It’s the economy, stupid! A ₹2,100 billion bonus

We love India Data Hub’s weekly newsletter, ‘This Week in Data’, which neatly wraps up all major macro data stories for the week. We love it so much, in fact, that we’ve taken it upon ourselves to create a simple, digestible version of their newsletter for those of you that don’t like econ-speak. Think of us as a cover band, reproducing their ideas in our own style. Attribute all insights, here, to India Data Hub. All mistakes, of course, are our own.

Payday!

₹2,100 billion.

That’s the over-sized, unexpected dividend the RBI will be forking over to the Central Government this year. I know, I know, the Government always deals in such big numbers that it’s hard to appreciate just how big any one number is. For context, though: the total amount of money the Union Government expected to earn this year from all sources – including the taxes that you and I pay – was ₹30,802 billion.

So that’s a surprise bonus of ~7%. Not too shabby, huh?

This mega-dividend is almost two-and-a-half times what the RBI sent over last year.

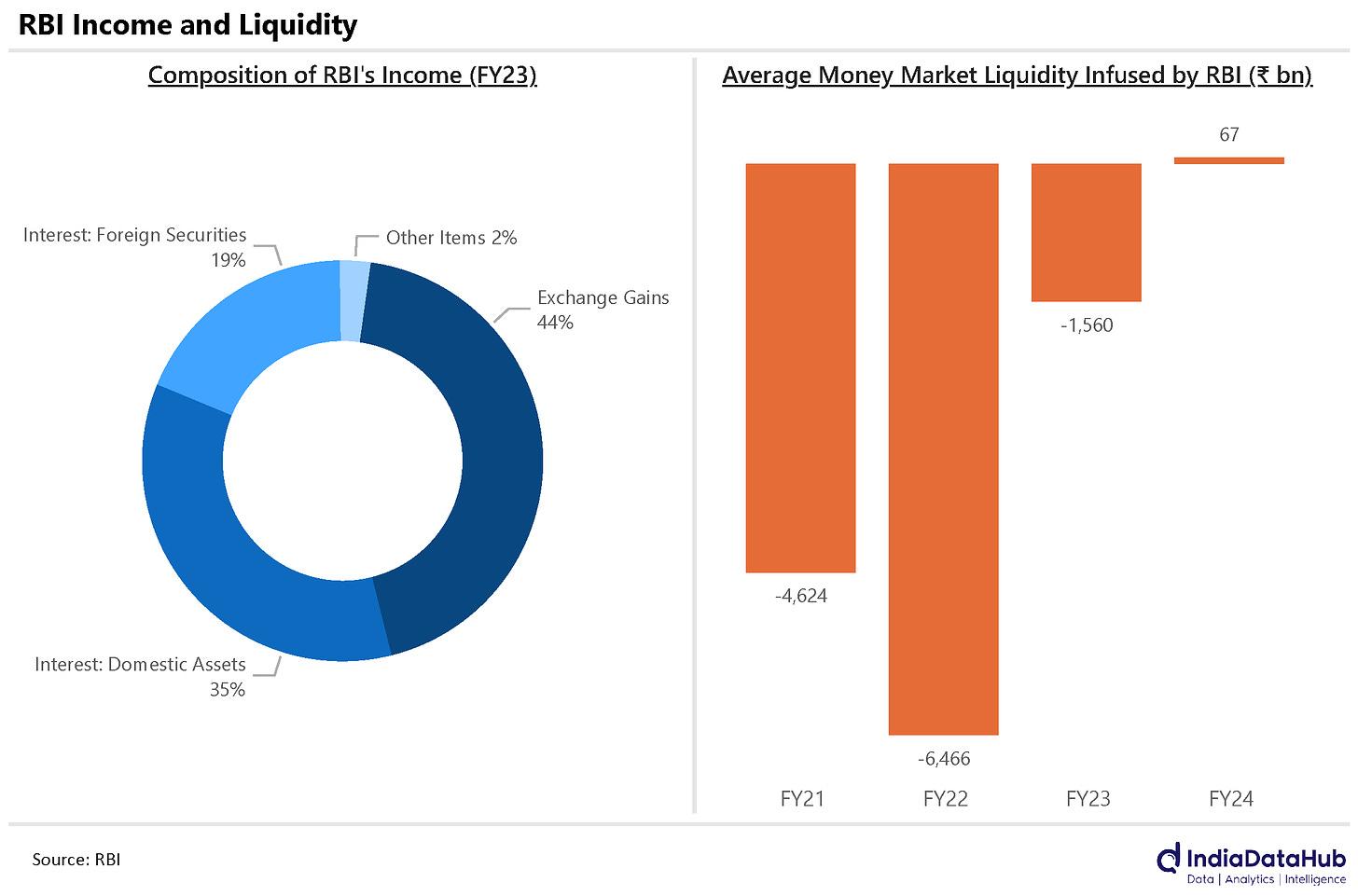

Why so? We’re not sure: the RBI is yet to release its accounts for the last financial year. But the good folks at India Data Hub have a theory. And that is: RBI stopped paying interest and even started earning some.

See, for three years between FY 2021 and 2023, there was too much money in our economy. The RBI spent these years “absorbing liquidity” – or, in simpler words, borrowing lots of money from the banks so that they could give less of it to other people. This was important to keep inflation down, but it also meant the RBI had to pay out interest to banks.

Then, in FY 2024, things changed. The RBI stopped pulling money out of the economy. In fact, it actually started ‘infusing’ liquidity – which is, it gave loans out to banks and pocketed the interest. Not too much, just ₹67 billion. But that’s quite a dramatic reversal nonetheless, as the graph below tells you.

Of course, that doesn’t account for all of the ₹2,100 billion. The RBI probably also made a lot of money selling its foreign exchange reserves through the financial year. To over-simplify things, if the RBI bought 100 US Dollars in 2019 for ₹7,000, they’d sell for ~₹8,300 now, because of how the dollar has appreciated against the Rupee. That’s a neat ₹1,300 in profit for the RBI. Of course, the RBI doesn’t sell its foreign reserves in order to earn an income – but that’s nevertheless how the money appears in its books. Last year, these ‘exchange gains’ were the largest source of the RBI’s income.

The RBI’s mega-dividend gives the Government quite some space to play with its expenditures. You’ll probably see this accounted for in the revised budget that will be presented before the next Lok Sabha in July.

How big is its impact? Well, the Government expected to receive a total dividend of ₹1,000 billion from all banks and financial institutions put together through this year. The RBI alone has now exceeded twice that figure. That’s a lot of money to get as a surprise.

A bad year for foreign investment

FY 2024 has been a bad year for Foreign Direct Investment in India. If you’re wondering what that is, by the way, we’ve written about it before:

…You put in serious money for the long haul. You see a country as a good place to do business, and so, you roll up your sleeves and dive in. You buy up a big piece of a company, or if you’re very brave, you start a business from scratch, and then get involved in running it. This is ‘foreign direct investment’ (FDI).

December last year marked the first time, since the RBI started keeping track in 2011, that India had lost more FDI than it received. Now, though, that’s become somewhat common. A net of US$ 4 billion in FDI left the country this March, for instance.

A lot of the money that has come into India over the last decade is being ‘repatriated,’ as investors sell off their investments and take their returns back to their home countries. In March, investors took out US$ 6 billion from India. All in all, over the financial year, a record US$ 44 billion in investor money returned to source countries. It’s the highest amount that’s ever been repatriated from India – jumping up by 50% from FY 2023.

Meanwhile, the amount of investment India received hasn’t risen. If you subtract what was sent back from it, on the balance, in FY 2024, India got just US$ 10 billion in foreign investment. That’s the least net FDI we’ve had in a decade, falling 60% from last year.

That’s that for declining investment. There’s another rather curious sense in which India is losing FDI money, though. And that is: Indian entities are investing a lot abroad! In March, Indian companies made investments of US$ 3.8 billion abroad. That’s the highest we’ve ever recorded.

In total, Indian companies invested US$ 16 billion abroad in FY 2024. That’s a good figure – it’s up 15% from a year ago. It isn’t unprecedented, however. In fact, it’s actually down 10% from our outbound investment in FY 2022.

Swades(?)

Though foreign investments are stalling, the March quarter saw record NRI deposit inflows.

The month of March saw the highest net inflows for any month since the ‘taper tantrum’ of November 2013. Back then, the US Fed essentially announced that it would stop printing money, and bond investors threw a massive hissy-fit, which was felt across the world. It set off a period of sudden volatility for the Rupee, to counter which, the RBI had permitted Indian banks to take in deposits from NRIs.

NRIs deposited US$ 2.9 billion more in India than they withdrew in March. Across the quarter, they deposited a net of US$ 5.4 billion in India – the highest since June 2015.

Inflation, around the world

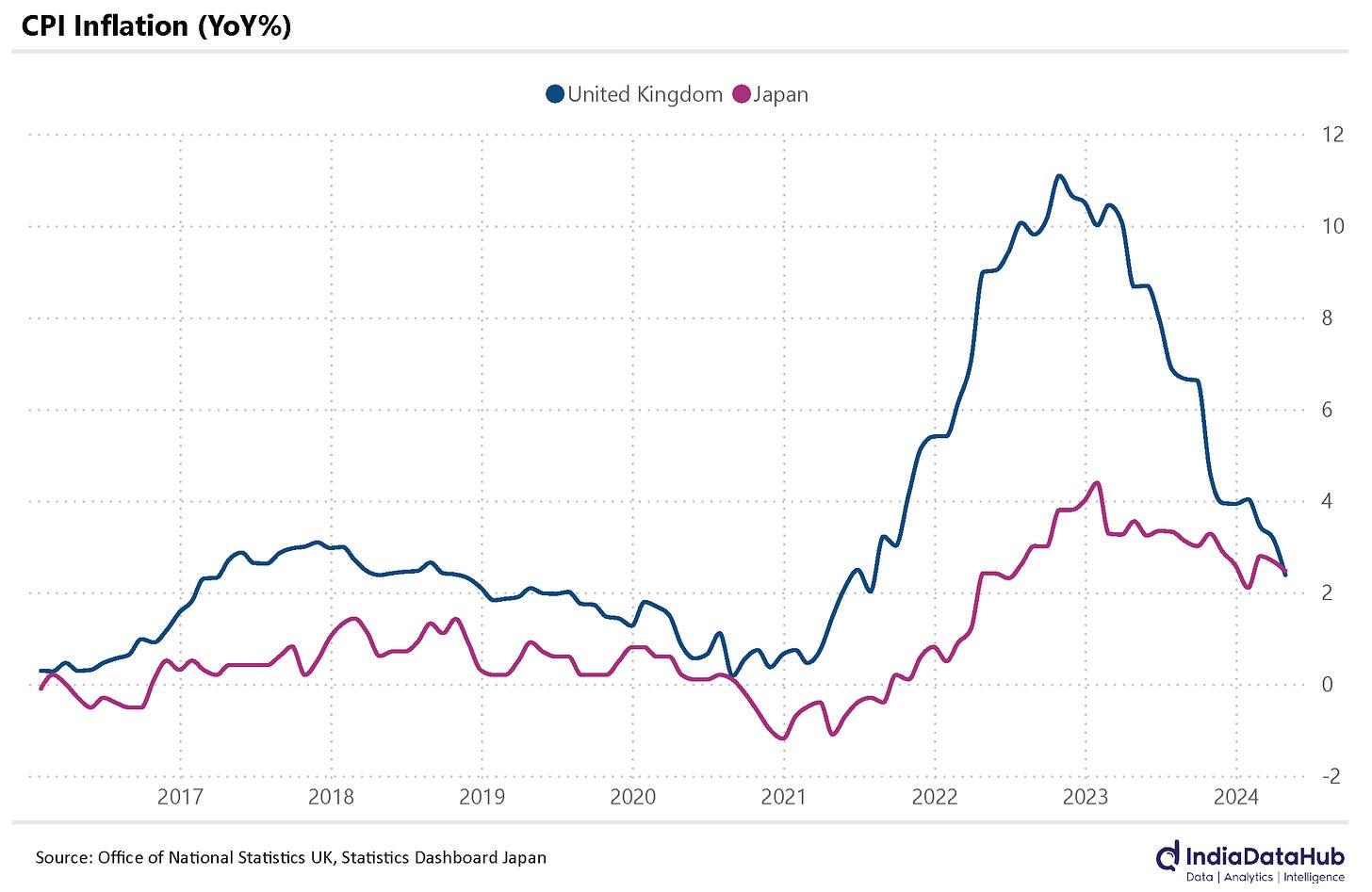

If you know one thing about Japan’s monetary situation, it is this: Japan has ridiculously low inflation. Here’s some news, though: the UK’s inflation reading for March came in under that for Japan! That’s unthinkable.

Last month, the UK registered a 33-month low inflation rate of 2.4%, falling 0.8% from March’s 3.2%. It was helped along by deflation in the price of goods by 0.8%, compared to March last year. UK’s goods prices, in fact, fell for the first time since February 2021. In contrast, Japan had an inflation rate of 2.5% – marginally higher than the UK.

Meanwhile, at the deep end of the inflation pool, Turkey’s inflation refuses to come down. In April, it saw inflation of 70% year-on-year. That’s not a typo. Seventy per cent.

Turkey’s Central Bank has kept its policy rate at 50%. Sounds bad, doesn’t it? If you borrow 100 Lira in Turkey today, you’ll have to pay more than 150 Lira back just next year. But the funny thing (or it would have been so, if it weren’t distressing) is that those 150 Lira would be worth 88 of today’s Liras, as things are going. In a way, then, it’s a profitable proposition to borrow Turkish money, even at usurious rates.

That’s all for the week, folks! Thanks for reading.