2.1– Speculator Vs Trader Vs Investor

Depending on how you would like to participate in the market, you can choose to speculate, trade or invest. All three types of participation are different from one another. One has to take a stance on the type of market participant he would like to be. Having clarity on this can have a huge impact on his Profit & Loss account.

To help you get this clarity, let us consider a market scenario and identify how each market participant (speculator, trader, and investor) would react to it.

SCENARIO

RBI in the next two days is expected to convene to announce their latest stance on the monetary policy. Owing to the high and sticky inflation, RBI has hiked the interest rates during the previous 4 monetary policy reviews. As we know, an increase in interest rates means tougher growth prospects for Corporate India – hence corporate earnings would take a hit.

Assume there are three market participants – Sunil, Tarun, and Girish. Each of them views the above scenario differently and hence would take different actions in the market. Let us go through their thought process.

(Please note: I will briefly speak about option contracts here, this is only for illustration purpose. We will understand more about derivatives in the subsequent modules)

Sunil: He thinks through the situation, and his thought process is as follows:

- He feels the interest rate are at an unsustainably high level.

- High-interest rates hamper the growth of corporate India.

- He also believes that RBI has hiked the interest rates to a record high level and it would be really tough for RBI to hike the rate again.

- He looks at what the popular analysts on TV are opinionating about the situation, and he is happy to note that his thoughts and the analyst thoughts are similar.

- He concludes that RBI is likely to cut the rates if not for keeping the interest rates flat.

- As an outcome, he expects the market to go up.

To put his thoughts into action, he buys call options of State Bank of India.

Tarun: He has a slightly different opinion about the situation. His thought process is as below:

- He feels expecting RBI to cut the rates is wishful thinking. In fact, he thinks that nobody can clearly predict what RBI is likely to do

- He also identifies that the volatility in the markets is high. Hence he believes that option contracts are trading at very high premiums.

- He knows from his previous experience (via backtesting) that the volatility is likely to drop drastically just after RBI makes its announcement.

To put his thoughts into action, he sells 5 lots of Nifty Call options and expects to square off the position just around the announcement time.

Girish: He has a portfolio of 12 stocks which he has been holding for over 2 years. Though he is a keen observer of the economy, he has no view on what RBI is likely to do. He is also not worried about the policy’s outcome as he anyway plans to hold on to his shares for a long time. Hence with this perspective, he feels the monetary policy is another short-term passing tide in the market and will not have a major impact on his portfolio. Even if it does, he has both the time and patience to hold on to his shares.

However, Girish plans to buy more of his portfolio shares if the market overreacts to the RBI news and his portfolio stocks fall steeply after the announcement is made.

Now, what RBI will eventually decide and who makes money is not our concern. The point is to identify a speculator, a trader, and an investor based on their thought process. All three men seem to have a logic based on which they have taken a market action. Please note, Girish’s decision to do nothing itself is market action.

Sunil seems to be highly certain on what RBI is likely to do, and therefore his market actions are oriented towards a rate cut. In reality, it is quite impossible to call a shot on what RBI (or for that matter any regulator) will do. These are complex matters and not straightforward to analyze. Betting on blind faith, without rational reasoning backing one’s decision is speculation. Sunil seems to have done just that.

Tarun has arrived at what needs to be done based on a plan. If you are familiar with options, he is simply setting up a trade to take advantage of the high options premium. He clearly does not speculate on what RBI is likely to do as it does not matter to him. His view is simple – volatility is high; hence the premiums are attractive for an options seller. He is expecting the volatility to drop just before RBI decision.

Is he speculating on the fact that the volatility will drop? Not really, because he seems to have backtested his strategy for similar scenarios in the past. A trader designs all his trades and not just speculates on an outcome.

Girish, the investor, on the other hand, seems to be the least bit worked up on what RBI is expected to do. He sees this as a short term market noise which may not have any major impact on his portfolio. Even if it did have an impact, he believes that his portfolio will eventually recover from it. Time is the only luxury markets offer, and Girish is keen on leveraging this luxury to the maximum. In fact, he is even prepared to buy more of his portfolio stocks in case the market overreacts. His idea is to hold on to his positions for a long period of time and not get swayed by short term market movements.

All the three of them have different mindsets which lead them to react differently to the same situation. This chapter’s focus is to understand why Girish, the investor has a long-term perspective and not really bothered about short-term movements in the market.

2.2 – The compounding effect

To appreciate why Girish decided to stay invested and not really react to short term market movement, one must understand how money compounds. Compounding in simple terms is the ability of money to grow when year 1 are reinvested for year 2.

For example, consider investing Rs.100, which is expected to grow at 20% year on year (recall this is also called the CAGR). At the end of the first year, the money is expected to grow to Rs.120. At the end of year 1, you have two options:

- Let Rs.20 in profits remain invested along with the original principal of Rs.100 or

- Withdraw the profits of Rs.20.

You decide not to withdraw Rs.20 profit; instead, you decide to reinvest the money for the 2nd year. At the end of the 2nd year, Rs.120 grows to Rs.144. At the end of 3rd year, Rs.144 grows to Rs.173. So on and so forth.

Compare this with withdrawing Rs.20 profits every year. Had you opted to withdraw Rs.20 every year than at the end of 3rd year the profits would have been just Rs. 60.

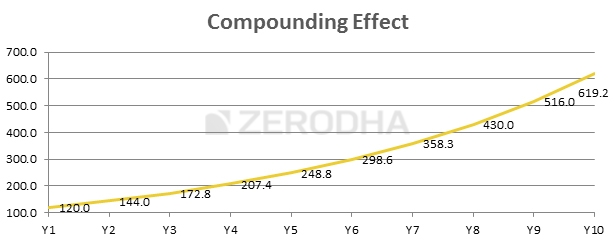

However, since you decided to stay invested, the profits at the end of 3 years are Rs.173. A good Rs.13 or 21.7% over Rs.60 is generated because you opted to do nothing and decided to stay invested. This is called the compounding effect. Let us take this analysis a little further, have a look at the chart below:

The chart above shows how Rs.100 invested at 20% grows over a 10 year period. If you notice, it took almost 6 years for the money to grow from Rs.100 to Rs.300. However, the next Rs.300 was generated in only 4 years, i.e. from the 6th to 10th year.

This is, in fact, the most interesting property of the compounding effect. The longer you stay invested, the harder (and faster) the money works for you. This is exactly why Girish decided to stay invested – to exploit the luxury of time that the market offers.

All investments made based on fundamental analysis require the investors to stay committed for the long term. The investor has to develop this mindset while he chooses to invest.

2.3 – Does invest work?

Think about a sapling – if you give it the right amount of water, manure, and care would it not grow? Of course, it will. Likewise, think about a good business with healthy sales, great margins, innovative products, and ethical management. Is it not obvious that the share price of such companies would appreciate? In some situations, the price appreciation may delay (recall the Eicher Motors chart from the previous chapter), but it will always appreciate it. This has happened over and over again across markets in the world, including India.

An investment in a good company defined by investable grade attributes will always yield results. However, one has to develop an appetite to digest short term market volatility.

2.4 – Investible grade attributes? What does that mean?

Like we discussed briefly in the previous chapter, an investible grade company has a few distinguishable characteristics. These characteristics can be classified under two heads: the ‘Qualitative aspect’ and the ‘Quantitative aspects’. The process of evaluating a fundamentally strong company includes a study of both these aspects. In fact, I give the qualitative aspects a little more importance over the quantitative aspects of my personal investment practice.

The Qualitative aspect mainly involves understanding the non-numeric aspects of the business. This includes many factors, such as:

- Management’s background – Who are they, their background, experience, education, do they have the merit to run the business, any criminal cases against the promoters etc

- Business ethics – is the management involved in scams, bribery, unfair business practices.

- Corporate governance – Appointment of directors, organization structure, transparency etc

- Minority shareholders – How does the management treat minority shareholders, do they consider their interest while taking corporate actions

- Share transactions – Is the management buying/selling shares of the company through clandestine promoter groups.

- Related party transactions – Is the company tendering financial favours to known entities such as promoter’s relatives, friends, vendors etc. at the cost of the shareholder’s funds?

- Salaries paid to promoters – Is the management paying themselves a hefty salary, usually a percentage of profits.

- Operator activity in stocks – Does the stock price display unusual price behaviour, especially when the promoter is transacting in the shares.

- Shareholders – Who are the significant shareholders in the firm, who are the people with above 1% of the outstanding shares of the company

- Political affiliation – Is the company or its promoters too close to a political party? Does the business require constant political support?

- Promoter lifestyle – Are the promoters too flamboyant and loud about their lifestyle? Do they like to display their wealth?

A red flag is raised when any of the factors mentioned above do not fall in the right place. For example, if a company undertakes too many related party transactions, it would send favouritism and malpractice. This is not good in the long run. So even if the company has great profit margins, malpractice is not acceptable. It would only be a matter of time before the market discovers matters about ‘related party transactions’ and punishes the company by bringing the stock price lower. Hence an investor would be better off not investing in companies with great margins if such a company scores low on corporate governance.

Qualitative aspects are not easy to uncover because these are very subtle matters. However, a diligent investor can easily figure this out by paying attention to the annual report, management interviews, news reports etc. As we proceed through this module, we will highlight various qualitative aspects.

The quantitative aspects are matters related to financial numbers. Some of the quantitative aspects are straightforward, while some of them are not. For example, cash held in inventory is straight forward; however, ‘inventory number of days’ is not. This is a metric that needs to be calculated. The stock markets pay a lot of attention to quantitative aspects. Quantitative aspects include many things, to name a few:

- Profitability and its growth

- Margins and its growth

- Earnings and its growth

- Matters related to expenses

- Operating efficiency

- Pricing power

- Matters related to taxes

- Dividends payout

- Cash flow from various activities

- Debt – both short term and long term

- Working capital management

- Asset growth

- Investments

- Financial Ratios

The list is virtually endless. In fact, each sector has different metrics. For example:

| For a retail Industry: | For an Oil and Gas Industry: |

|---|---|

|

|

Over the next few chapters, we will understand how to read the basic financial statements, as published in the annual report. As you may know, the financial statement is the source for all the number-crunching required to analyse quantitative aspects.

Key takeaways from this chapter:

- The mindset of a trader and an investor is different.

- The investor has to develop an investment mindset if he is serious about investing.

- The investor should stay invested for a long period of time for the returns to compound.

- The speed at which the money doubles increases drastically the more time you stay invested. This is one of the properties of compounding.

- Every investment has to be evaluated on two aspects – qualitative & quantitative.

- Qualitative aspects revolve around the non-numeric information related to the company.

- The quantitative aspects involve analyzing numeric data. The financial statements are an important source of finding quantitative data.

Dear karthik sir,

I wanted to study and understand the investments done by FIIs in India.

Like, out of total investments done by all the FII put together, how much % of total funds is allocated in Index funds or large cap stocks or how much % invested in government bonds, so on and so forth. ?

Where can we get to see those data. Please share the details.

Thanks & regards,

Vaishakh

Hmm, not sure of this information is available. Do check once with the exchanges?

Sir how to identify fishy promotor most oftenly in smaall scale industry (sme market) there is less very less info available for there promotors on internet?

good afternoon sir .. sir can we create prompt that can analyse fin statement more easily if yes can you help us to list down hwhich factor shouldd we focus and how to identify red flag in companies management through ai ?

Arvnav, I think you can do that. I\’d suggest you speak to folks at Tijori Finance for this.

One way is to look at the financial statements, annual reports and get a sense of their business practice. That Is the only way.

Myself Shreyas Natekar, I\’m a finance enthusiast and a 1st year BBA student at MIT WPU, Pune with a business background in the family. I am planning to pursue CFA and I\’m planning to answer CFA L1 in my late 2nd year of college. I want some guidance by Varsity experts on what topics I should have a good knowledge in stock market and related fields so that I\’m well prepared for starting my CFA journey. I have a decent knowledge about commerce as a student. I\’ve been following Varsity since 1-2 months and it was a great experience learning here, but somewhere I feel I need more knowledge in the same field. I need your guidance and I have few questions as well:

1. Is CFA suitable for a student with no work experience in current learning stage? (cuz I\’ve seen most of working professionals pursuing CFA while working in financial analyst industry)

2. What are the things I should be well versed in before starting CFA?

3. When should I start working as a financial analyst so that it will benefit my CFA studies?

Your guidance will help me alot in my career, hoping for a helpful response!

Regards,

Shreyas Natekar

Hi Shreyas, I finished my CFA and got a charter about two years ago. Let me try to address your concerns.

Varsity is a good starting point for someone looking to pursue CFA. Sometime during my Level 2 prep, I realized my basics were not clear. So, I studied the Fundamental Analysis module on Varsity, and it set me well. This is before I started working at Zerodha Varsity :).

As far as your questions are concerned,

1. When I started my CFA journey, one could do it only after completing graduation. But the eligibility has changed since then. I think you can do Level 1 before completing your graduation. Many students now are doing it. When I received my charter, there were many that had completed all three levels but did not receive their Charter because they did not have enough experience. So, you can pursue CFA and complete all levels, you will get the charter after you have the relevant experience. And someone who has cleared all levels, your worth in the job market might be more.

2. The CFA Institute\’s course material is good enough for someone with basic commerce knowledge, which you say you already have. So, some diligent preparation should set you up for Level 1.

3. If you want to pursue CFA, relevant roles for you would be to work at a mutual fund, PMS, or AIF in their fund manager\’s team. You could also do wealth advisory or consultancy at a wealth management firm. You could also explore some roles in private equity, VCs, or investment banking firms. You can start working whenever you can. As a student, maybe look for internships to get a more real life understanding that you will learn in your CFA curriculum.

Hope that helps 🙂

Hello,

Thank you Vineet, that was really helpful. This greatly helps me to achieve a good amount of confidence to start my CFA journey.

Thank you again!!!

All the best! 🙂

I want to ask, does amount matter if we want to invest? Not just time, people tend to have opinion to invest in your early teens but I don\’t think so it\’s true since that amount should be invested in one, to improve skills, to travel or make new connection and get a better pay once left from grad. What\’s your opinion on this, sir?

Amount does matter. Yes, you need to spend your money on other things as well. This is where your sense of financial balance comes into play. But amount you invest in investments do matter.

Thanks a lot, will look into CQF and FRM too

Good luck!

Hi Karthik,

I hope you\’re doing well.

Thanks to these modules, I’ve developed a strong understanding of financial markets—Thank you!!!

I’m currently considering taking the CFA Level 1 and the NISM Research Analyst exams, and I wanted to get your opinion on them. Given my background in Computer Science, I’m also curious if there are other certifications or exams you would recommend for someone looking to break into this field.

I’d love to hear your insights!

Thank you

Glad to know, Abhay! CFA can be a big value, for sure. NISM is good too. If you are interested in the quantitative side, then do check out CQF and FRM.

http://www.nseindia.com/education/content/nse_pgp_others.htm

This link is not working can you provide new link?

Ah, they have updated the website, dont know where they have put it now.

I think it\’s perhaps this – https://www.nseindia.com/learn/find-a-course – But I haven\’t seen the earlier version so not a 100% sure.

Hi Karthik needed validation regarding following scenario. In order to address the sticky inflation, Central Bank raise interest rate, this move reduces liquidity in the market. Since liquidity is reduced for overall economy, this pushes businesses to reduce price of goods & service as demand is affected. Is this theory correct? Thanks in advance.

Yup, higher interest rates slows down consumption as there is lesser money in the hands of the people wanting to spend. As a side effect to this, merchants try to reduce prices to encourage spends.

I am reading this today, the link for nse education material is not there, I guess its after NSE site changed. Could you please point me to the new link of simila content in NSE?

Ah, not sure which link you are referring to. But do goto NSE India and click on LEARN tab 🙂

Can you please explain in detail how one can ascertain that the qualitative checklist is true for a company?

Please do check the module towards the end. I do have a checklist.

Just wanted to clarify one point – compounding in traditional sense works when you take the principal and interest and reinvest it. So for compounding to work in stocks – should i book my profits every year and then reinvest both the capital and profit or just stay invested….

Ah no, you just have to stat invested. But compounding in stocks is volatile, not as smooth as in a FD 🙂

Hello sir..!

I\’m a 23 old year trader having 4 years of experience with some good capital.

Now I\’m looking to invest.can you give me an idea about how it varys fundamental from technical other than holding period ?

These two are completely different studies. I\’d suggest you look at fundamentals especially since you are looking at investing.

Thank you sir it was really helpful.

Happy learning, Amrutha.

Hello Sir,

1.What is renounce rights, regarding right to issue of shares? Could you please explain it in layman\’s term?

2.Is it a trap or beneficial to buy the offered shares at a discounted price after the record date, how to buy them means via Demat account and how to trade them in open market?

3.In case if we do not buy renounce rights what will happen to our current holding shares? Will it get adjusted to discounted price or will there be any price adjustments like in case when the dividend payouts happen?

Check this, Amrutha – https://www.youtube.com/watch?v=m7U4liUJAkE&list=PLX2SHiKfualGOP9093b6qo11EsgCz8IuQ&index=7

YOu will get all your answers in this video 🙂

Hello Sir,

I want to redeem my ELSS tax saver funds, all units are completed necessary holding Period, now my question is if I place redemption order before 3pm will I get yesterday\’s NAV value? Which value do I get if I place it after 3pm?

Its best if you call the support desk for this, Amrutha.

Thank you for answering all my questions so patiently, Happy Sankranthi Sir🙂

Wishing you a very happy Sankranthi!

And also Sir regarding to my previous question reply, if I am not wrong we can not place trailing stop loss for CNC shares, in that case is it better to add our stop loss price as Limit order price or is there any other way around?

Yes, you will have to trail it manually.

Hello Sir,

Thank you for your valuable inputs,

1.Is there anything specifically, Can we do to reduce transaction cost in case of frequent swing trading?

2.Whats your thoughts about cup with handle pattern?

1) Place limit orders, choose liquid stocks, and dont overtrade 🙂

2) Its like any other candlestick pattern. Before you use it, make sure you\’ve back tested and have a sense of what to expect.

Hello Sir,

Thank you very much for answering my question, It\’s needless to say Zerodha team especially varsity is boon to retail investors.

I got few more questions to ask,

1.While logging to Kite we get the risk disclosure, One of which is Those making net trading profits, incurred between 15% to 50% of such profit as transaction cost. Could you please suggest us how this can be avoided?

2.Being a small retail swing trader in the urge to build trading capital I tend to sell my holding quite soon let\’s say within a week or two from making anywhere between 5-10% not holding too long even though I know the stock can goes up further by considering the market volatility and also nifty is trading at all time high with the fear of losing, Sometimes at the end I also feel instead of hopping between stocks like this for smaller profits which in turn causes increase in transaction cost, I would have stayed invested for a bit long period but to do so volatility is the concern. What would have been your approach sir in this situation, When we are aiming to build trading capital?

Thanks for the kind words, I\’m happy to note that you found Varsity useful.

1) The only way to improve is by constantly learning and implementing your new learning in the market. Of course, you also need to pay a lot of attention to risk management.

2) Yes, developing a mindset to hold stocks, that are especially trending in your direction is essential. Thats how wealth is created. One way to do this is to also trail a stoploss. Keep moving your SL, as and when the underlying stock moves in your favor.

Hello Sir,

Compounding will not happen in share market the way it does in FD or PPF, we have to manually sell the shares and reinvest along with the principal and profit amount is my understanding correct?

Yes, also compounding is not linear in stock markets. There will be volatility throughout.

What is equity futures , options , and other terms with these words sir ?

Please do read up all the modules on Varsity, we have explained each one in great detail.

this app is great for the new generation

Glad you liked it. Happy learning 🙂

Hi Karthik

As I have read this module and some queries

1. How can I check the above qualitative data about promoters, Related party transactions, operator activity in stocks etc?

2. How does compounding work in stocks sell and purchase?

1) Try sites like Tijori or Screener

2) Check this – https://www.youtube.com/shorts/hRaq52k8Q1Y

thankyou sir our brain is so complex. Iam reading again

Happy reading and learning 🙂

didn\’t get you sir what do you mean by to find a work around.

You need to find a solution here to figure what works for you Kris. This is largely via experimentation.

sir no company is perfect when it comes to qualitative analysis. then what should we do?

We have to accept that reality and find a work around 🙂

It\’s very very helpful, I\’m very with your way of explanation. It is easy to understand all the reports from core.

Happy learning, Divya!

Sir is there any app in which we can reinvest without selling share . Like,Just profit amount in protfolio.

Not sure if i can think of any.

Hi Karthik,

Firstly thanks for the modules on Varsity . I find them really informative .

I am presently on Module 3 on Varsity.

I am learning my way. I am actually from a shipping background but because of situations i am presently out of a job . I used to teach as a lecturer in the shipping field but was operated for brain tumour in June 22.

I actually am a member of Zerodha , my id is BP7487

I tried investing in shares on my own but ended up losing money.

Please can you guide me on the steps i must take to improve my trading skills and knwledge as this is now my primary source of earnings.

Please can you point me in the correct direction.

Thank you.

Conrand, I hope things get better soon for you. Sustaining monthly via trading activity is very stressful and can be very stressful. I\’d advise you against it. Instead, maybe find something you can do that will also pay you a monthly salary. This will ensure you have a line of income. Once you have this, you can maybe add trading as a 2nd source of income.

As far as knowledge is concerned, Varsity has enough and more to lead you in the right direction.

T S Venkatesh.

Sir, really very useful information, i am new to market, my one simple question that is a 60+year\’s person is it O.K for long term investment like 5 to 10 years in SEP method. I am very impressed Zerodha how to open Dmate a/c online.

Thanking you

T S Venkatesh.

Glad you liked the content, sir. Yes, you can start SIP at 60. In my own personal experience, my father started SIP when he was 60 and stopped a few months ago when he turned 79. Make sure you invest an amount that can be left untouched for a long time.

You can open an account online with us, check this – https://zerodha.com/?ref=varsity

21.7% How it is calculated? Formula for this?

However, since you decided to stay invested, the profits at the end of 3 years are Rs.173. A good Rs.13 or 21.7% over Rs.60 is generated because you opted to do nothing and decided to stay invested.

Its the compound interest formula. I\’ve explained this in the chapter itself.

Hi Karthik!

I have a question related to this

\”You decide not to withdraw Rs.20 profit; instead, you decide to reinvest the money for the 2nd year. At the end of the 2nd year, Rs.120 grows to Rs.144. At the end of 3rd year, Rs.144 grows to Rs.173. So on and so forth.\”

How exactly are profits reinvested? Sell the shares and immediately buys set of shares investors has identified? If possible can you pls elaborate on reinvestment part?

In this case, the interest is paid on the interest accrued, so in a sense, it is reinvested.

completed technical analysis ….very well explained.

Happy learning, Aditya!

\’an increase in interest rates means tougher growth prospects for Corporate India, can you justify this statement please ?

A higher interest rate implies the cost of debt, which means higher finance payments, lower margins, hence lower earnings, and therefore lower growth.

I read zerodha\’s motto behind varsity. You guys are really awesome. But more than I am humbled by your efforts of replying to comments, which I think is a great way to learn.

Two questions:

1. Are there only 11 qualitative aspects or this list is also endless?

2. Assume, I have gone through annual reports and promoters interviews etc, how do I learn more about any business like ground operations, challenges faced, malpractices, previous executives etc ? Also learning about a sector sometime is not enough I guess because each business is different in some sense in that industry.

Thanks for the kind words, Mohit!

1) It could be more, I just listed the ones that I think are most important, and I\’m fairly certain that we have covered the ones which matter the most.

2) The Easiest way is to search for management interviews and analysts interviews/articles.

Sometimes forums like valuepikr also helps.

Hey Karthik, I had the somewhat same topics in one of my undergrad\’s electives. Was not quite intrigued back them and seem redundant to know about these as a Mechanical student. Now it all makes sense now. I\’m 22 now and new into investing, Varsity seems to be the right place to start this journey.

Appreciate your efforts.

I\’m glad you liked the content and find Varsity useful in your journey. Happy reading 🙂

Hello Sir,

1) Where can I find the related party transaction information of a company?

2) What is considered to be a high related party transaction so one would be worried?

3) Recent it was announced that HDFC bank is purchasing a stake in HDFC ergo from HDFC Ltd. Is this considered a related party transaction and are there red flags to this?

Sunil,

1) You can find this in the annual report

2) Look at it wrt to the gross sales

3) Not really.

This is mentioned in one of the comment \”Varsity has a its own twitter handle – https://twitter.com/ZVarsity. All Varsity updates are posted here.\”

It\’s wrong, this handle belongs to someone else, please update it.

Ouch. Changing that. Thanks for pointing that out.

\”Girish’s decision to do nothing itself is market action\”- this line reminded me of the Five Star commercial where the boy eating five star saved an old lady from a falling piano. BTW excellent job by Team Zerodha. Cant wait to give (guru dakshina) invest when Zerodha goes public.

Happy learning, Sarkar 🙂

Hi Karthik,

I am beginner, forgive me if it is silly argument but I feel compounding works best when value of an asset is expected to grow steadily and surely.

Please consider this example,

A person holds 100 Infy shares at an average of 800 and LTP is 1000. A pandemic like Covid arise and price starts declining heavily.

Wouldn\’t it be wise to sell off shares and book whatever profit investor is getting?

Lets say person sells off shares @ 900 and when share price hits lowest lets say 600, person can accumulate more shares with the money he got by selling shares at 900.

My point is, would you still recommend to hold all 100 shares ignoring short term but heavy volatility and wait till market recovers and compounding takes effect? or would it be wise to book profit and accumulate more shares when share price hits rock bottom?

You are absolutely right. Equity returns are lumpy and are not expected to grow steadily like an FD. However, we generally tend to say EQ returns compound with the underlying premise that it is held on a long term basis.

Sir, different websites show different values of ratio. Example- In screen the P/E ratio of a stock is 24 & in tickertape the same is 28. Which one to choose or should we calculate it on our own:p

Hence, its always best to calculate this yourself. Make sure you take the consolidated numbers.

trust me zerodha team , you guy\’s deserve\’s to publish this book and be on amazon.I highly appreciate the effort\’s you guy\’s have made in making this course and absolutely free. Thankyou for this amazing effort .

Thanks, Ahmed. We will stick to the blog form for now 🙂

Good

valuable lessons

Happy learning!

Hello sir, I know you have been asked this plenty of times but I am still somehow not clear on where should I start my qualitative analysis from? Like, where can I find the list of promoters, their pledged shares and all the other required details. Ofcourse, I do not expect it to be readily be given somewhere, I just want to know where can I find the details?

Dhruv, you can find the list of promoters, their shareholding, pledged shares, other domestic/international institutional shareholdings, public shareholding and everything else in the annual report of the company. Do look through the same 🙂

Karthik sir, i hope you are fine

thank you for the superb modules.

sir, i have one doubt which is out of the module\’s context,

Why are you providing all these modules and why so much of efforts with free of cost? just asked out of curiosity.

Because we love doing this 🙂

Hello Karthick,

I have one question about relevance of compounding in stock investment. If I buy a stock at certain amount and hold it for long term, the value of the stock will keep increasing or decreasing depending on the market condition. It is not that I am selling when the price is high and buying again when the price is low. Then how is it that my profit (when the price is high) is getting reinvested? Plese clarify.

Thanks!!

The concept of compounding works as a conceptual thing in stock markets, used only to explain the returns. The profits are not reinvested unless you do it yourself 🙂

hello Sir!!

Great content. I have a question on compounding effect. As every year, the interest adds to the invested amount invested last year, so compounding will have an effect. Where as, in stock market, that is not the case. What I mean by this is, if I invest 100, there is no guarantee that by next year, the investment will become 120 and then 20% can be calculated on 120 to make it 144 in the coming year.

Can you please tell me how this compounding works in stock market where there is no guarantee in waiting for years.

You are right, compounding effect works perfectly well in the FD context. In equities, it may not be directly applicable, but you explain the overall returns using this concept.

Hi Karthik,

I am big fan of your work and have been following your work since 2015. First of all, thank you so much for giving all these valuable information for free.

I am working towards becoming a growth investor. After learning from you and also Learning App Zerodha, I beginning to understand that qualitative analysis of a company is more important than quantitative analysis. As a small scale retail investor, it\’s hard for me to assess the qualitative aspects.

So, I was wondering why don\’t I take inspiration from the portfolios of top Indian investors as they must have analysed the company and it\’s health way better than any small scale retail investor would have done. Do you think this strategy has to be part of fundamental analysis? Do you recommend any legitimate websites to follow the portfolios of top investors?

Thank you

Yes, qualitative aspects has to be a part of fundamental analysis, it is as integral as quantitative analysis. Not sure about websites, maybe you should check tijori finance once.

Dear Sir,

India Best Governed Company

1. Cipla

2. HUL

3. Tata Motors

4. Infosys

5. Tata Power

6. Wipro

7. Marico

8. Dr. Reddy

9. HDFC bank

10. HDFC

Which you suggest to right now to invest.

Unfortunately, I cannot comment on this 🙂

Dear Sir,

Which Mutual Fund or SIP has given 20% CAGR in last 20 years?

Thanks in advance

Vidyadhan Gedam

Sir, how to get out of a long term investment after finding red flags long after the investment is made.

You sell it mercilessly and get out of it, Jojo 🙂

Hi,

I am confused with so many volatilities. May please throw some light based on the below questions:

1. Why volatility is high before announcement by regulators and drops after the announcement. Which volatility is referred here and how to arrive at the number?

2. Also, from my understanding, VIX is for all F&O stocks. Is this right?

3. How Implied volatility for all strike prices of options are arrived?

1) Before a baby is born, wouldn\’t the family be anxious? In markets, anxiousness = volatility. Implied volatility is what is referred to here. More on this in the options module

2) Yes

3) The math is quite complex, I think NSE has put up a paper on this.

\”However since you decided to stay invested, the profits at the end of 3 years is Rs.173\”

It should be 13 Rs instead. Needs correction.

I meant to say profit plus principal.

How can i take Pdf copy? please let me know is there any way

Scroll to the bottom of the module page to download the PDF – https://zerodha.com/varsity/module/introduction-to-stock-markets/

Hi sir

How compounding work in stock market?

For example consider you invest 1share @ Rs.100 which is expected to grow at 20% year on year (recall this is also called the CAGR). At the end of the first year the money is expected to grow to Rs.120. At the end of year 1 you have two options:

Sell this 1share @120 and buy again @120rs for 1 share repeat this year on year for long term basis or

As invested 100rs for 1share and don’t sell for 10 years

This is awesome what u guys have done for anyone who is beginning to invest, keep doing the great work thank you so much.

Happy reading, Pavan 🙂

Hi Karthik,

Thank you for your great work. It is really very inspiring and interesting to read varsity content.

Do we have similar documents for mutual funds?

If yes then please share the same.

If no then please share the references to read the same.

Regards,

Yuvraj

We are working on the MF content, it will be a part of the Personal finance module. You can keep a track here – https://zerodha.com/varsity/module/personalfinance/

Hi Karthik,

I find myself lucky to have stumble upon this website. I do not have a business background and this platform has provided me with significant amount of knowledge regarding the basics of investing and how the market operates. I really appreciate your effort in this regard.

I am currently 25 years old and I am planning to start investing some portion of my income in stocks with a mindset of holding onto them for long term. I started recently and I am reading some books that have known to be the masterpieces in this sector and alongside going through educational materials like this one. As I have already decided to invest for long term, I find myself cornered with few basic questions. if I may ask:

1. When do you think a company is a good buy for long term investments?

as an add-on to this – How do you know the company is currently not overvalued?

2. When do you think it is a good idea to sell the stocks for a particular company instead of clinging onto them (even though you perceive them as a long term investments)?

3. How do you choose companies to invest in. (I currently work for an IT company in the United States and I have knowledge of a handful of companies in this domain)

4. When and how do you figure out that a company that was once promising to be a good long term investment is actually not a good candidate?

I know the questions are overwhelming, but the answers would provide me a good foundation. I am sure to come up with many more questions as and how I explore. Thank you so much for the time and patience you showcase by reading each and every comment/concern and answering to them.

Regards,

Pavan

Pavan, I\’m glad you are willing to invest in markets and that too for long term. This according to me is the right mindset to create wealth in the markets.

1) For this you need to develop a perspective into valuations. I\’d suggest you check this module on Fundamental Analysis – https://zerodha.com/varsity/module/fundamental-analysis/

2) Whenever you think the price does not justify the future earnings or when you think the original thesis that you bought the stock on is no longer valid

3) Perhaps, to begin with, you should pick and choose companies from this sector and leverage your domain expertise. Maybe start looking at other related sectors and gain knowledge about how they function. One of the best ways to gain knowledge about new sectors is by reading the annual report (Management discussion and analysis section) of the industry leader of that sector

4) This is an outcome of many things – financials, corporate governance, changing customer preference etc.

Good luck and happy investing, Pavan 🙂

Thank you so much Karthik for answering my questions :).

Good luck and happy learning, Pavan 🙂

Hi Karthik,

How can we make discisons on mid cap companies?

And small cap companies?

The same checklist applies.

The investment checklist towards the end of this chapter should help you with the selection process.

Thanks.

hello sir,

i want to ask ….how relevant is p/e ratio in valuing and analyzing growth of companies for long term investment ???

It is quite relavent, Anubhav. Helps you get a sense of valuations.

Also Sir,

I read somewhere in previous modules/chapters where you said that what a company pays to its employees has nothing to do with its share price.

Extending that to here, can it be deduced that what a company pays to its promoters and employees has nothing to do with its fundamentals/FA?

You need to watch how much the promoters make, if they are making a significant portion of PAT, then it is quite worrisome.

Thanks Sir for your prompt responses.

You are HERO-da of Zerodha !!

Lol 🙂

Thanks for the kind words 🙂

Not exactly .. What a company pays to its promoters also reflects strongly on the vision , ethics and integrity of the promoter. So an obscenely high amount compared to PAT will be alarming.

Cannot agree more, Himanshu!

Sir, Regarding point 10 about political affiliation:

In fact, when it\’s almost impossible to imagine setting up a company in India without political affiliation or patronage, how can a company be detached from political strings?

Most of the companies since 1947, were either set up under political patronage or evidently were too close to a political party and flourished!

Now, what about PSUs in which Govt. (in turn ruling political party) is major shareholder?

How a PSU can remain disaffiliated from a political party when the direcctors of that PSU are appointed by the ruling party itself?

Even American capitalist companies aren\’t dissociated from political parties. They too have inclinations.

How to identify a company\’s affiliation/inclinations towards a political party? (No Co. publishes it in their AR)?

How to decide whether an affiliation/inclinations is good or bad for the company?

Or

Should I drop the attribute no. 10 at all given that it ideally doesn\’t exist?

Well, you do have a point. But there are examples of companies which have performed extremely despite this – Infosys is a classic example.

can a retail investor buy research reports on companies/sectors etc from professional research organisations like CRISIL, foreign banks, Morningstar etc.? or are such reports by big organisations solely for the use by institutional investors even if the retail investor is willing to pay the money to buy such reports?

I\’m really not sure, maybe you should reach out and check. My guess is it should be easily available against a fee.

This Varsity is really good enough to start with… I honestly felt the need of a printable format..

Regards,

Santosh

Thanks, Santosh. Unfortunately, we do not provide printout/books of the content.

Pdf copies are available which can later be printed

Yo have mention to compare the company performance with its peers. But if some of the peers are not listed in the exchange then in that case how can we compare with those non listed peers?

Yes, in that case getting access to financials will be an issue and therefore cannot make an effective comparison.

Hi

In your qualitative criteria I think ethics should be segregated into breaches of ethics that hurts shareholders and those that help the company. I think the difference is significant for the purposes of an amoral shareholder.

So I do not see why no. 10 in your criteria is a negative. In fact the two questions you ask here are quite different; being close to a political party is a boon while \’requiring\’ political support implies a competitive defect which is a bane.

There exist several examples of Indian corporations that have close political connections and have grown in value over the long term(*cough, cough* RIL, Adani Group *cough, cough*) and I am sure every entity of a certain size has political connections in this country.

Also, are these criteria India specific? While some ethical criteria do apply weakly to India, they would apply even less in, say, banana republics where having ties to a despot is a competitive advantage.

These are sort my own checklist, developed over the years. Nothing is set in stone. There are not two ways about ethics and certainly no classifications. Yes, I do agree with you on the political connections – the question really is, how much of that connection is being leveraged for running the business.

What is the importance of pledge percentage? Can we buy the shares if the company has pledged its shares?

It indicates the % of shares the promoter has pledged. I\’d be concerned if this % is very high.

I analysed one company in IT sector \”8K Miles Software\”. Its growth is good. But its pledged percentage is 7.90. Should I analyse this further? The industry leader TCS also has pledged percentage of 2.98. So please mention how much % is ideal. Also please explain more about this factor in this chapter.

I\’m not sure if 7.9% is high or low. What you need to be doing is to investigate why so many shares are pledged and what are the promoters doing with the amount received.

Sir,

I have my trading account with broker Motilal Oswal and zerodha, I want to quit from Motilal Oswal and continue to trade on Zerodha.I hold some stocks with MO, can I transfer in zerodha to keep in the account are sell from here, charges or brokerages etc will be applicable? what is the procedure please help me out.

Check this – https://tradingqna.com/t/how-do-i-transfer-shares-from-one-demat-account-to-another/10825

sir, what is cash flow

and what kind of information this gives us?

Check this – https://zerodha.com/varsity/chapter/cash-flow-statement/

how to check Company fundamental

Annual Reports.

Also you mentioned about Suzlon being a wealth destructor. Do you see it as a turnaround company capable of generating long term wealth? Any specific checks that I can do?

Yes I too have same question about Suzlon..May be due to some bad decisions it was struggling..But some how feel it would grow as growth of Renewable energy and back up from Govts.

Hi Karthik

Comments please on how to analyze..

As I mentioned, I\’ve not been tracking this stock. So I\’m afraid I cannot comment. However, you need to see how the cash flow, P&L is performing. Also check if the debt has been reducing (or restrucured).

I had seen the balance sheet few months back, they are reducing their debt significantly. And they started making profits also I think last year. But I will go through the full Fundamental Analysis module, and then do my own analysis and then get back to you. (might take some time, please don\’t vanish).

And I wanted to thank you soooo much for developing Zerodha Varsity. Past couple of months, before coming across Zerodha, I was just reading randomly on Google, or watching some videos on Youtube. They were okay, I was getting to know what things are, but it was only when I started reading here, that I started to understand things fundamentally which is making my base strong. Zerodha Varsity is the Holy Book for me. And even more thanks for being there, answering to each and every question, no matter what it pertains to. Its a very good feeling to know that someone is out there to guide when we stumble across something. You are way more than wonderful with what you are doing. A big thank you from all of us, the budding trader and investors, for making us learn the words of wisdom 🙂

Thank you so much for the kind words and encouragement, Sansriti!

I hope I won\’t vanish 🙂

Not sure, I\’ve not checked that stock in a while now.

Hi Karthik

When you write \”However since you decided to stay invested, the profits at the end of 3 years is Rs.173.\” Do you mean the value will be 173 and the profit will be 73 only?

Yes, thats what I intended to say. The idea is to show that money grows at an exponential rate.

Actually in the first case you referred to profits as 60, and in the second case you said profits as 173. That\’s why I thought to point it out.

Ah, you have a point 🙂

Hello Kartik,

How can we find Operator activity in stocks.

Volumes to some extent give you that insight!

1, How to check shareholding pattern of a company. For example for Eicher Mototrs in moneycontrol.com I am just able to see Individuals / Hindu Undivided Family are holding 3.4% shares. But I am not able to see their names, so how to check their background? I even checked bse official website.

2. Also I checked corporate action in bse(for eicher motors). There it was mentioned that independent directors were appointed in march,june. So what deductions cn be made from these.

1) Use the annual report for this

2) Appointing independent directors is mandatory, nothing unusual about it.

Hi karthik, i have a question for you. While using charts on Pi, we see option to place a buy or sell order instantly through \”Quick limit order\”, so is there anyway this can be made \”quick market orders\” by changing the settings?

Hey sorry for asking this. i just discovered that it\’s possible after downloading the recent updates of Pi

Cheers!

Kathik bhai! You have become my guru because of the amazing work you did with Zerodha Varsity. I\’m a budding trader and i\’ve started my stock markets journey with zerodha only. Hope you grow to great heights, the market needs hardworking and committed people like you. Keep rocking. Luv from Hyderabad

Nadeem mia, shukriay for the kinds words !

Happy learning and best wishes from Zerodha HQ 🙂

Is there any website where we can check the any updates of the company

like announcement made by company regarding opening new unit,

None that I know off. However, I use google alerts to keep track of all the companies I\’ve invested in.

Hi Karthik

Where I can get easily about the qualitative aspects details from?

Thanks

I have provided few pointers here in this module. You can develop on those..also, the more time you spend in the market doing qualitative analysis, the better you get.

My means where can i get from? annual report of the company or any link

thanks

Not sure about the original source. Annual reports certainly wont have this.

Dear, why did you repeat the same thing (Profitability and its growth

Margins and its growth) The quantitative aspects. Is there any difference?

Thanks

Not sure, need to check up again. Thanks.

Hi dear, Does the registration have free of cost on the Zerodha Varsity?

No, Zerodha Varsity is free for all. You can read the rational on why we have kept this free here – http://zerodha.com/z-connect/queries/stock-and-fo-queries/introducing-varsity

HI Karthik,

Little out of context and personal question but i am sure you can help me.

I am a b.tech graduated from nit kurukshetra and this may i left my job because i want to make my carrier in finance as this is the field i love to learn and i am trading now as a perspective of learning only,But i think i must have to join a good corporate industry so that i can learn fast.So i am here for your guidance,What i do for a head start in this industry? i don\’t have a financial background but i am following market from last 4 month actively and i think i have a sound knowledge of market and its working.Had a interview with future first but i didn\’t make it.Need your guidance and i think you got my point.I want to work either as a trader or as a analyst.

I am reading continuously zerodha-varsity and i can say it is the best platform for everyone and specially for a non financial background.Thanks for your valuable work and this remind me the people who work hard for humans for a better knowledge and life,thanks for the valuable time,efforts and dedication.

Thanks for the kind words, feels satisfying when people benefit from our efforts 🙂

I think the best way forward for you would be to take up a globally recognized certification in Finance. I\’d highly recommend these three –

1) Get a CFA for a career in Asset Management – https://www.cfainstitute.org/pages/index.aspx

2) Get a FRM for a career in Risk Management or say a Business Analyst at large BFSI companies – https://www.garp.org/#!/frm

3) Get a CQF for a career in Quantitative trading – https://www.garp.org/#!/frm

Good luck.

Hi karthik,

Thanks for your prompt reply to my query,really appreciated your answer.

Still i satisfied with your answer but i have no plan to study further for a year or two because i want to get full market knowledge and experience and after that i will take a course in finance either through MBA in finance or the courses you recommended so here again i want you to suggest me further on my approach,i can do anything for my dreams.I hope you understand my concern.

Thanks for your kind support.

I understand, but a formal certification early in your career will take you a long long way later on, so do think about it.

hello MADHUSUDAN great to know you want to make career in stock market.

i also want to make my career in stock market. however my age is 20 year old. i preffer you de CFP (certified financia planer) course this is sort turm couse if you have clg deggre then you can complete this couse under 3 month (if you wiing to do study hard). you also got good job in future in stock/ finacial insutusion

sorry for my bad english.

Hi Karthik,

Do we have to manually do fundamental analysis by our own? It will be helpful if you mention some websites where those information is readily available.

Thanks,

Deepak

Check out https://www.screener.in/ and http://ratestar.in/

Hi, sir

How can we find red flag is raised pls explain about this once again

Like I said, its all in the Annual Reports. Reading it end to end helps. Additionally read and watch as many management interviews as possible. This will help as well.

Hi, sir

You have mentioned 11 Qualitative aspects in this model

But how can we get all these information about Related party transaction,operator activity in stock,political affiliation and all

Its all in the Annual Report, you need to read between lines 🙂

Annual reports as the name implies are only generated once a year.. Between the remaining 364 days, isn\’t this too a big a period where everything can happen ?

Secondly given the qualitative parameters you have indicated , will there be any company which will be satisfying all of them ? For e.g. even Infosys has been mired in ethics case w.r.t US visa misuse

Well, you can keep track of the company and the developments from its quarterly results. P&L is additive, so you get a good sense of how the sales and expense are trending. Any major debt the company raises is also reported.

No, its highly unlikely to find a company that scores well on all criteria.

Sir,what is your profession?What courses do i need to study to enter the investment business?

Durjoy – have you seen this? http://www.nseindia.com/education/content/nse_pgp_others.htm

Hi Karthik,

Zerodha Varsity\’s stock market education is not enough to do business as an investor, trader in Indian stock markets.

Still must we go for this http://www.nseindia.com/education/content/nse_pgp_others.htm to learn investment business?

Thanks and Regards,

Naidu.

I think this is good enough 🙂

How can I actively connect with Zerodha. I am a swing trader.,especially ther services & pricing/charges part. Thank you.

Best source – http://www.zerodha.com and our blog http://www.zerodha.com/z-connect.

We are also active on FB, Twitter, and other social media platforms.

Varsity has a its own twitter handle – https://twitter.com/ZVarsity. All Varsity updates are posted here.

Hi Karthik/ZeroDha Team,

Thank you for explaining the way one should approach towards wealth creation. Really helpful.

I have a question. As I\’m completely new, I\’ve gone through all the chapters (and modules) till this part. So, I tried to look at Zerodha margin claculator for Equity and Equity Futures and here are my doubts/quesries:

1) One can hold Equity Futures as NRML till its expiry date while the same stock could very well be bought for investement as an Equity under CNC order and it gets into ones DEMAT account

2) Zerodha margin caculator comes pre-populated with the stock price for Equity Futures but not for Equity. Which means, If I opt for Eicher in Equity Futures margin caculator, I get the price as \”18499.2\”. Now, if I want to check how many shares I can actually buy for long term investment for Eicher, I got to Equity margin calculator, bring up Eicher, enter the cash available and the price \”18499.2\” obtained from Future margin caculator and click Go to see the number of shares I can buy. The Equity margin caculator comes pre-populated with \”100\” as price for all equities it seems

3) NIFTY and BANKNIFTY are available under Equity Futures but not under Equity. Does it mean the indexes can be traded only in futures and if one wants to really buy equities as an investment specifically from the index like Nifty/BankNifty, one can buy that for individual companies listed in Nifty/BankNifty (I mean indexes)

Please bear with me as I\’m completely new and got confused at this point of time. Really thanks in advance for reading through my questions.

Glad to know you are liking the Varsity\’s material. Here are the answers –

1) Yes you can buy futures under NRML and hold till expiry or buy spot CNC and hold as investments in your DEMAT

2) Yes, you can modify the quantity and price. In fact I would suggest you look at nseindia website for live prices and you can feed the margin calculator with that price for more accurate results

3) Yes, you can trade NIFTY and Bank Nifty under the derivatives segment. However if you want to buy and hold, then you can buy the ETF. A nifty ETF called Niftybees is like a stock which you can buy and hold for long term…and the value of Niftybees varies as per the daily index value. Check this link for more details – http://www.nseindia.com/products/content/equities/etfs/etf.htm

Also, please feel free to ask us how many ever question you want. After all the purpose of Varsity is to share knowledge and help each other to become informed market participants.

Karthik, REALLY thanks for the awesome explanation. I have sent a mail to zerodha support to get the membership details. I saw Zerodha Pi section, it seems user can see charts on it and can place orders as well from the chart. Is it correct?

Good to know that Aditya 🙂 Hope you get on boarded fast, I\’m sure you will have a great experience with Zerodha.

Yes, with Zerodha Pi you can trade from the charts. Check this – https://zerodha.com/pi/

One question Karthik, can CNX NIFY JUNIOR be traded?

No futures on that yet, so cant trade I guess.

Can I go short for ETF? If yes, then how long I can open ETF short position?

You can short the EFT if its listed here – https://zerodha.com/margin-calculator/Equity/ , I can see Niftybees here, so you can short it. It works the same way as you short any other stock.

Please note, you will have to close your short position at 3:20 PM….also, I would be a bit hesitant to short ETFs as the liquidity is quite shallow.

Got it.

Thank You, Sir 🙂

Welcome!