Coin newsletter #2: Expectations, disappointments and regrets

There’s nothing new that you can say about investing. The basics – save more, spend less, diversify, keep costs low, and don’t tinker with your portfolio have remained the same for ages. It’s just that we have to find new ways to keep saying the same old things.

And since most of you are probably first-time investors, this is another post on the basics that you already know but ignore😜 This is the second issue of the newsletter, here’s the first one in case you missed it.

For supposedly being the smartest creatures in the known universe, we do some really silly things when investing. Things that would shock us if we reflect on them, which we conveniently choose not to😂

One of the big reasons investors stop their investments early is that they tend to have wrong expectations. Why? It’s an interesting question.

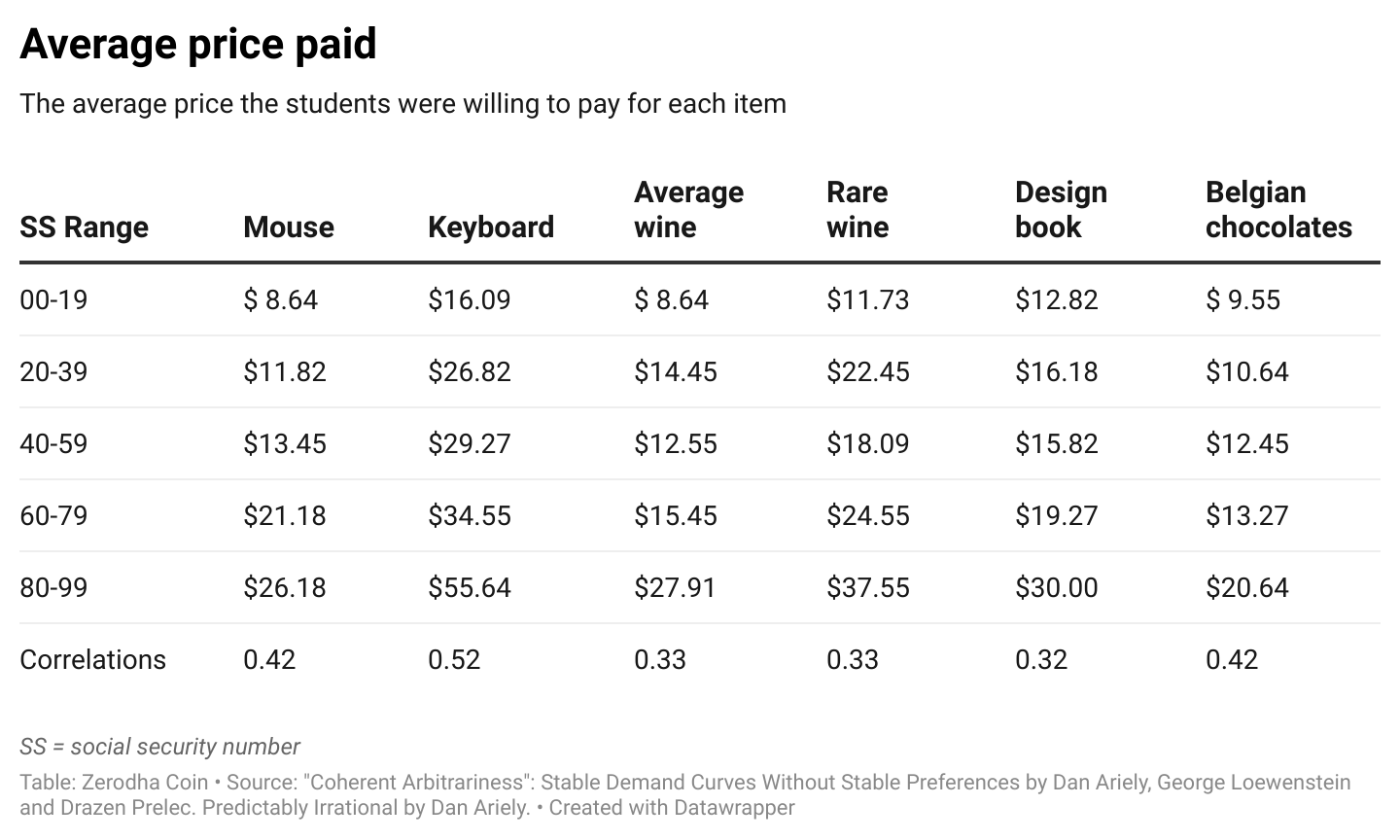

Dan Ariely, George Loewenstein and Drazen Prelec had conducted an interesting study with students at MIT Sloan School. They showed the students five items – a mouse, a keyboard, two bottles of wine, a design book and Belgian chocolates. They asked the students to write the last two digits of their social security number and the maximum amount they’d be willing to pay for the items on a piece of paper. Now, if you think logically, a student’s social security number should not affect how much they’d be willing to pay for something.

But we humans aren’t always logical. The results of the study were quite surprising. Students with lower last two digits in their social security numbers bid lower for all the items, and those with higher last two digits bid higher. Here are the results:

The willingness of the students to pay was influenced by the last 2 digits of their social security numbers.

When the researchers asked the students if writing the social security digits influenced their bids, they were quick to say, “no way!”.

Before you laugh this off as a funny study, here’s another experiment described in the book Thinking, Fast and Slow By Daniel Kahneman, one of the founding fathers of behavioural economics.

The power of random anchors has been demonstrated in some unsettling ways. German judges with an average of more than fifteen years of experience on the bench first read a description of a woman who had been caught shoplifting, then rolled a pair of dice that were loaded so every roll resulted in either a 3 or a 9. As soon as the dice came to a stop, the judges were asked whether they would sentence the woman to a term in prison greater or lesser, in months, than the number showing on the dice. Finally, the judges were instructed to specify the exact prison sentence they would give to the shoplifter. On average, those who had rolled a 9 said they would sentence her to 8 months; those who rolled a 3 said they would sentence her to 5 months; the anchoring effect was 50%.

This behaviour is called anchoring. It’s our tendency to rely on irrelevant numbers, first impressions and experiences when making decisions. Remember that expression “you only get one chance to make a first impression”; this is the reason behind it. There’s rich academic literature spanning decades that has shown the anchoring in various settings.

We all anchor to various things in investing as well. The most common example of this in the markets is when you ask people about their returns expectations over the long term. The most common answer is 15%+. Often, there’s no basis for their expectation; it’s mostly because that’s the most common answer you hear when you ask other investors about the returns you can expect from Indian equities.

You probably would’ve experienced this anchoring effect yourself. If you had bought a stock at Rs 100 and it falls to Rs 30, you’d probably think of selling if the stock goes back to Rs 100, which is now your anchor. Most investors thought that Nifty would go to zero in March 2020. Today, they think Nifty is going to the moon because of the initial anchor. This happens because we don’t adjust our anchors enough.

Ok, what does this have to do with investing?

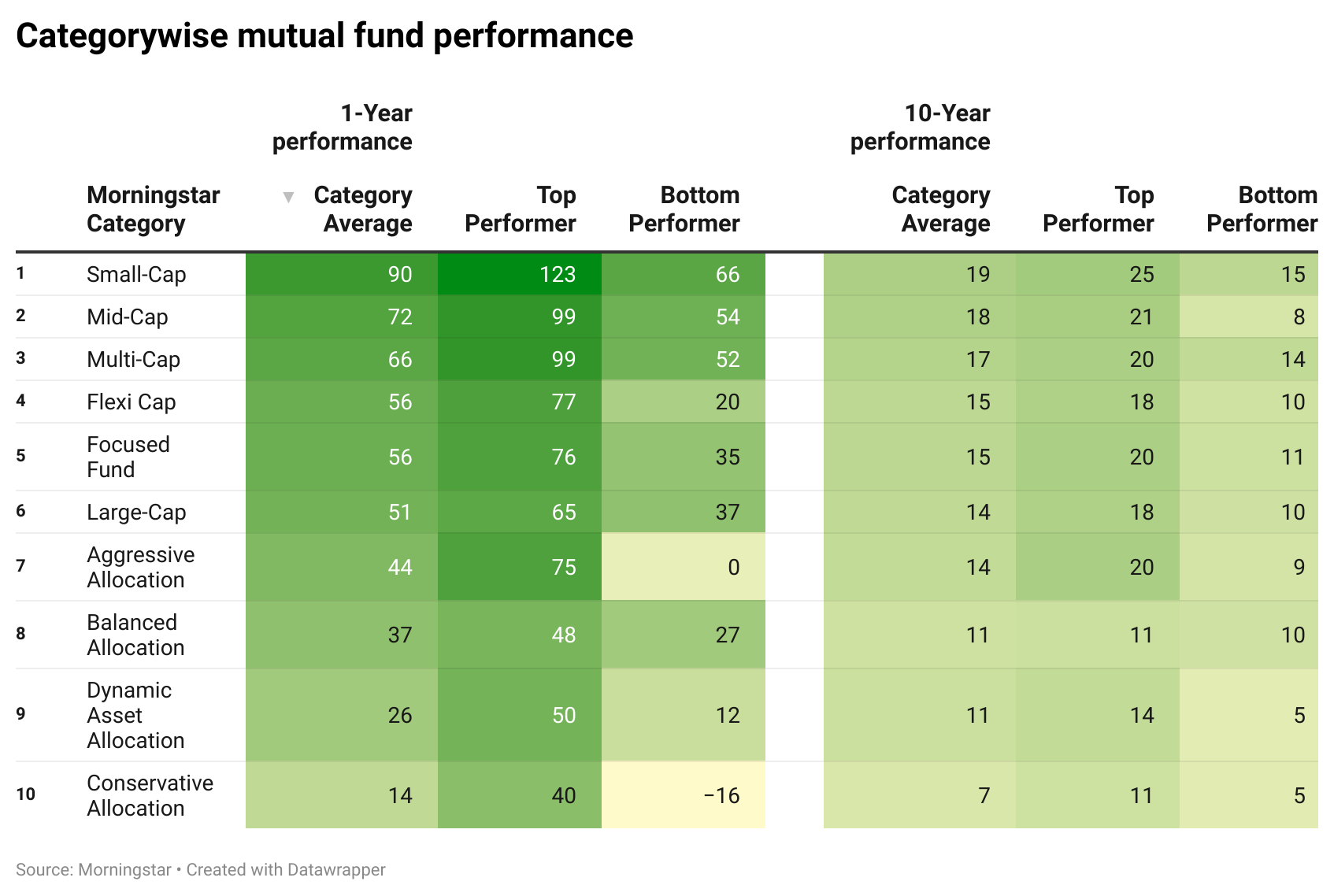

Take a look at the 1-year category returns for equity funds:

Categorywise mutual fund performance

The returns across categories are phenomenal. They are even more surprising considering that the markets recovered from one of the deepest corrections in history. The broad large, mid and smallcap indices were down between 35% to 40% in March 2020. On a side note, if you look at the difference between the top and bottom performers, you’ll also realize the importance and the difficulty of fund selection.

When things are this good, investors tend to become complacent. Most first time investors nowadays think that “stocks only go up”😐 Given that we all anchor and we’re prone to a lot of common biases like:

- Loss aversion: A 50% loss hurts twice as much as the joy of gaining 50%. This is also why we check our portfolio frequently, which is a terrible idea.

- Recency bias: Relying on the most recent information. In this case, thinking that the good returns in the present will continue.

- Confirmation bias: Seeking data or information consistent with our viewpoints and ignoring conflicting data.

- Overconfidence: Our tendency to overestimate our abilities. In the current bull market, this manifests itself in this form👇

Given all this, you now have a dangerous cocktail of behavioural quirks.

Just because we’re listing out biases doesn’t mean we’re flawed. Most conversations about investor behaviour quickly come to the conclusion that investors are stupid. It’s quite the opposite. As behavioural researcher Meir Statman says, “we’re all normal”.

Our biases aren’t a bug but rather a feature. All our biases have evolutionary origins. For example, as irrational as loss aversion might sound, that’s what helped our ancestors find their next meal, not get killed and ensure their line of descendants continued. The short term mattered, but the world has changed. The biases that helped us survive long ago aren’t suited for investing today, which is all about the long term.

So, how do you deal with these behavioural biases? A few things you can do:

- Always look at the data. In investing even 5-year returns can be noise. The first step is to zoom out over long periods and see how the markets have performed. If you look at the 10-year returns in the above image, you’ll see a much more sanguine picture.

- Have an investing process and automate it. This is where tools like SIPs help. It’s not a solution to everything, but it definitely helps. Similarly, if you have rules for your asset allocation, rebalancing etc., the odds of you making mistakes reduce. The lesser the discretion, the better it is. All you can do is control the process, not the outcome.

- Avoid noise. Unless you’re a trader or an investment professional, there’s very little use to constantly tracking what a fund or a stock is doing. Checking your portfolio occasionally and rebalancing annually is the best thing you can do. Rather than watching business news channels, you’re better off reading classic investing books.

- Don’t complicate things. Your brain wasn’t built for it. Keep things as simple as possible so that you can stick with your personal finance plan.

Having said that, writing is easier than doing it, but it’s not impossible. But here’s hoping🤞

Smallcaps blues

In August, smallcap investors had a mini freakout as the smallcap index fell about 9% before ending the month down by about 3%. The funny thing was that #Smallcap was also trending on Twitter for a while. Well, it’s funny only if you didn’t lose money😬

Nifty Smallcap 250

Things were a little scarier at an individual stock level. But still surprising given that since the market bottomed out in March, the Nifty smallcap 250 index is up 200%. The fall in August was barely 10%. This is a classic example of loss aversion like we just discussed above.

This shows a lot of smallcap investors might have misplaced expectations and that a lot of money has come into these funds post the run-up in the index, which isn’t surprising. Again, this is the anchoring effect at play. The price, NAV or index level at which investors started investing becomes an anchor and if the price falls below that, they freak out.

Everyone says smallcaps are risky, but that means nothing. So, how risky can smallcaps be?

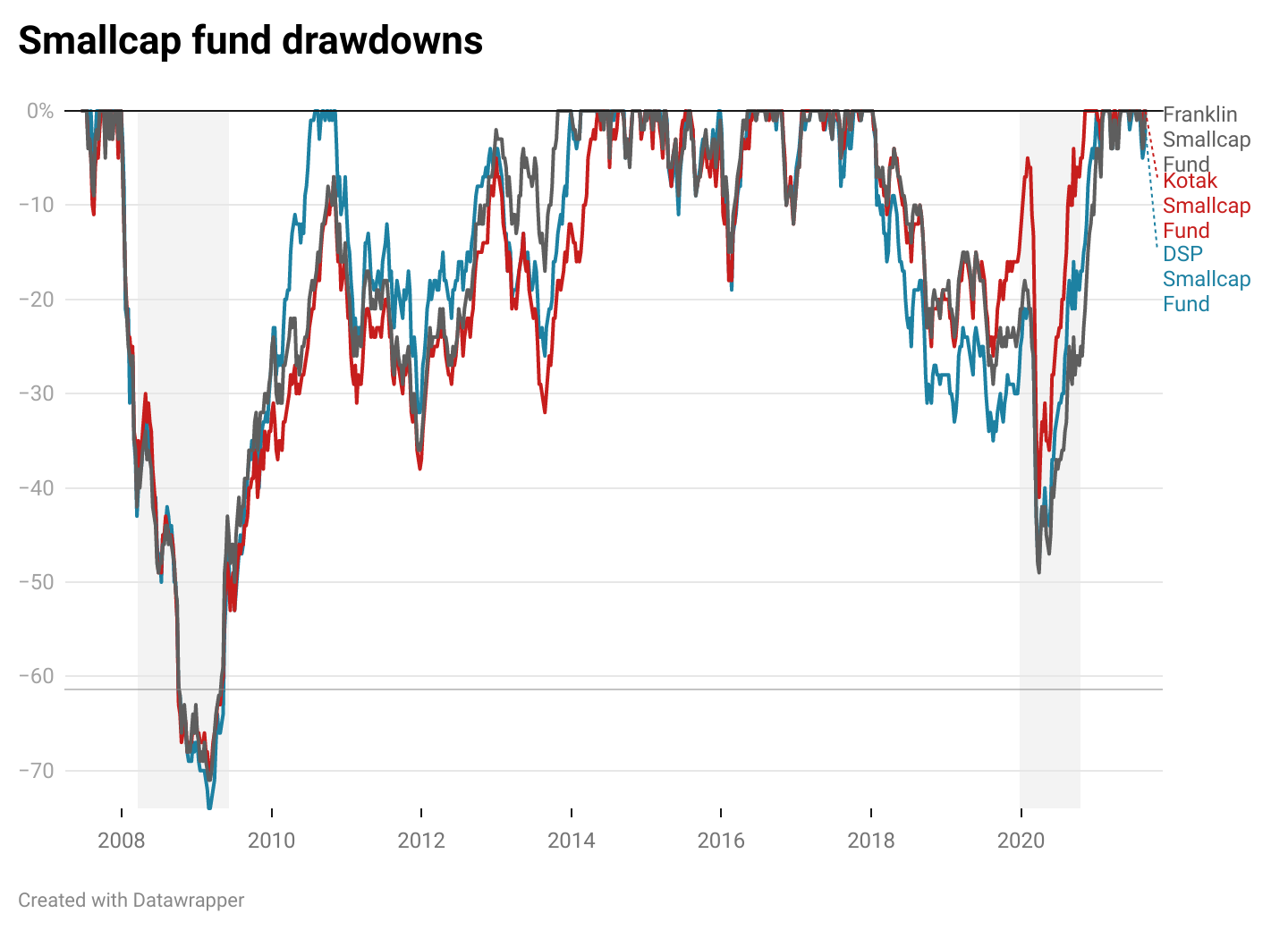

One quick way to understand just how risky smallcaps are is by looking at their historical drawdowns or percental fall from peak to troughs. Here are the drawdowns of 3 of the oldest smallcap funds. During the 2008 crash, they were down between 65-70%. So, if you had invested Rs 10 lakhs at the peak in 2008, it would’ve become Rs 3 lakh when the market bottomed out.

Historical drawdowns of smallcap funds

The sales pitches for smallcaps will tell you that these stocks are tomorrow’s blue chips. Sounds nice in theory, but not so much in reality. Smallcaps tend to go up sharply and crash equally hard. Such sharp rallies and crashes tend to bring out the worst behaviour in investors. It’s important to build a portfolio that allows you to sleep peacefully.

Investors often sell when smallcap funds crash and buy when they’ve already gone up substantially. It’s very hard for most investors to stay invested when a smallcap fund is down 50%-70%. That means the chances of you making a mistake are higher in smallcaps.

Moreover, smallcaps always don’t mean high returns just because you invest for the long term. You can see this from the 10-year smallcap fund returns from the image above. You can even check the 10-15 year SIP returns of the best-performing funds across large, mid, and smallcap categories. You can call it a starting point bias, hindsight bias etc but it’s hard to make a case for the so-called “smallcap premium.”

Moreover, most of the flows come into smallcap funds once there has been a significant runup in the index.

A few things to keep in mind:

- Smallcap funds may not be for everyone, and buy & hold doesn’t guarantee high returns over the long run.

- It’s easy to invest in a smallcap fund in good times and tough to hold on during bad times.

- Most investors are better off with a mix of large and midcap funds.

Keepsakes

- Our biases aren’t a flaw, and we can’t become rational emotionless machines either. The way to deal with them is to make sure you’re as hands-off with your investments and automating as much as possible.

- Good times don’t last. Don’t think you’ll continue to have 50%+ return years. The markets are perfectly capable of doing nothing for a long time. Temper your expectations.

- The stories about smallcap funds sound nice in theory, not so much in reality. Be very careful about investing in them.

Podcasts

We recently caught up with Prashanth Jain, the CIO of HDFC Mutual Fund. Prashanth is a true market veteran and the first Indian fund manager to manage a single mutual fund scheme for over 25 years. He manages some of the largest active mutual fund schemes in India.

In this conversation, Prashanth talks about the current market valuations, the opportunity set in India, active vs passive, his research process and a whole lot more. Listen to the full conversation here.

https://open.spotify.com/episode/0ZbBznHldA3wlhWmxYWEG5?si=fnjyMK-uSKWHydjBDjrOMQ&dl_branch=1

We also caught up with Chirag Mehta, senior fund manager at Quantum Mutual Fund. The views about gold as an asset class ranges from a must-have in a portfolio to a useless shiny rock. In this conversation, Chirag spoke about what’s the role of gold in a portfolio, how to invest in gold, central banks and their impact on gold, the pros and cons of gold options like SGBs, ETFs and a whole lot more. Listen to the full conversation here.

https://open.spotify.com/episode/2DRdvrVEB2hWMj2c36tu4H?si=SLR_uymgRXKi1_PeHdkVpA&dl_branch=1

Thanks for reading this issue of the Coin newsletter. Please do leave a comment if you have any feedback, suggestions or ideas for us.

Share this with your friends👇

Make sure that the podcasts dont exceed 8 mins. Edit and make it concise and crispy.

Who has 45 mins to listen to a single person?

Really very informative

The whole think is that Market test us every time

Thanks for this insightful article. What I liked about it is its informal tone. One sentence struck me particularly: “All you can do is control the process, not the outcome.”

Isn’t this precisely what Lord Krishna says in Bhagavad Gita? ‘Karmanye vaadhikaraste, maa faleshu kadachan.’ The word ’Adhikaar’ is commonly translated as a ’right.’ But in Sanskrit also means ’control.’

If we take the trouble of looking into our traditional texts, we will unearth a wealth of wisdom for every sector including of course for investing.

Hope you will send a newsletter in future detailing investing wisdom from our traditional texts.

This is very well compiled and structured. Same old information but in a very new perspective. I enjoyed reading this and this certainly helps to read something that’s really meant to help me as an investor. Brilliant editing, hope to see more of these.

This article provides very valuable advices for a novice investor and also acts as a refresher notes for an experienced investor. Looking forward to the next Coin newsletter #3

Great efforts, I always love all the content provided by you(Coin, Varisty ) solely because of point to point talk, no nonsense or extra discussion.

Keep doing the good work.

Thanks

Well articulated. Informative too.

Since you guys were kind enough to give the amazing insights on smallcap funds. Can you also suggest ways to invest in smallcap funds. I know one should invest as per the risk tolerance and goals etc etc ( have read all the classic books on keeping costs low, taxes low, turnover should be low and stuff like that but it works majorly in US markets, i mean invest in index funds, yes sounds good if you have index like snp500. But i am skeptical if it works for Nifty 50, given that 10 companies hold around 60% weightage of index). That being said any help would be amazing on how to navigate the troubled waters of mutual funds be it large cap, mid cap, small cap etc.

Such a nicely written informative article. You guys at zerodha are such amazing individuals, the information and products are at a next level with competitive pricing. Feels good to be associated with a company like yours.

I AM VERY HAPPY

That is a nice peep into my thoughts! So true, the flaws pointed out!

The SmallCap analysis too is a xL ent one: be aware & beware.

Thanks

This is a good news letter, you may also consider to make a video of the content with someone speaking and explaining, the effect and understanding of such video is impactful as they say visuals help more for a better understanding.

profound information!

really loved the depths this article goes.. really loved reading it – particularly the anchoring effect explanation..

This type of reports definately clear the view where to invest, it’s appreciable.

Great note, but if you can publish the same kind of data putting stocks (Large, Mid, Small) it will be very beneficial for us to make our investment decesion.

My zerodha coin not login please suggest me

This will definitely help us to decide on what funds should we invest in. Thank you for sharing with us!

gud

Very Informative