It’s the economy, stupid! US and India’s paths diverge

We love IndiaDataHub’s weekly newsletter, ‘This Week in Data’, which neatly wraps up all major macro data stories for the week. We love it so much, in fact, that we’ve taken it upon ourselves to create a simple, digestible version of their newsletter for those of you that don’t like econ-speak. Think of us as a cover band, reproducing their ideas in our own style. Attribute all insights, here, to IndiaDataHub. All mistakes, of course, are our own.

Is our low inflation good news? Or just an illusion?

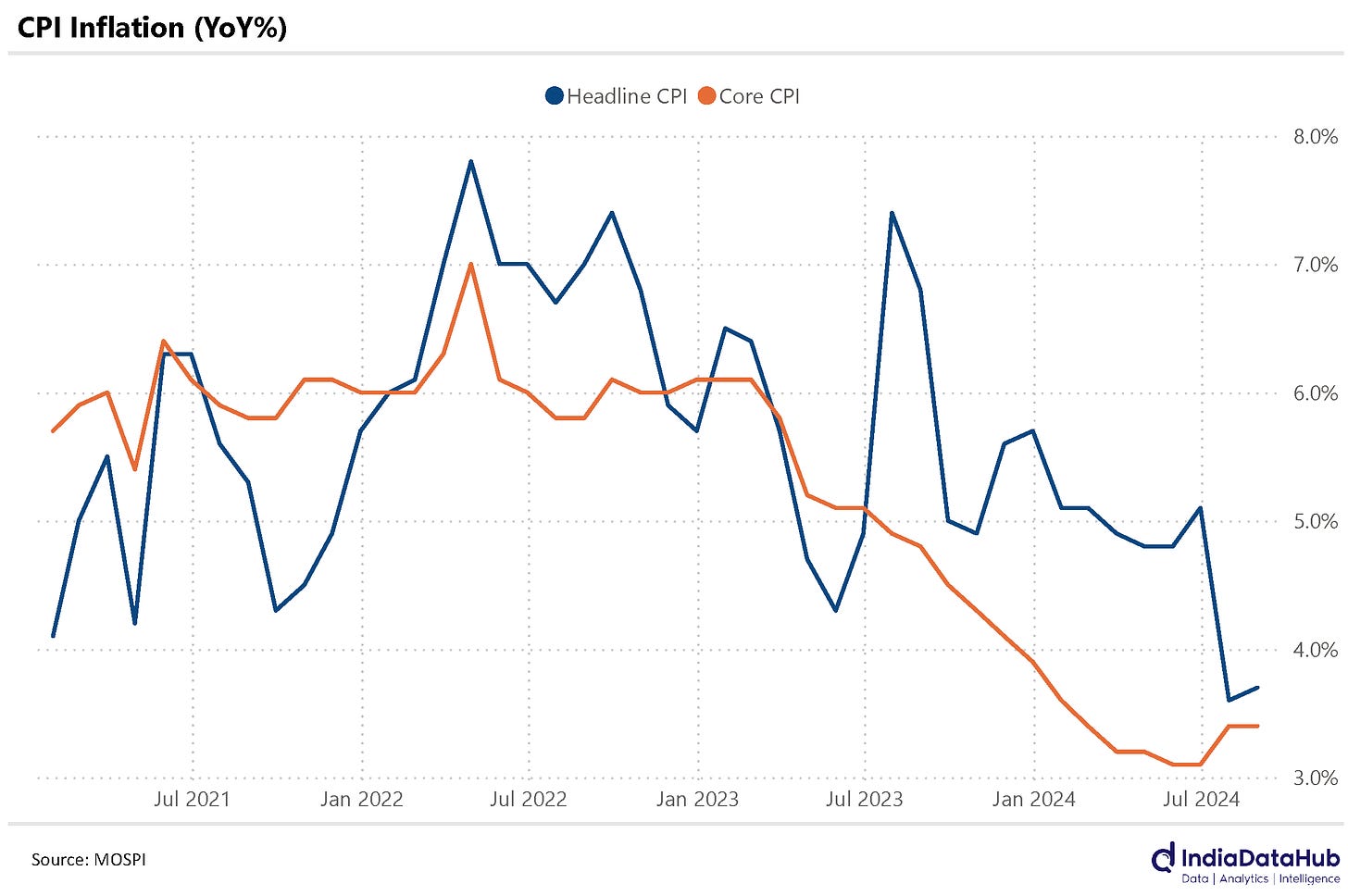

Last month, we talked about some fantastic inflation-related news: for the first time in years, inflation was below the RBI’s target of 4% this July. On the surface, that good run seemed to continue in August. August’s reading — at 3.65% year-on-year — was within a whisker’s breadth of July’s 3.6% year-on-year inflation.

In essence, July marked the first month since 2019 where inflation was where the RBI would want it to be. And then, one month later — August marked the second.

But here’s the problem: this stabilisation in prices might just be an illusion, because at least some of it just comes from ‘base effects’ doing their thing. As we wrote last month:

To calculate inflation, you basically compare prices from a month with prices in the same month from the previous year. For July 2024’s inflation, you compare July 2024 prices with those in July 2023. Now, if July 2023 prices were unreasonably high, prices from July 2024 would look benign in comparison, and you’d get an inflation number that’s deceptively low. That’s the ‘base effect’: when the base number you compare something against is an anomaly, it distorts the whole comparison.

Food was really expensive last August. After all, the year saw a terrible heat-wave, followed by a weak monsoon. Vegetables — and tomatoes in particular — saw massive spikes in prices. Is it any surprise that, compared to those terrible conditions, this year doesn’t look too bad?

On the other hand, ‘core inflation’ — inflation stripped off the effect of those things for which prices fluctuate a lot, like food or petrol — has actually increased by 0.2% since last month.

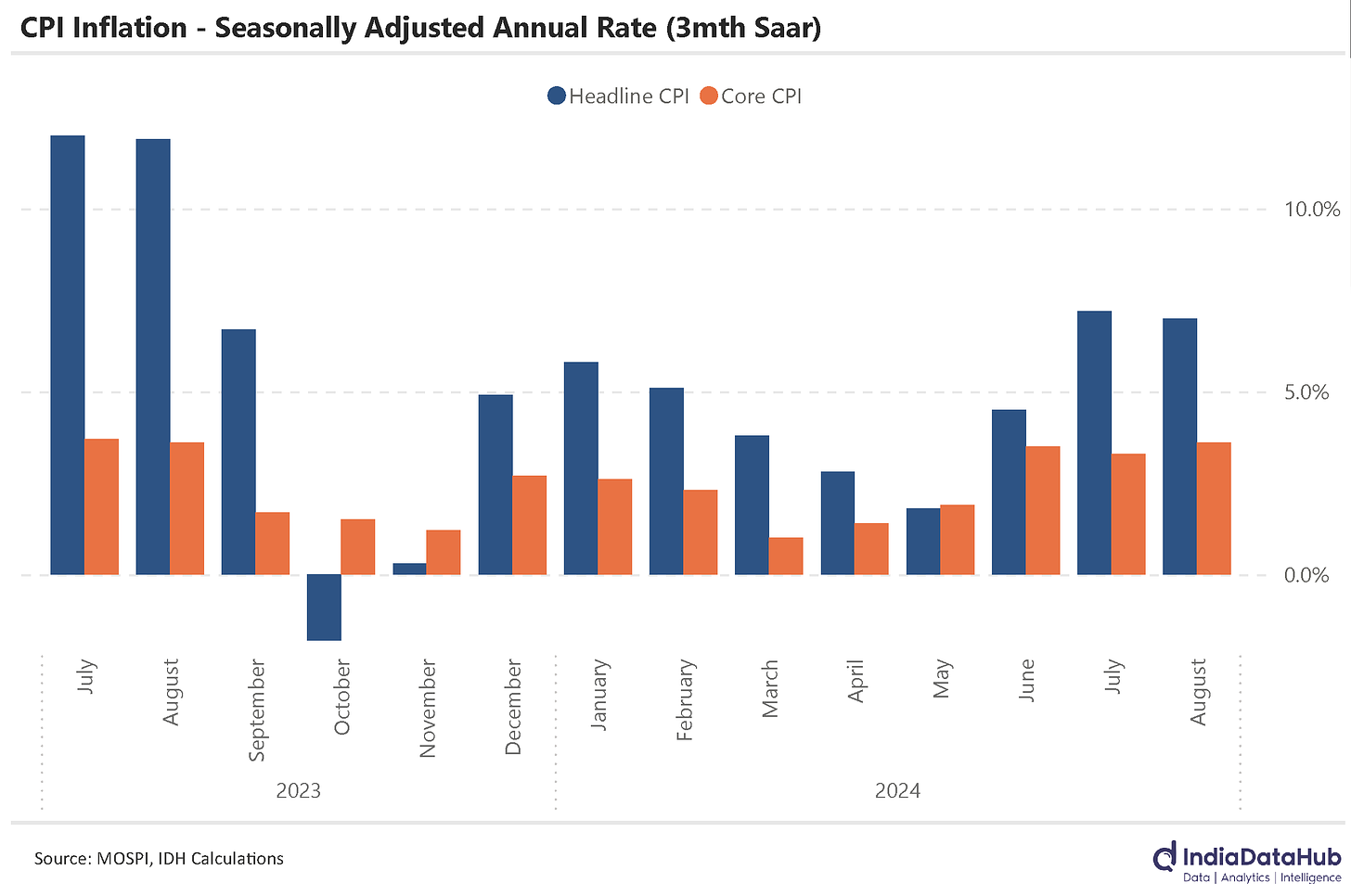

In fact, there is some evidence that inflation might actually be ticking up a little. The good folks IndiaDataHub use some fancy models to clean out the effects of seasonal variations from the data on prices, and then give you a sense of how prices have moved over three month-periods. Here’s what they’ve found: at the moment, as per their model, inflation is the highest it’s been in a year. If this entire year looked like the last three months, our inflation rate would actually be ~7%!

Inflation’s easing up in the US

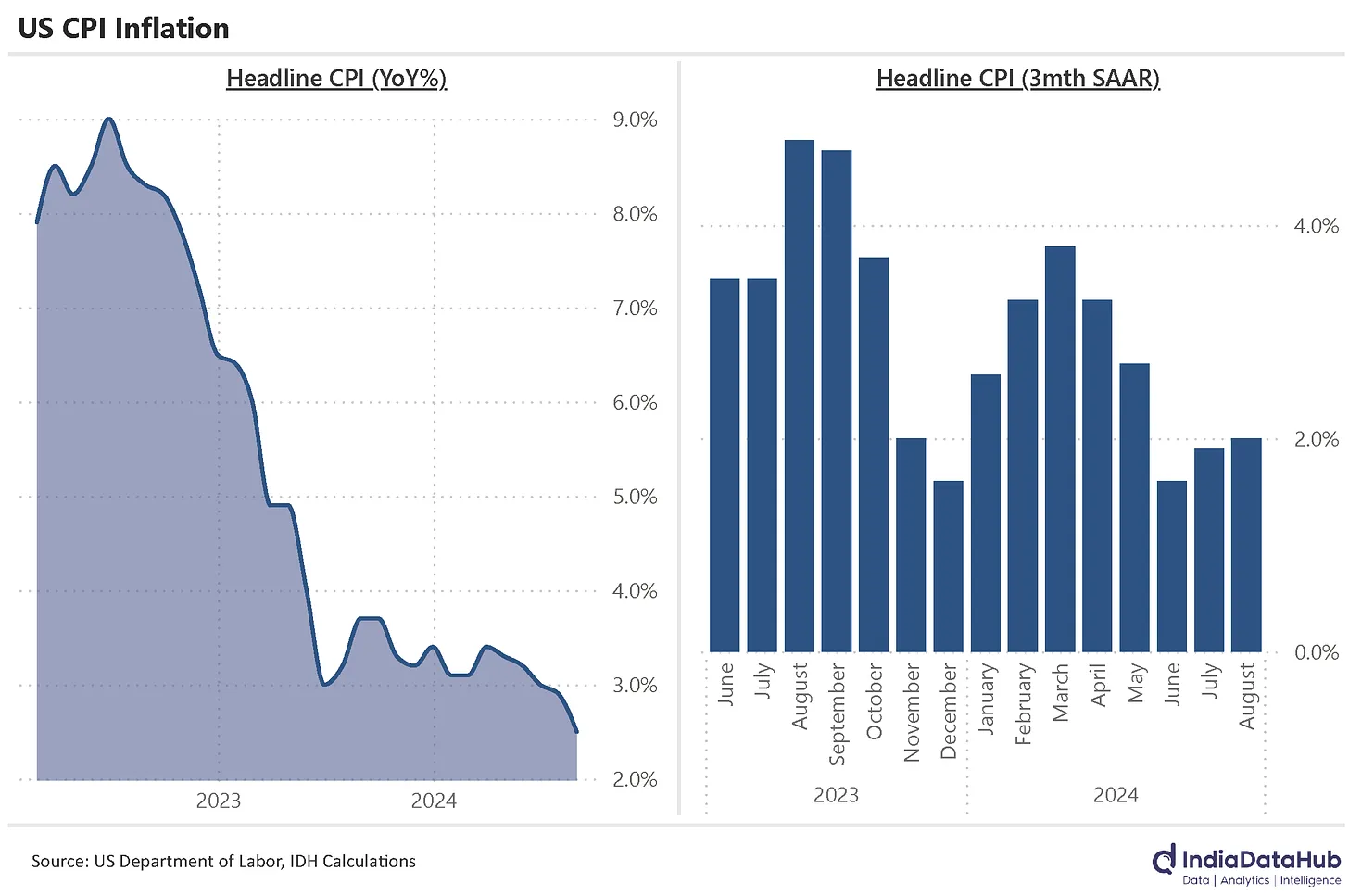

In contrast to India, the United States is actually seeing a sustained fall in inflation. Their inflation dropped to 2.5% year-on-year as per the official data. On top of that, IndiaDataHub’s models show that if the last year looked anything like the last three months, inflation would hover around a mere 2%.

This is where India and America’s trajectories depart. While, on the surface, inflation seems like its coming down dramatically in both countries, American prices have truly flattened off-late, while Indian prices are inching back upwards — hidden under the cover of base effects.

And so, when the central banks of the two countries see inflation data, it suggests very different things, despite superficial similarities. While the US Fed just cut interest rates by a massive 0.5%, the RBI is likely to be a lot more cautious.

What the divergence means

One way of thinking about a rate cut is that it makes money easier to access. If the US Fed cuts rates while RBI keeps things where they are, the US Dollar is available more easily, while nothing changes for the Rupee. Now, the more scarce something is, the higher it is in value, and vice versa. So, if the US Dollar is less scarce while the Rupee stays the same, the US Dollar may actually fall in value compared to the Rupee.

Now, imagine: you’re an Indian business that is ‘exposed’ to Dollars. Maybe all your clients are located abroad, for instance, and you charge them in Dollars, which your bank converts into Rupees for you. If you don’t want your business to go kaput overnight, you’d probably like something that saves you from the risk of US Dollars suddenly going down in value, relative to the Rupee.

That ‘something’ is a ‘forward contract’. A forward contract lets you book an exchange rate for when you’re exchanging currencies in the future. In return, you pay a small premium to book this rate. As a change in the USD-INR exchange rate becomes more likely, those premiums are beginning to go up. Early in September, the premium on 6-month forward contracts was at 1.7% — far higher than June’s 1.2%. This is the highest this rate has been since October last year.

Now, historically, interest rates in the US have been much lower than in India. And that’s reflected in forward premiums. Since 2011, for instance, the average premium was 5% — well higher than it is now. It’s only after COVID-era rate hikes that the two came close together. As a result, over this period, forward premiums have been unusually low. This graph is a good illustration of how they’ve fallen:

If things return to how they were before COVID struck, and US and Indian interest rates diverge again, you’ll probably see forward premiums peak again as well.

Tepid August

August was the month temperatures came down in a lot of India. But it looks like a lot of businesses weren’t feeling so hot either.

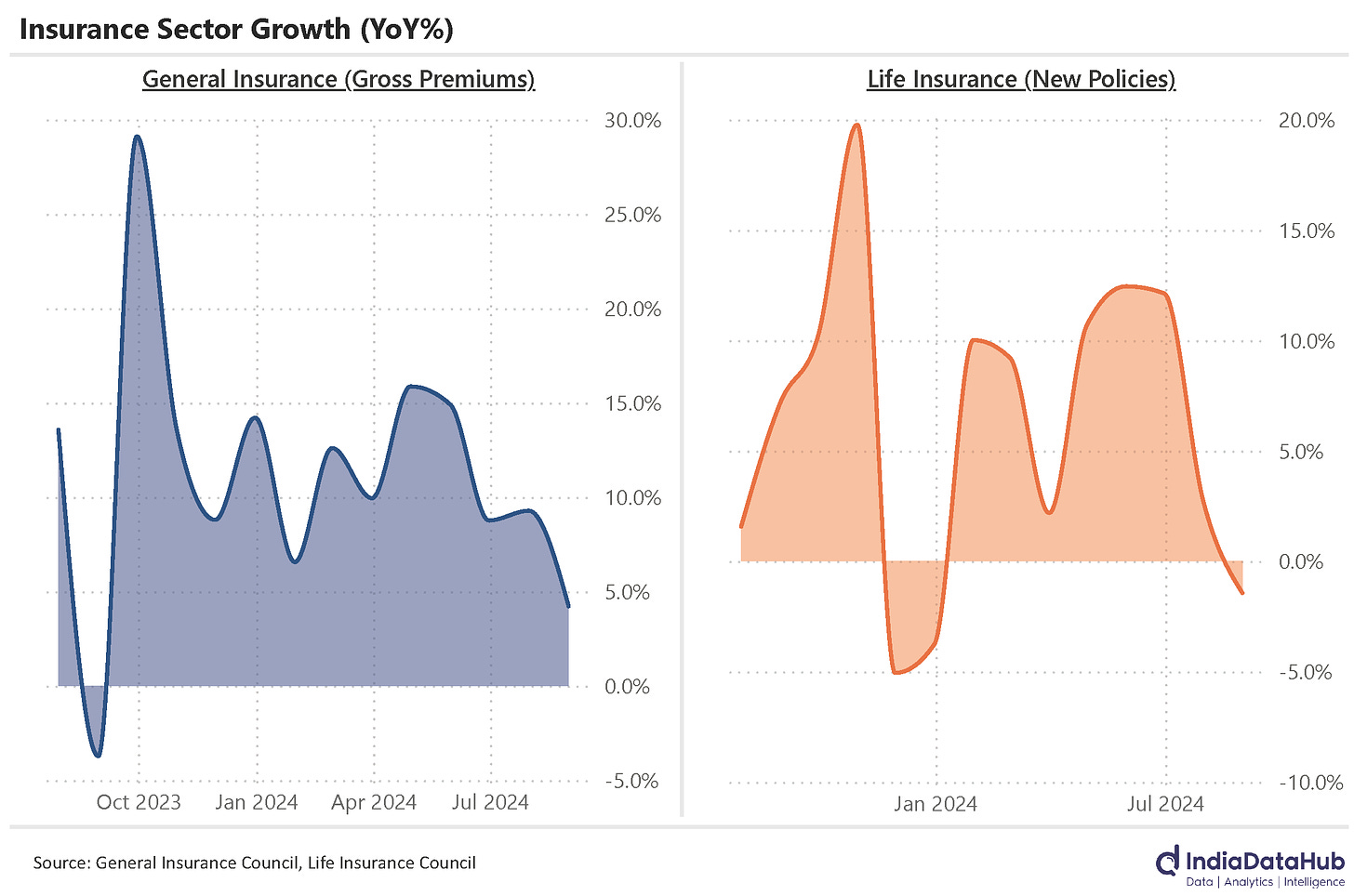

Take insurance.

Our insurance industry, as we discussed last month, is slowing down. This August, it saw its poorest growth in a year — since August last year, in fact. Even when compared to an already weak month, year-on-year, August saw growth of a mere 4%. Essentially, the fact that we see growth at all this August is just an illusion created by base effects.

The new business premiums of the life insurance industry look decent, growing at 20% year-on-year. But this, too, comes from base effects. Last August had exceptionally bad new business premiums. They’d fallen by 18% year-on-year, in fact. Once you factor that in, this August no longer looks too great. Meanwhile, the actual number of policies life insurers sold has actually declined, even compared to the weak business they did last August.

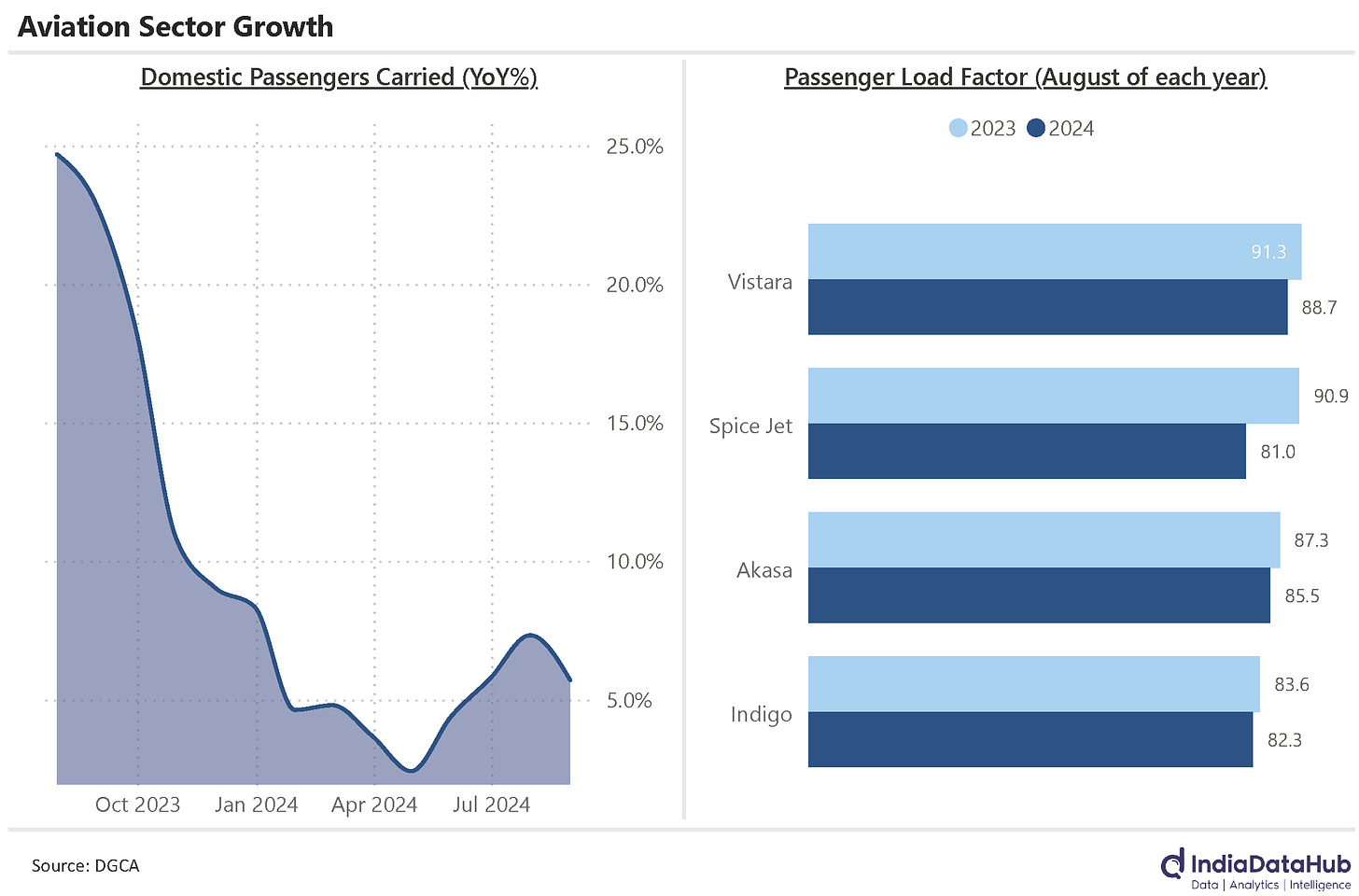

Airlines, too, are facing a turbulent time.

This August, India’s aviation industry carried just just 5.7% more people than it did in August last year. This is despite the fact that all the big airlines have been adding flights. As a result, their ‘passenger load factor’ (PLF) — which measures how full flights are — has gone down year-on-year. This is a broader trend, actually. There’s been a consistent drop in PLFs over the last five months.

Clearly, airlines are adding seats faster than they’re finding people to fill them.

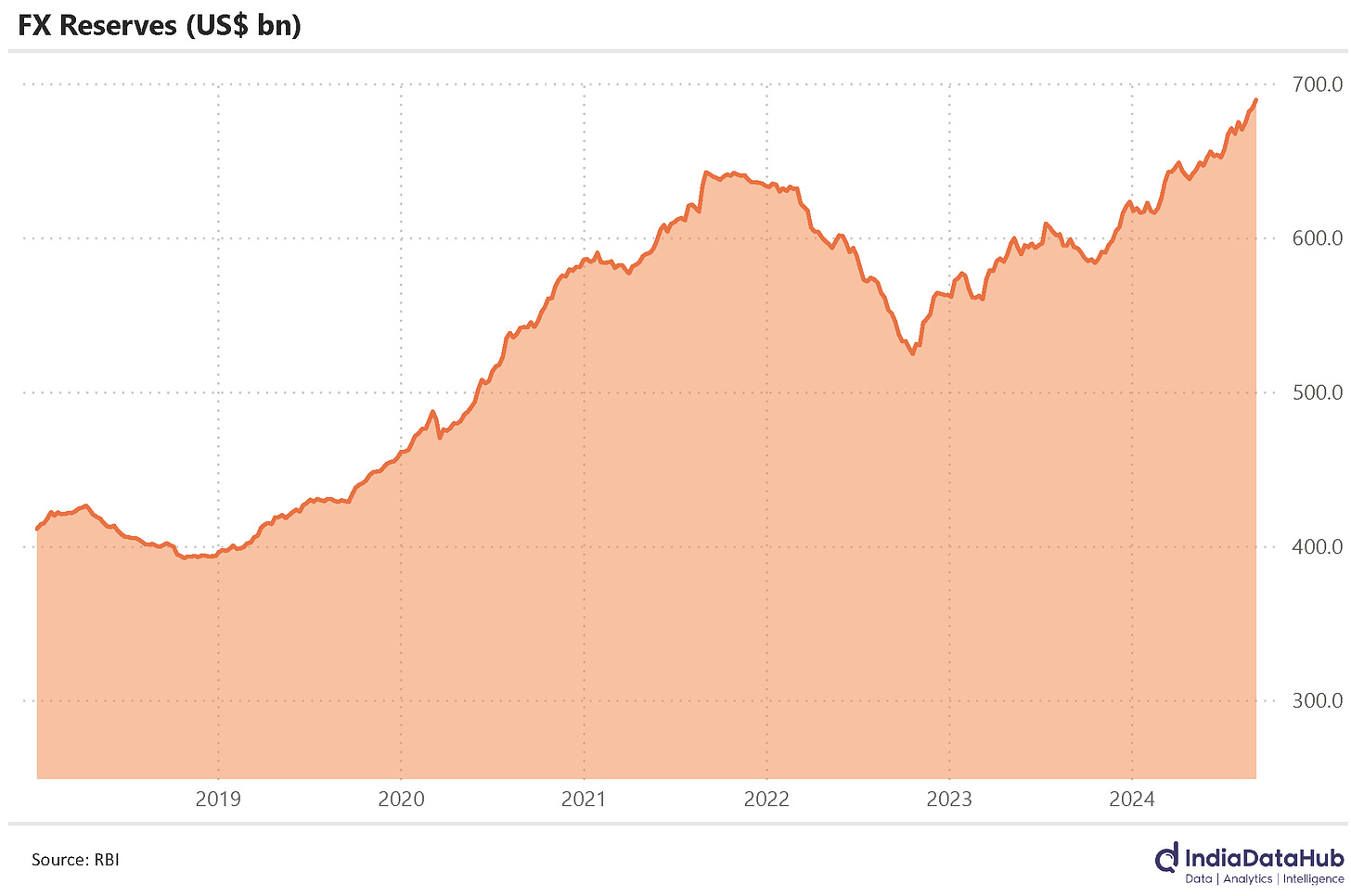

India’s highest ever forex count!

India’s forex reserves continue to set records. On 6th September, our reserves hit US$ 689 billion — the highest they’ve ever been, so far.

US$ 689 billion can buy 11 months worth of India’s imports, in a worst case scenario where no more money comes in. It can pay off every single Dollar of debt we’ve taken. With reserves this high, we can breathe easy in the knowledge that we won’t simply crumble in the face of an external shock.

That’s definitely comforting in a time like today, when the world economy’s run off-kilter for the last few years. Volatility may just be around the corner, and it’s good to know that we can survive it.

The cutting phase is underway

The European Central Bank has cut interest rates: slashing rates on deposits by 0.25%, to 3.5%, and on refinancing by 0.6%, to 3.65%. This was followed by a massive 0.5% slash in interest rates by the US Fed.

Clearly, rate cuts are the flavour of the season!

That’s all for the week, folks!

Good