3.1 – What is an Annual Report?

The annual report (AR) is a yearly publication by the company and is sent to the shareholders and other interested parties. The annual report is published by the end of the Financial Year, and all the data made available in the annual report is dated to 31st March. The AR is usually available on the company’s website (in the investor’s section) as a PDF document, or one can contact the company to get a hard copy of the same.

Since the company’s annual report, whatever is mentioned in the AR is assumed to be official. Hence, any misrepresentation of facts in the annual report can be held against the company. To give you a perspective, AR contains the auditor’s certificates (signed, dated, and sealed) certifying the sanctity of the financial data included in the annual report.

Potential investors and the present shareholders are the primary audiences for the annual report. Annual reports should provide the most pertinent information to an investor and communicate its primary message. For an investor, the annual report must be the default option to seek information about a company. Of course, many media websites claim to give financial information about the company; however, the investors should avoid seeking information from such sources. Remember the information is more reliable if we get it to get it directly from the annual report.

Why would the media website misrepresent the company information you may ask? Well, they may not do it deliberately, but they may be forced to do it due to other factors. For example, the company may like to include ‘depreciation’ in the expense side of P&L, but the media website may like to include it under a separate header. While this would not impact the overall numbers, it does interrupt the overall sequencing of data.

3.2 – What to look for in an Annual Report?

The annual report has many sections that contain useful information about the company. One has to be careful while going through the annual report as there is a fragile line between the company’s facts and the marketing content that the company wants you to read.

Let us briefly go through the various sections of an annual report and understand what the company is trying to communicate in the AR. For the sake of illustration, I have taken the Annual Report of Amara Raja Batteries Limited, belonging to Financial Year 2013-2014. As you may know, Amara Raja Batteries Limited manufactures automobile and industrial batteries. You can download ARBL’s FY2014 AR from here (https://www.amararajabatteries.com/Investors/annual-reports/)

Please remember, this chapter’s objective is to give you a brief orientation on how to read an annual report. Running through every page of an AR is not practical; however, I would like to share insights into how I would personally read through an AR and understand what kind of information is required and what information we can ignore.

To better understand, I would urge you to download the Annual Report of ARBL and go through it simultaneously as we progress through this chapter.

ARBL’s annual report contains the following 9 sections:

- Financial Highlights

- The Management Statement

- Management Discussion & Analysis

- 10-year Financial highlights

- Corporate Information

- Director’s Report

- Report on Corporate governance

- Financial Section, and

- Notice

Note, no two annual reports are the same; they are all made to suit the company’s requirement keeping in perspective the industry they operate in. However, some of the sections in the annual report are common across annual reports.

The first section in ARBL’s AR is the Financial Highlights. Financial Highlights contains the bird’s eye view on how the company’s financials look for the year gone by. . The information in this section can be in the form of a table or a graphical display of data. This section of the annual report generally makes a multi-year comparison of the operating and business metrics.

Here is the snapshot of the same:

The details you see in the Financial Highlights section are basically an extract from its financial statement. Along with the extracts, the company can also include a few financial ratios calculated by the company itself. I briefly look through this section to get an overall idea, but I wouldn’t say I like to spend too much time on it. The reason for looking at this section briefly is that, I would anyway calculate these and many other ratios myself, and while I do so, I would gain greater clarity on the company and its numbers. Over the next few chapters, we will understand how to read and understand its financial statements and how to calculate the financial ratios.

The next two sections, i.e. the ‘Management Statement’ and ‘Management Discussion & Analysis’, are quite important. I spend time going through these sections. These sections give you a sense of what the company’s management has to say about their business and the industry in general. As an investor or a potential investor in the company, every word mentioned in these sections is important. In fact, some of the details related to the ‘Qualitative aspects’ (as discussed in chapter 2), can be found in these two sections of the AR.

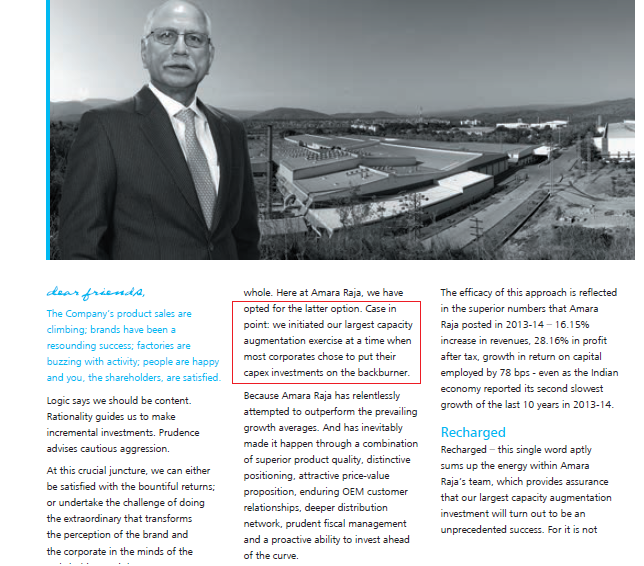

In the ‘Management Statement’ (sometimes called the Chairman’s Message), the investor gets a perspective of how the man sitting right on top is thinking about his business. The content here is usually broad-based and gives a sense of how the business is positioned. When I read through this section, I look at how realistic the management is. I am very keen to see if the company’s management has its feet on the ground. I also observe if they are transparent in discussing what went right and what went wrong.

One example that I explicitly remember was reading through the chairman’s message of a well-established tea manufacturing company. In his message, the chairman was talking about revenue growth of nearly 10%. However, the historical revenue numbers suggested that the company’s revenue grew by 4-5%. Clearly, in this context, the growth rate of 10% seemed like a celestial move. This also indicated that the man on top might not really be in sync with ground reality, so I decided not to invest in the company. Retrospectively when I look back at my decision not to invest, it was probably the right decision.

Here is Amara Raja Batteries Limited; I have highlighted a small part that I think is interesting. I would encourage you to read through the entire message in the Annual Report.

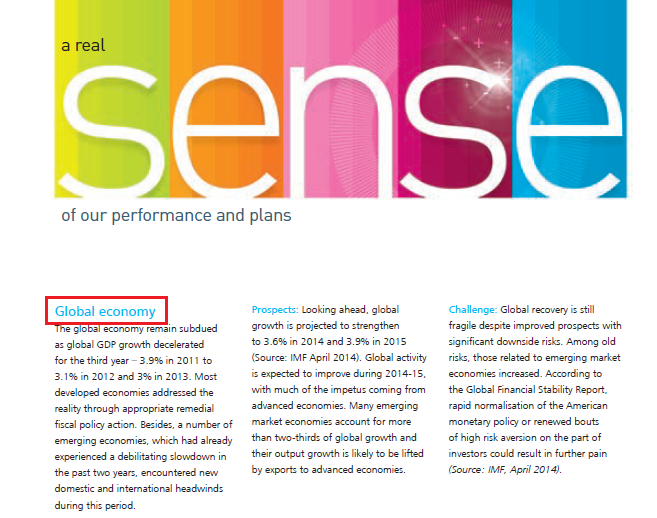

Moving ahead, the next section is the ‘Management Discussion & Analysis’ or ‘MD&A’. This, in my opinion, is perhaps one of the most important sections in the whole of AR. The most standard way for any company to start this section is by talking about the macro trends in the economy. They discuss the overall economic activity of the country and the business sentiment across the corporate world. If the company has high exposure to exports, they even talk about global economic and business sentiment.

ARBL has both exports and domestic business interest; hence they discuss both these angles in their AR. See the snapshot below:

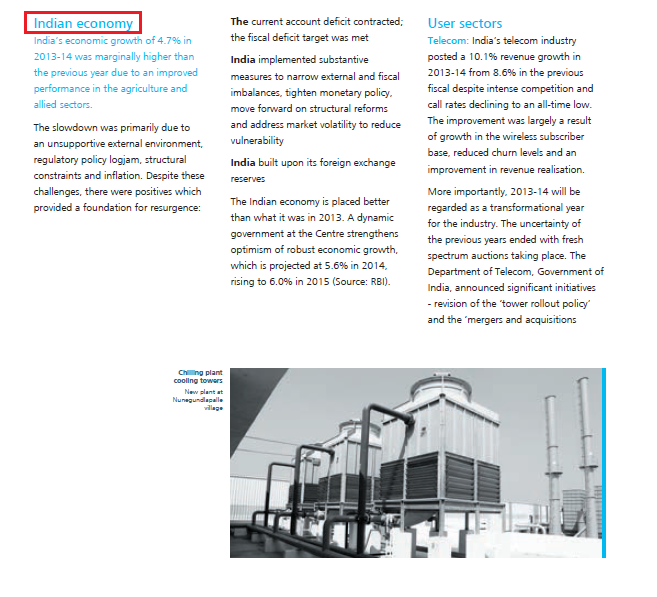

ARBL’s view on the Indian economy:

Following this, the companies usually talk about industry trends and what they expect for the year ahead. This is an important section as we can understand what the company perceives as threats and opportunities in the industry. Most importantly, I read through this and compare it with its peers to understand if the company has an advantage over its peers.

For example, if Amara Raja Batteries Limited is a company of interest, I would read through this part of the AR and read through what Exide Batteries Limited has to say in their AR.

Remember, until this point, the discussion in the Management Discussion & Analysis is broad-based and generic (global economy, domestic economy, and industry trends). However, in the future, the company would discuss various aspects related to its business. It talks about how the business had performed across various divisions, how it fares compared to the previous year, etc. The company, in fact, gives out specific numbers in this section.

Here is a snapshot of the same:

Some companies even discuss their guidelines and strategies for the year ahead across the various verticals. Do have a look at the snapshot below:

After discussing these in ‘Management Discussion & Analysis,’ the annual report includes a series of other reports such as – Human Resources report, R&D report, Technology report etc. Each of these reports is important in the context of the industry the company operates in. For example, if I am reading through a manufacturing company annual report, I would be particularly interested in the human resources report to understand if the company has any labour issues. If there are serious signs of labour issues, it could lead to the factory being shut down, which is not good for its shareholders.

3.3 – The Financial Statements

Finally, the last section of the AR contains the financial statements of the company. As you would agree, the financial statements are perhaps one of the most important aspects of an Annual Report. There are three financial statements that the company will present namely:

- The Profit and Loss statement

- The Balance Sheet and

- The Cash flow statement

We will understand each of these statements in detail over the next few chapters. However, it is important to understand that the financial statements come in two forms at this stage.

- Standalone financial statement or simply standalone numbers and

- Consolidated financial statement or simply consolidated numbers

To understand the difference between standalone and consolidated numbers, we need to understand a company’s structure.

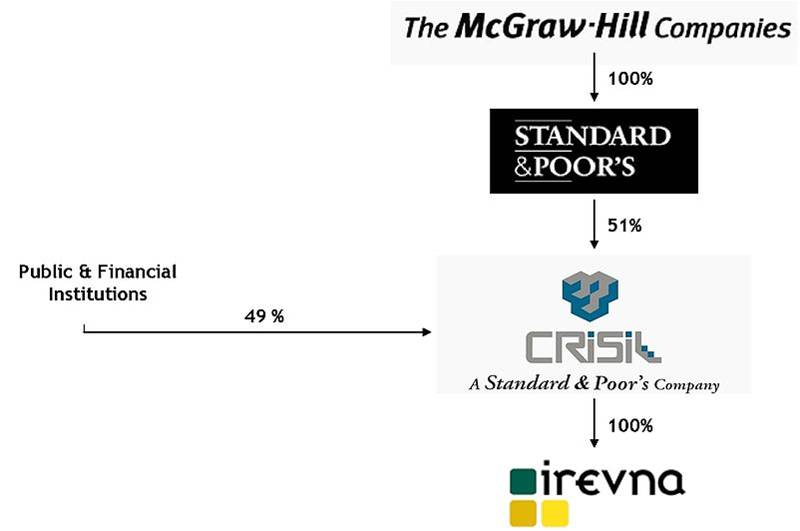

Typically, a well-established company has many subsidiaries. These companies also act as a holding company for several other well-established companies. To help you understand this better, I have taken the example of CRISIL Limited’s shareholding structure. You can find the same in CRISIL’s annual report. As you may know, CRISIL is an Indian company with a major focus on corporate credit rating services.

As you can see in the above shareholding structure:

- Standard & Poor’s (S&P), a US-based rating agency holds a 51% stake in CRISIL. Hence S&P is the ‘Holding company’ or the ‘Promoter’ of CRISIL.

- Public and other Financial institutions hold the balance of 49% of shares of CRISIL.

- However, S&P itself is 100% subsidiary of another company called ‘The McGraw-Hill Companies’

- This means McGraw Hill fully owns S&P, and S&P owns 51% of CRISIL.

- Further, CRISIL itself fully owns (100% shareholding) another company called ‘Irevna’.

Keeping the above in perspective, think about this hypothetical situation. Assume, for the financial year 2014, CRISIL makes a loss of Rs.1000 Crs and Irevna, its 100% subsidiary makes a profit of Rs.700 Crs. What do you would be the overall profitability of CRISIL?

Well, this is quite simple – CRISIL on its own made a loss of Rs.1000 Crs, but its subsidiary Irevna made a profit of Rs.700 Crs, hence the overall P&L of CRISIL is (Rs.1000 Crs) + Rs.700 Crs = (Rs.300 Crs).

Thanks to its subsidiary, CRISIL’s loss is reduced to Rs.300 Crs instead of a massive loss of Rs.1000 Crs. Another way to look at it is that CRISIL on a standalone basis made a loss of Rs.1000 Crs, but on a consolidated basis, it made a loss of Rs.300 Crs.

Hence, Standalone Financial statements represent the company’s standalone numbers/ financials and do not include its subsidiaries’ financials. However, the consolidated numbers include the companies (i.e.standalone financials) and its subsidiaries financial statements.

I personally prefer to look through the consolidated financial statements to represent the company’s financial position better.

3.4 – Schedules of Financial Statements

When the company reports its financial statements, they usually report the full statement and then follow it up with a detailed explanation.

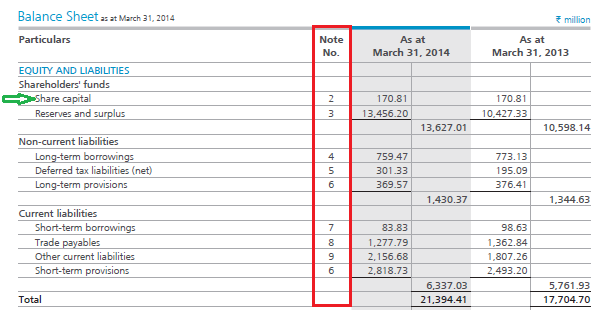

Have a look at the snapshot of one of ARBL’s financial statement (balance sheet):

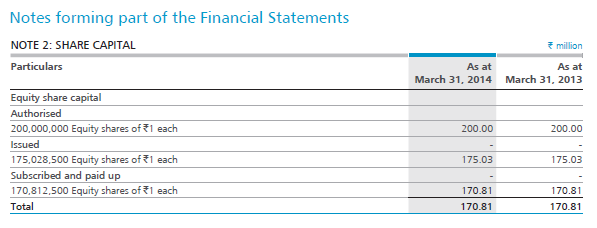

Each particular in the financial statement is referred to as the line item. For example, the first line item in the Balance Sheet (under Equity and Liability) is the share capital (as pointed out by the green arrow). If you notice, there is a note number associated with share capital. These are called the ‘Schedules’ related to the financial statement. Looking into the above statement, ARBL states that the share capital stands at Rs.17.081 Crs (or Rs.170.81 Million). As an investor, I would obviously be interested in knowing how ARBL arrived at Rs.17.081 Crs as their share capital. To figure this out, one needs to look into the associated schedule (note number 2). Please look at the snapshot below:

Of course, considering you may be new to financial statements, jargon like share capital makes much sense. However, the financial statements are straightforward to understand, and over the next few chapters, you will understand how to read the financial statements and make sense of it. But for now, remember that the main financial statement gives you the summary and the associated schedules give the details about each line item.

Key takeaways from this chapter

- The Annual Report (AR) of a company is an official communication from the company to its investors and other stakeholders.

- The AR is the best source to get information about the company; hence AR should be the default choice for the investor to source company-related information.

- The AR contains many sections, with each section highlighting a certain aspect of the business.

- The AR is also the best source to get information related to the qualitative aspects of the company.

- The management discussion and analysis is one of the most important sections in the AR. It has the management’s perspective on the country’s overall economy, their outlook on the industry they operate in for the year gone by (what went right and what went wrong), and what they foresee for the year ahead.

- The AR contains three financial statements – Profit & Loss Statement, Balance Sheet, and Cash Flow statement.

- The standalone statement contains the financial numbers of only the company into consideration. However, the consolidated numbers contain the company and its subsidiaries financial numbers.

How can one know that whatever is written in the annual report is correct and not manipulated or twisted as per the investors interest and to please them? Is there an entity or personal verifying the same?

Yes, thats is why we have the auditor\’s signature and report included in the AR.

From share capital notes,

200 million authorised shares and around 175 million issued.

what about those remaining shares.

Its authorized but not issued.

Hello Mr. Karthik, I couldn\’t figure out how to comment separately hence replying to your comment;

With the onset of ChatGPT and other AI which can be used to write literature, do you still think management statements/analysis are still relevant?

Can they not be easily outsourced or be slyly manipulated by AI in order to match with shareholder values while not reflecting the managements\’ genuine values and outlook?

Thank you for what you are doing and I appreciate that you continuously update this section with answers.

Of course, it becomes easy. In fact, we recently put up a post on social media that talks about this.

how to use Ai or ChatGPT

Watch this – https://youtu.be/4eYIRofAAP0?si=dPCt61VPEBIHeVkX

Dear Sir, my question is whether everything is done on AI, then how to analyse Annual Report because Fundamental Analysis is based on it.

You can use AI to help you with that as well 🙂

Great question and I love to reply it. Basically the company has the permission to create or issue only 200,000,000 shares however the company only issued 175,000,000 keeping the remaining unissued coz of many reasons like future fund raising , future mergers or acquisitions ( some companies don\’t give cash they give shares) etc . Therefore companies keep some shares unissued.

Happy learning 🙂

Dear Karthik Rangappa Sir,

First of the I really appreciate this useful, Important, well-structured and High quality free Education and I want to thank you and whole Zerodha team for providing this free Highly valuable Education and to the point .

I have One Question.

Q1- In 3.3– The financial statements, You have shown us the structure of CRISIL and whom it is owned by and who it Owns. My Question is that Since, STANDARD&POORS have equity which is 51% in CRISIL AND CRISIL has 100% equity in Irevna and since STANDARS&POORS owns CRISIL 51%, does that directly or indirectly makes them(STANDARD&POORS) shareholder in Irevna too,because they have CRISIL equity which is 51? If no, then Why and if yes, then is it same as crisil equity which is 51% or more or less?

I know one thing that since standards&poors owns crisil and they own irevna, they do have influence over irevna because they own crisil, basically indirect control.

Thank you for your time,

Much love and support from Punjab.

Thanks Pratham. I\’m happy you liked the content on Varsity!

So S&P and Irevna become related party and indirectly, there is ownership as well and by virtue of that, there will be some influence as well 🙂

in the example you mentioned in this chapter about the ownership percentage. so my question is how much profit of theMCGRAW-HILL

Dont remember now, Sujal. Request you to pls check the screenshots, I\’ve included the P&L statements.

much more valuable information for new participants

Happy learning 🙂

When a number is given in parentheses on a profit and loss statement, it indicates a negative value. I did not know this, hence above statement is correct 🙂

Ah ok 🙂

In 3.3 Financial statements, correction is needed -> (Rs.1000 Crs) + Rs.700 Crs = (Rs.300 Crs) this should be (Rs.1000 Crs) – Rs.700 Crs = (Rs.300 Crs)

Checkin this, Ajinkya.

It\’s correctly written as 1000 Crs in bracket, so it is considered as the negative figure.

If its in brackets, then yes, its considered negative.

Sir

In number of shareholders column , it includes total number of share i.e. (number of promoters shares + number of investers shares ) or it includes only number of investers shares only ??

It includes all the shares that are held by investors.

Hi Karthik,

Thank you for the efforts you and your team has put in!

Following are my questions

1. How reliable are these annual reports of the company, is there any way to ensure the trustworthiness of the numbers provided in the annual report and assurance that they are not manipulated.

2. There can be situation where companies has to pay money out of the records to get things done, how are these money handled and gets accounted into annual report?

(Note: I don\’t mean all companies do these, but we have seen these instances happening)

1) These are signed by the auditors, so we assume its accurate and true.

2) They dont, unless its a cash payment and it gets recorded. If you are talking about bribes etc, then they dont 🙂

How to find the most recents orders that a company has received and the deadline to fulfill that order ?

If possible an entire log or orderbook of a company?

You need to keep track of the corporate filings made to the exchanges.

Being simple is being genius. Excellent simple way for layman to understand.

Thanks Vanitha. Happy learning 🙂

Tq, karthik sir for this wonderful explanation

Glad you liked it, happy learning 🙂

I am reading this in September 2024, and the content still holds up. It’s better than anything else out there.

Happy learning 🙂

Hi Karthik,

Thanks for your efforts in making these modules. It helps a lot for the fresh investors like me. I just couldn\’t able to understand why you have stated that you prefer consolidated financial statement. Let\’s consider the same example with a minor change that Irvena making profit of 1200 crs. Now if I look at the consolidated statement, the Crisil is making a profit of 200 crs as a whole but the actual case is Crisil is going in loss. If I review the consolidated statement and invest in Crisil thinking that it is making profit as a whole and sometime in the future Crisil sells its stake on Irvena for some reasons then their financials will look bad and their shares may incur losses.

Please help me understand why its better to review consolidated statement rather than standalone statement. Thanks.

But in reality, there is a cash flow exchange between the two companies. So the market will value the entire thing as a single entity.

In equity and capital section

What is mean by authorised,issued, subscribed and paid up..

Do check this video – https://www.youtube.com/watch?v=q-T2svXZ77s&list=PLX2SHiKfualGOP9093b6qo11EsgCz8IuQ&index=22

this information was much better

Glad you liked it, happy learning 🙂

pictures used in the contents aren\’t clearly visible

You can click on it to enlarge and see them properly.

okay, Thank you for the info 🙂

Sure, happy learning 🙂

Yes, may be. but I am not able to find its release date, any idea where to find it?

I think most ARs will be published towards end of May.

Thank you for your reply 🙂 I have asked my query in your previous reply

yes I understand that we are in 2024-25 financial year and it is the problem that I am not able find its release date. But I am looking for AR for 2023-24. Could you please let me know where I can find its release date or where to find on which date company is going to release their annual report?

Chances are the AR is not published yet?

correction for 1st sentence –

Why do companies write 2022-23 in their annual report for Financial year 2023? It should be written as 2023-24 right because it is from April’23 to March’24?

FY2022-2023 AR will be punished in 2023 right? Also pls see my previous reply.

sorry for basic question-

Why do companies write 2022-23 in their annual report? It should be written as 2023-24 right because it is from April\’23 to March\’24?

For example – Google says TCS released its on 15th April but in the annual report it is mentioned as Integrated Annual Report 2022-23. Also TCS have not added there Annual report in pdf format it is in kind of website format which is quite confusing while learning.

Please let me know, waiting for reply.

In India, the financial year is between 1st April to 31st March. So as of today we are in FY 2024 – 2025 and the previous FY was 2023-2024.

typo mistake- in the example of CRISIL- the loss of company is 300CR which is 1000-700, used + sign instead of – sign

Ah, let me check this, thanks Pranav.

Should you always look at consolidated financials or are there cases wherein looking at the standalone figures might make more sense. For example, Mahindra owns tech mahindra, m&m and mahindra financials. In such a case where the subsidiaries are in different sectors wont it make more sense to look at the standalone figures

If the company is small (unike RIL where there are 300 subsidiaries), then you can look at standalone numbers. Else Consolidated works.

Hi, just wondering if there is an optimum number of stocks one should have in their portfolio. Also is there an optimum number of stocks one must invest in, in any particular sector of choice. Thank you

Check this – https://zerodha.com/varsity/chapter/hedging-futures/

I think all research points to about 20-25 stocks across at least 5-8 sectors.

good explaination

Thanks a lot karthik.It cant get more simplified ,Very much grateful to you🙏🙏

Happy learning, Durgesh!

The PDF that can be downloaded isnt having table of contents. Can you please update it ?

Sure. Alternatively, you can con convert the content as a PDF from the browser I guess 🙂

What does it mean when the Independent Auditor Report says, \”following companies have unfavourable remarks, qualification or adverse remarks given by respective auditors\” about the subsidiaries of a company? Does this mean that the governance of the parent company itself is in question and its better to stay away? Came across these kind of reports for 2 companies recently.

Thanks.

Yes, it means the company under consideration should be evaluated carefully, including the subsidiaries.

sir i have downloaded the annual report of 22-23 it consist of 172 pages we cant cover all the information in the md&a could you suggest us important information and the information we can ignore in md&a

Maybe you can try this – https://www.arsummary.com/

Hey Karthik

This website isn\’t working. Any other trustable website to get the summary?

Do check this – https://www.tijorifinance.com/ideas-dashboard/

only a person with 99% knowlege should come here for that remaining 1%

Greate Information. Nice way of teaching

Happy learning!

Sir, as You know there are little information available on microcaps. I did some digging into the AR of one of those. I found the Management analysis and discussion section the worst, hardly 1 page. They didn\’t even spend time to elaborate. Obviously concalls won\’t be available. So I dug into credit rating reports and some info on valuepickr. Then visited the company\’s website. Some of the companies look extremely undervalued given the cash flows and fundamentals, but lack of information is a problem. Could you suggest me something that I can look into in addition to these to get more information in these situations? Thanks.

I get your point. The best possible way is to figure out what their competition has to say. If that also does not help, then secondary research like industry data etc will help.

Sir/Madam,

I am clear with \”Share Capital\”, could you pls explain it

Check this Prakash, have explained here – https://www.youtube.com/watch?v=iH3ODZ5PYU4

Just now watched your whole video on Annual Report you made on youtube a long time ago. Well made sir. I have 3 questions.

1. Is there anything you would do to quick check the integrity of the audit itself. Like it failed in the case of Satyam. I\’m currently focusing on learning account forensics, so this would really help.

2. In TA side, is 50 DMA a good indicator for making sell decisions if I find that the company\’s story is not intact.

3. Could you point out to a good book or source that helps in making sell decisions. I actually find this more challenging.

Thank You.

1) So far, I just go with the repute of the company doing the audit. But I\’d love to dig more and identify landmines.

2) Yes, you can use that. Best to combine both TA and FA here and not just TA

3) No book dedicated to just this topic. At least, i cant think of one 🙂

Is this information updated sir. I see comments from 2014. By the way very good information

Comments keep pouring in, Krish. Also, understanding of the company\’s AR remains the same across time 🙂

You can also check this – https://www.youtube.com/watch?v=8rUc0MaMzik&list=PLX2SHiKfualFGenPFh2onjzsh8TeprEmU

Thanks again man

If only my teachers at school would explain in such way

Happy learning, Basim!

Thanks a lot for that clarification. Just completed your personal finance and mutual funds module. Never thought analyzing a mutual fund should be based on so many factors. Very well written. Wish there was a certificate test for this.

Thanks for the kind words, Sathish. I hope you continue learning on Varsity. We will soon add Varsity certification here-Varsity certified please do keep an eye out.

1. But when I did a basic account forensic check like contingent liabilities as a % of networth, EBITDA – CFO convertion, Auditor\’s fees increase etc, most of the companies passed. They are fundamentally strong based on financial statements. Valuation is good. But the only thing is that promoters are part of these committees although not the chair person. So is that enough of a red flag to stay away despite other things looking decent?

2. In case of a broking business contingent liabilities as a % of networth will be higher given the nature of the business due to huge bank guarantees for margins. So should I not look at this criteria for a broking business or is it still relevant?

Thanks Sir.

1) It is common in India for promoters to be a part of these committees, especially in smaller companies. Dont discard the company just on this one factor. Dig deeper.

2) You should. By the way, the BG business will reduce going forward in the broking business.

I see many companies, especially small caps, having promoter in their audit committee, Nomination and renumeration committee and risk management committee which I guess is a red flag. But what about directors? Norms say(if I\’m not wrong) that 2/3rd should be independent. Could you clarify as to how exactly we need to analyze this aspect briefly? Thanks Sir.

Yes, you should pay a lot of attention to these things and see if there are any red flags in corporate governance. In the Indian context, getting a sense of good corporate governance is super important.

Thanks brother 💜

Happy learning!

580*

Hi, let\’s assume CRISIL holds a 60% stake in Irevna. So, in that case, the net loss of CRISIL is = (1000) + 60% of 700 = (1000)+ 420 = 560. So in this case net loss in the consolidated statement of CRISIL will be 560 Cr. Am I right in assuming this?

Yes, that right.

Everything at one place .Thank you so much.🙏🏽

Happy learning 🙂

Hey Karthik,

Hope you are doing well. I would like to appreciate your efforts towards educating India to world of Finance. Thank You.

Question :

While going through an Annual Report, if i have this information:

Ratio to median remuneration of employees : 10.03,

The median salary at global level of employment is : 11,73,300

how do i calculate this person\’s salary?

Thanks in advance.

Not sure how once can do that, Awanish. You can only get the company\’s average and maybe median salary. But that information will not be of much use in my opinion.

Kharab Ipad tha isliya Abhi tak nhi diya

Even in 2022, Karthik Sir\’s Varsity helping the newcomers in a great way with good examples. Thank you, Sir… நன்றி.

Happy learning, Vijay 🙂

Great article.

A topic I have dreaded to learn due to its sheer size and complex jargons.

Thanks for breaking it down and explaining it so well.

I\’m glad you found the topic helpful and early to understand. Happy learning 🙂

Sir,today everyone is considered about pitrioski score for investing in stocks.does it is reliable?

Cant comment, as I\’ve never used it myself for investing.

Not sure if companies can hide some facts in annual reports e.g. showing wrong profits, order pipelines ? If no then who are the validating authorities for annual reports ?

The auditors sign off the company\’s financial statements, so at least the company\’s financials can be trusted unless the auditor is also involved. But That said, other things in the annual report are basis what the company says.

Thank you very much for the chapters and I think anyone can understand lessons easily.

Simple but powerful.

Happy learning, Jamshad.

How to get hard copy of annual report every year from a company?

You can write to them and request for a copy, provided you are the company\’s shareholder.

Thanks for such a wonderful content.

Simple and crisp.

Happy reading!

Hello Karthik. How do we get better at reading the management discussions and analysis to figure out which company is actually worth investing in? Won\’t all companies talk optimistically about their company? As mentioned, we could use quantitative analysis to figure it out, but in terms of qualitative analysis, how do we know if a company is good. Does it come through practice? Please let me know. Thank you.

Tejas, the only way to get better is by reading as many MD&A as possible. One specific trick that helped me is to read peer ARs. For example, if I\’m dealing with BAjaj Auto, I\’ll also read TVS and Hero\’s AR to get a perspective.

Hey Karthik,

Great content and thanks for spreading the knowledge.

Any plans to release Varsity web application. It is sometimes cumbersome to use mobile app to read huge content. Humble request to release the web application.

Thanks and Regards,

Raghu

Thanks Raghu. No plans for a dedicated web app. But will pass this a a feedback to the team.

amazing explaination. i am new to fundamental analysis, this module was very helpful.

Glad you find the module helpful, happy learning 🙂

The graphic at the beginning is really cute (and apt).

Thanks, Saket. I\’ll let the illustrator know 🙂

Sir how can one do stock picking. Which stocks should be choosen for evaluation, how will it be decided??

I\’d suggest you read this module to get an understanding of that Surya 🙂

Great content! Thanks for sharing your knowledge in such a good way

Happy learning, Karan!

great initiative sir.

Happy learning!

very nice & informative

Happy learning!

Hi, can you please tell me where I can find in the investments made by the company in AGM report

Please see the investment section in the Balance sheet and then the associated notes.

These is the best content I ever read relating to capital market

Happy reading, Priya!

Anyone getting profits in stock market?

I m the beginner

With. Your ans I can decide

I can proceed in market or not

If*

In company A owns 20% of company B(less that 50% so B is not a subsidiary of A ), will the profits(numbers) of B be reflected in company A\’s consolidated numbers?

\” Along with the extracts, the company can also include a few financial ratios calculated by the company itself.The reason for looking at this section briefly is that, I would anyway calculate these and many other ratios myself\”

So my question is, if the ratios are already given by the company why would you calculate them again?

It later says \”while I do so, I would gain greater clarity on the company and its numbers.\” Could you please explain How you gain clarity by doing so?

Companies dont give out all the ratios, you will have to calculate these yourself. When you do so, you may as well calculate the ratios that\’s given by the company as well. When you do so you can be doubly sure about things like taking numbers from consolidated financials.

Like how many shares they offered to public and how many shares public has subscribed .

Yeah, I have no idea, need to check this myself 🙂

Thanks…karthik

But I didn\’t find on any website..I tried to find \’ history of Amara Raja IPO \’ but didn\’t get any clue on google.

Can you share that page or link where you could able to find it .

Regards

Shubhika

I need to Google it myself 🙂

Sir the last screenshot of financial statement show the difference between issued capital and subscribed capital .

That difference is wondering me. It means public have not fully subscribed the capital of the company

Isn\’t it a negative point of the company

As company offer a shares to the public and haven\’t subscribed it fully by public .

If we check balance sheet of 2020 -21 still it unsubscribed.

Help me on this to understand

Yes, at the point of its IPO, the shares were not fully subscribed, hence the difference between issued and subscribed. This will continue to reflect in the BS 🙂

Your writings make life easy. Simple and easy to understand.

Happy learning, Sachin!

I liked it to much. We also need to explain terminology of annual report

Yup, hopefully, this chapter helps.

Thanks a lot man. Reading it at 3 in night love the way you wrote it .Hats off.

Happy reading!

Great work. loved the simplicity of all the modules.

Happy learning, Aryan!

Will I get a notification if someone replies me?

Not really, you will have to check it manually.

Hi Karthik, quick question – what news apps do you follow to stay abreast of current developments?

Pulse – https://pulse.zerodha.com/

Can you please darken the paragraph text? It\’s a little difficult to read.

Hmm, not sure if that can be done.

I am very happy to see comment sections still being monitored. Good to know that our queries will be answered. Just one thing. A financial report runs 100s of pages. How can one read that for every company? And if one finds the company not good(Which is a good thing) his time and effort are gone and he has to start again with another company. Isn\’t it like finding a needle in a haystack?. So can one really invest well without reading all the 100s of pages, while having his daily job to do?

I understand, Kamal. People usually follow a top-down approach, as in analysing the sector, identify the companies within the sector and then shortlist 2-3 companies based on broader numbers. Weekend reading is good enough in my opinion.

Sir, your writing imparts well-needed simplicity to these complex concepts.

Happy reading, Himanshi 🙂

Request to change the link for the annual report. As of 2021, the link does not lead to the report page.

New link is https://www.amararajabatteries.com/Investors/annual-reports/

Thanks, Jay. Will do that.

thank you for this wonderfull content….waiting for more fundamental analysis content…

The module is complete but will add a Financial modelling module sometime this year.

Thank you so much for explaining in such simple terms. Mr. Kartik and entire Zerodha Varsity team deserve a loud applause. Even the most difficult topics have been made simple. I regret that i could not read this 2 years earlier. My financial literacy would have been different. Keep on writing.Your efforts are making a difference in our lives.

Happy reading, Doc! Glad you liked the content 🙂

Wow!! Great course made note of every point. Reading it in 2021- I am a budding investor 😊 this is really helpful. Much better than the paid content circulating on YouTube and other platforms

Thanks much!

Happy to note that, Nagasri 🙂 Hope you enjoy reading the content!

The explanation was excellent. Easy for a beginner to understand it ! Great work ..!

Good luck, Siva!

Sir how much time should one spend reading annual report

Time does not matter as long as you get all the information 🙂

plz any tell me how to find out interest rate on percentage for the stock

Sorry, I dint get that.

Your modules are so simple to understand and encourage to learn more. Hope to continue on a profit journey here on.

Happy learning, Radha!

The annual report isn\’t accessible from the link anymore. Can you update the link?

Yeah, I guess the company has changed the link. Can you please google for the annual report?

The link to Annual Report of Amara Raja Batteries Limited is not working and it redirects us to the main website of Amara Raja. can somebody please help?

Please google for Amara Raja Annual report, you will be directed to the right link.

Hi Karthik, You mentioned that One needs to read atleast last 3-5 years of AR\’s before investing. So while doing so, do I need to read MD&A, director\’s statement form all the AR\’s? or do I only need to read MD&A from the recent annual report?

Yes, that will help you understand the company and its business better.

valuable lessons

Sir, I was going through the annual report (2018-19) of LIC and want to know which one is consolidated/standalone financial statement out of

1. \”Financial Statement (Segmental)\” and

2. \”CAPITAL REDEMPTION (INCLUDING ANNUITY CERTAIN) INSURANCE BUSINESS\”

in the pic?

Link for the pic: https://i.ibb.co/4ZKwq6s/lic.png

According to my understanding 1. will give information about the company\’s financials(consolidated) and 2. will give information about its insurance business alone.

1) This seems like segment-wise P&L

2) Not sure about this

Before the financial statement, the company will explicitly mention that the financials are consolidated.

good evening sir Ji

A few questions regarding this article

1- you have mentioned the use of \”tijori finance\” and \”screener\” in the comments sections

Isn\’t \”Tickertape\” better than these both and also a subsidiary of zerodha?

2-as mentioned in this chapter that crisil is 51% owned by S&P so now if crisil makes 100 crore profit,

so does 51 crore of total profit generated go to S&P?

thank you😊

Tickertape is good as well. Its just that the other two are free to use.

That depends on the profit share/royalty arrangement between the two companies.

i couldn\’t

find amar raja\’s annual report on its site as well through the link you have given

I guess ARBL would have changed/updated the site.

thanks a lot for sharing this information

Happy reading, Tarun!

Hi karthik, Do i need to read everything in management discussion and analysis(MD&A)? Considering ITC it has 78 pages of MD&A. Do i need to study everything or do i need to skim through it?

You can skim through it. Most of it will be subtle marketing but do read between the lines and look at the fine print. It usually provides valuable insights not just on the company but also about the industry 🙂

Was simple and easy to understand. Thanks so much!!

Happy reading!

Thanks Karthick, hoping to get some good news soon 🙂

Hi Karthick,

Just a Suggestion, I see the Varsity in the playstore and I believe you are providing certificates if a module is completed over the App. I presume that content is almost the same in both Varsity app and varsity web, but I don\’t see any options to get certificates in Varsity web. I am a kind of person who is comfortable reading through big screen (laptop, compute) rather than in Mobile, I believe most people will be just like me. If you could set Quizzes in the end of every module and provide certificates the readers will be more motivated to learn. Thanks

Thanks for the feedback. We are actually thinking of doing something better with regard to certification. Ironing out the details. Hopefully, we should have something soon.

Doubt:

If I find that some companies are going to perform well, I will simply invest by buying their shares.

But, if I think that some companies will not perform well ahead, should I invest by making a sell order?

No, you can simply avoid buying these companies.

Hi Karthik

I have a query regarding the financial statements of the companies.

There are various online sites such as tijorifinance and screener where the financial numbers are a bit different then the ones which are mentioned in the annual reports of the companies. Is this a small margin which we can overlook or is it always recommended to look into the annual reports and make the excel sheets from their although that would be time consuming. What would you suggest?

Thanks!!!!

I prefer to take the numbers directly from AR and do the excel work. But if it is for a quick and dirty calculation, I rely on one of these two sits. They are more or less accurate.

Even after considering only FINANCIAL HIGHLIGHTS, THE MANAGEMENT STATEMENT,MANAGEMENT DISCUSSION AND ANALYSIS. We still have around 30 pages out of ~100. Do we need to study all the matter present or Still there is a need to eliminate some matter?

What you need is MD&D, Director\’s report, and Consolidated financials. Everything else is a good add on.

Hi Karthik,

Usually AR range any where between 100-300 pages. When going through AR how can a Newbie filter out required data and eliminate unwanted publicity by the company. Simply asking how can a person decides what is useful and what is not and skip it?

Thats exactly what I\’ve highlighted in this chapter. You can also check this video – https://www.youtube.com/watch?v=fTIOzRPOXsk

Great example for the differentiation between standalone and consolidated basis! Thank you so much sir!

I\’m glad you could relate to it, Mohit.

Do every investor is entitled to get a hard physical copy of the annual report?if yes how to get it.

Yes, but now you can just download the AR from the company\’s website.

Thank you.

Hello Mr. Karthik,

Wonderful explanation, shows the effort gone in making this notes.

Can we get the fundamental data in excel format?

Thanks!

You can check sites like screener or Tijori, they may provide an excel download option.

Hello sir,

Here you said that they will show in the AR.

For example, if I am reading through a manufacturing company annual report, I would be particularly interested in the human resources report to understand if the company has any labor issues. If there are serious signs of labor issues then it could potentially lead to the factory being shut down, which is not good for the company’s shareholders.

But I think so the company will not disclose such things in his report.

What you say sir?

They are supposed to highlight the same in AR, especially the manufacturing companies.

Hello Karthik,

I have been referring varsity for quite sometime. I must appreciate the hard work you have put into this study material. You paid attention to details nevertheless made sure it doesn\’t get too theoretical and monotonous. Awesome piece of work !! Thanks much for everything!

what is long-form.EBITDA, EBIT, PAT.?

Earning Before Interest, Tax, Depreciation, and amortization.

Earning Before Interest, Tax.

Profit After-tax.

https://bankermind.com/biggest-stockbrokers-in-india/

this website show Zerodha is no.1 broker in India….. It is true?

Nice explanation sir.Sir do we use only TA for trading or FA is also used. Kindly tell me because I want to start trading ASAP I completed the TA module now should I start trading or complete all the other modules then paper trading. And at last actual trading.

THANK YOU.

FA is great from making investments, while TA is good for taking trading positions. I\’d suggest you paper trade for a while until you get the necessary confidence to trade in real markets.

I would really like to appreciate the way things have been explained , So simple and yet powerful. A layman can easily understand this. Hats off to the writer.

Happy to note that, Ranjeet 🙂

Thanks a lot.

The post really meant and helpful for beginners like me. I am still learning stock picking and stock analysis by using free services of

https://ticker.finology.in/ and money control but I want to know how good and helpful is their premium plan offerings. Any help would be greatly appreciated.

I\’ve never really used a premium service, so cant comment 🙂

Good morning karthik…… While reading this varsity I came to know that this was written in 2014…….so I didnt post any comments… Coz i thought I won\’t get reply…. But recently in previous chapters I saw comments with replies 😍…. Even after so many years u r following it…. Thanks for that…. It will help many new beginners……..

Back to the topic…

In this chapter u have taught… How to read annual report….. But how will we conclude that this is this good annual report or not to investigate further or not to invest??

Thank you 😊

We make it a point to answer as many queries as possible on a daily basis 🙂

Generally speaking, after reading through the AR, you should not have any queries. Which means to say, all the information available to you must be detailed in the AR. This would make it a good AR 🙂

The table in page 21 (in pdf) is very different from the actual annual report i downloaded from the company website.

The heading are same but the content is different in both the tables under management\’s discussion and analysis.

Did they change it or what ???

Is it for the same year? They aren\’t supposed to change the contents/numbers, if they do, they usually do with a clarifiecation.

And for these above mentioned companies should I consider consolidated statements.

Yes, please.

Hi,

If I take the standalone statements do I get a good analysis or I have to go for consolidated statement.I didn\’t clearly understand as to which companies I have to consider consolidated statement as for tata motors there are many shareholding companies.Do I have to check the annual report of each shareholding companies. And for other companies like mahindra,maruti suzuki ,L&T and hero honda motors.

Sam, it is consolidated by default for all companies. Consolidated gives a better picture of the company\’s overall financial health.

I reading these chapters and I have some questions.

1. it\’s basic or advance level information in these chapters?

2. After completion of these chapters, I have to attend more classes or its sufficient to analyze a stock fundamentally?

This is fairly everything that you need to know, Roshan. Of course, you can build on this, it\’s entirely up to you. But this is good enough information for you to get started.

Really a nice initiative from Zerodha to educate newcomers and its users. I read this chapter and I found its very easy and simple wording and a nice way to educate people who want to learn it. it\’s from my heart, I salute the guy who wrote this article really a wonderful explanation.

Thanks for the kind words, Roshan. Happy reading 🙂

I\’m actually doing a financial analysis of selected automobile manufacturing companies in India.I\’ve taken tata motors as one company,should I consider standalone statement or consolidated statement as I am a new comer in finance.

Consolidated statements. Good luck with the analysis 🙂

http://www.amararaja.co.in/annual_reports.asp link doesnt redirect me to annual report.

They must have changed the URL, please look at the website > investor section.

Is the mandatory for all the companies to send me a hardcopy of the annual report on my request, if I own even 1 share in the company ?

Nope, not mandatory. They can email as well or make it available on the website from where you can download.

Explained in simple words.. Thank you !

Happy reading!

Really great. Everything is in it.

Thanks! Happy reading 🙂

Hi Sir, what according to you is not published in Annual reports. What information about the company are you looking for which isnt there.

Thank you !

I think pretty much all details an investor need is present in the AR. If you are looking for information beyond what\’s available in the AR, then maybe you are over analysing a company 🙂

extremly usefull content

Happy reading!

Hi Sir,

I have couple of doubts regarding reporting

1. Do companies publish Quarterly reports. If yes where can we find them

2. For e.g. if a company\’s overall liabilities have increased, can we also check where have they used the additional funds as in which projects etc.

1) Companies publish only P&L data on a quarterly basis

2) Yes, but this will be made available yearly, in their annual report

>such a woderful read\’, I really liked it<

Are these annual reports standard across the world or is this format (P&L statement, CF, and Balance sheet) only specific to India. I was going through the annual report of one U.S. company but I could not find any schedules with breakup of the various components under the P&L statement. Also I could not find the Cash Flow statement as well, there were other financial documents however.

Nope, this is specific to India. The US has a different format of publishing the AR. However, financial statements are similar. You can find the associated notes in the supporting documents I guess filed with the SEC.

Sir, Very Nice Explanation. Time and again I feel it should be in Video Format. I couldn\’t download annual report of Amara raj Batteries. It Takes me to the website, but there is no investor column. Please Help. Even in NSE website, i couldn\’t get annual report.

Thanks in advance.

I think the company has changed its site. Check this – https://www.amararajabatteries.com/Investors/annual-reports/

Hey Karthik,

Thanks for so much Information on AR

As you have mentioned going through Management Discussion & Analysis is important and there is a ton of information in it, Since I\’m new to investing, I\’d like to ask, is it important to take notes for MD&A and compare them with other Companies of Same sector,

And can u suggest where exactly we need to take notes, Since I can\’t remember all the information on an Annual Report

Anirudhh, comparing MD&A of two different companies in the same sector is a golden practice, suggest you do that 😉

The link has been changed to below:

https://www.amararajabatteries.com/Files/AnnualGeneralMeetingFiles/2013/Annual-Report-2013-14.pdf

Thanks for the update, will get this changed.

[…] How to Read the Annual Report of a Company […]

The link of AR of the Amara Raja batteries (http://www.amararaja.co.in/annual_reports.asp) is no more available kindly provide some other example.

Thanks

They must have changed the URL, I\’d suggest you look up on their site. The technique remains the same irrespective of the example.

I have never read something this good, So much content to understand yet so short. Great work!!

Happy to note that, Vinay! Glad you liked the content 🙂

Hey Karthik,

I was going through INOX leisure\’s Annual report, it had the management discussion and analysis report but didn;t have the Management Statement

So…….?

And also what are \’executive directors\’ ?

Executive Directors are full-time employees of the firm who also have decision making a role in the company.

Karthik could you please suggest me a book or something from where I can get to know the structure of a company like directors chairman ceo and all that.

I think any basic business book should help you with this. Maybe 1st year MBA finance books?

That is ok, few companies combine it within MD&A.

I want annual report of skdrdp

Suggest you check their website >>> investor section.

Could you recommend me books that would provide me with further details on fundamental analysis

I\’d suggest Securities Analysis by Graham.

Hi sir

Where can I see employees are holding their company\’s share or not?

I can\’t found in annual report shareholding pattern section .

If the holdings are less than 1%, then you will not know. Shareholdings higher than 1% will be disclosed to exchanges and will appear in the quarterly shareholding statement.

sir, why there is some difference between the closing amount of a year and the opening amount of next year

example if there is 2000 in 31st march 2016 then in next year it will show 1800 or 2100?

Thats the amount added or utilized during the year. The notes will have the details.

Hi sir,

I would really like to connect with you and discuss my investment ideas with you. I\’m a young, passionate and curious student who is extremely fond of investments and would be grateful to have an opportunity to speak to you.

Revant, I\’m not sure of if I can devote time to individual queries/investment ideas. However, I can certainly help you with learning related to the subject. Please do feel free to ask however ever queries you have here, on this platform. Thanks.

Can we check the annual report of Banks also?

Yes, you certainly can.

As a Learner, This is the Best Platform for Learning the whole market and its strategy, your explanation strategy is also unique.

Thank you so much for providing this material.

May God Bless you, sir.

Thanks for the kind words, Pratik. Happy learning 😉

Can you share any link or discuss on \”Accounting policies\” – where to get the data and how it manipulates?

I think being completely aware of how balance sheet works (explained in this module), will help you deal with this.

Can we replace annual report from stockreport+ by zerodha??

Nope, Stockreport+ is not really a replacement for the annual report.

So what are the actual use of stockreport+, Then it is worthless ??

Well, if it was worthless, why would TR deploy so much resource 🙂

Check this to know more – https://www.youtube.com/watch?v=ct5IkGcJNtc&t=334s

Sir you have mentioned that a shareholder can get a Hardcopy of the Annual Report by contacting the company. I have mailed the company\’s investor\’s relations to send me a copy of the same. I haven\’t heard from them and its been more than a month. What do you suggest I do?

Sundeep, if you are not too particular about the hard copy, then you can download the softcopy from their website. Look for it under the investor section. Thanks.

Thanks for sharing so much important information about the AR.

Good luck, Lokesh. Happy reading 🙂

Good………..

Very good…….

Excellent…………..

Super…………………….

Thanks, Suraj 🙂

Hello sir,

You have explained things wonderfully! It\’s commendable.

My question is related to the example quoted by you above where in S&P held 51% stake in CRISIL. Now, if S&P or let\’s say Mc graw hill generate the AR, will they also include whole of the 700cr profit in their AR considering the fact that CRISIL is not a 100% subsidiary of any of them?

Thanks for the kind words, Ankit. Yes, they will have to report this in AR.

Sir, can u post a article on how to read a annual report of Insurance companies. Thank u.

I\’ll try and do that, Karthik.

Hello,

Sir, why there is difference between the value of financial data of 2017 (in balance sheet of 2018), and financial data of actual 2017 balance sheet. For example in 2018 balance sheet, the financial data of 2017 shows total Assets of 1,16,094 Lakhs, but in actual previous year annual report, financial data of 2017 shows assets of 78,866 lakhs. Why there is difference and which numbers should we consider?

Sometime, the management may want to restate the numbers. For this reason, I always look at the current year AR to look at the previous year\’s number.

Fundamental analysis not so easy its all about which positive points we could figured out from balance sheet & directors speech.

Yes, it takes some effort to learn FA 🙂

I am not able to find AR(Annual reports) of AMARA RAJA Company. Can you again share the link or an Excel or word file. So that we can connect properly with this>??

Waiting for your reply.

Beginner!

P.S.

The link you shared in this chapter is not working.

Ah, can you visit their site and look for it in the investors\’ section? Thanks.

You can download the report from here – http://www.amararaja.co.in/annual_reports.asp

404 – File or directory not found.

The resource you are looking for might have been removed, had its name changed, or is temporarily unavailable.

After clicking on the link you provided sir, above written line is coming.

Ah, let me check Manish. Meanwhile, I\’d suggest you check directly on the company\’s website.

Hi Sir,

It\’s Just Amazing to read this Lessons I m thoroughly enjoying it\’s written in so easy to language that a Layman like me can also Understand it.

I have a small Request sir Could u plz add a chapter for \”How to read the AR of the BFSI companies\” and the important ratios to watch out.

Thank you.

Thanks for the kind words, Rajdeep 🙂

I\’ll try and put up a chapter on it.

Hi sir

1 .is related party transactions is one type of expense ? If yes then where is show in profit n loss statement ?

2.this type of transaction of done from reserve n surplus balance ?

I see only in annual report but not in balance sheet or P& L statement

Give explanation in detail

1) This will be mentioned separately in the annual report, Amit. You cannot differentiate this by looking at the financial statements

2) From the regular income. Like I said, this information is no included in the financial statement.

Hi Karthik,

Varsity is a gem among the stock market information sites, with simple as well as clear in depth info.

Thanks for sharing the info.

Glad you liked it, Shankaran. Happy learning!

Hi sir

Where can I find a management\’s commentary which release every quarterly results ?

And what\’s its title if it\’s available in its website ?

Visit the Investor\’s section on the website of the company you wish to track. Within this section, you can find the Quarterly results. The quarterly results contain various things like P&L, management view etc. Here is the link for Infy – https://www.infosys.com/investors/reports-filings/Pages/index.aspx#quarterly

Hi Sir ,

Thanks for your articles .Your articles are pure gold .

In qualitative aspects I know what to analyse but I don\’t how to analyse .

For eg. I know I should check management\’s background but i don\’t know what to check in management\’s background

Here are a couple of things –

1) Check if their past experience – indicates if they deserve to be where they are

2) Check for compensation – are they drawing more than what is fair practice

3) Their Lifestyle – remember Suzlon/Kingfisher

4) Other directorships/ownerships

I\’d suggest you check the latter chapters in this module for more insights.

Thanks a lot sir

I have read all the modules altleast two times. It is pure gold.

Varsity takes a nursery student to PhD level.

Thanks for the kind words, Jasdeep 🙂

Good luck!

Hi Sir,

Thank you for varsity!!

Awesome articles ever I loved reading.

Good luck and happy reading, Santosh 🙂

Awesome content.sir.1question sir.there are thousands of companies there.where can I find which company is doing well???.and which news and magazines can I read to have better knowledge about investing.thank u sir

Its best if you start using a screener for this. You can give your criteria and start filtering out stocks. Check out https://screener.smallcase.com/welcome (paid version) and https://www.screener.in/ (free version). Good luck.

So in the example of CRISIL owning 100% of IREVNA, which statement would actually affect the share price of CRISIL; the standalone one, or the consolidated one??

The consolidated one.

DO U HAVE E BOOK FOR THIS WHOLE TOPICS OR IN PDF TO TAKE A PRINTOUT , IT WILL BE BETTER TO STUDY.

The PDF is available for you to download at the end of this page – https://zerodha.com/varsity/module/fundamental-analysis/

Hi Sir,

Very informative article.

I have a question, where does a company declare its quarterly result first?

I mean for example, suppose TCS is going to declare its quarterly result, then where do they announce their result at very first?

On their websites they post the result after sometime of announcement, so where do they actually announce result first.

Thank you!

Regards,

Vikram

They send the results first to the exchanges and then update the same on their websites. Some even hold a press meet to discuss the results.

Hi,

Thanks for replying and clearing the doubt.

Regards,

Vikram

Welcome, Vikram.

Hello Nitin here!

First i would like to thank for such information described in simple manner.

Pls share more more information helpful for every one..

What sort of information are you looking at, Nitin?

Hi,

First of all, a heart felt thanks for the wonderful and lucid article on FA. I was into this FA since 1 year and have tried lot of books and websites (paid as well). However, i can\’t remember any one of them even trying to match with the work done here.

Simply, hats off.

However, my question, out of the thousands of companies, how do we chose one for FA. I have seen an answer to this as selecting from a screener website (screener.in). Also you said you mentioned about the filter by end of the module. Apoligies, but i could not get this.

Can you please help us on this as well on how to pick a company first? May be i missed the filter, can you please enlighten?

Once again, thanks for the wonderful article.

By filter, I mean a site like screener. You can always start with an industry that looks interesting to you and then selecting companies that fit your criteria. For example, if you like tyre manufacturers as an industry, then look for companies within it – this will narrow down your search from few thousands to few handful of companies.

Hey Karthik,

I work as an Equity Research Analyst in an IB. You statement on consolidated v/s standalone caught my eye.

\”I personally prefer to look through the consolidated financial statements as it gives a better representation of the company’s financial position.\”

Umm, as an Analyst, I infact screen the PnL of a company while calculating many ratios so that it doesn\’t include the effects of inorganic growth like earnings from its subsidiaries, inorganic earnings due to foreign currency appreciation, one-time earnings and other non-recurring earnings etc.. I usually exclude them and in many cases scale them down so as to reduce the impact of such inorganic growth parameters on the parent company I am analyzing and that is the norm kinda followed across IBs.

Shouldn\’t we infact and exclude (or scale down) the impact of subsidiaries from the consolidated financial statements? Shouldn\’t the core business of a company be analyzed since core operating earnings are the ones we use to value the company using FCFF or FCFE DCF method 🙂

Amit, perhaps I should have worded this better. Here is another way to look at this – If the company is focused one couple of verticals and has a few products, then chances are that its standalone FS is pretty much consolidated. So in a sense, by taking in the consolidated, you are also accounting for the residual value. Now, if the company is large enough to derive significant value from other subsidiaries (Coromandel and EID come to my mind), then maybe it does make sense to value it on an overall basis.

I understand your argument, but I guess the market, at the end of the day values the business in its entirety.

Hi Karthik,

Thanks for enlightening it furthur :). Makes sense. I just graduated from b school and have joined this IB. Apologies if what I said was naive or not appropriate. Just entered this field. Happy to learn more from a professional like you and looking forward to learn from other varsity modules as well. Many thanks for these modules!

Hey Amit, no apologies here 🙂

Your opinion is as good as mine. Good luck and I hope you have a glorious career ahead!

When looking at the financials for a subsidiary company, should I also factor in the financials of it\’s parent company? Let\’s say- the subsidiary has been incurring losses in last 2 FY but parent company had impressive figures in their income statement. In this scenario, parent company most likely will rescue it\’s subsidiary.

Yes, you certainly have to consider the parent company\’s financials.

Alright, thanks!

Cheers!

Hi Kartik,

Your content is simply amazing for a new investor. Can you comment on the below strategy

1. Doing deep FA on stocks under 100rs and keep investing in them ?

2. Keep yourself limited to Nifty 50 and invest according to TA ?

1) Doing deep FA is good, but why do you want to restrict it to stocks under 100? The value can be anywhere, could be in a 100 Rupee stock or a 1000 Rupee stock

2) Stick to Nifty 50 for trading

Hiii

What is exact related party transactions?

Is that amounts is subtract from revenue or add in revenue ??

Please describe in detail .

Company A paying out Company B (which is closely related to Company A)…or the other way round….. is termed as related party transaction.

Ya but if company A is paying out to company B then how can calculate this amount ? Is that minus from company A profit or something else ?

You will find a separate section in the Annual Report meant for Related party transactions, I\’d suggest you please do have a look at it.

Hi

Thank you for posting a nice info in simple language .

I have following question

1. How can I know the chairman ,MD ,promoters past records like involved in bribery ,crime etc ? And their life style ?

2. \’Related party transactions\’ and salary of MD ,chairman ,directors where can I find in annual reports of company ?

1) I usually take the help of Google. Type the promoters make plus scam and Google will throw up results

2) Look for the related party transactions in the Annual report.

What is shareholder equity?

Shareholder equity = Reserves & Surplus + Share Capital. This is also called the net worth of the promoters.

Hi,

Let me first express my thanks for sharing this info in a very simple and easy way.

My question is

Its very important to read and understand Management Statement’ and ‘Management Discussion & Analysis. The Mgmt might mislead and put a better picture forward which is not actually there or conceal vital information. How do we validate this.

True, that is very much possible. Hence, it\’s important to read this MD&A of a competing company as well. Companies with similar business landscape will have similar business challenges…and this comparison will help in understanding if the company is misleading or not.

In this case I need to check every fund that if any of those had purchased particular company .but practically it is difficult.

I agree, hence this is best does as a once in a quarter task.

Hi Sir

Where can I find that when mutual fund bought the shares of particular company? For example particular company bought reliance shares in the month of jan_2017 .Where can I get this details.

The fund house itself updates this information on the fund\’s fact sheet, this is available on the website of the fund.

Not sure if you are looking for this..it gives insight of which mutual funds owns a particular stock

https://www.valueresearchonline.com/funds/comres.asp

You can use Coin as well – https://coin.zerodha.com/

Hi karthik

could you please share this excel sheet if possible

Sure, will try and upload this. Thanks.

Hi sir

could you please share the financial calculation excel sheet ?which you have shown in below u tube training

https://www.youtube.com/watch?v=fTIOzRPOXsk

Hi Karthick

It is pretty good artical

I would like to know below detail

Where can I get the sector details? for example which sectors are performing well now and which are not performing well in the current year?

Which sectors will be good and not good in the year ahead ?

Could you please tell few websites wherein I can know these details.

You can look at the sectoral charts to get an update on the overall sector performance. This is a fair indication of how things are moving in the sector.

Hi Karthick

Thanks for reply.

Where can I get sectoral performance details?

Any website are there to indicate sectoral performance?

Check this – https://www.nseindia.com/products/content/equities/indices/indices.htm

Thanks for useful update .

Thanks to zerodha Team.

Cheers! Happy learning.

Hi Sir,

In case of consolidated and standalone financial statement, if a holding company is making a loss and subsidiary is making profit such that the consolidated statement is ends in profit, doesn\’t that mean the holding company is not performing well?In this case if we look at the consolidated statement and if it looks attractive (profitable- only because of subsidiary company) ,then can we invest in holding company? Or instead we should invest in subsidiary? or neither of both?

Hi Sir,

Kindly answer clarify my doubt.

Sorry, I seem to have missed your query. You can choose to invest in the subsidiary. However, I really don\’t think it would matter especially if the holding company has no other investments. I can think of Coramandel Fertilizers and EID Parry as an example here.

The annual reports of only last 5 years are available in NSE website. Where can one find the reports since the beginning of the company sir ?

Check on the company\’s website itself, the annual report will be under the investor\’s section.

Sir that\’s what I thought too. I was researching company called NATCO Pharma. Looks like it was listed in 1995. But even in the company\’s website I couldn\’t find the annual reports before 20011-12. Can you please help look into it and help me? Thanks in advance.

Here is what I found – http://www.bseindia.com/stock-share-price/stockreach_annualreports.aspx?scripcode=524816&expandable=0

How can we get the quarterly result publishing date of all the companies listed in stock exchange?

You will have to keep a tab on the company. The dates can vary across companies.

Usually when quarterly result gets published the share price changes accordingly. In this case how can we benefit from reading the annual report?

In case of Quarterly results, you need to be in a position to understand the quarterly numbers keeping the numbers stated in the AR in perspective.

Dear Karthik. Hats off to your efforts in bringing an article so easy to understand on how to read an AR.

I am deciding to invest my money in equity but I see so many companies with good financials that I couldn\’t finalize where to invest in.

I am 23 years, working in a PSU and very much interested in personal finance. It was Zerodha only from where I took entry in share market, a place where money can me made at the highest rate possible in current scenario with heavy risk. I lost some money during initial days in day trading and then I realized it is very important to gain substantial knowledge in this field to save the capital. Then I saw VARSITY!! I fell in love with it when I read it just for the first time. I have committed to myself without adequate learning, I won\’t swim down. Thanks for helping me in my process of being a good swimmer!!

Vicky, I\’m so happy to hear this!

Like they say, the only edge in the stock market is you \’Knowledge\’. So stay committed, work heard, and learn! I\’m sure markets will reward you for it 🙂

Good luck, stay profitable.

dear karthick sir,

can u explain the things mentioned in note number 2, how the value is 178.0 something

Ah, note 2 is talking about the share capital, which is basically core to the share holder\’s equity. Gives you information on authorized capital, issued, subscribed capital etc.

CRISIL making 1000cr losses!!! CRISIL is fundamentally very strong.The hypothetical example was way too much :). Thanks for yet another lovely chapter.

Cheers! Glad you liked the chapter 🙂

can we have a chapter on valuation of companies pls?

We already have that covered – https://zerodha.com/varsity/chapter/dcf-primer/

beautifully explained, hatsoff

Cheers!

Why is issued share capital more than the paid-up capital?

Are all paid up shares also issued shares?

Most likely.

Where does the money raised from series-A and series-B funding add up? Does it add up in the issued share capital or paid-up capital or neither??

Where does the money raised from series-A and series-B funding add up? Does it add up in the issued share capital or paid-up capital or neither?

Issued.

In the last snapshot, how is the subscribed capital more than the issued capital?

No, its not.

Articles are good. I am going through it one by one. Are you having downloadable ebook. As I am new to market I have started to read this articles as per index. But I feel it is better to learn first fundamental then technical. You should have given fundamental topics first and technical articles afterwards. What you think, I am correct or I should understand first technical analysis first.

Once again thanks for providing this easy to understand and assisting to gain the knowledge of market.

It\’s all online Sunil, you can choose to read FA first and then TA. It does not make any difference in my opinion 🙂

Happy learning.

Hi there ,

What is Indian equivalent of SEC filings in the US. I ask because in US , AR are jazzed up compared to SEC filings. Please advise.

Nothing as of now, we just depend on the AR.

Hi Karthik

Is there a place where we can find the exact time of the result release. Every website only publishes the date but not the time of release.

Not sure if this is reported anywhere.

So, we keep looking at the stock price for break-out, confirming the results 😉 ?

Something like that 🙂

Hi Karthik Sir,

Awesome articles. I have never found any article about Fundamental Analysis of such simplicity. Thank you very much for your effort.

I have one question. How can I make sure whether the management of a company of my interest is good enough to sustain the growth of that company?

Thanks for the kind words!

Estimating the management is the most difficult thing to do, no straight solution for this 🙂

Nice very informative

Cheers!

What will be some good reading material to follow to study and know about companies for Fundamental Analysis ?

You are at the right place to learn about FA. Start here and follow up with companies Annual Report.

Ok. Thanks Karthik. Will the company\’s annual report be enough to learn about the company..?

Yes, much more than enough 🙂

Properly written ..Will definitely go through all of the topics…

Thank you for all these efforts…

Welcome! Happy reading.