What did we learn?

Happy Christmas and a new year in advance, everyone. What a rollercoaster this year has been for the markets. Given the war in Ukraine and the dramatic spike in inflation and interest rates, there’s been carnage in the growthy and most speculative segments of the markets. In the words of every sell analyst, the term “regime change” describes the year best. Given that we’re at the end of the year, now is as good a time to take stock of the year in the markets and hopefully learn a thing or two.

2021: Everything is going to the moon

2022: Did you know government bonds offer ~7.2% guaranteed?

In a shocking turn of events, new investors this year discovered that the markets don’t always go up. Last year, investors were happy that everything from stocks to pictures of monkeys was going up. But this year, they are talking about recessions and crash landings. The change in sentiment is stunning.

The last three years were weird. We’ve probably lived through ten years of events in just three years and forgotten a lot of it. Given where we’re today, I think it’s worth reflecting on how we got here. Maybe it will help us gain perspective for what comes next.

It’s hard to overstate the impact of the pandemic. If you think of civilization as a person, the pandemic was a heart attack. There are very few historical parallels that even come close to 2020. When talking about crises, the typical examples people like me reach for are the 2008 crisis, the 2000 dot-com crash, or the great depression of the 1930s. But the pandemic was different; it was an existential health crisis, a social crisis, and an economic crisis all rolled into one.

Think about it for a second. We shut down large parts of the global economy and locked people in their homes. Shutting down an economy is not like switching off a light bulb. The pandemic led to the death of millions, and the social impact was devastating. The economic damage was equally staggering. Hundreds of millions of lost jobs, over $17 trillion in lost lifetime earnings, and over $10+ trillion in lost economic output.

To contain the fallout, governments and central banks around the world unleashed fiscal and monetary policy stimulus on a scale never seen before. In just the first two months, governments had introduced over $10 trillion worth of support measures. By the end, the US alone had spent over $6 trillion to support households and businesses. Interest rates were slashed to zero in advanced economies and to record lows in emerging economies. We’ve never seen such a gigantic economic response in the post-war period.

The low rates and stimulus measures averted a global depression, but it had some unintended knock-on effects. The easy money environment due to low interest rates and stimulus payments incentivized risky behavior in markets on a scale we haven’t seen since the dot-com bubble.

With people bored and locked in their homes without entertainment, the stock market became the go-to place for cheap thrills. Retail investors were speculating on everything from penny stocks, call options, SPACs, crypto, NFTs, and all other things that didn’t even exist a few years ago. It was pure mania on 10X leverage. From 2020-2022, we saw as many new investors as in the preceding ten years. While there was good behavior, it was far outweighed by the bad.

This craziness was most apparent in the US. Indian markets were relatively tame, thanks to all the regulations by SEBI. It was a frenzied environment where everything was going up. Fundamentals and valuations became dirty words. But nothing lasts forever in the markets— everything is cyclical.

My earliest memory of a market crash was the 2008 crisis. I’m part of a generation that has only seen a bull market and a stable inflation environment. Being a post-2008 bull market baby, I hadn’t appreciated the destructive impact of inflation and rising interest rates. The combination of both has been like a wrecking ball. As interest rates rose around the world due to inflation, the prices of speculative assets crashed.

The crash in growthy and speculative corners of the market has been so severe that people have rediscovered the meaning of cash flows, profitability, and valuations in a span of months.

None of the dumb things that have happened in the last couple of years are unique. People have made the same mistakes since the invention of money, but we never learn. As the saying goes, “Those who do not learn history are doomed to repeat it.”

So, what did we learn?

Stories will always get you in trouble

The world is chaotic and unpredictable, but the human brain hates uncertainty. In fact, knowing that something bad might happen is more painful than knowing for sure. We tell ourselves stories by arranging random events into coherent narratives to deal with the uncertainties of life.

It’s the same with the markets, they are inherently random and unpredictable, and we use stories to make sense of things. “The markets rose today because of the union budget” is much better than “I don’t know why the markets went up.” We tell a story by abstracting the actions of millions of traders and investors into a single headline. Stories are a coping mechanism.

The markets move based on narratives as much as they do based on numbers. When the markets bottomed out in April 2020 and stocks started rallying, the fundamentals justified it as most companies recovered from the pandemic shocks. After all, the markets are forward-looking and constantly discount the future.

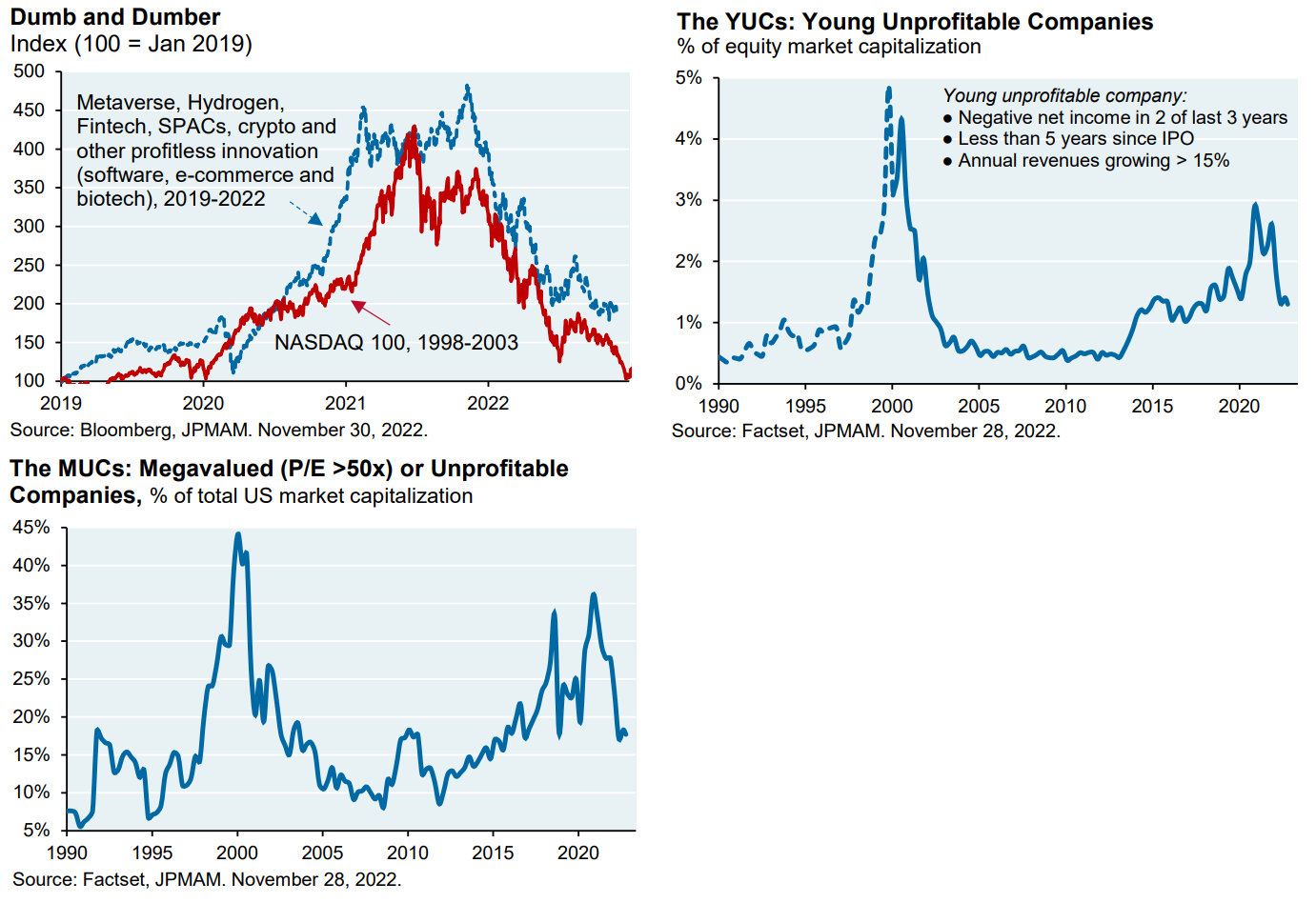

But it wasn’t just quality that was going up, but junk too. All bull markets start with some link to reality and devolve into insanity. In the last three years, large segments of the market were gripped by speculative mania. Unprofitable companies, thematic ETFs, penny stocks, special purpose acquisition companies (SPAC), crypto tokens, and IPOs all went to the moon.

Take a look at the charts below.

These assets weren’t going up because of the fundamentals, but stories. A well-told story can do everything from making garbage seem like gold to starting a revolution. What makes stories dangerous is that they appeal to emotions, not logic. We aren’t robots to get rid of our emotions, but they can be a liability in markets if not managed properly. In the last three years, stocks, funds, and other assets with vague and meaningless sales pitches like “disruptive innovation,” “megatrend,” and “revolution” saw billions in inflows.

The sales pitches were designed to induce FOMO—if you weren’t investing in these products, you would miss out on the mega-cap companies of the future and the opportunities of a lifetime. People who didn’t buy this nonsense were mocked with the phrase, “Have fun staying poor.”

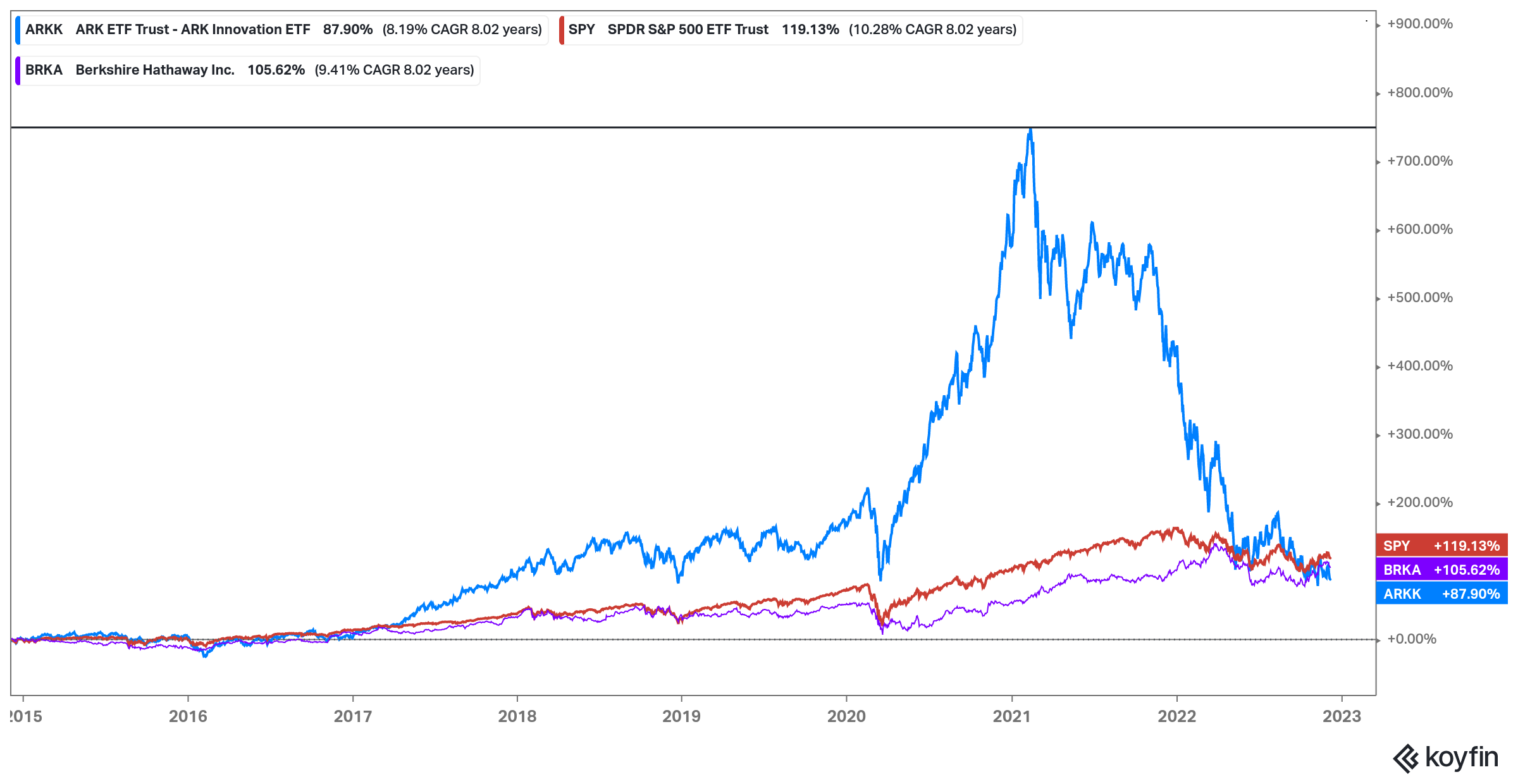

The ARK Innovation ETF was the poster child of this mania. The fund had less than $5 billion in AUM in Jan 2020, but by mid-2021, it had $25 billion. Cathie Wood, the manager of ARK ETFs, was hailed as the next Warren Buffett. For a while, she really did look like a genius as high-growth stocks saw stupendous rallies. The chart below shows the performance of the ARK Innovation ETF vs. Berkshire Hathaway and the S&P 500. Compared to ARK, the S&P 500 and Berkshire Hathaway look like liquid funds.

ARK Innovation Vs. S&P 500 and Berkshire Hathaway

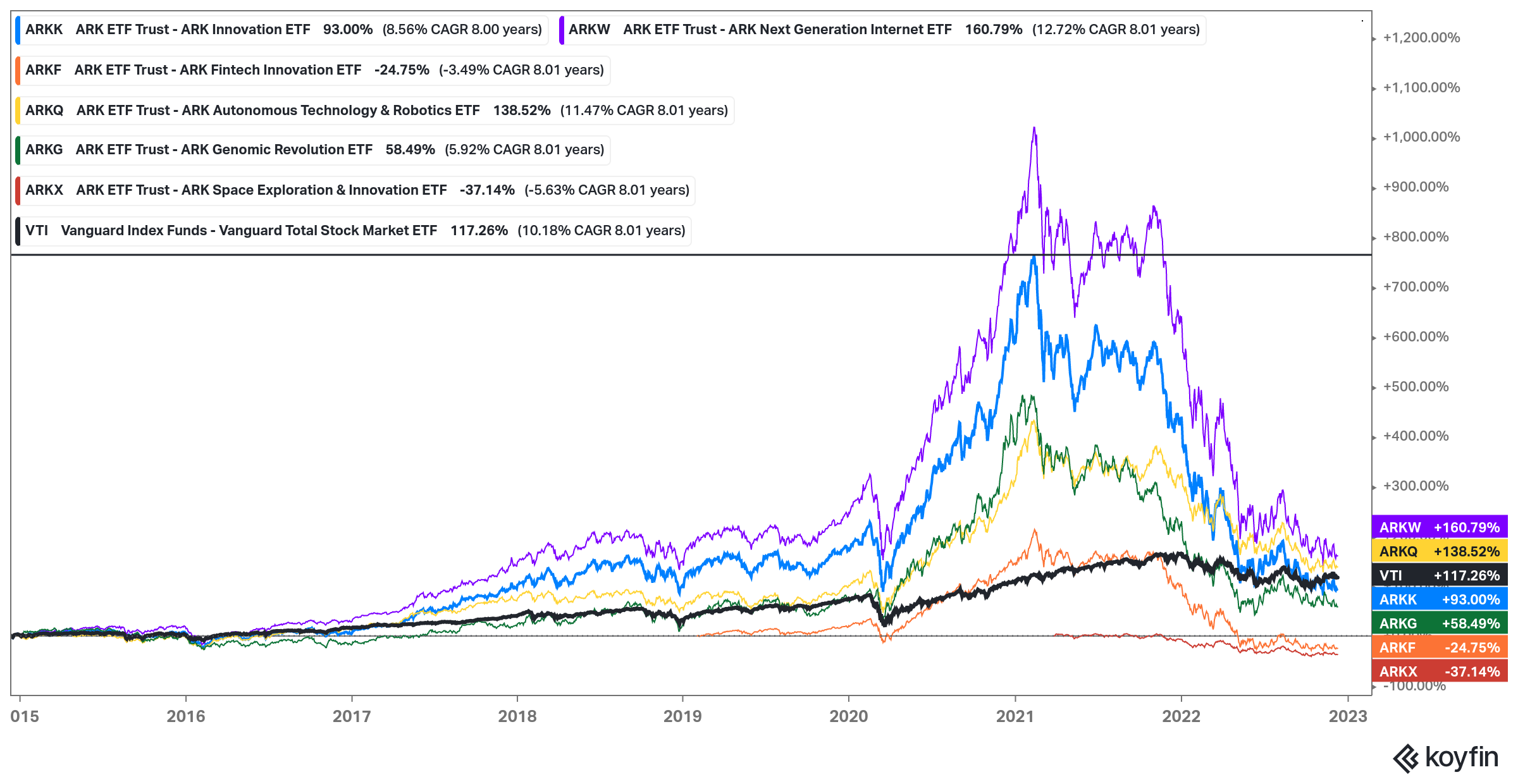

But, as it turns out, it wasn’t genius—it was just low interest rates and a bull market. It wasn’t just ARK; most tech-themed funds went up in a straight line. But this year, they’ve all fallen back to Earth from the moon. The sheer destruction in these speculative names is a sight to behold.

ARK Thematic ETFs

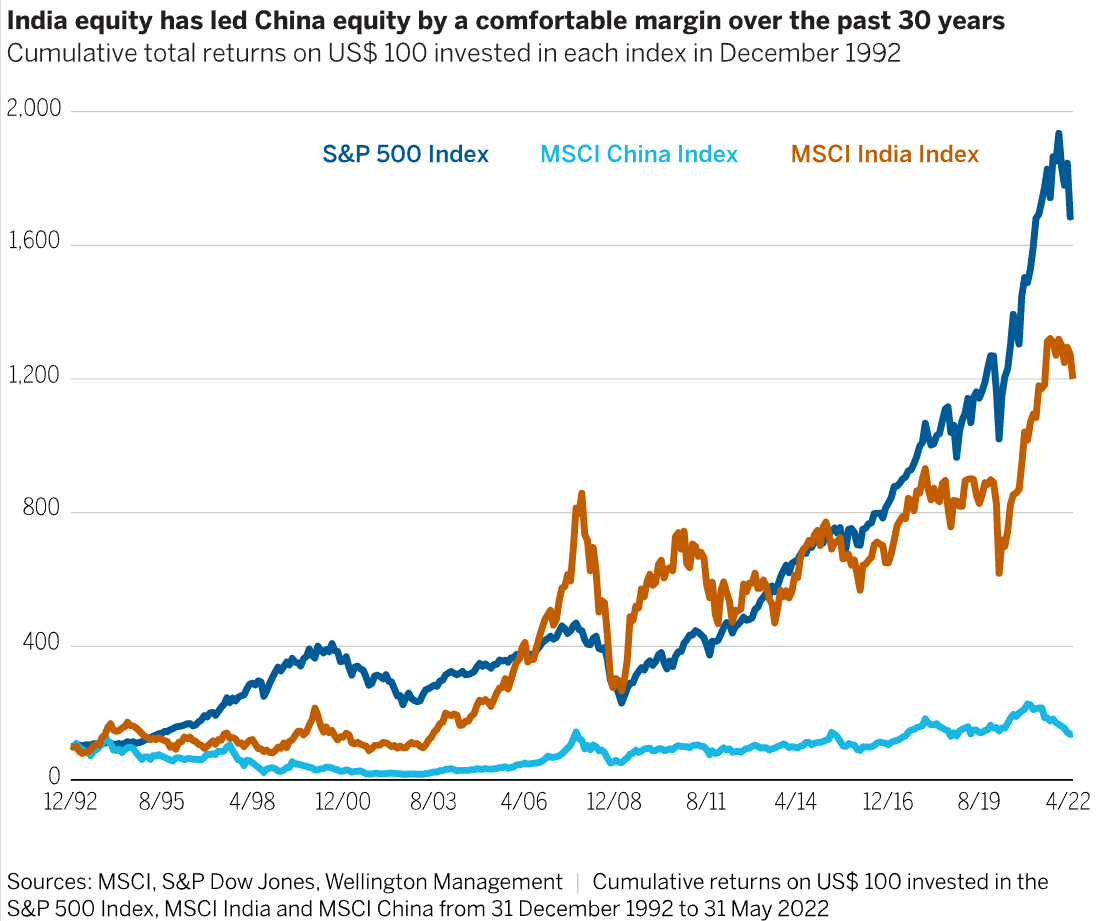

It isn’t just these newfangled things; stories can lead you astray, even when investing in countries as a whole. For decades, China has been touted as an investment opportunity of a lifetime. Even in all the 2023 market outlooks, overweight China is a recurrent theme. The pitch was that it was the world’s fastest-growing economy and home to some of the largest and most innovative companies like Alibaba and Tencent. If you weren’t investing in China, you’d be poor.

The story was true, but that doesn’t mean it made money. The MSCI China Index has generated 0% since its inception—China has been all risk, no return. The China story hides the enormous political risk, high share dilution, the lack of the rule of law, and shareholder rights. We saw this on full display in this year’s tech crackdown. The most important aspect this story hides is the fact that there’s no link between a country’s GDP and the stock market.

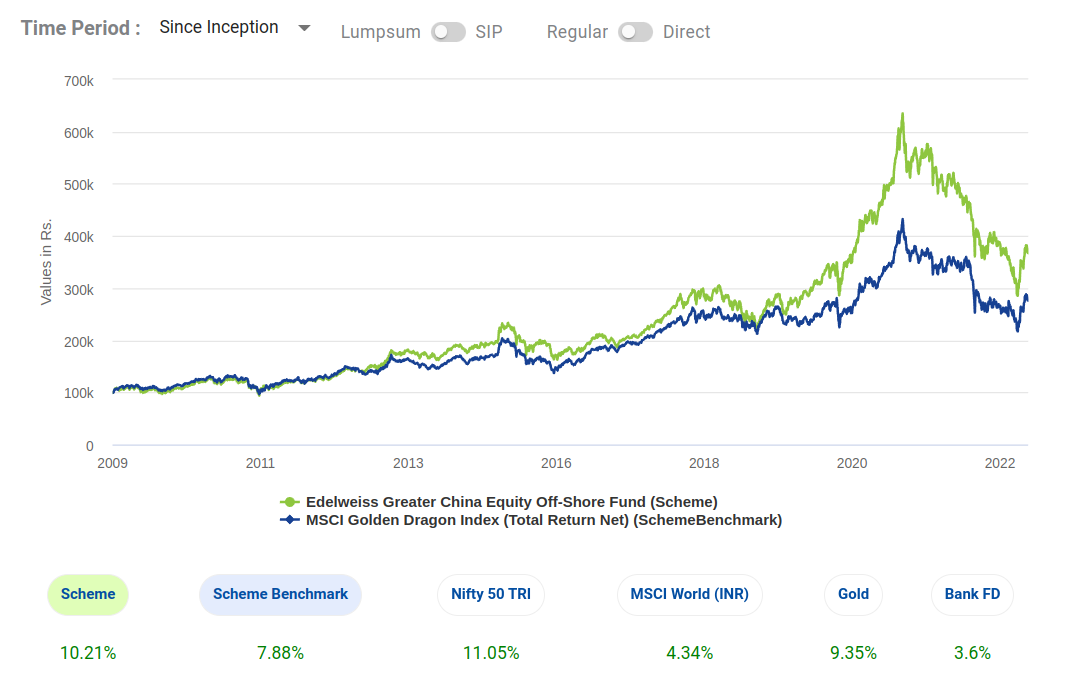

Edelweiss has a fund of funds that invests in JPMorgan Funds – Greater China Fund. The crash in Chinese equities has wiped out years of outperformance in months. I am not making a judgment if this fund is good or bad. What I’m trying to say is that single-country funds, like thematic or sector funds, need robust risk management and timing, especially when you are buying a story.

Edelweiss Greater China Equity Off-Shore Fund

Keepsakes

Investment decisions should be based on evidence and hard data, not stories. We’re naturally drawn to investment stories because they are a shortcut, but that rarely ends well. Market history is littered with stories of investments that have imploded spectacularly. Just look at Nifty 50 stocks (In the US) in the 1970s, tech stocks in 2000, Brazil, Russia, India, and China (BRIC) funds in the early 2000s, housing in 2008, and Indian power and infra stocks in the late 2000s.

SPACs

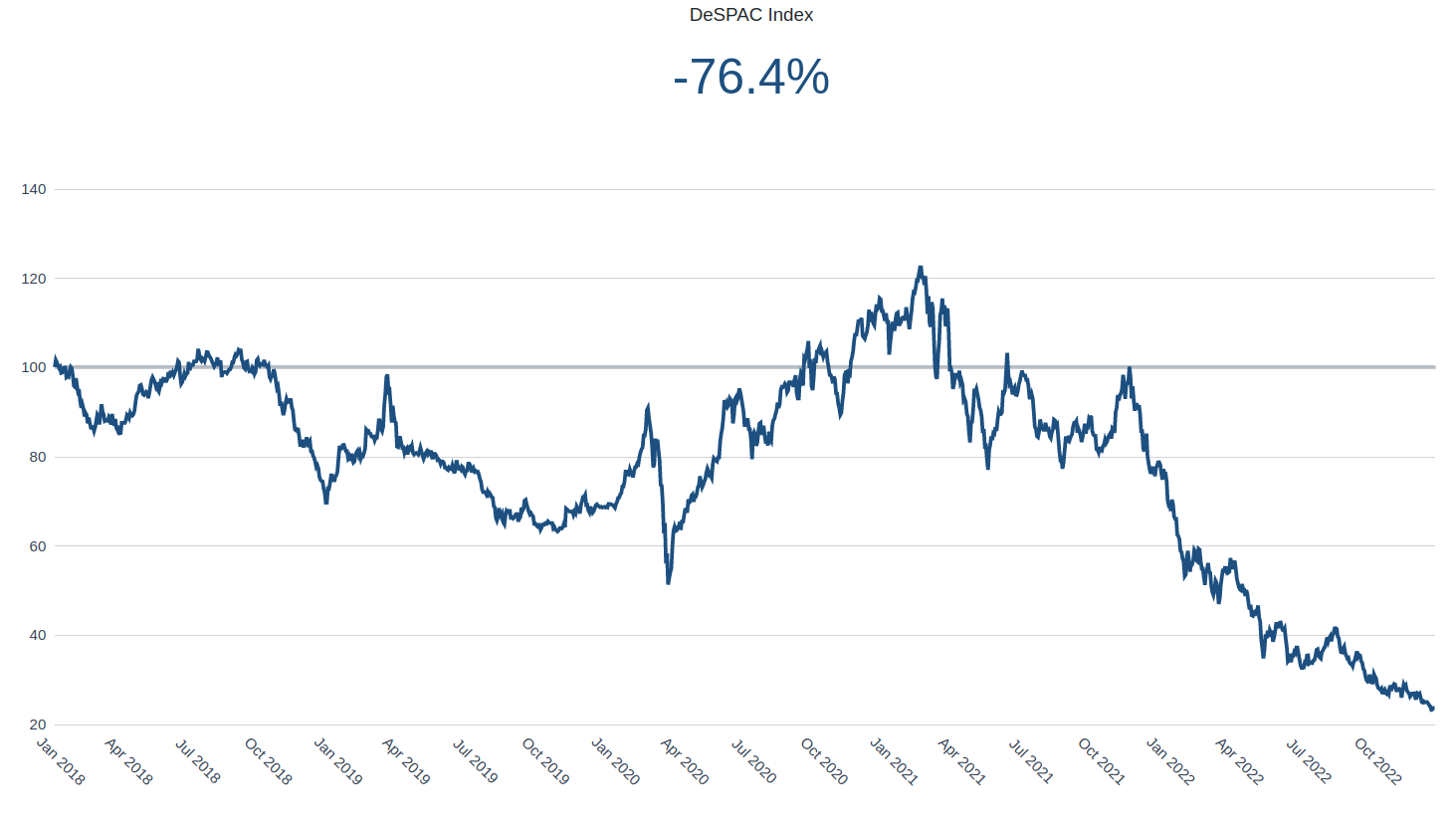

The scariest part of a bull market is when stories trump numbers. It’s that phase in which you can put lipstick on a pig and call it a Chihuahua, and people will believe it. Every bull market has that one pig with lipstick that symbolizes the excess; this time, it was the special purpose acquisition company or SPAC in the United States.

SPACs are popularly known as blank check companies; they are an alternative to IPOs. In a regular IPO, an existing private company lists on the exchanges. But a SPAC raises money first from the public and then tries to acquire or merge with a company. SPACs were last popular during the 2008 crash, but volumes dried up after the crash—they barely raised a billion until 2019. But from 2020-2022, SPACs in the US raised over $250 billion.

SPACs became popular because of regulatory arbitrage. Since they were already listed and trying to acquire a company, the pitch was that they were a much faster way to go public than an IPO with fewer regulatory requirements.

The other advantage SPACs had over IPOs was the liability over future projections. Companies that went public through regular IPOs don’t make forward-looking projections because they can be sued—this reduces the creative BS. But SPACs were protected from any liability. SPACs took advantage of this to make wildly optimistic future growth projections without bothering with trivial things like accuracy and reality. Check out this filing of Donald Trump’s social network, which tried to go public through a SPAC—a fantastic work of fiction.

Then there was the case of flawed incentives. SPACs were wildly lucrative for the promoters. As compensation for putting together a deal, promoters get 20% of the SPAC shares. SPACs became the preferred way to dump the shares of VC-backed loss-making companies like Opendoor and Grab and worthless and downright fraudulent companies like Nikola and Lucid on retail investors.

Nothing, in my view, symbolized the grotesque excess of the last three years more than the SPACs popularized by people like Chamath Palihapitiya—another next Warren Buffett.

Retail investors bought into the stories sold by SPACs and piled into them. Much like GameStop and AMC Entertainment, SPACs were a retail favorite on social media forums like Wall Street Bets.

How did this end?

Pitchbook DeSPAC Index

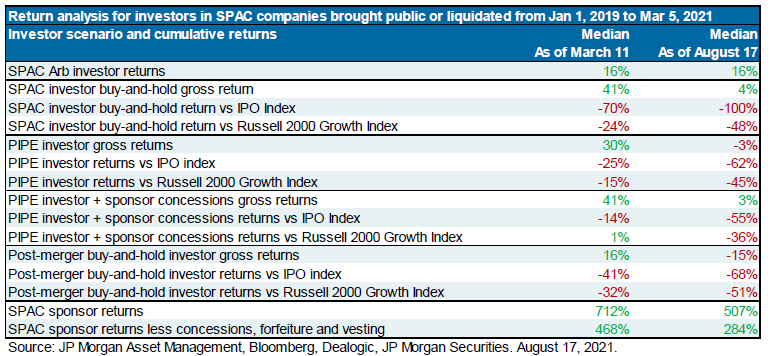

Who made money?

Everyone except retail investors.

Return analysis of SPAC investors

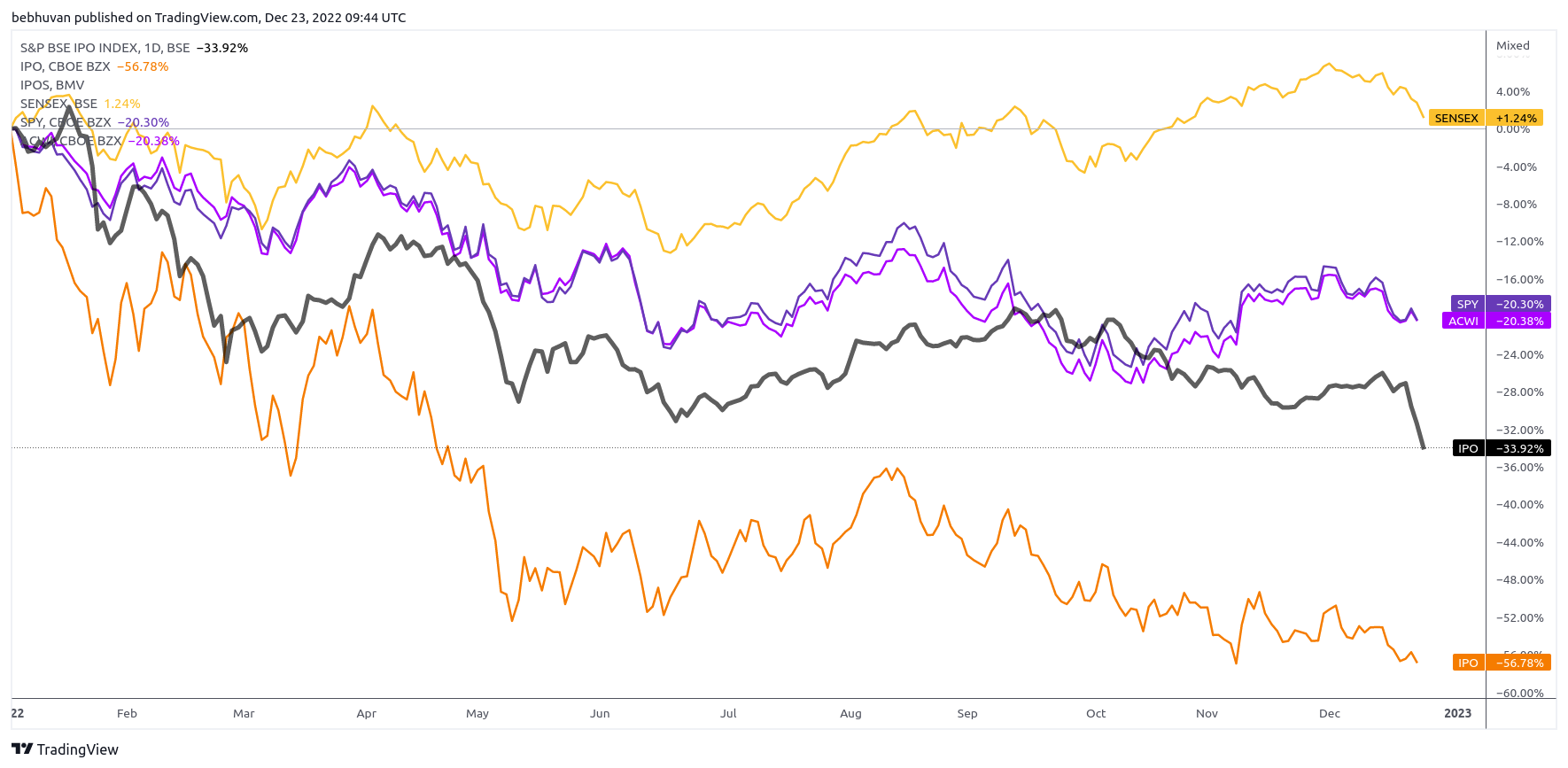

It was the same with IPOs. 2021 saw the highest number of IPOs globally since 2000. Investors thought IPO companies were future megacaps, and listing gains were guaranteed in the last 2-3 years. Investors didn’t bother looking at IPOs and realizing they were terrible investments.

How did it end?

BSE IPO Index, Renaissance US, and international IPO ETFs vs. MSCI ACWI, Sensex, and S&P 500

Keepsakes

Every bull market has its share of generous salespeople selling you the opportunity of a lifetime. Unless you’re careful, you will always be taken for a ride. Incentives are a powerful force that shape human behavior; this is especially true in the financial markets. Whenever you come across a superb story that seems too good to be true, always look at the incentives of the person selling you the story.

No matter how much information and context you have, nothing is more persuasive than what you desperately want or need to be true. And as Daniel Kahneman once wrote, “It is easier to recognize other people’s mistakes than our own.” What makes incentives powerful is not just how they influence other people’s decisions, but how blind we can be to how they impact our own. — Morgan Housel

Chasing shiny objects

The one sad part about writing such blog posts is just how unoriginal investors are—It’s the same old mistakes. One of the oldest mistakes in the book is performance chasing. Unless you are skilled at market timing, it rarely ends well.

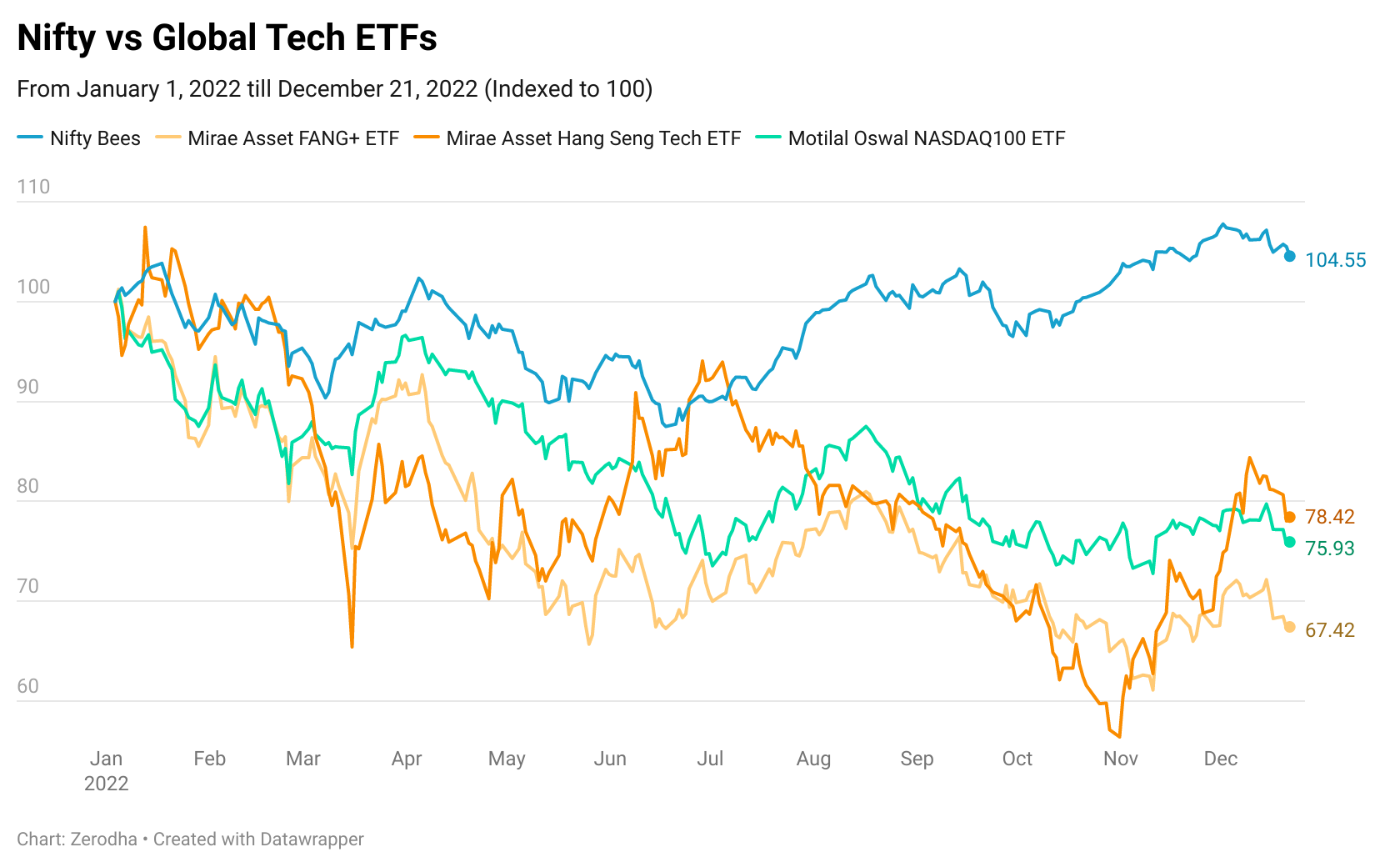

During this bull run, performance chasing was most apparent in thematic and sectoral funds. Take the example of Mirae’s FANG+ ETF and Hang Seng TECH ETF, both of which are down over 20% since inception. I don’t mean to imply that these funds are good or bad, but I’m just using them as an example to highlight the behavior.

These funds, like many other US tech funds, were launched when US markets were rallying sharply—especially tech stocks. Investors rushed in, believing the sales pitches filled with mentions of artificial intelligence, machine learning, deep learning, blockchain, and other meaningless buzzwords. But in hindsight, the launch of these thematic ETFs marked the top.

Performance of Tech ETFs vs. Nifty 50 in 2022

It was the same thing across the world. There are two sides to this story: the AMCs and the investors. Let’s look at the AMCs first. Since we don’t have many thematic ETFs in India, let’s look at the international evidence.

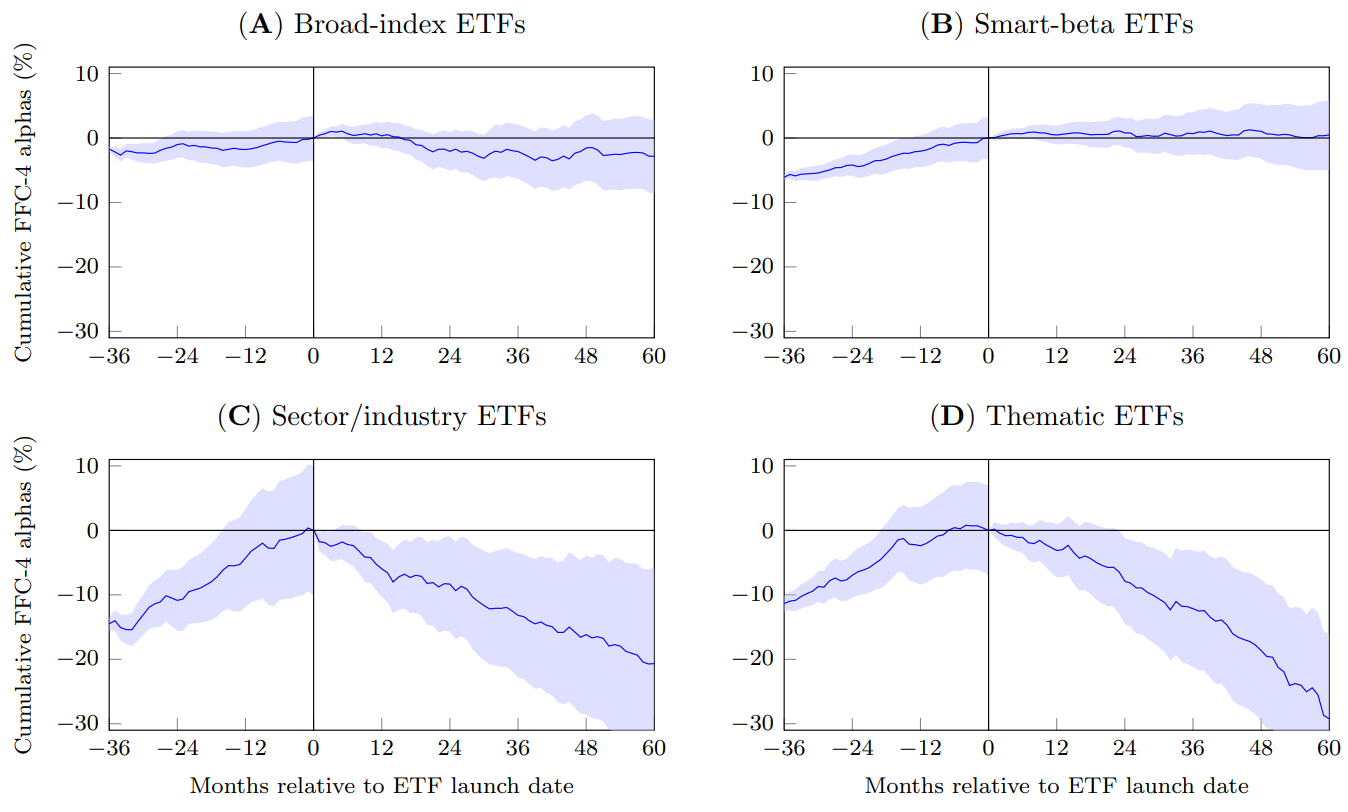

A 2021 study looked at 499 sector and thematic ETFs in the US from 2000 to 2019. The authors found that most sector and thematic ETFs are launched once an index or theme has done well and the valuations of the underlying stocks have peaked. Even AMCs have no real skill in picking themes that can perform well in the future. In the first five years of the launch of these ETFs, they fall by about 30%.

Performance of the ETF indexes pre-and post-ETF launch.

Performance of the indexes underlying newly launched ETFs

According to another Morningstar analysis, as of December 2021, 60% of US thematic funds had shut down, and just 22% of funds had survived and managed to beat a global index.

Investors

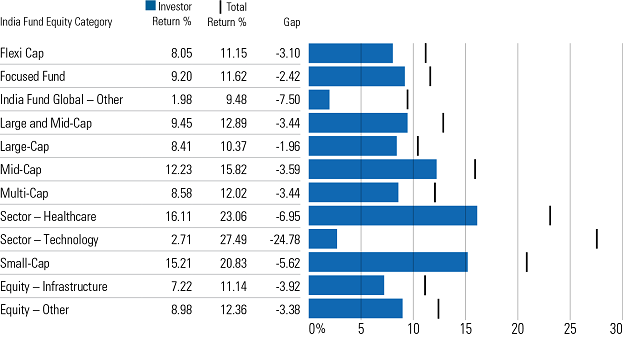

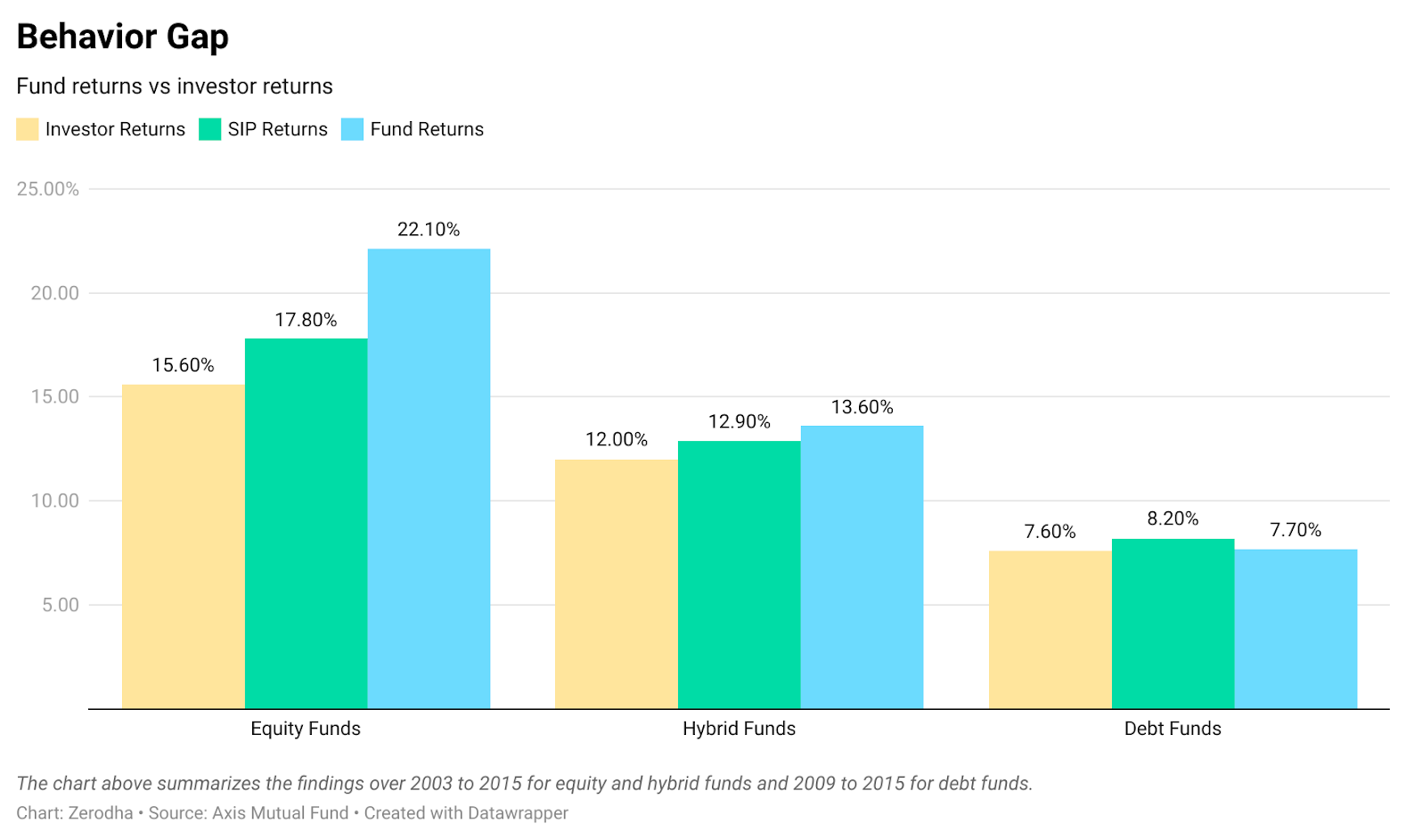

Investors are notorious for performance chasing. Morningstar conducts an annual study comparing the total returns of a fund with the returns of the investors in the fund or the dollar-weighted returns. The data shows that investors consistently earned less than the fund returns because they bought high and sold low.

Look at the image below and notice the difference in returns in thematic funds compared to other categories. The gap in thematic funds is far higher because thematic funds tend to be more volatile than diversified equity funds. Investors buy when a theme has already gone up and exit when the performance inevitably reverses.

Behavior gap in India — Mind the gap study by Morningstar

A study by Axis found the same.

Axis behavior gap study

Studies about the investor behavior gap aren’t without controversy, and the Morningstar study isn’t as egregiously overstated as the DALBAR study. But anecdotally, from what we see, most investors earn far less than what they would’ve made if they were disciplined.

Keepsakes

I’m not saying thematic funds are useless, but rather that the performance is cyclical. Look at this image below, in which I’ve compared broad Nifty indices (in black) to various themes and sectors.

Broad Nifty indices vs. thematic and sector indices

Buy and hold is a terrible strategy in thematic funds. You have to time these themes and sectors to get in and get out at the right time. Needless to say, most investors aren’t skilled enough to pull that off. Your core portfolio should always consist of broadly diversified index or active funds. If you still want to bet on themes and sectors, have a small allocation in your satellite portfolio.

Crypto

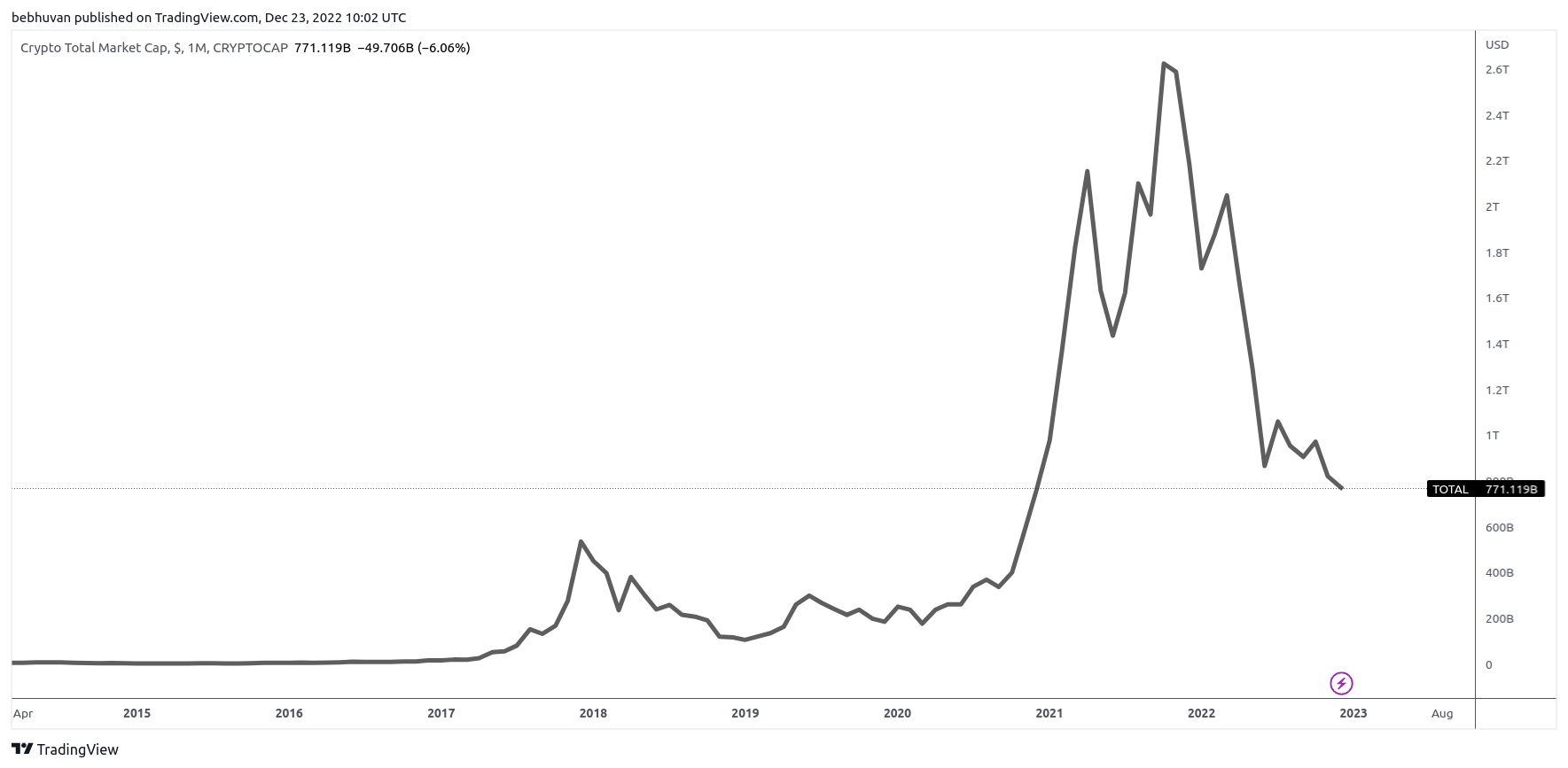

While the stock market had its share of craziness, nothing compares to the madness in the crypto markets. Crypto saw more new users in the last three years than traditional financial markets saw in a decade. Anything that moves 100%-5000% in a year doesn’t need a sales pitch to attract investors.

Cryptocurrency marketcap

Crypto is also a perfect example of stories driving prices more than reality. The true believers think crypto is the solution to everything, from corrupt banks and the debasement of money by central banks to looming hyperinflation.

As things stand today, these are vague and empty promises. After a decade since the origins of crypto, it has very little to show for it in real-life use cases, unless you count gambling—not that there’s anything wrong with that use case. For most investors, crypto = price goes up, and that’s what attracts them. They don’t care whether it is a blockchain or a bicycle chain.

Rising interest rates and inflation have been nothing short of a death knell for crypto and the narratives surrounding it. On the one hand, you have falling prices, and on the other hand, you are seeing the spectacular implosion of some of the biggest players in crypto, from large exchanges to so-called “stablecoins” and everything in between.

From the 10000% rallies in random crypto tokens to the sale of pictures of monkeys for millions, the sheer mania in crypto was stunning.

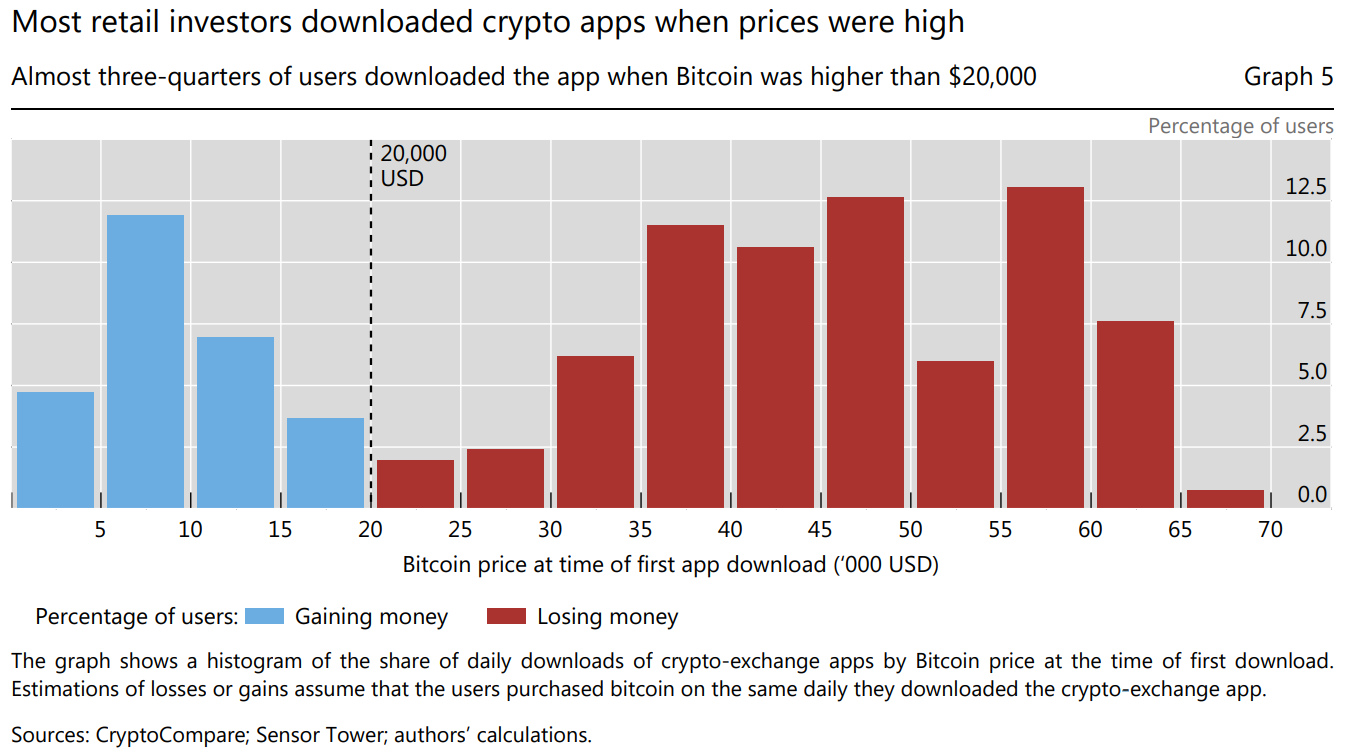

While people say things like XYZ token is still up X thousand percent despite the recent crash, the reality is most people in crypto don’t make money. People buy when something has already gone up and lose money when the tide turns. It’s not just crypto; it’s the same in the stock market.

Most retail investors downloaded crypto apps when prices were high

Most crypto investors don’t make money.

Only a few investors made large gains, while the majority likely lost money

Crypto also became a hotbed of scams. Investors collectively lost tens of billions due to theft, fraud, pumps, and dumps, and investing based on celebrity and influencer endorsements.

Keepsakes

It doesn’t matter if it’s crypto or some other shiny object, it’s hard not to get attracted to something that goes up by 1000%. But betting a large part of your portfolio on assets that are unproven, unregulated, and full of fraud is a sure way to lose money.

Whether it’s crypto or some other new thing, unless you are an insider or have a deep understanding, the only way not to lose everything is to invest only what you can afford. I know this is a cop-out, and losing money, regardless of whether it’s a small or a big sum, hurts, but this is the way.

Pied pipers

Money has the amazing ability to make people do some remarkably dumb things. We saw this with celebrities in the last couple of years, with the likes of Ranveer Singh, Matt Damon, and Kim Kardashian peddling crypto with stupid claims that they were “simple” and “safe.” For better or worse, many people look up to and follow these people. But rather than being role models, they became pied pipers, peddling risky and outright scammy products with reckless abandon. It’s not a stretch to say that people must have lost hundreds of crores by listening to these fools.

The other development I have watched with some trepidation is the rise of influencers; I had written about it earlier. I’m not saying all influencers are bad—some influencers do a brilliant job of spreading financial literacy. However, for every sensible person, there are ten loudmouths saying not only wrong things but also dangerous things in order to gain views and earn money from ads, courses, and sponsorships.

It blows my mind that people spend days researching what mobile phone to buy but invest their hard-earned money based on some random idiot on the internet or some celebrity peddling something for the money.

I get that the thousands of stocks, mutual funds, insurance products, and platforms can be intimidating when you start your personal finance journey. But that’s not an excuse to wing it. Your financial decisions today will impact your retirement 30-40 years later. If you want to spend your retirement as you wish, you must be serious about your finances. It’s not rocket science, either. All it takes is a few good decisions.

But investing isn’t about beating others at their game. It’s about controlling yourself at your own game.

― Benjamin Graham, The Intelligent Investor

Keepsakes

There’s nothing wrong with listening to other people to learn, but it shouldn’t be a shortcut to learning or seeking professional help. But deciding who to listen to is just like picking a stock, you need to have the ability to determine whether an influencer is smart or an idiot.

To judge if someone is making sense, you first need to have a basic understanding of finance. If you don’t want to go through all this hassle, hire a financial advisor. But relying on random people on the internet to make personal finance decisions is a guaranteed way to lose money. Spend 5-10 minutes reading Varsity, and in a few months, you’ll be happy that you did. Remember, there’s no easy or quick money in the markets.

Wisdom of the crowds vs. delusions of the crowd.

“Don’t follow the crowd” is common advice in the markets, and there’s some truth to it. If you have to beat the market, you can’t do what everyone else is doing. This reminds me of an excerpt from a Howard Marks letter that illustrates this point beautifully:

Remember your goal in investing isn’t to earn average returns; you want to do better than average. Thus your thinking has to be better than that of others – both more powerful and at a higher level. Since others may be smart, well-informed and highly computerized, you must find an edge they don’t have. You must think of something they haven’t thought of, see things they miss, or bring insight they don’t possess.

You have to react differently and behave differently. In short, being right may be a necessary condition for investment success, but it won’t be sufficient. You must be more right than others . . . which by definition means your thinking has to be different. . . . For your performance to diverge from the norm, your expectations – and thus your portfolio – have to diverge from the norm, and you have to be more right than the consensus. Different and better: that’s a pretty good description of second-level thinking.

Beating the market and being different from the crowds sound romantic and nice in theory, but it’s not for everyone. In some cases, it’s better to go with the crowd. One such example is a broad market index fund. One reason for owning an index fund is that the market reflects the prices collectively set by millions of traders and investors, and it’s hard to beat that. Does that mean the market is always right? No. But given the evidence that some of the most intelligent investors and institutions haven’t been able to outperform a simple index fund, it’s better to invest assuming that the market is right. By that, I mean investing in broadly diversified low cost index equity and debt mutual funds. Not YOLO’ing into thematic funds and penny stocks.

James Surowiecki, the author of the new book The Wisdom of Crowds, put it succinctly in an interview:

How about investors? Should they embrace the wisdom of the crowd by only buying index funds?

Well, that would be my advice, boring as it sounds. I certainly don’t think the market is always right, but I think it’s very hard to know when it’s wrong, and even harder to make money from that knowledge. So staying with index funds seems like the right strategy to me.

But you also have to be wary of the delusions of the crowd. Episodes like GameStop, crypto, IPOs, and flavor-of-the-moment products are a result of the collective delusions of investors. Knowing when to follow the crowds and when not to is important.

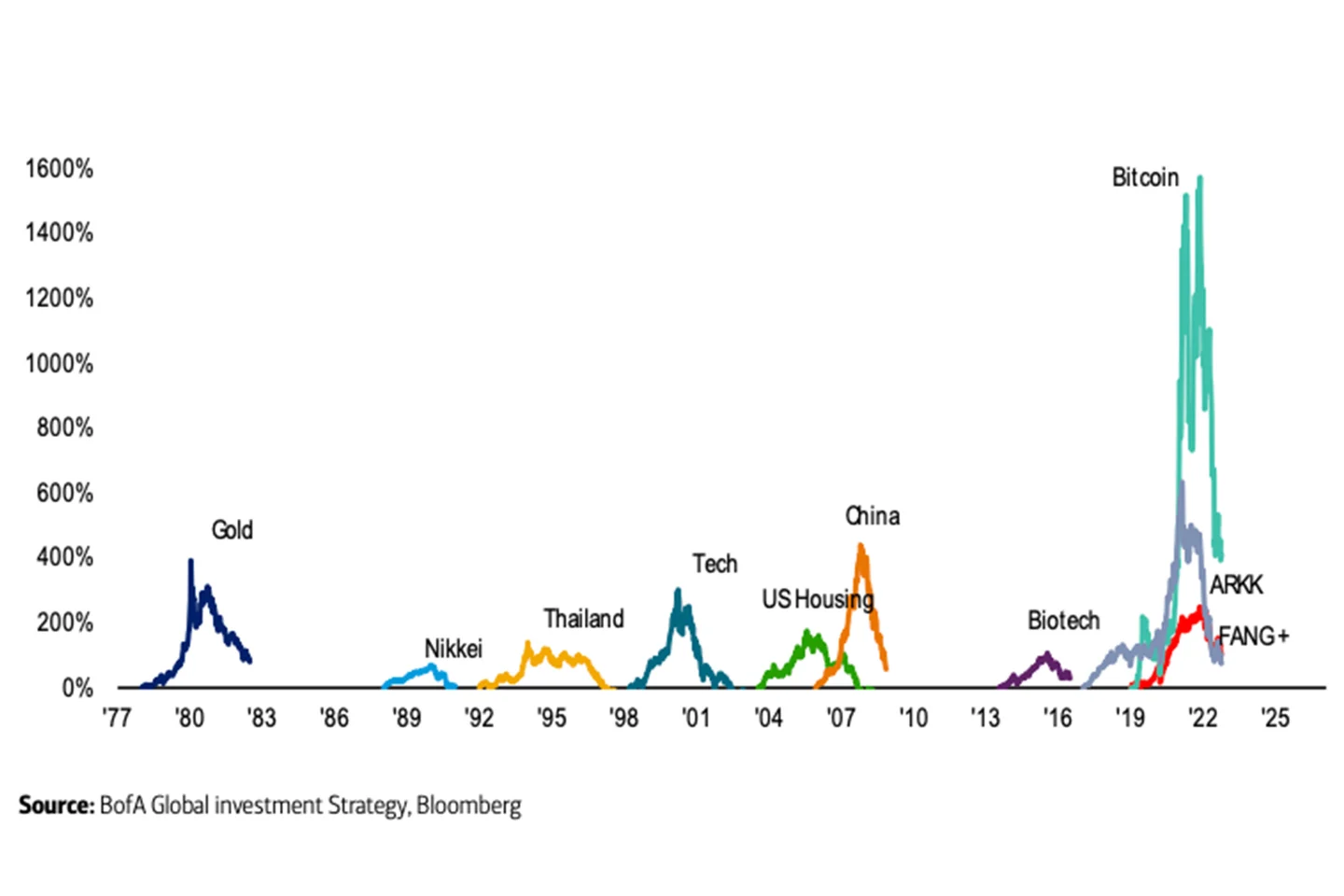

Biggest bubbles

Being comfortable looking like an idiot

At any given point, some stock, sector, theme, or asset class always goes to the moon. Inevitably, either by luck or timing, someone will always be in the right place at the right time and make a lot of money. Of all the human flaws, comparing ourselves to others is among the most destructive and poisonous. We can’t help it because we’re social creatures. Consciously or unconsciously, we constantly determine our self-worth or validate ourselves and our actions by comparing ourselves to others. This is dangerous, both in life and in the markets.

Compared to someone doing well, we’ll always look like idiots, and that’s ok. Most people, who get lucky, rarely keep what they make. The hardest part about investing is being comfortable looking like an idiot in the short term. Investors who are comfortable looking like idiots in the short term will always do well compared to those who act like idiots. Your benchmark is not someone doing well, but the amount of money you need to make to reach your goals. Everything else is either noise or a recipe for ruin.

Standing still while the entire world is going crazy is a superpower.

As long as you have a reasonably diversified portfolio, to quote Cliff Asness, you should hold on to it “like grim death.” The more you tinker with your portfolio, the more you pay in costs and taxes and the less you earn.

Here’s a beautiful excerpt from another old post by Cliff Asness:

One of the secrets of Buffett’s success is that he takes a lot of volatility. In fact, he runs a portfolio with volatility generally well north of the S&P 500.

Furthermore, he produces this by leveraging a portfolio that stand-alone would be less risky than the S&P. There’s nothing wrong with that (in fact we think it’s kind of right). But the real magic skill of his is that despite some fairly horrific and none-too-short relative and absolute return periods, he’s stuck with his style, and his risk level, like grim death.

There’s no sign he’s ever backed off through multiple down years and drawdowns, including a horrific experience during the technology bubble when he underperformed the stock market by 76%.

Speaking of Warren Buffett, this reminds me of all those magazine covers that anoint someone as the “Next Warren Buffett.” From Bill Ackman and Chamath Palihapitiya to Cathie Wood, countless people have been dubbed the “new Buffett,” but they’ve all faded away or, in the case of SBF, jailed!

The next Warren Buffett is the old Warren Buffett.

Next Warren Buffett

Keepsakes

Be very careful who you look up to and what you read because most people will disappoint you. You are better off reading the letters and books of people who’ve survived the markets for decades and been successful, rather than listening to some bull market genius or loudmouth of the moment.

As counterintuitive as it sounds, the deck is stacked in your favor as a retail investor. All you have to do is get a few basics right and behave. Remember this Charlie Munger quote:

All I Want To Know Is Where I’m Going To Die So I’ll Never Go There

So, what did you learn?

Fascinating insights! I appreciate how this post breaks down complex crypto concepts into digestible bits—especially the part about blockchain’s role in reshaping financial systems. It’s incredible to see how fast the space is evolving. Curious to know what you think about emerging trends like tokenized real-world assets or decentralized social platforms. Keep the great content coming!

One of the best informative blog I read. Perfect balance of all the facts in simple words.

Thanks for posting.

Have a great year ahead.

I have never read a piece as outrightly honest and simple as this. We are a family of four-all zerodha members. Thank you for the wonderful insights.

Wow, such wonderful insight..

When is MTF being launched? I’m waiting for it since ages.

Hi Souvik, we are yet to start margin funding or MTF. Will keep you posted.

fantastic read. well done.

Very nice article covering all the aspects in a nutshell. Thank you.

Beautifully written article. This addresses so many of recent failures in few words. Also gives advice on how to navigate the future.

Great read! This is a piece that will be timeless and apt many years into the future. Thank you!