11.1 – Context

In the previous chapter we understood that for the long straddle to be profitable, we need a set of things to work in our favor, reposting the same for your quick reference –

- The volatility should be relatively low at the time of strategy execution

- The volatility should increase during the holding period of the strategy

- The market should make a large move – the direction of the move does not matter

- The expected large move is time bound, should happen quickly – well within the expiry

- Long straddles are to be setup around major events, and the outcome of these events to be drastically different from the general market expectation.

Agreed that the directional movement of the market does not matter in the long straddle, but the bargain here is quite hard. Considering the 5 points list, getting the long straddle to work in you favor is quite a challenge. Do recall, in the previous chapter the breakdown was at 2%, add to this another 1% as desired profits and we are essentially looking for, at least a 3% move on the index. From my experience expecting the market to make such moves regularly is quite a challenge. In fact for this reason alone, I think twice each and every time I need to initiate a long straddle.

I have witnessed many traders recklessly set up long straddles thinking they are insulated to the market’s directional movement. But in reality they end up losing money in a long straddle – time delay and the general movement in the market (or the lack of it) works against them. Please note, I’m not trying to discourage you from employing the long straddle, no one denies the simplicity and elegance of a long straddle. It works extremely well when all the 5 points above are aligned. My only issue with long straddle is the probability of these 5 points aligning with each other.

Now think about this – there are quite a few factors which prevents the long straddle to be profitable. So as an extension of this – the same set of factors ‘should’ favor the opposite of a long straddle, i.e the ‘Short Straddle’.

11.2 – The Short Straddle

Although many traders fear the short straddle (as losses are uncapped), I personally prefer trading the short straddle on certain occasions over its peer strategies. Anyway let us quickly understand the set up of a short straddle, and how its P&L behaves across various scenarios.

Setting up a short straddle is quite straight forward – as opposed to buying the ATM Call and Put options (like in long straddle) you just have to sell the ATM Call and Put option. Obviously the short strategy is set up for a net credit, as when you sell the ATM options, you receive the premium in your account.

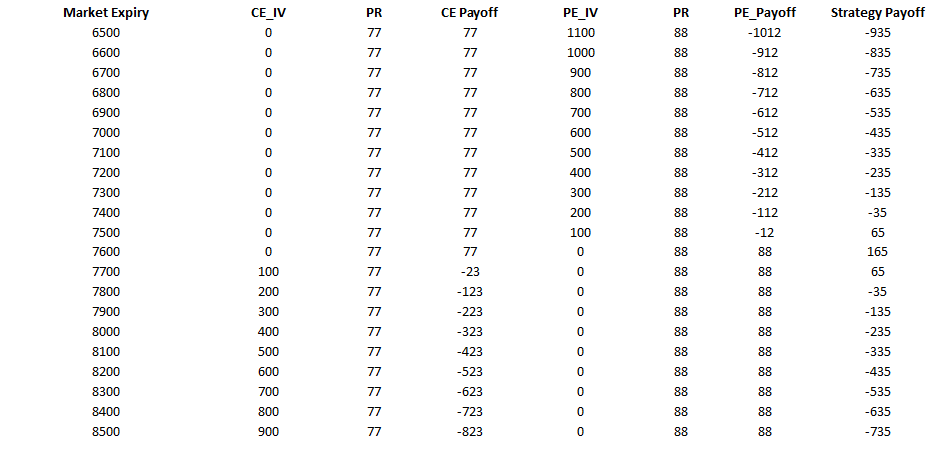

Here is an example, consider Nifty is at 7589, so this would make the 7600 strike ATM. The option premiums are as follows –

- 7600 CE is trading at 77

- 7600 PE is trading at 88

So the short straddle will require us to sell both these options and collect the net premium of 77 + 88 = 165.

Please do note – the options should belong to the same underlying, same expiry, and of course same strike. So assuming you have executed this short straddle, let’s figure out the P&L at various market expiry scenarios.

Scenario 1 – Market expires at 7200 (we lose money on put option)

This is a scenario where the loss in the put option is so large that it eats away the premium collected by both the CE and PE, resulting in an overall loss. At 7200 –

- 7600 CE will expire worthless, hence we get the retain the premium received i.e 77

- 7600 PE will have an intrinsic value of 400. After adjusting for the premium received i.e Rs.88, we lose 400 – 88 = – 312

- The net loss would be 312 – 77 = – 235

As you can see, the gain in call option is offset by the loss in the put option.

Scenario 2 – Market expires at 7435 (lower breakdown)

This is a situation where the strategy neither makes money nor loses any money.

- 7600 CE would expire worthless; hence the premium received is retained. Profit here is Rs.77

- 7600 PE would have an intrinsic value of 165, out of which we have received Rs.88 as premium, hence our loss would be 165 – 88 = -77

- The gain in the call option is completely offset by the loss in the put option. Hence we neither make money nor lose money at 7435.

Scenario 3 – Market expires at 7600 (at the ATM strike, maximum profit)

This is the most favorable outcome for a short straddle. At 7600, the situation is quite straight forward as both the call and put option would expire worthless and hence the premium received from both the call and put option will be retained. The gain here would be equivalent to the net premium received i.e Rs.165.

So this means, in a short straddle you make maximum money when the markets don’t move!

Scenario 4 – Market expires at 7765 (upper breakdown)

This is similar to the 2nd scenario we discussed. This is a point at which the strategy breaks even at a point higher than the ATM strike.

- 7600 CE would have an intrinsic value of 165, hence after adjusting for the premium received of Rs. 77, we stand to lose Rs.88 (165 – 77)

- 7600 PE would expire worthless, hence the premium received i.e Rs.88 is retained

- The gain made in the 7600 PE is offset against the loss on the 7600 CE, hence we neither make money nor lose money.

Clearly this is the upper breakdown point.

Scenario 5 – Market expires at 8000 (we lose money on call option)

Clearly the market in this scenario is way above the 7600 ATM mark. The call option premium would swell, so would the loss –

- 7600 PE will expire worthless, hence the premium received i.e Rs.88 is retained

- At 8000, the 7600 CE will have an intrinsic value of 400, hence after adjusting for the premium received of Rs. 77, we stand to lose Rs. 323( 400 -77)

- We have received Rs.88 as premium for the Put option, therefore the loss would be 88- 323 = -235

So as you can see, the loss in the call option is significant enough to offset the combined premiums received.

Here is the payoff table at different market expiry levels.

As you can observe –

- The maximum profit 165 occurs at 7600, which is the ATM strike

- The strategy remains profitable only between the lower and higher breakdown numbers

- The losses are unlimited in either direction of the market

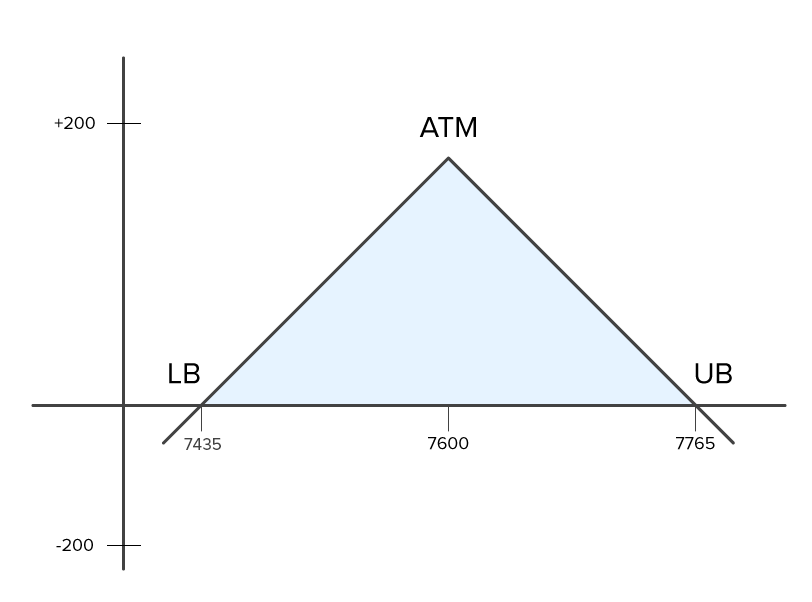

We can visualize these points in the payoff structure here –

From the inverted V shaped payoff graph, the following things are quite clear –

- The point at which you can experience maximum profits is at ATM, the profits shrink as you move away from the ATM mark

- The strategy is profitable as long as the market stays within the breakdown points

- Maximum loss is experienced when markets move further away from the breakdown point. The further away the market moves from the breakdown point, higher the loss

- Max loss = Unlimited

- There are two breakdown points – on either side, equidistant from ATM

- Upper Breakdown = ATM + Net premium

- Lower Breakdown = ATM – Net premium

As you may have realized by now, the short straddle works exactly opposite to the long straddle. Short straddle works best when markets are expected to be in a range and not really expected to make a large move.

Many traders fear short straddle considering the fact that short straddles have unlimited losses on either side. However from my experience, short straddles work really well if you know how exactly to deploy this. In fact in the last chapter of the previous module, I had posted a case study involving short straddle. Probably that was one of the best examples of when to implement the short straddle.

I will repost the same again here and I hope you will be able to appreciate the case study better.

11.3 – Case Study (repost from previous module)

The following case study was a part of Module 5, Chapter 23. I’m reposting the same here as I assume you would appreciate the example better at this stage. To get the complete context, I’d request you to read the chapter.

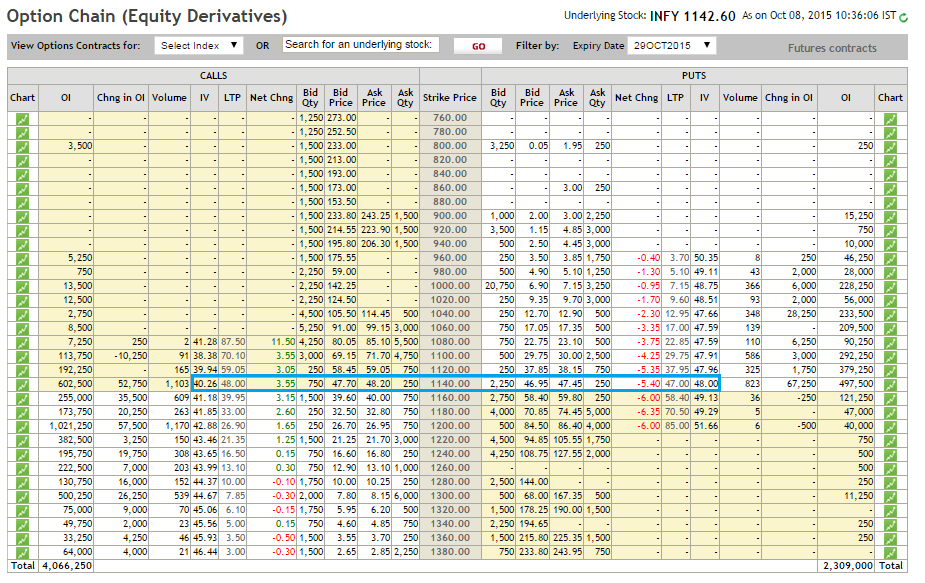

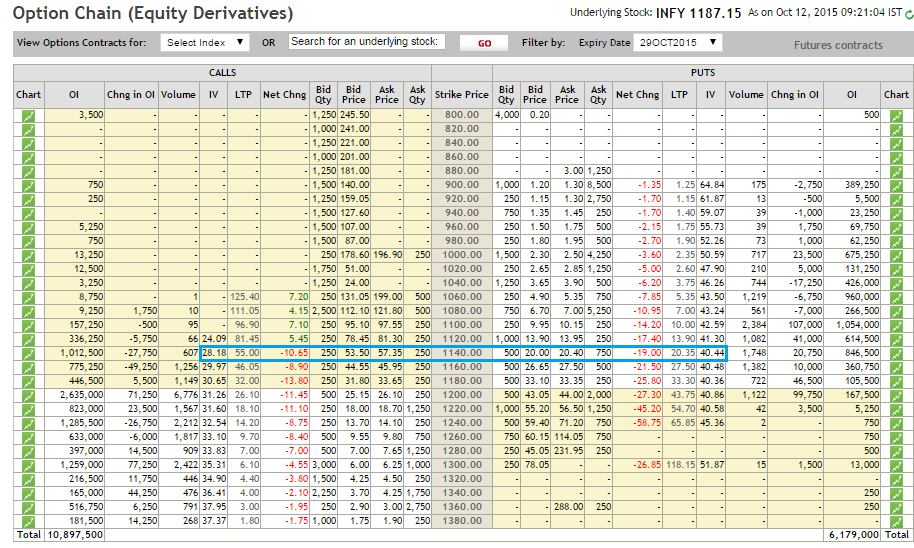

Infosys was expected to announce their Q2 results on 12th October. The idea was simple – news drives volatility up, so short options with an expectation that you can buy it back when the volatility cools off. The trade was well planned and the position was initiated on 8th Oct – 4 days prior to the event.

Infosys was trading close to Rs.1142/- per share, so he decided to go ahead with the 1140 strike (ATM).

Here is the snapshot at the time of initiating the trade –

On 8th October around 10:35 AM the 1140 CE was trading at 48/- and the implied volatility was at 40.26%. The 1140 PE was trading at 47/- and the implied volatility was at 48%. The combined premium received was 95 per lot.

Market’s expectation was that Infosys would announce fairly decent set of numbers. In fact the numbers were better than expected, here are the details –

“For the July-September quarter, Infosys posted a net profit of $519 million, compared with $511 million in the year-ago period. Revenue jumped 8.7 % to $2.39 billion. On a sequential basis, revenue grew 6%, comfortably eclipsing market expectations of 4- 4.5% growth.

In rupee terms, net profit rose 9.8% to Rs.3398 crore on revenue of Rs. 15,635 crore, which was up 17.2% from last year”. Source: Economic Times.

The announcement came in around 9:18 AM, 3 minutes after the market opened, and this trader did manage to close the trade around the same time.

Here is the snapshot –

The 1140 CE was trading at 55/- and the implied volatility had dropped to 28%. The 1140 PE was trading at 20/- and the implied volatility had dropped to 40%.

Do pay attention to this – the speed at which the call option shot up was lesser than the speed at which the Put option dropped its value. The combined premium was 75 per lot, and he made a 20 point profit per lot.

11.4 – The Greeks

Since we are dealing with ATM options, the delta of both CE and PE would be around 0.5. We could add the deltas of each option and get a sense of how the overall position deltas behave.

- 7600 CE Delta @ 0.5, since we are short, the delta would be -0.5

- 7600 PE Delta @ – 0.5, since we are short, the delta would be + 0.5

- Combined delta would be -0.5 + 0.5 = 0

The combined delta indicates that the strategy is directional neutral. Remember both long and short straddle is delta neutral. In case of long straddle, delta neutral suggests that the profits are uncapped and in case of short straddle, the losses are uncapped.

Now here is something for you to think about – When you initiate a straddle you are obviously delta neutral. But as the markets move, will your position still remain delta neutral? If yes, why do you think so? If no, then is there a way to keep the position delta neutral?

If you can build your thoughts around these points, then I can guarantee you that your options knowledge is far greater than 90% of the market participants. To answer these simple questions, you will need to step a little deeper and get into 2nd level of thinking.

Do post your comments below.

Key takeaways from this chapter

- Short straddle requires you to simultaneously Sell the ATM Call and Put option. The options should belong to the same underlying, same strike, and same expiry

- By selling the CE and PE – the trader is placing the bet that the market wont move and would essentially stay in a range

- The maximum profit is equal to the net premium paid, and it occurs at the strike at which the long straddle has been initiated

- The upper breakdown is ‘strike + net premium’. The lower breakdown is ‘strike – net premium’

- The deltas in a short straddle adds up to zero

- The volatility should be relatively high at the time of strategy execution

- The volatility should decrease during the holding period of the strategy

- Short straddles can be set around major events, wherein before the event, the volatility would drive the premiums up and just after the announcement, the volatility would cool off, and so would the premiums.

Download Short Straddle Excel Sheet

Sir if I had executed a short straddle today and waited for next day to get the advantage of theta decay, now suppose next day the black swan event happened, I will erode the whole account balance, so for protecting our capital not only in short straddle but any selling strategy, what one must do?

That risk always exists. In fact, we can this happen during 2026 budget, where the volatility instead of cooling, actually increases and these straddles and strangles actually bled a lot of money. One way is to set up things like Iron condors, but the trade off is that these positions are expensive and involve a lot more option legs.

Hi Karthik, can u pls suggest a option strategy on Natural Gas.

Example. If current price of natural gas is 600, and I sell a call at 600 and sell a put at 600 means I make a short straddle

To hedge this,

Shud I buy a put at 500 and buy a call at 700 or

Shud I buy a put at 700 and buy a call at 500.

what strategy can be adopted.

Instead of hedging a short strangle why not think of an Iron condor? Net net, its the same.

I have surrendered. Please tell us is it possible to keep the position delta neutral until expiry in the case above which you have asked ?

No, you will have to keep adjusting the position as and when the underlying price changes. Delta is not constant.

Okay thanks

Happy learning 🙂

Sir

Regarding your question :

When you initiate a straddle you are obviously delta neutral. But as the markets move, will your position still remain delta neutral? If yes, why do you think so? If no, then is there a way to keep the position delta neutral?

My humble opinion is delta of an option is also dependent on Implied Volatility:

which reflects market expectations of future price volatility. As it is not a scientific value, it can vary on any given time for put and call option of the same underlying

the sign and magnitude of the delta of an option depends on whether the option is bought or sold.

Hence as the put call ratio of the option of the same underlying with same strike price expiring on same day can be different hence the delta magnitude can vary

Am I right sir?

Yes, delta is a variable, and changes as the underlying changes direction.

to keep Delta neutral in straddle buy OTM option CE or PE depends on the market direction?

For example: CE delta moves to .75 ITM buy PE OTM .25 to offset? is that right?

Not sure if I get the query fully, but generally, to maintain delta neutrality, you need to ensure the total delta adds up to 0.

\”Now here is something for you to think about – When you initiate a straddle you are obviously delta neutral. But as the markets move, will your position still remain delta neutral? If yes, why do you think so? If no, then is there a way to keep the position delta neutral?

If you can build your thoughts around these points, then I can guarantee you that your options knowledge is far greater than 90% of the market participants. To answer these simple questions, you will need to step a little deeper and get into 2nd level of thinking\”

I just answered for the above part from the article.

My answer:

to keep the Delta neutral in short straddle sell OTM option CE or PE depends on the market direction.

For example: CE delta moves to .75 ITM sell PE OTM .25 to offset? is that right?

Sort of. To perfectly balance, you need to offset by the same magnitude of delta.

I have doubt on

\”Key takeaways from this chapter:

8. Short straddles can be set around major events, wherein before the event, the volatility would drive the premiums up and just after the announcement, the volatility would cool off, and so would the premiums. \”

In fact, I have very much skepticism on Naked Short Straddles as it would wipe out your years of profit in case of Black Swan.

what do you suggest?

Of course, one way to deal with this is to hedge volatility.

Request to please check the Excel sheet for Short straddle. Its mentioned as Max Profit as Unlimited. I think it should be Max Loss as Unlimited.

Regards

Himanshu Bhardwaj

Oh yes, loss is. Not profits. Thanks for pointing that out.

Hi Karthik Sir,

1.The trader has decided to execute a short straddle based upon the high IV for the Options. Is that Right?

2. Sir what you are saying is since the IV was very high, even the good results will reduce the premium for the options?

3. What if the company\’s results are Higher profits than the Expected, Is there any chances of shooting up of premiums way more than this?

4. If the very IV is less before the results and if the results are decent also will the premiums shoot up? In this situation, we can use long straddle right?

1) Thats right

2) No, the results don\’t matter. What I\’m suggesting is that the IV tends to cool off once the uncertainty of results is out

3) Maybe, maybe not. But the tendency for IV is to cool off as the results and its uncertainty wanes

4) Same as above

Please make videos on Options stragegies, and also on systematic trading

Noted.

Is there any plan to have Candle pattern chart in Sensibul Watchlist(New) for Strategies. At the moment Strategies can only be viewed in Line Chart.

Ah, you will have to check this with Sensibull team.

how to adjust straddle pieces:-

Eg – Stock ABC is trading in a range of 100-120 and we create a straddle with the same break-even points (i.e. 100-120) and in some time stock reaches 119 and closes at that prices, now here is the risk that the stock might break above its range the next day. So how do we hedge our positions in this case, my guess is to buy a call option but if we buy a call option and the price fall from 119 then we\’d lose money on it. So, is there any method instead of closing our positions.

So any adjustment to this means that you no longer have a straddle. You create a new strategy altogether. You will have to visualize the position\’s P&L, breakeven. Personally, not a big fan of these adjustments 🙂

Very nicely explained .thanks

Happy learning 🙂

Hi Karthik,

Selling options seem to have a high POP, however there is always a bad risk-reward while selling options. What is the trade-off? How to balance this situation?

Hmm, but why do you say there is a bad risk-reward in selling options?

sir in the Key takeaways from this chapter you tell

The maximum profit is equal to the net premium paid, and it occurs at the strike at which the long straddle has been initiated

there is a wrong in this line

this is short stradle and premium well be credited

Checking this, thanks for pointing.

Ok, thank you sir..

Happy learning 🙂

Sir,

If I took short position with Iron butt erfly strategy for weekly /monthly expiry, it is showing Max. Profit 37500 (i. e. Premium )& max loss 12000 at expiry for 5 lots. My question is that

1) when do we have to exit the position- on the day of expiry or one day before expiry?

2)If we got the above showed loss at expiry , can we get the showed premium or not? Plz reply..

1) Technically you can exit the position anytime you wish. I would prefer to close out before 🙂

2) If you hold to expiry, then your final P&L will depend on the settlement price.

Hello karthik. Thank you for the wonderful explanation. I am looking forward to the chapter in delta hedging using futures. Hope to see it soon. Thank you.

Thanks, Kalyan. Happy learning 🙂

How to deploy this in streaks? For BNF

Please do talk to them Arun, they will be happy to help.

Last question sir,

[1] In short straddle big break evens are better because of theta decay, and in long straddle the sooner to get out of break evens the better it is right sir?

[2] And if big break evens are better , why people avoid short strangle as the break evens are much bigger in ITM short,but still use short straddle with small break evens?

Thank you in advance.

1) Absolutely

2) Big breakevens (actaully cut off points) are better only under low volatility situation. So unless you have a perspective on volatility, you should not be deploying this.

Sir, if I use this strategy hedging with future, supposed I deployed short straddle right before market close at around 3;20 and exit at the next day opening, either way it gaps , profit will be booked right. As long as it sways between the breakevens.

/

/

/

break even -> ————————-

/

Yes, as long as the premiums behave the way you it to behave 🙂

What will be the settlement days in short straddle…?

Sorry, settlement days as in? Can you elaborate on you query?

Do you use spot or underlying future price when entering as well as adjustments becoz in case of say next month expiry the difference in future and spot price can be quite a lot..Just a query as I did not see it mentioned anywhere

I\’d prefer to use spot prices 🙂

Sir,

Is my understanding correct about using the negative sign in PE delta ?

The negative sign used in the PE delta to denote the fact that when the underlying price move upwards and increase in value, the value of PE premium decreases. Therefore, in option chain PE delta denotes with negative sign and CE delta with positive sign.

About that virtual trade, at EOD the 4 legged trade was showing around 2500 Rs loss overall. Hence what intervention can be done ?

Yes, using -ve sign to indicate the direction is ok.

As far as the intervention is concerned, yes, you can tweek individual positions but that also means you will incur costs. Sometimes the costs are prohibitive to make these changes.

Sir,

Please share your expert suggestion regarding these below queries.

Yesterday (27/06/2023) I initiated a virtual trade of iron fly set up in Banknifty, short 43700PE at 147.25 and 43700CE at 170.05 and then buy 43200PE at 26.65 and 44200CE at 20.10… Post 1.30pm the banknifty started upward movement and the PE sell position was giving profit and CE sell was giving loss… The CE sell option was shifting to deep ITM where delta was around 0.9 while the delta of PE sell option was -0.06 … Hence the loss from CE sell (by EOD above 7000/- )was far more than the profit from PE sell (by EOD around 3000/-) … In this scenario what should be my stand ?

Should I square off the whole trade while at breakeven or square off only the CE sell leg or shift for any other adjustments ? If I opt for any adjustments then what will be the changes ?

If I plan to square off the PE 43700 leg (Which was giving profit) and sell another PE at 43900 while both the CE and PE buy leg intact, what will I do with the CE sell leg ( which was running under huge loss) ? Is it even a right approach to shift the PE sell leg ?

Anindita, delta cannot be -ve. So PE delta will be 0, not -0.9. You should not look at individual positions when executing a multileg position, you need to look at the overall profitability.

If the position is making a loss as a whole, then maybe some intervention is required, else you don\’t need to worry.

Hi Karthik,

If we do not hedge the straddle to keep it \”delta neutral\” until expiry, what is the expected outcome at expiry? Will it not follow the straddle\’s payoff chart?

It will follow the straddle\’s payoff upon expiry.

HI KARTHIK

COULDN\’T GET THE ANSWERS YOU ASKED IN MODULE 6 – OPTION STRATEGIES

CHAPTER 11, THE SHORT STRADDLE

\”\”Now here is something for you to think about – When you initiate a straddle you are obviously delta neutral. But as the markets move, will your position still remain delta neutral? If yes, why do you think so? If no, then is there a way to keep the position delta neutral?

If you can build your thoughts around these points, then I can guarantee you that your options knowledge is far greater than 90% of the market participants. To answer these simple questions, you will need to step a little deeper and get into 2nd level of thinking\”\”

WHAT IS YOUR ANSWERS OF THE ABOVE QUESTIONS

PLEASE REPLY

REGARDS

AMARJEET CHHABRA

DSA326

Amarjeet, that is because as the markets move, so does the delta of the options and hence the positions don\’t remain delta neutral.

Sir,

I am trying to say that it is not buying but rather selling CE/PE to adjust delta.

If the delta requires to be made neutral and some +ve delta needs to push, won’t be it good to sell put options and receive premium. Similarly, during -ve push of delta to make neutral, won’t be it good to sell call options and receive premium?

Yes, you can adjust delta to bring it back to the neutral position by either selling an option or by buying an option. It\’s just that the selling option requires a lot more capital due to the margin required.

Sir,

The delta neutral strategies are good undoubtedly. Meanwhile, adjustments will be quite painful here each time. So, what would be your best suggestion- Should we go for delta neutral strategies without adjustments at the end of every day/ Is there any particular difference in delta only when we should go for adjustment?

Also, if the delta requires to be made neutral and some +ve delta needs to push, won\’t be it good to sell put options and receive premium. Similarly, during -ve push of delta to make neutral, won\’t be it good to sell call options and receive premium?

Your suggestion is sought here.

Buying CE or PE to adjust deltas will only increase the cost of the strategy, but yes, these are techniques of adjusting the position to bring it back to delta neutrality.

Sir,

Is the below correct?

In case the Corporate result doesn’t meet general mass expectation—Volatility increases much more than 4-5 days before corporate result etc. and premium also increases much more than 4-5 days before a corporate result etc

Yes, thats right Anirban. Anything unexpected in the market usually tends to increases the volatility in the market.

Sir,

In case of premium value, kindly let me know if I correctly understood what you described in the chapters for the expected outcome of the premium value based on volatility:

(i) Just before 4-5 days of a corporate result etc.—– Volatility increases and premium increases

(ii) After the Corporate result as per general expectation.—— Volatility decreases and premium decreases

(iii) In case the Corporate result doesn\’t meet general expectation—Volatility increases much more than point no. (i) i.e, before 4-5 days of a corporate result etc. and premium also increases much more than point No. (i) i.e, before 4-5 days of a corporate result etc

Thats correct. Generally speaking, volatility increases as we approach corporate results or any other event and it cools off as the event unfolds.

Sir,

I have the below three queries:

(i) In case of delta neutral strategies, should we have to check if the delta is neutral at the end f everyday and act accordingly to buy/sell futures/options accordingly to ensure neutrality? I mean to say what is the standard process to track and ensure of the delta neutral? Have you made any topic on the same? If yes, could you kindly send the link?

(ii) Also, in case of several bearish/bullish outlook based strategies (as you have vividly explained throughout), we have to ensure that the delta is -ve/+ve respectively. However, here also, sometimes the result could alter to +ve/-ve. Do we also have to track on each day basis and act accordingly through buying/selling futures/options? Please suggest. I am not getting this area.

1) Yes, ideally it will be good to track if delta neutral is still delta neutral at the end of the day. But this also leads to frequent readjustments, which I\’m not too fond of.

2) Not really, these are ok not to check daily.

Big no to unlimited risk, it\’s okay if I don\’t earn but it\’s not okay to lose large amount by taking unlimited risk..

Alternative pathways , Russian roulette game in psychology is example if this.

It very bad to be poorer than you are currently.

Never take unlimited risk.

Think what would have happened to Adani option seller ? They will never recover.

Yes, one should always keep risk under check Kirit.

Ohh, Okay thank you. Now my doubt is cleared

Sure, happy learning 🙂

I am glad to thank you for the lessons you have updated on the Zerodha varsity platform. I am a student of yours and follow every lesson you updated on Zerodha varsity. Here is my doubt future hedging in Delta is good but when the market moves downward we are facing too much of losses. Here is my scenario for the heading based on delta neutral.

Now the Option spot is trading at 18000 future contract is trading at 18100 and we are entering the 18000 short straddle option contract at the same expiry date, premium of a call option is trading at 50 and the premium of a put option is trading at 60. At the time of expiry, the market went down by 17800 where we will receive a full premium amount from call option Rs. 50 and we will lose Rs. 140 on the put option total loss from this strategy is Rs.90 and in the future, we will make Rs.300 as loss total loss for this whole strategy is 390. Then, how can be this a hedging strategy?

Its hedged at the time of entering a trade, Ram. But as the market moves, one of the legs gets into a loss. This is when you may want to think of either exiting or adjusting the positions. Which also means, the best time to implement something like this is when you expect markets to remain sideways and not really when its trending.

If i have short straddle in stocks and i let it expire by itself, there is any physical delivery obligation of ITM option or it gets cash setteled?

If both options are ITM, then there is an obligation for physical delivery. If only leg is ITM and the other is OTM, then there is physical delivery.

Yes sir. I see the point. I stopped making adjustments after you clearly explained to me last time. But what I meant was if markets move, the delta will also change. So if there is a way to keep the positions neutral, it must only be through adjustments right? Or is there anything I\’m missing here?

Yes, you are right about that Sathish.

Towards the end of the chapter, the explanation goes like, \’Now here is something for you to think about – When you initiate a straddle you are obviously delta neutral. But as the markets move, will your position still remain delta neutral? If yes, why do you think so? If no, then is there a way to keep the position delta neutral?\’.

Are you talking about any adjustments here? Because I remember you telling me that you aren\’t a fan of adjustments. So if not could you explain briefly what you are implying, because I don\’t get the point no matter how many times I give this a read? Thanks Sir.

I\’m not talking about adjustments here, I\’m talking about the changing delta position. Yes, you can adjust this position but at a higher cost 🙂

Hi,

For short straddlle, how much margin money is required.

Is it summation of both legs or is it for one leg only?

Regards

It is the sum of both. Check this – https://zerodha.com/margin-calculator/SPAN/

Hi Karthik, can u pls suggest a option strategy on Natural Gas.

Example. If current price of natural gas is 600, and I sell a call at 600 and sell a put at 600 and to hedge, I buy a put at 500 and buy a call at 700.

Would it be a prudent strategy.

What if on expiry gas prices move to 800 or 1000? what strategy can be adopted.

Thanks.

In this case, you are fully hedged, Mayank. So it should be ok. YOu can key in these numbers in Sensibull and visualize the payoff.

Hi Karthik, would you say range bound strategies like short straddle are good in currency trading? I mean currency can get very volatile (like whats happening now) but it mostly trades with low swings

Yeah, any range bound asset actually.

Hi sir can you please tell me using correct time to use this strategy and when we using other strategy please tell me sir ?

halo sir

i am following you and like your material and go through all modules and comments now my question is typo errors mentioned in different modules is rectified by today date and material is now compiled

We are working on it, Mukesh. We will fix all the typos 🙂

Where can i get live straddle chartsor create one ?

YOu can check Sensibull platform for this, Vivek.

sir , how to calculate current day breakeven point before expiry ?

For option buying you profit moment you cross the premium paid. For example, if you\’ve paid 10 as a premium, you are breaking even at 10 and anything higher than 10 is your profit. Likewise, if you have received 10 as premium, you are breaking even at 10, lower the premium goes the higher is your profit.

hi Karthik,

Its 2022 now. still waiting for your delta neutral delta hedging chapter.

can you please post a link where you or anybody explained this.

I\’ll probably do a video on this.

how put stoploss and target orders for short straddle in zerodha..My SL order is not accepted

Not sure why, I\’d suggest you call the customer desk once.

the nifty spot was at 17704 and i purchased for creating short straddle

1) short atm ce at 17700 – Rs 156 premium

2) short atm pe at 17700 – rs 163 premium

net credit – Rs 319 , lower break – 17381 , upper break – 18019

so between breakeven points i shouldnt have loss

but on same day around 2 pm nifty spot was at 17555

and my PE premium went to Rs 240 ( 163-240 * 50 ) = -3850 loss

and CE premium went to Rs 108 (156-108 *50) = 2400 profit

so i have to incurred loss of Rs -1450 ( -3850+2400)

why it happened even the nifty spot was trading between lower and upper breakeven points ?

Mahi, in between the breakeven points, you wont have a loss, provided you hold to expiry…but it can result in temporary loss during the expiry as the premiums can fluctuate as they are a function of various other option greeks.

Sir can you explain how delta will not be neutral for you question

Long deltas and the short delta will cancel out.

Sir, why call & put option volatilities are different for a particular strike price? Does it has something to do with direction of market?

Thats mainly due to the demand and supply dynamics/mismatch.

Yes, True

Thanks very much, sir for your response

I have been watching your videos, on learn app, as well as on youtube. You are doing a great job. Your and Prateek sir\’s initiative has transformed the stock market learning in a structured manner. Even a Toddler can understand the Market very easily.

I am highly motivated to meet you and Prateek Singh(CEO learn app)

I am just a 1-year college student. That\’s why I am tyro to the market.

Thanks, Vikash. Glad you liked the content. Prateek is a great educator, we are super happy to have been associated with him 🙂

First thing first, Before Diving deep into answering the question.

A massive Thank You, Dear Karthik Rangappa sir for creating this Wonderful course

Now comes answering Part,

What I believe

1-Delta won\’t stay neutral because there is the effect of other Greeks also on the Delta as well on the IV

2- Also, we can Keep Delta Neutral by adjusting (rolling up or down) our Position.

I believe I could be right to some extent. Since I am a Tyro, I could be possibly wrong as well. So please correct me.

Thank You

1) Yes, as stock price moves, so does the delta and therefore your delta neutral position wont stay delta neutral

2) That\’s right

Tyro – I had to Google that 🙂

Sir,

I have a basic understanding that a trade must have a buy and a sell. So incase of long strangle we buy both call and put options. And in case of short strangle we sell both buy and put options. Hence positions will be open in both cases. What about the selling activity for CE and PE in long strangle and buying in short strangle.

A trade is when you execute the 1st leg of a trade. A trade is said to be complete when square off the initial trade by taking up the opposite side. For example – I buy 100 shares of HCL (trade initiated)……after 15 minutes, I decide to sell 100 Shares of HCL (square off, trade completed). The same with strangle or straddle. You initiate by buy (or selling) 2 option…..and when you decide to square off, do the opposite trade but ensure the quantities match.

Resp. Sir

I want to draw your kind attention that the exelsheet given at the end of the chapter is wrong. That is the same as long straddle. Please check and undo the wrong.

Regards.. Ashutosh.

I will check and update this, Ashutosh.

Yes Sir! Thanks!

I quoted you, Sir! You have written that

\”Obviously the short strategy is set up for a net credit, as when you sell the ATM options, you receive the premium in your account\”.

So why the xlsheet showing net debit?

Lol, I\’m sorry, too many things in parallel. Yes, when you sell options, you receive a premium, which is net credit. If you pay a premium (when you buy options, it\’s debit).

Resp Sir

Where is your update on delta hedging?

Again, the xlsheet for short straddle shows net debit whereas we create the strategy for net credit by selling ATM CE-PE STRIKES? To quote you:\”Setting up a short straddle is quite straight forward – as opposed to buying the ATM Call and Put options (like in long straddle) you just have to sell the ATM Call and Put option. Obviously the short strategy is set up for a net credit, as when you sell the ATM options, you receive the premium in your account.\”

Though the result is ok,that is, 165 as per your example of Nifty.

Regards. Ashutosh.

How net credit? When you sell options, you receive premium right?

Sorry! Pl do not read the above.

Resp Sir,

Today I did some paper trading.

Nifty spot–16352

ATM CALL SELL 16350

ATM PUT SELL 16350

CE PREM RECD 232

PE PREM RECD 223

TOTAL RECD 455

EXP 30 JUNE

STRATEGY SHORT STRADDLE

I KNOW I COULD BE WRONG,BUT I SUPPOSE MARKET WOULD MOVE WITHIN A RANGE–

14900–15500.

Volatility is 22.30 (INDIA VIX).

HOWEVER, THIS THE RANGE WHICH PROMPTS ME TO GO FOR THE STRATEGY.

JUST WANTED TO KNOW WHETHER THIS THOUGHT PROCESS IS OK?

REGARDS. ASHUTOSH.

If you expect the market to trade within a range, then why are doing a short straddle? Maybe you should try short strangle instead.

Thank you Karthik.

Unrelated question, no doubt that conviction will build by experience in trading day in and day out, but is there a book on building conviction in market and decoding various market events/trades/price-movement to get sense of the direction and quantam of change in Indexes/stocks or voltaility in market.

General reading helps, Mohit. Plus there seems to be a lot of good content online on platforms like Twitter as well. Do keep track of that 🙂

Karthik, what happens if an event is after market hours?

As today GDP data is going to release for Q1 and Let\’s say I created a short straddle on BANKNIFTY before the event with high volatility so that I can exit as soon as voltaility drops after event. what is all that can wrong here from short straddle point of view? Can volatility go up due to gap opening next day?

There is a chance, Mohit. The general expectation is that the volatility will cool off after the event. Having said that, events can induce more volatility also, this is more so when the events occur overnight (off-market hours) when there is more time for analysis. If the event unfolds during market hours, you are likely to get that small window where the volatility dips and offers you a chance to exit the position.

Sir it will be great if you can incorporate some adjustment technique in each of the option strategies explained by you…

Will try and put up something on this.

Options are way too strenuous to comprehend. I have ample doubts regarding options, but just wanna ask a few:-

1. How FUTURES delta is always = 1?

2. What about the delta value of long futures and short futures?

3. Why the combined delta value should be = 0?

4. The combined delta of the LONG STRADDLE strategy will also alter if the market moves, just like SHORT STRADDLE. Then, why is the same isn\’t discussed there, i.e. how to remain always delta neutral?

is this possible to make 5000 per a day using 10 lac capital and using option selling strategies that what i\’m going to mention below SELL in the money

BUY ATM options

because the end of the contract date in this type of strategies are getting well returns in my paper trading and strategy builder sites

needed some clarification over all that if we\’re able to achieve 0.5% to 1% in a day sir

Nothing is certain, Yuvraj. If that was the case, one may as well target trading with 10Cr and making 5L per day. The point is that markets are uncertain, and having money targets is not a great idea.

I have made a short straddle but i am not able to understand theta decay. Will it show in my P and L the next day or i will get that credited after i square off my position? Or will i have to square off on expiry for it?

No, theta decay is a phenomenon where all else is equal, the premium today reduces compared to premium y\’day. The acceleration increases as we go closer to the expiry date.

Yes I actually checked it later! Thanks a lot!

Sure, good luck!

This is very great strategy no doubt! but is there any way I can manage to lessen my margin requirements to execute this strategy? I have heard about hedging but I am just clueless about how to do hedging in this case. can you explain a bit if any way exists?

I\’d suggest you check the Iron condor chapter for this.

Paper trade was 70 % accurate… But we have to be very strict stop loss of at least 20-30% ..

Like with all trades 🙂

When we initiate a straddle we are obviously delta neutral. But as the markets move, will our position still remain delta neutral? If yes, why do we think so? If no, then is there a way to keep the position delta neutral?

No, it won\’t remain same in rangebound market, if breaks resistance then again should made the ATM short position of put option and if breaks support level then again should buy ATM short position of call option so that the delta value would be neutral.

Yup, the position won\’t remain delta neutral. Markets need not have to break S&R to gain or lose delta, even a simple move will change the delta. To bring the position back to delta-neutral, you can buy or sell options.

In the Infy example:

1. Shouldn\’t the volatility (and resultant premiums) have gone up post the announcement, since the results were better than expected?

2. This trader only made money b\’cuz the Call option premium did not rise as quickly, right?

B\’cuz if it had, he/she would\’ve lost money or made lower profits, right?

Basically, he/she got lucky?

3. Due to the call option premium not rising as quickly, a person who, for example, took a long straddle instead of a short straddle, would\’ve lost money if he/she closed the trade?

If yes, what should the people who took a long straddle do in this case?

4. A person who took a long straddle would\’ve made a profit if the price of Infy (and the call option premium) would\’ve gone higher than the upper breakeven, correct?

5. Regarding your question at the end, if the combined delta of the options post a market movement is +0.9, we will have to short futures to become (approximately) delta neutral, right?

6. Also regarding your question at the end, if we take Futures positions to delta hedge, won\’t we end up losing money?

7. How often/in what interval should delta hedging be done – every day/every week..?

8. It\’s 2022. Have you done a chapter on delta hedging?

1) Volatility increases when there is uncertainty in the market, when the event unfolds, volatility tends to decrease

2) It was designed for such an outcome, not a random trade right?

3) Yes

4) Yup

5) Yes

6) Not really, since you are hedged out

7) As and when the position delta changes

8) Nope, decided not to do since its an very expensive affair for most retail participants. Please see the comments.

Hi,

Could you please clarify this.

if I initiate short Straddle of SBI at strike price of 520, what are the settlement/delivery rules if price on expiry date is 518/ 522. i.e., Should I have margin for purchase of stock when price on expiry date is 518 / should i deliver the stocks when price on expiry date is 522. Or both 520 PE and 520 CE cancel each other?

Thank you.

So the easiest way to figure this is to remember that whichever option is ITM, it becomes due for physical settlement. If both the options are ITM, they can net off and cancel the physical settlement.

Hey. Let\’s assume for the above mentioned Infosys example ,as the market moves up the CE sell becomes ITM and delta goes to 0.6 and the PE sell becomes OTM and delta goes to -0.4, So the net delta becomes 0.2 ! Now can I hedge the position by selling one more put option of delta -0.2 ? to make the position neutral? (provided I have enough capital to make more adjustments)

Thank you!!

Yup, you can. This is how you keep positions delta neutral 🙂

1)I CAN SELL (SHORT)ONE PAIR OF BANK NIFTY MEANS WHEN I CAN SQUARE OF

2)IF I HAD SHORT THE OTM BANK NIFTY AND I FAILED TO SQUARE OF ON EXPIRY DATE MEANS WHAT WILL HAPPEN

3)JUST CONSIDER

TODAY IS 1ST JAN AS MONDAY

3RD JAN THURSDAY

10TH JAN IS THURSDAY

I CAN SHORT 1OTH JAN CONTRACT ON 1ST JAN OR NOT

IF I SHORT MEANS WHEN I WANT TO SQUARE OF

I CAN SHORT OTM CONTRACT OF 10TH JAN ON 1ST JAN

To short the bank nifty contract what is the requirement of cash in my account

Perumal, you can square off any time you wish, no need to wait till expiry for this.

Hi Karthik, hope you are well mate.

I am going through all the modules however didn\’t find any chapter on delta Hedging. Do you mean to use same technique which you told in Future to hedge the PF with Beta calculation.

Regards, D

Hi Dipak, yes delta hedging is not available for now. Will try and put that up sometime soon.

Hi karthik

Thanks for a wonderful content you for us. Can you please elaborate how to adjust short straddle or to keep delta neutral. I am new to option selling. I need your help.

Thanks

Irshad Alam

Irhsad, I\’m not a big fan of adjusting these positions are it consumes a lot more capital. But anyway, the end objective is to ensure we have a delta neutral position. So at any point, add up the deltas and figure if the overall position is +ve or -ve. Take up positions in such a way that it remains so even when markets move in a direction. For example, say you shorted ATM CE and PE. The market moves down, Puts gain in delta, overall position turns +ve, in this case, you may want to add another CE.

Hi Sir, regarding how the delta varies when market moves. I am confused here as to why the strategy becomes non-delta neutral when the market moves. If we see the delta values. When strategy is executed it has delta = 0 ( ATM ) but if market moves down then one of them becomes ITM ( 0.7 ) and the other OTM ( 0.3 ) , even then the overall delta is neutral. Am I missing something here?

It will be +0.7 and -0.3. So overall delta is +0.4, so it\’s not delta neutral.

Thank you for your immediate response sir .

since you have mentioned about the Volatility risk!

is the any way to reduce volatility risk?

since I am adding positions to keep delta as zero!

One of the ways to hedge volatility is by trading the ViX futures. But I guess that\’s not possible now. Your best bet is to reduce directional risk.

Hi Karthick,

I can also do adjustments to make my position delta neutral right and necessarily Futures?

let say I do a short straddle on 17500 on NIFTY

so my net delta is 0 , however lets say the market moves to 18000

so my 17500CE delta would be 1 and my 17500PE would be 0.1 (assuming) so net I\’m at -0.9 delta

so I can do delta hedging by selling one more PE STRIKE which has delta 0.9 so as to make my position neutral ?

When you initiate a straddle you are obviously delta neutral. But as the markets move, will your position still remain delta neutral? If yes, why do you think so? If no, then is there a way to keep the position delta neutral?

does this the question which you had mentioned above?

and does this also count as \”delta hedging\” by adding one more position to make it delta netural?

Exactly, that\’s how you keep adjusting your position to ensure the overall delta is 0. By doing so, you are eliminating the directional risk and sticking just to the volatility risk.

Hi

If i have have short straddle position, if i dont square off at expiry, what will happen, will i get premium or do i have to square off

Thanks

If both the options expire worthless, then you get to keep the premium.

what if I apply this short straddle on Wednesday one day before expiry will it be profitable ???

Everything depends on how the market moves right?

Hi

I would like to knw how the delata calculated when the lots is increased

Delta remains the same, Shahul. When lots increase, the delta is added up, as I\’ve explained in the chapter on Delta.

whether short position in ce can be adjusted with short position in PE

Short CE is bearish, like long put.

At the time of entering Straddle, is it necessary that premium of both leg should be same or almost same?

They should be more or less the same, Suhas.

Hello Sir,

Sometimes entering 4 legged strategies and exiting 4 legged strategies are extremely difficult as you have to do it one by one.

Even If I set up a basket order, they would go at mkt and not limit.

So is there a better way I could do this?

Ah no. You have two options – baskets or exit 1 by one.

Hi it says loss mai be unlimited but what if use stop loss for both the legs lets suppose 40% and lets suppose market starts to go down pe will hit the stop loss and ce will continue to gain so still we can be in profit right ?

Yes, if you use SL then you can cut your position early and manage your positions.

Let say for the infy example,as the market moved the CE becomes ITM and delta goes to 0.8 and the PE the delta goes to -0.3, the net delta is 0.5…how would buying a future option help in this case?

Do i have to short more ATM puts which have delta of 0.5 to manage the same?

If you want to maintain delta neutral, then you need to short an ATM option, that way the position will have a neutral delta.

Thanks to kartik sir for providing us with quality education.

When the market moves upwards, CE would become ITM and PE would become OTM resulting in a (-) delta in the short straddle. Can\’t we make it delta neutral by shifting the PE to higher strikes which are ITMs at the time of adjustment?

You can, but the adjustment can be quite complex and involve higher costs. But if you were to do it, then you need to ensure the deltas always add up to 0. So you may have to sell the option that has moved or buy more of the lower delta options.

can we have same knowledge with latest examples and some new strategies as this was published around 5-6 years ago and I have started trading/investing around 1 year back

Nothing really changes much now, Sanket. The concepts remain the same.

Hello Sir,

Reliance Ind has its AGM this week.

Its IV has increased substantially while its IVP is roughly in the 90 percentile.

Would it be better to short options or buy options.

Technically it is better to short options but there can be a big move once the news comes.

What exactly can one do?

It depends on your view on volatility. If you expect it to increase further, then you should short option, else you should look at buying. What is your view?

Sir

How to adjust short straddle with options. Please write in detail about short straddle adjustment.

Thank you

Adjustment is a very complicated and expensive process, Abhilash. Not suitable for a regular retail trader. hence I avoided discussing the same.

Hi Karthik

you mentioned about delta hedging by adding futures. is there any other way of neutralising the delta esp using the options.

regards

arun

You can, but gets very complicated.

Hello Sir,

1) Couldn\’t I set up an iron condor on monday morning and then square of my positions once the results are announced? (Since premium is high)

2) How do I know the time the results are announced? Is it during market hours or after market hours which results in the trade carrying on to tuesday?

1) Yes, you can.

2) You will have to track individual company news for this.

Hello Sir,

I hope you are doing well.

Now Naukri (info edge) has its results out on Monday. (I am not sure about the time the results would be out, Is there a way I can find the time?)

I am confused about whether I should initiate an iron condor or a long straddle.

The results are expected to be good, but no one can predict where the market moves.

The IVs for Naukri are slightly on the higher side right now.

If its Monday, then maybe its a bit late. I guess you should paper trade this one and be prepared for the next event. This is just a suggestion.

Hello Sir,

How does one identify said threshold.

Ideally when is the best time to implement a strangle straddle shot iron butterfly and short iron condor?

There is no predefined best time as such. Really depends on how the market develops.

Hello Sir,

In the Infy example above, why did the person not initiate the trade 1 day before the result? The IV would have been at its peak 1 day before the result and it would have resulted in a higher premium gain for him.

Ah, not really sure. But one reason could be that the IVs may hit a threshold and stay there till the event. Not necessary that it keep increasing till the D day.

hi karthik,if i have to intitiate short straddle in banknifty with stoploss and target orders together initially i used to do as bracket order but since bracket orders are stopped how can i initiate such short straddle with stoploss and target order together on zerodha,kindly guide?

BO was not possible for short straddle anyway. Anyway, yes, you can use GTT for this.

What happens when we don\’t choose ATM strike? Suppose BN is 35100 today and I go for 35500 short straddle, or may be 34600 short straddle

You won\’t get a perfect short straddle if you move away from ATM.

Hi Sir,

Just a question.

Selling a call is Bearish and Selling a Put is bullis

Selling a Call and a Put are opposite strategies which would cancel each other in the event of physical delivery correct?

If you sell a call and put together shouldn\’t the margin decrease by that logic as the two options are hedged against each other?

I get your point, but you are exposed to downside risk in both legs. Hence margins dont increase..

Your way of explaining the things are very simple and super. I learned everything from Varsity. Thank you very much. But, I always regret, why I haven\’t started reading before I start trading. Else, I would have had not booked losses.

I observed one thing.. you can make make consistently buy sell options with straddle strategy. The RR ration won\’t be applicable hear. Only the possibility will be applicable, considering black swan moment once in 7 years.

Believe me or not, I got this idea of selling just observing the markets and making data point. I never heard about the straddle and strangle. I was wondering, why buying the options before the result day not giving profits.. Now I understand from this blog that IV are high hence premiums are high. I will test the system in this direction now. Thanks a lot for the knowledge.

Thanks, Arun. I\’m glad you liked the content on Varsity! Happy learning 🙂

Thank you for this amazing chapter and module, 🙂

In the short straddle strategy, let\’s say when market moves high. The Call option of ATM strike will now expire as deep ITM. So delta here will approximately be close to 1. Since we have shorted CE, delta will be -1. Opposite to this when price of underlying increases at expiry, ATM put will expire as worthless OTM option so delta here will be close to zero. Hence net delta at expiry will be = Delta of CE + Delta of PE = -1 + 0 = -1.

To make Delta equal to zero, we would need to add some instrument which has delta =1.

We can Buy futures contract of same expiry series or we can buy ITM Call option (i.e. squaring-off Short CE option executed for short straddle)

Yes, Vaishal. The thing with straddles and strangles is that they are delta neutral when initiating but the delta-ness changes as the market moves. YOu can adjust this with futures, to ensure it\’s delta neutral. But this will always be an expensive affair.

Dear Sir,

With the onset of new events like quarterly results etc, the volatility always increases.

Would there be a case where it does not increase

Volatility does not always increase with events, it really depends on the events per say.

Hello Sir,

1) Should Short Strangles/Straddles be implemented the day before the result as that would have the highest premium due to volatility being the highest?

2) Lets say the result is good and market moves in a direction, could I exit the losing option and retain the winning one?

3) For Long Strangles and straddles I could just buy the options 4-6 days before and square off immediately after the result. Assuming I feel that there would be a good result?

1) yes, but this depends on the event and the kind of volatility it induces in the market

2) Yes

3) Yes and assuming the volatility also increases

7600 CE is trading at 77

7600 PE is trading at 88

In this case if you put a stop loss of (77) for the CE, and (88) for PE, say if the market moves in one direction,say up , then loss from CE will be zero ( 77 received in premium- stop loss from CE(also 77)). You get to keep the PE premium of 88.

So overall you end up in profit, if the markets goes down, you keep the call premiums and lose the put premiums. If the market goes up and then down, you lose both premiums. You still don\’t end up in loss.

This sounds a bit simplistic, do you think this works out in real trading?

Yeah, sounds simplistic 🙂

In reality, you will have to consider other variables like volatility and time and assess its impact on the premium.

Hi Sir, please explain why have you suggested to take position 3-4 days earlier than the result date – in the Infosys example?

To ensure you capture premium which is expected to be higher owing to higher volatility.

When it to implement for better result, first half of the expiry or second half of the expiry or very first day of the starting of a expiry series?

Depends on the market and the opportunity it provided 🙂

Dear Sir,

In case of currency option trading, short straddle is beneficial for which one, weekly or monthly option contract?

If done right, its works across all expiries.

Hello Sir,

Have you written about Delta, Gamma hedging in any of these chapters?

Yes, please do check the previous module.

Hello, Just a minor typo. thru this chapter and previous chapter. I think \”breakeven\” is referred as \”breakdown\” in all the occurrences. Thanks

Ah, need to check this. Thanks for pointing this, Easwar.

Sir, you explain everything very well .But I have a doubt in delta hedging. After constructing the short straddle , we buy a future to make it delta neutral. If market goes down sharply , then we lose money both for buying the future as well as writing the put option. Then how this strategy will be helpful

You are delta neutral when you sell the call and put option. By adding a long future, you are more long than short, hence not delta neutral.

Hi Karthik,

Wonderful explanation of short straddle, i really love your articles about trading, but i am still unable to reposition options for delta neutrality. how do i hedge it with futures.

Can u please make a chapter on that ( delta hedging), i see a lot of people asking the same.

Perhaps, Lakshmi. I\’m on the last chapter for personal finance, will probably do that once this is done.

1. I have two questions as follows

a) Can we make long straddle delta neutral by selling the future

b) Is Delta neutral is also possible by constructing a short straddle in the current expiry week and long straddle in the next expiry week simultaneously.

c) If b is correct then which will be beneficial short straddle in current week/long straddle in next week expiry or long straddle in current week/short straddle in next week expiry simultaneously

1a) Not really, by selling future, you add more to the short side

b) Yes

c) It does not really matter

Hi sir what if, once the market has moves and deltahas changed so we take a long position on it on each side of our short,can that be workable will that make delta neutral ??please relpy your reply will surely be appreciated Thanks sir for this chapter.

Atul, the easiest way to figure of you are delta neutral is by adding up the deltas. The sum of all the deltas across your positions should add up to 0, if yes, then you are delta neutral.

Hi sir,

In above case study what if,

As results announced @ 9:18am and due to great results market direction will start to moving up. Hence isnt it make sense to square- off the loss making leg (1140CE) and sticking to profit making leg (1140CE).

Will it be efficient or there is any risk to deploying this?🤔

Yes, you can. In fact, people do this quite often. But once you square off and ride on a single option position, then you are exposed to directional risk, you just need to be aware of this.

Hello Mr. Karthik

Very big fan of your writing and cheers to Team Zerodha for blessing us with Varsity.

In the previous module, if I\’m not wrong I remember learning that ATM options have relatively high gamma which eventually makes the deltas change rapidly. So my question is how would shorting the ATM strike would put us in a profitable position considering that aspect. Please educate me if I\’m wrong. Thanks

Thats right, Tharun. However, these are not naked shorts. These shorts are always hedged in spreads.

When we invoke the straddle then automatically we are insulated from the market direction, so where so ever the market will move, our position will remain delta neutral.

Right???

Great article

Happy reading!

Hey Karthik,

Writing you to share high adrenaline rush experience I faced while doing short iron butterfly on Mindtree, my first ever options strategy!!!

Hopefully, with your expert comments, other budding strategy executors will get some ready made experience from this episode and avoid potential mistakes. Based upon my analysis over the weekend, I wanted to do the following:

Mindtree spot as of Friday – 1393

Buy PE 1340 strike at 12

Sell PE 1400 strike at 50

Buy CE 1460 strike at 5

Sell CE 1400 strike at 23.55

I was all set to execute this trade this morning in the above order and also made ensure the sufficient margin for these positions using options calculator. Here is what happened:

1) I entered my buy PE order and left MARKET ORDER by default. To my horrific surprise, system executed this order at 18 and in a few moments dropped down to 7. As mentioned above, Friday\’s price for this leg was 12

2) For other legs, it took me various hits and trials to get it executed as either the strike prices were not available in the option chain or the order did not get executed as per my preferred price

3) Clearly, the difference in prices for my strikes skewed the entire risk/reward, making this trade less worthwhile

Now, I have reverse problem for squaring off these trades as some of the bids or offers are not available for the above strike prices.

Can I request you to share urgently what is the best way to get out of this trade well before expiry (say by wednesday) and future learnings for me and fellow options traders?

Many thanks,

Rajan.

1) Rajan, how did you place a market order on Mindtree? We don\’t allow market orders on stock options.

2) All strikes made available will be available on the trading terminal across all brokers.

3) Yes, execution risk is a big factor to consider.

Yes, that\’s true that ATM offers max profit/premium. But how can I know like this ATM price is perfect to make short straddle? How to select best ATM price for stocks or indices.

There is only 1 ATM strike for both CE and PE, so there is nothing to choose from 🙂

How to trade short straddle in intraday with stoploss?

Keep the SL as you\’ve estimated on each of the legs individually.

How to select strike price for Short Straddle? so that we will have max chance of getting premium in our favor.

This depends on the time to expiry. Usually, ATM offers the max premium.

To add to above, I observed the same when the underlying price was going down, and both PUT and CALL premiums were rising.

Ok. Do check my previous response.

Hi Karthick,

To check the Short Straddle strategy I was first doing virtual trading on Sensibull. I sold PUT and CALL options both of TCS. I noticed that as the underlying price of TCS moved up from ATM the Option premium of both PUT and CALL (of the ATM I shorted) was rising and I was in a loss in both PUT and CALL .

I noticed this for around 10 min and then TCS underlying price again started coming done. Was the increase in premium for PUT option b/c of change in IV?

If yes then how frequently does IV change for a strike price. Also are you aware of some FREE OPEN Rest endpoints which can return Option contract real-time.

Thanks.

Yes, the change can be attributed to IV change, although I suspect this won\’t have been a big change (considering a 10-minute window). Not sure about the data you\’ve asked. I\’m aware of this, but it is paid and I\’m not sure if its the same format you\’d need – https://www.nseindia.com/market-data/real-time-data-subscription

Hi,

This week starting , atm 11400 ce and pe is combined 250rs and next week atm 11400 ce and pe is combined is 350and the difference is 100. Always this week and the next week atm options difference is same or it changed, if it changed how and why..thanks

Premiums keep changing due to various reasons, bid and ask included.

Sir,

I sold both oct 1 expiry at the money 11500 ce and pe , nifty is at 11500 and brought 24 sep expiry 11500 ce and pe .Hear what is my max risk and reward for intraday and expiry.. please answer my question thanx

I\’d suggest you use this tool https://web.sensibull.com/options you\’ll not only figure the max, min P&L, but can also visualize it.

Hi Karthik,

I was looking to sell the Far OTM call option for weekly expiry nifty. ie. priced at Rs2.45 now (this has a ITM probability of 7%)

If i sell 1 lot, the premium will be Rs2.45*75 =183.75

But the brokerage i would need to pay is 20*2 = 40

which means the nett i can win here is 183.75-40 = 143.75 (excl. STTs)

This makes me uncomfortable writing this option. Is there any option to bring the futures pricing of 0.03% or Rs20 whichever is lower for options also ?

@street_trader_666

i would like to correct you, when you adjusts your deltas after the position has moved from being delta neutral it is referred as GAMMA HEDGING as gamma has added or removed deltas. delta hedging is when you establish delta neutrality or become directionally neutral when you establish a trade by simultaneously buying or selling the underlying.

and I believe the worst case of such position is one sided sharp move on either side. what if even after covering deltas the underlying keeps moving in a single direction, this will create even more deltas. so covering deltas will become expensive like Mr. Karthik said. Any further adjustments would cost even more, it will also increase your exposure in the underlying significantly. so a trader needs some experience to decide when to hedge and when to leave deltas open. also a trader can hedge by partially leaving some delta open to cover later if the possibility of one sided move is high.

With response to the question posted at the end of chapter, the only thing that could add or subtract more deltas and move one’s position from being delta neutral is GAMMA.

With GAMMA in mind, I suggest for the sake of all people interested in learning options deeply and deploying such delta neutral spreads, you mention the concept of gamma theta trade-off that the trader has to face when setting such delta neutral spreads and explain briefly about the effect/risk that gamma and theta can pose, and their directly proportional relationship. For example, it will help traders to know not to trade short straddle near expiry as gamma is highest, or even long straddle since the theta is also high. So risk factor is increased significantly near expiry.

Basically, if one want’s to market to move, passage of time hurts. If one wants market to stay still, passage of time helps. No trader can have it both ways

Thats true, you said it well, no trader can have it both ways 🙂

Gamma risk is the most misunderstood and complex risk wrt options. I\’ll try and dig deeper into this at some point and put up supplementary notes

as the delta of the position turns negative or positive we can neutralize the delta again by buying or selling of shares with the same delta.

example : – If the delta turns positive to +55 = short 55 shares of infosys.

if the delta turns negative to -10 = buy 10 shares of infosys.

this is one out of many ways to keep the short straddle delta neutral.

as we know the volatility crunch and theta decay is in our favor and the profitability increases.

the worst case in this delta hedging is when the markets rallied back or drop back to the strikes of the short straddle, we will miss out some profits by delta hedging.

Yup, that makes sense. Its an expensive affair though 🙂

hi karthik, how can i chart option spread as a whole. suppose i enter into a strangle and want one chart chart of combined premium

Ah, I think is is possible on Sensibull. Please do check with them once.

Hi

I want to understand one thing. Do we have to hold the strategy till expiry and not square off our position even on the day of expiry ? Because in the payoff, the difference of strike price is also considered.

Kindly elaborate.Thanks

Yes Pankaj, these are mainly with the expectation that the position is held to expiry. However, you can square off the position just before expiry.

Hello Karthik,

As someone said here that– \”As the market moves, position won’t be delta neutral any longer. In order to bring the position back to delta neutral one can make use FUTURE as it carries delta of 1. Options can also be used for the same. This strategy is a very good strategy for traders who just want to earn the TIME VALUE OF MONEY. The only catch is it is a very HIGH RISK – HIGH REWARD strategy.\”

I know that using futures can sum up the deltas to zero but nonetheless we\’re still using some options right? The deltas do change for the options, for e.g if I short two options with delta -0.5 and buy one futures at that time. But gradually the delta of the two options that we shorted will change and deltas won\’t sum up to -1.

Then why bother having a futures contract if the deltas change anyway

Its an assumption that it will hit 1, what if it is any other value?

Dear Karthik,

Thank you so much for your guidance, will definitely work on this.

with time I will develop more confidence in directional trade.

I am so thankful to you and varsity, I have utilize my lockdown time really well.

I will keep taking your help and advice shamelessly. I believe a teacher is 100 times better than 10000\’s of any influencer.

Good luck, Anil. I hope you continue to stay profitable 🙂

Took ATM Delta neutral strategy as well and this too is in profit. Risk & Margins are much lower compared to ITM for obvious reason.

the only reason I took ITM because puts premium has gone up over the last few days and expected it to fall.

I do try with bear put spread. and the only reason I am doing delta neutral is too avoid directional risk.

otherwise, OTM delta neutral strategy is giving good profit with minimum risk and less margin.

I am getting confident in building and executing trades. Thank you so much.

Thanking you is what I can do for now before I come and see you in Banglore.

Nice 🙂

Your profitability is always higher when you take directional bets, for example in this case you were bearish, so you need to take that bet. I\’m not saying market neutral is bad, 9 out of 10, I\’d prefer market neutral strategies…which implies getting the direction is hard, but when you do, you should bet. Of course, this makes sense only if you are super convinced about your directional view.

Sold Tata motors, 125 PE and 85 CE, both ITM. Collected Rs. 46 Premium

View on Tata Motors:

Bearish view post result.

IV: 95 and IVP – 73% higher than Historical IV.

PCR: 1.03.

Expectation:

IV will fall post result and had a bearish view based on fundamental analysis.

It was unlikely that tata motors will break its support 85 and resistance 125.

Expected IV and PCR to fall.

As per ND method, 1SD: lower range 90 and upper range 130.

My thought before trade:

Sell 125 PE and Sell 85 CE, premium and volatility will come down.

To protect against the directional move I choose Delta neutral strategy but on ITM options.

Holding Period: 8-10 days

Result:

Tata Motors fell from 105 to 95

Total premium fell from 46 to 36.

As there was a shift in the delta, to make it delta-neutral again, sold 115 CE.

Total Profit: 31175/-

Dear Karthik, please let me know if the thought process is right or how I can improvise this trade.

Anil, yes, thats right. Few things though –

Why are you doing this with ITM options and not ATM? I agree, you\’d have opted for ITM for higher premium collection but it comes with a higher risk. So do think about this. Maybe put some numbers down and figure what would have happened if you had shorted ATM strikes. Also, if the view is bearish, why delta neutral? Maybe you should have set up a bear put spread?

let us say currently banknifty ATM is 19900 and so if I follow this strategy I will sell 25 June 19900 CE and 19900 PE which have premiums of about 900 each. Along with that, I want to hedge the position by buying 19900-900 = 19000 PE AND by buying 19900+900=20800 CE for which I need to premium of 39 and 42 respectively in weekly series.

My doubt is that the will this above process can make my position delta neutral? My idea is to make the loss = 0. If there anything wrong in above process. Can you please correct me. Thank You

This will ensure that you are protected on either side, and your profit will continue to remain within the range i.e. between the upper and lower breakevens.

In case of any event by using short straddle, if the price goes below LB or Above UB we will be in loss. Can we minimise that loss by buying put option below LB and call option above UB. If so, can you please explain. I am new to options trading. Thank You

Yeah, you can but deep OTMs and protect the position. You will be paying for the premium but its ok.

Sir,

I wanted to know whether any brokerage is being charged for BUY side if I sell a naked option and let it expire OTM option having closing premium as zero on expiry day. My brokerage is charging brokerage and GST for zero premium call expired.

No brokerage if you let an OTM option expire.

At the end of the discussion on the short straddle, there is a excel template that can be downloaded. My qn is: for the short straddle, this excel template shows a number against \”max loss\”. And also shows \”Unlimited\” as the Max profit.

Isnt this incorrect?

Short stradde: max loss is unlimited – as I have understood this.

Appreciate a revert.

Tx

Yes, for both straddle and strangle, max loss to stretch to unlimited.

Hello Karthik,

I am novice in share market. I liked the way you have explained short straddle but I am skeptical about the figures that you have presented. If the nifty changes from 7600 to 7200 or 8000, so will it\’s premiums for call and put. Then, why all PL calculations are done using constant premiums (77 & 88)? Can the losses be capped by applying stop loss?

The premium is constant from your perspective. Once you enter a trade, the premium at which you\’ve entered becomes fixed for your trade.

Regarding the question asked, I think for small changes, net delta will remain ~0. But in case there are major changes in price, let say the spot is 7700 now from 7600 earlier, CE delta will be around ~1 while PE delta will be around ~0.

So the net delta would be ~1 (-1 since it\’s a short position).

As long as the underlying changes, there will is a non -zero change in delta. It is just that for major changes, the change in the delta is more tangible.

Edit: A short straddle at the start of the day and a long straddle at around 2 pm.

Figured as much 🙂

Hi Karthik Sir,