7.1 – Orientation

As you know, there are two commodity exchanges in India – Multi Commodity Exchange (MCX) and National Commodity and Derivative Exchange (NCDEX). MCX is particularly popular for the Metals and Energy commodities while NCDEX for all the agri commodities. However, there is a lot of activity picking up on MCX for agri commodities as well. My job over the next few chapters is to discuss these commodities which are traded on the exchanges and get you familiar with the commodity contracts.

We will look into every commodity that is actively traded on the commodity exchanges. The idea is to know how the commodity contract works (contract specification), figure out which contract to trade and identify the factor which influences the commodity. I will skip the usual background to commodities market part, the one which talks about the history, forwards markets, the farmers in the US, the Chicago Mercantile Exchange etc. You will find this in almost any material on the Commodity market. I want to get straight to the heart of the topic by slicing and dicing the contract specifications of commodities and other details around them.

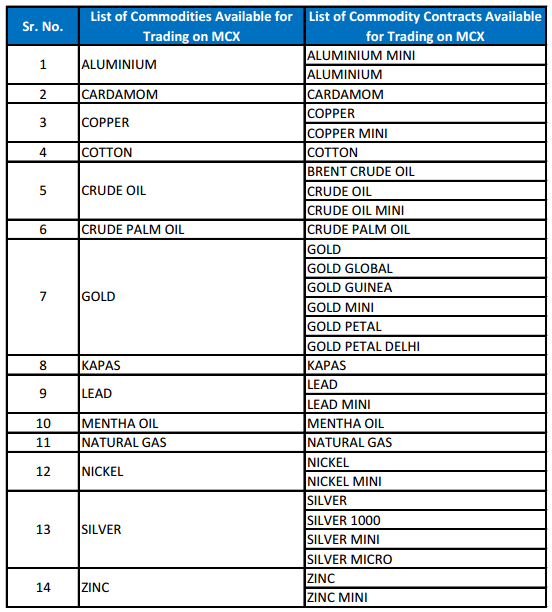

Here is the list of commodities available on MCX to trade; of course I got this list from the MCX website –

The idea is to cover all the major commodities that one can trade. Needless to say, one has to know how ‘Derivative Futures’ function before attempting to understand Commodities. So if you are not familiar with Futures, I’d encourage you to read the module on futures trading.

Anyway, assuming you are familiar with Futures, we will now start with Gold.

7.2 – The Gold Contract

Gold is a very actively traded contract in MCX. It has ample liquidity, with daily trades of roughly 15,000 contracts translating to a Rupee value of over 4500 Crore. Note, these numbers belong to just one type of Gold contract, often nicknamed “Big Gold”.

Gold comes in quite a few variants that one can choose to trade-in. Newbie and sometimes even the experienced commodity traders often get confused with these contracts, not knowing which one to trade and the difference between them. To begin with, let me list down all the different types of Gold contracts –

- Gold (The Big Gold)

- Gold Mini

- Gold Guinea

- Gold Petal

All these variants belong to the same underlying, i.e. Gold. I guess the best way to understand the difference is by understanding the contract specification of each of these variants. We will start with the big boy first, i.e. ‘The Gold’.

Here is the contract specification as per MCX, let me list the important things first, and then we will understand them one by one –

| Particular | Value |

|---|---|

| Price Quotation | Rupee per 10 grams inclusive of all taxes and levies relating to import duty |

| Lot Size | 1 kilogram |

| Tick Size | 1 rupee |

| P&L per tick | Rs. 100 |

| Expiry Date | 5th day of the contract month |

| Delivery Logic | Compulsory |

| Delivery Unit | 1 kilogram |

Let me discuss these details in the same sequential order so that it becomes easy for you to understand the subsequent contracts. We’ll start with the price quotation.

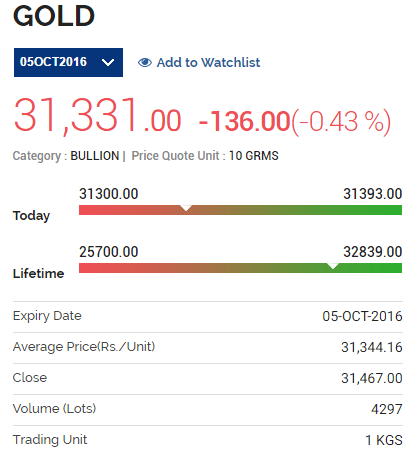

The price quotation, as you can see, is for 10 grams of Gold. This price includes all the import duties and taxes; of course, we will talk more about this at a later stage. For now, be aware that the price of MCX is all-inclusive. Have a look at the following snapshot, and it shows the last traded price of gold futures on MCX –

As you can see, the last traded price of Gold is Rs.31,331/-. Do note; this is the quote for 10 grams of gold. Since the lot size is 1 Kg (1000 Grams), we can calculate the contract value –

(1000 * 31331) / 10

= Rs.31,33,100/-

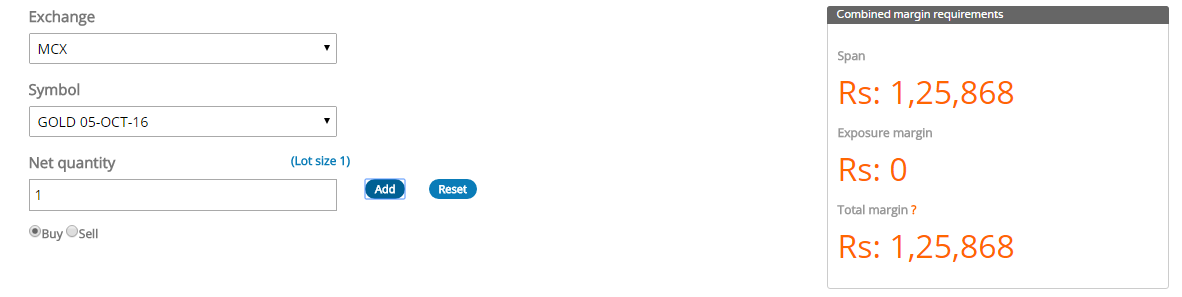

So what is the margin required to trade this? We can check this from Zerodha’s margin calculator –

The margin amount required is Rs.1,25,868/-, which means the margin percentage is roughly –

1,25,868 / 31,33,100

= 4.017%

As you can see, the margin percentage is just about 4%, which is pretty much similar to the currency contracts. However, the Rupee value of the margin is way too high, and it, therefore, prohibits many retail traders from initiating positions in Gold. In fact, this is the reason we have contracts like Gold Mini and Gold Petal, where the Rupee value of the margins is lower. We will talk about these contracts a little later.

Now assume you buy 1 lot of Gold on MCX, this means you have to park close to 1.25 lakhs as margin, and with each tick, you will either make Rs.100 or lose Rs.100 and how did we arrive at that? Well, it is fairly simple –

P&L per tick = (Lot Size / Quotation) * Tick Size

Let us apply this on Gold –

= (1000 Grams / 10 Grams) * 1 Rupee

= 100 Rupees

In fact, you can apply this formula to any futures and options contract to calculate the P&L per tick. Let me demonstrate this formula for the JPY INR contract. If you recollect the lot size for this contract is 100000 JPY, and the quotation was for 100 JPY, and the tick size is 0.0025, using this we can calculate the P&L per tick –

(100000/100)*0.0025

= 2.5 Rupees

Anyway, let us now focus on expiry. If you look at the expiry of Gold, it simply says 5th day of the contract month. Gold contracts are introduced every 2 months, and each contract stays in the system for a year, and at any point, you will have 6 contracts to choose from. Considering we were in August 2016, the following table should give you an idea of how this works –

| Currently available contract | Expires on |

|---|---|

| October 2016 | 5th Oct 2016 |

| December 2016 | 5th Dec 2016 |

| February 2017 | 5th Feb 2017 |

| April 2017 | 5th April 2017 |

| June 2017 | 5th Jun 2017 |

| August 2017 | 5th Aug 2017 |

Needless to say, the most recent contract is the most liquid contract to trade; in this case, it would be October 2016 contract. Now when the October 2016 contract expires on 5th Oct 2016, September 2017 contract will be introduced, and the most active contract from 5th Oct 2016 would now be the December 2016 contract.

Do recall, settlement in equities is always in cash and not physical. However, when it comes to commodities, the settlement is physical and therefore ‘delivery’ is compulsory. This means if you hold 10 lots of gold and you opt for delivery, then you will get 10 kg of gold. To get the delivery of the commodity, one has to express his intention to do so. This has to be done any time before 4 days to expiry. So given that the expiry is on 5th, one has to express his intent to take delivery anytime on or before the 4th (1st, 2nd, 3rd, 4th).

If you are trading with Zerodha then do note, we do not allow you to get into the physical delivery of commodities. So you will be forced to close the position before 1st of the expiry month. In fact, I personally prefer to close the positions early on and not really get into the physical delivery of commodities.

For all practical purposes, if you know these things about the Gold contract, you pretty much know what is really required before you trade the big Gold contract.

We will now move on to know the other variants of gold that gets traded on the exchange.

7.3 – The other contracts (Gold Mini, Gold Guinea, Gold Petal)

The big gold contract, as you realize demands a heavy margin requirement in terms of Rupee value. This prevents a lot of traders from trading the big gold contract, and perhaps this is the reason the exchanges introduced contracts with much lesser margin requirement.

The other gold contracts that are available to trade is –

- Gold Mini

- Gold Guinea

- Gold Petal

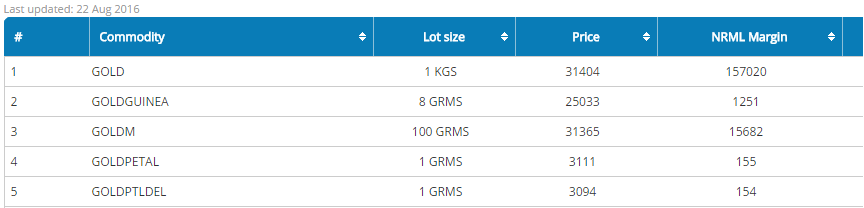

The details for the other gold contracts are as follows –

| Price Quote | Lot Size | Tick Size | P&L/tick | Expiry | Delivery Logic | Delivery Unit | |

|---|---|---|---|---|---|---|---|

| Gold Mini | Rs. per 10 gm | 100 gm | 1 rupee | Rs.10 | 5th day | Compulsory | 100 gm |

| Gold Guinea | Rs. per 8 gm | 8 gm | 1 Rupee | Rs.1 | Last day | Compulsory | 8 gm |

| Gold Petal | Rs. per 1 gm | 1 gm | 1 Rupee | Rs.1 | Last day | Compulsory | 8 gm |

I’m assuming the table above is a lot easier to understand now considering we have discussed these details earlier. Let’s dig straight into the margin details.

As you can see, Gold Mini (GoldM) contract requires a margin of Rs.15,682/-. In terms of percentage –

= Margin / Contract Value

Contract Value = (Price * Lot size)/Price Quotation

= (31365 * 100)/10

= Rs.313,650

=15682/313650

= 5%

In terms of margin percentage, this is roughly the same as big Gold. For the sake of completeness let us quickly calculate the P&L per tick for Gold Mini. We know –

P&L per tick = (Lot Size / Quotation) * Tick Size

= (100/10)*1

= Rs.10/- per tick.

Beyond the Gold Mini contract, we have Gold Guinea and Gold Petal contract. These are extremely tiny contracts which demand a shallow margin, as low as Rs.1251 (Gold Guinea) and Rs.154 (Gold Petal). The lot size is small, and therefore the contract value is small as well. You will find a few variants like Gold Petal (Delhi), Gold Guinea (Ahmadabad) etc., and I would suggest you ignore these, especially if your idea is to trade Gold.

Here is my honest opinion – if you are trading Gold stick to either the Big Gold contract or the Gold Mini contract, simply because the liquidity is quite bad in all the other contracts. To give you a perspective on liquidity on a regular trading day (on MCX) –

- 12 – 13K lots of big gold contracts get traded

- 14-15K lots of Gold mini contracts get traded

- 1-1.5K lots of Gold Guinea contracts get traded

- 8-9K lots of Gold Petal contracts get traded

The number of lots in Gold Petal should not entice you to believe that the liquidity is high, do remember Gold Petal lot size is just 8 grams, and therefore 8-9K lots translates to roughly 2-2.5 Crs.

Another important thing to note – liquidity is highest in the nearest month contract, so always stick to these. The thumb rule here is – farther the contract expiry, lower is the liquidity.

With this, I assume you are familiar with the Gold contracts and logistics. In the next chapter, we will discuss a few interesting topics such as the parity in domestic and International gold contracts, factors influencing Gold, the relationship between gold, equities, and dollar etc.

Key takeaways from this chapter

- Gold is one of the most popular bullion contracts that gets traded on MCX.

- The gold contract comes in a few variants – Big Gold, Gold Mini, Gold Guinea, and Gold Petal.

- Big Gold is the most popular contract, but requires a margin over Rs.1,25,000/-.

- The P&L per tick for the big Gold is Rs.100.

- P&L per tick can be calculated as = (Lot Size / Quotation) * Tick Size.

- Gold Mini is the 2nd most popular Gold contract, requires a margin of roughly 15K.

- Gold Petal and Guinea are other variants demanding much lower margin requirement. However, the liquidity in these contracts is quite low.

- It is always a good idea to stick to the nearest month contract as liquidity is high in these contracts.

- Delivery is compulsory for all these contracts; therefore, it makes sense to close these contracts at least 4 days before the expiry of the contract.

Does Zerodha support Electronic Gold Reciepts launched by NSE?? If yes,please explain how to purchase and sell them.

it launched them yesterday i.e. on 4th May 2026.

Still I could not able to see those EGRs

Yeah, the product just got launched.

Yeah, I know 🙂

No update from zerodha team on this EGR.

Not yet, hopefully soon.

Abhi tak to kisi bhi broker par nahi dikha raha EGR

Just want to thank you karthik sir

Happy learning, Sachin!

Where can I find a candle chart of Gold spot for Indian markets?

You can check Gold charts on trading view, not specific to Indian markets though.

why goldm september 25 future chart not visible in zerodha platform

Hmm, please do check with the support team once.

how to backtest the gold trading strategy if have no coding back ground.

You can check on the streak.tech platform.

Hey Karthik, I was checking for spread margin benefit found out that for GOLD ,LEAD, COTTONCNDY, STEELREBAR we are not getting calendar spread benefit , is this because they are categorised as LOW in volatility category ? Can you please help

As far as I know there is no spread margin in commodities, please do call the support desk once to check this.

No but was checking on the Zerodha margin calculator only we are getting spread benefit for natural gas , kapas, aluminuim, silver etc

Hmm, contract specific I suppose.

Hello kartik !!

I wanted to invest in gold so I decided to go for ICici pru golf ETFs but the problem is liquidity. There isn\’t enough volume in that etf.Then I looked for gold fund of ICICI pru mutual fund and in the overview section, it was stated that gold fund invests in the icicic pru gold etf.

My doubt is on liquidity of gold fund of icici. Will there be any liquidity problem in selling gold fund units if I accumulate large number of units of gold fund ?

I\’m saying this bcoz the gold fund itself invests in gold etf which is illquid so if I go to gold fund for redemption request, can he honour it assuming that I have large number of units ?

Instead of Gold Fund, look at Gold ETFs. I think most Gold funds invest in Gold ETFs. As far as honoring redemption is concerned, it should not be a worry.

The only gold etf which has great amount of liquidity is nippon india but it has expense ratio of 0.83%. ICICI gold etf has mediocre liquidity but it has expense ratio of 0.5%. So, if I invest in gold fund of nippon I need to pay 0.83% for etf plus 0.13% for fund expense so total charge is approx 0.96% whereas with ICICI gold fund the total expense is 0.5% for etf plus 0.1% for fund exp equaling 0.6% apprx.

So kartik dont you think it is better to invest in ICICI gold fund rather than its etf or nippons etf bcoz it solves my liquidity problem ( since fund can redeem the units easily) with lower expense ratio thereby increasing my returns slightly ?

Rest all the etf\’s either are either a bit illiquid or higher expense ratio.

Yeah, it does. Unfortunately, it is always a tradeoff and when investing in a Gold FoF, you are not dependent on secondary market liquidity like in ETFs.

Hi karthik sir,

Thanks for explaining all about gold. I still have one doubt,

As you said If we use continous option for the charts we could be able to analyse and track the past candlesticks also. But if i want to use 1 single chart for years, can i use continous option with the expired futures chart also.

For example, Now i am using Gold jun futures with continous option to analyse the patterns. may be on August, can is use the same gold jun futures chart to track the price action or i have to again shift to gold sep futures to track it. If so then i have to draw the patterns again in the sep chart right?

Hmm, not sure if I understand your query fully. But once you shift to continuous charts, it\’s good enough. You dont really have to shift back at every expiry.

Hi Karthik sir,

As you said I saw the video – It was very useful sir and gathered unknown informations like Liquidity to tender period, Gold – USD relationship, US fed rate cut, Inflation and Job market, Major global crises impact.

Sir, I really feel sorry, It can also be my mistake if i did not absorb properly. but i couldn\’t get the answer for the question that i have posted recently.

Sir, what is the symbol for gold as the main index to draw the chart on zerodha kite and analyse it technically. for april month contract i cannot see the candlesticks for last year, it is visible only from april month. It would be very helpful if you guide me through this.

Prashanth, that is a good point, and I missed mentioning it in the video. For doing TA, there is no separate chart for Gold. You will have to look at the Gold Futures chart itself, but do make sure you are looking at the futures continuous chart, and not just the contract-specific chart. You can call the Zerodha helpdesk to figure out how to switch to a continuous chart.

Hi karthik sir,

Like For an Individual stock there are chart (Bhel Chart) where we would see that chart and trade in the options but not on the particular options chart (eg – bhel apr 200 PE). Like wise there are many contracts for gold like (eg – gold apr 79100 CE). I just want to know which is the central index for gold where we can draw on charts and trade options….

Prashanth, please keep an eye on our Youtube channel, will be uploading a video around this.

Hi Karthik sir,

What are the symbols for Gold mini and gold petal to analyse the chart in zerodha kite?

In Kite\’s market watch, please type gold and you will find the contracts.

Hi Karthik

I am searching for strategies to trade in gold and silver futures, can you provide any document in zerodha varsity or other platform to gain good knowledge on gold and silver trading strategies for short term or long term

You can apply a few standard strategies for Gold like calendars, momentum etc. While there is no material that talks about Gold trading in specific, the other strategies have been discussed.

How to track gold spot prices, what is the code for it, can we track gold spot prices from zerodha or we have to track from other platform sir

The spot market is not traded, so there is data around that for retail public.

Hi sir

while trade nifty futures we refer nifty as reference for technical analysis like wise for gold and silver futures trades which one to refer for technical analysis

For gold and silver, there is no spot market reference Krishna. You will have to look at futures data only.

Thanks alot for great content, I am new to futures trading, to trade in Nifty futures we have Nifty50 as bench mark index, so for the gold futures which one we have to consider as reference before initiate trades in futures

Thanks, Satya. That would be Gold spot, but unfortunately its not traded like we see other EQ indices like Nifty 50.

Why the price of GOLD FUTURES IN MCX AND NCO DIFFER?

Contract\’s demand and supply adds to the difference?

Can i buy gold and hold it as log as i want , just like equity using commodity platform provided by zerodha ?

Yes, but not Gold Futures.

I want to buy gold and hold for short period ( one or two months), in international market preferably in USA. Is it possible in Zerodha ?

Nope, not possible via us.

Regarding Gold 25Aug Fut . In this 25 signifies expiry date?

Also I want to buy long term contract of Gold , is it possible?

YEs, thats right. You can buy Gold ETFs right?

Hi,

Can you pls tell, when i sell gold guinea, they do not return the whole money back at same time, they hold some part and give next day or next to next?

You will get credit instantly which you can use for other trades.

Dear Sir

How Prices of gold in India Calculated from global gold prices in dollars?

On 17.07.2024 Gold price in dollar was 2506$ & Gold prices in India was around 72000.

On 14.08.2024 Gold prices in dollar terms around 2515$ & gold prices near 67000-68000.

I just calculated by using USD-INR conversion but not matching.

Pls guide

Its not just the currency coversion, but it involves a bunch of taxes, duties etc.

It is mentioned 2 months after gold contracts are introduced. So after August 2017 it must be October 2017?. Or am I getting it wrong?

Why is goldbees price lower compared to gold petal or gold m ( talking about 1 gm equivalent) .?

How can I do a covered call on gold in zerodha ? What is the minimum options lot size available? And which underlying chart should I follow ?

Raj, not kept track of this. Perhaps its due to the duty arbitrage. Not sure, I need to double check.

How i will roll overy positions on gold mcx..,.

If i buy the contract of june month then when i have close my positions of june month (expiry) and how my contract will roll over to next contract(expiry),.

I have to close my positions and then again purchase contract or automatically by selecting OVERNIGHT my postions my roll over

Check this Nikhil – https://www.youtube.com/watch?v=FqRB7NGnOtA

Hey,

I got the answer from previous comments.

Thanks

Good luck!

Hey,

If i don\’t close my contract i will get physical delivery. The delivery can be collected from warehouse. Will the delivery be guaranteed? As I read in some some places that they don\’t give delivery to retail investors

Yes, delivery is guaranteed.

What are charges of physical delivery of gold

Mujhe tel ke vyapaar ke liye kya KRna hoga

in gold like nifty and bank nifty index is available or not?

like nifty index is available and i can get historical data , same way can gold index is available or not?

if available then how can i get historical price

Gold ETFs and Soverign Gold bonds are available, not sure if you are looking for the same thing.

For investing in gold, EGR was supposed to be the game changer but what happened after its launch at BSE in Nov 2022? There is no news on the internet. There is scrip code for EGR like G1G10B99 but one can not find these on Zerodha. ET formed that we need to activate trading in EGR segment, but there no such option. Any advice?

Looking for the same

How to trade option in gold sir

Please call the support desk for this, Kalai.

I wanted to trade in gold on intraday basics …so do I also need to avoid trading gold 4 days prior its expiry to avoid the risk of getting a compulsory delivery.

Yes. Also since its intrday, you anyway dont really need to carry forward the position right?

Is it possible to trade 100 lots of Big Gold? assuming that there\’s a big trader who want to trade only Gold with all his capital of let\’s say 6-7 crore.

– Will he face liquidity issue.

– Can he trade intraday with that big lot size without seeing much fluctuation due it his positions.

– If not, what will be alternative way for this.

You can initiate the trades, the market is liquid enough. But please be prepared for a 15-20 spread hit.

what is physical delivery in gold commodity

You get gold in physical form upon expiry.

@karthik can i trade gold petal options intraday?

And what will be the charges for commodity intraday options trading?

YOu can. But last I checked, the contract was not available to trade. Please verify before you trade.

Hello Sir,

\”Needless to say, the most recent contract is the most liquid contract to trade; in this case, it would be October 2016 contract. Now when the October 2016 contract expires on 5th Oct 2016, September 2017 contract will be introduced, and the most active contract from 5th Oct 2016 would now be the December 2016 contract.\”

The above lines. Instead of September 2017 contract will be introduced. It should be October 2017 contract will be introduced.

Thanks for the content.

Thanks for pointing out, Vinayaka. Let me check this.

How many times we can buy and sell GOLDM IN SINGLE DAY

As many as you\’d want.

Can we use GOLDM options contract plus Goldbees as Cash Secured put and Covered call strategy?

Yes, but there is no margin benefit here.

when i trade short call options on gold and what happens to the premium when it devolved into futures

It gets factored in.

Can we get the delivery of gold in commodities and if yes then what\’s the process…

Not possible.

I\’m new to commodities. From what I have read, there is always an expiry. I was planning to choose Gold as one of the investment. At first I thought to buy physical Gold from a Jewellery shop. But in reality I\’m not gonna do anything with that physical Gold. I also felt it is not safe to have much physical Gold in home. So I was looking for an alternative to buy Gold digitally. Since I already own some stocks and mutual funds in Zerodha, I was thinking to buy Gold through commodity market. But this expiry is my concern. I want to have these Gold on long term as long as I want for years like how we do for stocks. Any possibility for this?

Nishanth, you can always buy SGBs.

Hello

I am Mukesh Kevlya i have the below querries

1. Can i open an account with zeroda to trade on MCX in Gold.

2. Is MT5 available as a terminal on MCX, pls advise which terminal is available.

3. What is the lot size and margin requirement on MCX for Gold Global.

Appreciate reply on the above mentioned email

Regards,

Mukesh

1) Yes

2) No. But we do have Kite with ChartIQ and Tradingview integrated, which is really good.

3) Global Gold is discontinued

Does any of these have an option of delivery in demat ?

Nope.

Dear Karthik, I am not getting Gold Commodity options trading instruments in my zerodha app. Pls write the details of how to trade in gold options in zerodha… Thanks Macho Man

I\’d suggest you speak to the customer desk for this.

Thanks for the replies sir 🙂

This interaction is exactly what keeps varsity way above any other paid stock market learning modules.

Your video series are even better looking forward to them on the later modules too.

I really appreciate all of your efforts 🙂

Happy learning, Chetan 🙂

Sir on the site of MCX there\’s something said become a member Could you please explain them

It is for stocks brokers, Chetan. Not really for individuals.

Sir any comments on

The price difference in them Gold(1 lot) ,GoldM(10 lots) ,GoldPetals(1000 lots) makes an existence of an Arbitrage.

Perhaps, but you will have to match the quantities.

Given that using Zerodha we cant take physical delivery of commodities so is there any other way to invest in Commodities like Gold and Silver from a long term perspective

Chetan, if you are not keen on physical delivery, then try to explore both SGB, Goldbees, and Gold ETFs.

As you have mentioned Zerodha does not deliver physical gold; how is the position settled? Do user get cash equivalent of profit/loss in their account or do they get cash equivalent of 1kg of gold at expiry?

Also, Assuming contract is held by Zerodha in digital format on behalf of user, is it possible to present such contract at MCX delivery office and get physical delivery of commodities?

Yes, all contracts are cash-settled. Nope, MCX is an exchange, it won\’t deal with retail customers directly.

when was the last time the lot size for gold future contract got changed

I dont actively keep track on that Shivansh.

I think there\’s a mistake in delivery unit of gold petal and p&l of gold guinea in image .

Please keep an eye on our Youtube channel. Doing something related to this.

and as I was talking about arbitrage opportunity in gold and gold petal contracts but they have different expiries like as of now the April future expiry for gold is 5th April and for gold petal is 29th April. so on 31st march the gold and gold petal will have same rates (with some minor variation adjusted).

cause if they will not have same rates there is no point of arbitrage

Different expiry is a problem, you can maybe try intraday for price convergence.

I just noticed that in third last paragraph\’s second line its written gold petal lot is just 8gms but in the table above (where different gold contacts lot sizes is given) its written that gold petal lot size is 1gm and gold guinea has a lot size of 8gms

Ah ok. I think a mix-up. By the way, the lot sizes keep changing, keep a tab on that.

I was asking cause if they do it will create a great arbitrage opportunity

Yup.

does gold and gold petal contracts expires at same rate like gold and gold mini contract on expiry (adjusted with some minor variation)

I think they do 🙂

Sir, in kite by default for SILVER MAY FUT the qty is shown as 1

so did that qty 1 denotes 30 kg(lot size) ?

Yes, thats 1 lot.

What type of gold is traded in Gold ETF\’s/stocks/bonds/options & options ? Is it 18k,22k,or 24k ?

24K if I\’m not wrong.

Sir can we sell gold futures before expiry and get money in cash

Yup, you can buy and sell futures and options anytime before the expiry.

Why is GOLDM MAR FUT trading at a value lower than the GOLDM FEB FUT?

Demand supply mismatch I suppose.

Can I sell mcx gold (short selling) in delivery

Gold futures can be traded both long and short.

Sir I want to trade short tram on Gold MCX, how do I do ..?

I would do it on any software and how much minimum investment is needed if it was said in detail it would be very useful.

YOu can trade the Gold future.

Can I trade intraday in indian commodity market with 9-5 job?

Its tough and will be very distracting for you main work, Saurabh.

Karthik, you mentioned that Zerodha does not allow physical deliveries. I have a basic question, So if I am long on a contract and I sell to close my position. The counter party that buys will necessarily have to take Delivery right?

Yeah, most likely, unless that\’s an intraday buyer.

Sir what is tick size

and with each tick, you will either make Rs.100 or lose Rs.100 ,what do this mean

Didn\’t get this point

Tick size is the minimum movement in the underlying price.

Thanks Sir, which is best sgb for long term (name).

All SGBs are fairly similar 🙂

Sir, how to buy Gold for long term

SGB is a good option, check this – https://zerodha.com/gold/

the price for Gold Guinea was 37155 (we sell this contract which is 8 grams)

and the price of Gold petal was 4616 (we buy 8 contracts of 1 gram each) = 4616*8 = 36928

(these prices are as on closing of 9th April,2021 for the 30th April expiry)

now here we can make an arbitrage profit of 37155 – 36928 = 227 for every 8 grams

now my question is

case 1) Will the positions get auto squared off on the date of expiry (30th April) and we make arbitrage profit?

case 2) or do need to take the delivery of 8 gold petal (1 gram) and one give the delivery of 1 contract of gold guinea (8 gram)

please answer which case is applicable case 1 or case 2?

1) Yes, provided if you have the margins to hold to expiry (with other brokers)

2) We don\’t support the physical delivery of commodities, positions will be closed prior to the expiry

For gold mini, tick size is Re 1 and P&L is Rs 10. This means if I buy a lot for 45000 and the value becomes 48000, I will be earning 30000. Please correct me if I am wrong

Hmm, I think Gold Mini contracts are out and no longer available.

I Love to trade in Gold ETFs and SGB. However i am unable to track exact gold prices. I need to refer other websites/Apps for the same

You can track Gold futures price, Piyush.

Hello Sir,

I wish to know if one can track the exact gold/silver prices on the exchange in Zerodha watchlist? Like we can see real time value of any stock, could we do the same for 24 carat gold?

Yes, but these are for the futures contract.

Thank you. I will get back to you if I have any doubts.

Sure, Harshit. Happy reading!

Hi,

I am new to futures. I just wanted to know how does it work?

Say I want to buy Gold Mini. Cash in hand is ₹50,000/- and I checked the margin calculator, price as per margin calculator is ₹49418/-

So I can but 1 lot.

When is the expiry? Is it 3 months? 1 month?

and on the date of squaring off, how much profit will I make if the price is ₹51000/- or how much loss will I incur if the price comes down to ₹45000/-

Harshit, I\’d suggest you start with this module – https://zerodha.com/varsity/module/futures-trading/

how can i open scrip of nas goldmini option contract in kite platform

I guess Gold mini contracts are taken off by MCX.

Hi karthik,

Every nicely explained, i have a question many analysts believe gold is inversely proportional to stock market, is it true, if we experience the market crash, then can we invest in gold ?

Valuable advise please

The relationship may not always hold. But yes, you can diversify your portfolio by doing so.

Some correction related to above query.. I find the 24k gold spot price is approx 50600. Can you please explain this difference ?

Posted a response below.

It is said that generally the spot gold price is cheaper than the future price due to cost of storages, interest rates and speculations etc. But I wonder why at present time it is showing the opposite !! At the time of this writing, mcx gold dec future is trading at approx 50320 But the spot price of 24K gold in most cities ranges from 52250 to 52600. Can you please explain this difference ? Thanks in advance.

I suppose you got the spot price from jewellers, they add their own making charges to it.

Does Zerodha allow trading in NSE Gold mini options? If yes, what is the symbol for those options?

Hi Karthik ,

Above in 7.2 when we buy October contract which will expire on 5 October in this zerodha will close the contract on 1st of expiry month which is 1 October. So contract will trade only for 1 October so it\’s like INTRADAY. CORRECT ME IF I\’M TAKING THIS WRONG. And What will be the trade timings ?

Depends on the expiry day and when you buy right?

As we can buy gold on MTNL on line in same way how we could buy gold, silver or other commodity. Kindly clarify and give the link

I\’m not sure about MTNL, Vidod. You need to speak to them about it.

Sir, It is mentioned that \”The number of lots in Gold Petal should not entice you believe that the liquidity is high, do remember Gold Petal lot size is just 8 grams, and therefore 8-9K lots translates to roughly 2-2.5 Crs.\”

But actually the lot size is only 1gm as mentioned by you.

Please check n revert.

Thank you for the varsity sir

I think there is a revision in lot size 🙂

Hi Karthik, need your opinion on gold physical investment. I am a salaried employee and I have total 5 lakh rupees with me now. I am thinking to buy 1.7 lakh rupees of gold. Is it right for me to do it now or later? Please suggest

I really cannot comment on the timing bit, but all I say is that probably SGB is a better way out than physical gold, unless you have your own reasons to buy physical gold.

Hi, Sir I want to start trading in commodity especially in Gold. How should I go.

Start by learning about the nuances of commodity trading, futures, and gold fundamentals. All the information is available to you here.

Hi Sir , meine Commodity mein GOLDM SEPT FUT buy kiya hai lekin mujhe long term hold karna hai ..lekin mujhe Rollover nahi ata ..plz bataye ki Roll over kaise karte hai ..plz reply

Near expiry, you sell Sept and buy the next months contract. That all rollover 🙂

i opened recently account with zerodha i want to how to invest money into commodity gold mini it will unit price or 1 gram price. please let me know

thanks and regards

nageswaran

You can trade in Gold futures, which is different from investing. You\’d rather invest in Goldbees or SGBs.

What is the process if i prefer to take delivery?

Unfortunately, we don\’t support the physical delivery of commodities, so I\’d not be able to help you with this.

Thank you sir.

Welcome!

Hi sir,

I am new to commodity.

How to find out the support and resistance for gold Guinea, n for any commodity , is it by using any calculator or by price action ?

Thank you.

The same way you would for any stock or equity index.

https://zerodha.com/varsity/wp-content/uploads/2016/08/Image-1_A-list.png

I saw GOLD is 46727 and GOLDPETAL is 4705 right now.

I know it\’s a very basic question, but can this be considered an arbitrage opportunity?

Complicated due to different contract structures, but possible theoretically.

Sir when there is much of a difference between gold petal – guinea or gold – goldM

Can we arbitrage these difference based on them.

What is the minimum arbitrage for a profitable trade?

Yes, but I think the exchanges have withdrawn some of these contracts. Min arbitrage should be enough to compensate you for the charges and give you pop on that.

Hi sir just found that commodities can be traded from monday to saturday and have long trading time from 10:00 am to 11:55 pm on week days and 10:00 am to 02:00 pm on saturday.

Is this applies to all commodities on MCX?

Yes, this is applicable to MCX.

How about the delivery options? How to purchase/convert it into physical gold? Where to take delivery? Needed full details.

Unfortunately, we don\’t support that process at Zerodha, Saravana.

A big shoutout to your graphic design team, Karthik. The graphics throughout varsity have been really really cool and amazing. They add quite a lot of value to the content.

Thanks so much, Rohit!

Hi Karthik!

Are gold contracts as liquid as Index Options.

If an institution has to buy/ sell 300 contracts at a particular price, will they be able to?

Maybe not as liquid as the Index options, but they are liquid enough. Yes, 300 contracts is possible.

is gold contract advisable now ?

It depends on your world view, right 🙂

\”I will skip the usual background to commodities market part, the one which talks about the history, forwards markets, the farmers in US, the Chicago Mercantile Exchange etc. You will find this in almost any material on Commodity market.\”

Sir, can you please point me to a link where I can learn more about this.

Mohan, any textbook on commodity markets will give you this information 🙂

How can we get delivery of Gold in mcx.

We dont support physical delivery of Gold, Hitesh.

I can\’t understand just tell me is it equivalent to buy GOLD and ETFs

Means buying ETFs I buy GOLD it means I am equivalent to Jeweller business who buy and sell Gold

Pankaj, for long term delivery of Gold, you can even buy the Government\’s Soverign Gold Bond. Please see this – https://tradingqna.com/t/what-is-the-best-way-to-invest-in-gold-this-akshaya-tritiya/13139/5?u=bhuvanesh

Is it possible to convert ETF GOLD into physical gold or at least can convert into money

ETF offer which gold 22 carat or 24 carat

No, this is not possible Pankaj.

I want to clarify that Like Equity share Gold can be Delivery can sold after 1 years or onwards

In simple As you know Equity share eg . SBIN can take in Delivery position and can be sell at any time longterm position 10 to 20 years

Is this same occurred for GOLD

You can buy gold ETFs, check this – https://support.zerodha.com/category/trading-and-markets/trading-faqs/articles/list-of-etfs

Is taking delivery complsurry in gold petal

Nope, not necessary.

hello karthik

1.right now i choose 1 hr, 30 min and 15 min with macd and 9, 21 ema. i choose 1 min and 5 min chart for sideways market with same macd and ema. what is the best timing for intraday trading and for TA\’s effective performance ?

2. And frankly speaking karthik, after knowing this kind of precious knowledge as you teach in TA and in all varsity still i do not have courage to trade. i analyze the market with TA it works so well, for e.g if i see engulfing pattern in 1 hr or 30 min chart i still do not able to trade at a time. Is that something to overcome my fear ?

1) Depends on your risk appetite. Stick to EOD or at the most 15 mins time frame. 9×21 is a decent start for intraday trading.

2) You cannot swim by reading a book, you will have to swim at some point 🙂 So dont hesitate, go ahead and place a trade…even if it is with 1 share. The lessons you learn when you have a live trade is far more valuable the lessons you\’d learn otherwise.

I would like to know the weekly/monthly/annual calendar and timing of international data postings which affect the cost of major commodities like gold, Crude, Natural gas and base metals. I have heard that crude stock data posting on Wednesday affects crude price.

You need to explore this site – https://tradingeconomics.com/calendar

I WANT HISTORICAL DATA FOR MCX GOLD ,I HAVE ACCOUNT WITH ZERODHA CAN U PLZ HELP ME OUT.

sir pls explain how to buy options in gold index, at this hour I am trying buy GOLD SEP 38000 CE at Rs.150.45 but the system in not accepting my order

You need to check if you have sufficient free capital to buy the contract.

Hi Karthik,

Just started exploring commodity world, have some basic apprehensions, pls help clear them.

1. If I just want to do commodity trading with NO intent of taking physical delivery what needs to be taken care to avoid physical settlement.

2. Are all intraday commodity positions auto squared off by RMS by end of day and hence trader would be safe from physical delivery?

Regds,

Anshul

1) Just ensure you close the position before the expiry, this will take care of avoiding the delivery based situation.

2) Thats right.

What are the trading timimgs for Gold

You can trade gold between 9:00 AM t0 11:30 PM on all trading days. The holiday list is here – https://zerodha.com/z-connect/traders-zone/holidays/trading-holidays-2019-nse-bse-mcx

hello sir

1.is it possible in near future that we can use continuous chart in lower time frame

2.when will it be available for cds

3 is there any alternate way to see previous data in lower time frame???

1) We already have continuous chart on a EOD basis. Working on lower time frames

2) Nope, again this is on the pipeline

3) Can you try chartink?

Hi

what are bad thing about illiquid stock or metals (one i know it does not move parallel with BIg gold)

You have done a great work no one has to go anywhere after coming here

wish u happy holi

may god give crore of rs to both us 😉

Thanks for the kind wishes, Gautam. I really wish it comes true 🙂

Hello Sir,

I am new to Commodity Trading. Your Answers are really very helpful in my learning.

I have 2 queries:

1. Is there any max. limit or max. quantity one can hold ? Say for Example Only these many Lots of Gold is allowed to be bought by a trader..

2. Is there any restriction on the maximum number of trades that one can make on a Single day ?

Could You Please advise.. Thanks in Advance..

1) Each commodity has a restriction on position limits, its best to check on the MCX site for specifics.

2) No

Hello Sir,

Is physical settlement is same for other metals also like that of gold. Fr Eg: Aluminium. When we have to square off the position if settlement is on 19th. What will be the case if we have a arbitrage position. say short of 1 lot of mega and long of 5 lot of mini. What will happen in such cases if we didnt square off before 5 days of expiry.

Thanks,

Rashid

Its best you square off the position for the delivery period starts, Rashid. Else you will have to take the pains to go through the delivery process and the arbitrage opportunity may not exist.

Dear Sir,

Let me know the process for gold etf.

Thanks,

Harsh Pandya

8141167104

You buy it just like any other stock on Kite, Harsh!

Sir what is the \”delivery unit\” in the contract specification ?

That is the unit size of the commodity, that you will be obligated to take delivery upon expiry.

So if I buy 1 contract of gold petal, will I get 8 grams of gold upon physical settlement. The contract lot size itself is 1 gram.

The delivery size is 8Gms for Gold petal, check this – https://www.mcxindia.com/docs/default-source/default-document-library/gold-petal-may-2019-contract-onwards.pdf?sfvrsn=fa32d790_0

You will have to pay the money equivalent to 8Gms.

To be clear, you mean I cannot physically settle 1 contract but have to buy/sell. 8 contracts if I wish to go with physical settlement. Am I understanding right sir?

No, each contract has a delivery size of 8 grams of Gold petal. That\’s what I meant.

The details for the other gold contracts are as follows –

Sir I am still confused. Below table says that the contract size is 1 gm. So tell me the difference between lot size and delivery unit please. Thanks for your patience with me

Price Quote Lot Size Tick Size P&L/tick Expiry Delivery Logic Delivery Unit

Gold Petal Rs. per 1 gm 1 gm 1 Rupee Rs.1 Last day Compulsory 8 gm

Lot Size is the tradable quantity on the exchange while the delivery unit is the minimum quantity(in multiple) you can opt for physical delivery. Since it is not feasible to delivery 1 gm of Gold, Gold Petal carries a delivery unit of 8 grams. If you have a lower quantity, it will be cash settled.

Now when the October 2016 contract expires on 5th Oct 2016, September 2017 contract will be introduced, and the most active contract from 5th Oct 2016 would now be the December 2016 contract.

Just noticed that the above should be corrected. The new contract introduced will be October 17. Am I right sir?

Ah, thats a mix-up. Will plug that in.

No worries sir. Always you\’re the best!!!!

Good luck, Raj!

Hi,

I am new to commodity tading.I bought goldm 19 feb futures on 28.1.18 ,but i recived message to squre off my holding on 31.1.18 before 11.00a.m. pls let me know the expiry date of the contract.

I guess these are physically settled, better to rollover the contract.

i also want to trade agri commodities in ncdex .Will you advise me of any good broker which would provid eme trading in ncdex.

I\’m not sure, Anulekh. Btw, why do you want to trade agri commodities? Do you understand them better?

I think that in some cases their demand and supply could be understood better and that they can move by more percentage as compared to stocks which could result in higher gain if our direction is correct.Am i right?whtas your view on agri commodities.

As long as you stand to understand the demand-supply dynamics and know how to trade off it, its fine 🙂

Respected Sir,

Firstly I would like to thank You for this amazing job of educating the public you\’re doing. It is truly magnificent! I have a question for which I would greatly appreciate your input.

I tried calculating the Option Greeks for Commodities on the Black – Scholes Model. However, the MCX website does not provide the Implied Volatility column. Is there any other way to calculate the same for the Commodities?

I\’m not sure about IVs on MCX website, but then you can reverse engineer the B&S model to give you the IV. Check this – https://zerodha.com/z-connect/queries/stock-and-fo-queries/option-greeks/how-to-use-the-option-calculator

Thank You for the quick reply! The article is genius and makes perfect sense. Thank You very much Sir! All the best! 🙂

Good luck to you too, Lalit!

You said that delivery of gold contract is compulsory if position is not squared off.

if for some reason the trade cannot be squared off , what will happen then.

It will be treated as an expression of interest to take delivery.

Similarly if someone has shorted say gold and not squared off till expiry then he had to make delivery of gold. Is it so?

Also if the position is squared off even in expiry day then there would be no settlement issue or position should be squared off before 1st of expiry month.

You need to deliver 995 purity(or higher) Gold to the MCX vault who will, in turn, give it to the buyer of the contract. Failure to provide delivery will lead to a cash settlement with a penalty of 3% of the contract value on expiry (or more if the gold price has moved up). The MCX contract specification has more on this.

why you are not allowing delivery of gold in demat form.

This is Gold futures, there is no concept of delivery here. I\’d suggest you look at https://zerodha.com/gold/

Sir, what is a Bullion contract?

Bullion is nothing but Gold.

sir, when i am writing gold on search box it shows copperm aug future. Then how i trade on gold commodity?

Look for \’Gold MCX\’ on the market watch in Kite. You will find the futures contract. Good luck!

what are the timings of commodity market?

10.00 AM to 11.30 PM (up to 11:55 P.M. on account of day light savings typically between every November and March of the following year) for all Non-Agri commodities.

10.00 AM to 9.30 PM for Internationally linked Agri commodities (Cotton, CPO & RBDPMOLEIN)

10.00 AM to 5.00 PM for other Agri commodities.

Dear sir, I am member of zerodha and at present trading on equities only.

Sir in this chapter you have given a table for Gold Mini, Gold Guinea and Gold Petal in that in Delievery Logic you stated as Compulsory. Please clarify whether in these delievery is compulsory and it can not closed for cash.

Is it true

You can close for cash if you decide to square off the position before expiry.

so you mean to say that GOLD M August fut contract will expire on 5th of august?

Not sure of the date, but yes, the contract will expire on the designated expiry date.

when i type gold in kite it shows gold fut contracts, how do i get the gold spot chart???

Gold spot is not traded on MCX, hence the chart is not available on Kite.

then form where can i get the chart to analyse the longer time frame data?

YOu can always check the futures chart.

Hello Karthik Sir

I have read your pdfs\’ and I am simply mesmerized by the way you have written down the content comparing it with routine life along with the graphs. I have opened the account in zerodha. I am pursuing MBA and very much interested in capital markets. Actually we are 3 friends and I would like to know if there is any project for us or any internship opportunity under your guidance. Hoping to learn from your experience and knowledge.

Thank You

Thanks for the kind words, Mohit. I\’d suggest you reach out to our HR to know if there are any opportunities in Zerodha.

I want to take delivery of gold petal in demat. How can I do so..?

You cannot do this. However, you can take delivery of Goldbees, which is basically an ETF based on gold prices.

What an awesome tutorial this is !! Very nice and elaborate.. Just what we need… Thanks a lot for this…

One more thing.. Is there some sort of chart that lists the quotation, lot size, tick size, etc for all the actively traded commodities.. Like i was looking for a table that would list all the commodities in 1 place which would be easy to refer…

Thanks for the kind words, Manish.

MCX gives out that chart, I had a copy of the same (need to dig up)…will try and put that up sometime soon.

hi sir i dont have clarity on mcx contract expiry dates can u guide me what is best option to do commodity trading intraday or carry forward contract.when i need to exit before expiry or wait till expiry, i am also confused about physical delivery. i have read somewhere if u dont close ur contract it will goes to physical delivery what is that , what is warehouse receipt?

presently i am trading in equity but i am intrested to trading in commodity as well as currency so i am beginner in this commodity trading and eager to learn plz guide me on above question and suggest me any book for the same

thanks in advance

regards

atul

Most of the thing you\’ve asked is explained in the chapter itself. I\’d suggest you close the position before expiry. Intraday or swing trade really depends on your risk appetite.

Hi,

Was looking at the GoldM contracts. When I look at it in the Margin Calculator in the \’Net Qty\’, I see 100 (Lot Size). But, when I try to trade it; the qty says \’1\’. Does that mean 1=100, so the tick is Rs 100? Similar is the case with SilverM.

Yes, 1 refers to the multiplier.

Can we take short positions in gold mini and close it before 1st of expiry month, same as in nifty futures or there is difference in commodity trading n stock futures trading

Yes, you can short the contract, carry forward the same, and close it before the expiry.

( Now when the October 2016 contract expires on 5th Oct 2016, September 2017 contract will be introduced….). In this sentence isn\’t the month should be October 2017 that is 2 months after August 2017 as mentioned on the Table ?

And Thanks for all this. It is very helpful and informative and is explained in the most simple way possible. 🙂

Sumeet – Thanks for pointing out, I may have mixed up the dates.

Hi Karthik

Does commodities trade on saturday and sunday as well on MCX? , if yes , what is the timing on these days for trade

Regards,

MSP

Nope, they dont.

Hello All

I am a beginner in commodity trading. Kindly assist me in the following

1.Which type of analysis is suitable for the Intraday commodity trading.

2.Which pattern i should use ?

3.At present i am using a 5 minutes candlestick chart , Is that right to use.

4.At present i am trading only in Metals ,kindly suggest some best analysis & patterns to study & follow.

1) TA helps

2) Candlestick patters

3) You can use 5 mins, but my suggestion would be either 10 or 15 mins

4) Simple TA works like a charm, give it a try.

Hi karthik

Thanks for your reply,But i don\’t understand what is TA ? Please explain and provide some links to learn them.

Here you go – http://zerodha.com/varsity/module/technical-analysis/

Hi Karthik,great work by you and your team I have gone through all modules, excellent work!! .

Thank you 🙂

Lord of wisdom !

God of intellect !!

\”ShreeGanesh\” bless \’u\’..!!!

Thank you, and wishing you and family the same!

I have an account in Zerodha since last 4 years. But Commodity transactions is not active. What to do for that. Is there any separate charges for that? Can we trade commodities in kite ? Are there separate yearly charges for mainting commodity account? Please Post Crude related article at the earliest.

We will post chapters on Crude soon. You need to open your commodity account to trade commodities. Suggest you contact our sales team for that. Yes, you can trade commodities via Kite.

I wish to trade Gold mini futures. What is the market timing in India to trade this?. example ..Stock market opens at 9.15 a.m and closes at 3.30 p.m. beyond which we cannot trade..similarly is there any timing for commodity market?

10 am to 11.30 PM.

@Kartik, when the tioic on crude oil will be posted. Eagerly waiting.

Right after topics on Gold and Silver!

10:00 AM to 11:30 PM.

Hi Kartik,

Which is the most traded commodity in India ( or in Zerodha clients) gold, silver or crude oil or any other one and can you please specify the other major countries commodity market timings in IST, which are effecting Indian market

Gold and Crude has to be the most active commodities in India. They trade from 10:00 AM to about 11:30PM.

Thanks for the reply.

Could you please provide the market timings of other major countries like US, EUROPEAN, JAPAN etc

Most of the international currency pairs trade 24/7.

How can I invest in Gold? Like If I want to invest in SBIN I simply buy 1 share of SBIN by CNC trade.

How to buy Gold by CNC trade?

Yes, you can buy the Gold Bees EFT from the exchange, check this – https://www.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuote.jsp?symbol=GOLDBEES&illiquid=0&smeFlag=0&itpFlag=0

Karthik Sir, when you will write strategy for crude oilm……. waiting for it

Right after the chapter on Gold & Silver.

Market Guru,

Gold petal lot size 8gm or 1gm ?

Its 1 Gram.