11.1 – Mapping companies

I’m hoping that the previous chapter gave you some insight into the current situation of the crude oil fundamentals. Some of you may also be interested in learning how crude oil is extracted from the ground and supplied to various stakeholders such as the refineries. The ‘Oil and Gas videos’ channel on YouTube, has done a stellar job in putting up short animated videos on this topic. If not all the videos, I’d encourage you to at least watch this one.

This animated video gives a beautiful, high-level understanding of how oil is extracted from the ground and ocean beds. You will also understand what ‘oil rigs’ are in this video. They are those important pad-like things, floating in the ocean, with flames spewing out of the exhaust. Companies such as Aban Offshore, Selan Exploration, Cairn India etc., are involved in setting this infrastructure up. I know a lot of traders and even investors investing in these asset-heavy companies, without knowing the operational core of such companies. I think this is not a great idea; one should always know what they are dealing with. Given this, and the relevance of crude oil on many listed companies, I would like to discuss how the oil industry is structured briefly.

11.2 – Upstream, Downstream, and Midstream

A note of warning here – I’m no oil and gas expert; my knowledge is limited to just the basics. As a crude oil trader, I do think it is essential to know the industry dynamics simply because the trading opportunities may not always be presented to you directly. For example, there could be some fundamental change brewing in crude oil, it may not manifest into a trade-in crude oil now, but instead, a trade opportunity may come about in the downstream companies. For you to benefit from this, it becomes imperative to know the layout of the industry and identify areas of opportunity. My objective here is to familiarise you with the industry layout and help you map companies and how they fit into the overall oil and gas ecosystem.

So let us get started.

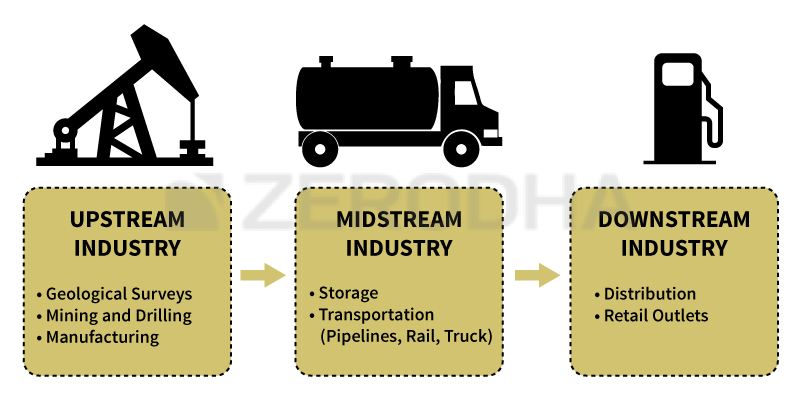

The oil and gas industry can be segregated into three sections –

- The upstream industry

- The downstream industry

- The midstream industry

Let us briefly discuss each one of them starting from the upstream companies.

Upstream companies

The upstream companies are the ones that do the dirty work – they take on geological surveys, dig up bore wells to get a sense of what’s in the ground underneath, and if they find oil reserves, they then begin the drilling and extraction of crude oil. It takes many years for upstream companies to identify an asset (potential oil well) and convert it into a fully functional, profitable oil well. Upstream companies manufacture and store crude oil in barrels (millions of barrels are produced every day). These companies do R&D and engineering and are asset-heavy. Therefore, they end up spending a lot of money (read as capital expenditure) to extract oil.

However, the price at which they can sell this oil in the open market is not really in their control. The price is determined by the markets in which market participants like you and I participate and influence the international oil price. Every upstream company has a breakeven point – defined as the cost of producing one barrel of oil. The breakeven point is also referred to as the ‘full-cycle cost’. Naturally, these companies would strive hard to keep their costs low and bring down the full-cycle cost.

Companies such as ONGC, Carin India, Reliance Industries, Oil India are some of the Indian upstream companies. Internationally, companies such as Shell, BP, Chevron etc., fall in this category.

The key point to note here is that low oil prices do not really favour upstream companies in general, especially the ones which have high economies of scale (the ones which have high full cost cycle). Obviously, the higher oil price is good for these companies as their efforts to extract oil remain the same, but margins improve drastically.

Downstream companies

We will talk about the downstream industry first and then discuss the midstream industry. Generally speaking, the job of the upstream companies ends at producing crude oil. ‘Crude oil’ as you realize is produced in its raw form. If we have to use it as petrol or diesel, then the crude oil has to be refined. This is where the downstream industry comes into the picture. These companies purchase the crude oil from upstream companies and refine the crude oil to various forms such as – petrol, diesel, aviation fuel, marine oil, kerosene, lubricants, waxes, asphalt, liquefied petroleum gas etc.,

Companies in this sector also go the extent of distributing these products across the value chain, right from business to business (B2B distribution) to business to consumer (B2C) distribution. In fact, petrol bunks are a good example of this phenomenon. Petrol bunks are nothing but a retail outlet, retailing petroleum products and owned by downstream companies.

Good examples of downstream companies in the Indian context are – BPCL, HPCL, IOC etc. Some companies try and integrate and operate across the value chain, i.e., they try and do both upstream and downstream operations. Companies that successfully combine these operations are often referred to as the ‘Super Major’. A classic example of this is the US-based ‘Exxon Mobil Corp’. They produce close to 4 million oil barrels per day and operate around 40 oil refineries across 21 countries. An operation of this scale is mammoth management and operational undertaking; not everybody’s cup of tea.

So, if the oil prices cool off, then it implies that the downstream companies can buy oil at lower prices from the upstream company (which is not so good for upstream boys as their efforts to produce oil is still the same). However, the benefit of lower oil price is not passed on to the end-user, i.e. you and me, but in developed countries like US and UK, this benefit is passed on to the end-users quite quickly.

Anyway, here is what you need to remember at this stage –

- Upstream and downstream companies share a see-saw relationship.

- Low oil prices are bad for the upstream boys but suitable for the downstream fellows.

- Higher oil price is right for upstream fellows but bad for downstream boys.

So the next time you see oil prices going down, don’t be in a hurry to short ONGC or BPCL. Take a minute to understand whether the company is a downstream or upstream company, and analyse the impact of oil prices on the company.

Midstream companies

We will quickly discuss the midstream companies before looking into other aspects.

In very loose terms, midstream companies are the ones act as a courier between the upstream and downstream companies. They are responsible for the transport of oil from the oil well to the refineries. They do this via pipelines, road transportation (oil takers), and by ocean shipments. Consider them as the wholesalers of crude oil. Some midstream companies try to deliver more on the value chain by refining the crude oil to some extent. Hence their operations sometimes overlap with downstream companies. Since midstream companies deal with both up and downstream companies, they are caught in the middle, they neither want oil prices to increase or decrease, but seek stability in oil prices. If oil price decreases, then upstream companies are affected, this is not good for them. Likewise, if the prices increase downstream companies are affected, this is again not so great for them.

Some of the top players in this segment are TransCanada, Spectra Energy, Willams and Company etc.

Here is a snapshot which gives you a quick overview of all the three industries –

11.2 – Difference between WTI Crude and Brent

Many people tend to speak about ‘Crude Oil’ as if it is a single uniform entity, something like Gold. However, this is not true. Did you know there are many varieties of crude oil that can be extracted from the ground below? The difference comes in mainly from the geographic variation and its unique characteristics. The impact of geography is so much that the characteristics of crude oil, right from thickness, color (light yellow, golden yellow, deep black), viscosity, sulfur content, volatility etc., change drastically.

Given this, naturally, there are many different types of Crude oil. I’ll not get into details, not that I don’t want to; it’s simply because I don’t know them myself 🙂 . I know the fundamental difference between to West Texas Intermediate (WTI) and Brent Blend, which is what matters to most of the crude oil traders and hence we will stick to it.

Before we get into the difference between the two, let us touch upon two distinct characteristics of crude oil, which define the variation of crude.

API Gravity – API here stands for ‘American Petroleum Institute’, which is essentially a metric to compare the lightness of crude oil with that of water. If the ‘API Gravity’ of a particular variety of oil is higher than 10, it merely indicates that the oil is lighter than water. Therefore the oil can float on water. API gravity less than 10 means that the oil is heavier than water; hence the oil will sink in water.

Sweetness – Crude oil of any form will naturally contain sulfur. The lesser the content (I was told sub 0.5%) the ‘sweeter’ the oil is considered. Higher the content of sulfur, then the oil is not considered ‘not so sweet’.

The difference between WTI and Brent mainly comes from the API Gravity and its sweetness.

West Texas Intermediate (WTI) – This is considered a very superior quality of crude; hence the final refined products are also meant to be of superior quality. The API gravity is 39.6 (recall higher than 10, then it’s lighter than water); therefore, WTI is considered super light. Further, the sulfur content is just 0.26 per cent, making it a lovely crude oil.

Brent Blend – Much like blended scotch, crude oil can also be blended to create variants with certain properties. Apparently, the Brent blend is created by blending oil from over 15 oil wells. Brent has a sulfur content of 0.37%, which makes it sweet, but not as sweet as WTI. The API gravity is around 38.06, which makes Brent quite ‘light’.

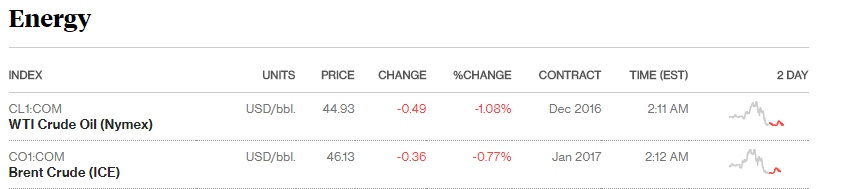

Clearly, due to the variation in the characteristics, the two are traded at different prices. Have a look at the price quote for these two variants –

Source: Bloomberg

Most importantly, you need to know that crude oil traded on MCX follows the WTI and not Brent crude.

By the way, you may also be interested to note, that Brent Crude has an optional delivery meaning, upon the derivative contract expiry, you can choose to either physically settle or cash settle the contract. WTI on other hand is physically settled. Probably this explains why Brent crude is priced higher compared to WTI

11.3 – Crude oil inventory levels

Supply-demand effects crude oil prices and therefore, the profitability of many companies linked at various points in the oil and gas ecosystem. This makes tracking the inventory levels of crude oil prices important on several counts. You can use this information to trade not just crude at MCX, but also set up trades on companies such as BPCL, HPCL, IOC, ONGC etc.

There are two organizations that put out the inventory details –

- US Energy Information Administration (US EIA) – They report the inventory levels every week. You can track the information here. Remember, inventories tend to increase when the demand is low, or there is an oversupply, either which way, it isn’t good for oil prices, and hence the upstream companies. Likewise, lower inventories mean either there is a lot of demand, or there is a production cut, both ways it’s good for crude prices and upstream companies.

- OECD Crude Oil inventory – OECD stands for ‘Organization of Economic Co-operation and Development’. OECD also gives out crude oil inventory (but not at a weekly forecast like EIA). You can track the inventory position on OECD’s website.

11.4 – The relationship between the US Dollar and Crude Oil

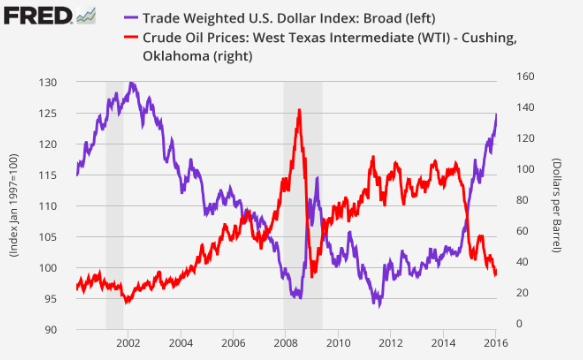

The crude oil and US Dollar share an inverse relationship. A strengthening US Dollar tends to drive the price of crude oil down. Likewise, weakening USD tends to drive the prices of crude oil higher. At this point, it is essential to note that both these assets have their own supply-demand dynamics influencing their price movement; however, they are also somewhat linked to one another.

If you do an image search for ‘Crude Oil versus Dollar’, you will find many charts which display this inverse relationship. Here is one for example –

The interesting thing to note here is, the dollar used in these charts is not the “USD Dollar Spot” but instead the ‘Dollar index’, which is a representation of dollar against major world currencies. This makes absolute sense as crude oil is an international currency priced in dollars, therefore irrespective of who is buying crude oil, payments happen in US dollars.

Given this, if the Dollar increases (for whatever reasons), then countries tend to purchase more oil for the same level of the dollar (more oil can be purchased for the same dollar level). This leads to quicker depletion of inventory levels, therefore the price of oil increases.

The argument above is generally true over long time periods. However, please do remember that both these assets have their own fundamental dynamics playing. So there could be instances where both of them may break their inverse correlation and head in the same direction.

Also, remember the inverse correlation only suggests that the two assets move in the opposite direction but does not say anything in magnitude. So, for example, if the dollar declines 10%, this does not imply that the Crude oil will increase by 10%.

In the next chapter, we will discuss the contract specification of Crude oil on MCX.

Key takeaways from this chapter

- It is important to understand the Oil & Gas ecosystem and map how companies are mapped under this ecosystem.

- Upstream companies are asset-heavy and are involved in extracting oil from the ground.

- Increase in oil price is good for upstream companies, while a decrease is not.

- Downstream companies mainly consist of refineries. Higher oil price is not good for them while lower oil prices are good (as their margins tend to increase).

- Midstream companies are involved in oil and gas logistics. They prefer stability in oil prices as they do business with both upstream and downstream companies.

- WTI and Brent are two variants of crude oil varying mostly in terms of API gravity and sweetness.

- Brent Crude is the international benchmark.

- Keeping track of inventory levels is critical. Increase in inventory tends to decrease the crude oil price, and drop inventory tends to increase the prices of crude oil.

- The USD index and crude oil share an inverse correlation over longer periods. However, this relationship may break over short time frames owing to their own supply-demand dynamics.

Very well written, reading in Oct 2024. Thanks for this chapter

Thanks Raju, I hope you continue to enjoy learning on Varsity.

THANK YOU

Happy learning, Vick!

Very well explained, all doubts clear

Hello,

Good day !!

as i am varsity reader, i am just little bit confused in this line mentioned below. I have download this module pfd and also i cross check with crude oil chapter 11 on web there is something mismatch in the same line

on webpage showing this line

\”Most importantly, you need to know that crude oil traded on MCX follows the WTI and not Brent crude.\”

in the PDF showing this line

\” Most importantly, you need to know that crude oil traded on MCX follows the Brent crude and not WTI. \”

which to consider !!!

thanks

Sorry about this, its the WTI Crude, Vick.

11.4 – The relationship between the US Dollar and Crude Oil

Given this, if the Dollar increases (for whatever reasons), then countries tend to purchase more oil for the same level of the dollar (more oil can be purchased for the same dollar level). This leads to quicker depletion of inventory levels, therefore the price of oil increases.

In the above paragraph, shouldn\’t it be : the Dollar decreases, instead of increases??

I mean $ is strengthening here Dhaval.

Thank you, sir. Understood now.

Sure, happy learning!

Dear Karthik Sir,

I have one doubt. Please clarify.

1. Upstream companies are asset-heavy and are involved in extracting oil from the ground. An increase in oil price is good for upstream companies, while a decrease is not.

2. Downstream companies mainly consist of refineries. Higher oil price is not good for them while lower oil prices are good (as their margins tend to increase).

Do you mean the final refined oil price in the above two cases? Or, the refined oil price in the first case and the crude oil price in the second case?

—

Regards,

Sanjay

Crude oil in both cases, Sanjay.

i am just a little confused on this if dollar and crude oil prices are inversely proportionate. should the following statement mentioned above mean, if the dollar decreases instead of increases.

Given this, if the Dollar increases (for whatever reasons), then countries tend to purchase more oil for the same level of the dollar (more oil can be purchased for the same dollar level). This leads to quicker depletion of inventory therefore the price of oil increases.

Avina, I\’m not sure if I get your query fully. Can you kindly elaborate?

With reference to above – Should it be \”if the dollar decreases…..\”?

Hi Karthik, I was not able to understand this clearly – \”Given this, if the Dollar increases (for whatever reasons), then countries tend to purchase more oil for the same level of the dollar (more oil can be purchased for the same dollar level). \”

If dollar appreciates, doesn\’t that mean countries that import oil will get less oil for the same level of dollar that they used to pay earlier?

Yes, its like a mirror image for importers and exporters.

Okay. One more question – what does take delivery mean? is it like the barrels will be delivered to your location or something? (might sound like a naive thought, but I can\’t think better, haha). I wonder if anyone really does this

Yeah, something like that. In this context, it will be delivered to a warehouse and you will get a warehouse receipt.

Hi Karthik,

\”Brent Crude has an optional delivery meaning, upon the derivative contract expiry, you can choose to either physically settle or cash settle the contract. WTI on other hand is physically settled. Probably this explains why Brent crude is priced higher compared to WTI\”

I was not able to understand why this fact leads to a higher price for Brent crude?

You can choose what to do upon expiry, either settle physically or take delivery. Traders love this option as they can take better control over their trading decision. This option comes at a cost, Pradeep.

Hi Kartik

U gave this statement

Given this, if the Dollar increases (for whatever reasons), then countries tend to purchase more oil for the same level of the dollar (more oil can be purchased for the same dollar level). This leads to quicker depletion of inventory levels, therefore the price of oil increases.

But it should be inverse right as per inverse relationship of dollar and oil

I think its a typo, it should be \’decrease\’.

thanks lot

In the earlier chapters you showed a chart taht showed the relation between Gold prices and Dollar that was inverse …

Thus Gold and dollar are inversely related Crude and dollar are inversely related so is it conclusive that Gold and Crude share a positive correlation

In the earlier chapters you showed a chart taht showed the relation between Gold prices and Dollar that was inverse …

Thus Gold and dollar are inversely related Crude and dollar are inversely related so is it conclusive that Gold and Crude share a positive correlation

Yup, they do.

Sir, It\’s Great that we can literally invest all of the asset classes using just a single zerodha Account However i have a little doubt that can we invest in Gsecs and Debentures using zerodha

Yes, you can. I\’d suggest you call the customer support desk for this and they will guide you.

Thanks. Please do consider fixing that ASAP. This page is the first result when you research that, and it\’s very misleading if it\’s wrong.

https://i.imgur.com/JmdVhG4.png

Varun, thanks for pointing that out. Made the change on the web, will do the same on the app as well.

Hi Karthik,

I have 2 questions.

1. In this chapter, you said that WTI is of superior quality than Brent (super light and sweeter). So why it is cheaper than Brent?

2. You said that MCX CRUDE OIL is Brent instead of WTI.

I tried to run a small test on tradingview.com. As you can see: Blue line = US WTI OIL price in INR, Purple line = US BRENT OIL price in INR, and Yellow line = MCX CRUDEOIL price in INR

So why does MCX CRUDEOIL line overlaps WTI instead of Brent?

https://s3.tradingview.com/snapshots/k/kikEOzAz.png

1) Could be a simple function of demand.

2) Its WTI, not brent. I need to correct that typo.

The relationship between USD and CL is not a consistent one. In the last five/six years the correlation coefficient fluctuated up & down between (+) 0.75 to (-) 0.89. There are four peaks and four troughs during this period. So, it\’s difficult to trust this relationship while taking a position. From June 2021 onwards they are moving in tandem with varying levels of positive correlation.

Just contributing a few minor points that I have learnt.

That helps! I\’ve not tracked the correlations in a while now. Thanks for chipping in 🙂

If you consider the (i) freight charges plus the (ii) time taken to transfer

to transport to CL several countries in Asia or Europe you would find that they are almost equal.

There is an exchange traded product called ARB, representing the difference between Brent and CL.

Responding five years & 3 months later 🙂

CL = WTI.

Thanks for the input 🙂

Sir, in the crude oil vs dollar segment,

it is given that if dollar price INCREASES, then more crude oil can be brought it leads depletion of investory therefore prices of oil INCREASES

but sir how could both increase since there is a inverse relationship know?

The inverse relation is because of this.

Thank you, it was very much informative to me.

Happy learning, Rafi!

given this, if the dollar increases (for whatever reasons), then countries tend to purchase more oil for the same level of the dollar (more oil can be purchased for the same dollar level). this leads to quicker depletion of inventory levels, therefore the price of oil increases.

This paragraph is wrong as when dollar is getting stronger then I will have to pay more for the same quantity of oil, so I will purchase less, which in turn will increase the inventory hence pushing the oil prices down.

Thats right, Anuj. It should be the other way round…i.e. when the Dollar weakens and the local currency strengthens.

Sir, why is there an inverse relation between USD and crude? Any particular fundamental reason to it?

I\’m a bit confused with this as you also mentioned \”if the Dollar increases (for whatever reasons), then countries tend to purchase more oil for the same level of the dollar (more oil can be purchased for the same dollar level). This leads to quicker depletion of inventory levels, therefore the price of oil increases.\”

Then how come the inverse relation?

Increase in Dollar means, the local currency goes down. Thats what I mean.

Sir, Does MCX still follow Brent to be the benchmark for crude prices in India?

As mentioned in the article below, it states that MCX follows WTI crude oil:

https://gcc.geojit.net/geodata/Dec2008/Dec2008Page11.html

It would be great if you could kindly confirm on this.

Thanks!!

Thats right, Jithin.

#1: Why Brent Blend is more expensive than WTI Oil? I may be wrong but I think high API gravity and high sweetness are desired qualities which WTI possess. So shouldn\’t WTI be more expensive?

#2: > Given this, if the Dollar increases (for whatever reasons), then countries tend to purchase more oil for the same level of dollar (more oil can be purchased for the same dollar level). This leads to quicker depletion of inventory levels, therefore the price of oil increases.

This means if the Dollar increases, oil price also increases. Earlier you said it\’s an inverse relation. So which one is true?

1) I suppose this is a function of both demand and quality

2) More buying power does not mean more demand right?

Hi Karthik sir, i guess you have mistakedly typed that Brent is the benchmark for crude in MCX. The benmark is WTI as per the contract note

\”Light Sweet Crude Oil confirming to the following quality

specification:

Sulfur 0.42% by weight or less,

API Gravity: Between 37 degree – 42 degree\”

is the quality specification and it is the quality of NYMEX WTI. More the NYMEX CL is WTI itself as far as my knowledge is .Kindly look into this.

Its a great pleasure reading through your content.

Regards Hariprasad K

Thanks for pointing, I will look into this again 🙂

Sir Today 18 April,2020

Brent – $28 (+3%)

Wti – $18 (-9%)

So according to the write-up

Crudeoil Should be (+3%) but it\’s showing (-9%)

So is MCX not following Brent Price?

India has a blended mix actually, but yeah follows Brent largely.

Sir mcx following wti

Hello,

In the comparison of usd and crude oil price,it is written that if dollar increases then crude oil price will also increase.what is the meaning of Dollar increases? If it means that Dollar strengthens then it should have positive correlation .

THANKS

Yes, $ increase means that the Rupee weakens…which means the USD INR pair value goes up.

how crudeoilM margins calculate during buy / sell ?

The margins are calculated based on SPAN calculations, Sreepathi.

Is it required to take physical delivery of crude oil or metals ? Or will it be settled in money?

Cash-settled, Ashwin.

Hello Sir,

Are you sure that the oil traded in MCX is Wti? Because in MCX website it says that

\”Due date rate shall be the settlement price, in India rupees, of the New York Mercantile Exchange’s(NYMEX) \”

And NYMEX follows WTI crude.

Kindly confirm. Would be helpful

Thanks in advance.

**Are you sure its Brent in mcx?

Yes, MCX follows NYMEX. Let me look into this and make the correction if required. Thanks.

As quoted in this chapter \”\”\”Given this, if the Dollar increases (for whatever reasons), then countries tend to purchase more oil for the same level of dollar (more oil can be purchased for the same dollar level). This leads to quicker depletion of inventory levels, therefore the price of oil increases.\”\”\”

My qn is dollar increases means dollar is weakening against other currency??

Yes, essentially this is the weakening of the Dollar against another currency.

Dear Sir,

I still have a doubt as i checked up on MCX Site, in the pdf there is a due date rate- which specifies taking NYMEX and RBI rate. So, on NYMEX it is WTI Crude Oil and thats why i am confused , maybe future instruments on MCX – CrudeOil and CrudeOil M follows WTI instead of Brent Oil ?

link 2018 contracts

https://www.mcxindia.com/docs/default-source/default-document-library/crude-oil-august-2018-contract-onwards.pdf?sfvrsn=0

As far I\’m aware its Brent. But I will double this again. Thanks.

Yes sir , do check to clear the confusion.

Yup, will do.

Sir one more question I want to ask.

Will the crude oil price on mcx remain same or move up , If crude price is stable at 66$ but USD is getting stronger against rupee.

Yes, stable crude prices will help the domestic currency.

Sir thank you for this information.

I want to know how to do technical analysis for crude oil. I am unable to find the methods specific to crude oil.

Is it the same as equities? I mean same indicators, signals and levels?

The same TA techniques that are applicable to Equities are applicable to Commodities as well. No change at all.

As long as its intraday its ok. Yes, liquidity increases in the next month\’s contract as we approach expiry.

Thank you so much

Damn bingo

Cheers!

Respected Sir,

As per the chapter, MCX follows Brent & it is international standard for oil price. This means when we say crude oil, we actually mean Brent Crude oil, right? But, as per my research work, I am getting flaws in my model when taking Brent crude price. Results are better when I take WTI prices.

1) Does MCX really follow Brent? If yes, there may be error in my model. 🙁 If no, please correct the typo.

2) Which crude oil price is standard for international oil price?

3) When we say crude oil (a. nationally, b. internationally), which type are we referring to (in both case)?

4) Which exchange is official/standard exchange for a. Brent (i guess UK branch of ICE) b. WTI (I guess NYSE for WTI) ??

Please clarify all.

Thanks & Regards

james

1) MCX has both Brent and WTI. India imports Brent so for any sort of fundamental analysis on BPCL, HPCL, ONGC etc, you are better off taking Brent. However, the world markets refer to WTI

2) WTI

3) WTI

4) CME for both I suppose.

Thanks, Thanks a lot Sir, it made many tiny details clear. Really, no one clarifies doubts better than you.

Regards

James

Happy learning, James!

HELLO SIR,

IN KEY TAKEAWAYS #8, YOU HAVE TOLD THAT INCREASE IN INVENTORY, PRICE DECREASES AND DECREASE IN INVENTORY PRICE INCREASES, BUT I HAVE BACKTESTED IT(FROM AROUND PREVIOUS 4 MONTHS) AND FOUND THAT 70 TO 80% OF POSITIVE INVENTORY DECREASED PRICE OF CRUDE AND NEGATIVE INVENTORY INCREASED THE PRICE. SO I REQUEST YOU TO PLEASE EXPLAIN SOMETHING ABOUT THIS IF POSSIBLE.

Maybe you should share the backtesting results and tell us what you\’ve noticed :;)

sir according to the example you gave above for the dollar and crude oil relationship then it should positive correlation between crude oil and dollar

They share an inverse relation, hence a -ve correlation.

how to check inventory immediately at 8 pm in wednesday ?

Not sure about this. I guess we will have to wait for the inventory data to be relayed across.

Banibrata go to forex factory website and look for news(event) calender. every wensday invotery resulst come and update same time 8pm in this size.

happy trading

Karthik, you guys are doing awesome job.

I am new to trading and i think this the best platform for beginner like me to learn about markets.

Is there any fundamentals that will affect the price of commodity? While i notice TA works only 40% to 50% of trades and lots of whipsaws.

Thanks for the kind words 🙂

Yes, fundamentals do affect commodities, however, since most of the trades on commodities are short term, tracking fundamentals may not help much. But yeah, good to be aware of whats generally happening on the fundamentals side.

Can you please suggest some books, periodicals, newsletters which a commodity trader should read?

There arent any good ones that I;ve come across. However, I do glance through Hindu Businessline\’s commodity section. I find it quite useful.

Does the crude prices on MCX really follow the Brent prices?doesnt MCX have a Brent crude future which is hardly traded….great tutorials btw…..have been learning a lot thru varsity….keep up the good work

The contract on Brent is no longer active on MCX. The crude prices on MCX is the Crude prices on NYMEX.

Hi Karthik,

I have a question, suppose I am trading only in one metal or say crude oil multiple times a day or say 3 times a day, (like a scalper) buying- selling, buying -selling , at the end of the day will the points made be averaged out or i will get the total points?, I mean as an eg. if for the first trade, i buy at 10 and sell it at 20 and then second time I sell it at 20 and buy it at 14, and for the third time, I buy it at 10 and sell it at 17, will the total point be 10+6+7=23 (not counting brokerage here), or the price would be taken as an average of three trades?

Thank you,

Saurabh

It is based on individual trade. However, it will also show up as a weighted average, which leads to the same answer anyway.

Thank you Karthik

Welcome!

Sir, on 30 th Nov I made a bullish opec bet on crude oil and gains good profit. Thanks for your teaching.

Happy to know that 🙂

Good luck and stay profitable!

Is it okay to say inverse relationship b/w upstream and downstream companies share price ? If bpcl or hpcl increases ,ONGC should go down . But last 1 year data says both companies share price effectively gone up.

last 1 year :

ONGC 235 -> 287

HPCL 282 ->481

Its hard to arrive at that conclusion for various reasons which includes the involvement of the government.

If crude oil price increase internationally. Does that means ONGC or Cairn India Indian upstream companies will also sell at higher price to Indian down stream companies ? What I want to know is that oil prices is determined internationally only or domestic angle could be their ? some thing like involvement of govt. as after all ONGC and BPCL both are govt. companies .

There are several layers here – if the oil prices increase, then upstream companies can sell them at higher prices. Therefore, their margins increase. Downstream companies have to buy it higher prices…internationally this increase in price is directly passed on to end customers. However, in India petroleum prices are regulated by the govt, hence customers are kind of insulated to these shocks….but not entirely. Another angle to note here is that increase in oil prices will increase Govt\’s import bills..and this tends to increase the fiscal deficit.

if WTI is Superior quality oil then why its trading at low price compare to Brent?

Remember, the price of commodities like everything else, is a function of demand and supply.

it\’s a great job sir

Thanks!

Sir I just read option module. last comments there were from 2015 so i thought of asking a doubt here. Can you please explain the drop in premium of put calls.

– ashok leyland otm puts will expire after 30 days, underlying price moved down. then why did some premium fall. was that because of drop in volatility. if that is so, then why there was increase in premium around(both for more and less strike) and only that premium fall particularly? can I attach a photo of option chain here?

Mukhul, I respond to queries everyday based on where it appears. Nothing else apart from Volatility and liquidity can explain this. I\’d suspect its because of drop in both.

Very well and concise information about Crude Oil. Eagerly waiting for next chapter on Crude Oil Trading.

Will try and put this up soon.