2.1 – Dual View

Think about a stock, Infosys for example, when you buy or sell Infosys – your view on the stock is straightforward – you are either bullish or bearish on Infosys. Therefore, you buy or sell Infosys. Now think about a currency pair – say USD INR, when you buy or sell USD INR, whether you know or not, you have a dual view on the pair. For instance, when you buy USD INR; it implies you are bullish on the US Dollar and bearish on the Indian currency.

Why is it this way you may ask?

Well, the value of a currency is always quoted against another. Recall from the previous chapter – the currency pair is quoted as –

Base Currency / Quotation Currency = Value

In other words, this format tells us how many units of quotation currency one can buy for 1 unit of the base currency.

If you buy a currency pair, clearly it implies that you expect the value of the pair to go up. Consider this example – USD INR = 65, one would buy the pair, hoping for the price of the pair to hit 68.

Now if the price of the pair is expected to increase, then it implies that in the future 1 unit of base currency can buy more units of quotation currency, i.e. 1 USD to buy more INR.

In other words, if the value of the pair goes up, then the power of the Base currency goes up while at the same time, the quotation currency weakens. This translates to you being bullish on the Base currency and bearish on the quotation currency at the same time.

Similarly, if you sell the USD INR pair, it implies that you anticipate the Base Currency to buy a lesser amount of quotation currency. This translates to you being bearish on base currency and bullish on the quotation currency.

Given this, “strengthening/weakening of a currency” refers to the following situations –

- Base currency strengthens when it can buy more units of quotation currency. For example, USD INR moves from 67 to 68; it means the base currency (USD) strengths and the quotation currency (INR) weakens.

- Quotation currency strengths when the base currency buys lesser units of quotation currency. For example, USD INR moves from 66 to 65; it means the base currency (USD) weakens and the quotation currency (INR) strengthens.

Note that strengthening and weakening of a currency are equivalent to a currency appreciating and depreciating. These terminologies are often used interchangeably.

Before we proceed, here is something you need to know. Just like a stock, the currency (and the currency pair) has a ‘two-way quote’. The two-way quote enables one to identify the rate at which one can buy and sell the currency (and currency pair).

Don’t get thinking on the ‘two-way quote’, it simply refers to ‘Bid and Ask’ rates J, but we do need to touch upon this as its vital to know how the two-way quote works.

Have a look at the image below –

This is a snapshot of the currency spot rates, as quoted on a Forex trading site. For the sake of this discussion, I’ve highlighted the two-way quote for EUR USD and GBP USD. The quote gives you the rate at which you can buy and sell the currency pair.

For example, if you want to buy the EUR/USD – you will have to buy the pair at the ‘Ask’ price, i.e. 1.1270. When you buy the pair, technically you are long EUR and short USD. Likewise, if you want to sell the EUR/USD, then you would do so at 1.1269 (Bid price), and here you would be short EUR and long USD (remember the dual view concept).

The pairs are sometimes quoted in a short form, which is actually quite a popular way to quote currencies internationally. The shortened two-way quote would be something like this for the EUR/USD pair –

EUR/USD – 1.1269/70.

If you notice in the shortened version, the ‘bid’ price is stated in full, but only the last two digits of ‘ask’ is stated.

Further, in the Forex lingo, digits are referred to as ‘pips’. Therefore, if the EURUSD moves from 1.1270 to 1.1272, then it means that the pair has moved 2 pips.

2.2 – Rate fixing and conversion path

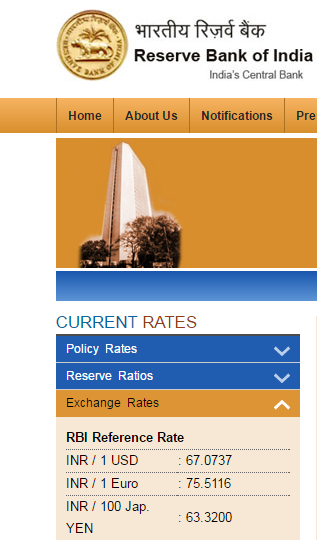

As of today, the USD/INR rate stands at 67.0737. This rate is fixed by the RBI daily, and is called RBI’s ‘Reference Rate’; in fact, RBI publishes these rates daily on their website. The Reference rate acts as a crucial input for the currency futures trading as all settlements are based on this Reference rate.

Have a look at this –

The above is a snapshot from the RBI’s site showing the reference rate for 14th June 2016. Do note; these are spot rates and not future rates. Future rates are as seen on NSE’s website.

Anyway, the obvious question is – how does the RBI arrive at this rate?

Well, nothing hi-tech here, RBI follows the age-old method of polling to arrive at the spot rate! Click here to see the RBI circular that explains the rate-fixing procedure, but if you are in no mood to read the circular, you could read the following points that summarize the procedure.

- RBI has identified a list of banks based on their market share in the foreign exchange market. RBI calls them the ‘contributing banks’

- Every day between 11:30 AM and 12:30 PM RBI calls a set of banks (randomly selected) listed under the contributing banks and ask them to give a two-way quote on USD INR

- RBI collates these rates and averages out the rate based on the bid and ask

- The average rate is set as the USD INR rate for the day.

- The same process is repeated every day except for weekends and bank holidays.

It’s as simple as that!

The procedure is quite simple; however, RBI polls only for the USD INR rates. For the other major rates, i.e. EUR INR, GBP INR, JPY INR RBI adopts a technique called ‘Crossing’ also referred to as the cross rate mechanism.

While crossing, the direct rate of one currency is not available concerning another. For example, the direct rate of Euro concerning INR is not readily available; one needs to cross these rates with a common denominator to arrive at the rates.

Let me take the example of deriving the EUR INR rate by crossing, keeping USD as the common denominator. Hopefully, this will give you better clarity on the crossing technique.

Let us begin with getting the spot rate for USD INR, as we can see from the snapshot above, the USD INR spot is –

USD INR – 67.0737

This is the spot rate; the two-way quote for this would be something like this –

USD INR – 67.0730 / 67.0740

This means if I have to buy 1 USD, I need to pay INR 67.0740 and if I have to sell 1 USD, I will receive INR 67.0730.

Let’s keep this information aside. We now focus on EUR USD spot rates from the international markets.

The two-way quote from Bloomberg suggests –

EUR USD – 1.1134/40

This means I need USD 1.1140 (Ask price) to buy 1 Euro. In other words, the cost of 1 Euro in terms of the US Dollar is 1.1140. Hence if I convert the price of 1.1140 USD to INR, then I will have enough INR to buy 1 Euro, and by doing so, I will also get the EUR/INR rate.

Now going back to the USD INR rate –

1 USD = Rs.67.0740

1.1140 USD = How many Rupees?

= 67.0740 * 1.1140

= 74.72044

Hence to buy 1 Euro I need 74.72400 INR, or EUR INR = 74.72400

Notice how the USD acts as a pivot in the crossing technique.

Now here is a simple task for you – using the crossing technique, we have calculated the ASK price of the EUR INR pair, can you extend this logic to calculate the Bid price for the EUR INR pair? Feel free to post your answers in the comments section below.

If you think about this, it’s now clear that the reference rates and the cross rates change every day based the sentiments of the contributing banks. This leads us to a bigger question – what influences the sentiment of the contributing banks?

The answer is quite simple – domestic and international events.

2.3 – Events that matter

Think about an event that can potentially change the sentiment on a stock. Quarterly result of the company is one such event. Estimating the change in sentiment based on this event is quite straightforward. If the quarterly result is good, the sentiment is positive; therefore, the stock price is expected to go up. Alternatively, if the quarterly result is not great, the sentiment is hurt, and therefore the stock price is expected to go down. The point here is, there is some linearity between the event and the expected outcome.

However, when it comes to currency pairs, there is no such linearity, which makes it a herculean task to assess the impact of events, a.k.a. fundamentals on currencies. The complexity mainly stems from the fact that currencies are quoted as pairs. While some factors lead to the strengthening of a pair, an event could occur at the same time that weakens the pair.

Let me give you an example to illustrate this – imagine two economic events running in parallel. Event 1 – India receives a continuous inflow of Foreign Direct Investments (FDI) geared towards long term investments. Clearly, this is a big positive for the economy, and therefore it tends to strengthen the INR. Event 2 – There is an uptick in the US economy (or a fear of a crash in commodities) leading to an appreciation in the US Dollar.

Given these two events occur in parallel – which direction will the USD INR currency pair move? Well, the answer to this is not straightforward. Eventually, the currency pair will take cues from the more dominant of the two factors and head in that direction, but until this happens, the pair invariably exhibits volatile behaviour. Hence, to successfully trade currencies, it becomes essential to track world events and assess their impact on the currency pair in question.

Here are few such events and data that you should track –

Import/Export Data – These numbers are highly significant, especially for a country like India, whose economy is susceptible to trade deficits. India exports goods and services such as rice and software and imports commodities such as crude oil and bullion. In general, an increase in exports tends to strong domestic currency, and an increase in imports tends to weaken the domestic currency. Why do you may ask?

When imports are made (crude oil, for example), the purchase has to be made in the International market, which requires one to pay in USD. Therefore one has to sell INR and buy USD to facilitate this purchase, which in turn causes a demand for USD and hence USD strengths.

We can extend the same logic to exports. When we export goods, we receive USD; we sell the USD received and convert to INR. This causes the INR to strength.

The Trade Deficit – the excess of imports over exports is a key factor to track as it influences the direction in which the currency trades. In general, narrowing the trade deficit is positive for the domestic currency. The trade deficit is also referred to as the ‘Current account deficit’. I’d suggest you read this news piece to reinforce your understanding of this topic.

Interest Rates – Typically, investors borrow money from countries where the interest rate is low and invest in countries where the interest rates are high and profit from the interest rate difference. This is called the ‘carry trade’. Clearly, the country offering higher interest attracts a lot more foreign investment into the country. Naturally, this leads to the strengthening of the domestic currency. This clearly implies that the ‘Interest rate’ is one big number of currency traders watch out for.

The monetary policy review conducted by the central banks (RBI in India, Federal Reserves in the US, and ECB in the Euro region) reviews the interest rates of the country. This is the reason why there is so much attention paid for the policy review. Besides tracking the actual change in numbers in the on-going review, the market participants look for cues regarding the policy stance. The monetary stance helps the participants understand the future course of action concerning the interest rate.

Dovish – Dovish is a term used to describe the central bank’s stance wherein they are likely to lower the interest rate in the future. Remember, lower interest rate weakens the domestic currency. Here is a new headline talking about the relationship between a dovish stance and the currency.

Click here to see the article.

Hawkish – Hawkish is a term used to describe the central bank’s stance wherein they are likely to increase the interest rate in the future. Remember, higher interest rates attract foreign investments to the country and therefore strengthens the domestic currency.

And here is another new headline which talks about hawkish stance.

Inflation – Inflation, as you may know, is the rate at which the prices of basic goods and services increase over time. If inflation increases, then it means the cost of necessities is increasing, therefore this affects the day to day living of the common man. Given this, the central bank strives hard to keep inflation in control. The link between inflation and currency movement is a bit tricky.

One of the direct mechanisms to curb inflation is by tweaking the interest rates. If the inflation is perceived as high, then the central bank is likely to take a hawkish stance and increase the interest rates.

What do you think is the logic here?

Well, easy money in the hands-on consumers and corporates increases spending; when spending increase merchants smell an opportunity to make higher margins, and therefore this leads to a rapid increase in prices, and thus the inflation increases. When inflation increases, the central banks tend to curb the spending by cutting access to easy money. And how do they do that? Well, they increase interest rates!

Therefore, when inflation is on the rise, expect the central banks to take a hawkish stance and increase the interest rates when interest rates increase, the domestic currency strengths!

Therefore, as I mentioned earlier, the relationship between interest rates and currencies is a little tricky. So traders eagerly track inflation data to figure out what the central banks are likely to do and accordingly take positions on the currency pair.

Remember this – if the inflation is high, expect a hawkish stance by the central government and therefore expect the domestic currency to strengthen. Likewise, if inflation is low, expect a dovish stance (as the central bankers want to encourage spending). Therefore the interest rates are likely to come down. This leads to domestic currency weakening.

Consumer Price Index (CPI) – The CPI is a time-series data, averaged out to capture the prices of basic goods and services. Hence the CPI is a measure for inflation. A rising CPI means inflation is increasing, and vice versa. For the most accurate Indian CPI data and information check this website.

Gross Domestic Product (GDP) – The GDP of a country represents the total Rupee value (for Indian GDP of course) of all the goods and services produced in the country for a given year. As you can imagine, the GDP would be a massive number, and it does not make sense to repeat the GDP number while making estimates or during conversations. Therefore one always refers to the GDP as a growth rate. For example, if the GDP of a country is 7.1%, it means that the GPD number is growing at a rate of 7.1%.

Higher the GDP growth rate, higher is the investor confidence in that country, and therefore the stronger the countries domestic currency.

The list of events that matter while trading currencies is virtually endless. At some point, you will realize that every piece of data you can look at is interconnected with one another. Honestly, it would help if you had not known the unknowns of each event the way an economist would. Understanding the cause and effect relationship is good enough. I’ve listed some of the key events/data points that matter while trading currencies. I guess this would serve as a good start If nothing more.

Key takeaways from this chapter

- The base currency is said to strengthen/appreciate against the quotation currency when it can buy more units of quotation currency.

- The base currency is said to weaken/depreciate against the quotation currency when it buys lesser units of the quotation currency.

- When you go long on a currency pair, you are essentially going long on the base currency and short on the quotation currency.

- When you go short on a currency pair, you are essentially going short on the base currency and long on the quotation currency.

- The RBI sets the reference rate of USD INR daily by conducting a poll; the ‘contributing banks’ participate in this poll.

- The reference rates for other currency pairs are derived by crossing technique.

- Understanding events and its impact on currencies are complicated, simply because of the currency is quoted in pairs and impact on the pair could be similar.

- Eventually, the more dominating event will set the direction for the pair.

- Countries with higher interest rates tend to have stringer currencies and vice versa.

- Lower the trade deficit of the country; stronger is the country’s currency.

- Higher inflation leads to the strengthening of currency and vice versa.

- Knowing the cause and effect of events on currencies helps while trading currencies.

Could you please clarify if the RBI reference rate calculation excludes extreme outliers in the interbank market? Very informative article.

Sir

Suppose I trade currencies, and inflation is high

and I\’m now expecting a hawkish statement from RBI

Here, I anticipate an increase in the quote currency for USDINR.

So I\’m supposed to short USDINR

Am I right sir??

Yes, if you are bullish on one currency and take a long position, that implies you are bearish on another.

Basically,

When there\’s increase in interest rate – Bond prices go down

– Equity market is expected to go down as the companies won\’t have money for

capex

– Currency strengthens (meaning quote currency in USDINR strengthens and the

value of this pair goes down)

Am I right sir?

Yes, thats correct.

Sir

Can u pls simplify why do rupee strengthens when we export and vice versa.

Why do we have to sell USD to strengthen rupee??

The domestic currency strengthens when the underlying economy strengthens. Also when you sell a currency, you are also buying another currency.

Few countries have devalued their own currency just to increase their exports. How can they do that?? By not asking for 2 way quote to contributing banks?

Not sure how and why, Anshul. I need to do some research on this.

How can I take benefit of carry trade? For example : Right now Interest rate are 6.25% in India and in venezuela contain 36% Interest rate so how can we take benefit of this?

Oh okay thanks

The modules offered are great and highly useful. I have one request, please update all the modules as per the current norms and policies. The data offered is of 2015/16 period and so many things have changed since then. I know the environment is quite dynamic and making the modules up to date can be hectic but please do so once in a while. For instance the Reference rate fixing procedure is completely different now. Again, thanks a lot for the information being provided.

Chirag, I get your point. So the intent is not make this a data source, but to help people understand the context of these numbers and how to interpret them. The numbers keep changing as the economy changes.

Recently I had heard a news when I was trading USD/INR.Here\’s the news link https://www.nasdaq.com/articles/snapshot-india-stocks-rupee-swaps-call-at-10:00-a.m.-ist . All these financial instruments they are referring to I have never heard of before. Could you please explain me what they are? What role do they play and where can I find the data for these instruments?

These are all money market instruments which only the institutional investors deal with, Shaunak.

the link http://in.reuters.com/article/india-economy-trade-deficit-idINKCN0Y41L7 given is not working its getting redirected. Can you please share the new link 🙂

Ah they must have moved the links. Let me check.

Hi Sir,

Higher the inflation you say interest rate is expected to go up and so domestic currency should strengthen but my doubt here is, if there is high inflation then doesn\’t it mean that more domestic currency (say INR) is in circulation compared to the same amount of foreign currency (say USD).so in this case as more domestic currency chasing same amount of foreign currency, the domestic currency is expected to weaken right ? why is not so !!

I\’d suggest you watch this video – https://www.youtube.com/watch?v=Qx3YMdcLTZo

Hi Sir,

You have mentioned that \”Higher the GDP growth rate, higher is the investor confidence in that country, and therefore the stronger the countries domestic currency.\”

But my doubt is if the GDP growth is High then won\’t it tend to increase the inflation rate and which eventually will cause interest rate to go up right and so it has to weaken the domestic currency right ? but on contrast you have mentioned it strengthen the domestic currency ! can you please explain .

Hi Sir,

As you have mentioned,

\”USD INR – 67.0737

This is the spot rate; the two-way quote for this would be something like this –

USD INR – 67.0730 / 67.0740\”

Could you please mention how did you get this 2way quote for USD INR based on the spot rate of RBI ?

Yes, its based on the prices from RBI.

Does USDINR weekly options expiry based on spot prize publiahed on RBI portal? Does USDINR spot fluctuate or it\’s constant for a day?

Its based on the futures price, Sandeep.

Will you please explain two way quote for currency pair.thank you in advance

Its the same as bid and ask, Prashant.

Sir i see people trading patterns in currencies. How does patterns work in currency if currency market is driven by global conditions?

The same way it does for Equities and commodities. In fact, anything that has a time series data, you can apply the same patterns.

is this 74.6801916?

You may want to revise the links/data for the RBI reference rate procedure. I think its currently a VWAP method put in place since 2016 and no longer whats mentioned in this article.

Noted.

Sir, so if I bought US$100000 IN USD/INR PAIR, THE PRICE OF USD GOES UP THAT DAY?

Are you asking if you bought a certain amount of USD/INR, will the price go up? Well, not really 🙂

Hi,

I read about Carry Trade and trying to understand . What I deduce from Carry Trade that we sell one currency at lower interest rate and invest in other currency at higher interest rate . For example, if the pound (GBP) has a 5% interest rate and the U.S. dollar (USD) has a 2% interest rate, and you buy or go long on the GBP/USD, you are making a carry trade. which strengthened the USD dollar and reason behind is providing a high interest rates.

On the other hand what I read relation between spot , forward and Interest rate

Example : INR/USD , Spot = 100 , Interest rate INR – 10% , Interest rate – 1%

Formula = Fp/b = Sp/b * [ 1+ ip ]/ [ 1+ib ] ; If we solve this equation we will get a forward value = 108.32 .We deduce higher interest rate leads to weaker the currency and its forward rate is trading at discount . While USD is having a low interest rate trading at premium and leads to strong currency .

Conclusion : When we talk about Carry Trade it means higher interest rate leads stronger the currency while in forward high interest rate leads to weaken the currency .

I hope, I am not blending the two different topics . I am just try to understand the interest rate .

Not sure about that formula, I\’ve not dwelled too much into it. You are right about the interest and currency though 🙂

When inflation is on the rise, expect the central banks to take a hawkish stance and increase the interest rates when interest rates increase, the domestic currency strengths! ( mentioned in module )

Karthik sir , If we connect above line with Import and export trade , when domestic currency strength with high interest rates and high inflation . High inflation leads to high cost on input which will impact the export and import ( less export more import ) and which leads to depreciation in domestic currency . whereas high interest rate leads to strengthen the domestic . On the other hand High inflation leads to weaken the domestic currency ( rise in inputs ) .

So we connect this points sir . Do i need to consider the other factors being equal in this export and import . Only then we can connect the high interest rate make the domestic currency strong .

Of course, there are several contributing factors which has an impact on inflation and therefore the interest rates. Some tend to pull up the interest rates and a few drag it down. So yes, as you mentioned one has to connect all these points to take a call on the currency and the economy.

Typically, investors borrow money from countries where the interest rate is low and invest in countries where the interest rates are high. I need a more clarification on this line . How does high interest rates attract the FDIs ? I guess, we are talking about high interest rate on borrowings .

If we are taking from income perspective like high interest on fixed income and invest in capital goods etc .

Are we talking about high interest rates on borrowing or income ?

I found this article for you, do give it a read 🙂

https://www.thebalance.com/introduction-to-carry-trading-1344843

RBI has identified a list of banks based on their market share in the foreign exchange market. RBI calls them the ‘contributing banks’. Can be include these below banks as \” contributing banks \”.

1.JP Morgan

2.UBS

3.XTX Markets

4.Deutsche Bank

One more question , How market share decide of these above banks . However , In equity segment free float help us to decide the market cap. of a particular company . Can we say transactions of currency exchange , trading of the particular bank in forex and other activities related to Forex market help them to extend their market share or is a base to calculate the maket share of a contributing bank .

Kindly answer my both question 1. JP MORGAN is contributing bank of forex market and what factors are considered for market cap. ?

Shibhika, the market share depends on the contributing bank\’s share in the offline forex market (spot).

Sir, as you have clearly mentioned that trade imbalances do affect the exchange rate and so does the interest rate. INDIA has a huge trade deficit but it also has higher interest rate as compared to other nations then why is it that the USD or be it any other foreign currency so powerful as compared to INR, like is the trade imbalance disadvantage much stronger as compared to the interest rate advantage we have.

The interest rate cannot be tweaked just by looking at the trade deficit, there are other factors at play as well. Like the inflation. The currency value is dependent on all economic factors and just the trade data.

Great read, Karthik. Is it okay to be a little slow in understanding currency quotations? Although it eventually makes sense to me, it takes me a little while to comprehend the different quotations quickly. Also, is currency trading legal in India? I don\’t remember where but I read that forex trading in the forex market or something is penalized by the RBI…I must have misunderstood this, could you please help me understand?

Pradeep, you can take all the time in the world to understand this. Remember, if you are pressed for time to understand and react to a market situation, then its simply not worth the chase. The most luxurious thing market offers is time, use it to your benefit.

FOrex is legal and whatever is legal is offered on NSE platform. Quotes outside this platform are not legal.

you have endless knowledge sir!!

Lol 🙂 Not at all.

uptick in the US economy (or a fear of a crash in commodities) lead to an appreciation in the USD

How are these 2 related?

How does the fear of a crash in commodities lead to appreciation in USD?

Do check this – https://www.thebalance.com/how-the-dollar-impacts-commodity-prices-809294

Hello karthik sir ,

Is Rbi reference Rate of USDINR is the spot price for currency option trading ? which spot price should i follow Rbi rate or the rate shown in investing.com ? kindly guide me .

Its the RBI rate.

Hi Karthik!

Can you recommend a book to get a deeper understanding for currency trading? (As in for options trading you mentioned Option Volatility & Pricing by Sheldon Natenberg)

Thanks

Ah, I\’ve not come across any particular book related to currency trading. I Will let you know if I come across it.

Very Nice informative article.

Thanks I wish i hadnt provided a feedback to make the article better. Please delete my feedback.

Thats ok, I hope you continue to enjoy reading Varsity 🙂

This article needs to be updated. Reference rate publishing and mechanism has changed.

The content is only setting the context to understand what these rates really mean so that the reader can understand whenever they read any news about these rates.

Thx for these modules 🙂

Happy reading!

I just went through the chapters again and I\’m glad I understood the concept. Thanks!

Glad to note that 🙂

Hey Karthik,

Are the exchange rates purely sentimental like the equity markets? So does that mean, the exchange rates change only due to the buying and selling off the currencies in the Forex Market? (It\’s mentioned here that when Brexit happened, there was a massive sell-off of the pound which resulted in the lower price)

Also, I had a few doubts regarding the interest rates and how it affects the exchange rates. In the next chapter, its mentioned exchange rates vary due to the interest rate parity. Its also mentioned that currencies which have higher interest rates are at a discount (according to the Interest Parity Formula). But you have mentioned in this chapter that when interest rates rise, the currency strengthens. How does this work?

So is it the interest rate parity or the sentiments of the players in the Forex Market which eventually affect the exchange rate?

Yes, the sentiments manifest as supply and demand, which has an impact on the exchange rates. I\’ve explained most of the things in the chapter and the subsequent comments, can you please take a look once?

I multiplied 67.0730 to 1.1140 to calculate bid price of EUR INR Pair. Is it right ?

But why? You can directly look at the bid-ask on the exchange right?

I am bit confused about interest rate. In one reply you are saying its the t-bill rate, but in another reply u r saying its repo rate. can u explain please?

They are nearly the same, Sundip. Go with the t-bills, easier to deal and understand.

Sure

Higher inflation leads to strengthening of currency and vice versa.

Sir, I feel this is not correct, because when a country has high inflation foreign investors would move away from investing and will result in outflow of foreign funds, which can actually weaken the currency. I agree that hike in interest iS good for the currency in short term ,but inflation is definitely not good.

Let me review the content again, Bashit.

Thank you so much Karthik.

Just one more suggession/idea/request. Can zerodha plan to have a FLAT brokerage costs per month or per year, especially for Currency segment. This will be quite useful for scalpers. There are some brokers who does that, but not as user friendly and reliable like Zerodha, So if your analysis that business works out good, then it will be win win situation. Please pass it on to Nithin incase you think that is optimum.

The idea is to have a simple broking plan across all segments and all clients, no differentiation whatsoever 🙂

I will bounce this off with the team anyway 🙂

Hi karthik,

Which app like zerodha is best for trading in forex market.

Online stock broker like zerodha.

and what is the brokerage charges ranges for trading in forex.

I don\’t know much about that, Milan.

Hi Karthik,

Thanks for all your patience and interest in answering queries.

USDINR Contract expires at 12:30 PM today for may month. And settlement happens with reference rate which is published at 1:30 PM ( if I am not wrong). so there can be a difference in what we see the last traded price and settlement price right ? and difference can be huge aswell incase we leave it to settlement and cannot squareoff by 12:30 ?

Also can we see in any webpage what is the exact reference rate declared at 1:30 pm today ?

NSE published the reference price on its website. I agree it is an open-ended risk, but from what I\’ve observed the difference is not really much.

Sir,

Interest rate is reduced by RBI to increase the demand in market and loan can be provided to the business at cheapest rate, and reduction in interest rate is also considered good for equity market. But how is reduction(Dovish) in interest rate is weaken for domestic currency in forex market and vice versa for Hawkosh.

Please elaborate to come out this confusion.

Higher interest rate means outside money gets higher yield, hence demand for local currency goes up. Likewise lower interest rate means it drives out the foreign money, hence reducing the demand for local currency.

is forex is legal in india

Yes, as long as you are trading with an exchange trading member and trading the contracts listed on the exchange – https://beta.nseindia.com/market-data/currency-derivatives

Hi Karthik,

Whenever anyone buy or sell more than 1% stock of particular company, then they have to inform exchange, similarly for

1. commodity

2. currency

3. Nifty

4. stock options also futures

if any individual is taking more than 1% order then, that person has to inform exchange ?

Example :

In commodity option orders are less so any one can take more than 1%, similarly in currency open interest is less so anyone can take more than 1%.

please answer.

Thanks,

Santosh

1) There are market-wide restrictions on the number of positions a single trader can carry. Check this – https://www.mcxindia.com/market-operations/trading-survelliance/TS-reports/disclosure-of-top-participants

2) Yes, check this -https://www.nseindia.com/products/content/derivatives/equities/position_limits.htm

3) Yes, check the above

4) Same as above

Hey Karthik,

While I was checking what was the reason for the 1.23% drop today in Nifty, I found out the major reason behind the slump was the Central bank cutting Interest rates. So why did the Indian Markets react so badly to the cut in the Interest Rates. And also why was the S&P 500 down?

🙂

We have our own domestic problems brewing right? LTGC, higher taxation, FPI etc.

On Friday expiry day which rate we will take to confirm option contract is ITM or OTM. Reference rate or future price.

If future price then at 12:30 pm or closing price.

You need to take the reference rate.

Hello,

On thursday there is RBI policy and since recently GDP growth went down RBI is likely to lower the interest rate to push more money in market.Lower interest rate means Domestic currency will weaken. But lower interest rate is good for banking sector(since they can borrow money at lower rate from RBI).so Banknifty is likely to go up. isn\’t it the contrary?

THANKS

Yes, it should work that way in an ideal circumstance 🙂

Karthik, are more modules gonna come out after the 11th module?

And is the content same on the Varsity Website and App?

Similar content on the app, but the app will have a lot more features. Have you checked the app?

Yeah I checked out the app

Its awesome! And specially the quiz zone.

Cheers! Happy learning 🙂

Yeah, ideating on the 11th module. Working on the app for now.

Karthik, we have heard Nithin\’s story when can we hear your\’s?

I don\’t have a story worthy of sharing, Ram 🙂

Are you kidding me, I think your story would be even better than Nithin\’s.

Haha, there are no individual stories, Ram. The story belongs to Zerodha and we play our parts 🙂

Hey Karthik,

The RBI fixes the referance rate on a daily basis, on which parameters do they change it and why do they change the reference rate?

And the Contributing Banks give a two way quote on the INR/USD daily between 11:30 and 12:00, so on which parameters is the two way quote given?

This they do based on their own demand-supply dynamics.

Could you please elaborate?

Let\’s say I\’m a participating bank. On any given day, I will have demand from customers for buying USD and also for selling USD. The customers could be individuals traveling abroad or factories exporting or importing materials. Based on all these demand-supply dynamics, I\’d arrive at a price to buy and sell USD….and this is the same rate I\’d quote during RBI\’s bidding process.

Karthik you are my superhero!!!!!!!!!

No superheroes, Sir….but yeah, Zerodha is the mothership 🙂

They collect bids from the participating banks. I guess this is explained in the initial chapters. Can you kindly check again, please?

Hi,

In the summary, I am pretty sure this statement is not correct:

\”11.Higher inflation leads to strengthening of currency and vice versa.\”

maybe you mean higher interest rates lead to strengthening of a currency

https://www.investopedia.com/ask/answers/022415/how-does-inflation-affect-exchange-rate-between-two-nations.asp

Let me run through this again, Rishika.

This is the bit I am always confused sir. High inflation and banks increasing the rates will result in increased cost of borrowing for firms and increased savings from households. So economy will slowdown eventually. On the other side institutional investors will invest more in the case where interest rates are high. So it\’s definitely not sufficient to say whether the currency appreciates or not

Can you help shed some light on this please

At higher rates, corporate borrowing also slows down, which means lower economic output and therefore more pressure on the economy. Hence more scope for the domestic currency to be under pressure.

Exactly, so higher inflation doesn\’t mean strong ccy if rates don\’t increase. Better interest rate in the context of fixed inflation means stronger ccy. Do you agree sir?

Yup.

1.How much time i can hold a currecy pair ?

2. Is their any conditions about quantity on buying lots?

1) Till the expiry

2) Limits in terms of lots are as below –

SYMBOL, CLIENT_LIMIT in contracts applicable for 01-OCT-2018

EURINR,6839

EURUSD,10000

GBPINR,5000

GBPUSD,10000

JPYINR,2000

USDINR,297241

USDJPY,10000

If one buys Euro-usd pair , he looks at the ask price . And while sellkng the pair one looks at the bid price ..

why so .. bid means the buy and ask -sell ? Why the opposite

Because the bid-ask is from the country party perspective.

There are two Interest Rates

One is Repe rate (Lending rate for banks ) and the T-Bill Rate (for the investment purpose) . What interest rate are you talking about when explaining thins above ?

Repo and Reverse repo rate are what I\’m referring to here.

1. Does contributing banks means that they participate in forex market or they have their bank listed in forex market?

2. why RBI polls out only USD/INR rates except EUR/USD, GBP/USD and USD/JPY rates from contributing banks?

3. why does they compute crossing if they can directly get the detail ofother pair from contibuting banks?

1) Contributing banks also participate in Forex markets.

2) Only USD?INR as far as I know

3) I\’m not sure about this, Ayush.

What\’s the currency trading time?. Isn\’t 24 hours. In India 9 to 5?

It is between 9 AM to 5 PM for all currencies with INR as the quoted currency. It will be 9:00 AM to 7:30 AM for cross currencies with USD as base currency – https://www.nseindia.com/content/circulars/CD37022.pdf

did you mean 9am to 7.30PM?

Ah, yes, 7:30 PM 🙂

Hi,

As , FED increased interest rates in US by 0.25% then this should strengthen USD right and if yes , then why USDINR went down?

The exit polls of Gujarat sate assembly indicates BJP will make a clean win, which implies the voter sentiment may not have changed for the next year Lok Sabha elections. Which market participants believe is good for the economy and the currency.

The interest rate of RBI referred in above paragraph is the rate which account holder gets by depositing money Right? Or is it the repo rate which had been discussed.

It\’s the risk-free rate one would enjoy if he were to invest in a RBI\’s t-bill instrument.

Can we get eventwise impact on currency in tubular presentation ? It will surely help to understand and quick decision making .

Thanks, Karthik

Will have to prepare one, Manish 🙂

What about the opening price of rupee we see daily on news at 9 am. Is it future price or spot price

I\’m not sure which TV, Rakesh. I\’m guessing, the folks on TV would mention this anyway 🙂

Why does the rbi increase the interest rate during inflation it should decrease the inflation instead so that there is enough money floating in the market

If RBI sets the currency rate by consulting selected banks and the average is selected as the currency rate then how does the currency rate keep on fluctuating every second?

RBI sets the reference rate. The rate that fluctuates is the currency futures.

Sir, slightly confused. Rbi sets the rate once a day but provider like centrum change it every second. Why ?

RBI\’s reference rate is fixed once, and its like the SPOT price. The rate displayed by forex guys are based on demand and supply in the market, it will hover ard the RBI\’s reference rate.

Exactly, so the rate that providers quote is not futures rate. It\’s spot rate. Do you agree sir ?

Yes.

How can I search EURO USD pair in zerodha

Euro USD is not available on exchanges, so you will not find it on Zerodha or for that matter any broker.

Hey Karthik, thanks a ton for valuable info.

You said when we import we sell INR and buy USD which creates demand of USD and strengthen it.

And when we export, we get USD and convert it to INR. Which means if we bought from country XYZ, they bought USD with their currency and paid us, which again increases demand of USD and strengthen it.

So doesn\’t it make USD kind of invincible currency which is always in demand? Or am I missing something?

There is no denying, as we stand today USD is a pretty strong currency 🙂

Sir, I m confused about relation b/w

1. GDP and Interest rate

2. GDP and currency

3. Interest rate and currency

Above it is explained that Higher GDP means more confidence = stronger domestic currency

Higher interest rate = More foreign investment = stronger domestic currency

But confusion comes with Interest rate vs GDP on currency.

Isn\’t it higher interest rate= low GDP or vice versa.

Which leads to opposite conclusion i.e. higher interest rate = weaker domestic currency due to low GDP

Not really. Frankly these variables share a complex relationship. Think about it – higher interest rate tends to attract higher foreign investments which is in turn good for GDP…leading to stronger domestic currency. However, it also depends on how the markets perceive interest rate, while the monetary authority may look at it as a stable rate, markets may have an opposite view. This is where the complexity arises.

sir i m a bit confused , pls correct me-

increase in interest is a BEARISH sentiment for STOCK MARKET as corporates will get fund on higher interest ; Whearas BULLISH sentiment for CURRENCY market as Foreign investors invest in indian market creating demand for INR .

pls correct me if my view is wrong.

Yes, hence it is tough balance to strike.

Hi !

When we compare forex vs stocks, with my limited knowledge, I came to this conclusion that

apart from having high liquidity, round the clock trading hours and no stt, forex is less lucrative compared to stock trading. Please correct me if I am wrong.

Well, everything takes a backseat, as long as you know which direction to bet on 🙂

Sir, in the above calculation of \”Ask\” price for EUR INR you have multiplied \”Ask\” price of EUR USD with \”Bid\” price of USD INR. Should it not be the multiplication of \”Ask\” price of both EUR USD & USD INR ?

Tushar – you have a sharp eye 🙂

Thanks for pointing this, I made the correction.

Thanks to you sir for making available such valuable knowledge in its simplest form.

Pleasure is ours, happy reading!

Nitin Ji, Being new to forex I want to know the following:

1. If I buy 1lot(1000) USD/INR for december 16 future at 67.5 and when price falls to 67 on that same day , then will I be able to square off on that day or i would have to hold it for last settlement day

2.If USD/INR rises to 68 it means I am incurring loss and If it falls to 67 it means I am incurring profit ? Plz correct me on that

1) You can square off the same day, no need to hold to expiry.

2) If you are long, you will make a profit if the price increases and make a loss if the prices fall.

Will it be possible to show the USD or JPY current exchange rates with INR in trading terminal itself?

You mean the spot rates? I\’m not sure if this is possible, however, let me confirm this again for you.

How to trade EUR USD?

When it will be available in Zerodha?

RBI has given the approval, not sure when the exchanges will take it live. Moment its on the exchange, it will be available with us.

Hi Karthik

What exactly is interest rate? Is it lending rate (loans) or borrowing (deposits) rate or both?

What I understood from this is that FII\’s are attracted towards high interest rate…obviously that would mean high returns on their investment/deposits right?

Now why would RBI increase interest rate (read as deposit rate) if inflation is high? So that people could deposit money in bank instead of spending on commodity leading to inflation? Am I right?

My understanding is this…please please correct me if I am wrong.

More Inflation = Increase in interest rate = Increase in FII = strengthening of economy = Bull market

So basically inflation is good for market makes my head go dizzy. Please explain

Interest rate is a regulator knob of your ceiling fan. Higher the interest rate, lower is the circulation of money in the economy…afterall, who wants to borrow at higher rate?

So when inflation is high, central banks try to curb the supply of money by tightening the supply of money….and the way to do this is by maintaining higher interest rates in the economy.

Yes, once interest rates are high, deposits tends to give higher yeilds…but this may not be very good for the markets right? Why would you want to move away from a high yielding FD to a risky asset like equity?

Hi karthik, a small doubt

today the reference rate of USD/INR is 66.8804. and in spot market USD/INR is 67.07.

now my doubt is what is the exact use of this reference rate (is this ref rate is only useful for calculating cross currencies OR there is any other use).???

please kindly clear my doubt.

Thanks&Regards

Reference rate is updated once a day at the end of the day. Ref rate is the one based on which the futures market works. Btw, USD/INR of 67.07 is the futures rate and not really the spot.

Hai sir how can we calculate trend side up or down and find the future.. crude oil..in day

Check out the ADX indicator – http://zerodha.com/varsity/chapter/supplementary-notes-1/

BID PRICE OF EURINR IS 74.6801 RIGHT?

Yup!

Hi is there any method to separate the boring candle in the chart by separate color in candle stick pattern…

No 🙂

Sir, when can I expect updates on commodity markets? Eagerly awaiting!!!

We are working on it Manoj…few chapters on currencies and then we move to commodities.

Oki Sir, Thank you!!

Welcome!

Namaste to u market GURU.!

Namaste to markets, the ultimate Guru!

Hello Sir,

I have a general doubt. Are the financial instruments same in india and other global markets? If not what additional knowledge do we need to aquire. I\’m interested in US markets.

The basic functioning of the futures instrument would be the same, but logistics (expiry, lot size etc) would change.

what is Repo Rate n Reverse Repo Rate? is it related to currencies anywhere?

Repo and Reverse repo are the key outcomes of the monetary policy, and yes it does have an impact on the currency. Read more about these events here – http://zerodha.com/varsity/chapter/key-events-and-their-impact-on-markets/

as per my calculation Bid price of EURINR 74.6790782

Yup!

can u plz explain?