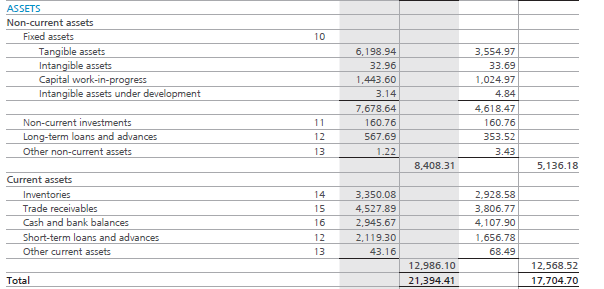

7.1 – The Assets side of Balance Sheet

In the previous chapter, we looked at the liability side of the balance sheet in detail. We will now understand the 2nd half of the balance sheet, i.e. the Asset side of the balance sheet. The Asset side shows us all the company’s assets (in different forms) right from its inception. Assets in simple terms are the resources held by a company, which help in generating the revenues. Here is the snapshot of the Assets side of the balance sheet:

As you can see, the Asset side has two main sections, i.e. Non-current assets and Current assets. Both these sections have several line items (with associated notes) included within. We will look into each one of these line items.

7.2 – Non-current assets (Fixed Assets)

Similar to what we learnt in the previous chapter, non-current assets talk about the company’s assets, the economic benefit of which is enjoyed over a long period (beyond 365 days). Remember, an asset owned by a company is expected to give the company an economic benefit over its useful life.

If you notice within the non-current assets, there is a subsection called “Fixed Assets” with many line items under it. Fixed assets are assets (both tangible and intangible) that the company owns, which cannot be converted to cash easily or which cannot be liquidated easily. Typical examples of fixed assets are land, plant and machinery, vehicles, building etc. Intangible assets are also considered fixed assets because they benefit companies over a long period of time. If you see, all the line items within fixed assets have a common note, numbered 10, which we will explore in great detail shortly.

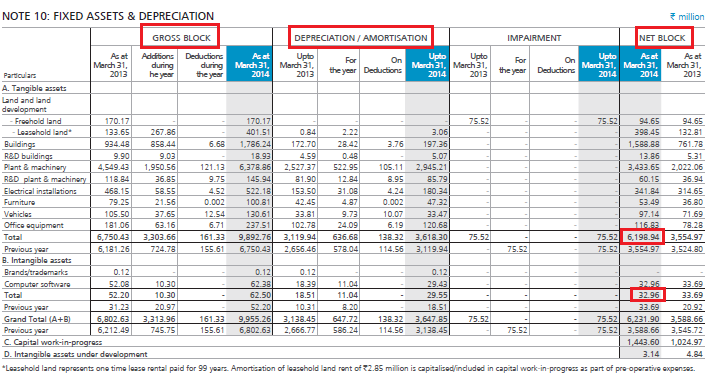

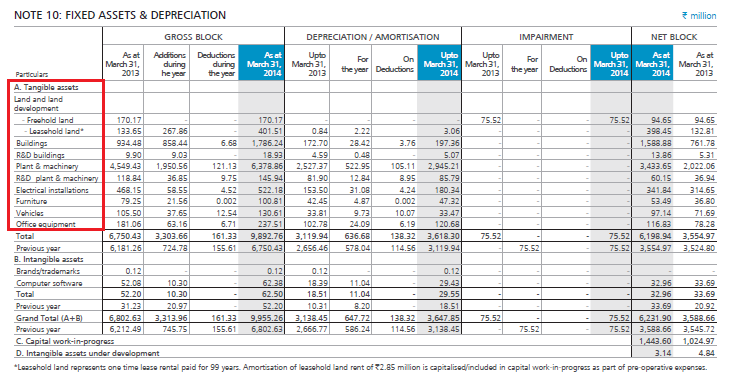

Here is the snapshot of fixed assets of Amara Raja Batteries Limited:

The first line item ‘Tangible Assets’ is valued at Rs.619.8Crs. Tangible assets consist of assets which have a physical form. In other words, these assets can be seen or touched. This usually includes plant and machinery, vehicles, buildings, fixtures etc.

Likewise, the next line item reports the value of Intangible assets valued at Rs.3.2 Crs. Intangible assets are assets which have an economic value but do not have a physical nature. This usually includes patents, copyrights, trademarks, designs etc.

Remember, when we discussed the P&L statement we discussed depreciation. Depreciation is a way of spreading the cost of acquiring the asset over its useful life. The value of the assets depletes over time, as the assets lose their production capacity due to obsolescence and physical wear and tear. This value is called the Depreciation expense, shown in the Profit and Loss Account and the Balance Sheet.

All the assets should be depreciated over its useful life. Keeping this in perspective, when the company acquires an asset, it is called the ‘Gross Block’. Depreciation should be deducted from the Gross block, after which we can arrive at the ‘Net Block’.

Net Block = Gross Block –Accumulated Depreciation

Note, the term ‘Accumulated’ is used to indicate all the depreciation value since its incorporation.

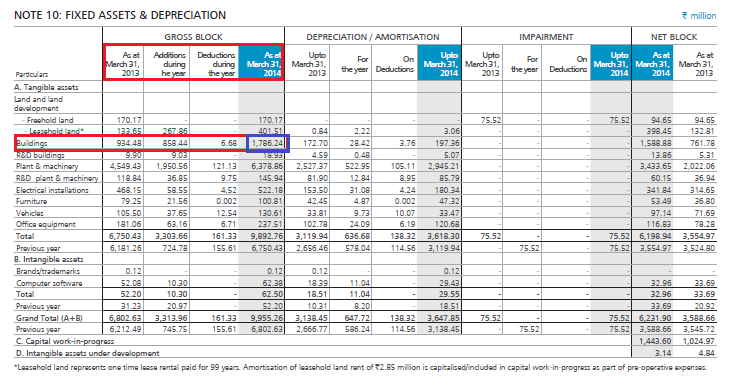

When we read tangible assets at Rs.619.8 Crs and Intangible assets at Rs.3.2 Crs, remember the company is reporting its Net block, which is Net of Accumulated depreciation. Have a look at Note 10, which is associated with fixed assets.

At the top of the note, you can see the Gross Block, Depreciation/amortization, and a Net block is highlighted. I have also highlighted two netblock numbers which tally with what was mentioned in the balance sheet.

Let us look at a few more interesting aspects of this note. Notice under Tangible assets you can see the list of all the assets the company owns.

For example, the company has listed ‘Buildings’ as one of its tangible assets. I have highlighted this part:-

As of 31st March 2013 (FY13), ARBL reported the building’s value at Rs.93.4 Crs. During the FY14 the company added Rs.85.8Crs worth of building, this amount is classified as ‘additions during the year’. Further, they also wound up 0.668 Crs worth of building; this amount is classified as ‘deductions during the year’. Hence the current year value of the building would be:

Previous year’s value of building + addition during this year – deduction during the year

93.4 + 85.8 – 0.668

= 178.5Crs

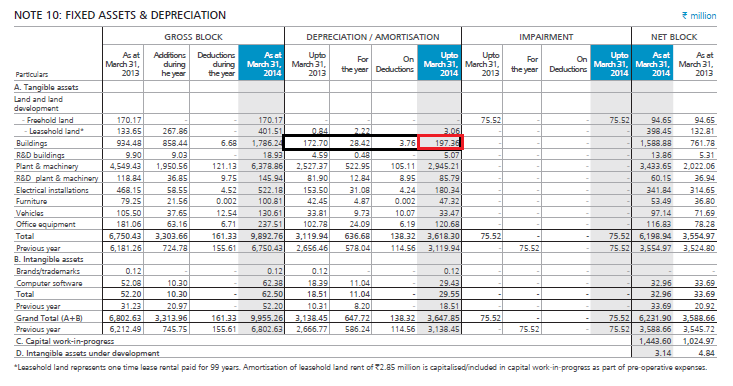

You can notice this number is highlighted in blue in the above image. Do remember this is the gross block of the building. One needs to deduct the accumulated depreciation from the gross block to arrive at the ‘Net Block’. In the snapshot below, I have highlighted the depreciation section belonging to the ‘Building’.

As of 31st March 2013 (FY13), ARBL has depreciated Rs.17.2 Crs, to which they need to add Rs.2.8 Crs belonging to the year FY14, adjust 0.376 Crs as the deduction for the year. Thus, the Total Depreciation for the year is:-

Previous year’s depreciation value + Current year’s depreciation – deduction for the year

= 17.2 + 2.8 – 0.376

Total Depreciation= Rs.19.736 Crs. This is highlighted in red in the image above.

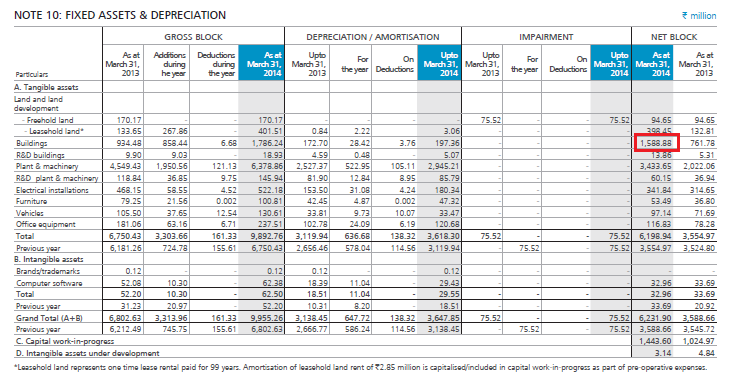

So, we have to build gross block at Rs.178.6 Crs and depreciation at Rs.19.73 Crs which gives us a netblock of Rs.158.8 Crs ( 178.6– 19.73). The same has been highlighted in the image below:

The same exercise is carried out for all the other tangible and intangible assets to arrive at the Total Net block number.

The next two line items under the fixed assets are Capital work in progress (CWIP) and Intangible assets under development.

CWIP includes building under construction, machinery under assembly etc. at the time of preparing the balance sheet. Hence it is aptly called the “Capital Work in Progress”. This amount is usually mentioned in the Net block section. CWIP is the work that is not yet complete but where capital expenditure has already been incurred. As we can see, ARBL has Rs.144.3 Crs under CWIP. Once the construction process is done, and the asset is put to use, the asset is moved to tangible assets (under fixed assets) from CWIP.

The last line item is ‘Intangible assets under development’. This is similar to CWIP but for intangible assets. The work in the process could be patent filing, copyright filing, brand development etc. This is at a minuscule cost of 0.3 Crs for ARBL. All these costs are added to arrive at the total fixed cost of the company.

7.3 – Non-current assets (Other line items)

Besides the fixed assets under the non-current assets, there are other line items as well. Here is a snapshot of the same:

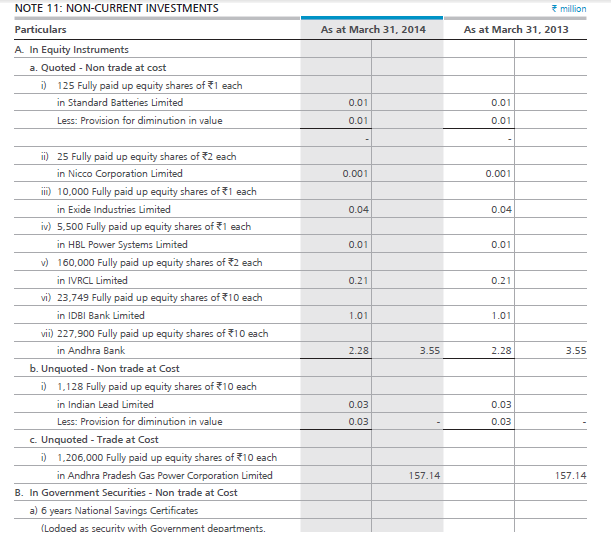

Non-current investments are investments made by ARBL with a long term perspective. This stands at Rs.16.07 Crs. The investment could be anything – buying listed equity shares, minority stake in other companies, debentures, mutual funds etc. Here is the partial (as I could not fit the entire image) snapshot of Note 11. This should give you a perspective.

The next line item is long term loans and advances which stand at Rs.56.7Crs. These are loans and advances given out by the company to other group companies, employees, suppliers, vendors etc.

The last line item under the Non-current assets is ‘Other Non-current assets’ which is at Rs. 0.122 Crs. This includes other miscellaneous long term assets.

7.4 – Current assets

Current assets are assets that can be easily converted to cash, and the company foresees a situation of consuming these assets within 365 days. Current assets are the assets that a company uses to fund its day to day operations and ongoing expenses.

The most common current assets are cash and cash equivalents, inventories, receivables, short term loans and advances and sundry debtors.

Here is the snapshot of the current assets of ARBL:

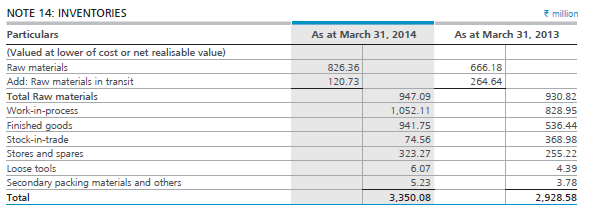

The first line item on the Current assets is Inventory which stands at Rs.335.0 Crs. Inventory includes all the finished goods manufactured by the company, raw materials in stock, goods that are manufactured incompletely etc. Inventories are goods at various stages of production and hence have not been sold. When any product is manufactured in a company, it goes through various raw material processes to work in progress to finished good. Snapshot of Note 14 associated with the inventory of the company is as shown below:

As you can see, a bulk of the inventory value comes from ‘Raw material’ and ‘Work-in-progress’.

The next line item is ‘Trade Receivables’ also referred to as ‘Accounts Receivables’. This represents the amount of money that the company is expected to receive from its distributors, customers and other related parties. The trade receivable for ARBL stands at Rs.452.7 Crs.

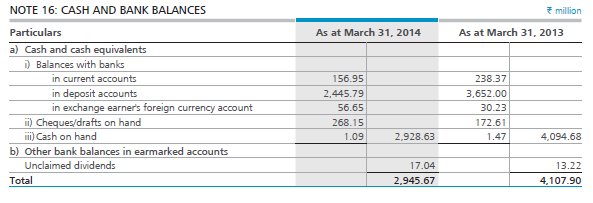

The next line item is the Cash and Cash equivalents, which are considered the most liquid assets found in any company’s Balance sheet. Cash comprises of cash on hand and cash on demand. Cash equivalents are short term, highly liquid investments with a maturity date of fewer than three months from its acquisition date. This stands at Rs.294.5 Crs. Note 16 associated with Cash and bank balances is as shown below. As you can see, the company has cash parked in various types of accounts.

The next line item is short-term loans and advances that the company has tendered and is expected to be repaid to the company within 365 days. It includes various items such as advances to suppliers, loans to customers, loans to employees, advance tax payments (income tax, wealth tax) etc. This stands at Rs.211.9 Crs. Following this is the last line item on the Assets side and on the Balance sheet itself. This is the ‘Other current assets’ which are not considered important, hence termed ‘Other’. This stands at Rs.4.3 Crs.

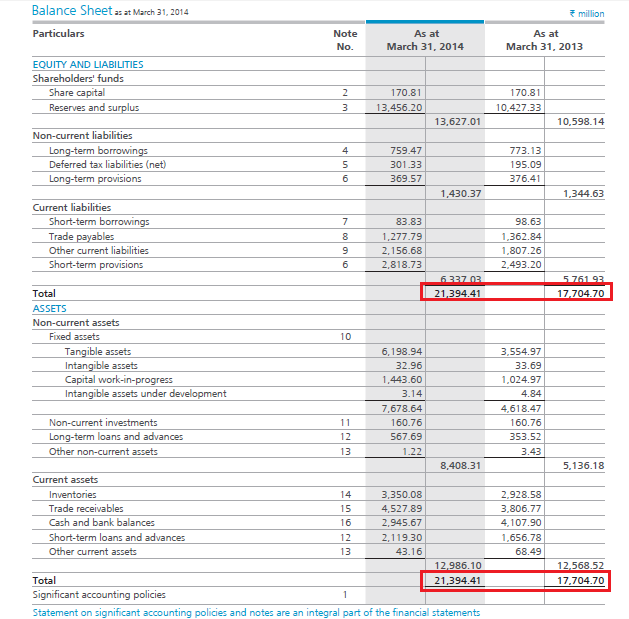

To sum up, the Total Assets of the company would now be:-

Fixed Assets + Current Assets

= Rs.840.831 Crs + Rs.1298.61 Crs

= Rs. 2139.441 Crs, which is exactly equal to the liabilities of the company.

With this, we have now run through the Balance sheet’s entire Assets side, and in fact the whole of Balance sheet itself. Let us relook at the balance sheet in its entirety:

As you can see in the above, the balance sheet equation holds for ARBL’s balance sheet,

Asset = Shareholders’ Funds + Liabilities

Do remember, over the last few chapters we have only inspected the balance sheet and the P&L statements. However, we have not analyzed the data to infer if the numbers are good or bad. We will do the same when we look into the financial ratio analysis chapter.

The next chapter will look into the last financial statement, which is the cash flow statement. However, before we conclude this chapter, we must look into the many ways the Balance sheet and the P&L statement are interconnected.

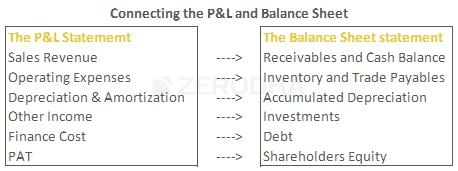

7.5 – Connecting the P&L and Balance Sheet

Let us now focus on the Balance Sheet and the P&L statement and the multiple ways they are connected (or affect) to each other.

Have a look at the following image:

In the image above, we have the line items on a typical standard P&L statement on the left-hand side. Corresponding to that on the right-hand side, we have some of the standard Balance Sheet items. From the previous chapters, you already know what each of these line items means. However, we will now understand how the P&L and Balance Sheet line items are connected.

To begin with, consider the Revenue from Sales. When a company makes a sale, it incurs expenses. For example, if the company undertakes an advertisement campaign to spread awareness about its products, the company has to spend cash on the campaign. The money spent tends to decrease the cash balance. If the company makes a sale on credit, the Receivables (Accounts Receivables) go higher.

Operating expenses include the purchase of raw material, finished goods and other similar expenses. When a company incurs these expenses, to manufacture goods, two things happen. If the purchase is on credit (which invariably is), then the Trade payables (accounts payable) go higher. Two, the Inventory level also gets affected. Whether the inventory value is high or low, depends on how much time the company needs to sell its products.

When companies purchase Tangible assets or invest in Brand building exercises (Intangible assets), the company spreads the asset’s purchase value over the asset’s economic useful life. This tends to increase the depreciation mentioned in the Balance sheet. Do remember the Balance sheet is prepared on a flow basis. Hence the Depreciation in the balance sheet is accumulated year on year. Please note, Depreciation in the Balance sheet is referred to as the Accumulated depreciation.

Other income includes monies received in interest income, sale of subsidiary companies, rental income etc. Hence, when companies undertake investment activities, other incomes tend to get affected.

When the company undertakes Debt (it could be short term or long term), the company obviously spends money towards financing the debt. The money that goes towards financing the debt is called the Finance Cost/Borrowing Cost. Hence, when debt increases the finance cost also increases and vice versa.

Finally, as you may recall the Profit after tax (PAT) adds to the company’s surplus, which is a part of the Shareholders equity.

Key takeaways from this chapter

- The Assets side of the Balance sheet displays all the assets the company owns

- Assets are expected to give an economic benefit during its useful life.

- Assets are classified as Non-current and Current asset.

- The useful life of Non-current assets is expected to last beyond 365 days or 12 months.

- Current assets are expected to pay off within 365 days or 12 months.

- Assets inclusive of depreciation are called the ‘Gross Block.’

- Net Block = Gross Block – Accumulated Depreciation

- The sum of all assets should equal the sum of all liabilities. Only then the Balance sheet is said to have balanced.

- The Balance sheet and P&L statement are inseparable. They are connected in many ways.

Hello Sir,

I have a very basic question.If a company buys an asset (let’s say a PC), then according to accounting terms, we show the cost through depreciation. However, in real life, the full amount is paid upfront for that PC.

So, where can I see the total cash outflow for that purchase in the financial statements?

and Doesn’t this also affect the balance sheet?

For this, you need to look at the cash flow statement.

Hi Karthik, Good Work on the content. I have doubt, in my company the profits are generated year on year. I move them to reserves and surplus. How will my Assets gets adjusted to show Assets = Liabilities + Equity + Reserves, eventhough there are no actual growth in the assets for past few years.

hmm, if the profits increase, something on the assets side is also increasing. Else it wont get balanced. For example Profits from P&L goes to reserves on the liabilities side, and cash balance on assets increase.

Thanks Karthik…

Happy learning!

HI sir,

As I have understood deprecation has been done three times, once in Gross Block and twice in Deprecation collum, also in P&L statement.

can you please explain this.

thank you.

They all have different accounting treatment, Ali. The one is Balance Sheet is year on year, while the one in P&L is for the given year.

How to know whether networth of company is positive or negative

Thanks

Check the balance sheet please 🙂

1. I\’m thinking of investing 500 into the INVESCO QQQ, what are your

thoughts on that?

2. How should I find the next coca cola?

Thank you

1) I dont track that, so cant really give an opinion. But I\’m guessing you cant go wrong with it 🙂

2) Research, observation, and generally looking at the world through an investor\’s lens 🙂

Thank you for the quick response. Of course, I understand your point.

I have a quick question: If you were my age and wanted to invest 1000$ into the stock market, what advice would you have loved to receive? How would you have split your money? Would you have bought ETFs and played it safe or would you have liked to take the risk, put in the time and tried to find the next Coca Cola as Warren Buffet did in the company\’s early stages. I hope you can understand what I\’m confused about and give me advice, considering the amount of financial responsibilities I have. (which is pretty much nothing as I\’m still going to school and live with my parents obviously).

Since you are young, perhaps you can take the risk with dabbling with stocks 🙂 Why not split your funds in two portions –

1) Buy an ETF, no brainier this one.

2) Go find the next Coca Cola.

Hello Karthik Sir,

I am about to turn 17 soon and am curently living in Europe. I just did a summer job and earned my first 1000 dollars which I am now planning to invest into stocks. I know that it is not such a big amount but that is all I have. I came across your website and want to tell and ask you a few things.

I think you have created a wonderful website where you have explained a lot of things pretty clearly, so thank you for that.

And I find it extremely impressive that you have taken so much time to answer every single question that people have asked here. And the fact that this information if for free without ads is amazing.

I realised that your written chapters are much more thoroughly explained than your video modules. Can you please explain the topics on a similar deep level in the videos, as well?

Thank you once again!

Thanks for the kind words, Prakhar. $1000 is quite a bit at 17, I hope it grows manifolds over the years 🙂

Cant really compare writing to videos. I can take as much time to write and delivery all nuances, but videos has a high cost both in terms of $$ and the attention span. So kind of forced to keep them short and touch upon the highlights.

But feedback noted. Will try and cover as many nuances as possible going forward.

If i buy a share and hold till record date, and after record date, i sell the share, would i be eligible for their corporate action, i.e. dividends, bonus issue, stock split, etc.

Yes, you\’d be eligible.

Hello Karthik

Could you please explain a bit about a line item called Right of use of assets in the non current asset\’s section?

Also is this line item considered in calculating the Gross block or no?

Ah, is this something to do with royalties and other intangible assets? I need to figure as well 🙂

Hi Karthik! Please explain further what this means

As of 31st March 2013 (FY13), ARBL has depreciated Rs.17.2 Crs, to which they need to add Rs.2.8 Crs belonging to the year FY14, adjust 0.376 Crs as the deduction for the year. Thus, the Total Depreciation for the year is:-

Previous year’s depreciation value + Current year’s depreciation – deduction for the year

= 17.2 + 2.8 – 0.376

Total Depreciation= Rs.19.736 Crs. This is highlighted in red in the image above.

What are the previous year and current year depriciation and what is deduction?

The depreciation stated in P&L is what we are refering to here. The previous year is referring to the previous year\’s depriciation, and current year is refering to the current financial year.

These two add up and gets stated in the balance sheet, if there is any mismatch, that gets treated as deduction.

Previous year’s depreciation value + Current year’s depreciation – deduction for the year

= 17.2 + 2.8 – 0.376

What is Deductions For The year in depreciation ? (In the formula you mentioned)

These are small difference that arise due to different treatment of depreciation.

Can I ask what is impairment in fixed assets and what means deductions for the year?

Got this defenition from the accounting (IND AS) website – An impairment loss is the amount by which the carrying amount of an asset or a cash-generating unit exceeds its recoverable amount. The recoverable amount of an asset or a cash-generating unit is the higher of its fair value less costs of disposal and its value in use.

When I saw the Balance sheet of \”Siemens Ltd\”,its Fixed assets are 1000cr in(i.e., consolidated format) but when I open that fixed assets plant missionary is almost 1277cr and building 444cr and land 37….my question is how fixed asset is showing 1000cr but deep down in that fixed assets row… those fixed assets are more than what they mentioned….how does that difference happened…?

You also need to factor in depreciation and amortization when looking at this.

How to analyse balance sheet of banks and what ratios are important while analysing the banking sector stocks

Anwit, we will soon put up a chapter explaining how one can analyze banks in detail. Please keep an eye on this here – https://zerodha.com/varsity/module/sector-analysis/

after reading this, I went to other companies\’ balance sheets where I found a right-of-use asset. What is the right of use asset?

Ah, I think the right of use of assets must be linked to royalties, etc. I need to do some research on this 🙂

Hello Karthik sir,

I really appreciate your work. Also, this comments section Q&A is helping a lot in consolidating my understanding.

Glad to note that, Sahil! Happy learning 🙂

When a company buys raw material it gets showed in both profit and loss(raw material consumed) and balance sheet (inventory) right?

Yeah, the raw material purchase is in expense, and yes, you can see that expense in P&L (Raw material consumed). In the Banalce sheet, you see the inventory (finished goods from raw material).

Many of my long term doubt has been cleared by your simple discussions.Conneting P&L statement with Balance Sheet was extremely difficult for me.Fundamental concepts of finance are required to understand the fundamental analysis. Your discussions helped me a lot.

Happy to be of help, Sudipta. Hope you continue to learn and benefit from Varsity 🙂

then assets get added to the assets side (not liabilities side), isn\’t it ?

Yes, thats right.

Hello Sir,

Suppose at present a company has a debt of 100 cr. and they are planning to clear this debt soon. Once it\’s clear, liability of the company gets reduced and hence asset (as debt has been paid from assets) too get reduced in same amount. So its satisfy the equation : asset = share equity + liability. Now my question is : if company takes a loan again in future let\’s say 150 cr…it means liability increased then what will get added in left (asset) side of the equation so that the asset becomes equal to the liability again. Thank you..

So assume the loan is for CAPEX, then assets get added to the liabilities side to equate the balance sheet.

hai sir, i have doubt that if company raises funds from ipo those funds will be in securities premium reserves in liability side and how this funds balance in assests side sir?

As well as for debt also?

It can be parked in current investments (on asset side), Srikanth.

Why are buying of equity shares by the company listed under Non-Current assets, when they can be easily converted into cash? Shouldn\’t they come under current assets?

But why convert a long-term liability or asset into short-term and let go of long-term benefits?

Sir, What are the conclusions that can be drawn from the difference that occurred during the year.. For e.g What does a increase in CWIP implies, and maybe a reduction in Finance cost implies (From the P&L statement). And how to actually intercept the data we receive from Annual Reports.

CWIP increasing means more money is getting sucked into capital expenditure. Reduction in finance cost means company\’s debt is reducing. Once you are familiar with all the line items, it becomes easy to understand the implications.

Dear Karthik sir,

Thank u so much for lucid explanation.

Sir, I want to ask one thing here in point no. 7.5, u have co-related P&L stmnt to Balance Sheet, can u elaborate giving bit example on it.

They are related in a couple of ways, I\’ve discussed it in the video series actually, maybe you can check that once.

Thank you very much.

Good luck!

Hello…I would like to know from where we can calculate the Capex of the company…Thanks in Advance

I\’ve explained that in the later part of the module, Prashanth.

Hello sir ,

Can you please tell me what these terms means \”Trade at cost\” and \”non trade at cost\” in the balance sheet?

Not sure, can you refer to the notes is any? Please do share your findings 🙂

I might be pretty late to go through this content but I really appreciate the efforts in explaining it to investors. I have started my FA journey and feel the starting point has been awesome! Thank You!

Thank you 🙂

I hope you like the content and enjoy reading on Varsity!

Hello sir,

If all of the businesse\’s retained earnings go into reserves and surplus then where did the cash and equivalents come from? Since external funding and profits are the only ways a business can have cash

Not all, a certain portion does.

Hello sir,

my question is sometimes on the assets side we find Investment Property, So this Investment Property will come under fixed assets?

Thats right.

Why cwip / gross block is a indicator of pilferage and what does this imply sir ?

Deep, we are dealing with gross block in detail in the financial modelling module, request you to please check that.

Hello Sir,

General Reserve is not cash on hand then where is it? What do you mean that it is available to the company? Where exactly would it be in an FD or over night fund or something?

When I see Borrowings, what parameters does one need to check if that debt is sustainable or not?

Haroon, reserves will be parked in FD or liquid funds. The company\’s treasury department will take care of these funds. To see if debt is sustainable, do calculate the interest coverage ratio of the company.

Hello Sir,

When does a one know if a company has restructured its loans?

Are general reserves considered cash on hand? Cash is kept as a current asset, not reserves correct?

Lastly If I see a company with a market cap of 6000 cr having very low reserves of 200-300 cr. With borrowing of 600 Cr. Should I be worried? If a company borrows more than its reserves?

Company will state the restructuring if its of any significance. General reserves is not cash in hand, but thats the amount of money available to the company. Reserves of 200-300 Crs with 600Cr borrowing seems not so comfortable (market cap is just a function of price increase). The borrowing bit, do check how the topline and PAT is growing.

Hello Sir,

I hope you are doing well.

1) When a company has long term and short term borrowings. They pay off the interest from their quarterly profits correct? What if they make a loss that quarter, do they pay it off from their reserves?

2) If a company has created a short term loan with the expectation of clearing it in one year and towards the end of the year they decide they would be unable to do that. Do they move it to a long term borrowing? When does the shareholder get to know this?

3) When it is time to pay of a loan, does the company clear the loans from its reserves?

4) Why cannot a company use its reserves as a current asset? Why just keep it for safekeeping?

1) Not necessary, they can pay it off in any sequence

2) Yes, companies can restructure their loans

3) Possible or from the profits it earns

4) Cash is kept as current asset

Hello Sir,

I am talking about Negative net debt to equity.

Net debt is Debt – Cash/Cash equivalents on hand

So a negative net debt/equity company would be relatively good correct?

Ah, I dint notice that. Yes, if its net, then its +ve.

Hello, I have an doubt?

look, when we talk about the shareholder fund – which is around 13,456 crore. Does it mean company owe them 13,456 crore? or it is amount of money company has in its hand?

Especially, when we add up all the profit of company every year in surplus section, I did not get that part. Does it mean its the money company has that belong to shareholder or its just amount that company is obliged to pay? isn\’t the profit every year a type of cash in hand, should not it belong to assets side.

For example – suppose I did start up a company 100 crore initial share capital, well 100 crore is used up in assets setup and 1yr operating expense. now at the end suppose company generated around 10 crore profit. Now if you add up this amount in shareholders side ,how come it become balanced?

honestly I am very confused? plz help!

This means that the funds belong to all the shareholders and will be used for shareholders welfare (bonus, dividends etc). The profits sit in the reserves of the company, which is also a part of the shareholder\’s funds.

Hello Sir,

Sorry for asking a follow up.

What is wrong with a company with a negative debt to equity ratio? Isn\’t that good?

It just means that the company has -ve shareholders equity or no real worth. So it is super risky to invest in such companies.

Hello Sir,

Ideally I should hope to have a debt to equity ratio under 1 correct? If there is negative net debt to equity (ie its cash can easily pay of its debt) i could still invest in it correct?

For interest coverage ratio, what is considered a good ratio? Anything above 1?

I\’d think twice to invest in companies that have -ve debt to equity ratio. Yes, I personally prefer companies with an interest coverage ratio of more than 1.

Hello Sir,

I trust you are doing well. Hope your family is safe also.

For ROE, companies that have debt cause a skewed ROE date. The dupoint method helps, but if I see a company having an ROE of 30% while it has considerable debt I am extremely conflicted.

What can I do about it?

Yes, the leverage factor has an impact. Hence do look at the debt the equity ratio, interest coverage ratio etc to get a better perspective.

Hello Sir,

I hope you are doing well.

EPS gets affected by debt.

What is a way I can understand a companies true EPS if the data is skewed by debt?

EPS gets affected by debt — you mean to say because of higher interest expense? If the debt exists, then you should factor it and not remove it 🙂

Hello Sir

I have read through the first two chapters of your module.

Is there a time frame for you to release the rest of the stuff?

No particular time frame, Tusshar.

Hello Sir,

Sorry I meant diluted EPS.

I have often seen EPS and diluted EPS.

How to understand that.

Second, many a times I see Enterprise Value and financial ratios taken with enterprise value?

Got it. This is when the company factors in the equity dilution. Btw, please keep track of the latest module on Varsity, I\’ll be discussing all of these terms and more.

Hello Sir,

What is the difference between ROE and diluted ROE.

What do you mean by diluted shares?

Also, what is the difference between Class A shares and Class B shares?

The difference between Class A and Class B is related to voting rights. We don\’t have this in India. Diluted ROE? Where did you get that? Diluted earnings are when you consider potential future dilution in Equity.

Really amazing content.

I had one question,

Does the Balance Sheet Always Balance?

That\’s the idea 🙂

(7.3) In the \”non-current investments\” schedule, it is shown that ARBL has invested in exide industries.ltd. What should an investor infer from this given that exide is a major competitor of ARBL?

Its a small investment right?

I am a young acccounting practioner and I ahve got this very interesting esp reading your notes , i would like to print some for home reading but it seems the notes are not downloadable hence cannot be printed.

Can you help me?

You can download and print the PDFs, this is available at the end of module page – https://zerodha.com/varsity/module/fundamental-analysis/

Sir depreciation is spread over it\’s useful life for ex 13000 every year

Will company add extra to depreciation in future above 13000

With the addition of new assets, yes, they will add, right?

Hats off to you for the content and detail! Great work Karthik and Zerodha!

Happy reading 🙂

it is been shown under the cash and bank balance part in the notes (16), so how is it related to cash as it is a liability?

Did you check the associated notes for more details?

why unclaimed dividends is a part of current assets as it is a liability to the company?

Unclaimed dividend is a current liability, let me check this again.

Thankyou,

I have one more doubt in this chapter, why advance tax payment is considered as an current asset as it is still tax which the company is paying in advance ?

Adv tax is an estimate and will remain an asset till the income tax is settled for the year.

I have one more doubt,

Why the unclaimed dividends are shown as an asset under cash and balances because the company can\’t use that money and if it remains unclaimed for next 7 years the company has to transfer that money to Investor Education and Protection Fund ?

Thats right, but if its on the current asset side, I\’m guessing this is the dividend the company is to receive and not claimed yet. If true, I\’m assuming this wont be a large value.

Please let me know after you check it, Thankyou.

Will do.

In Non-current investment what is Quoted-Non trade at cost, Unquoted-Non trade at cost and unquoted-Trade at cost ?

Ah, I\’m not sure either. Let me check.

Karthik Sir how are you doing? I love the work you are doing for the people around the world. This is truly amazing. Fan of Varsity and Finshots. I\’m a physiotherapist from Mumbai and invest in the stock market on behalf of my mother since the last 4 years. I\’m 26. You are the best. I salute all your efforts and the time you have put in to create this content. I had read an article about you from a Google Chrome suggestion and related to Zerodha. I love you… Stay blessed always…

Thanks so much for the kind words, Sahil!. I\’m really glad you liked the content on Varsity. Happy learning 🙂

AS ON Accumulated Depreciation page you have mentioned as \”As of 31st March 2013 (FY13) ARBL has depreciated Rs.17.2 Crs,\” i calculated this value but cant find solution how this value comes for previous year and present year.

Can you elaborate this point?

This is the current year depreciation, Vivek. No need to add the previous year\’s depreciation.

why company vehicles are fixed assets? Vehicles can be easily sold right?

So can buildings, right?

Hi,

Really amazing content.My question is under the depreciation/ammortisation column,what is the difference between \”for the year\” and

\”on deductions\”.While explaining the Deduction , below the table you have mentioned:

Previous year’s depreciation value + Current year’s depreciation – Deduction for the year

I am unable to appreciate the difference between current year`s depreciation and deduction for the year

Thankyou

For the year means the amount of depreciation considered for the year. This is present is the P&L. Deduction usually arises of a sale of the fixed asset from the gross block.

I see \”This is at a miniscule cost of 0.3 Crs for ARBL. All these costs are added to arrive at the total fixed cost of the company.\” Is this right? Should it be said as Cost or Assets?

Its cost right?

hello sir,

have a query regarding surplus &reserves in equity section..

what i feel it should come under asset instead of liability..

plz reply..

thanks..

No, the R&S belongs to shareholders, so from the company\’s perspective, this is a liability.

Total Depreciation for the year is:-

Previous year’s depreciation value + Current year’s depreciation – Deduction for the year

what is \’Deduction for the year\’ in this?

Sale of fully depreciated assets.

Hi

In balance sheet

investment also not increase

Hi

Yes I saw a consolidated number .it invested more means ? Where can I see they invested because investing cash in negative

In that case, please inspect the associated notes to the Gross block line item in the asset side of the balance sheet. You will get a perspective of all the CAPEX the company has carried out during the year.

Hi sir thank u for reply

But cash from.investing activities from -41 to -191cr. It\’s negative what it means ?

It means they have invested more in terms of fixed assets. It somehow does not makes sense. Are you looking at consolidated financials?

Hi sir

What it means if company\’s fixed asset continually decrease since six years despite sales ,profit ,operating CF increase .is it good or bad for company?

It most likely means that the company is selling off its assets. This will reflect in cash flow statement as well (increase in cash from investing activities).

Sir

What is 7.52 Cr \”Impairment\” shown under Fixed Assets and Depreciation against \”Free hold\” Land and Land Development ?

Dont remember now, please check the associated notes. Thanks.

Hello.

Is it a red flag when companies purchase a minority stake in some company which is not really in the same line of their business or related to the business in some way?

What are your thoughts?

Yes, hence you need to understand the rationale behind the investment. The company should give a detailed explanation of the investment.

hi,

why the cash and bank balance is so small as compared to the reserve and surplus, arent they the same?

Depends on the company and the way they manage their financials 🙂

How to know disposal value

Sie

It will be mentioned in the annual report, associated notes.

Hi,

Referring to \”The value of the assets deplete over time, as the assets lose their productive capacity due to obsolescence and physical wear and tear. This value is called the Depreciation expense, which is shown in the Profit and Loss account and the Balance Sheet\”. But to my understanding from P&L statement chapter, In P&L statement, depreciation expense is a part of the total asset cost which is spread across its useful life time. Whereas in balance sheet, full asset cost is in the net block value, depletion value of those assets are the depreciation value. Am i right? If right, it contradicts the above referred statement which says same depreciation expense is put in both P&L and balance sheet.

I\’m not sure if I fully understand your query. The depreciation that you see in P&L is the depreciation for the year, whereas the one in B&S is what gets carried forward from year to year.

Hi.

Great content. Easy to grasp for a person from a non-accounting background.

Question: If a company sells one of its subsidiary company, will the earnings from this transaction reflected in the current FY (financial year) or will it be distributed over various FYs?

Same question for the case when a company buys another company?

Technically this is not an earning, so this will be reported in other income. It will be included in the same financial year.

sir,

1. How CASH & CASH EQUIV. and Reserve & surplus are different. Aren\’t they a CASH park in bank accounts of a company. Can\’t we use the money of both (Cash & Cash Eq. and Resere & Sur) for similar purpose like paying debt or acquire physical asset etc. While analysing a company Can we consider a cash in hand of a company by combining both. If not, why.

2. Where Will the Profit for the year go, eithr in Cash & Cash Equivalents OR Reserve & Surplus?????

1) There are statutory requirements for a company to have money in capital reserves (if I\’m not mistaken). Yes, you can consider the reserves as a part of the overall cash. Also cash in the bank is a current asset, which means we cannot consider that for long term purposes

2) Earnings get added to reserves.

thank you sir

sir,

what is a hedge fund company ?

please do explain in detail sir .

Hedge Funds are essentially an investment company that invests your money and manage the risk on your behalf. In India Hedge Funds are called AIF 3 – https://en.wikipedia.org/wiki/Securities_and_Exchange_Board_of_India_(Alternative_Investment_Funds)_Regulations,_2012

sir,

what is investment bank ? please explain me in detail.

thank you

Its a financial institute which carries out several financial services except retail banking.

How is the interest earned(if any) on long/short loan advances under Assets Balanced in the the liabilities??

It comes under other income in the revenue (P&L) and further distils down to retained earnings and reserves in the balance sheet.

OK. Can you also please answer the 1st question? What is additions during the year for Fixed Assets?

In this context, additions during the year refer to the new purchase of fixed assets.

Hi Karthik,

Can you put more light on \”addition/adj during the year\” of Fixed assets? What is that?

My next question is,

If I bought a land worth Rs 100 for 10 years and depreciated by Rs 10 every year, the value of the land after 10 years written on balance sheet would be 0 (assuming the cost of land doesn\’t rise)? What if I bought the land for indefinite period of time?

Thanks,

Eshan

Eshan, as per accounting standards, land is not depreciated.

I am reading varsity chapters for the first time. And things are not clear. May be because I am not from business background and a beginner in this field. Can you suggest me how should I plan my study so that I can choose stocks myself. Thanks.

Utpal, the content is designed keeping first-time readers in perspective. I\’d suggest you start from the very first module here – https://zerodha.com/varsity/module/introduction-to-stock-markets/

Hello,

Just an interesting thought, If a company involves in a manufacturing of product/s which can not be utilised or consumed within year will it fall under finished goods of current asset or fixed asset ?

what is your take on it?

THANKS

It will show up in the increase in inventory under current assets.

What is meant by \”Cash on Demand\”?

I guess this is a sort of provisioning. As good as payable on a call.

Hi sir

1.if R&S in cash form then what is the difference btw. R& S and cash ?

2.Why that two mention separately in balance sheet ?

1) R&S is earmarked for a purpose

2) That\’s because they are two different balance sheet items. R&S is liabilities and Cash is an asset.

Hi

suppose one company having a 1500 cr R&S

Means that company have 1500 cr cash

M I right ??

Yes, thats right.

First of all thanks for the content.

Sir i want to ask the following questions

1. Is share capital is the minimum amount which should be there with the company after paying its dividends and all?

2. If yes then, if a company has no face value, then whatever the investors willing to pay for shares will become its share capital as there is no share premium. So now when an investor buys a share the amount will go into the share capital account which will obligate the company to maintain that amount after all the payouts of dividends etc. So is that is the reason why company keep a face value but a very lower one?

1) No, share capital is the amount of funds the promoters bring in

2) All shares need to have a nominal value/face value.

Thanks, Content is very rich and helpful for a novice like me. Feeling gr8 to be a customer of Zerodha

Good luck, Shankar!

Hey Karthik,

What are secured and unsecured trade receivables?

Ah, I\’m not sure about that.

Hi sir

I want to know which depreciation( ex.any figure ,any ratio etc.) is good and which one is not fair ?

Bcoz. I confuse in it .so plz explain in detail

Thank u

Sorry, I dont seem to get your query. I\’d suggest you read through all these chapters to get complete clarity. Thanks.

Hi sir

Means some company depreciate more amount and some less compare to its assets .

What is good for company ?

Which is ideal according to you ?

Amit, depreciation should be proportional to the fixed assets held by the company.

sir,can you please explain me what component of debt to be taken while calculating enterprise value?

does it include provisons and deffered tax liability?

I\’d suggest you take the long-term debt into consideration.

long term debt minus the provisons for long term debt and deffered tax laibilities?

Sorry, I\’m unable to get the context.

what to take from balance sheet while calculating enterprise value ? long term debt and short term debt but is provisions for debt are included in calculating debt?

You need to take the long-term debt.

Hi Karthik,

I have two questions.

1) Let say a company goes public and raise 100 cr. So, 100 cr will be its SHAREHOLDER\’S EQUITY. Now, company a new plant and machinery from it. So, those will be its FIXED ASSESTS.

Now, I am little confused that the same thing is included in two parts.

2) Why is it needed to include SHAREHOLDER\’S EQUITY every year? Doesn\’t that money is converted into some kind of asset over the year?

1) Yes, if the company goes public, these shares will belong to the shareholder\’s equity. Assets like building, plants, machinery all belong to Fixed Assets

2) Shareholder equity only considers the face value of the shares

What is the difference between Current year’s depreciation and Deduction for the year?

Which deduction are you talking about, Sandeepan?

Hi Karthik,

I’m finding it difficult to comprehend the balance sheet equation. Can you please advise where am I missing?

For the illustration purpose let’s assume this hypothetical case where I set up a company on the first day of financial year. Company took 1 cr rupees loan, the company’s business ran successfully and generated 2cr by the end of financial year. I then decided to close the company. After repaying the loan, selling everything that belongs to company and deducting all the expenses incurred (including the taxes, interest, salaries and so on) to generate that 2 cr rupees, the company is left with 0.5cr excess cash in hand.

Now, the equation assets = liability doesn’t hold true as the company had no assets and liabilities at the end of the financial year except 0.5cr cash on hand.

Can you please advise where am I missing here?

Kind regards,

Guru

At the beginning of the year, you have 1 Cr in Cash (asset side) and 1 Cr as borrowings in the liability side.

You spend cash to buy assets to commence business. Cash values come down but other assets increase. The balance sheet is still balanced here.

Business generates revenue of 1 Cr, lets say after all the expenses you are left with 50L profits. This goes to Reserves and surplus on the liability side. This is the net worth. Assets and liabilities still match at 1 Cr.

Hello!

e.g. A company takes a loan of 1 Cr from Bank. So, 1 Cr is its liability. Now, it purchases machines worth of 1 Cr. Assets sections mentions the depreciated value of machines, not the actual one. Let\’s say, it is usable for 5 years. Hence, company will mention 0.2 Cr for 5 year in the Assets.

Then, how the Balance sheet is going to balanced?

Thanks in advance. Let me know if I missed something.

The assumption is that the machine is used to manufacture goods which when sold translates to cash (so assets increases).

Hi Karthik,

When putting AMRL\’s balance sheet data in an excel I found out that there is some difference in the numbers for the same year (2014) but in Annual reports of different years.

Like –

In AR of 2014-15, Balance sheet > Current Liabilities > Short-term provisions of 2014 = 1,259.78

In AR of 2013-14, Balance sheet > Current Liabilities > Short-term provisions of 2014 = 2,818.73

Why is there such a discrepancy?

When should one make of this discrepancy?

Which data should be used ideally? Cause the values differ quite a lot and may have impact on some ratios !!

Can you please tell some \”good practices\” to be followed for such cases ?

Sanket, yes, the companies can restate the numbers, for this reason, I always prefer to take the next year\’s AR to refer to this year\’s numbers. For example, I\’d look at 204-15 AR to see the numbers of 2013-14.

Understood. Thanks for the quick response! 🙂

you guys are doing a great job !

Cheers! Happy learning!

Hi Sir,

Developed a very good content, have not gone thru this one have a question, mine might be a very starter,

1) How do you derive at networth/share holder equity (actually everywhere it says simple total assets – total liabalities which i saw in balance sheet which would be zero) can you help me this?

2) and from there on wanted to calculate the ROE of the company? is there a better way or formula?

1) Networth is attributable to the amount equal to reserves/surplus and share capital.

2) No, use the simple formula = PAT/Share Capital

But does the ROE give the complete profitability picture? Since the company might have bought the profit from the loans. So ROIC gives the better picture ?

If so does the ROE really makes sense for the companies with no borrowings?

Thanks in advance !

Yes, ROE can be distorted by financial leverage. ROE is very important, but like you pointed out, make sure you look at it keeping financial leverage in perspective.

My Question is – how Operating Expenses related to the Inventory?

Can u plz explain this..sir.

I m very Happy with this note… Thanks a lot for writing this Zerodha Varsity..!

Glad to you know you liked Varsity. Can you please share more details regarding your query? Thanks.

Dear Faisal

Very thanks for feedback from Zerodha team

But if you look at rain industry ltd Q3 results ,they have only released P&L statement . I have searched the Balance sheet for that company.I could not find anywhere else.

i think ,this company has only released P&L for Q3 .

Is it possible that the company can release the P&L sheet without updating Balance sheet and released ?

Yes, companies only update the P&L during the quarter. B/S is updated once a year.

Ho karthick

During every quarter results in the financial year ,the balance sheet will be updated and released based on that particular year quarter P &L statement ?

Yes, companies put out a quarterly P&L statement and an updated Balance Sheet for that period

Hi Kartik,

This query related to equities in the Balance sheet note, what are \”quoted at cost\” and \”un-quoted at cost\” terms?

Ah, I need to verify this myself Vivek.

Hi Kartik,

In the case of CWIP – how do we know how much investment has been originally made in the company?

Secondly, CWIP could also mean machinery purchased, how do we know what machinery has been purchased?

You will have the track the CAPEX for this, which is available in the asset schedule associated with the Fixed assets on Balance sheet.

the images of balance sheet are not clear and readable. pls reload with zoomed in image.

Will take a look, thanks.

Hi Karthik,

You have made an excellent video on how to read cash flow statements\”..

Can you please make one video on analyzing balance sheet and one on basics of fundamentals like FV,equity dilution etc.

Yes, will certainly do that, Rohan.

1. What is the relevance of face value of share and how it is used for analysis as it is much below cmp like rs 10 or rs 2?

2. What is the meaning of share capital and how it is different from market cap and what is the relevance of share capital?

1) A share needs to have a basic value assigned to it, to signify the economic value. Hence the face value. The face value helps during corporate action like dividend, splits, bonus etc. Also in calculating the number of shares outstanding

2) Share capital is the initial capital that the promoters bring in, share cap divided by face value is the number of shares outstanding

Hi Karthik!

I \’m not entirely sure of the difference between P and L statement, and Balance statement. Is the difference just in that the PL statement gives yearly data while Balance statement gives consolidated data?

P&L reports the profit or loss made during the year. Balance sheet, on the other hand, reports various other financial metrics of the company like – debt, net worth, share holders wealth, fixed assets etc. I\’d suggest you go through these chapters in detail to get a sense of whats happening with these two statements.

\”Further they also wound up 0.668 Crs worth of building;\” What do you mean by this statement?

Sale of asset.

HI Karthik,

Thanks for great work , really is very helpful.

Quick check. If the asset of .668 is sold , should it not reflect in the P&L statement in other income?

Regards

Ujval

Yes, usually the sale of assets is recognized under the other income bit in P&L.

HI Karthik,

This is really helpful , thanks for great work . Much appreciated.

A small check , If the asset of .668 is sold , should it not reflect in the P&L statement in other income.

Regards

I find it difficult to believe it, that you are not good at reading the financial statement\’s of bank, I hope your reply is not sarcastic one.

Not really. I\’ve not spent time reading banking statements, maybe I should 🙂

Hello Karthik,

Since I have Invested in Syndicate Bank, I Just want to study Bank\’s financial statement , as Bank\’s Financial statement is different from any other company\’s statement, Is there any website wherein I can get detailed study of Bank\’s , since it a service sector, the balance sheet is different any other company

I agree, and I must confess I\’m not really good at reading the financial statement;s of banks. Also, I\’m not sure from where you can understand this.

Hello Karthik,

I just did a DCF valuation using your excel on Asian Paint stock and the lower & upper intrinsic values(considering 15% error leeway) came to Rs. 425 and Rs. 575 respectively. However the current stock price of Asian Paint is Rs. 1160 – almost double the price of upper intrinsic value.

I am confident that my inputs to the excel are fairly correct, so why there is so much price gap? I am holding 100 shares of it at an average price of Rs. 1157 – so if my DCF calculation is correct I should be selling it immediately – isn\’t it? Also I find in the news that few analyst are predicting the stock price to go up to Rs. 1230 – so I am confused what to consider here.

Not sure Kris…DCF is just the last step. Have you made sure you\’ve taken the right FCC, discount rate etc?

Thanks a lot for sharing this vital information with everyone, you are doing a wonderful work by educating people about market which makes people aware about the market and once again thanks a lot.

Thanks for the kinds words John.

Why the depreciation in Balance sheet is different than the depreciation in P&L Statement?

in P&L Sheet its 645.71 & IN Balance Sheet it is 647.2

This is the way it would work, assume a new company starts today –

Year 1 depreciation = 10 Crs

For this year in both P&L and BS depreciation amt would be 10Crs

Year 2 depreciation = 5 Crs

For Year 2 P&L depreciation would be 5 Crs and BS depreciation amt would be 10 + 5 = 15 Crs

So P&L gives yearly data…and BS gives you accumulated data.

Hi Karthik,

I really appreciate your nuanced explanation about balance sheet. Great work. Just as I dwelled deeper, I came across many more things in Moneycontrol, so if you go their website, in balance sheet section of any company. Taking here the example of AmaraRaja Batteries, can you explain the Other information part, containing CIF value of Imports and The FOB VALUE of goods. In fact the whole part under the section of Additional Information. And how and where these values have been incorporated?

Thanks in advance.

Victor

Generally all these would be included under one main header in the balance sheet. Suggest you read through the notes of the company for a quick narration of the line item.

i have finally getting the answers for my doubts remained after spending no of months of time on internet searching for useful material for doubts of balance sheet and other financial statements. i am thankful to you. but here my doubt is how can we get related information related to each item as you explained in the this article?

Usually the Annual report of the company has all the narrations wrt to the line items in the Financial statements.

Thanks Zerodha for sharing this wonderful knowledge …..

I appreciate your handwork . I have Question …

In balance sheet, the net profit is added in reserve and surplus ( liability side ) .Consider if the company AAA make profit 200 cr without change in Asset ,then How they will maintain balance sheet equation \” Asset = liability \”

Well, I suppose it gets balanced out with other assets – inventory, Capital work in progress, receivables etc.

What a fantastic module on P&L stmt and Balance sheet, which is written in way it can be easily understood by any retail investor. Hat\’s off to you Karthik sir and ZERODHA. This is what called passing value to customers (in fact to anybody as you have made it as open source). And this is one of the reason ZERODHA is distinctly different from other discount brokers and from many traditional brokers as well. Once again well done and am happy that i am a customer of ZERODHA.

And we are equally happy to have you as our client 🙂

Sir i am truely impressed by your work…It was very useful to me. Hope you keeod doing the good work. One more important thing that this webpage has no advertisements at all. It was a good experience learning hear.

Happy to know that Shashank 🙂

Your work helped me to form a base for understanding the statements and balance sheet however i want deeper insights to understand companies fundamentals. I Request you to provide me some books to get advanced knowledge for the same.

Thank you

Nishanth not sure about books, but I would suggest you start reading blogs and articles from http://www.safalniveshak.com/. Its highly rated and no nonsense blog. All related to value investing and understanding businesses better.

This is amazing. thanks for sharing the blog detail.

Happy reading!

Hi,

Really amazing content. my question is there is a deduction of 0.668 cr under the example cited here i.e buildings. Does this mean it is sold off? if yes then where is this amt added?

Also i would like to mention a few suggestions only because i like your work so much and it would mean a lot to contribute:

1) Not on this topic but earlier ones used to contain a lot of comments. That\’s a good thing as they contain little bits and examples that cant be contained in the chapter but i wish there was some liking( or +1 ) kind of feature or curation from your side to make the best ones come first or appear larger or whatever. Basically some ranking kind of thing to rank the best interactions without having to read every comment. And a lot of people ask doubts too early in the wrong chapter i hope u c

an create a provision to move those from your side.

2) The share button is very distracting and obstructs the text sometimes. If you just allign it to the right I think it would greatly reduce the problem.

3) Its amazing that you don\’t have any banners and adds on this site but this works against u in one aspect that is its much easier to read a body of text that has 7 – 10 words per line (a pretty standard rule of calligraphy).

Thank you so much for the suggestions Praneeth!

The 0.668 Crs has been written off the books of account and is no longer considered as assets, hence it would not be added to any other part of the Balance sheet.

The ranking idea for comments is good, I will check internally if this is implementable by us.

Will try and lighten out the share button, so that it is less distracting….and also thanks for the tip on calligraphy method, I will try and incorporate it.

Please do continue to share more inputs so that we can turn this into a meaningful resource.

One last thing: when i try to zoom in to make the text on the screen larger this is what happens.

Ah, will look into this. Thanks for pointing.

This problem is not yet solved.

Sorry for that..will try my best to get it sorted.

simple, easily explained for a person from non-financial field. Good job.Thanks a lot.keep it up sir.

Most welcome 🙂 Please do stay tuned for more.

Sir i am actually going to ask something out of topic .

I was going through the annual reports of torrent pharma . I calculted some ratios , and roe was good , its above 25% . Can you tell me about torrent pharma\’s other ratios . why its debt is rising , Its consolidated profit is less than its standalone profit .

I want to ask , is it a good stock for investment .

ROE can be good but if it comes at the cost of excessive financial leverage then it may not be that impressive. Suggest you break down ROE in terms of DuPont analysis and check once. To understand why debt is raising etc I would suggest you read the AR. I\’m certain the management has given an explanation there.