13.1 – Sumitomo Copper scandal

If you are remotely connected to the commodity world, then this is one story you must have heard of – ‘The Sumitomo Copper Scandal’. This scandal unfolded in Japan, around 1995, but the severity of this event sent a ripple down the spine of the entire commodity trading world. So much so, that it’s talked about even today and it gets a special mention whenever the financial world talks about ‘rogue trading’.

Sumitomo Corporation is a huge conglomerate, incorporated and listed in Japan. The company is involved in general trading of goods and commodities. Back in the days, Sumitomo had a significant copper trading division. Sumitomo’s copper trading involved buying of copper in the spot market and physically storing them in its warehouses. The company also had a large exposure to copper futures on the London Metals Exchange (LME). Yasuo Hamanaka was Sumitomo’s chief ‘Copper Trader’. He was Sumitomo’s go-to man for anything related to Copper.

So here is what happened –

- Yasuo Hamanaka bought copper in physical form (spot market) and hoarded them in warehouses.

- He bought copper not just in Japan, but across the world and stored it at different locations/ports.

- Essentially, he was long copper in the spot market.

- His exposure in the spot market was around 5% of the entire world’s outstanding reserves. At that point, he was probably the only man on the planet with so much copper. This meant he could control the prices of copper, quite literally.

- At the same time, he also bought Copper Futures at LME.

- Every trader knew that Yasuo Hamanaka was copper bull, but nobody knew the extent of his exposure (as LME wasn’t publishing open interest data at the time).

- Whenever traders or trading firms shorted copper, Hamanaka would buy. He could buy because Sumitomo was cash-rich and funded these trades.

- Since he bought in such large quantities, copper prices went up.

- Remember, copper is an international commodity, and the price is market-driven (LME futures).

- So LME prices went up – short traders were squeezed, Hamanaka made profits on futures.

- Short traders would eventually default, which meant they had to deliver copper upon expiry.

- Invariably these traders would end up buying copper from Sumitomo at a premium, which meant Sumitomo minted crisp profits on their spot position as well.

- The profits snowballed, and Yasuo Hamanaka became the undisputed king of copper.

This set up functioned really well for over a decade. However, sometime around the early 90s, China upped its copper production, to an extent where they flooded the market with excess supply. Naturally, the prices started to cool off, and Yasuo Hamanaka started feeling the heat. His exposure was so large that it was difficult for him to offload the contracts (especially since he was doing most of the buying)! He went to the extent of borrowing funds to maintain his long positions. Remember, these were all leveraged positions, and when you have super large quantities of any leveraged positions, a small move against you can result in massive losses.

This is exactly what happened – copper prices crashed, and Yasuo Hamanaka’s copper kingdom collapsed. Losses piled to the extent that the Sumitomo Corporation filed for bankruptcy. The estimated losses were close to a whopping $5 billion, in 1995!

What followed next were the routine blame games, lawsuits, denials, and all the resulting drama. However, the key take away from this story is the importance of risk management. We will talk about this soon in a separate module altogether.

Anyway, that was that; let’s move ahead to copper basics.

13.2 – Copper Basics

Copper is a base metal, highly traded on MCX. A metal is classified as a ‘base’ if it is not precious like gold and silver.

The daily traded value is approximated at INR 2,050 crores across an average of 55,000 lots. So, as you can imagine, copper on MCX is a very liquid contract. The liquidity matches that of crude oil and gold.

Copper is an exciting metal. It is the 3rd most consumed metal after steel and aluminium. The price of copper (much like aluminium) is directly dependent on global economics. You may know, copper is one of the best conductors of electricity, and therefore, copper is the preferred choice of metal in electrical wires. In fact, did you know, at the core of Tesla’s hybrid car there is a copper motor as opposed a regular engine motor (permanent magnet motor)?

Check this article.

Of course, apart from this, copper finds its application in a whole host of other things such as –

- Building and construction

- Copper alloy moulds

- Electrical and electronics

- Plumbing solutions

- Industrial uses

- Telecom

- Railways

But my favourite application of copper has to be this –

Can you guess what this is? If you can, then probably you and I have a common interest. J

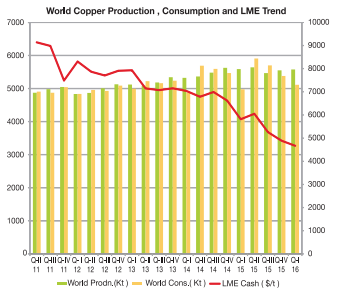

The demand – consumption of copper, showcases similar trends as aluminium. Have a look at this snapshot –

Source: Hindalco annual Report (2015-16)

Source: Hindalco annual Report (2015-16)

In 2015, the global demand for refined copper was 24 million tons; half of this demand was from China and Japan. The supply was higher than the demand (look at the last two bars from right), and thanks to the recent commodity glut, the price has considerably cooled off over the last few years.

It’s good to know fundamentals, but like any other commodity; I’d rely on charts to trade copper. Given this, let’s focus on the contract specifications. Of course, both aluminium and copper have two contracts – the big copper contract and its mini version. Let me list down the contract specs of the big copper contract.

- Price Quote – Per kilogram

- Lot size – 1 metric ton

- Tick size – Rs.0.05

- P&L per tick – Rs.0.05 * 1000 = Rs.50/-

- Expiry –Last day of the month

- Delivery units – 10 MT

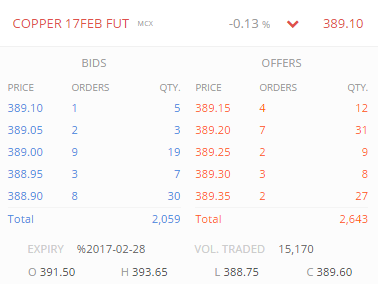

Here is the snap quote of copper, expiring in Feb 2017 –

The price as seen here is Rs.389.1 per Kg. The contract value, therefore, would be –

Lot size * price

= 1000 * 389.1

= Rs.389,100/-

The NRML margin is as shown below –

Rs.30,544/-, which works out to 7.8%. MIS margin is half this amount.

The Copper Mini contract has a lesser lot size, therefore lesser P&L per tick, and lesser margins.

- Price Quote – Per kilogram

- Lot size – 250 Kgs

- Tick size – Rs.0.05

- P&L per tick – Rs.0.05 * 250 = Rs.12.5/-

- Expiry –Last day of the month

- Delivery units – 10 MT

I’d suggest you look at technical analysis to trade copper, and commodities in general. They work really well on liquid commodities such as copper. So essentially, you need to know the contract details to get started.

Onwards to Aluminium!

13.3 – Aluminium Basics

Remember, our objective here is to understand basic information. We are not going deep into the subject, simply because most of us would be trading this commodity with an average holding period of not more than 2-3 days. When this is the objective, it makes more sense to spend time on the price dynamics rather than the fundamentals. Hence, I’ll stick to basics, and for ease of reading, highlights of the chapter are presented as bullet points. Post this; we will dig deeper into contract specifications.

Talk about Aluminium and chances are you will think about that wafer-thin, silvery foil, which wraps your leftover food in your refrigerator. Well, Aluminium’s applications go beyond that.

Here are a few things you need to know (have collected this information from various online sources) –

-

- There is plenty of Aluminium (supply is not an issue) – roughly 8% of the earth’s crust is made up of Aluminium. This makes aluminium the third most abundant, after oxygen and silicon.

- The fact that aluminium resists corrosion makes it a very desirable metal.

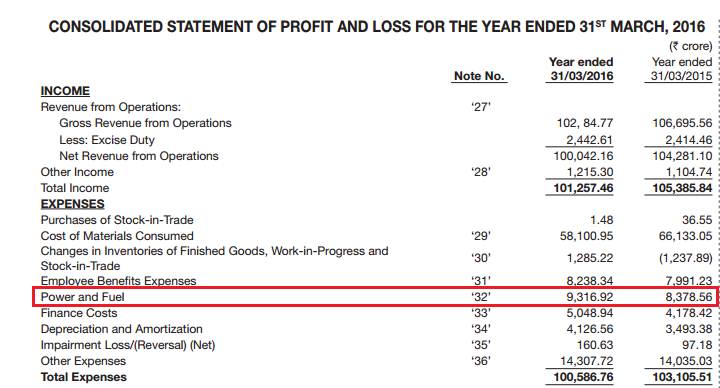

- Aluminium manufacturing is power-intensive – it takes a whopping 17.4-megawatt-hour of power to manufacture 1 metric ton of Aluminium. Check this –

This is power and fuel cost of Hindalco (the leading manufacturer of Aluminium), and as you can see, nearly 10% of the expense is on power and fuel. Remember, Hindalco has its own captive power units. So, I’m guessing this power is consumed over and above what Hindalco generated internally.

- That said, recycling aluminium is a power-friendly affair. It requires just about 5% of the power to recycle.

- Aluminium has a wide range of applications – right from a smartphone to a Boeing 747. Did you know you need approximately 70,000 kilograms of aluminium is used up in a single Boeing 747?

- Aluminium is also used up in other industries – automotive, building & construction, defence, electrical, electronic, pharmaceuticals, white goods, etc.,

- Aluminium is one metal that has abundant supply and demand.

- Aluminium prices on MCX closely follow the international prices of aluminium which is traded on the London Metal Exchange (LME).

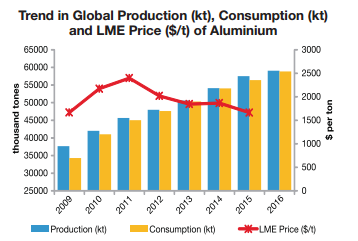

In fact, here is a snapshot which gives you the trends in production, supply, and the average price of aluminium on LME –

Source: Hindalco Annual Report (2015-2016)

This is a fascinating chart; in fact, based on this chart alone, a few basic trading principles can be formulated. Let’s break this graph up in smaller bits –

- The global production (blue bar) of aluminium in 2015 stands at 56 million tones. This represents a growth of about 4% from the previous year.

- The global production nets a CAGR of 6% over the last 8 years.

- The demand (yellow bar) on the other side matches up to global production – this implies that there are no supply-demand disruptions.

- In fact, demand and supply have remained more or less stable over the years.

- The price of aluminium over the last few years has declined. Its averages to $1,500/- per ton, which is a decline from its recent peak of $2,500/- per ton. You must have heard about the global commodity glut. Clearly, the Chinese demand plays a key role in the aluminium’s global pricing.

- The Indian demand, on the other hand, is better than the global demand (in percentage terms). Hindalco, in its annual report, claims the demand for aluminium in India is about 2 million tonnes. Much of this demand is met by importing aluminium.

I guess these basic points should help you get started on Aluminium fundamentals. However, I’d be happy to trade aluminium based on technical analysis, simply because of my short holding period, usually not exceeding a few trading sessions.

So, with this, I’d like to move ahead and discuss contract specifications, which will help you understand the practicality of trading aluminium on MCX.

13.4 – Aluminium contract specifications

As you may have guessed, there are two main aluminium contracts to trade on MCX. They are the big aluminium contract and the aluminium mini contract. Clearly, both of them differ on the lot size and therefore contract value. We will discuss the big aluminium contract first.

The daily average traded value of big aluminium is roughly about INR 375 Cr. On a good day, the volume could reach a little over INR 500 crores. As you may have realized, the value is not as high as commodities such as gold and crude oil.

The contract details are as follows –

- Price Quote – Per kilogram

- Lot size – 5 metric ton

At this point, you may have realized that this is a huge contract. A metric ton is 1000 kilograms, so 5MT makes it 5000 kgs. Since the price is quoted per kg, and the lot size is 5000 kgs, each tick will cause a P&L of Rs.5000/- PROVIDED the tick is Rs.1/-. Since this would be very large, especially for retail trading, MCX has reduced the tick size to the lowest possible value, i.e. Rs.0.05

- Tick size – Rs.0.05

- P&L per tick – Rs.0.05 * 5000 = Rs.250/-

- Expiry –Last day of the month

- Delivery units – 10 MT

Let’s understand this information in better detail. Aluminium on MCX is quoted on a per kilogram basis. Have a look at the image below; this is the snapshot of Aluminium’s market depth –

As you can see, the aluminium expiring in Dec 2016 is trading at Rs.118.4/- per kg/

The lot size is 5 MT (5000 kgs), which means to say that if you want to buy (or go long) on Aluminium, the value of such a contract will be –

Lot size * price quote

= 5000 * 118.4 (offer price to go long)

= Rs.592,000/-

The price movement in aluminium is 0.05, which means, if aluminium moves from 118.4 to 118.45, the profit will be –

118.45 – 118.4

=0.05

=0.05*5000

=Rs.250/-

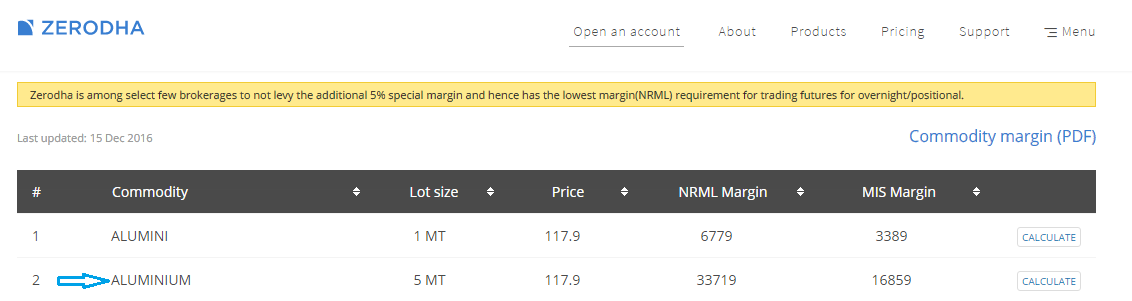

What about the margins? Have a look at the following snapshot –

The NRML margin charged is Rs.33,719/- which works out to 5.6%. However, MIS margin is almost half of the NRML margin.

Here are the contact details of Aluminium mini –

- Price Quote – Per kilogram

- Lot size – 1 metric ton

- Tick size – Rs.0.05

- P&L per tick – Rs.0.05 * 1000 = Rs.50/-

- Expiry –Last day of the month

- Delivery units – 10 MT

The contract value is quite small –

= 1000 * 118.4

=Rs.118,400/-

NRML margin is Rs.6,779/-,, which is 5.7%. MIS margin is much lesser at Rs.3,389 or just about 2.8% of the contract value.

P&L per tick is Rs.50/-, a value which is much ‘deal-able’ while trading.

I guess this info is good enough to get started on trading with Aluminium. Frankly, you need to look at the chart, develop a point of view, and place trades based on the chart pattern. If you are keen on digging deeper into aluminium, I’d recommend you spend time reading up on www.world-aluminium.org and www.aluminium.org.

Key takeaways from this chapter

- Both Copper and Aluminium are base metals.

- Aluminium is found in abundance (next only to silicon and oxygen).

- The demand-consumption of aluminium and copper seem to have some equilibrium.

- The prices of both aluminium and copper have declined over the years.

- The prices of aluminium and copper on the London Metal Exchange (LME) act as a reference price for these international commodities.

- Both copper and aluminium have two contracts – the big one and mini.

- The contracts vary in lot size and therefore contract values and margins.

Last 2 days saw international spot copper moving ~7% but Copper futures in MCX moved barely 2%. There was similar disparity in silver. Given the MCX future is based on international spot price, why is it not moving in line with the international spot price?

Let me check this, Siddharath. I\’m not really following the copper market.

isnt..crude oil and natural gas cash settled.

Check this – https://support.zerodha.com/category/trading-and-markets/trading-faqs/commoditytrading/articles/mcx-expiry-settlement

Hi kartik, thanks for quick reply. please can you also clarify settlement procees for below.

1. Silver Mini

2. Crude Oil Mini

3 Natural GasMini

I did check on internet, but some say its physical, some say its cash settled. thanks. please clarify the latest.

They are all physically settled, but you need to close the position 5 days before the settlement.

Hi Karthik, Is aluminium mini contract cash settled or physical delivery. please explain. and how many days before should we close the contract to avoid delivery.

Heena, it physical delivery and the contract should be closed 5 days prior. Check this – https://docs.google.com/spreadsheets/d/1AdXr4voOKs2RpxftI_eJ78J7j-fBremMGiOOnf0I9jc/edit?usp=sharing

Karthik is a single malt kinda guy, haha, it was a fun trivia there in the pic.

Lol 🙂

Sir, Why Steel is not traded as commodity in international market like Cooper and aluminum.

Ah no idea, Suraj. Need to figure why 🙂

Hi Karthik, What all are the factors affecting for metals and how it is affected to MCX metal prices ?

I\’ve tried to explain this in the module itself, request you to kindly check once.

Are copper mini and aluminum mini contracts not available now ?

I don\’t think these contracts are available now.

Sir I\’m tracking,every commodity you have mentioned Which are liquid

For ex now I need to look at Copper this month contract same with chart after expiry I need to look at next month contract

Is my thought process right

Thats right, Bharath.

Sir to track only Charts which contract to follow there are many contracts with different prices

Track only the liquid ones, Bharath. The ones which are easy to buy and sell.

Great work man ! Even in lovkdown I am learning this and studying on it. It looks so simple but the hardwork behind that is very much.

Thank you

Happy reading, Krishna!

hi sir,

does diwali effect the price of gold

Not much, Gold is an international commodity 🙂

The commodity charts are by contract. Does Zerodha provide long term charts for all commodities with spot prices. If not please advice alternate website for long term analysis and chart comparison (eg: Aluminium prices with Hindalco for last 5 years)

Hi Karthik

i am going to trade in commodities , for that could you provide solution for the below

1) For Trading base metal what will be the frequency of technical chart (30 min , 1 day etc..,), i am not going to do intra day

2) For Trading Precious metal what will be the frequency of technical chart (30 min , 1 day etc..,), i am not going to do intra day

1) If you are not doing intraday than you can look at EOD charts

2) Same as above

Thanks for you solution

For setting target and stoploss can i use 1 year data

Yes, start with 1-year data and then get a perspective by considering 6/3 months data.

What is the difference between NORMAL order and MIS order.

Normal provides you regular leverage and used when you want to carry forward the position overnight. MIS is when you want to trade intraday and want extra leverage.

Hello.

Small Correction : \’this is the snap shot of Crude oil’s market depth\’ above aluminium market depth window in explanation of aluminium contracts 🙂

Ah, thanks for pointing this Kiran. Will check this.

Hi karthik,

what is delivery units.

The quality that will be physically delivered, in case you wish to take delivery of the contract.

Dear karthik,

isn\’t the application of copper u shared a picture with in this chapter is the whisky barrels??

Yup, belongs to the Glenmorangie Distillery 🙂

Karthik

I am trying to analyze both Copper and Aluminium futures using ML Concepts and trying to predict future prices. Where i can get either individual tick data or 5 min or 1 hour data for last 1 to 2 year. I am ready pay for the data too. Kindly re-direct me where to buy or download it.

Regards

Seetharaman

You can load 1-minute data of these commodities in Pi and download the same.

Nice,

Can you give a chapter on Zinc?????

I seemed to have missed that, will try and put up a note on it. Thanks.

All Latest Aluminium news:

https://aluminiumcurrentnews.blogspot.in

1.) How copper and aluminium price on market is related ?

2.) What clue aluminium gets from copper price ?

3.) Copper and aluminium is how much dependable ?

Santosh, I\’m afraid I don\’t have these answers for you. Like I have mentioned in the module, I\’ve largely stuck to TA for commodities.

Hi,

Please tell trade timings of international markets like lme, cme, shfe according to indian hours.

Each market has a different timing, it\’s best you google for this information.

Thanks for the information you\’re sharing Karthik 🙂

Any plans to introduce us learners to Bond markets anytime soon?

That has been on the cards for a while, Prabhav…bot not a priority as of now. Hopefully, I will do that sometime soon.

What happens if my commodity margin sufficient exceeds the required margin available in my account.Will it be automatically squared off at the closing time?I have bought the commodity as NRML position.If so i have 3 positions, which one will be squared off?

Gajha, at the end of day, the system will check for Cash balance in your account and settle it for your Mark to Market losses. However, if there is no cash balance, your position will be squared-off if NRML margin falls to 70-80% of required margin. This is at the discretion of our RMS team

The commodity charts are by contract. Zerodha must provide the chart for the MCX commodities without contract years it will help trades. Currently trader need to use Investing.com that is not real-time.

We will soon provide continuous charts for commodities.

Thanks for amazing module sir, very informative.

PS: we do have common interests 😀

And that common interest in Gaelic is called, \’Uisce Beatha\’ 🙂

Cheers to that 🙂

Hi Karthik, which software, website or app you recommend for technical analysis on copper or commodity in general?

Kite.zerodha.com 🙂

Thanks for your valuable effort KARTHIK, It is very helpful.

Any particular topic on Zinc ?

Thanks Ravi.

Will try and put up a chapter on Zinc sometime later. As of now, I believe the contract is not too liquid.

why dont we have limit cover order (only market order)for commodity?

Will get back to you on this soon.

I know i read it,but i wanna more depth on it

What are you looking at specifically?

About LME and fundamentals,demand & supply…..

Sir plz make some detailed modules for base metals.

We have covered quite a few base metals, Vishal. Are you looking for anything particular?

yes about aluminium & lead.

Already there Vishal.

Dear sir,

I am fresh in trading… now i am trading with MIS (intraday) based copper commodity. i want to know how to trade with long term stock holding rules and regulation…

I\’m not sure if there are any rules and regulations as such to keep in mind. Is there any particular area concerning which would like to know more?

Hi Karthik,

Wishing you and your family a very happy and prosperous year.

Do you have plan of module on Mutual Fund?

Thanks and wishing you and family the same!

Yes, in fact personal finance is a module I\’m eager to write. But the next module will be on Risk management. But will do MF bit soon.

Sir there is no download pdf option for commodity market

Commodities module is still work in progress. We will have the PDF once the module is complete.

Wishes a happy new year to u yr family and entire team.

Thank you and wishing you the same 🙂

Sir any best book as per you to learn stock marker trading stragety?For intraday or shortterm.

Thank you..

We will be discussing few of them here on Varsity, I\’d suggest you look into that 🙂

Also, I;m not too sure good books on the topic you mentioned.

Have any chance to copy of Varsity in Tamil Language

Not yet, maybe sometime in the future 🙂

Hi Karthik,

Can you please suggest some books related to trading, which you think are good/must reads.

Thanks!

Any particular topic within trading?

Hi Karthik,

Wishing you a happy new year,I request your take on Trading Discipline,Though it may differ from every individual on planning his or her day for the trading hours.

Thanks Surya. wishing you the same!

Hopefully, the next module will be on this topic.

Hi,

Reading about scandal something came in mind.

Do you know what happened with Religare online securities ? They got in some issue and didn\’t return money for the retailers who had gold in their account.

Not sure Varun.

Please write a detailed article on \’shorting\’ in particular and also \’intraday trading\’ in general.

Here you go – http://zerodha.com/varsity/chapter/shorting/

Thanks Karthik for putting up this module and looking further for other base metals 🙂

My questions:

1. Where can I get a detailed chart for Copper/Alu say for an year or two to analyze? The one on the Feb Contract (e.g.) will not have enough price action details unless it is a near term contract.

2. Is commodity less volatile than equity in terms factors (operators, insider trading e.g.) and move more in line to TA?

Regards,

Somnath.

1) Kitko metals/Net dania are both good places for historical LME prices

2) Not really, at time commodities can get more volatile than equities.

Sirji, how to see MCX chart for longer term? I am unable to see on the site

Try Kite or Pi for this.

Sumitomo Corporation story was amazing. i heard this news but didn\’t know real insight. Thanks for sharing the story. The whole topic about Copper & Aluminium is as usual very good. Hope next chapter will publish in new year. Till then wish you all Zerodha team merry Christmas and a very happy new year.

Glad you found it engaging 🙂

Wishing you a brilliant new year!

Thank sir for this new chapter

Happy Merry christmas to you and your family.

Thanks and wishing you the same 🙂

Very nice reading and informative Karthik. Thanks.

Welcome!