5.1 – The Expense details

In the previous chapter, we had learnt about the revenues a company generates. Moving further on the P&L statement, in this chapter, we will look at the expense side of the Profit and Loss Statement along with the associated notes. Expenses are generally classified according to their function, which is also called the cost of sales method or based on the expense’s nature. An analysis of the expenses must be shown in the Profit and Loss statement or the notes. As you can see in the extract below, almost all the line items have a note associated with it.

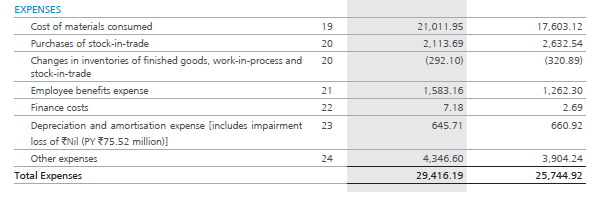

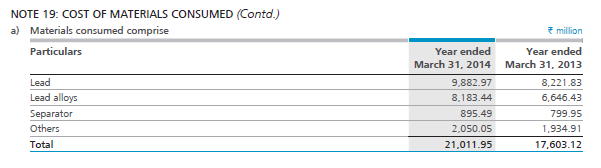

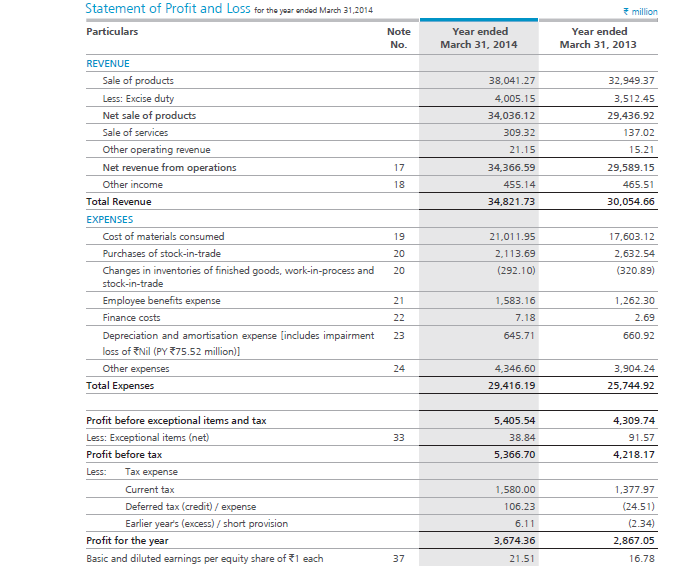

The first line item on the expense side is ‘Cost of materials consumed’; this is invariably the raw material cost that the company requires to manufacture finished goods. As you can see, the cost of raw material consumed/raw material is the company’s largest expense. This expense stands at Rs.2101 Crs for the FY14 and Rs.1760 Crs for the FY13. Note number 19 gives the associated details for this expense; let us inspect the same.

As you can see, note 19 gives us the details of the material consumed. The company uses lead, lead alloys, separators and other items, all of which adds up to Rs.2101 Crs.

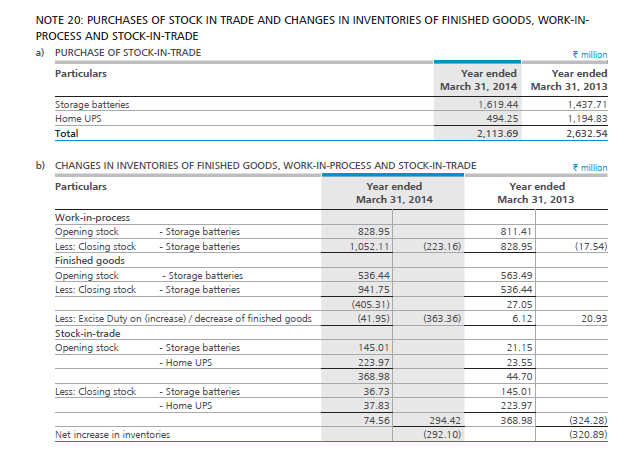

The next two line items talk about ‘Purchases of Stock in Trade’ and ‘Change in Inventories of finished goods, work-in-process & stock-in-trade’. Both these line items are associated with the same note (Note 20).

Purchases of stock in the trade refer to all the purchases of finished goods that the company buys towards conducting its business. This stands at Rs.211 Crs. I will give you more clarity on this line item shortly.

Change in the inventory of finished goods refers to the costs of manufacturing incurred by the company in the past, but the goods manufactured in the past were sold in the present/current financial year. This stands at (Rs.29.2) Crs for the FY14.

A negative number indicates that the company produced more batteries in the FY14 than it managed to sell. To give a sense of proportion (in terms of sales and sales costs), the company deducts the cost incurred in manufacturing the extra goods from the current year costs. The company will add this cost when they manage to sell these extra products sometime in future. This cost, which the company adds back later, will be included in the “Purchases of Stock in Trade” line item.

Here is an extract of Note 20 which details the above two line items:

The details mentioned in the above extract are quite straightforward and is easy to understand. At this stage, it may not be necessary to dig deeper into this note. It is good to know where the total lies. However, when we take up ‘Financial Modeling’ as a separate module, we will delve deeper into this aspect.

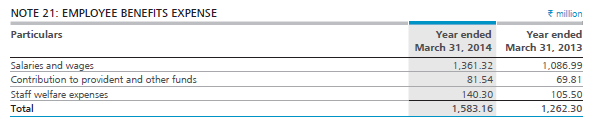

The next line item on the expense side is “Employee Benefits Expense”. This is quite intuitive as it includes expense incurred in terms of the salaries paid, contribution towards provident funds, and other employee welfare expenses. This stands at Rs.158 Crs for the FY14. Have a look at the extract of note 21, which details the ‘Employee Benefits Expense’.

Here is something for you to think about – A company generating Rs.3482 Crs is spending only Rs.158 Crs or just 4.5% of its sales on its employees. In fact, this is the pattern across most companies (at least non IT). Perhaps it is time for you to rethink about that entrepreneurial dream you may have nurtured.

The next line item is the “Finance Cost / Finance Charges/ Borrowing Costs”. Finance cost is interest costs and other costs that an entity pays when it borrows funds. The interest is paid to the lenders of the company. The lenders could be banks or private lenders. The company’s finance cost stands at Rs.0.7 Crs for the FY14. We will discuss the debt and related matters more when we take up the chapter on the balance sheet later.

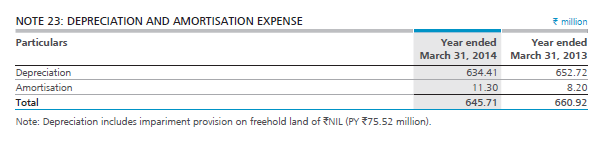

Following the finance cost, the next line item is “Depreciation and Amortization” costs which stand at Rs.64.5 Crs. To understand depreciation and amortization, we need to understand the concept of tangible and intangible assets.

A tangible asset has a physical form and provides an economic value to the company—for example, a laptop, a printer, a car, plants, machinery, buildings etc.

An intangible asset does not have a physical form but still provides an economic value to the company such as brand value, trademarks, copyrights, patents, franchises, customer lists etc.

An asset (tangible or intangible) has to be depreciated over its useful life. Useful life is defined as the period during which the asset can provide economic benefit to the company. For example, the useful life of a laptop could be 4 years. Let us understand depreciation better with the help of the following example.

Zerodha, a stockbroking firm generates Rs.100,000/- from the stockbroking business. However, Zerodha incurred Rs.65,000/- towards the purchase of a high-performance computer server. The economic life (useful life) of the server is expected to be 5 years. Now if you were to look into the earning capability of Zerodha it appears that on the one hand, Zerodha earned Rs.100,000/- and on the other hand, spent Rs.65,000/- and therefore retained just Rs.35,000/-. This skews the earnings data for the current year and does not really reflect the company’s true earning capability.

Remember the asset even though purchased this year, would continue to provide economic benefits over its useful life. Hence it makes sense to spread the cost of acquiring the asset over its useful life. This is called depreciation. This means instead of showing an upfront lump sum expense (towards the purchase of an asset), the company can show a smaller amount spread across the useful life of an asset.

Thus Rs.65,000/- will be spread across the server’s useful life, which is 5. Hence 65,000/ 5 = Rs.13,000/- would be depreciated every year over the next five years. By depreciating the asset, we are spreading the upfront cost. Hence after the depreciation computation, Zerodha would now show its earnings as Rs.100,000 – Rs.13,000 = Rs.87,000/-.

We can do a similar exercise for non-tangible assets. The depreciation equivalent for non-tangible assets is called amortization.

Here is an important idea – Zerodha depreciates the cost of acquiring an asset over its useful life. However, there is an actual outflow of Rs.65,000/- paid towards the asset purchase in reality. But now, it seems like the P&L is not capturing this outflow. As an analyst, how do we get a sense of the cash movement? The cash movement is captured in the cash flow statement, which we will understand in the later chapters.

Here is the snapshot of Note 23, detailing the depreciation cost.

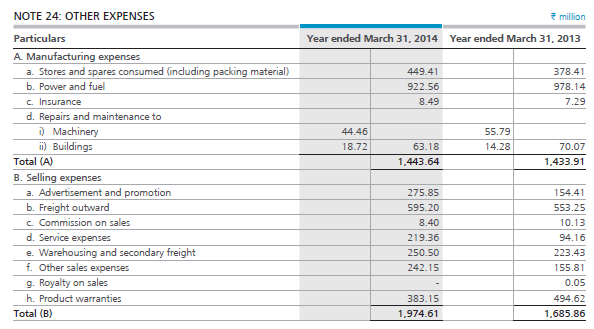

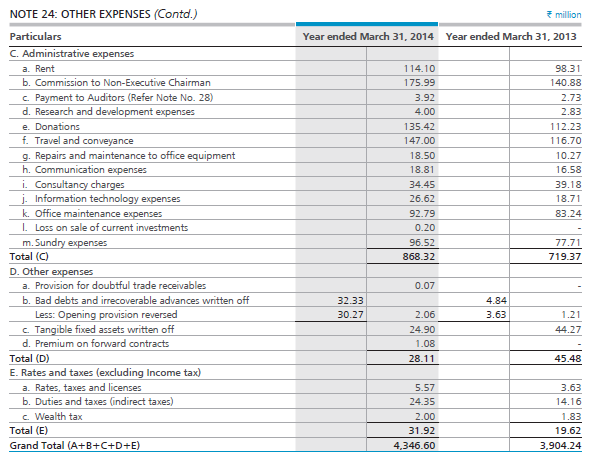

The last line item on the expense side is “other expenses” at Rs.434.6 Crs. This is a huge amount classified under ‘other expenses’. Hence it deserves a detailed inspection.

The last line item on the expense side is “other expenses” at Rs.434.6 Crs. This is a huge amount classified under ‘other expenses’. Hence it deserves a detailed inspection.

From the note, it is quite clear that other expenses include manufacturing, selling, administrative and other expenses. The details are mentioned in the note. For example, Amara Raja Batteries Limited (ARBL) spent Rs.27.5 Crs on advertisements and promotional activities.

Adding up all the expenses mentioned in the expense side of P&L, it seems that Amara Raja Batteries has spent Rs.2941.6 Crs.

5.2 – The Profit before tax

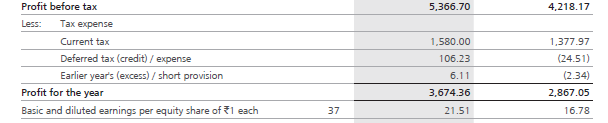

It refers to the net operating income after deducting operating expenses but before deducting taxes and interest. Proceeding further on the P&L statement, we can see that ARBL has mentioned their profit before tax and exceptional item numbers.

Put the profit before tax (PBT) is:

Profit before Tax = Total Revenues – Total Operating Expenses

= Rs.3482 – Rs.2941.6

=Rs.540.5

However, there seems to be an exceptional item/ extraordinary item of Rs.3.8 Crs, which needs to be deducted. Exceptional items/ extraordinary items are expenses occurring at one odd time for the company, and the company does not foresee this as a recurring expense. Hence they treat it separately on the P&L statement.

Hence profit before tax and extraordinary items will be:

= 540.5 – 3.88

= Rs.536.6 Crs

The snapshot below (extract from P&L) shows the PBT(Profit Before Tax) of ARBL:

5.3 – Net Profit after tax

After-tax, the net operating profit is defined as its operating profit after deducting its tax liability. We are now looking into the last part of the P&L statement, the profit after tax. This is also called the bottom line of the P&L statement.

As you can see from the snapshot above, to arrive at the profit after tax (PAT), we need to deduct all the applicable tax expenses from the PBT. Current tax is the corporate tax applicable for the given year. This stands at Rs.158 Crs. Besides this, there are other taxes that the company has paid. All taxes together total upto Rs.169.21 Crs. Deducting the tax amount from the PBT of Rs.536.6 gives us the profit after tax (PAT) at Rs.367.4 Crs.

Hence Net PAT = PBT – Applicable taxes.

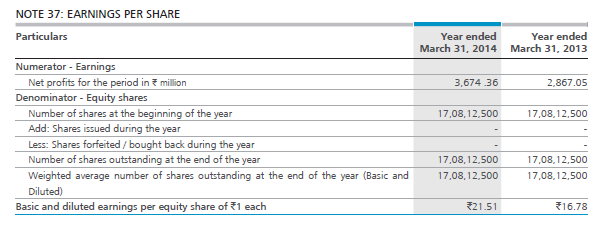

The last line in the P&L statement talks about basic and diluted earnings per share. The EPS is one of the most frequently used statistics in financial analysis. EPS also serves to assess the stewardship and management role performed by the company directors and managers. The earnings per share (EPS) is a very sacred number which indicates how much the company is earning per face value of the ordinary share. It appears that ARBL is earning Rs.21.51 per share. The detailed calculation is as shown below:

The company indicates that 17,08,12,500 shares are outstanding in the market. Dividing the total profit after tax number by the outstanding number of shares, we can arrive at the earnings per share number. In this case:

Rs.367.4 Crs divided by 17,08,12,500 yields Rs.21.5 per share.

5.4 – Conclusion

Now that we have gone through all the line items in the P&L statement, let us relook at it in its entirety.

Hopefully, the statement above should look more meaningful to you by now. Remember, almost all line items in the P&L statement will have an associated note. You can always look into the notes to seek greater clarity. Also, we have just understood how to read the P&L statement at this stage, but we still need to analyze what the numbers mean. We will do this when we take up the financial ratios. The P&L statement is also very closely connected with the other two financial statements, i.e. the balance sheet and the cash flow statement. We will explore these connections at a later stage.

Key takeaways from this chapter:

- The P&L statement’s expense statement contains information on all the expenses incurred by the company during the financial year.

- Each expense can be studied concerning a note which you can explore for further information.

- Depreciation and amortization is a way of spreading the cost of an asset over its useful life.

- The cost of interest and other charges paid when the company borrows money for its capital expenditure.

- PBT = Total Revenue – Total Expense – Exceptional items (if any)

- Net PAT = PBT – applicable taxes

- EPS reflects the earning capacity of a company on a per-share basis. Earnings are profit after tax and preferred dividends.

- EPS = PAT / Total number of outstanding ordinary shares

I think there is a slight correction and please correct me if I am wrong but \”A negative number indicates that the company produced more batteries in the FY14 than it managed to sell. To give a sense of proportion (in terms of sales and sales costs), the company deducts the cost incurred in manufacturing the extra goods from the current year costs. The company will add this cost when they manage to sell these extra products sometime in future. This cost, which the company adds back later, will be included in the “Purchases of Stock in Trade” line item.\” This is wrong. next year, when the excess produced inventory is sold – the ‘Change in Inventories of finished goods, work-in-process & stock-in-trade’ will turn positive, unlike stated in the paragraph. The \”Purchase of stock in trade\” is related to purchase of finished goods from outside only. Please clarify.

Hey Ashish, I need to review and clarify this myself. Will get back.

Sure, thanks. Please don\’t forget to update up.

Hi Karthik,

Thanks for this wonderful write up.

I have one doubt, basically who defines useful life of a product (5 years) in the above example. Why not 3 years or 7 years?

Thanks

Mithun

Well, thats the beauty of any financial analysis. You can use any time period you think is good enough, as long as you can justify why. For example, 5 years (or 3), for me strikes a balance between what the management says in their guidelines and projections that we can make as analysts.

Can you confirm that total COGS is the sum of Cost of materials consumed , purchase of stock in trade and Changes in inventories of finished goods, work-in-progress and stock-in-trade

Yes, thats right.

Hi Karthik,

What do you mean by \’ordinary shares\’ in the last takeaway point?

Ordinary shares means the regular shares that you and I can buy from the exchanges.

Dear Sir,

Note 19, Number of materials consumed

I have a question , Don\’t you think Others cost which is 2050 million rupees is a huge cost, i mean it is more then separator, so don\’t you think they should have mentioned large amount in other and should have classified more info?

Don\’t you think it raises a Kind of red flag?

Thank you for your response in advance.

Its not, its a standard practice. The notes anyway give you the proper split.

Sir, I didn\’t understand the line items \”Purchases of stock in trade\” and \”Changes in inventories…\” at all! Essentially note number 20. Can you please try and re-explain this using a simpler example maybe? For stock in trade and finished goods, shouldn\’t we deduct the amount of stock in trade sold and amount of finished goods sold? Why are we deducting \”Purchases of stock in trade\”? For COGS, we never deduct \”Cost of goods purchased\”, we only deduct \”Cost of goods sold\”. Why is the treatment different for \”Stock in trade\” and \”Changes in inventory…\”?

I\’ve kind of explained this in the comments a few times, request you to check once 🙂

wow still you are entertaining such questions..

my question is that point 20a purchase of stock in trade and in 20b stock in trade are same thing or what?

Yes, stock in trade, is stocks in trade 🙂

Hi Karthi,

Thank you for the wonderful content!

You mentioned that assets are purchased and depreciated over their useful life—in other words, the cost is spread over time. In your example, a one-time cost of Rs. 65,000 is depreciated over five years, resulting in an annual depreciation expense of Rs. 13,000.

You also mentioned that the full investment amount appears in the cash flow statement. Could you clarify how this is reflected in the balance sheet?

Looking forward to your insights!

Thats right, Krishnan. Do check the associated notes under the operational activity. If its a large expense, it will be mentioned.

Hello sir,

line item \”Changes in Inventories of Finished Goods, Work in Progress and Stock in Trade\” amount to (292) for the FY 14. In that case, would it be safe to assume that the same amount will be added to the top line of FY15 as and when the sale happens ? or will it be less or will it be above?

Yes, if the inventory converts to sales, then the revenue will be recognized.

Dear sir

1). What is equity share ??

2). Does outstanding shares have the total shares of the company including promoter, retailer, mutual funds, fii and dii ?

Suppose a company have one crore outstanding share in which promoter having 50% and FII having 5 % and DII having 10% and rest of retailer that is 35%.

So my question is – does it mean that promoter have 50 lakh share (50% of outstanding share , one crore) and FII having 5 lakh and DII having 10 lakh share and retailer having 35 lakh share. Is it true ?? Requested you to Please clarify it.

Pramod, all these things are explained here – https://zerodha.com/varsity/module/introduction-to-stock-markets/

After adding total head in expenses section, we are getting total expenses 30000.39 while total expenses is shown 29416.19 in the above ..

Plz clarify it . How it happened ?

Sir

After adding total head in expenses section, we are getting 30000.39 in inspite of 29416.19.

Plz look in

Checking, but can you share a bit more details. Also pls double check the details.

Yes, that\’s true, so it will automatically be included in the opening stock for next year. So do we still add it in \”Purchases of Stock in Trade\”?

New additions will be if there any such transactions during the year.

Sir, in section 5.1, it is written that \”To give a sense of proportion (in terms of sales and sales costs), the company deducts the cost incurred in manufacturing the extra goods from the current year costs. The company will add this cost when they manage to sell these extra products sometime in future. This cost, which the company adds back later, will be included in the “Purchases of Stock in Trade” line item.\”

Why will the cost of manufacturing excess goods included in purchases of stock in trade, instead of opening stock for next year?

Abhinav, anyway the closing stock for this year will be the opening stock for the next year right?

Hi Karthik,

In the addendum note 20, we consider below items:

1. Purchase of stock in trade (essentially any finished goods purchased directly). These may be purchased from some other seller or carried forward from last year (closing stock of unsold finished or WIP goods).

2. Change in stock in trade opening and closing stock. (this is straight forward as it just sees what is the opening stock in trade and closing stock in trade)

Then shouldnt we be able to see some matching in 1 & 2. Since if the above definitions as per my understanding are correct, then any purchase of stock in trade done in 2014 should also be equal to change in stock in trade at the opening and close. Why do we see that the change in stock in trade is only 294 while purchase is so much larger than this 2193?

Wont really be the same, Yaqoot as there is the addition of new stock in trade and also flushing out of old stock in trade and recognizing as revenue. So you have to factor in these things as well.

Hi, Karthik.

If Purchase of Stock in trade = Cost of unsold FG from PY that are sold in CY.

Then, if the changes in inventory is positive, that means cost of extra FG sold is already accounted for, right?

So doesn\’t this lead to double counting?

Why do I have Purchase of Stock in Trade as a separate line item, when changes in Inventory accounts for less/more units sold?

Ah no, it cant. The idea is that the provious year\’s number is not recognised as cash inflow.

Hi Karthik, In Note 20, shouldnt the Opening Stock for FY 2014 match with the closing stock for FY 2013?

Ideally it should, but we go with the data from AR, and look for the supporting notes in the addendum.

Can negative number in change in inventory be explained? im having trouble wrapping my head around how the number becomes negative when you are including previous year\’s number

Usually this happens when you sell more than what you have by taking an advance from customers.

Hello sir,

I hope you are doing well.

This is regarding Consolidated and Standalone Statements.

Lets say a real example, Godrej Industries is the Flagship holding company of all Listed Godrej companies.

Standalone the company is making a net loss. Consolidated the company is making a net profit.

So When reading a profit/loss statement, Shouldn\’t the income generated from being a stakeholder of other companies come under other income sources? How do you classify this as I am a little confused for the same

Yes, it does in consolidated right?

EPS is mentioned as 21.51 in the last part of P/L which states that all values are in Rs(million). Shouldn\’t they specifically mention it individually as Rs 21.51 for better clarity? One might assume that it is Rs21.51 million.

Ah will state it explicitly, but EPS of 21.51 Million, I hope nobody assumes that 🙂

Hello Karthik, I might be wrong but the thing is under the section 5.2 PBT & 5.3 PAT you have called them as Operating income and operating profit. But what I understand is, it cannot be that because under the Revenue section of the company there is \”Other income\” which comprises of interest and income from equity, mutual funds etc. which is non operating in nature.

So in my opinion exclusion of \”other income\” leads us towards operating income or profit. Please clarify

Its ok, as long as the other income is a tiny portion of the over all operating revenues.

Purchase of stock in trade – cost of finished goods purchased required for company.

change of inventory – cost of manufactured goods in past which are sold in this current financial year.

then from where company will withdraw the cost of extra manufactured goods and where is the negative sign ?

and when they will be sold they will be added in the purchase of stock in trade .

so the picture of expenses which is displayed

what really purchase of stock in trade shows ??- cost of finished goods purchased OR cost of extra manufactured goods of past which are sold in this year

and what really change of inventory shows ?

We have discussed this in the past in detail, request you to kindly check the comments section above.

Hi,

Can you please check Note 24- D.Other expenses- d.Premium on Forward Contracts- 1.08 million.

What is exactly the kind of expense? Should it not form part of balancesheet.

Forward contracts are like futures contract where the company tries to hedge its forex risk by entering into agreements with banks or institutions. The margin is referred to as the premium for forwards.

Profit before tax & extraodinary items should not deduct amt of extraodinary expenses because it is before not after

Yeah, we do if its usually stated in the P&L.

Hi,

Thanks for this. But what if a company is a trading company and doesnt manufacture products in house. In that case how would the COGS look like across a) Cost of materials consumed b) Purchases of stock in trade c) Changes in inventories. Thanks in Advance.

There will be expenses even if it is a trading company right?

as we know (interest, company has to pay on the loan taken) what else comes in Finance Cost?

It is just the interest component that comes in finance charges, Kushal.

Under the expense side, the first three line items as given for Amara Raja batteries are:

Could you kindly let know if I rightly understood for the above three?

1. Cost of materials consumed: Denoting \”Cost incurred to purchase against those finished products that are sold in this FY\”

2. Purchases of stock-in-trade: Denoting \”Cost incurred to purchase against those finished products that are prepared in last FY but sold in this FY\”

3. Changes in inventories of finished goods, work-in-process and stock-in-trade: Denoting \”costs incurred against those products that are produced but not yet sold/ work in progress/ produced in previous FY but yet to be sold this FY\”

Yes, these are correct, Anirban.

Sir this may be a silly question but how the numbers are rounded off.Means to the higher decimal value or lower decimal value. Ex 55,30,56,456 Rs is written 55.31 Cr or 55.30Cr.

They are not rounded off, they are treated as actual. If you are unable to see in excel, that is because the decimals are hidden.

I had a silly question… if we consider buildings as Assets, and since all assets must be depreciated, I wanted to know what happens to those building assets that appreciate in value over time, is there any considerations for this in the accounts?

Gian, Building as asset if this is used for Business purposes the Depreciation can be Claimed and a Depreciable asset when you sale it will be Short Term Capital Gain. And if it is in some individual name and he has plan to Exit in the Future he should not depreciate the office building.

I would also like to know whether there is any quick way to calculate the interest rate of debt for the company? Thanks.

Interest paid or finance charge paid divided over total debt will give you an idea of the interest rate obligation.

\’Purchases of stock in the trade refer to all the purchases of finished goods that the company buys towards conducting its business.\’

Sir in this, what do you mean by \’purchases of finished goods\’? Why does a company need to buy its own finished goods? Are you talking about retaking their finished products in case of warranties or does it mean something else? Thanks.

Its more of a revenue recognition method where in finished goods made last year, but not sold are taken back to books the year in which its sold. Have explained in comments.

When the company says that they have incurred an inventory gain in this quarter. what it is inventory gain and loss in that sense? Does -ve number denotes inventory gain or loss?

It just means that the old inventory has appreciate in value.

Is ROCE the only criteria to see whether a company is reinvesting its profits and growing its business. Or can you suggest something in addition to ROCE?

No, you can even check the movement in cashflow Sathish to get a sense of how the company is allocating its capital.

I understand your point sir. But \’changes in inventories\’ is reported on quarterly basis as well in P/L sheet and it keeps getting changed. That is why the confusion. Also where would \’the number of inventories not sold\’ which are not being deducted get entered? Thanks

Ah ok, Sathish. The reporting of the number of inventories not sold, I\’m not sure if that\’s explicitly mentioned. Needs to be extracted I guess.

Sir I have read your explanation on comments section also regarding changes on inventories but still couldn\’t understand the meaning of negative value. In the example you gave, if company manages to sell 80 out of 100 manufactures (each battery cost 50), we are deducting 20*50 = 1000 Rs from current quarter. (out of Rs.5000)

1. Then where would that remaining Rs.1000 get entered?

2. Even if you add this 1000 to next quarter\’s change in inventories, in the eg, you gave if company manages to sell the additional 100 + remaining 20 it produces previously, still we are deducting this number in addition to the 5000Rs only right? The how can we get a positive number. Shoudn\’t it be (-6000) Rs?

I have done enough google search and forum reads, but couldn\’t understand this negative number concept sir. If you could answer this, it will be of big help. Thanks.

The correct way to think about it is basically apportioning the expenses of manufacturing to the time when the inventory is sold. Also, these are balance sheet adjustments that happen on a yearly basis and not quarterly.

What is the difference between Purchased of Stock in Trade and Changes in Inventories of Finished Goods , as what i understood from the above article is Purchased of Stock is the Items manufactured in the last year where as sold in the Current Year so that particular cost has been added now , Similarly Changes inventories of Finished Goods also have the same meaning , can u please clarify

Yes, thats right.

During the discussion on employee benefit expenses, it looked like a small expense, 5% of the revenue.

However, looking at PAT of 367 Cr, the employee benefits of 158 Cr doesn\’t look that small anymore.

Indeed!

Hi Karthik Sir,

Hope u r doing great.

Small doubts:

1.Why Change in the inventory of finished goods is under expenses , however this is something which the company will anyways sell and make money.

2.Does the opening and closing stock means how much at the start of the FY and end of the FY.

3. Can you please put some light on the value of Change in the inventory of finished goods being negative or positive.

1) Yes, so it gets recognized when the sale happens. If the sale does not happen, it will remain an expense right?

2) Yes

3) It just indicates the increase/decrease in inventory position.

How can i find COGS? My Questions is given:

opening inventory, Raw material consumed, Electricity/ power&fuel, Changes in Inventories of finished goods & raw material, employees benefits expenses, depreciation and amortization, other expenses, Finance costs

You just have to add all these things which make up for the COGS of the company. Thats it.

Hii! Karthik bro! A serious mind boggling doubt from me. Please give me a solution. If Inventory decreases, old goods would be sold now. You said that C. O. M. G will be included in purchases of Stock-In-Trade. That means same thing is being added twice. In brief, what is the difference between stock-in-trade and change in inventory?

Stock in trade includes things that will be used to make the final product. The final product if unsold will remain in the inventory. Nothing is added twice 🙂

Hi Karthik, Can Exceptional items under expenses be credit type?. Example if some company sells one of its subsidiary and this is an one-off event. In this case company gains money and will this be added in revenue side or still be under expense side.

It will show up as other income or an exceptional income item.

Sir,

what is purchase of stock in trade?

Purchases of stock in the trade refer to all the purchases of finished goods that the company buys towards conducting its business. -i found it on google.

ARBL is manufacturing company, why its purchase finished goods insted of manufacturing them on its own?

Raw materials which come in the form of finished goods.

Vry sry 2 say, dis is not exactly what I want 2 know..my question is how can I calculate this value 64.5 cr (63.4+1.13)..I can\’t match dis value from balance sheet.. actually I don\’t hv enough idea about accounting..so plz lf u clarify dis..I can solve my doubt…thnk u..

64.5 is the D&A number, it is calculated by the company\’s auditors.

Hi , Karthik..wd u plz like to xplain me ,hw could u find the value of \”dep and Amortization” costs which stand at Rs.64.5 Crs. Bcoz I am not able 2 find dis value from balance sheet \”accumulated depreciation \” section.

Pari, please check in the expense side of the P&L statement.

I\’m not able to understand change in inventory of finished good and how it is different from stock in trade meticulously. Sir kindly explain it explicitly.

Vineet, have explained this in the chapter and across the comments. Can you please check this once?

This article is so helpful. But I am not able to find the added notes in the P and L account of a company. So it\’s getting a bit difficult for me. How do I find it out?

Riya, please scroll down the AR. You will find the details.

it\’s a request to add a dark mode to the web page as it put stress on my eyes while reading.

Noted, Vaibhav.

karthik sir in above paragraphs you are saying that whatever finished goods are not sold in current year their cost of manufacturing deducted and adds in purchase of stock in trade. in comments you are supporting manoj sirs comments where they are saying something different. can you please review comments of both of you. because its making confusion to me.

Ah, I need to check the old comments. Will do that sometime soon 🙂

Great information .

Very helpful for beginner .

Keep uploading these type of information.

Happy learning, Raushan!

key Takeaway point no. 8

It should be Total number of outstanding ordinary shares / PAT not the other way around.

Checking this.

Karthik, thanks for the reply. Can you please elaborate the sentence \”other comprehensible income includes unrealised P&L owing to investments (FX hedge)\”. Also, can you please make me understand the meaning of realised and unrealised P&L?

It includes notional profits or losses for the year arising out of investments or hedges. You can exclude this in your calculations Attraya.

Sir one thing that I would like to say \”मजा आ गया\”

Hi Karthik, In P&L statement of most companies now I am getting two additional sections after the PAT section: Other Comprehensive Income and Total Comprehensive Income for the year.

1) Could you please tell what these means and their significance?

2)Does calculating EPS we need PAT or Total Comprehensive Income for the year?

The total comprehensible income is the net P&L, but other comprehensible income includes unrealised P&L owing to investments (FX hedge) etc.

For EPS, take the total comprehensible income.

Sometimes, when there are operating losses, which i mean, expenses are more than revenue, and in that case we see taxes in negative number. What does negative tax mean?

Taxes cant be -ve. Can you please double-check this?

How to find cost of goods sold in above statement?

Please look at the expense side of the balance sheet.

Hi Sir, thank you very much for this wonderful learning opportunity.

EPS is equal to PAT/Total No of Share or PAT/No of share outstanding in market?

i.e is it (17,08,12,500) total number of share available in market? what about the share holding by Promoter , Is should not be part of EPS?

Total number of shares, DJ.

Hello sir,

Where would that be shown in the quarterly result?

Assume I have a sale of 1000 Cr for 1 quarter.

Out of the 1000 cr sale i only receive payment of 800 cr. The rest 200 is still pending.

On the quarterly sales do I show 800 cr or 1000 cr?

That will reflect in trade receivables of the balance sheet.

Hello Sir,

Does that mean that after the company had a turnover of 1000 cr they received a PAT of 100 Cr?

What about money they have not received? Like some of their customers have not paid up, they would still have a turnover of 1000 cr but the profits would reduce correct? Is there a way they mention this or adjust this?

That would be pending in the balance sheet, once its received, will get added to the accounts.

Hello Sir,

I hope you are well.

For Quarter 1

Company X has a revenue of 1000 Cr.

Net PAT is 100 Cr.

How much of this 100 Cr profit is actually received by the company? Is there still money to be received from debtors??

Its 100Cr after factoring in all the costs, hence PAT is also called the bottom line of the company.

Sir,

Can you pls tell me which figures in P&L we should really bothered to buy stocks. How to judge a stock from P&L??

And really thanks for the effort.

Not just the P&L, its the financial statements in its entirety that you need to consider.

Hello Sir,

To follow up with my previous question.

Can you explain free float market cap?

Also I don\’t understand your statement of diluted shares. What exactly is it?

Will try and add a chapter on this.

Please Correct me if am wrong. Section 5.2 is saying about Profit before tax. \”It refers to the net operating income after deducting operating expenses but before deducting taxes and interest\” I guess it should be written only Tax & Not Interest. Since it PBT.

Yup, thats right.

Hi Sir,

The number of equity shares outstanding is shown in the liabilities side of a balance sheet correct?

Is the entire number of shares created? This would mean the sum of all Promoter + FII+DII+Public = 100?

Could you explain free float market cap?

Also lastly could you explain diulted share equity/ diluted EPS? What does diluted mean?

Yes, from the company\’s perspective, this is a liability. Yes, it includes all the shares. Diluted means the shares come into existence by considering the further issue of equity.

Thank you Karthik.

One more question! How will we know when(on what date) a particular company is going to announce their results ?

Tough Sunil. You will have to track the company and get the news around that.

Hi Karthik,

May I know, What is EBITDA, I here a lot about EBITDA when some is looking at company\’s Announced results !! Will the Financial reports contains any details about EBITDA ?

Sorry! I\’m still going through chapter by chapter, please let me know if there\’s any mention about EBITDA in any chapter. Thank you.

Earnings before interest, tax, depreciation, and amortisation = EBITDA

Basically income minus the expense. Helps you get a sense of how profitable the company is at an operating level.

Okay. Thanks 🙂

Greetings,

In the following statement what does this line means \”which is also called the cost of sales method\”? Do you mean to say \”which is also called the cost, of \’sales method\’ \” OR \”which is also called the \’cost of sales method\’ \”?

And how do I comprehend/Interpret it ? I tried google but not much help. Can you please re-word the whole sentence?

Please revert, Thank You

Main Statement => \”Expenses are generally classified according to their function, which is also called the cost of sales method or based on the expense’s nature.\”

Ah, let me relook at the context, but I guess I meant expenses is also the cost of sales. I\’ll get back on this.

How do I know the auditors cost in annual report?

Do check other expenses under the expenses section in P&L.

Karthik Rangappa – Very nice work and initiative from you and Zerodha 🙂 Keep producing great content like this for everyone\’s Financial and Market literacy.

Happy learning!

Hello Sir,

What about companies that have a large amount of other income.

Way more than their operational income??

For example, holding companies like Alembic Ltd.

That could be a cause of concern, you need to figure out why such an income exisits. It could be due to an asset sales, please check if its recurring or one off.

Hello Sir,

When reading the company\’s quarterly report, where can I find the source of other income?

When can I classify other income as a bad thing or a red flag per say

In the associated notes. All companies have other income, its not a red flag.

Current FY Yr – company manufactured 100 batteries, 50 R/- each one, so total cost incurred is 5000.

But company only mangaed to sell around 80 batteries, so they decided to deduct 20 batteries cost (1000 R/-)

* Change in Inventories of finished goods, work-in-process & stock-in-trade = -1000

Now next FY Yr – company did the same output again, but this time they mangaed to sell 120 batteries (20 more in stocks). So now they needed to add 20 batteries extra cost (1000)

* Purchase of stocks in trade = +1000

Am I right?

Yes, that\’s roughly how these line items are treated.

This is too good. I mean the whole material that too available for free, its awesome!!!!! Thank you zerodha and Karthik sir!!!!

Happy reading, Keshav!

hi sir…

what about the transportation cost of a company…can you tell me about it?

You need to look at the annual report for that.

Hi karthik,

Is the Earnings per share anyway related to the share price.Say,will this amount be given to the share holders

Not really. Earnings per share is an indication of how much the earning of the company is on a per-share basis.

Hi sir,

Thanks for sharing, What is difference between excise duty and tax paid on the same revenue.

Excise duty is on manufactured goods, I don\’t think this is applicable anymore.

Very nice infosir

Happy reading.

First of all, big thanks to team Zerodha for Zerodha versity.

I am reading Zerodha varsity and learning a lot day by day. It is very interesting to read it as the method of teaching is very simple and language as well. The journey would be more wonderful if I get a printed copy of it. Please let me know if you have any facility of providing printed copy of Zerodha versity, if not please include the same facility.

Thanks for the kind words 🙂

Unfortunately, there is no option to print the content. However, there are PDFs made available, which you can print (if required).

Sir I\’m asking 65000 will be shown on expense side of Profit and loss account, but in cash flow statement 15000

Sir will 65000 will be deducted as depreciation for current year only as entire amount

It is on a yearly basis.

Sir in previous chapter you have explained about stock in trade in this chapter you have wrote about purchase of stock in trade does both mean same, I read this chapter for 4th time no clarity on inventory or stock in trade scrolled through comments no use, can use brief me about this topic sir

Have explained this several time in comments, can you please check?

In note 20 changes in inventories, why some of the numbers are written in brackets ()?

Usually indicates outflow.

valuable lessons

Thankyou sir

Can you please elaborate, I am still confused because the stock in trade is already counted in inventory and it will get reflected in changes in inventory, then why it is added as an expense again ?

Btw, this is not a standard line item in P&L, so don\’t worry too much about this. Inventory is a balance sheet item, which is representative of the year on year change, it cumulative. Whereas the P&L accounts for the yearly details, hence since this is an expense, it will be reported in the P&L as well.

\”A negative number indicates that the company produced more batteries in the FY14

than it managed to sell. To give a sense of proportion (in terms of sales and costs of

sales) the company deducts the cost incurred in manufacturing the extra goods

from the current year costs. The company will add this cost when they manage to

sell these extra products sometime in future. This cost, which the company adds

back later, will be included in the “Purchases of Stock in Trade” line item.\”

In this paragraph, you said that the cost will be included in the \”purchase of stocks in trade\”, but stock in trade means the finished goods that the company buys to sell them as they are. Then why the cost of the goods that the company manufactured and was unable to sell will be added in \”purchace of stock in trade\” ?

By the way Thankyou very much for the articles, you are doing a great job by helping people learn for free. These articles are really amazing and helpful.

Neel, that would reflect the previous year\’s excess, unsold, and included in this year. Happy learning 🙂

Purchases of stock in trade, refers to all the purchases of finished goods that the company buys towards conducting its business, My confusion to this is that why do a company have to buy a finished good if they\’ve only made it or is the statement referring to all the finished raw materials a company requires. .

Treatment of the inventory carried forward from the previous year and sold in the current financial year.

It is written, \”Purchases of stock in trade, refers to all the purchases of finished goods that the company buys towards conducting its business.\” I just wanted to know..why is it written as \”refers to all the purchases of finished goods\”.. why not \”refers to all the purchases of raw materials\”

Can you please explain change in inventories of finished goods, WIP and SIT and Purchases of stock in trade with example to get more clarity?

Also explain WIP and SIT a bit.

Really appreciate your content. Very helpful and informative.

I have done that in the chapter and comments itself. Is there anything, in particular, you are looking for?

thanks karthik 🙂

Hello karthik..hope your are doing great..just a small query. Couple of times companies change their accounting policies for treatment of depreciation or something else, just to change their figures of profit. i just want to know, how shall we know about these changes. Whether they mention clearly in annual report or we only have to figure it out by ourselves.

Manish, companies have to comply with the accounting norms set by the regulators, they cannot change the policies as and when they wish. Also, if there is a change, that would be explained in the AR itself.

I understood how a tangible asset can depriciate but how a non tangible asset like brand name can depriciate? Because it is older the brand higher the trust 🤔🤔

Intangible assets are amortised 🙂

Karthik, Thanks for clarification. 🙂

Good luck!

Dear Karthik,

Thank you for such an informative session. I have one doubt regarding the “basic and diluted earnings per equity share of Re. 1/- each”. As i understand the Face Value is assumed as Re 1/- to calculate the EPS. But, suppose the Face Value is some other value other that Re 1/-, for eg Re 5/-. Then do we need to divide the EPS by 5.

There are companies whose Face Value is not 1. So, the calculation will vary to calculate the EPS?

Thanks in advance.

Amol, you dont really consider the face value of the share to calculate the EPS, what you need to consider is the number of shares outstanding. Divide the earning by the number of shares.

Sir, your example for depreciation cost (for server purchased) was very helpful and understandable. For better understanding, could you please give us an example of amortization as well?

Will try to do that. It is just that amortization is applicable to intangible assets such as say goodwill or brand.

While I completed intermediate level on Fundamental Analysis, an answers at the end of intermediate quiz was marked wrong.

Q. Two parameters required for calculating EPS?

—> I choose PAT and No. of O/s Eq Shares option. But the app marked it wrong and the correct answer according to it was Share Price and No. of O/s Eq Shares, which I feel is incorrect.

Please Clarify.

That\’s a mistake. What you opted is the correct answer. Will have this changed. Thanks for pointing.

Thanks a lot Karthik.It resolved my query.:-)

Happy learning!

what is the difference between \’\’Basic\’ and \’diluted\’ earnings per equity share ?(Basic vs Diluted)

Have explained this in couple of queries, request you to please check that. Thanks.

Sir, didnt understand the Purchase of stock-in-trade and the Change in inventories and their relation

Have explained this in couple of place in the article and comments, Mohit.

Purchases of stock in trade, refers to all the purchases of finished goods that the company buys towards conducting its business. Why does a company buy its own goods towards conducting its business? Or am I interpreting it in the wrong way?

Every manufacturing company needs raw material right?

Sir, Regarding previous question about circuit. Maybe a silly question. In an upper circuit we will not be able to buy that particular stock unless the upper circuit breaks right? Similarly how will the sellers be able to make profit when there are no buyers available in lower circuit.

Sellers get an opportunity to sell at a higher price when the stock hits upper circuit and buyers get to buy the stock at lesser price when the stock hits lower circuit.

hello sir,

What exactly happens when a stock falls under upper circuit/lower circuit?

For ex. Now adanigreen stock is under lower circuit. It has only sellers and no buyers. So how exactly are the sellers booking profit when no buyers are available? who is buying them now?

The circuit is like either the buyers or sellers get adamant and refuse to budge. For example, if a stock is very bullish, sellers would want the highest price because they know buyers will buy at any cost. So sellers won\’t budge. Ice will break only the next day or when sellers decide to cool off the price.

Sir what is price action strategy or price action?

Trading based on the price movements is referred to as price action trading.

Thanks Kartik..for the reponse.

But do we have any site where industry specific cut off will be mentioned based on ROCE and ROE??

Regards

INSAH

Cant think of any, Indranil.

Hi sir,when will financial modeling will come from your pen eagerly waiting sir!!

It will take some time Mahesh, I\’m still working on the personal finance module.

Dear Karthik

Thanks for sharing this details expalnation for P&L Statement

I have few Question.

1)For calculation Operational Income the formula u mentioned is

Operational Income =Operational Revenue (Sales+ other operational income) – Operational Expenses.There are some other incomes as u mentioned like Dividents, interest on deposits,etc which are non operational revenue.Does these also should be considered under Operational Revenue to calculate the Operational Income

2) If the Promoter has around 70-71% stake in an organization , what conclusions can be drawn from this.For Ex: NHPC

3)Is there any logic like if a company has zero Debt then we need to consider ROE and if a company has debt we need to consider ROCE.

4)What can be the cut off target for selection companies based on ROC and ROCE.

Kindly share your suggetion

Regards

Indranil Saha

1) I\’d prefer not to consider the other income to get a sense of the operating income

2) It is just that it has a high promoter holding – so more skin in the game, in a way this is good

3) Nope

4) Depends on the sector. You really need to look at the industry and take a call. One shoe does not fit all 🙂

How is amortization calculated on intangible assets. How can we reach out to the amortization amount deducted per year and the number of years in which it will be calculated? Thanks!

Depends on the company, they usually publish this in the amortization schedule made available in the annual report.

Hi Kartik,

Depreciation and armotisation expenses are divided equally for the whole life of the asset as is shown same each year but what about the time value of money.

Sorry, what about the time value? I dont seem to get your question.

Hey Karthik,

Thanks a lot for all the useful information published !

Just had a small doubt

What is exactly the deferred tax and short provisions tax?

Also, the taxation in companies would have changed right? Specially after some alterations made last year to the corporate tax.

So what all taxes are required to be paid at a company to arrive at the net profit figure?

Please do let me know

The deferred tax arises out based on the way depreciation is treated. The applicable tax is kept aside and provisioned for and paid the following year when there is more clarity.

And….

If depreciation and amortisation are non cash expenses…..

And it is shown as cash going out of the company or from profits…..

But where does it actually go….

To depreciation fund a/c???

But not all company created this a/c!

It gets adjusted over the useful life of the asset. For example, if a company buys something for 1Cr today, it won show 1Cr as expense today. It will only show a part of it every year.

Hi,

I was studying fundamental of delta corp Ltd…..

In that, even after showing PAT… there are some extra lines called \’Other Comprehensive income\’

And \’profit attributes\’… Etc etc….

Should we look in to it…???

Yes, do look at it, will be explained in the associated notes.

Sir

Purchases of stock in trade, refers to all the purchases of finished goods that the company buys towards conducting its business

From note 20 it is shown that they have bought batteries and ups

Does this means that they have bought ready to sell ups and batteries from outside.

No, these are products that they manufacture. This is stock moving from previous year inventory and getting recognised as a sale during this year.

Dear Karthik sir

i did research on it

actually i did wrong calculations

right is as follows

in yr ended march 31 2014 column

Net increase in inventories (294.42-223.16-363.36)= -292.10

while in another march 31 2013 column

Net increase in inventories ( 20.93-17.54-324.28)= -320.89

now both calculations are right actually i forgot to focus on negative value that\’s why this happened. but now i understood . Thanks again for this wonderful contents.

I\’m glad you could figure that 🙂 The annual report of good companies are usually very clear with their numbers.

Happy reading!

Dear Karthik Sir

I tried to find out every details of note 20, but i didn\’t get any regarding information. may be it was mistake or you suggest .

Ah, need to check this. I\’ll do as and when time permits.

Dear Karthik Sir

In Change in inventories of finished goods etc

in yr ended march 31 2014 column

Net increase in inventories ( 223.16+294.42-363.36)=154.22

how 292.10 is showing ?

while in another march 31 2013 column

Net increase in inventories ( 17.54+324.28-20.93)=320.89 this is right

Sir can you please explain the difference showed in first column

You need to inspect the associated notes in the annual report for this where a detailed explanation would be given

Hi Karthik,

I want you to know there are some questions in the varsity app quiz part that have wrong answers. I\’ll try making a list. For example, Fundamentals intermediate quiz question 9.

Thanks Robin, as and we get any feedback, we update the app.

Sir,

Many of the services based companies(IT) I do not see COGS or Cost of services then how would i calculate Gross Profit which is revenue minus COGS* . As i see in many US companies balance sheet i see either COGS or cost of services or in similar lines according to industry*. I asked many they confused me, Can you please elaborate on the same.

for example HDFC AMC : how to calculate gross Profit can you explain and generalize how to calculate for any indian company?

Revenue from Operations

Asset Management Services – 1,915.18

Other Income – 181.60

Total Income 2,096.78

Expenses

Fees and Commission Expenses 240.26

Impairment on Financial Instruments 22

Employee Benefits Expenses – 206.27

Depreciation, Amortisation and Impairment – 12.85

Other Expenses 222.70

Total Expenses 722.08

Profit Before Tax 1,374.70

Tax Expense

Current Tax 445.47

Deferred Tax (1.37)

Profit After Tax 930.60

Its simple Pradeep, everything that company mentions as an expense is the COGS or COS. That\’s it.

I did not understand purchase of stock in trade and it cycle.

Can u please tell me in detail or reffer any website or artical so that i can understand it fully.

Thanks

Karan, do read the associated notes once.

Hi Karthik,

Thank you for a enlightening chapters.

I was going through other company P&L statement where I came across these terms. what do these mean Would you please explain?

Other comprehensive income/(loss)

A. (i) Items that will not be reclassified to profit or loss

(a) Remeasurements of the defined benefit plans.

(b) Equity instruments through other comprehensive income.

(ii) Income tax relating to items that will not be reclassified to profit or loss.

B. (i) Items that will be reclassified to profit or loss

(a) Debt instruments through other comprehensive income…

(b) Effective portion of gains and loss on designated portion of hedging

instruments in a cash flow hedge…..

(ii) Income tax relating to items that will be reclassified to profit or loss…………………….

I\’m guessing here, please refer to the associated notes for full clarity –

A (i) – Both could be something related to the market-linked product, so taking M2M into consideration

A (ii) – Deferred tax income

B (i and ii) – Same as A

Thank you sir and waiting for financial modelling course. Hope to see it soon..

Appreciate your work.. Keep learning and keep teaching..

Happy reading, Arjun 🙂

Sir if change in inventories, work in progree, finished goods is positive.. Then should we include that in cost of good sold..?

Ah not really. It\’s best to include the actual costs incurred.

\”how much the company is earning per face value of the ordinary share\”

what per face value means regarding EPS?

like if EPS is ₹20 and face value of share is ₹5, then does it mean that company has earned ₹20 on ₹5?

EPS is earning per share. Suppose earning is 100 and the number of shares is 20, then earning per share is 100/20 = 5

Sir are the batteries and home UPS purchased as part of stock in trade a trading business of amara raja batteries ? If yes, why do they undertake the manufacturing and trading of the same item ?

Hello Karthik Sir,

In the above P&L study in the lesson,

The company indicates that there are 17,08,12,500 shares outstanding in the market

How can one calculate the outstanding shares. Is it like, the number of shares in the stock market for the company on 31st March?

Kindly clarify

Continue caring and enlightening people like me

Regards

Yup, shares outstanding in the market indicates the shares which are available to trade in the market.

Great work. Thank you. When will you publish module on Financial Modeling as mentioned by you in Part 2 of PL statement?

Trying to do some work around it, Rahu.

1. Sir I would like to know that what does it suggest about a company whose profit has increased more than 50% from last year just because it’s change in finished goods /inventories/wip has changed from +50lakhs (last year) to —1701laks(current year) .

2. Since you said negative sign shows the extra products company didn’t sell but has produced so a sudden shift from +50 to -1701 shows the company’s INABILITY to sell its products .

3. This sudden increase of 50% in profit before tax of current year is not a good sign if this profit is caused only due to a sudden shift in the change in inventory/wip/finished good from +50lakh(last year) to —1701lakhs (current year) .

1) This probably shows an inventory pile up

2) Yes, inventory pile-up is not a great sign. Indicates that the product is not moving, perhaps the consumer\’s preferences are changing.

3) Yes, I\’d agree.

Hi Sir,

How to find COGS of an IT Company, as unlike Amara Raja, there are no goods manufactured here?

COGS is equivalent to the expense incurred. This will mainly be the HR expenses for an IT company.

Hi

Yes it\’s consolidate data both side

Perhaps the deferred tax got added back?

Hi sir

In p/l statement and cash flow from operation statement tax paid figure is different .why ? No clarifiaction about it in its associated footnotes and I saw data in its annual reports of so many company.

Hmm, it should not differ. Are you sure you are comparing the consolidated data across both the statements?

Hello sir, first of all thanks for your such contribution to enhance our financial knowledge.

My doubt is under 5.2 topic you defined PBT which is equal to Total operating revenue – Total operating expenses.

I want to ask why Total operating expense?? It should be Total expenses because other expense are also taxable.

Manish, the idea is to find out the profitability at the operating level for the company. Other expense could be one-off and may not reoccur.

Thank you for your reply sir.

I want to clarify about few more things:

a) Under Expenses the total expenses is Rs 29,416.19 millions but if I calculate it reflects 30000.39 millions.

b) Under extract of Note-20 (a) – total purchase of stock in trade is Rs 2113.69 millions,does it mean company buys goods worth Rs 2113.69 millions from last F/Y i.e. 2013????

c) Under the same extract of Note-20 the change in inventories of finished goods,work in process & stock in trade. I understood about how the individual figures comes from but unable to understand the Net increase in inventories figure which is 292.10 million.

d) Under topic 5.2 in which you describes the PBT= Total revenue – total Operating expenses but you take the figures of total expenses.

Sir my theses doubts may be silly doubts for you but it makes huge sense for me. Please help Sir.

a) This can be a case of minor debit and credit, I would suggest you look at the notes associated with the expenses for a more granular view

b & c) Frankly, I need to review these numbers, it has been a while now 🙂

d) PBT if you want to calculate from an operations point of view, then its Total Operating revenue – operating expense – D&A

Hi Karthik.. I am in a confusion..about purchases of stock in trade and change in inventories. From the topic u have given I came to know that… 1.if the company sells less than the goods manufactured..the cost incurred for the extra manufactured goods will be taken in the column of change in inventories with negative sign. And the same amount will be added up in the next year\’s purchases of stock in trade column of next year\’s statement..am I right???

Thats right, Sai. The expenses are recognized in the next year.

If same thing happens in a quarter does the expenses will be recorded in the next quarter??

All balance sheet items are at the end of the year basis, P&L is on a Q on Q basis.

1.what is meant by the positive number of change in inventories.column.. As u told negative means goods are sold less than manufactured so the extra goods manufactured cost will be shown with negative sign and same amount is added up in purchase of stock in trade in next year\’s statement. as u confirmed by sending ur reply to my previous question… So positive number of change in inventories means last year\’s unsold goods are sold this time r8.the cost incurred for them to manufacture will be added in this r8.

If so what will be added in the next year\’s column of purchase of stock in trade..

2.if zero in changes in inventories what does it mean.

1) This will depend on the way inventory moves, right?

2) Then status quo

Hi Karthik.. Kindly answer to my queries.. Thank u very much for ur support. My query Is where this 2113.69 million in the purchase of stock in trade has came from.?

This is unsold inventory, I guess I replied to your query earlier.

1.why the (pusrchase of stock in trade) unsold inventory cost is put up in the expenses column. of this year..it would become a balance sheet item r8..if not sold….

2.how to know the calculation of it in the above 2113 millions which is given right there in the column..

1) The balance sheet is on a carry basis, whereas P&L is year on year basis.

2) You can refer to the notes associated with the line item.

Sir, can cost of raw material consumed be negative. And if it is so,what does it imply?

No, how would the be possible?

Thanks a lot for your thorough teaching. But could you please explain more about the Purchases of Stock in Trade and Changes in inventory of finished goods, WIP and stock in trade? I\’m still very confused with all these terms, and the reason this concept represents the cost of goods sale.

I\’ll try and put up a supplementary note on this.

Thank you so much for explaining this complex subject into easy to understand language ,

Happy learning, Subeer!

Sir, when is the module for financial modeling is getting started?

Pinak, I\’m working on another project related to Varsity. Will look at this module once the project takes some shape.

Thank you Sir for replying. I am eagerly waiting for the module to get started as you have a great talent to explain these complicated things in a very easier way. I appreciate your effort. Best of Luck for the Project !!!

Thanks, Pinak. Hope you will like the new project as well 🙂

Certain clarification to look into. The Chairman of ARBL gave a statement predicting or foreseeing 10% growth which can be assumed to be a bluff on his part and so the analyst decided to not invest in it. However, the EPS figures of the said company look relatively attractive. Under such circumstances how can a decision be made? and with what level of certainty?

This was not a conflict with ARBL if I\’m wrong. I think this was the case with TGBL. Can you please reconfirm? Thanks.

Yes you are right. I missed the point as it came in between the discussion about ARBL. It would be helpful if you mention the name there or insert coloured font or atleast highlight the tea manufacturing company part if you do not wish to reveal the name.

One example that I explicitly remember was reading through the chairman’s message of a well established \”tea manufacturing company\” (double quotes inserted to highlight in this case for your kind reference, the same are missing in the article \”https://zerodha.com/varsity/chapter/read-annual-report-company/\”).

Thanks again for responding. It verifies the assumption that company with higher EPS can be trusted.

Point noted, will include this 🙂

Thanks for responding. This initiative of varsity must have saved tons of users from getting bankrupt. It is very very helpful. God bless everyone at zerodha. keep up the good work!!!

Thanks for the kind words 🙂

Happy learning!

Sir,

Don\’t this Company have any expenses towards loan repayments? Also the Interest to be paid for the loans. Where do we account these items?

Hari Narayanan

I suppose, it is the finance cost. Sorry for bothering you.

Not an issue. Happy learning!

As far as I recollect, the company had very little loan outstanding, hence very small finance charges.

\”Perhaps it is time for you to rethink about that entrepreneurial dream you may have nurtured\” Can you pl explain it.

Well, its just a motivational line, drawing inspiration from the balance sheet 🙂

Does a large no. of exceptional items too drag a red flag?

Of course, it would.

Thanks.

Hi Karthik,

While you were explaining Purchases in trade, one question came in my mind what if a company never manage to sell some goods? So when would they add the cost of that goods?

Yes, also it will start showing up in the P&L.

Thanks

Hey Karthik,

What is EPS for continued and discontenued operations?

oops sorry posted it double

It means EPS for a business which is functional and non-functional.

Sorry couldnt understand that.

Ram, actually, even I\’m not sure 🙂

Hi Karthik,

What are you a trader or a investor?

I occasionally trade and I regularly invest.

That was a great answer

By the way Thanks.

Thanks, Ram. Thats exactly what I do 🙂

Hey Karthik,

What is EPS for continued and discontenued operations?

Not sure, need to check this myself.

Hi sir

Can u suggest me some ration for insurance company?

Sorry, I\’m unable to understand that.

Hello Sir

Could you please help in explaining these points:

1. Why Excise Ta is not included in the Expense Section, rather than Totals Sales first reduced by this amount and then shown in Revenue section

2. Does the closing inventory goes like Current Asset in balance sheet ?

3. What is meant by Basic and Diluted keywords in shares.

Thanks a lot for your help.

Regards

Dan

1) Excise duty is applicable to manufacturing, hence. By the way, I suspect this must have changed with GST in place. I need to check this too

2) Yes

3) Basic and Diluted are used in terms of EPS. Basic does not factor in any convertible shares, but diluted does.

Thank you !

Welcome!

sir,

Question of EPS Viz a Viz \”Face Value \” of Share

Assume there are TWO Companies A and B

1) A has an EPS of 8 and Share \”Face Value \” is 1

2) B also has an EPS of 8 BUT Share \”Face Value\” is 10.

so, sir….. which company should be considered as having BETTER EARNING Capacity. ??????

and what is the REASONING to be used ???

THANKING YOU

I\’ll assume both the companies are comparable in the first place i.e same industry, similar in size. If true, then company B obviously is better. Also, please note, the face value of the share does not really matter here.

sir,

This is in reply to your answer,

My Reasoning was that

In case of company A if they have split up the share from a FACE VALUE of 10 to 1.

Then can we reason that

\”\” INSPITE OF \”\”TEN TIMES \”\” more SHARES NOW…..THIS COMPANY \”A\” is able to GENERATE an EPS of 8

HENCE…….,COMPANY \”A \” should be considered as more profitable.

( You can ASSUME both company from same industry…both offering \”STAND ALONE \” Quarterely results.

please confirm OR share your views

I feel this point will help many investors n traders

thank you

The face value matters in terms of calculating the number of shares outstanding in the market. Yes, in a sense it does make sense because we get to know the extent of dilution. Now, it really boils down to which financial ratio you are looking at. Based on that you may just want to consider the face value as well.

Sir – If the Depreciation value alone is shown from P&L while the total asset value is going out of company, how will the cash balance match ?

Senthil.

I guess you are talking about cash proceeds from the sale of assets. The cash will reflect in other income.

Sir – My concern is of during purchase of say a machinery for rs.10000 and as you mentioned P&L only reflects the depreciating value say rs.2000 per year…

In this case money going out of the company is rs. 10000 wherein we are showing only rs.2000 so wouldn\’t the balance differ..?

No, in such a case the asset would be written off and hence no depreciation charges against this.

Sir , Excellent and fundamentals are explained in very simple manner.it can be understood for beginner to expert level. Thank you very much for sharing this knowledge for free of cost. I really appreciate

Happy learning, Suresh.

Sir, have you posted pdf on financial modelling? thanks

No, have not created that module yet.

Hi Karthik,

Thanks for this wonderful article.

I fondly remember of me searching for some kind of this material since 2010 – a long wait put to an end.

I have got few questions related to Note 20(b)

Q1 – Work-in-progress section:

Why is the OS-CS not shown as negative in the note? 828.95-1052.11 should give us -223.16. However, it was shown as positive.

Finished-Goods Section:

Same question as above, why not -ve while the company sold lesser no.of stocks than they manufactured.

Q2 – Net increase in inventories:

How did 292.10 arrived?

Thanks in advance.

Sunil, it is in -223.16. Shown as -ve.

Net Inventory is the sum of OS, FG, and stock in trade.

Is it good to look at quarterly/annual reports of the company or reports from top brokerage houses will do the needful?

I\’d advise you look at the AR to avoid any sort of biases in your judgment of the business.

What does increase/ decrease in stock mean? Also can can pl again explain meaning of purchase of traded goods.

Tejas, have explained this couple of times in the comments above. Can you kindly run through it once? Thanks.

if i add all the item from expenses (i.e 21011.95+2113.69+292.10+1583.16+645.71+4346.60) then sum is coming 30,000.39 million rs but in statement it is shown 29,416.19 …. am i missing something hear …???

I guess you are, request you to please recheck. Do refer to the schedule as well.

I had a concept of depreciation as \’decresase in the value of an item\’ which is opposite/different to what you explained about depreciation!

I need to ask…….

1. Does \’depreciation\’ not mean \’decrease in the value of an item\’?

2. If it also mean decrease in the value of an item, then what difference is there between inflation and depreciation?

1) It roughly means the same – decrease the value systematically over a period of time

2) Inflation is a steady increase in price.

Depreciation is an accounting concept, inflation, on the other hand, is an economic concept.

Highlighted excerpt:

\”Here is something for you to think about – A company generating Rs.3482 Crs is spending only Rs.158 Crs or just 4.5% of its sales on its employees. In fact this is the pattern across most of companies (at least non IT). Perhaps it is time for you to rethink about that entrepreneurial dream you may have nurtured.\”

It was very astonishing to come to know this fact !!

It\’s also a daring, eye opener and guiding fact unravelled.

Entrepreneurs out there may take a cue from this.

Keep unravelling Sir !

You bet! The stories are always hidden deep in the numbers 🙂

Hi Karthik,

I have a query related to EPS. As we know, EPS is the PBT divided by no of shares.

Due to various corporate activities like stock split, bonus, buyback, the no of shares change (increase/decrease). in this case how will be the EPS for the previous year be calculated – using the new on of shares or the old no of shares corresponding to that period?

For example, let’s say the PBT for a company XYZ for yr2017 was 100cr and no of shares 20cr, so EPS in the year 207 was=100/20=5.

now in 2018, the company declared 1:1 bonus. So, the no of shares now 40cr. The PBT for this year is 120cr. EPS for this year=120/40=3

What will be the EPS for 2017 now?

will it be same as last year i.e. 5?

or

with new on of shares, 100/40=2.5

The reason I am asking this is we have to compare the historical data. So, if I compare 5 with 3, its showing negative growth whereas if I compare 2.5 with 3, it shows positive growth.

Please clarify.

a small correction. Its PAT not PBT.

Figured as much 🙂

Valid question, Jyoti. Corporate action is something that you need to consider carefully, for this reason, it makes sense to look at this on an as-is basis. When you analyze, be aware of this and do not make an adjustment to the previous years\’ data. Btw, do seek a 2nd opinion on this. Kindly share your learnings here.

Hello team,

i want to ask that form which side this snapshots of the income statement is taken?????

Sorry Kunal, I\’m not sure what you are asking about. Can you please elaborate this? Thanks.

The paragraphs above Employee benefits expenses in Section 5.1 says \’Financial Modelling\’ as a seperate module. Can you point out the module from the chapters in Varsity?

We have not developed that yet, maybe sometime during this year.

Hey,

I was reading this

http://www.shekhawatiyarn.com/images/SHEKHAWATI%20POLY-YARN%20LIMITED_31.12.15.pdf

The fifth note says:

\”During the quarter the company has reversed quantity discounts which was receivable from various suppliers pertaining to earlier years amounting to Rs. 6,564.36 lacs which are no more recoverable. Accordingly, the said amount has been written off and included under exceptional items.\”

Can you help me understand this?

Thanks!!

Clearly, the company is writing off receivables from the previous years. Not a great sign according to me.

Karthik,

How numerator of EPS is calculated?

Sorry for this naive doubt. It is PAT as mentioned in takeaway points.

Does Zerodha as a company does have done any CSR project till date? Where to know if yes?

Yes, we do. Some of it is here – https://zerodha.com/cares

I work as volunteers in an NGO, along with i am ZLM parnter, So just an idea stuck in my mind, as a fastest growing company Zerodha will also love there work, may be you would you like to support? Where we can connect for ZERODHA CSR contact person?

Hello sir

What is CSR expenditures?

Every company of a certain size spends upto 2% of its profits on social service. This is called Corporate Social Responsibility or CSR.

Thanks a lot Mr. Karthik for replying of all my queries.And soon i will disturb u again in future.

Please do!

Hi karthik

As I was looking the annual reports of jsw energy pvt ltd 2017 and 2016.The EPs of 2016 is different in 2017 annual report.And its quite a big difference.so isn\’t it misleading? There is changes in revenue and expenditure too. Why this happens?And which one I should take into my consideration?

Thanks

Maybe the numbers were restated? Take the 2017 AR numbers.

And sir

Can u recommend me any govt of India website,so by reading the statistics I might get to know the which sector indian govt is boosting up?

You will have to keep a tab on the news and reforms for this. Not sure if there is a website for this.

Hi karthik

Sorry to disturb u again!

Please guide on other comprehensive income?

What\’s that?

Other income includes non-operating revenue such as rent, interest, dividends, and sale of assets.

But sir

Here I am looking something different in this annual report of jsw energy Ltd

Other comprehensive income

(i) Items that will not be reclassified to profit or loss

– Remeasurements of the net defined benefit

liabilities / (assets)

(ii) Income tax relating to items that will not be reclassified

to profit or loss

I\’d suggest you look into the notes, Aashish. There will be an explanation for this.

Hey karthik

What is outstanding shares? Is it Authorized,issues or subscribed? Which one?

Issued shares.

Hey karthik

Thanks for teaching us

How do we calculate weighted average no. Of shares?

That would be –

Sum of – Number of shares * Trader Price / Total Volume.

Can u give me example on it?

Coincidently, I just gave an example earlier in the day – https://zerodha.com/varsity/comment/49095/