary items.Can you please explain what is \”Interest Reversal\” and can that be added to the net cash frm operations

Most likely, this is the interest paid but reversed for whatever reason. Can you check the associated notes once if the company has stated details?

Hi karthik,

While analysing a stock,the \”Purchase of tangible assets\” value is not clearly specified in cashflow statement.Can this value be taken from the balance sheet-\”additions made during this year in tangible assets\”.

Check the capex spend once, Tamizh?

Never Ever invest in a company with negative cash flow from operating activities.. Its my opinion.

Of course, that is an important fact to remember.

Hi sir ,

Net Cash Flow 1,256 -1,895 203 -634 3,826 -3,914 1,905 -2,752 3,835 1,248 7,675 -3,991

This is the bharti airtel net cash flow. Here what does -3991 means ?? negative number means what ? no cash in bank ???

-ve value in cash flow indicates cash outflow from the system.

Sir,

why depreciation is a non cash expense and why it has to be added back to get the true value of OA.

Because depreciation is just an accounting entry and not really an expense.

Hi Karthik,

At last we calculated closing cash and cash equivalent. Is this the same as Free Cash Flow investors usually talk about? Also, what is the difference between net cash flow and free cash flow?

Thanks.

Pratik, I\’d suggest you keep track of the new module where we would be discussing cash flow in detail.

For AmritVikram\’s question about the two columns, why is the corresponding amount mentioned in the first column but for IA and FA, in the second column? Actually, it\’s just the separation of columns to represent the calculation clearly. For ex, You can see under OA there are many factors that need to be added and subtracted and eventually, you got the total profit before working capital changes whereas there is no such calculation was needed for IA and FA. There was direct entry of Purchase of fixed assets or Dividend Paid.

You can consider it like the first column is to adjust the subheads of the concerning factor and second column is to show the final amount of the corresponding factor.

Phew! Thanks for clarifying that Sonali 🙂

Hello Sir,

Yes I totally understand.

But the company could just park that excess cash into yearly/half yearly government bonds. Those are pretty much risk free extra income. No need to manage money in that aspect correct?

If they foresee that they do not need the money for a 1 year they could park that excess cash there and get a decent and safe return. After which reutilize that money correct?

Just releasing excess cash as dividends does not really help growth correct?

Ah yes, for the short term they certainly can. In fact, the treasury department of a company will do this.

Hello Sir,

Yes I totally understand.

Hello Sir,

Sorry for the late response.

If the company has already used what ever it could for growth. Why not use the remaining cash and park it into safer investments like MF or government bonds or something like that. Those can add some additional income to the company which in turn helps its growth.

But is that what the company is supposed to do? Manage investments in financial instruments? No right? A company is supposed to focus on growth and improve shareholder\’s wealth.

Hello Sir,

When a company has a large operational cash flow.

What should it do with that excess cash? Invest it in creating an asset/ invest it in stocks/mfs/bonds or put it in an FD?

Do companies generally put money in MFs/Bonds to safe keep?

They could also give dividends if required, but isn\’t it better to invest it back into the company?

Based on the growth stage the company is in, it ca either decide to reinvest in itself for growth or give out dividends. The company should not indulge in investments for no reason.

Hello Sir,

Thank you for your response.

When a company increases it operational cash flow and also increasing is investing cash flow thus reducing its overall cash flow. Is this a good sign or bad?

I see the company is investing in creating several assets etc, but the overall cash of the company is reducing.

Yes, as long as the nature of investment is justified by the growth in operations.

Hello Sir,

You have mentioned that companies that have a positive cash flow from operating activities is a good sign.

In the Gym example, all the operational cash flow activities were causing cash flow to decrease.

So how does a company have positive cash flow from operating activity?

When sales increases, operating cash flow too increases.

1.Sir i wanted to know why dividends and interest received are shown in operating activities instead of financing activities?

2.Why the value received in dividends and interest received are negative when its the cash inflow for the business?

Yash, both these things I\’ll explain in the current module i.e. Financial modelling.

Hello Sir,

When we look at a cash flow statement, we would like the cash generated from OA to be positive, IA to be negative and FA to be minimum or negative correct? CAN FA be positive?

We would like the company to gain from OA and use that cash from OA to spend on IA?

Yup, FA can be +ve. I\’ll discuss this more in the new module i.e. Financial Modelling.

Why is in interest received from bank deposits listed in both operating as well as investing activities?

YOu need to check the notes associated with this. But it should be investing activities.

Hi Karthik,

Thanks for explaining things very clearly.

Cash Flow from Rupees Crores (2013-14) Rupees Crores (2012-13)

—————————————————————————

Operating Activities 278.7 335.4

Investing Activities (344.8) (120.05)

Financing Activities (53.1) (34.96)

———————————————————————-

Total (119.19) 179.986

Can you please explain why operating activities is mentioned as positive and rest two negative?

Each activity either generated cash or consumes cash. If it generates cash then it it will be positive. Here cash is generated by operations.

If company’s total cash position is Rs.292.86 Crs. then why don\’t they pay-off the short term borrowings of Rs. 83.83 Crs. (from Balance sheet)

what could be the rational behind continuing with debt, as it is eating up the Profit Margin!

Can your kindly share your thoughts!

Well, maybe it could be an easy/low rate loan that the company enjoys.

Is not Long term borrowing presented in Cash Flow statement from financial Activities ?

If yes then Where to look for it?

Short term borrowings has been presented in financial activities.

Thanking you in advance.

Balance Sheet?

Why is depreciation added to operating cash flow. Doesnt depreciation mean the depreciation of the value of the asset over a period of time? Should it not be an expense which reduces the cash balance?

Depreciation is an accounting entry, not a real expense. Hence it\’s added back.

Hi Karthik,

Thanks for this material which is really helpful for beginners.

Why is cash-inflow activities are mentioned as (less) in cash floe statement? cash-outflow activities are shown as +ve, Add.

For example, Dividend received/Ineterest Received/Increase in trade recievables is shown as -ve, where as or Interest paid is shown as +ve

This is after taking the impact (effect) of decreasing or increasing cash. For example, taking debt is considered positive since cash comes into the company.

No sr it was standalone,but there is difference in consolidated too…and it is same manner

Ah ok, but I\’m guessing there won\’t be much difference in the consolidated statements. Btw, stick to the annual report as the source for all your data.

Sr I have one doubt, as I was going through Asian paints annual report of 2018 – 2019 ,I found Cash and cash equivalents in balance sheet is 98.33 Cr, but as I gone through cash flow statement there I got cash and Cash equivalent as 1156.36 cr. Now this additional 1062.38 and 4.35 cr they took from investment in liquid mutual funds and Bank overdraft respectively(but it should come under investment), then why don\’t they mentioned this whole amount in cash and cash equivalents in balance sheet,

Are you checking the consolidated numbers?

Sir, I have found another point of interest i.e. if we look at Operating Activities Point No. O (Dividend received) & P (interest received on bank and other deposit) of amount (144.19) & (137.94) these two points are also mentioned in Investment Activities Point no. H and G with same amount but with positive balance. This will make total effect on cash flow \”Zero\” but the question is why? What is the purpose to showing first in OA and thereafter in IA? If it didn\’t mentioned in OA it will not be balanced.

Hope I\’m not shooting confusions. Thanks.

Regards,

Mayur Pansheriya

Ah Mayur, I need to take another look at this to get the exact context, its been a while 🙂

But I\’m still not sure why this shows up in OA.

Sir, Ta for your early response. Ok let me check with other resources and will get back to you.

Sure, please do.

Dear Sir,

I have observed that \”interest received on bank and other deposit\” amount i.e. (137.94) is deducted from cash flow statement while it\’s increase cash flow.? and there are other such a activities which are increasing the cash flow but it\’s deducted from statement. Why?

Regards,

Mayur

Mayur, you need to reference the cash flow with respect to the overall effect it has on the cash flow. Some items tend to increase the cash flow, which some reduce. That said, receipt of cash via deposits should increase the cash flow, not sure why its deducted. Please do check the notes for explanation.

Hi Sir, need ur help.

In Cash Flow from Investing Activities, why is Purchase of Tangible/Intangible fixed assets a negative figure. As far as Im aware, if something is purchased, cash goes out and hence in cash flow st. outgoing cash is shown as a positive figure. So why is Purchase of Tangible/Intangible fixed assets a negative figure.

Cash is going out of the books, hence its considered -ve cash flow.

valuable lessons

Sorry, I asked a wrong question.

In the profit and loss statement we deduct depreciation and amortization from the revenue to calculate the profit before tax, then why do we deduct depreciation and amortization again from the profit before tax in cash flow statement ?

We dont, in fact, we add it back. Check under operating cash flow.

I am finding it difficult to differentiate between IA and FA. Could you please elaborate how to distinguish better between the two.

For instance, if Investing activities are \”activities pertaining to investments that the company makes with an intention of reaping benefits at a later stage\”, doesn\’t \”seek a short term loan from bankers\” also qualify as IA in that sense? Similarly if FA are \”activities pertaining to *all* financial transactions of the company\”, aren\’t \’all money related\’ matters FAs i.e. IA appears to me to be a subset of FA? Given that, how do you distinguish clearly between IA and FA? Thanks.

Short terms loans — > this is usually to fulfil short term CAPEX requirements and is not considered as an investment. Not all financial activities are similar, for instance recongnising revenues, this is an operating activity rather than a Financial activity. Hope that makes sense?

I assume \”Buy new fitness equipments to replace worn out equipment\” is Investing activities rather than Operating activities, as those Property, Plant and Equipment.

Reply to Amitvikram regarding Columns: Since P/L is a club of all types of expenses which all IA, FA and OA activities. Since OA activities tend to adjustments for excluding IA and FA activities, we present OA activities in first (before adjustment) and the result (after adjustments) later column. Hence, there we undertake in a later column for FA and IA activities because it was prone to adjustments.

+ve cash flow from Operating activities is considered good???????????

As a thumb rule

Yes, of course. That indicates that the business is generating cash from operations.

Plz, Tell me how to calculate free cash flow is free and net cash flow same?

Have explained the same in the chapter right?

In operating activities, why is profit mentioned in the beginning, and adjustments added/subtracted from it?

Because the Net profit is the starting point in a cash flow analysis.

Hi!

I have noticed while analysing the Balance sheet & Cash flow of companies that the value of \”addition of fixed assets\” in a particular year (without the CWIP) does not match with the value of \”purchase of fixed assets\” under cash flow from investing activities.

For eg. for ITC in the year 2003-04, the additions in fixed asset were 597.23 Cr. However the purchase of fixed assets in cashflow is shown to be 515.44 Cr.

Why is this happening?

Sorry, I am unable to post snapshots of the figures for clarity.

This could be adjusted against the sale of any old fixed assets as well.

Hi Karthik, I understood balance sheet, P&L, cash flow individually. but i\’m unable to view all the 3 financial statements combined. can you provide any video or source to learn more about how to view all 3 financial statements combinedly?

Dont have a video, but I\’ll try to put this in a nutshell for you –

1) P&L is year to year basis, it does not work on a cumulative basis.

2) BS is incremented/decreased on a year on year basis. Its cumulative.

3) The final number from the P&L i.e. the Net earnings flows into the reserves of the company, which is in BS.

4) The yearly depreciation in P&L is added to BS.

5) Point 3 & 4 establishes two connections between P&L and BS

6) The Net income from P&L is the starting point of the cash flow statement

7) Other things like depreciation is also considered from P&L to cash flow

8) Point 6 and 7 connects CF and PL

9) The capex number from BS also flows in to CF

10) The final net cash number from CF flows into the Cash component of the BS (current assets)

11) Point 9 and 10 establishes the connection between BS and CF

Hope that helps 🙂

Yes i did go through the notes….

Could not find anything there, hence i posted the question here.

Sure, need to check this.

The closing balance of FY 19 gets added to the opening balance of FY 20. I get this.

But what i am saying is that the opening balance for fy19 is shown as 2 different numbers in 2 different annual reports.

I have send you the screenshot of what i am trying to tell you in your email sir. Please check it out when you have the time. Thank you!

Ok. But dd you try comparing the associated notes of both these years? Associated notes of the opening balance I mean.

Hi Karthik,

I was going through bank cash flow statements .It seems that most of the bank has Operating activity cash flow as a negative.

I think it may be because of the cash they have to give to customers as a loan. So we can\’t say that bank is not performing well looking at -ve cashflow.

In this case how we can judge whether bank is worth investing or not looking at operating cash flow?

Do you have any article or link where i can study the bank cash flow to have better idea to take decisions on investment?

Thanks

Thats right, the regular financial statement analysis does not work for banks. I dont have any article on banks because I dont think I\’m the right guy to discuss banks. But have been wanting to get better and discuss this here, hopefully soon.

1)In the fy19 annual report opening cash balance was 4255 Cr. (for the year 2018-19)

2) In the fy20 annual report opening cash balance was 7336 Cr. (for the year 2018-19)

3) There is a difference of 3081 Cr. Thats a huge differnce!

Ah, that is because the closing balance of FY 19 gets added to the opening balance of FY 20, this is called the base rule in accounting.

Hello Karthik sir!

I was going through Cash flow CONSOLIDATED statements of RIL( reliance industries limited) and found the opening balances of cash for the Fy2019 to be different in the annual reports of Fy2020 and Fy2019. How can this be possible? cannot send you a screenshot here. can you please check?

Thats ok as long as the difference is not much. Companies usually restate to represent the accurate number.

Sir, In case of reliance Jio if investments are made from different companies, it means that existing share holders are selling it to new comers. Hence the amount directly goes to Exiting share holders. In that case how company\’s debt is reduced. Please clarify.

If mukesh ambani himself sells the stake and pocket the money, how debt is reduced since money directly goes to him. Please clarify.

Also if Mukesh Ambani sells stake and use inflow money to reduce debt is not it a loss for him as he is using his money to pay off the loan. Please through some light on this. Thanks in advance.

This will be the company\’s share capital dilution, with some promoter stake dilution I guess.

but it seems that the effect has taken place in IA of the cash flow statement. so why do they need to make a negative entry in the OA?

Thats because the bank interest is a source of investment I suppose.

Hi Karthik

I have checked it but it does not seem to have any entry/effect in FA with reference to Interest received on Bank and other deposits. All they have posted is just cash outflows in FA.

hi Karthik

why Interest received on Bank and other deposits in OA is in a bracket(negative)? if we have received an interest then it should have a positive effect on the cash entry.

Thats right. Guess its treated +ve in FA. Can you please check?

Hi Karthik,

I was reading financial reports of few companies for doing fundamental analysis. The number provided in current year\’s report does not match the number provided in previous year\’s report.

For example in annual report of ITC, FY16-17 & FY15-16 the numbers of FY16-consolidated Cash flow does not match. Could you please tell me what are the reasons?

If in case, one of the reason might be the change in company\’s accounting policy, how to know which numbers to be taken for ratio analysis?

Not just ITC, I found out the difference like these in a lot of other companies as well.

P.s: Thank you for the hard work in putting together a great knowledge material

This could be because of restating the numbers. The difference would not be much I suppose. I generally prefer to take the numbers for FY15-16, from FY16-17 report. FY16-17 in FY17-18 report, so on.

No offence sir but FA seems a little bit boring so can I skip this module because as of now I am not very interested in long term investments and want to start with trading ASAP. Later I would surely complete this module as well. Also sir I have some doubts regarding studying charts so do you have any videos where chart reading is explained.

That is entirely up to you, Surya 🙂 If trading is what you are looking for then TA and derivatives will help.

Hi there sir I have completed TA, Futures trading and introduction to stock market module. What should be my next step to start with trading? I am now completing this FA module so after completion of all the other modules should I start with trading (talking about paper trading first then the actual one) or I can start now also.

Yes, you can start paper trading now itself and do FA in parallel.

Sir recently I watch your video upon cashflow statement on YouTube. Sir it was beautiful explained. Sir, my small request to you to make videos upon all the fundamental topic available in zerodha varsity.

Thanks, Yogesh. I will try and do these, its just that the bandwidth to do this is very limited.

Sorry, my mistake it\’s in IA. In OA and IA both. Why is this?

If you see, dividends for example, they are netting out. But I still need to figure out why OA, will do some research around it 🙂

I am confused, why there is \”Interest received on Bank and other deposits\” has been showed in both Operating and Financing activities. Why it is negative in Operating and Positive in Financing?

Interest received is cash flowing in, i can understand its Financing activity effect. Can\’t understand Operating activity effect.

Interest received on Bank and other deposits – this is only in OA not in FA. Can you please recheck? I\’m guessing these are short term deposits associated with current items/working capital requirements, closely tied to the operations, hence in OA.

Hi Karthik,

I have understood that why we adding depreciation in cash flow from operations but why are we adding provision for gratuity, provision for wealth tax etc. Could you please advise?

Thanks!!

These are just provisions right? Cash is not moving out or in, hence.

Hello Karthik,

In the above section you have mentioned the following statement:

\”If cash is current and cash is an asset, shouldn’t it reflect under the current asset on the Balance sheet?

Exactly and here it is. Look at the balance sheet extract below.\”

But why are the values mentioned in the cash flow statement and the Balance sheet not matching ??

Cash Flow statement value: 2928.63

Balance Sheet Value: 2945

Can you please help me know what this difference is ?

Which number are you trying to match between cash flow and balance sheet? The one that should match is the cash and cash balance.

Why the cash balance in the balance sheet Rs 294 crores is different to the ending cash and cash equivalent amount in the cash flow statement Rs 292 crores ??

Ideally, it should match the exact Rupee. I need to check this as well.

Under activities of a company, how is buying a new fitness equipment considered to be an operating activity instead of an investing activity as fitness equipment is an asset to the fitness centre?

I guess the assumption was that the fitness equipment has a high mortality rate, so needs to be replaced often.

sir,

do i need to learn \’accounting\’ for doing fundamental analysis.

waiting for your reply sir.

Not really but a background in accounting helps. Btw, I myself don\’t have an accounting background.

Sir,

1. How can we find that the amount of profit shown in a company\’s P&L account is true.

For instance, I was compairing a last 5 years net profit of a company with its last 5 year cash flow from operation, There is huge difference in the result amount. The cash flow is 3 times more than its net profit. Could it be possible. Can you suggest a process to link the P&L acc. with Cash Flow.

Thanks

It will be hard. This is the reason why we place so much faith in the auditor\’s report.

When referred to \’buildings\’ in the tangible assets does it imply that the building are rented or owned? how do we find out if the company is paying rent for the space or owning it?

It is assumed owned, rented properties is not an asset 🙂

You can find out the rent paid details in the other expense section of the P&L.

Which factor shows the cash received by the company and the cash yet to be received?

Revenue and receivables respectively.

It is an Outflow,It is mention in the cash flow from operating activities(sequence d ) above in varsity module.

Need to check this again.

Hello Sir,

What does it indicate \” Net Income on sale of tangible fixed assets is (2.26)\”

means How can business has cash outflow on sale of tangible fixed assets ?

Thanks in advance Sir

It says net income which is an inflow right?

[…] In case you are new to the concept of cash flow statement and cash flow from operations then zerodha…. […]

Once again heartily thanks for sharing your knowledge sir.sir I have a doubt if only \”cash and cash equivalents\” worth money is present in company\’s bank accounts what is the point In calculating \”debt to equity ratio\” isn\’t that we should be calculating \”debt to cash and cash equivalents ratio\” as equity of a company is already used for various purposes except for general reserve if I am not wrong.kindly clarify sir.

Equity also includes the shareholder\’s equity, which has both reserves and share capital. You need to consider this as well.

Hey sir, I wanted to ask that if closing balance of cash equivalent is decreasing in a year. What conclusions can be made?

Not a great sign. However, I\’d suggest you inspect each of the cashflow sub statements i.e CF from IA, OA, and FA.

Great boss. Thank you so much for very insightful chapter. I have changed my approach to looking at a company fundamentals. Now first I look Cash flows and then BS & then PL.

Yes, all there are super important 😉

I can understand following statement , correct me if i am wrong.

1) If Net Cash flow is -ve means company has spend more money out of reserves or current years profit. in such case Bank account can be zero also or a positive. Cash spending can be from any of the source like

1) Reserves

2) bank account

3) Cash flow from asset sales etc

If net cash flow is -ve for the year, then it means that on an overall basis (across all 3 activities), the company has consumed more money than it generates. The cash guzzler can be either the investing activity or the financing activity…or the operations itself could bleed money.

As you said total net cashflow indicates a cash lying in current accounts of the company. What if the same figure is -ve.

This means the company is losing more money than its generating. Not a good sign for the company.

Hello the modules are really great & helpful but can you please more elaborate the cash flow & each item under the three activities ? I am still not clear. Please possible publish module more on the three activities & the components under each.Thank You !

Sure Ronak, I will try and do that. Meanwhile, check this – https://www.youtube.com/watch?v=JRNEH8eJ6jg

Hi,

Are your examples all from standalone statements of the company as opposed to consolidated? Because I was looking at Hinduja Global statements on screener.in website and in the consolidated statements things are not adding up.

For example. Net cash flow in Mar 2016 was -109 (negative 109). However, in the balance statement the cash equivalent has gone up by 20Cr (from 354.27 to 374.81).

Also, in cash flow statement Fixed asset purchase shows as 253.75 in 2016. However, gross block in balance statement has gone down (from 1333.21 to 1064.53).

How do we explain these differences?

I\’ve considered consolidated statements. In fact, you always should. The case with Hinduja, I\’m not sure, you really have to deep dive into the statements and check. For example, check the depreciation and amortization schedule for fixed assets, you may get some cues there.

Hi Karthik,

In ARBL\’s cash flow statement dividend received in operating activities is termed as negative while dividend received in investing activities is termed as positive?

Ram, are you sure? How can company operations receive the dividend?

Yup. Look it up in the the chapter

Point O from operating activities which is dividend received is negative while Point H from investing activities which is dividend received is positive.

Sorry, just to reconfirm are you talking about ARBL?

Thank you Karthik for providing very useful insights about fundamental analysis into very simple language.

Happy reading, Dubey!

Hello Sir,

I have few doubts, kindly clarify…..

The snapshot (Cash Flow from Operating Activities) attached at Para 8.3, showing Depreciation and Amortisation entries. Why these entries are being indicated in Cash Flow Statement ?? (The Cash Flow Statement should indicate the actual amount paid to acquire an Asset.). Also, why these entries are showing positive in the Cash Flow Statement. In fact, i am not able to understate the sign (Positive/Negative) of none of the entries showing in the snapshot (Cash Flow from Operating Activities) attached at Para 8.3.

Regards,

To arrive at the cashflow from operations, we need to add back the cash deducted for D&A. Remember, D&A are just accounting entries.

Yes Sir, i remembered but D&A entries were only to reflect the true earning capability of the company in P&L Statement. Let\’s say one Company spend Rs. 1 Crore towards buying an Assets (Assets useful life = 5 years). So in P&L Statement the Company would show Rs. 20 Lacs in D&A entry. As the Company actually spent Rs. 1 Crore, this should reflect in Cash Statement of the Balance Sheet. (Otherwise, how one would know the actual amount spent??).

Also, the there are two D&A entries in Cash Statement (One in \”Cash Flow from Operating Activities\” and other one in \”Cash Flow from Investing Activities\”) and these both are eventually cancel out each other.

Sorry, I am new to this subject. Not able to catch up with you……

Yes, this will show up in the investing activity of the cash flow, right?

Hello karthik

I am ravi and have account with zerodha

I need your feedback for below point.

Why previous year account payable and receivables are compared with current year in cash flow statement?

In cashflow statement? I\’m not sure where this has happened, can you give an example? Thanks.

Ok .I will give example

Trade payable @2017 =100 crore

Trade payable @2018=250 crore

The difference is 150 crore(cash Inflow). Hence we have to add 150 crore to operating activity (to net income) as per indirect methode.

Here my question is that why we have to add the difference 150 crore instead of 250 crore?because 250 crore is the current trade payable.i am really confusing.

That is because we are trying to evaluate the difference in operating activities and not really the actual number. Remember, towards the end we take the net increase/decrease, add it to the current year\’s opening balance (which is the closing balance of the previous year), and that should give us the same number.

Hey Karthik,

How does finance costs have + sign in operating activities?

Very thanks for prompt reply

Happy learning, Rajkumar.

Hi karthick

I have seen your webinar about case flow statement .you had taken 10 years cash flow for explanation

Now I have two questions

1.where can I get 10 years cash flow statement of company? because company or other sites have only 5 years record of financial reports.

2.during calculation should we take net cash flow from operations activities?

1) I took it from Screener.in

2) Yes, net CF from all activities, including Operational activities

Dear Karthik,

Many persons have asked this question but still remain unanswered or confusing.

The money coming in company is +ve and going out is -ve. With this,

OA -ve

IA -ve

FA +ve

Hence net cash flow shall be (OA+IA)-FA. But u have used OA -(IA+FA) to arrive at 119 cr. Why IA has been treated as +ve?

Yes, money coming in is +ve and going out is considered -ve. But remember, each of these activities can either generate cash or consume cash. So you will have to treat it accordingly.

Than you so much for such a detailed article.

How to calculate cash flow per share, is it cash from operating activities divided by the number of outstanding shares or do we need to subtract remove something from the \’cash from operating activities\’?

Thank you.

For this, you will have to divide the net cash flow i.e CFO+CFF+CFI by the total outstanding number of shares.

sir, could you tell me please that if the net cashflow of a company goes to cash and cash eq. and to bank acoonts then what goes to reserve and surplus?

Thats also in the form of cash, Sunil.

Hi sir

Positive operating CF and negative investivg CF in reliance industry last 5 year

. How possible for a company to all its earning invested in business even though they reserve n surplus increase year on year ?

This is possible, Amit. RIL is CAPEX intensive, especially with Jio coming in the picture.

Ya

but then how\’s it\’s possible R&S continuosly increase?

Are you looking at standalone or consolidated numbers?

Consolidated

But in both same situation

Well, Amit, the answers will be found in the notes associated with the line items. You will have to dig it up 🙂

Hi Sir. The content is great and is extrememly helpful for people like with almost no financial background. I have 1 doubt. The AR tell details till about the end of march of that year. What if we have to analyze the stock in month of december when the next AR will take another 3 months. How can we take into picture the effect of things happened between march and dec.

Glad you liked the content, Rachit.

If you are looking at a stock in Dec, I\’d suggest you look at the historical numbers till March and then look at Q1 and Q2 data.

I have doubt in OA

Why Net income on sale of tangible assets (2.26) is negative?

Because when company sells its tangible assets it receives money from outside and thus it has to be cash inflow right?

Maybe its showing the net increase or decrease with respect to the previous year?

SIR PLZ EXPLAIN TO THIS TOTAL CASH FLOW HAS TO BE 675

Asmad, I\’d suggest you look at the annual report for this.

SIR……

U SAY THAT

Cash Flow of the company = Net cash flow from operating activities + Net Cash flow from investing activities + Net cash flow from financing activities

Cash Flow from Rupees Crores (2013-14) Rupees Crores (2012-13)

Operating Activities 278.7 335.4

Investing Activities (344.8) (120.05)

Financing Activities (53.1) (34.96)

Total (119.19)

Sir is free cash flow is equal to the total of (operating cash flow + financing+investing cash flow ) or there is some difference and if any Please clarify sir.

An easier way is to deduct the CAPEX from Cash Flow from Operations. This will help give you the free cash flow.

How to read financial sector cash flow statement.?

Check this, Selvaraj – https://www.youtube.com/watch?v=JRNEH8eJ6jg&list=PLkxTRam6E2V_Kq5l-H4Xihh-nWgO6Z4d9&index=27

First of all thank you very much for sharing valuable information

I have one query

What\’s is the exact meaning of negative cash flow from operations ? Is it bad or not ?

Cashflow statement as such represents the money coming in and going out of the companies account. Think of it as your personal bank statement. From your bank statement, if you add up all the debits and credits you will get the balance. If the balance is positive, then you have money, if the balance is -ve, that means you owe money. Likewise for the company.

These +/- signs for cash inflow/outflow are creating confusions.

Isn\’t there a uniform accounting standard (AS) from where we can see how to put +/- sign against inflow/outflow of cash?

Or why don\’t companies use note/schedule nos. like balance sheet to explain these and avoid confusion?

This is actually quite simple – all the money coming into the company\’s account is considered positive cashflow (+ve) and all going out is negative cash flow (-ve).

Thanx sir.

Came across your site a few days ago. Very impressed with the way you teach. For older people like me with little financial knowledge – I find it so well explained. Thank you

Thank you so much for the kind words 🙂 Happy learning!

\”Look at the section highlighted in green (for the year 2013-14). It says the opening balance for the year is Rs.409.46Crs. How did they get this? Well, this happens to be the closing balance for the previous year (refer to the arrow marks). Add to this the current year’s cash equivalents which is (Rs.119.19) Crs along with a minor forex exchange difference of Rs.2.58 Crs we get the total cash position of the company which is Rs.292.86 Crs. This means, while the company guzzled cash on a yearly basis, they still have adequate cash, thanks to the carry forward from the previous year.\” Why this Rs.119.19 is substracted to previous year cash flow ..it should be added to the previous year cash flow…..

The company generated a negative cash of Rs119.19 Crores for the current year, but the previous year was cash positive, hence this has to be deducted from the previous year\’s balance.

This question has been asked a lot many times but i still dont get it.

When in OA it is clearly mentioned dividend RECEIVED which means cash is received(inflow) then why write it as -ve and consider it as outflow? Had it been written as dividend paid then it would mean outflow of cash. And if it really is outflow then why add it in IA ?

Thank You.

Ah, I get it. You are referring to the first section of OA, which is used calculate the PAT from operations. The dividend received is not really from operations, this is from other investments made, hence needs to be deducted. After all these adjustments, the final PAT is arrived at, which flows into calculating the CF from OA.

Hi,

I have doubt on Cash flow from operating activities.

I thought Depreciation amount to be shown as -value and dividend received to be shown as + value.

Could you please explain me on this to understand better.

Thanks,

Manjunath