7.1 – Spreads versus naked positions

Over the last five chapters we’ve discussed various multi leg bullish strategies. These strategies ranged to suit an assortment of market outlook – from an outrightly bullish market outlook to moderately bullish market outlook. Reading through the last 5 chapters you must have realised that most professional options traders prefer initiating a spread strategy versus taking on naked option positions. No doubt, spreads tend to shrink the overall profitability, but at the same time spreads give you a greater visibility on risk. Professional traders value ‘risk visibility’ more than the profits. In simple words, it’s a much better deal to take on smaller profits as long as you know what would be your maximum loss under worst case scenarios.

Another interesting aspect of spreads is that invariably there is some sort of financing involved, wherein the purchase of an option is funded by the sale of another option. In fact, financing is one of the key aspects that differentiate a spread versus a normal naked directional position. Over the next few chapters we will discuss strategies which you can deploy when your outlook ranges from moderately bearish to out rightly bearish. The composition of these strategies is similar to the bullish strategies that we discussed earlier in the module.

The first bearish strategy we will look into is the Bear Put Spread, which as you may have guessed is the equivalent of the Bull Call Spread.

7.2 – Strategy notes

Similar to the Bull Call Spread, the Bear Put Spread is quite easy to implement. One would implement a bear put spread when the market outlook is moderately bearish, i.e you expect the market to go down in the near term while at the same time you don’t expect it to go down much. If I were to quantify ‘moderately bearish’, a 4-5% correction would be apt. By invoking a bear put spread one would make a modest gain if the markets correct (go down) as expected but on the other hand if the markets were to go up, the trader will end up with a limited loss.

A conservative trader (read as risk averse trader) would implement Bear Put Spread strategy by simultaneously –

- Buying an In the money Put option

- Selling an Out of the Money Put option

There is no compulsion that the Bear Put Spread has to be created with an ITM and OTM option. The Bear Put spread can be created employing any two put options. The choice of strike depends on the aggressiveness of the trade. However do note that both the options should belong to the same expiry and same underlying. To understand the implementation better, let’s take up an example and see how the strategy behaves under different scenarios.

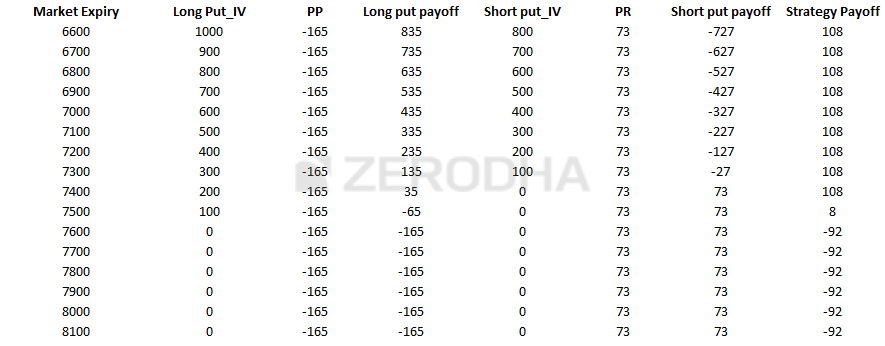

As of today Nifty is at 7485, this would make 7600 PE In the money and 7400 PE Out of the money. The ‘Bear Put Spread’ would require one to sell 7400 PE, the premium received from the sale would partially finance the purchase of the 7600 PE. The premium paid (PP) for the 7600 PE is Rs.165, and the premium received (PR) for the 7400 PE is Rs.73/-. The net debit for this transaction would be –

73 – 165

= -92

To understand how the payoff of the strategy works under different expiry circumstances, we need to consider different scenarios. Please do bear in mind the payoff is upon expiry, which means to say that the trader is expected to hold these positions till expiry.

Scenario 1 – Market expires at 7800 (above long put option i.e 7600)

This is a case where the market has gone up as opposed to the expectation that it would go down. At 7800 both the put option i.e 7600 and 7400 would not have any intrinsic value, hence they would expire worthless.

- The premium paid for 7600 PE i.e Rs.165 would go to 0, hence we retain nothing

- The premium received for 7400 PE i.e Rs.73 would be retained entirely

- Hence at 7800, we would lose Rs.165 on one hand but this would be partially offset by the premium received i.e Rs.73

- The overall loss would be -165 + 73 = -92

Do note the ‘-ve’ sign associated with 165 indicates that this is a money outflow from the account, and the ‘+ve’ sign associated with 73 indicates that the money is received into the account.

Also, the net loss of 92 is equivalent to the net debit of the strategy.

Scenario 2 – Market expired at 7600 (at long put option)

In this scenario we assume the market expires at 7600, where we have purchased a Put option. But then, at 7600 both 7600 and 7400 PE would expire worthless (similar to scenario 1) resulting in a loss of -92.

Scenario 3 – Market expires at 7508 (breakeven)

7508 is half way through 7600 and 7400, and as you may have guessed I’ve picked 7508 specifically to showcase that the strategy neither makes money nor loses any money at this specific point.

- The 7600 PE would have an intrinsic value equivalent to Max [7600 -7508, 0], which is 92.

- Since we have paid Rs.165 as premium for the 7600 PE, some of the premium paid would be recovered. That would be 165 – 92 = 73, which means to say the net loss on 7600 PE at this stage would be Rs.73 and not Rs.165

- The 7400 PE would expire worthless, hence we get to retain the entire premium of Rs.73

- So on hand we make 73 (7400 PE) and on the other we lose 73 (7600 PE) resulting in a no loss no profit situation

Hence, 7508 would be the breakeven point for this strategy.

Scenario 4 – Market expires at 7400 (at short put option)

This is an interesting level, do recall when we initiated the position the spot was at 7485, and now the market has gone down as expected. At this point both the options would have interesting outcomes.

- The 7600 PE would have an intrinsic value equivalent to Max [7600 -7400, 0], which is 200

- We have paid a premium of Rs.165, which would be recovered from the intrinsic value of Rs.200, hence after compensating for the premium paid one would retain Rs.35/-

- The 7400 PE would expire worthless, hence the entire premium of Rs.73 would be retained

- The net profit at this level would be 35+73 = 108

The net payoff from the strategy is in line with the overall expectation from the strategy i.e the trader gets to make a modest profit when the market goes down.

Scenario 5 – Market expires at 7200 (below the short put option)

This is again an interesting level as both the options would have an intrinsic value. Lets figure out how the numbers add up –

- The 7600 PE would have an intrinsic value equivalent to Max [7600 -7200, 0], which is 400

- We have paid a premium of Rs.165, which would be recovered from the intrinsic value of Rs.400, hence after compensating for the premium paid one would retain Rs.235/-

- The 7400 PE would have an intrinsic value equivalent to Max [7400 -7200, 0], which is 200

- We received a premium of Rs.73, however we will have to let go of the premium and bear a loss over and above 73. This would be 200 -73 = 127

- On one hand we make a profit of Rs.235 and on the other we lose 127, therefore the net payoff of the strategy would be 235 – 127 = 108.

Summarizing all the scenarios (I’ve put up the payoff values directly after considering the premiums)

| Market Expiry | Long Put (7600)_IV | Short Put (7400)_IV | Net payoff |

|---|---|---|---|

| 7800 | 0 | 0 | -92 |

| 7600 | 0 | 0 | -92 |

| 7508 | 92 | 0 | 0 |

| 7200 | 400 | 200 | +108 |

Do note, the net payoff from the strategy is in line with the overall expectation from the strategy i.e the trader gets to make a modest profit when the market goes down while at the same time the losses are capped in case the market goes up.

Have a look at the table below –

The table below shows the strategy payoff at different expiry levels. The losses are capped to 92 (when markets go up) and the profits are capped to 108 (when markets go down).

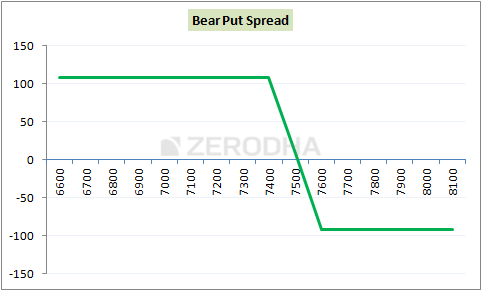

7.3 – Strategy critical levels

From the above discussed scenarios we can generalize a few things –

- Strategy makes a loss if the spot moves above the breakeven point, and makes a profit below the breakeven point

- Both the profits and loss are capped

- Spread is difference between the two strike prices.

- In this example spread would be 7600 – 7400 = 200

- Net Debit = Premium Paid – Premium Received

- 165 – 73 = 92

- Breakeven = Higher strike – Net Debit

- 7600 – 92 = 7508

- Max profit = Spread – Net Debit

- 200 – 92 = 108

- Max Loss = Net Debit

- 92

You can note all these critical points in the strategy payoff diagram –

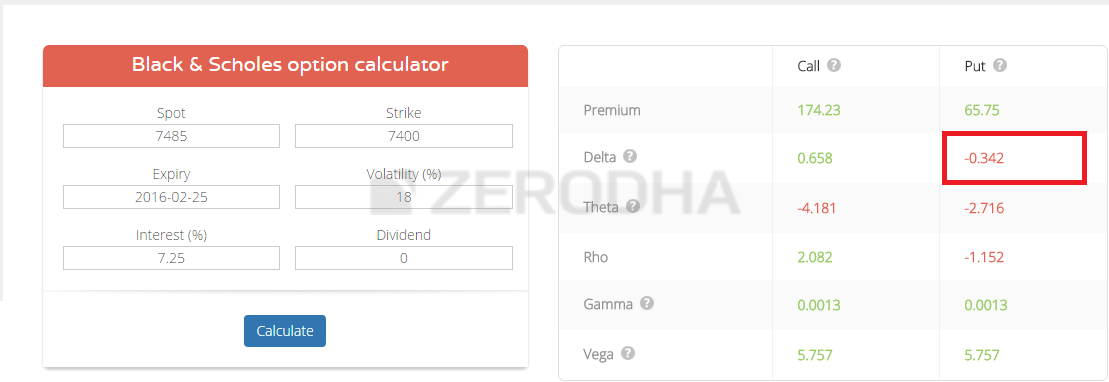

7.4 – Quick note on Delta

This is something I missed talking about in the earlier chapters, but its better late than never :-). Whenever you implement an options strategy always add up the deltas. I used the B&S calculator to calculate the deltas.

The delta of 7600 PE is -0.618

The delta of 7400 PE is – 0.342

The negative sign indicates that the put option premium will go down if the markets go up, and premium gains value if the markets go down. But do note, we have written the 7400 PE, hence the Delta would be

-(-0.342)

+ 0.342

Now, since deltas are additive in nature we can add up the deltas to give the combined delta of the position. In this case it would be –

-0.618 + (+0.342)

= – 0.276

This means the strategy has an overall delta of 0.276 and the ‘–ve’ indicates that the premiums will go up if the markets go down. Similarly you can add up the deltas of other strategies we’ve discussed earlier – Bull Call Spread, Call Ratio Back spread etc and you will realize they all have a positive delta indicating that the strategy is bullish.

When you have more than 2 option legs it gets really difficult to estimate the overall bias of the strategy (whether the strategy is bullish or bearish), in such cases you can quickly add up the deltas to know the bias. Further, if in case the deltas add to zero, then it means that the strategy is not really biased to any direction. Such strategies are called ‘Delta Neutral’. We will eventually discuss these strategies at a later point in this module.

Also, you may be interested to know that while the delta neutral strategies are immune to market’s directional move, they react to changes in volatility and time, hence these are also sometime called “Volatility based strategies”.

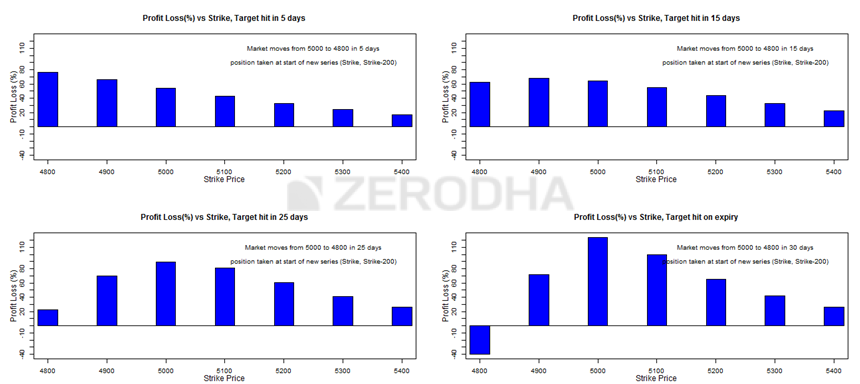

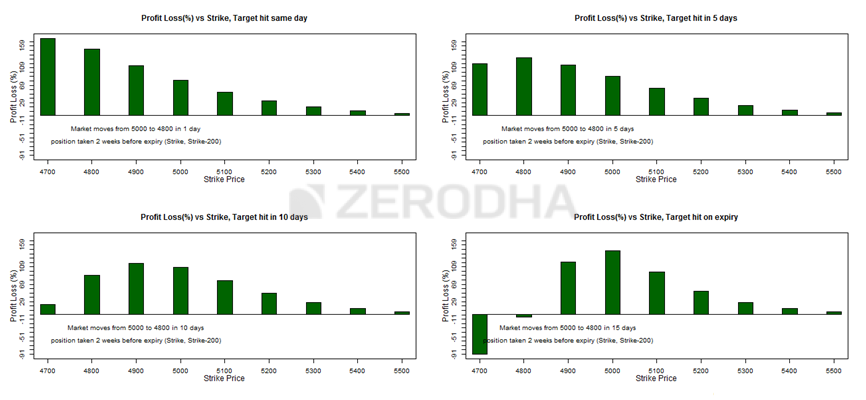

7.5 – Strike selection and effect of volatility

The strike selection for a bear put spread is very similar to the strike selection methodology of a bull call spread. I hope you are familiar with the ‘1st half of the series’ and ‘2nd half of the series’ methodology. If not I’d suggest you to kindly read through section 2.3.

Have a look at the graph below –

If we are in the first half of the series (ample time to expiry) and we expect the market to go down by about 4% from present levels, choose the following strikes to create the spread

| Expect 4% move to happen within | Higher strike | Lower strike | Refer graph on |

|---|---|---|---|

| 5 days | Far OTM | Far OTM | Top left |

| 15 days | ATM | Slightly OTM | Top right |

| 25 days | ATM | OTM | Bottom left |

| At expiry | ATM | OTM | Bottom right |

Now assuming we are in the 2nd half of the series, selecting the following strikes to create the spread would make sense –

| Expect 4% move to happen within | Higher strike | Lower strike | Refer graph on |

|---|---|---|---|

| Same day (even specific) | OTM | OTM | Top left |

| 5 days | ITM/OTM | OTM | Top right |

| 10 days | ITM/OTM | OTM | Bottom left |

| At expiry | ITM/OTM | OTM | Bottom right |

I hope you will find the above two tables useful while selecting the strikes for the bear put spread.

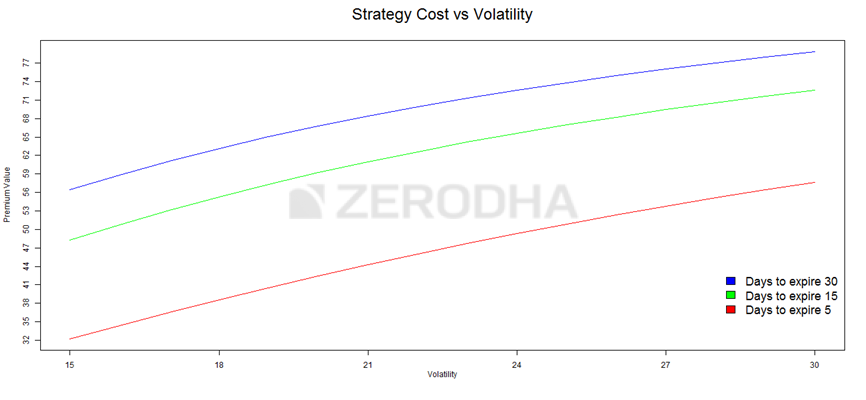

We will now shift our focus on the effect of volatility on the bear put spread. Have a look at the following image –

The graph above explains how the premium varies with respect to variation in volatility and time.

- The blue line suggests that the cost of the strategy does not vary much with the increase in volatility when there is ample time to expiry (30 days)

- The green line suggests that the cost of the strategy varies moderately with the increase in volatility when there is about 15 days to expiry

- The red line suggests that the cost of the strategy varies significantly with the increase in volatility when there is about 5 days to expiry

From these graphs it is clear that one should not really be worried about the changes in the volatility when there is ample time to expiry. However one should have a view on volatility between midway and expiry of the series. It is advisable to take the bear put spread only when the volatility is expected to increase, alternatively if you expect the volatility to decrease, its best to avoid the strategy.

Key takeaways from this chapter

- Spread offers visibility on risk but at the same time shrinks the reward

- When you create a spread, the proceeds from the sale of an option offsets the purchase of an option

- Bear put spread is best invoked when you are moderately bearish on the markets

- Both the profits and losses are capped

- Classic bear put spread involves simultaneously purchasing ITM put options and selling OTM put options

- Bear put spread usually results in a net debit

- Net Debit = Premium Paid – Premium Received

- Breakeven = Higher strike – Net Debit

- Max profit = Spread – Net Debit

- Max Loss = Net Debit

- Select strikes based on the time to expiry

- Implement the strategy only when you expect the volatility to increase (especially in the 2nd half of the series)

Download Bear Put Spread Excel Sheet

In the strike selection graphs shown above, which strike does the graph represent lower strike or the upper strike

Sir, In the bull call spread example

When the market is expected to rise from 8000 to 8300 within 5 days from the start of the expiry then as per the graph 8600 (much higher than the expected rise)is most profitable

But in case of bear put spread example when the market is expected to fall from 5000 to 4800 in 5 days starting from the start of the expiry, as per the graph 4800 (the same as the targeted fall )is most profitable

For getting most profit, Why is the strike much higher than the targeted rise in case of bull call spread ? and why is the strike price the same as the targeted fall in bear put spread ?

This is based on multiple factors – direction of the move, speed of the move, volatility, and time to expiry. These suggested strikes are after factoring in all that 🙂

But once you have also mentioned that market falls much faster than moving upwards. So the speed of the move as you have mentioned above should be higher in case of downward direction.

Yes, but it also depends on the kind of panic 🙂

Thank you for Great work Karthik. After going through this chapter, just wanted to have advise from you. I bought naked December Nifty 23000PE @242 few months back to hedge my stock portfolio (based on recommendation from someone). Looks like this will expire worthless this month. After reading this chapter now just thought that by creating bear put spread maybe I could recover some money back on expiry. Please guide on the following as I am quite new to F&O:

1. Is it better to wait for few days to check if the volatility will increase before initiate the spread? (I thought present volatility not much and hence put premiums seems very low). Do you recommend 1st half or 2nd half to creat spread or any other advise ?

2. What is the recommended strike price to short PE based on my PE buy mentioned above

3. Any other better strategy than bear put spread to recover some money in this situation?

4. For the future, is there any better method to hedge the portfolio than simply buying naked PE and do you recommend spread instead of naked buying of PUT.

Thanks for the kind words, I do hope you continue to enjoy reading on Varsity.

1) Firstly, a hedge should be considered as an expense. But if you insist on recovery, you need two things going for you – increased volatility, decreased time to expiry. So please look for that situation in the market.

2) Short at least 2 -3 strikes away from your current option, this will create a good spread.

3) This seems to be one of the cleanest attempt

4) Nope, its naked position, but treat that as an expense.

Karthik i have an off topic question as I think you being an entrepreneur must have some insight on this

1. Why didn\’t vending machines took off in India ?

2. Suppose I install some coin only vending machines, and suppose at the end of month I have incurred 10,000 in sales but all in coins, so my question is all such business which primarily earns in coins in India, what\’s the procedure to deposit them in the bank ? Like do i have to just fill a bag with thousands of coins & take it to bank Or is there some another procedure ?

I\’m really not sure about the answers to these questions 🙂

But I think the useage of coins has drastically reduced in the country, especially with UPI kicking in 🙂

As far as deposits are concerned, you can deposit them like any other currency notes, right?

Sir,

Grossly, if we divide the time series into three portions as below:

1. Early of the series

2. Mid of the series

3. Late of the series

Which is/are the greek that affect the most for the above three of the series?

All greeks affect the premiums across all periods. But the intensity may vary. For example, theta has a higher effect at the end of the series.

Sir,

You have discussed one section called, \”Strike selection and effect of volatility\”. In that section one graph is drawn for \”Volatility vs premium\” for \”Different days to expiry\”. However, on the top it is written \”Strategy cost vs volatility\”.

I would like to know that this \”strategy cost/ premium\”— Is it signifying the net debit/ net credit which do away during setting the trade? Please confirm.

Yeah, strategy cost is the money required to execute the strategy.

what\’s the difference between \”BULL PUT\” and BEAR PUT\” strategy

One is bearish strategy employing puts and the other one is bullish.

Hello Sir,

You way of making learners understanding is realy worth appreciation but issue that i am facing with these strategies is what if i am having target,and i am not wiling to take my trade upto expiry thn how can i execute the trade?

YOu can still initiate the strategy and hold it up to expiry and square off before expiry.

Sir,

Topic: Strike Selection (and Effect of Volatility)

For 2nd half of series,

Target hits the same day, graph suggests OTM(HS) and OTM(LS)

Targets hits in 5 days, graph again suggests OTM(HS) and OTM(LS)

Target hits in 10days, graph suggests ATM/OTM(HS) and OTM(LS)

Target at expiry, graph suggests ATM (HS) and OTM(LS)

However, the table suggests ITM/OTM(HS) and OTM(HS) for all, should be it ITM or is there a typo here..?

It should, rechecking this.

Thanks!🙏🙏

Dear Sir,

Hope you will excuse me for my dim wit.

Which is higher strike for bear put spread–5000 or 4900?

Higher strike and lower strike is confusing to me.

Regards. Ashutosh

Instead of higher strikes and lower strikes, you can also classify them as ITM and OTM. Anyway, 5000 is the higher strike here.

Hello sir, from our previous discussion on volatility we come to know that when there is ample time to expiry the change in volatility has a higher impact on the premiums so if volatility rises and time to expiry is more shouldn\’t the strategy cost more?

It does right? The premiums are higher when there is more time to expiry.

Where is the correction about delta add up?

Have discussed in the Delta chapter in the previous module.

Thank you Karthik for the strategies series.

I have a question,

\”Please do bear in mind the payoff is upon expiry, which means to say that the trader is expected to hold these positions till expiry\”

I assume this is for the calculation carried out or Are we trying to say that these strategies won\’t be applicable for trading options before expiry?

They are equally applicable, it is just that the payoff will be different. You can use Sensibull for visualizing the payoff before expiry.

Hi Karthik.

can you please share rational behind why in first half of the series with 5 days of expectation on targets, makes far OTM the preferable strike, as opposed to classic bear put strategy: Buy ITM put and Sell OTM put?

I was internalizing which Option Greek could best explain far OTM theory and this is what I found:

1. Delta: The far OTM option has far less delta compared to ITM, this brings far OTM strike the potential to gain delta if the moneyness of the far OTM changes to ITM.

Ex: far OTM put delta is -0.2 then if my directional view(4% bearish) is correct, my far OTM strike would turn either ATM or slightly ITM, making its delta as -0.6, a significant gain of 0.4 as compared to gain potential if we choose ITM strike.

2. Gamma: As we have ample time to expiry I\’d expect all strike to behave same in regards to Gamma

3. Vega: Keeping in mind that we are just moderately bearish, assuming this is true, then the effect of vega on far ITM strike would be more or less similar.

4. Theta: Again, we have ample time to expiry so theta has more or less same effect on all strikes

If I assume my pov on above Option greeks is true, I\’d rule out Gamma, Vega, and Theta as rational behind selecting far OTM option, and would give significance to Delta.

Please share your thoughts, and help me wrap my brain around strike selection.

Thank You in Advance, from my past two comment I see you are very prompt at replying and helping us selflessly : )

Punit, you are right. But when there is ample time to expiry the two greeks that weigh in more than the others are delta and vega, the delta in particular. The direction of the market dictates the premium. The transition of the option from OTM to ITM (when there is more time to expiry) results in a very high percentage change in premium, which leads you to make a sweet ROI in your trade 🙂

doing a great job

Hi Karthik,

Foremost, Thank you for these modules.

Today the Nifty spot price is at 17646.

Please let me know that, can we trade 2 ITM (to be precise Deep ITM).

Example:

18000PE – 326.15 (Buy)

18100PE – 482.30 (Sell)

Please let me know what happens if the Nifty closes in below scenarios.

i) Below 17800

ii) Below 18000

iii) Between 18000 – 18100

iv) Above 18100

When I explore this strategy in Sensibull & Opstra websites, It is showing 0% loss.

Request you to look into this and let me know.

Darshan, I think you would have done 1:1 instead of 1:2, can you double-check that? Check your other input parameters as well. No strategy will have 0% loss 🙂

Sir I get bit confused as what is the logic of getting maximum profit based on time to expiry ….

Eg if we are in first five days we need to trade in option at far out of the money… I know you said that Theta plays important role but can\’t exactly connect the concept in executing the order as selection of strike price is crucial for executing the strategy…. I just don\’t want to mug up the concept but want to understand the very soul of the concept…

Thats good Aditya. But which part is confusing you? If you can tell me that I can try and help you specifically.

please also add option adjustment of every option strategy

Hello Sir,

On what basis do you buy monthly options?

Do you hold them till expiry or do you exit when ever you can?

Whenever opportunity arises 🙂

Hello Sir,

Thanks for the reply.

Suppose I have written 26 august, 15550 PE and bought 15000 pe. This is a fairly large spread and the risk is roughly 500 points if nifty expires on 26 august.

Is it better to write monthly or weekly options?? Also if my 15500 start to become ATM I should adjust my position by taking a loss correct?

I\’d always prefer monthly options, Kalpesh. The point with adjusting these options is that the transaction costs shoot up driving your profitability lower.

Hello Sir,

I hope you are doing well.

You have mentioned multiple times that it is better to buy/sell monthly nifty options rather than weekly as if you are wrong you have more time to change your position.

Now, how should I go about writing nifty monthly PE option contracts 2 weeks away from expiry? Via SD calculation nifty would be 2 SD around 15550.

So I could write 15500 PE with there being 12 days away and purchase 15000 PE for reducing margin.

What exactly could I keep as a stop loss? This is what confuses me?

When should I adjust my position or when should I completely square it off for a loss?

Kalpesh, if you are writing and buying PE, then you are naturally hedging your position. There is no need to adjust. By adjusting your cost of transaction increases and therefore your profitability reduces.

sir,

can we apply bear put spread or bull call spread on the day of expiry

sir,

can we apply this bear put spread or bull call spread on the day of expiry

May not be the best time, try and see if you can do this a little earlier to expiry.

For example, I sell a 50 PE @ Rs.25 for 1 lot of 1000 shares today. Then buy one lot of it @ Rs 0.05 before export. What would be my P&L. Please explain.

You will make 25/- times the lot size.

Sir,In the graph of strategy cost vs volatility,blue line with lot of days to expiry react/varies more with increase in volatility than red line then why in here red line is written as varies more than blue line sir pls explain 🙂

Its just to illustrate how it varies wrt time 🙂

I\’m not sure if I got your question fully.

Dear Karthik,

Firstly, thank you very much for creating this wonderful platform. Appreciate all the efforts you have put in here.

I have a query regarding the option bear put spread strategy. I have been experimenting as part of learning with various strike prices and expiry date and today i.e. 13-06-2021, I tried to create a bear put spread strategy which goes like this

NIFTY 1st JUL 16300 PE – BUY

NIFTY 1st JUL 16200 PE – SELL

Surprisingly, I noticed the MAX profit is 7500 and the MAX loss is 0. (I am using Sensibull strategy builder). I am pretty sure what I am trying to comprehend here is wrong. Could you please advise what the numbers would actually look like? And will I be able to place this order? Any potential risk?

Thank you once again!

Cheers

I\’m sure there is something wrong, hard to pinpoint without really looking at premium numbers.

Thank you, Karthik.

Wish to meet you someday and thank you in person.

Hopefully. Good luck, Sanyam 🙂

Would the charts of strike selection and effect of volatility stand true for weekly expiry as well? (considering the first 3 days as 1st half and next 3 days as 2nd half)

Yes, it does. Everything kind of gets squeezed, but the approach remains the same.

Sir

Thank you for your modules. In

Any of the strategies , i.e. Bear Call or Bull Spread or etc.. one will have to hold to expiry as i have been tracking prices on Excel and notice even if the prices move by 5% the premium for the OTM and ITM calls or puts do not reflect the change as per original stratergy and one may make loss.

Mohit, why don\’t you track this on Sensibull?

Hi,

How did you get the Strike selection charts? Is it in Zerodha?

Rendered it using the software.

Sir if target is achieved can we get out or wait till expiry

Please do bear in mind the payoff is upon expiry, which means to say that the trader is expected to hold these positions till expiry?

Yes, you can get out before expiry, there is no need to wait to expiry.

Lets say I initiate any spread strategy (bull call, bull put, bear call, bear put.)

Lets say I don\’t plan to intiate till expiry.

1)

When and how exactly can I exit from these strategies?

2) What kind of stop loss can I maintain?

1) You can exit just before the expiry or hold to expiry also. Really depends on how you want to deal with it

2) Spreads usually have a defined TGT and loss levels, why not stick to that?

Hello Sir, I didnt quite understand the graphs. Lets just take an example of the 1st graph which shows P&L (target hit in 5 days in 1st half of the month)..

Should I use the graph as a ref for the upper strike only? and just subtract the spread for the lower strike? kindly clarify.

Could you share the strikes for all the 8 cases shown in the graphs for better understanding.

Not sure if I understand your query fully, but the graph is of both the option legs.

how much margin required to create nifty index bear put spread ?

I tried with margin calculated but could not get.For eg. buy nifty 11feb 15150 pe and sell nifty 11 Feb 15050

or vise versa.

pl.reply, thanks

Use this for monthly contracts and get the margins, weekly will be roughly the same.

Respected sir,

My query is about \’stratergy cost vs. Volatality\’ .Sir, why volatality matters here?

I mean if i am gonna hold it till expiry and payoffs for stratergy are depend upon \’ stratergy cost at the moment I take these two position and strikes.

Then how premium change due to volatality matters? Whatever change in premiums, i get paid off according to premium i paid/receive.

Then why change in premiums (increase in stratergy cost) matters. If i hold till expiry .🤔

Yes, if you hold to expiry, then all that matters is the intrinsic value of the option. The other things matter if you intend to actively trade.

All the strategies are clear and my doubt is when we need to select a particular strategy out of 14 strategies?

That depends on how well you understand the markets 🙂

New to zerodha. Please can you explain how to buy these strategies on zerodha. Like spreads, Iron Condors and other

Onkar, you can use basket order for trading these strategies – https://support.zerodha.com/category/trading-and-markets/kite-web-and-mobile/holdings/articles/kite-basket-orders

Hi Karthik,

While calculating delta in B&S calculator, how to input the values of \’Volatility\’, \’Interest\’ & \’Dividend\’?

Thanks in advance.

You can take the value of ViX as a proxy for volatility. Interest rate is the one prevailing in the economy. Do check this – https://zerodha.com/z-connect/queries/stock-and-fo-queries/option-greeks/how-to-use-the-option-calculator

Nifty spot 11371

11500 PE Buy @ 156 x 1 lot

11300 PE Sell @ 57 x 3 lot

profit = 15 to 215

loss = 0

Is it OK to create such spread or there is any negative in this or calculation is wrong.

There is no strategy with zero loss 🙂

Got it sir.Thank you!

Welcome!

What is the relationship between moneyness of an option and Vega?

Do check this, Roshan – https://zerodha.com/varsity/chapter/vega/

Hello Sir,

Apart from time to expiry,does moneyness of strike impact change in premium due to change is volatility?

Yup, all these factors are intertwined.

Dear Karthik,

Some strike combinations in Sensibull show -7 and -20 for Bank Nifty in this strategy.

1) What would be effect on P&L?

2) Delta Neutral is must while selecting strikes?

I\’m not sure if I get the complete reference, maybe you should check with Sensibull support for this 🙂

Today Nifty is at 10100. I expect it to fall within next 2-3 months. If I buy the NIFTY PUT of 27th Aug.2020 available @ 69 for strike Price of 8000 to hedge my Existing EQUITY Folio I may Lose Rs.69×75 = Rs.5175 if NIFTY does not fall to 8000 Level on 27th August.

I am not sure if NIFTY fall below 8000 before EXPIRY, then I shall be gainer or Loser. Can you Clarify.

Is it a correct Strategy to hedge a Bigger Portfolio of more than Rs. 10 Lakh.

Suraj Prakash Sharma

Suraj, you will have to hedge it with maybe 2-3 lots. YOu will profit if Nifty falls below 8000 on or before expiry.

Karthik Rangappa says:

May 17, 2020 at 9:35 am

1 & 2) YOu will have to let it expiry and take physical delivery, more on this here – https://support.zerodha.com/category/trading-and-markets/margin-leverage-and-product-and-order-types/articles/policy-on-physical-settlement

3) It would be 1900, this is the strike. When you write options, your profit is limited to the extent of the premium received.

Hi Karthik, first of all thank u very much for your help. In my first option trade I earned profit of 10k and it is all because of you.

I have some doubts regarding settlement (although I read the above mentioned article). is it mandatory to give/take physical delivery? Someone (a reputed CA) told that either we can settle it physically or by cash.

1) If I buy a call of Bajaj finance 2500 CE, and on expiry the price become 3000, do I have to take delivery of shares by giving total amount or can I settle it by taking the cash (3000-2500 = 500)?

2) if I sell Bajaj finance call 2500 CE and on expiry the price becomes 3000, do I have to give shares or can I just pay the money ₹500/share? if I have shares there would be no problem and those would be deducted from my account, if I don\’t have shares what should I do?

If it is mandatory to give physical delivery and I don\’t have shares can I exit the trade on expiry day by paying the high premium? On expiry day till what time we can exit the trade on premium?

3) if I buy put 1500PE, and the price becomes 1000, if it is mandatory to give delivery, can I buy the shares in cash at a price of 1000 on expiry day and give delivery or to give delivery I have to buy the shares atleast 3 days before to expiry to avoid short sell?

3) if I buy put 1500PE, and the price becomes 1000 after 2 days, if it is mandatory to give delivery and I don\’t have shares, can I buy a lot in future at a price of 1000 and on expiry settle the option contract with it or to settle option trading I have to have shares in my account?

Thanks in advance and sorry for such long questions?

Congrats on that, happy for you 🙂

1) If you let it expire, then you will have to take delivery

2) Yes, that is right. Shares would be deducted. Best is to figure if you want to enter expiry or square off before itself

3) Yes for all. If you are entering the physical delivery by expiry, you have to give or take delivery.

Hi Kartik,

I guess these strategies are very useful. But I have a doubt that the premiums keeps on changing so how will be the loss be limited. Once we take a position with particular strikes and premium, feed it in excel. But then obviously the premium keeps changing so the loss also varies and not fixed. So I wanted to know if these strategies work with varing premium. Is there a percentage of loss and profit?

Thank you.

Thats right, once you initiate the position, your P&L is with respect to the change in premium. This works just like how buying a stock works.

Hi Karthik,

Bajaj finance spot price is ₹2086. I want to buy it @₹1900, so I sell it\’s 1900PE @ premium of ₹70,

A) the price doesn\’t drop below ₹2000, so the premium that I got would be my profit.

B) the price drops to 1900

1) my mood changes and I don\’t want to take delivery, on expiry do I need to squared off it or let it be settled automatically? Or there are extra charges for automatic settlement?

2) I want to take delivery,

how can I get delivery in zerodha, do I just need to put the required money in zerodha account or do I have to call zerodha? Zerodha team is not reachable now a days as they don\’t pick up the phone even after waiting on call for hours, so what should I do and at what time should I inform zerodha? When should all the required money be put in zerodha account, on the expiry date or before that?

3) In this case the net cost would be ₹1830, right? So I would be benefited by ₹70.

There would be no loss till price drops below ₹1830.

For buying a stock this strategy seems to be wonderful, yes if price drops drastically (for eg. to ₹1500 or 1000) it would be problematic, but it may also happen if a person buy stock in spot @₹1900.

OR are there other hidden risks of this strategy? Seeking your valuable guidance.

Thanks in advance

1 & 2) YOu will have to let it expiry and take physical delivery, more on this here – https://support.zerodha.com/category/trading-and-markets/margin-leverage-and-product-and-order-types/articles/policy-on-physical-settlement

3) It would be 1900, this is the strike. When you write options, your profit is limited to the extent of the premium received.

One more thing…you mentioned that the near and far month contracts are not shown because they are illiquid right? But then how can traders trade them if they don\’t show up at all? I mean how do they determine the liquidity…?

Like the chicken and egg situation, in markets liquidity chases liquidity 🙂

Thank you Karthik.

And I suppose my max loss in the above scenario would be:

Max loss = ((Put strike – Fut sell price) – (premium received from shorting PUT))

Right?

Hmm, perhaps. It is always a good idea to put these numbers on excel and see how the parameters work up. In that way, you are absolutely sure about it.

Hi Karthik,

Hope you are doing well. Need your help to understand this better:

1. The option contracts for certain companies are restricted to current month only…i.e. we can\’t see their near and far month contracts..e.g. we can see option chain of May series of YesBank on NSE website but the June or July series are not listed. Why is it so?

2. Supposing, I am short YesBank May 30 PE. And I also \’shorted\’ a YesBank May Future at \’25\’. Let\’s say YesBank spot closes at 20 on expiry. So my put is deep ITM and I am in loss premium wise but my future would be in the plus. Since this is a compulsory physical delivery equity…could you tell me exactly what would happen at expiry?

Thanks.

~ Abudhar al Hassan.

1) This is because they are illiquid

2) Short Pur results in buy stock obligation and short futures result in deliver stock obligation, hence they both net off nets off

Sir, suppose I initiate a Bear Put spread today with

BUY 19000PE

SELL 18000PE

there will be a net debit, then a margin block

And then some margin benefit transferred back to my trading account.

Now suppose market moves down and both the options become ITM.

So,

Buy position will be making good profit

Sell position will be making loss

But in major cases, I think (profit in buy position>loss in sell position)

So, at the end of the day, will the broker be asking for more margins?

Another question,

If I buy the PE option first and then sell the PE option, will I be required to first provide full margin or could the trade be executed at even the (margin required-margin benefit) amount?????

Being a student, I am asking you these questions.

Sameer, there will be a slight increase in the margin as the volatility increases, but I suspect it won\’t be much. If Vol increase, so will the SPAN margin requirements.

Hi Karthik,

Nifty is trading at 9154. If I aaply this strategy and buy 1 at the money put ( 91000 PE) @ premium for ₹380 and sell 1 out of the money put 8500 PE @ premium for ₹181, maximum loss would be 380-181=199 = 199*75= 14925, is it correct in any case or the loss may go beyond it?

What would happen if I don\’t hold the contract till expiry and trade only at premium, in that case also would the maximum loss be ₹14925 or would it be increased?

Also instead of applying this strategy wouldn\’t it be better to buy a deep out of the money put 8000PE @ ₹96 premium as here the maximum loss would be ₹7200 (96*75).

Thanks in advance.

1) Yes, both the profit and loss are capped

2) You can trade the premium, but P&L will be very different

3) That would be a directional call. Depends on your conviction.

Hi karthik,

I am still not clear about why to employ this strategy (or similar strategies).. in the NIFTY example explained in the chapter.. in case I am moderately bearish on the market than rather than employing this strategy why shouldn\’t i buy naked 7400PE with premium of 73, that ways my max loss will be Rs. 73 instead of Rs. 92 and the profit potential will also be unlimited.

With this, you are capping your downside also. For example, naked PE would cost you 73, but you can reduce that to 53 (just saying) by employing this strategy.

Thanks for the prompt reply Karthik. However, when you check the market depth of the option, kite is still showing the closing price as 6.9. Its the YesBank 30 May PE.

Secondly, shouldn\’t the closing price get updated on the same day itself? If it gets closed at a price not liked by a trader he or she could place an AMO to exit the same day itself right?

Mkt depth will always show the LTP. The team is aware of this, on the list of things to do.

Hi Karthik,

How are you? Hope you & your family are safe and the lockdown isn\’t bothering you much 😊.

I had a question related to a put option. The LTP and Closing price of a put option was at 6.9 yesterday…this is a May expiry put option hence there wasn\’t much movement in the premium. The premium was still at 6.9 even post market session yesterday as per Kite. However, in the morning well before 9 am, i.e. the pre market session, I saw that the premium had jumped to 8.35. How is this possible when the markets are not even open? It is my understanding that even AMO orders are executed at pre market session only and not before that…am I right? Then how come the premium jumped up during off hours?

Thanks & Regards,

~ Abudhar al Hassan.

All good, hope the same with you as well 🙂

I guess the close price was 8.5, which gets updated on Kite the next day.

Karthik, I didn’t know that its different. Thank a lot 🙂

Appreciate your help 🙂

Happy trading 🙂

Karthik, thanks for your reply but my question was different.

As per the payoff chart it shows details about 1 lot only. Can you please suggest how to calculate the payoff chart for 2 lots. i.e Long (1 lot) and Short (2 lots)

OR

Long (1 lot) and Short (3 lots)

Saurabh, a bear put spread has to be executed in a 1:1 manner only, any other ratio becomes a ratio spread.

Hi Karthik,

I am new to the option trading so it would be really helpful if you can guide me here. As per your above example we are going Long for 1 lot of 7600 PE and Short for 1 lot of 7400 PE but how can I use the payoff excel sheet to calculate the data for Long 1 lot of 7600 PE and Short 2 or 3 lots of 7400 PE. Do I need to multiply the \”Credit for short put\” * number of lots for short put? e.g. 73*2= 146 for 2 lot short and 73*3= 219 for 3 lot short.

Sorry, if my question seems illogical 😐

Saurabh, I\’m not sure if I get your query fully. Anyway, if you examine the excel, the payoff is actually a combined payoff of both the legs. However, the excel also has individual leg payoff.

Hi Kartik,

while applying option strategies on market wrt expiry dates will you refer to the above mentioned graphs EVERTIME to select the stike prices or will you do you it without refering the graphs jus by calculating the P&L at that moment

I\’ve developed a sense of which strikes to opt for, so I stick to them if at all I\’m taking a trade. Btw, it is usually in and around ATM.

Thank you karthik for the quick response.

I cannot come out of these positions as there are no buyers and sellers for these options. I have learnt the lesson the hard way. An obligation for long 840 PE means I got the right to sell the Mindtree stock at 840. The lot is 800. So, around 800 stocks of mindstock would be sold. A short position would open in my account. correct?. Then, What happens to 750 Short Put?. Since it expires at 0, and i sold these at 8.9/-, I would get 8.9*800 credited into my account, right?.

750 PE would be worthless. Yes, you would get to retain the entire premium. Hence, please check the liquidity of the option before entering position.

Hi Karthik,

Thank you so much for the courses.

I sold Mindtree 750 PE at 8.9/-. I bought Mindtree 840 PE at 79.85/-. The options would expire on 26th March. I am not being able to close out the positions because of illiquidity. I dont need to take any physical settlement, right?. Does it depend on the price at expiry?. If yes, please explain how it pans out considering different expiry prices. The current price is 792. What happens if the expiry price is i)720, ii)800, iii)900

Please advise at the earliest

Yes, it depends on the price at expiry. The physical delivery is net off only if both positions are ITM. In this case, as of today, 840PE is ITM and 750PE is OTM. So you will have a physical delivery obligation for 840PE

1) 720, both positions are ITM, hence net off

2) 800, 840 is ITM, 750 OTM. An obligation for long 840 PE

3) 900, same as 2.

Best is to get rid of the position before expiry.

suppose i am a buying a put with a delta of -0.5 and selling put with a delta of -0.35.

now my position delta is -0.15

wouldn\’t it be the same as buying a put with -0.15 delta

what advantage does a bear put spread give me over buying this naked put ??

Hmm, a delta neutral hedge is supposed to equate your delta to 0. This way you have protected your position both ways.

yes, but in example given there underlying used was same (nifty 50). I mean if we have 2 options on different underlying can we add up their deltas to get the portfolio delta?

You cannot add the deltas of two different underlying. You can for the same underlying, different strikes.

Hi Sir,

Can we add delta of options on different underlying?

As in? We have that covered in delta chapter right?

There could be reason that i might not have selected right strikes like in the above article you mentioned that when in second half of the series and 4-5 days to expiry left,select OTM strikes?

Yes, that is possible too Vidit.

Hello Abid,

Thanks for responding to all my queries.

1) I usually trade intraday Bank nifty,1% move either side is now a days normal in it. So if i trade direction,and i buy a call but some how market rotates back,i will suffer a loss in it if i trade futures.

So to reduce loss, what i am doing is trading spreads on intraday on directional basis and when buy signal come on higher time frame say on 30min and after adding some filter (higher high or lower low) to be sure that it will move up or down,i remove one leg of spread and then trade on naked leg of option.

Is this kind of approach is correct as i do not want to lose much?

Yeah, you can have a hedged position while waiting for the directional cue, you can remove the hedge when the direction is established and the underlying starts to move.

I traded TATA Motors in morning today,i made put spread but it worked other way around,it started making loss even TATA Motors was falling,and similarly i made put spread in IBULHSGFIN and it started making profit even the prices were rising,but it should be in loss as prices were rising.

I selected ITM AND ATM as strikes. Difference in option premium of both strikes in case of Tata motors was Rs 2/- and in case of IBULHSGFIN was 8/-

What could be the reasons that put spread was working other way around?

Vidit, did you check the volatility for these options? If the volatility was high at the time you wrote the option, then it is possible that the premiums did not react the way you expected it too, despite a favourable movement in the underlying.

Hi Karthik,

I have a query regarding delivery in spread strategy, since now all stock options are physically settled.

I sold Wipro 240 CE @7.4 and bought 250 CE @3.8. My max loss is 20480 (without other costs)

Assuming i don\’t square off and assuming Wipro\’s price on expiry date is 255, Will the physical settlement on two legs net off or not?

Thanks

Ratan

Since the expiry is 255, both the legs are ITM, hence it will get net off and no physical delivery settlement required.

Thank you so much for the response.

Also wanted to know, if we can use the stock in our acc as the margin for option writing?

Yes, Ajay. You can. Remember, 50% of the margin has to come from cash. More on that here – https://zerodha.com/z-connect/tradezerodha/margin-requirements/online-pledging-of-stocks-for-trading-fo

Hi Karthik,

Is the margin required for a put spread is same as selling a naked put.

For ex: To sell a naked put, i need X rs as margin.

For a put spread(Sell a put, and buy a lower strike put), Do i need the same amount of margin?

Thanks

Ajay NM

Yeah, it is roughly the same. You can use this to check the actual margin required – https://zerodha.com/margin-calculator/SPAN/

Hi Kartik,

Sorry for the trouble..I found my mistake..

the trade will have losses (potentially unlimited) once nifty goes below.. 10800 – spread = 10700

cheers

Om

Yup, I\’m not surprised 🙂 There are no guarantee profits in the markets 🙂

Hi Kartik,

I was playing around with the payoff excel sheet. I might be horribly wrong here, please correct me if i am wrong.

Can we make this a credit spread instead of debit by short 2 lots OTM PE and buying 1 lot ITM PE

I agree this may not convert into a credit spread all the time.. but eh current 5-Sep-2019 option chain show that.

10900 PE long at -145

10800 PE Short 2 lots +202

If we hold this till expiry, will i make either 57 points or 157 and never make losses..? that does not sound correct there cannot be a trade that wins or wins lees.. so i must be wrong but I am not able to see where.. If you can find time.. to reply to this plz..

cheers

Om

Something does not seem to add up here. Have you put up the numbers on excel to figure this out?

Hi Kartik.. I am bearish on Ashok Leyland.. Right now it is trading at Rs.90 and I think by the time of expiry it will be around Rs.80. Since Expiry is reasonably far.. So, as per bear put spread, I purchased one lot ATM option @ 87.5pe and sold one lot deep OTM option @ 80pe.. As per sensibull, it is showing maximum loss of Rs.6200 if it goes against my strategy and I hold it expiry and maximum profit of Rs.23,363..

I have 2 doubts..

1- Is there any possibility that my maximum loss can be more than Rs.6200 if position goes against me?

2- What do you think would be better alternative than this strategy?

1) No, since this is a spread, the loss is restricted to 6200 (provided the math you\’ve done is correct)

2) RRR is good so worth the bet. But if you are sure about the outcome, why not buy a slightly OTM PE?

Karthik,

Would appreciate your opinion on the following:

Let\’s suppose Nifty spot is @ 11000. I am \’moderately bearish\’ and feel that Nifty would touch 10800 within a week. At the same time, I am sure it would stay above 10500 for let\’s say at least the whole of next month. Now my intention is to profit purely from the premium rise so I go ahead and buy the current month\’s weekly PUT option i.e. NIFTY 21st FEB 11000 PE for Rs. 100/-. Clearly, I would be risking 100X75 = Rs. 7500/-, which would be my max. loss. I intend to sell the PE 11000 if the spot goes below 11000 and touches 10900 or 10800.

However, 7500/- is beyond my risk limit and I don\’t want to put up a stop loss fearing the volatility we see in weekly options before expiry. So…

1) What if I short NIFTY 28th MARCH 10500 PE @ Rs. 90/- and collect a premium of 90X75=6750/- so as to partially finance the FEB weekly PE that I bought above and thereby bring my risk down to 7500-6750 = 750/- ?

2) Assuming the trade goes my way and the spot touches 10800 in FEB, will the premium of the 10500 PE of MARCH be affected hugely?

In other words, I am basically asking whether we can buy an ITM option of current month and sell a deep OTM option of a far month and benefit from the premium rise? (I do not intend to hold any of the options till expiry)

Thanks,

~Abudhar al Hassan.

This is perfectly valid, Abhudhar as this is a spread and should protect your downside (as well as the upside). The tricky bit is with the expires. Why don\’t you do both these on monthly expiry?

Karthik,

If I go for same month expiry options…and the price goes down as I expect it to…then the premium for both the bought and sold options would increase at similar pace…so the gains from the bought option would be offset by the losses of the shorted option.

If I buy a very near weekly expiry ATM option and short a deep OTM FAR MONTH option, and if the price moves down as I expect it to, then the premium of the near weekly option would rise at a far more rapid pace than that of the shorted far month OTM option..right? And thus make some profit from the premium differences. Remember I mentioned I dont intend to hold the options till expiry..want to play with the premiums only.

Do you think this makes sense? Or am I overlooking something here? Please advice.

P.S.: Not a big deal but my name is spelled \’Abudhar\’ and not \’Abhudhar\’ 😀 🙂

Thanks.

~ Abudhar al Hassan.

the premium for both the bought and sold options would increase at similar pace —-> this is not true. The pace at which the premium would increase depends upon the moneyness and expiry of the option.

Apologies for misspelling your name, I\’ll remember it for the next time 🙂

Another reason to short FAR month OTM option is that they would be relatively priced higher. So shorting and collecting their premiums would bring down the cost of the weekly option that I would buy by a great deal.

Again I could be wrong and I an pretty sure I am missing something here…

~ Abudhar al Hassan.

Like I said, the movement in the far month OTM will be far lesser, so you may not really get the desired outcome.

Dear Sir,

I bought a 10900PE Buy for Premium 170 and 10700PE Sell for Premium 105, while nifty was at 10880 on 31st Dec for the Jan options.

Hope this qualifies a Bear Put Spread with following characteristics:

Spread=200; Net Debit=65; Breakeven=10900-65=10835; Max Loss=65 @ 10900 and above; Max Profit=200-65=135@10700 and below.

However, the change in premium values are never confirming this (@ Nifty 10715, premium values are 252 & 160 respectively).

Also, should I hold this position till the expiry (31Jan) in order to square off and realize the profit/loss?

Please revert.

Best Regards,

Hari Narayanan

Hari, yes, this is a bear put spread. You can square off the position anytime you wish. There is no need to hold till expiry. The bear put spread pay off will play out only upon expiry, however, there is no need to stick till expiry.

Thanks for the clarification.

Good luck, Hari.

Hi,

Today OCT17 Bnifty 25200PE closed at Rs 3 even though the spot was 25188.60. Ideally it should be around 11.40/-

Can you please explain why this difference?

Kindly note, for exercise the in money options stt will be 0.125% because of its trading in discounted price.

Can you please check the close price again? Thanks.

Yes. I do not have the option to post the picture here. But I checked one more time in historical prices. The price was Rs 3/-

The option is pricing in the STT, Ashwin, which is 0.125%.

Hey Karthik

There is a trade in Adanipower 15 CE- 4.1 and 17.5 CE- 1.45.

credit received is more than difference in strike prices. NO risk trade.

what can go wrong? liquidity?

Sorry should be in bear call spread.

Well, the only risk is the execution risk then 🙂

Hi Karthik,

Assume my view is bearish.

If we trade on \”Bear put spread\” strategy and market goes against our view, Can we enter into \”Bull call Spread\” to cover the losses?

The idea is only to cover the losses not to make any profit when market goes against our view? Is it possible to come out with out losses?

Please confirm.

Thanks

Satya

Satya, deploying a bull call spread, just to hedge a position can be a costly affair. Instead of this, you can add one more lot to the bullish position and ride on the wave.

Hi,

Can you please explain which option to add one more lot of ? What would be the bullish position in this spread ?

Thanks..

Ravi, sorry, didn\’t quite get that query. Can you please elaborate?

Hi,

Thanks for your quick reply, sorry for not being clear in earlier query.

In the above reply you had said

\”Instead of this, you can add one more lot to the bullish position and ride on the wave.\”

I wanted to ask which is bullish position referred to here..

Thanks…

To sell OTM Put position.

Hi karthik,

what is meant by strategy cost?

Here is a strategy: Buy Nifty ATM call at 102 and buy Nifty ATM Put at 90. The cost of executing this strategy is 102 + 90 = 192, which is nothing but the strategy cost.

How to calculate time to target objectively?

You could give Support and Resistance a try – https://zerodha.com/varsity/chapter/support-resistance/

Hi:

Since last two month, I am watching Nifty call and put option. I did trading on Nifty PE and CE and got the experience by Zerodha trading account.

I have one doubt about Put(PE) Sell. Please see the following example and try to give my answer.

Ex. Second week of month NIFTY JUN 9500 PE premium is around 40. If I buy this NIFTY JUN 9500 PE have to pay 75*40= 3000 Rs premium. Which will be day by day reduce or Zero on expiry.( If it increase price I can book the profit.)

Now my question is here , If I sell this NIFTY JUN 9500 PE (40) have to pay 46000 premium, which include span + exposure margin + option premium. Now, I want to buy this PE just one week ahead of the expiry and price of this 9500 PE is around 15.

1) Let me know can I buy this put that time and book the profit ?

2). If Yes then how much I can earned profit ?

3). Is there any affect on SPan and exposure margin ?

4). How much safe this option ?

Hope you will clarify.

Regards,

HARESH

Hi Karthik,

While trading stock option where to check the volatility of stock and how to decide if its low or high? based or that we can decide where to buy or sell option.

Is it the case that for stock also we need to check the INDIA VIX ?

http://www.moneycontrol.com/indian-indices/india-vix-36.html

Thanks,

You can compare its current volatility with its historical vol to estimate if its high or low. Yes, India Vix helps while trading Nifty.

Can you please let me know where to check stock option current and historical volatility ?

For current implied volatility, check on the option chain on NSE website or you can even use an option B&S calculator. Historical vol has to be calculated.

Sorry to bother you again, Just little confuse here.

I checked your option module and you explain the method to calculating daily and historical volatility. but i could not find the calculation for historical Implied Volatility and that is what deciding factor for shorting or buying the option right ?

and the greek calculater shows VEGA and on NSE daily implied Volatility are same? means VEGA Is the Implied Volatility ?Hope you get my confusion related with the volatility 🙂

Thanks,

I\’m not too sure about the techniques of calculating historical IVs. Hence I decided to keep away from it. However, for all practical reasons, I think its good enough if you compare today\’s IV versus historical volatility. B&S calculator is also used to calculate the IV of the option. You enter the price and get the IV. Check this post – http://zerodha.com/z-connect/queries/stock-and-fo-queries/option-greeks/how-to-use-the-option-calculator

Hi Karthik,

I have a problem in understanding the volatility curve graph.

It says that in each scenario the Strategy Cost increases with an increase in Volatility.

So this is a Bear Put Spread happening on a net debit in this case -92.

So what is basically increasing with the increase in Volatility.??

And if it is the net debit we are talking about here, then the Y axis should be represented by negative value…

And how can the net debit increasing be beneficial for the spread.

Facing the same problem with all the Volatility graphs in this module.

Kindly explain. Think I am missing some thing crucial here..

With increase in volatility, option premiums increase….and with the increase in premiums, the cost of writing options also increases. So if your strategy involves a net debit, then with the increased premium, the debit will be higher. In other words the cost of strategy is higher.

So when you traverse right side on on the y-axis, the cost increases and likewise on the left side it reduces.

Thank you

Welcome!

Hi Karthik,

Thanks for your Option Strategies. Can you please add +50 to the Nifty strikes in the excel and update in the modules.

I think will get more clearer RRR in 50\’s rather difference of 100 in strikes.

100 intervals have better liquidity compares to strikes with 50 difference.

Hello Sir,

1. If I intend to trade options before expiry I need to consider all the geeks

2. If I intend wait till expiry I need not consider other geeks only choosing the right strike is important

Am I right?

In all probable situations considering Greeks will be helpful!

Could you tell me sir how greeks can be useful in case I wait till expiry, I had thought only a right strike has to be considered.

In multiple ways – all of which has been explained in great detail in the previous module. Hope you\’e read that!

I am really sorry, I mixed up the jargons, from 2nd case I meant exercising the option. I got it now 🙂 Thanks !

Welcome!

I was today trying to place the below order, for 20 lots

long 7800 Nifty Jun PE

short 7900 Nifty Jun PE

In above the maximum theoretical loss can\’t exceed 1.5L, but when I try to place the order from kite my sell order gets rejected with message that margin required is 7.5L+, why this is so?

That\’s because margins are blocked when you sell options, the margins are similar to futures margin.

Then how do I execute the various strategies you are teaching. And one thing I didn\’t get if I only have a sell order then margin should be blocked but for this order my loss can\’t exceed 1.5L then why so heavy margins? How can I bring them down.

When you sell, your risk is unlimited, hence the margins are blocked. As long as you have sufficient margins, you can execute any of the strategies, if need be.

but I also have a long order along with that? Shouldn\’t that bring down the margins. If I want to square than both or none legs should be squared.

If the position is hedged then you will get a margin benefit. Check this – https://zerodha.com/margin-calculator/SPAN/

Is there a plan to incorporate buy/sell of option strategies from Zerodha platform (Pi/Kite)? Something similar to thinkorswim where the strategies can be executed in a single go.

It is certainly in the list of things to do, cant commit on timeline 🙂

Good to know we are gonna get this in future. Thanks 🙂

Hopefully sooner than I can imagine 🙂

I am little confuse that when to form option strategies specially when starting of the month. and also guide we don\’t have to form strategies in 3rd or 4th week of the month.

The theta graphs should help you with this. If you have any specific doubt, I can try to answer it for you.

Hi Karthik,

Good to know that my understanding of relative DELTA value was right and you were kind enough to accept it and make the correction in the tutorial.

All this knowledge and understanding of options I have gained only from YOU , but still I am not able to garner the courage to trade options/spreads , maybe fear of losing money as in the past when I had no understanding of options and lost money trading them.

Avinash – all it takes is a little bit of confidence about what you know. You clearly seem to have the flair to grasp things, I\’m sure you will be successful if you take the plunge!

Thank You, Karthik

Welcome.

Sir, u r not yet discussed about putcall ratio..

Eventually sir, request you to kindly wait.

Hi,

How many days will take to complete this Option Strategy Module?

Really you are doing very great job, we are very great full to you for giving such a precious information.

we got a lot of knowledge from this Modules, now we are getting confident in Trading and Investing in Stock market

Thank you so much

Suresh, there are at least another 7 – 8 chapters in this module. Will try my best to wind up as soon as possible.

Good luck to you, stay profitable.

Hi Karthik,

Good to read about the Bear Put spread.

Sub: Your example of adding up Deltas in the Bear Put Spread ie Delta of 7600PE (-0.618) + (-o.342) = (-0.92).

I feel we should add Deltas when we are long both the put strikes because when market moves down, our change in position will be in sync with the total DELTA value ie(-0.92)

But when we are setting up a spread we are actually long 7600PE(-0.618) Delta and short 7400PE(-0.342) Delta. So strictly with reference to DELTA, Our total change in position will be the difference of the two DELTAS ie (-0.276), because one position gains and the other one loses.

Our profit/change in premium with reference to DELTA will actually be ,Change in premium= ( points change in underlying x DELTA -0.276).

Your clarification will be very helpful.

Hey, I think I\’ve made silly mistake. You could be right…let me recheck and updates the content. Thanks for pointing this.

sir i have one doubt is there any possible to go short sell in both call side and put side ,for example 27600 (ce) option sell side and 27700 (pe)option sell side i want to go sell side at a same time , if the market is in the 27650 range, if possible what is amount required for this purpose, pls tell me the detials pls ,sir reply this one pls.

Yes, this is called a short straddle. You will have to park margins on both the contracts. Check this – https://zerodha.com/varsity/chapter/the-short-straddle/