Coin newsletter #3: Starting troubles

Wishing you all a Happy and prosperous Diwali🪔 from all of us here at team Zerodha!

This post got a little big because we wanted to cover some basic yet extremely important personal finance concepts. This was the first post that we wanted to write but there was so much other crazy stuff happening in the markets that we had to address that first. If you missed reading the previous issues of this newsletter, you can check them out here.

Whenever you ask someone for some investing advice, the most common piece of advice you’ll hear is start now, start early or some variation of it. There’s nothing wrong with it. If you can start investing early, it’s an incredible advantage because you can save more.

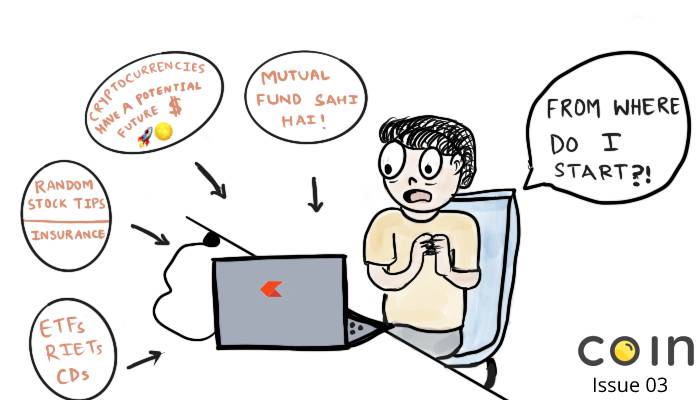

But just telling people to start investing early is not enough because everyone knows this at some level. Despite that, if only a handful of people invest, that means there are other problems. There are too many, in fact, but I want to talk about one of the big ones.

There’s never been a better time to be an investor. You can invest in pretty much all asset classes globally. You can invest in stocks, ETFs, bonds, REITs for free on Zerodha. In the early 2000s, brokers used to charge ~1% brokerage. Some brokers still charge about 0.50%. Today, you can invest in direct mutual funds for free without paying commissions; there were no direct plans until 2013. There are some amazing tools and platforms like Tickertape, Varsity, and ValueResearch, all of which are free.

Despite all these advantages, there’s never been a harder time to invest. There are too many choices, and there’s too much noise. We assume that more choice is always good. Our brains certainly tell us so. But the reality is, beyond a certain point, more choices are bad. Our brains are lying to us.

The thing is, our brains aren’t built to handle all these choices. Think about the 1000s of choices we have to make every day, our brains unconsciously make most of these choices. This is an evolutionary shortcut we humans figured out. If we had to choose and decide every small thing consciously, our brains would explode.

Psychologist and Professor Barry Schwartz call this the paradox of choice in a book by the same title. He says that more choice doesn’t always make us happy, in fact, it makes us anxious and miserable.

Learning to choose is hard. Learning to choose well is harder. And learning to choose well in a world of unlimited possibilities is harder still, perhaps too hard. – Barry Schwartz

In the US, companies offer retirement accounts called 401K plans to employees. A part of the employee’s salary is automatically invested, similar to India’s National Pension System (NPS). In 401K accounts, employees have the option to choose the funds and asset classes they want to invest in.

Sheena Iyengar, Gur Huberman, and Wei Jiang, professors at Columbia University, analyzed the retirement accounts of 793,794 people across different employers. They wanted to see how investors would behave when presented with various fund choices in 401K accounts.

What they found was surprising. In 401k plans that only had 2 fund choices, they found that 75% of employees saved for retirement. But when the number of funds increased to over 50, only 60% of employees were saving. They clearly showed more choices, beyond a point aren’t good for people. They give up and do nothing and numerous other studies show the same.

It’s the same with personal finance content—crores of blogs, books, videos and podcasts. There’s so much information today that, frankly, it’s a nightmare. There are over 1500 mutual fund schemes. Then regular, direct, growth, dividend plans, exit loads, etc. Say you somehow manage to pick a mutual fund. There are some 150+ health insurance plans, 30+ term insurance and plans and 1000s of other ULIPs, endowment policies and lakhs of bank relationship managers (RMs) and insurance agents trying to mis-sell them to you.

People starting their personal finance journeys today have to go through this jungle and not lose their minds. All these choices and noise are the biggest reasons why most people who can invest do nothing and keep money in their savings bank account.

There’s a psychological explanation for this. We’re all loss-averse—losses hurt twice as much as gains. When we have to deal with so much choice, our brains start to think, what if I choose wrong and lose money? So, most people end up:

- Doing nothing and just putting money in a saving account.

- Do something random.

- Rely on defaults like recommended mutual funds on a platform, best-performing funds from lists, asking friends for recommendations, listening to bank RMs etc.

- Rarely, people choose to delegate, like hire an advisor, for example.

Choice overload scares most people into inaction because they’re afraid of making the wrong choice and regretting it. But it’s not such a big problem that it takes a PhD to figure things out.

The New York Times asked a bunch of brilliant people for some tips on how people could manage their personal finances that can fit an index card. Here are the rules of Scott Adams, the creator of Dilbert. He had also written about these rules in his book Dilbert and the Way of the Weasel. Apparently, he wanted to publish this as a 1-page book, but no publisher agreed.

Just take a look at the 8 tips, they are so simple that even people with little knowledge of personal finance can start implementing them:

https://twitter.com/nytimesbusiness/status/685472978147082240?s=20

Let’s break down the list because these tips were written in the American context:

- You need to have a will. It’s a legal document that explains what happens to your assets in the case of your death.

- Avoid credit card debt. Even today, most people don’t realize that the annual interest rate on credit cards can be between 20-40%. Swiping is easy, but it’s damn costly.

- Get a term insurance policy. A term policy pays out in case of your death. It’s super important to have one if you have dependents. Along with a term policy, it’s important to have health insurance for you and your family members. The Ditto guys explain this in the second half of this post.

- IRAs and SEPs are retirement accounts in the US. Retirement is the ultimate goal we all save for and mutual funds are perfect for this.

- Buy a house only if you can afford it. Don’t borrow too much.

- You can face emergencies anytime, and you’ll need liquid cash in such situations. It’s important to keep X months of expenses in cash that’s readily accessible. A liquid fund or an overnight fund is perfect for this. How much to keep? Read this build Mutual Fund Portfolio chapter in varsity.

- Most people think picking the “right fund” is important, but to be honest, it’s the least important thing in your personal finance journey. All that matters at the end of the day is if you have enough money to fulfil your goals. Constantly trying to pick the best funds and best managers is a waste of time for most people and is a costly distraction. It’s perfectly possible to achieve your goals with market returns by investing in index ETFs or index funds with a reasonable asset allocation. Moreover, 70-80% of active funds don’t beat index funds. Here’s more about index ETFs and index funds.

- If you don’t want to do all this, you can always hire a good financial advisor to help you with all this. There are two fee models that advisors follow:

1. Fee-only: Here, advisors charge a % of your assets (AUM). For example, if you have Rs 10 lakhs in investments and if an advisor charges 1% of AUM, then Rs 10,000 is the advisory fee. It keeps growing as your assets grow.

2Flat-fee: In this model, advisors charge a fixed fee every year regardless of the AUM. - This one is from me. Don’t forget to add nominees to your account, it makes life easier for your loved ones in the case of your demise. You can add nominees to your account online.

Now, if you, like me, were intimidated by all things when starting, I want you to pause for a second and think about these 9 tips. They aren’t complicated at all. They are simple rules that cover most of the important financial aspects.

Do these rules cover everything? Of course not, but that’s not the point. You can waste your time doing nothing or get started with these rules, which cover 70-80% of things and then figure out the other things later by going through the Personal Finance Module on Zerodha Varsity. There’s an old quote that’s quite apt here:

“Don’t let perfect be the enemy of good”

How to protect yourself and your loved ones?

This post id=”insurance”> is by folks at Ditto (by Finshots). Given that insurance can be quite complicated and it’s heavily mis-sold, they are working on simplifying insurance for people like you and me. All the nightmares over the past year have taught us how important insurance can be. Speaking from experience, If not for health insurance, my own personal nightmares would’ve been a whole lot worse this year. So this advice is really timely.

Most people in this country live on a tight budget. They don’t have a large savings corpus. They don’t have an emergency fund. They don’t have a lot to fall back on. Even those with better financial security are wholly unprepared to deal with the odd curveball life throws at you.

But this isn’t their fault per se. If anything, this isn’t a fault at all. People shouldn’t spend every waking minute of their life thinking of all the possible things that could go wrong. And they shouldn’t be living in a constant state of worry and panic. It would be a sorry way to live. Having said that, however, to throw all caution to the wind wouldn’t be prudent either. As any good driver would argue:

Eyes firmly planted on the street but for the occasional glance at the rearview mirror.

You too would do well, to check the rearview mirror every once in a while.

When a family friend passed away recently, he left a grand total of 4 lakhs in savings. This was a loving, intelligent man who deeply cared about his family. And by all measures acutely aware of his mortality. Yet, for all his noble attributes, he had no insurance. He didn’t have a large saving corpus and his family now has to face the daunting prospect of carving a livelihood without the sole breadwinner. It is truly inexplicable.

For about Rs. 15,000 a year, he could have left his family close to Rs. 1.5 crore. If he had only considered buying a term insurance product. Yet, he didn’t and knowing him, I can write with some conviction that this will probably be his biggest regret.

The point of this story isn’t to scare you. And it most certainly isn’t to induce terror. In all likelihood, you will live beyond the age of 60. You will see your kids grow and your grandchildren too. But probabilities only tell you half the story. They don’t tell you what happens “if” and “when” you die. That narrative, while uncomfortable, is all too real for you to ignore. For most people reading this, paying Rs. 15,000 a year isn’t really a herculean task. It’s a small cost to bear for a lifetime’s worth of protection. So if you have dependents, there’s a very strong case for you to consider a term insurance product right now.

The other thing that can completely cripple you is a trip to the hospital. It can drain you physically. It can drain you mentally. And it can drain you financially. The prospect of healing from physical and mental trauma is already daunting as is. But to deal with a massive financial burden as you’re recovering from a debilitating illness can be devastating. Some would argue that this is an isolated experience. That the government aids individuals who truly need the money. However, reality tells a very different story. Two-thirds of all medical costs are borne by individuals in their personal capacity. In some areas, it can be as high as 90%. You don’t get a lot of help from outside and even when you do, you have to work really hard for it.

In most cases, a single hospitalization can wipe out years of saving. In other cases, it can push people into a debt trap. And it’s not just the hospitalization you have to worry about. Oftentimes, you’ll have to contend with a whole host of diagnostic exams before doctors can figure out what’s wrong. Post-hospitalization, you’ll have to contend with medication costs. Modern treatments meanwhile are really expensive and medical inflation usually peaks at 7–8% each year.

If your employer already offers you a health insurance plan, you already have a head start. But if you don’t think that that plan is good enough to cover all exigencies, then you should definitely consider buying a health insurance plan for you and your family. And if you are still not sure how to go about things, we have a whole host of explainers at Ditto. We are hoping it’ll set many things straight. If you have other queries, you can talk to us directly.

On Zerodha Educate

This bull run in the markets has made investors happy, scared and confused at the same time. So we caught up with Kalpen Parekh (MD & CEO) and Sahil Kapoor (Head of Products) of DSP Mutual Fund) to talk about what’s happening in the markets, Indian and global economy, inflation, asset allocation, investor behaviour, debt funds in a low return environment and a whole lot more. This was super fun, hope you enjoy the conversation too.

https://open.spotify.com/episode/29vQHovgIEgZIMeDV9Fe1o?si=BRBwD1hzQ3SQEUdHJB4_cg

<

p data-selectable-paragraph=””>Hope you found this issue useful. We’d love to hear your thoughts, please do leave a comment below.

Sir,

I am looking for hierarchical nomination. That is when the first level nominee (100% allocation) also passed away along with the account holder, the second level nominee should be automatically allocated 100% allocation. We need such provision as sometimes, the entire family involve in accident or some other mishaps.

This kind of nomination is required nowadays.

Good

Yes this is Very Usefull

I also Accept this

content is helpfull but need more clarity on this

I accept with swathi

Who ever invest in bit coin this post will be very helpfull

yes this will be helpfull for starting traders

I have forgot mu user id and password

ggg

rtdt

p

I Love the News Letters! Reading all of them 🙂 . While reading i thought you are going to start Insurance division like coin for MF’s 😉

The artical of financial planning in the present situation is good, many many financial advisor are doing the job in that idea, I’m also sale this idea. But in this platform you advice our customers in direct purchasing the idea. I don’t like this because your platform Zerodha also commission or brokerage collect in your customers, and it is necessary your astavblishment run the journey. You also known that in our country more than 30 to 40 lack people directly do this job successfully and service the nation many yrs. In this world any kind of work that is called business. So any business without commission or brokerage is not possible. Artical direct idea is not possible in our present market aspect. Direct idea also get the brokerage.

Personal Financial Investment decision is the Most difficult one to make in everyone’s life. It’s very easy to advise others, but to practise the same, is really tough. Very sincere and honest approach by the author. At 60, I start loving Zerodha!’”>s

Personal Financial Investment decision is the Most difficult one to make in everyone’s life. It’s very easy to advise others, but to practise the same, is really tough. Very sincere and honest approach by the author. At 60, I start loving Zerodha!