3.1 – Brexit, the event extraordinaire!

I originally planned to dedicate this entire chapter to the USD INR pair, which as you may know is the largest traded currency contract in India. But then, the BREXIT issue happened today, and I can’t help writing about it as it has huge relevance to what we just discussed in the previous chapter – events and their impact on currency pairs.

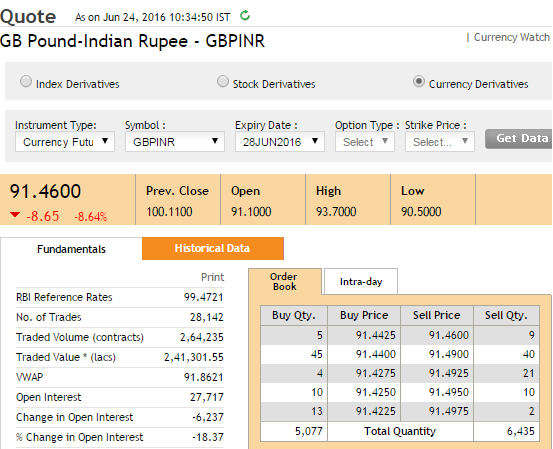

To give you a sense of what happened, have a look at how the Great Britain Pound (GBP) reacted to the event. It was down a massive 8.64%, which you will eventually realize is a big deal in currencies.

The Guardian UK had this to say about the event –

Here is the article.

My objective here is to simplify Brexit to the best of my knowledge and help you understand why the pound reacted the way it did. Obviously, the bigger agenda here is to help you understand the potential impact of such events on currencies. By doing so, you’ll get a grip on how to summarize global events such as Brexit and understand what kind of impact they could have on currencies.

For the sake of simplicity and brevity, let me bullet point Brexit for you. We start with a bit of history –

- After World War 2, Germany and France debated the idea of forming a union of sorts. The thought process was that if countries traded and did business together, then they are less likely to wage war against each other.

- This laid the foundation for forming a bigger union called the ‘European Union’ (EU) with more European countries agreeing to join the EU.

- The EU formed a single market of sorts where goods, service, and people moved easily across countries. So much so that the EU decided to have its own currency called the ‘Euro’.

- The UK, although was a part of the EU, never accepted the Euro as their currency. Note there are many other countries in the EU which still have their own currency, example – Switzerland, Chez Republic, Denmark etc…

- There was a growing debate in the UK in recent times on whether the UK should remain in the EU. Many of UK’s citizens believed that the UK was better off outside the union as the rules laid out by the EU commission was more taxing on the UK’s citizen than actually benefiting them. In simpler words – they believe they would progress faster and better economically and as a society being outside the EU.

- Britain option to exit from the EU was called ‘Brexit’.

- The UK decided to formally seek its citizens’ vote on 23rd June 2016, wherein the citizen would vote for being in or leaving the EU. This is called a ‘referendum.’

- The outcome of the referendum was a bit of shocker with the UK actually deciding to opt-out of the EU. In fact, many in the UK and the world believed that the UK would vote to stay in the EU.

The referendum’s outcome sent a shiver down the spine for traders and investors around the globe. The GBP crashed to a 31 year low, the major European indices dove close to 8-10%.

Now, why did this happen? Why did the markets fall? What is the connection between the Brexit and the currency markets and the work markets?

Now here is where I’m hoping the previous chapter comes to help us J

Recall in the previous chapter; we discussed how a strong economy (defied by inflation, interest rates, trade deficit etc.) leads to a strong currency.

Given this, think about the UK – clearly, the UK is one of the strongest economies in the world and contributes significantly to the EU. Now with UK opting out of the EU, things are set to change both economically and politically.

While the UK has a trade deficit with the rest of the world, it maintains a trade surplus with the EU. This should give you a sense of how strongly the UK’s economy is coupled with the EU. With UK opting out of the EU, its finances are certainly going to take a hit.

Further, the problem is with clarity. Everyone knows that the economic situation is bound to change, but to what extent is something no one really knows. How will the Bank of England react? Will, they cut the rates near zero?

Uncertainty is one thing that the market despises, and given its nature, Brexit has many. Therefore, as a result, the markets cracked.

You, as a currency trader, should be in a position to study the event and understand some basics. From my experience, sometimes the best trades are set up backed by simple common sense and basic knowledge.

Remember if you had studied the event and arrived at a conclusion not to take on a trade, then that in itself would have been a good trade, as the rule of thumb says “when in confusion, do nothing”.

The point is – when you have events of this magnitude around the corner, it is mandatory for you to know what is happening. Taking on a trade without the prerequisite knowledge is equivalent to a blind speculative bet!

So, that’s about Brexit and how events like this can impact the currencies.

Let us move ahead to figure out a few other currency concepts.

3.2 – Fairy Trade

Imagine a perfect world, wherein you can borrow money at a certain interest rate, invest the borrowed money at a higher rate, and earn the differential in the rates. Confusing? Let me give you an example to simplify this.

The interest rate in the United States is about 0.5%, arguably one of the lowest in the world. Assume you borrow $10,000 from a bank in the United States at 0.5%; invest this borrowed money in a country like India where the interest rate is about 6-7%.

To do this, you will have to convert the borrowed money (which is in USD), to INR. At today’s conversion rate, a US dollar gets you 67 INR. Therefore $10,000 fetches Rs.670,000/-. We invest the converted money in India at say 7%.

At the end of the invested year, we get back 7% interest plus the initial capital. This would be –

670000 + 670000*(7%)

= 670000 + 46900

= Rs.716,900/-

We convert this money to USD, assume the conversion rate is 67; we get back $10,700. We now have to repay the principal amount plus 0.5% in interest. This would be $10000 plus $50.

So after repaying $10,050, we get to retain $650, which if you realize is a risk-free gain!

If you realize, $650 is the interest rate differential times the borrowed money –

10000*(7%-0.5%)

10000*(6.5%)

650

This is a simple case of arbitrage, quite easy to implement, don’t you think so?

Given this, imagine a situation where you could borrow large amounts of money from the US and invest this large amount in India and make pot loads of money year on year, right?

Well, sorry to burst the bubble, such trades happen only in fairy tales J. In the world we live in, such easy risk-free profits does not exist. Even if it did, it would vanish before even you realize.

However, the bigger question we need to answer is – why is this ‘fair trade’ not possible?

3.3 – Forward Premia & Interest Rate parity

The problem with the above trade is that there are one too many assumptions, we assumed–

- We could borrow unlimited amounts of money in the US

- We could deposit unlimited amounts of money in India

- There is no cost of the transaction, no taxes

- Easy movement of currency between countries

- Most importantly we assumed the conversion rate stayed flat at 67 after 1 year

Given that such arbitrage cannot exist for long, the currency rate a year later should be such that it would prohibit the arbitrage from existing. In other words,

The money we receive from India a year later = Money we repay to banks in the US a year later

From the example we discussed above, we borrowed $10,000 from the US, invested the same in India and a year later we received Rs.716,900/-.

For the arbitrage to NOT exist, at the end of 1 year, Rs.716,900/- should be equal to $10,050.

This means the conversion rate should be –

716900/10050

= 71.33

This is called the ‘Forward Premia’ in the currency world. The approximate formula to calculate the Forward Premia is –

F = S * ( 1+ Roc * N) / (1 + Rbc * N)

Where,

F = Future Rate

S = Today’s spot rate

N = Period in years

Roc = Interest rate in quotation currency

Rbc = Interest rate in base currency

Let’s apply this formula to check if we get the forward rate right for the above situation. Remember the spot rate is 67,

F = 67*(1+7%*1) / (1+0.5%*1)

= 71.33

Further, note that the forward premia rate is approximately equal to the spot rate plus spot times the difference in interest rate i.e. –

F = S*(1+difference in interest rates)

= 67*(1+ 7% – 0.5%)

= 67*(1+6.5%)

= 71.35

This is called the ‘Interest rate parity’.

Think about this – Indian Rupees is trading at 67 today compared to 71.35 in the future. Therefore the Rupee is considered to be at a discount now. Generally speaking, the future value of any currency which has a higher interest rate is at a discount to a currency which has a lower interest rate.

So why are we discussing all this and what is the relevance to currency trading? Well, the forward premia play an important role in determining the futures price!

We will discuss more on this going forward.

Key takeaways from this chapter

- Events like Brexit tend to have an extraordinary influence on currencies.

- A country whose economy is expected to suffer tends to have a weaker currency.

- Forward premia are the expected spot rate over a given period.

- Forward premia = S * ( 1+ Roc * N) / (1 + Rbc * N)

- Interest Rate parity indicated that the forward premia are approximately equal to the spot rate plus spot times the difference in interest rate.

- Future value of any currency which has a higher interest rate is at a discount to a currency which has a lower interest rate

Really a eye opener for a beginner like me,

Simplified explanation with relevant examples..

A big thank you karthick

I\’m glad you liked the content, happy learning Shrikanth!

Im confused with one point here…If i borrow money from US for Investing to get indian interest where would i actually invest that money??? Obviously i have to invest in Bonds Right??? if so where did USD/INR trade comes into picture???

You borrow funds in US, that means you get Dollars right? Now that has to be exhcnaged to INR to invest in India. And when you sell your assets in India, you again have to exchange INR to USD.

Why are there no option contracts for GBP/INR EUR/INR and JPY/INR?

You will have to check with the exchanges on this 🙂

Well I can answer your 2nd question. Firstly most people will never be able to take part in the arbitrage trading opportunities as they are quickly figured out by extremely fast bots and filled instantly and even if you found it it\’s not worth it for most people as considering the charges and all the returns aren\’t really that great at all.

Hi Sir,

You have mentioned that \” Given that such arbitrage cannot exist for long, the currency rate a year later should be such that it would prohibit the arbitrage from existing. \”

Questions:

1. why cant the arbitrage cannot exist for long and currency has to catch up to forward premia !how the arbitrage will vanish ?

2.Even if this arbitrage can exist for a short time (not for a long time ) still then the person whom so ever find it first , can make a killing out of it ?

3. why is it necessary for the currency of higher interest rate to depreciate and move to the forward premia level so that for arbitrage to not exist? what will happen if such arbitrage exist! will it affect the quoted or base currencies countries in any way ?

4. so if always the interest rate parity exist then how the carry trades are done now or is carry trade really not possible now a days ? if not possible how the interest rate can affect the currency as mentioned by you in previous chapter (you mentioned that people generally do carry trades right)

1) Any sort of arbitrage opportunity means lower risk and no risk. That means such opportunities will attract more people to act upon, and when such a thing happens, the opportunity ceases to exist. Assume, you are the only Onion seller in the market, since you its just you, you can demand whatever price. Given your pricing power, someone else starts selling onions, now there is competition and you can no longer command a premium. Now imagine a 100 people selling onions?

2) Yes, this is always the case with any sort of arbitrage

3) Certainly, both currencies will get impacted. Also there are economic aspects here which you need to consider. Most importantly, inflation, check this – https://www.youtube.com/watch?v=Qx3YMdcLTZo&list=PLX2SHiKfualEyD05J9JsklEq1JFGbG6qJ&index=2

4) This is also an arbitrage opportunity (carry trade), and as more people flock to it, the opportunity no longer exists.

Hi Sir,

you have mentioned \”While the UK has a trade deficit with the rest of the world, it maintains a trade surplus with the EU. This should give you a sense of how strongly the UK’s economy is coupled with the EU. With UK opting out of the EU, its finances are certainly going to take a hit.\”

Question : If UK is having a trade surplus with EU and deficit with rest of world and when it opt out of EU, wont this cause the supply cut to EU countries more than affecting UK finances ! as UK can export those cut down goods to some other no EU country and manage their finances and so that would certainly better the UK trade deficit numbers with rest of country right and so GBP should have appreciated for brexit than nosediving. why it didn\’t happen !! where my thoughts are wrong. please teach me 🙂

Well, there are far more important factors like \”Politics\”, that play a role in such outcomes than actual economics 🙂

So whats good and what makes economic sense does not play a primary role in geo-political situations.

Thank you for the article

\”Think about this – Indian Rupees is trading at 67 today compared to 71.35 in the future. Therefore the Rupee is considered to be at a discount now.\” My doubt is – is it not the other way around? A Dollar is 67 Rupees today and will become 71 in the future. So the dollar is at discount?

The dollar is said to have strengthened no?

In history usdinr crash happened?

What is the highest % move in a day usdinr?

Is it safe to (nse usdinr options)short naked position in overnight?

Ah, I\’v not really kept track on this. But should be fairly easy to figure by looking at a long-term chart of USDINR.

Can anyone please simplify this statement. \”Future value of any currency which has a higher interest rate is at a discount to a currency which has a lower interest rate

Hi Karthik,

I wanted to know more about how \”Forward Premia\” is factored in the prices, I checked in the next chapters also but there was no mention of this.

Can you please share some thoughts or links where I can read more on this. It seems if we keep the contract(with future premium) for long enough time it can actually be profitable.

if we keep the contract(with future premium) for long enough time it can actually be profitable —– > possible, but how do you define long enough?

I\’ll try and find links, don\’t have anything on top of my mind just yet.

Sir in previous chapter you told for ex

India having high interest rate is good for domestic currency and US having low is not good

Given this how can INR trade in discount in future given in india interest rate remains high

As said in this chapter

Hmm, have explained this in some of the queries I guess. Can you please check? Thanks.

Hi Karthik,

Thank you very much for writing this article. Just one thing, doesn\’t forward premia and interest parity imply that USDINR will keep appreciating if the current trend continues (i.e. the RBI having higher interest rates than the US Fed). When I say USDINR will keep appreciating, I mean that the strength of the dollar will be more than the strength of the rupee (speaking in relative terms).

Technically yes, but for that interest rate should be the only factor to affect the pair, but in reality its not as there are multiple factors at play.

Sir,

In previous chapter you discussed about interest rates/ carry trade where it is mentioned that the currency with higher interest rates will attract more investment and currency goes stronger.

But by interest parity the currency with high interest rate loses it\’s value.

Please throw some light on this

At a conceptual level yes, but then the traders set up currency hedges on forward rates and cover for the any value erosion.

Sure Karthik. Thanks. Small feedback – Would be great if there is a notification whenever a query is raised or answered. I believe there was another user who also mentioned this. Will help immensely. With the amount of effort and dedication that you and the team have put into compiling all of this, eventually the notification thing will get sorted out also.

Thanks, Himanshu. I will check on the notification bit. Last time I checked, the notification turned into a SPAM, especially since the number of queries is quite a few.

Hi Karthik,

Referring to the end of the module: \” Generally speaking, the future value of any currency which has a higher interest rate is at a discount to a currency which has a lower interest rate \”. However, \” Clearly the country offering higher interest attracts a lot more foreign investment into the country, naturally this leads to the strengthening of the domestic currency \” as per the previous chapter. The above points seem contradictory. Kindly clarify and explain. Thanks.

Hmm, let me check this again. But in general, there are several moving parts Himanshu. Interest rate, its relative perception (high/low) to other currency, which in turn is connected to inflation and the underlying economy. So when dealing with currencies, you need to look at all these attributes.

Great article on forward premia and interest rate parity.

I want to know that does this concept of forward premia always applicable in the forex markets? If so, the INR will continue to diminish against USD because in USA the interest rates are low in comparison to India and one can easily take advantage of this.

Or is it just a theoretical model and price actually depends on various other factors? If so, how can we use the concept of forward premia to design a trading strategy? I mean how will we know that the other macroeconomic events will overpower the concept of forward premia and will actually create a chance for fairy trade.

It is a theoretical model and fluctuates based on the real demand-supply forces in the markets.

I thought that\’s the gist of this chapter.

Forward Premia, F = S * ( 1+ Roc * N) / (1 + Rbc * N)

India has higher deposit rates than US. So it means India has high forward premia. Which means INR will continue to weaken over time to cancel the arbitrage opportunity.

So seems like, \”High-interest rate = High Forward Premia = Weaker currency\” is also true.

I agree on the abr opportunity diminishing. However, not with the \’INR will continue to deminish\’, I\’m not sure 🙂

So from my understanding

High-interest rate = Low inflation = Stronger currency

Also,

High-interest rate = High Forward Premia = Weaker currency

What?

High-interest rate = Low inflation = Stronger currency — yes.

Not sure about the other one.

Hi Karthik,

I have gone through Interest rate parity formulla.

What my doubt is as per this formulla if interest rate in India is higher then INR will goes on depriciating ..

But Interest rate in India will remain always higher India is growing country in which gdp growth likely to remain rate is 7-8 % and so the inflation will remain in this range and so the Interest rates going to be 7-8 % in future .

Whereaa USA is developed country and interest rate are not going to go up more than 3 %

So due to this diff will (7- 3 )% in future so does this mean by formulla , that INR will goes on depreciating ?

Not really, remember the strength of the currency also depends on trade outputs, geo political situation, macros etc.

Hi Karthik,

Since STT is not applicable on currency futures, is it not more profitable trade than equities?

Or is there any hidden charge (Income Tax) which will turn the equation?

Thanks,

Akshay

No hidden charges as such, Akshay. All charges are mentioned here – https://zerodha.com/charges

Hi Karthik,

If the concept of Forward Premia holds good, keeping all other factors constant, the value of INR should depreciate every year against USD to hold up interest rate parity. But this does not happen, INR has pretty much ranged in 60s against USD for so many years. Why so?

Thanks,

Akshay

Akshay, does the forward premia capture all the macro (both economic and geopolitical) factors in play? If the answer is no, then perhaps its a flawed model to begin with.

So that means that Interest Rate Arbitrage Opportunities do exist?

I suppose so, Akshay.

Since we discussed that carry trade opportunities do exist and USDINR does not always depreciate linearly at risk free interest rate, does it make sense to short one year future contract (USDINR 19 OCT is trading at 73.23, 18 DEC is at 70.80) with the hope that 1 year future spot rate will be less than 73.23?

Well, from what I hear, the carry trades are losing its sheen. Btw, what you suggest is a straightforward directional trade, you should if you think the INR will gain strength.

Hi karthik,

CAN u plz in ur simple language explain its meaning:::::“Generally speaking, the future value of any currency which has a higher interest rate is at a discount to a currency which has a lower interest rate.”

thanks.

Basically, if a country offers higher interest rate (risk-free) then the currency strengthens against another country\’s currency where the interest rate is lower. This is just one of the factors which influence the currency movement.

Sir in the previous chapter you said that when a country\’s rate of interest is high the country receives higher FDI and correspondingly its currency value increases. Since India has a higher rate of interest shouldn\’t the USD/INR pair value decrease after one year instead of increasing to 71 after 1 year ?

Hina, the rate of interest is just one of the factors. There several other factors which influence the currency pair.

\”Generally speaking, the future value of any currency which has a higher interest rate is at a discount to a currency which has a lower interest rate.\”

Future value of INR is at a discount to present USD or present INR?

This can be attributed to general demand and supply situation in the currency.

a correction needed: In the last para \”Rupee is considered to be at a discount now\” should be \”Dollar is considered to be at a discount now\”

Let me check this Kumar. Thanks for pointing this out.

Please expedite your presentation on FNO currency trading dollar rupee.

All chapters on currencies is already done.

Thanks Karthik Sir

right now focusing on USDINR pair. trying to fully understand its swings & effect of different factors playing on it

Good luck Arvind!

seems like currency trends within limited range & easy to predict than stocks . it can be better option if play by rules. we can always get out tommorow if i made a loss . is there any catch , hidden charges ? 🙂

Nope, no catch, no hidden charges. If you know your game well, then there is nothing that can stop you. Good luck.

am i getting it right ? trading in currency is less risky than trading in equity , indices or commodities & offers better returns ? 🙂

Less risky? Yes, I personally believe so since the volatility is on the lower side. Better returns? I cannot comment on this 🙂

Fantastic Article of Forward Premia & Interest Rate parity thank You sir and Thank You fot the Future Price Formula

Thank you John!

SIR,

please add more lessons , my currency exam on 12-6-2016 , i completed nism equity derivatives. exam with 75 % mark all credit goes to zerodha varsity…

Good to know that Sarath!

It takes time to add chapters, request you to have patience.

In currency option trading there is no fixed lot size ? and showing qty in 2 ,562, 307 like wise so what is the amount required to trade in currency usdinr option which is showing 0.34 @ 67.5 call option

Lot size is fixed to $1000, in fact in the next chapter we will be discussing this.

Nice article waiting for more. I would suggest one thing, please add a form of notification like fb, or a automated email sender, whenever you are replying. I am replying in so many modules and have no idea what you replied. WordPress has extension for that.

Thanks for pointing this, We will look into it.