16.1 – Anchoring Bias

I’ve spent close to about 13 years participating in the stock markets. I’ve spent these years in various capacities – as a trader, investor, broker, money manager, analyst etc. I’ve had my fair share of happiness and regrets in the markets and I’ve learned a lot (still continue to learn) during these years. I’ve realized that happiness and regret may not always be a linked to the outcome of a trade that you’ve taken up – you feel happy when you make a profit and regret when the trade results in a loss. These feelings can also manifest out of trades that you’ve not taken up. Let me tell you one of my biggest regrets in the stock markets till date.

I the recent years, August / Sept 2013 was one of the greatest times to build a long-term portfolio from scratch. Stocks of great business were available at throwaway valuations. I was fortunate enough to be aware of this situation in the market and I was really busy structuring my equity portfolio. I had a tough time selecting stocks to include in my portfolio. Tough time in the sense that there were too many opportunities to choose from. In fact, this is what a bear market does to you – it spoils you for choices.

I included few stocks in the portfolio (which I still continue to hold) and I let go of many stocks including MRF, Bajaj Finserve etc. The decision to let go of these stocks was based on the fact that I perceived investing in other stocks more attractive. Stocks like MRF and Bajaj Finserve have performed phenomenally well, but then I don’t regret my decision.

However, the decision to not invest in Sundaram Clayton Limited pains my heart – I consider this as one of the biggest regrets.

Take a look at this chart –

I did my usual stock research and was convinced that the stock was a great buy. I’ve circled the area around which I wanted to buy – roughly around 270 per stock. Given that it was a bear market, I was kind of rigid on the price to buy – 270 or lower.

The stock price moved slightly higher to about 280, but I did not budge. I waited. The stock price moved to 290, I waited. A couple of days later, the stock shot to 310 and I remember convincing myself – the stock will retrace back to 270 considering that it was a bear market. After all, I was in no mood to pay a 15% ‘premium’ on a price that I perceived as ‘the best price’.

As you may have guessed, 270 never occurred and I never got to buy this stock, and here is what really happened to the stock later on –

I’ve circled the 270 price mark again for your reference, which is where my so-called ‘price conflict’ occurred – all in my mind!

I probably missed out one of the greatest investment opportunity in my life, and all thanks to the games my mind played with me. More formally, what really prevented me from buying Sundaram Clayton can be attributable to a notorious trading bias called ‘The Anchoring Bias’.

I was looking up on Wikipedia for ‘Anchoring Bias’, and I discovered a new term for the same – it is also called ‘Focalism’. Anchoring bias belongs to a group of biases grouped under ‘Cognitive Biases’. Cognitive bias is a systematic error in our thinking that affects the way human beings make their decisions or judgments. Anchoring Bias leads the list of cognitive biases.

Under the influence of Anchoring Bias, we tend to get fixated to the first level of information we get. For example, in my very own case, the first price I saw on the terminal was 270 (for Sundaram Clayton), and I was fixed to that price. Here 270, formed a price anchor.

Think about your own trading situations – how many times you may have missed placing that buy order or a stop loss order because the price that you perceived as ‘right’ never occurred, only to later see the stock perform exactly the way you thought it would. After all, in most of these situations, the price difference between what we perceived as right and the one available in the markets would be marginal – few Rupees probably, but then our minds just do not permit us to go ahead.

Like any other biases, there is no real cure for anchoring bias. The only real cure is to be aware of it and adopt critical thinking in your approach to markets.

16.2 – Functional Fixedness

This is yet another cognitive biases – although you will not read much about this particular bias in the trading world. However, I think it kind of has its impact on traders, especially the ones who trade derivatives.

Let me give you a generic explanation of ‘functional fixedness’ bias and then relate this to the trading world.

There is juice shop near my office which I frequent for a glass of fresh juice. On one of those visits, I asked for my regular orange juice, but the guy at the juice shop was busy fixing the mixer jar. The handle of the jar was loose and had to be fixed. The guy was busy trying to find a screwdriver to tighten the mixer’s handle. Unable to find one, he was kind of clueless on how to proceed.

At the same time, his colleague walked in and learned about the issue. He simply picked up a spoon which was lying around, used the other end of the spoon (which basically has a flat side) as a makeshift screwdriver and tightened the jar. Problem solved, juice was served.

This is functional fixedness at its best. Functional Fixedness is a cognitive bias that limits a person to using an object only in the way it is traditionally used. We assign tasks to objects and we live with that rigidity all our lives. For example – we have all grown up with the notion that we only need to look for a screwdriver to tighten screws, without which one cannot. However, a simple spoon can do the same job! One has to start thinking out of the box to solve problems in unconventional ways.

There are few ways in which Functional Fixedness limits our way of thinking when it comes trading. Let me start with a classic example.

Assume you have Rs.100,000/- in your trading account. You have identified a great trading opportunity in Nifty and you expect to hold onto the trade for the next 2 or 3 days. Since you intend to hold this trade overnight, you have to opt for a ‘NRML’, product type. The typical margin blocked for this trade would be about Rs.65,000/-.

So you take the trade around 3:20 PM and carry the position forward. End of the day 65K would be blocked as margin and 45K would be your available balance, which can be utilized toward another trade the next day.

The next day market opens, Nifty starts moving in the direction that you expect it to move. You are happy with the way things are going.

Now, assume that you spot a great intraday opportunity, TCS stock futures, which requires you to pay an MIS margin of 60K. What will you do? The available margin is 45K, you’d fall short of 15K right? Therefore you cannot take the TCS intraday trade.

Now, this is where the functional fixedness is playing the culprit. We consider the NRML (margins blocked for overnight positions) as ‘margins blocked’, and we invariably forget about this capital until we square off the position.

With a little bit of ‘out of the box’, thinking (and some efforts) we can, in fact, continue to hold the overnight position plus take up the intraday opportunity.

Here is how it would work –

- At the start of the day, you have available margin of 45K, short of 15K to take up the intraday trade

- Convert the NRML Nifty position to MIS. When you do this, from the 65k that was blocked, nearly 39K would be freed up – as MIS for Nifty is about 26K

- You now have 45K + 39K or 84K free cash for the day

- With 84K, you can easily place an MIS order, blocking 60K. You will still have 14k as available margin

- End of the day, square off the MIS stock futures trade – remember this was an intraday trade

- Your available margin goes up to 84K

- Convert back the MIS Nifty trade to NRML and carry forward the position

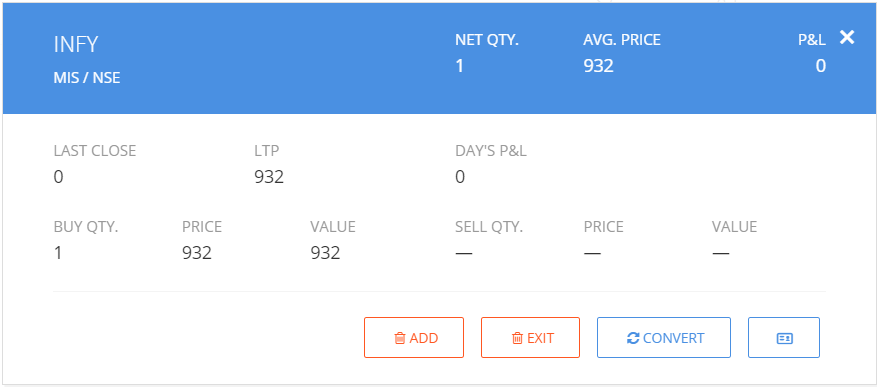

The snapshot below shows you how you can do this on Kite –

16.3 – Confirmation Bias

Have a look at the Tata Motor’s below

I’ve marked few important points on this chart –

- The stock is around 430 today

- 430 seems to be a price action zone considering the past price reactions

- Sometime in early August, the price cracked through 430 and declined to 370

- The stock price stabilized around 370, quite evident with the double/triple bottom formation

- Since 370, the price has consistently trended up, all the way back to 430, which is where the current stock price is

Considering the above, guess the stock is all primed up for an up move – don’t you think so?

Also, keeping that analysis in the back of our mind how would you view this piece of news which made the headlines earlier today –

Chances are that you will views this news piece as a trigger for Tata Motors to edge higher and therefore support your logic of buying the stock. However, in reality, the fundamental news may not really be a great trigger to drive the stock price higher. But then, at a subconscious level, you start looking for pieces of information that support your view. In other words, when you form a trading opinion, no matter what happens, you only look and assimilate information that supports your view. Your brain somehow does not allow you to pay attention to information that does not support your original contention.

This is called the ‘Confirmation Bias’.

Critical reasoning is the key to overcome the confirmation bias. You got to ask yourself – so what?

16.4 – Attribution Bias

This one is funny.

How many times have you had a winning trade and ended up feeling proud of your analysis? Perhaps you bought an option and it gained 100% on the premium or maybe you bought a stock and saw it appreciate multifold.

Every time you make a profit – it is somehow because of your smart trading logic, and therefore you give yourself a pat on your back. But what about the times you’ve made a loss? How do you deal with it?

Coming from a stockbroking industry, let me tell you one thing – when people make a loss, they invariably attribute this as broker’s fault and not really their own. Traders find all sorts of reasons to blame the broker – broker’s system failed, charts not loading, orders are slow, and what not.

Everything thing is attributable to someone else’s mistake (mainly the broker) and not really the subpar analysis in the first place!

This is called the ‘Attribution Bias’ and people succumb to it owing to acknowledge the fact that they are wrong. One way to overcome the attribution bias is to maintain a trading journal and make entries which reason outs why you’ve entered into a trade and why you decided to close the trade. These journal entries over time give you a great insight into your own trading behavior.

16.5 – And it’s a wrap!

The list of these biases gets endless. Naturally, covering all of them would be hard. However, here is what I’ll do – I’ll keep this chapter open and I will continue to add more biases as and when I discover them myself ☺

With this chapter, I’d like to close this module on Risk and Trading Psychology. As usual, I hope you enjoyed reading this module, as much as I enjoyed writing it for you all.

Keep those comments coming!

Key takeaway from this chapter

- Anchoring Bias can be quite notorious – tricks the trader/investor to anchor them to the first piece of information

- Anchoring Bias may lead you to miss great opportunities

- Functional Fixedness fixes your opinion on the utility of the tools, restricts your imagination

- One can overcome functional fixedness by practicing ‘out of the box’ thinking approach

- Confirmation bias makes you seek information (or tricks you to assimilate information) which can support your original hypothesis

- In a typical trading world, traders attribute losses to problems in the outside works and not really because of subpar analysis

- Attribution Bias can be overcome by maintaining a trading journal

You were talking about how you missed out on Sundaram Clayton as an investment. Would you be able to share what factors/parameters you were considering while researching this stock and how you got reasonable assurance that the stock is a good long-term investment?

Pavan, it was basic fundamental analysis of business, basic valuations, and an overall understanding of what was happening in the auto ancillary segment. No rocket science 🙂

Hello Karthik,

Hope you are doing good .

I have an idea/concept of tech based risk management. A Risk Management console in Kite -A feature that could reshape how traders interact with capital, emotion, and habit.

can you please let me know if I can share my idea with you directly and how can I do reach out to you ?

Vinay, please do share your thought on this via a ticket and the support agents will share it with the respective team.

Nice lessons and easy readability. Congrats!! Can you include the Optimization with \’Minimum variance port weights\’?

Thanks Yasaswi, have discussed it here – https://zerodha.com/varsity/module/risk-management/

Thanks for the valuable insights Sir !!

When it comes to learning without any confusion, Varsity has been my goto place for past two and half years.

Sincere Regards !

Thanks for letting us know, happy learning 🙂

Sir , I mean to say is Zerodha charging something for chart like trading view

No, there is no separate charge for this. If you have access to Kite, then you have access to the charting software.

sir , are they free of cost and they charge ?

What are you referring to?

sir , yesterday i want to take downside trade in nifty future as it was a great opportunity of 200-300 points as am a swing trader , but the investing.com chart did not upload the chart , broker s app was very slow , was not showing price . somehow and other i took trade at 20 points premium price . although the trade was successful getting around 200 points but often happened to me , sometimes broker remains at fault.

second thing , I want to trade with zerodha app , plz suggest me is there any chart of zerodha like I see in investing .com ?

We do have two charts engines integrated within Kite – ChartIQ and Tradingview. Both are excellent charting platforms and gives you enough and more charting utilities.

In my second question, what I meant was…that, if after consuming (or using) my collateral funds, my \’EQUITY Collateral\’ in the \’FUNDS\’ section\’ of zerodha will show \’0/- (zero)\’ ,right….? so, if now I add 100000/- cash in my \’KITE account fund\’ , will my collateral of same amount be released automatically……?

I Hope this time I\’m sounding more clear than before.

Sir,

I\’ve pledged \’liquidbees\’, and got collateral margin(cash equivalent) of \’100000/-\’ against it.

Now, next day I bought some shares of some company \’XYZ\’ of amount \’100000/-\’ with that collateral.

1. Can I pledge these \’XYZ\’s shares too?

2. As I have bought the shares from collateral, now I should have zero collateral balance, right…? so to gain collateral of same amount (100000/-) shall I have to add funds of amount 100000/- cash to my KITE account

3. Can I Sell these \’XYZ\’ shares the next day after buying ?

4. Can I unpledge my \’Pledged LIQUIDBEES\’ without adding cash?

Must say Mr. Karthik , absolute gems of knowledge you have presented here , it can vastly help one to gain insights which will help in avoiding the costly mistakes . Thanks a lot.

Happy learning 🙂

Your effort to bring forward these modules is much appreciated sir, Thank you.

Happy learning, Andrew!

Sir, how can we control over trading in intraday

By having a strict approach to capital management and a very tight trading discipline. I understand this is easier said than done, so your individual persona as a trader matters, Vivek. How well you can control yourself is what matters 🙂

last query is you said in \”Functional Fixedness \”convert nifty NRML to MIS , and after square off TCS future then convert again nifty MIS to NRML, Please explain that if we convert nifty NRML to MIS next day and TCS future is also in MIS then how to convert again nifty MIS to NRML after square off TCS future at the end of the day, will nifty future should not be square off as both are traded in same day.

Or may be we should convert nifty MIS to NRML before market closes at 3:30 pm and after square off TCS future,

Please correct me and explain me a little bit of confusion when to convert that.

Yes, this was discussed keeping intraday in perspective.

Also in this line — \”With 84K, you can easily place an MIS order, blocking 60K. You will still have 14k as available margin\”

From 84k ,if 60k is margin for MIS then it should be 24k as available margin instead of 14k.

Man, dont know how these typos happened, will fix 🙂

In Functional Fixedness topic you assume the capital 1 lakh in example in which for nifty trade 65000 would be margin blocked , and remaining available balance is 45000, but in 1 lakh if 65k deduct as margin then remaining balance should be 35000 , and above calculation is based on 45k little bit confused , please correct me if i am wrong?

Ah, a typo. But the concept remains the same.

Hello! I spent some time on book you suggested- Ganapaty Vidyamurthy’s ‘Pair trading’ book. As you said this topic is deep. I am getting issues while understanding some concepts from the book. Can you suggest me any books where I can first clear my mathematical/statistical concepts or whatever necessary before diving in quantitative trading concepts?

It will be very helpful for me

Maybe you should start with Schaum series for basic mathematics then.

Thanks a lot! Will certainly check that!

Sure. Good luck!

Hello! Content you have posted on whole Varsity is only one of it\’s kind I will say.

I was till now, trading in markets based on technical analysis and making & loosing money. I just played cost to cost game. but since I read options theory, strategies, trading systems and this risk management module, I am getting one feeling that quantitative approach to trading as well as risk management is what makes you better trader. Some risk that are bound tightly to markets we can\’t remove but we can make sure that we are doing it correct from our side at least. Enough words w.r.t my tiny knowledge of markets!

Straight to questions-

1. How do I become quant trader? What should be my path ahead assuming I have only high school level statistic/mathematics knowledge?

2. Where to start learning it? Books/courses/certifications?

3. Where is quantitative trading more suitable/profitable? Cash market or derivative market?

Please elaborate on it as much as you can. I am 21 and I can easily use coming multiple years learning and practicing these things!

Also I just want to know do institutional people focus more on quantitative approach rather than traditional technical approach? 😁

1) Quants is too deep, starts from as basic as adding numbers to Ito process. Its a whole new world. I\’d suggest you pick up books on quants and give it a try. I would suggest you start with Ganapaty Vidyamurthy\’s \’Pair trading\’ book.

2) Try the CQF certification. Its one of the best for Quantitative finance

3) It is another technique to trade markets, just like FA and TA

As I mentioned, please spend some time looking at CQF and the content around that. It maybe worth it 🙂

SIR, PLEASE CORRECT THE FIGURES YOU USED IN THE PART- \”FUNCTIONAL FIXEDNESS\” IT IS 35 K REAMINS AFTER 65 K FROM 100,000, 🙂

Sure, let me check this again.

It would be great if there was a feature where we could mark the chapters we have completed reading.

I\’ll take that as feedback.

Hi Karthik,

Since you has mentioned that you would be adding few more concepts later if required, would you be adding any new points in this trading psychology chapter which you encountered in last 4-5 years?

Specially for traders with small capital which has entered stock market in huge number since 2020 fall and more into option trading (buy side)?

Abhinav, no, dont think I plan to add anything more now. Maybe at a later point, I may.

Definitely Sir,

It was asked just because of your extensive time in the market and what you discovered so far.

I used to follow instructions provided in Technical Analysis Chapter. And most of the time it worked in Swing Trade.

Thank you for such a worthy article.

Will love to read more…

Happy learning and trading, Nilesh.

Sir, we now know about Investing, Swing Trading, Day Trading and Derivatives. All these are different from one another and must be used as per objective. However, can you tell us that out of these, which is probably a better profit making system?

Thank you!

Very hard to say, Nilesh. if I say swing, that works for me, and may not work for you. You will have to do this discovery yourself.

i learnt very much from this module .i found many my scarcity during trade. this module give me a chance to intospect myself. thank you much sir .

Happy learning and exploring 🙂

Art of thinking Clearly by Rolf Dobelli – excellent book for all types of biases – a must read and perhaps we can deduce many more such biases from the book.

Making a note of this, thanks for the suggestion.

Great work.

I was more interested on the psychology of trading/investing.

Anchoring bias has done a lot of damge to my investments. I lost opportunities in GRM overseas (240), Rallis (150), Biocon (216!), LTI(800), LTTS(800), Advanced enzymes(105) and many others. I had even an order placed for advanced enzyme at 105 when it was trading at 106.

So has confirmation bias and gambler\’s fallacy to my trading. So sad.

Trying to get over these barriers.

Thanks.

Its very relatable 🙂

Hopefully such damage wont occur in the future!

After reading about Sundaram Clayton, decided to buy Bector Food at 360. My limit price was 350.

Sure, I hope you\’ve done the research and I hope it moves as you think its supposed to. Good luck 🙂

Hello Sir,

I hope you are doing well.

Can you please tell me avoid a confirmation bias??

In the example you gave earlier, you have mentioned that Tata motors has been rising from 370 to 430. It is going through a good bull run. It receives additional news about a new EV factory set up.

Sure the broad picture is Tata motors sales are down and it has a lot of debt.

But in the short term it looks a decent trigger to buy for a short time correct??

Do let me know what could be done?

Depends on how short your short term really is 🙂

I had anchoring bias for Tesla and I regret that I did not buy it on March – April 2020. Every time it moves up 5% I thought rally is over and it will come back. The funny part is even now I think it’s over valued but yesterday also it went up 5% . Thanks for explaining the psychology. Missing Tesla rally is the biggest missing of 2020.

Tell me about it 🙂

I am keeping my point, Sir, others may differ from my point of view.

I think Technical Analysis and Biases cannot go hand in hand.Please give whats ur take on this.

Suppose,

If there is fundamentally bad news for a stock and the market takes bad news into account and price declines.

After a few days, green candles pop up ( maybe bullish engulfing ).

Now, Recency bias won\’t allow us to take a long position, and if price

the price is near support, RSI level showing oversold ( expect reversal ).

How to handle this situation Sir.?

Recently this happened in Reliance, bad news a few days back but started an uptrend from yesterday.

So I was stuck, whether to go with bias or TA, and I didn\’t take a long position and now I\’m regretting it.

Hope I have placed my question clear.

Thank You

Regards

Abdul

Abdul, you need to arrive at what you want to do. Are you looking for fundamental factors which can impact the price in the long term or are you looking at just the price and trading the price? If its the latter, then look at what the charts are suggesting and swing your trade accordingly and go with the drift.

As always, very neatly explained.

I am also a teacher, but I wish I can explain this good.

Learned new things.

Apart from biases, I knew that one can convert MIS to NRML position.

But I didnt knew about NRML to MIS.

Is it possible sir ?

Thank U

Regards

Abdul.

Thanks for the kind words, Abdul. Yes, it is possible to convert NRML to MIS.

every part was clean and simple, but i wish there is more simple way about that covariance… math part 🙂

Ah, its an elaborate math, no other way to do this 🙂

Can you suggest any book regarding biases, Karthik?

I\’d suggest you read – https://zerodha.com/varsity/module/innerworth/ , these are some of the best lessons on biases, behavioural finance and everything related.

Dear Karthik,

Thanks for your contribution which is a great guide.

I am a new entrant in the Intraday TRADING and sometimes swing trading and have tried few technical indicators. But not confident yet on their efficacy. Currently trying Ichimoko cloud. What is your reaction to use of this system? In theory the system looks interesting.

Appreciate your candid comment please.

Sanjiv

Sanjiv, I\’d suggest you take a look at it, understand its behaviour, and then paper trade it for a while before you actually implement it and take real trades. This will give you some confidence before trading.

Hi Karthik,

I would like to know how covid crisis affected your portfolio and what learning did you draw from it ? Also, i am trying to built a fresh portfolio in Zerodha due to the March fall and unable to decide how to proceed on the same. My current portfolio is down ~ 40%(exiting stocks as and when they reach breakeven) due to the fall and i don\’t want it to happen again. If you can nudge me in the right direction it would be great. Not asking for specific stock tips.

I did take a massive hit on my little portfolio. I\’ve learnt that asset allocation is for real, I\’m implementing that. Few things to keep in mind –

1) Ensure the companies you invest are all solid with a good balance sheet. Not that these stocks won\’t fall when markets crash, it is just that the recovery in such stocks will be quicker and stronger

2) Dont have concentrated portfolios, ensure you have a fair amount of diversification

3) Asset allocation is key – ensure you have a good mix of stocks, MFs, and a bit of gold.

I personally dealt with this, We as humans tend to overestimate what we achieve in short term and underestimate what we can achieve over a year or long term. This kind of creates a resistance in our thinking and thus in work too ! Also due to the over-excitement of the short-term gain, we(people) tend to become more charged up, and if anything goes wrong suddenly give up the entire task.

And also, i can understand your feelings about Sundaram Clayton investment after realizing the missed hit was a Multibagger 😢.

Thank you for amazing contents 🙂

I agree with you Vaishakh. Sundaram Clayton ship has sailed for me, no point looking at missed opportunities, we just have to learn from it 🙂

marvellouse course by zerodha.

Happy reading 🙂

hey, Karthik

Assume you have done your fundamental analysis, checked that company\’s background and all and came to a conclusion that you are going to invest long term in that company. Consider the current COVID-19 situation, where some stocks are still going down and everyone knows that 2020 won\’t be a great year and all but we definitely know things will get better like it always does. Will you put a stop-loss in that stock? If so, by what percentage?

Difficult to place a stop because the stock could fall due to macro reasons and not really because of trouble within the company. So, at times like this, investors have no option but to go through this. In fact, these are the most challenging time for the investor.

Sir, knowledge you\’re providing is great and unmatchable 🙏🙏

Happy learning, Suraj 🙂

Under \”Functional Fixedness Bias\” I\’ve just noticed a something amiss. If the fund available is 100,000 and 65K is blocked for NRML margin in NIFTY then shouldn\’t the balance be 35K and NOT 45K?? Kindly correct me if I am missing something here..

Guess that was a typo, will fix that.

Hey Karthik,

Now its 1AM, I am still reading. I have started reading Zerodha Varsity after making a big lose. I just regret that why I didn\’t I read all this earlier. But any how its not late. I really enjoyed everything in all modules. Especially the examples to make reader understand are outstanding. Felt bit uneasy with Math calculations. But will try to learn it later but everything is so nice. Your patience to answer everybody\’s questions is great. I felt happy over all. My next task is to implement whatever I learnt here and see the outcome. Thanks a lot bro.

Gopi, you made my day! We feel rewarded when people put in the time to read and understand the content we\’ve put out for them. Happy reading!

i need to know some strategies to deal with whipsaws .

anyone can help please give reply to me

Try the simple moving average crossover system, Basudev. That helps 🙂

Karthik

You are the second person I want to meet if ever I get an opportunity..First person is M S Dhoni..You do the live audio visual talking with the structuring of your words..You seem to have written the whole material sitting in Himalayas..Great work.

Thank you.

Hahah, Sunil….I don\’t think I\’m worthy of such accolades 🙂

Everyone at Zerodha strives to do everything possible for clients, I\’m just playing my part.

Hi Kartik,

I have 2-3 doubts. I hope you can answer

1) Can strategies like RSI divergence or pattern like H&S be applied universally or a precedence in the particular script be looked at?

2) If you look at OI chain, normally but put and call have large OI written 2-3 strikes away. In that case how to take a directional view?

3) Is it fair to say if breakout takes and candle is not touching bollinger band ( low volatility) it isnt a failed one. Any other way?

1) All technical patterns and indicators can be applied to all assets which have an OHLC data

2) In my opinion, OI does not give you a sense of direction. The price action (aka the charts), gives you a sense of direction

3) This is an interesting way, I\’ve never thought about it actually. But if it does touch the upper or lower band, then that\’s a conflicting signal. This is because the breakout suggests continuation but the BB suggests otherwise.

Thank you kartik sir.

Welcome and happy leaning 🙂

Karthik Sir,

Thanks for spreading knowledge through these easy to understand modules.

In Anchoring bias, you mentioned how you lost a big opportunity to invest in a stock (Sundaram Clayton Ltd.) I am wondering how one can identify such an opportunity in an early stage. I have gone through Module 3 (Fundamental analysis) and in Chapter 3 you mentioned how to generate stock ideas to invest. May you like to suggest some books (or any other resources) so that I can learn to analyze such potential investment opportunities.

Thank you very much.

I\’d strongly suggest you read \’One up on Wall Street\’, by Peter Lynch. That\’s a great book to pick up a few great stock picking ideas.

Thanks for your advice!

Good luck, Nitesh.

Love it as always!! I hope more and more content will be produced!! Can you write a few points on Overtrading as that is one of the biggest problem that the amature traders face and Tips on how to prevent it. Thank you!

Glad you like it, Prathvi. That\’s a good topic you\’ve suggested. Will try and add some notes on it. Thanks.

Hi Karthik

great fan of your writings.. Few month ago i have entered into the trading world and did some loss making trades.I have decided that right now i\’ll stay away from market and during this time i want to get some knowledge about the market(although it\’s a sea) .I know trading is a complex subject and needs to be patient enough to stay safe and profitable.Vesrsity is a great platform to understand all the basics of stock market(specially for a amateur like me).I have some queries,if you check those out it will be highly appreciated…

a. How can i make myself prepared before going into the market(again..:-))?

b. Should I become a trader of investor frist?

c. What should be the mindset before buying or selling a stock?

1) Nothing really substitutes for reading and gaining knowledge. I\’d suggest you read as much as you can and get familiar with the way the market works.

2) I\’d suggest you try out investing first

3) Ideally long term 🙂

Thank you ….

can you suggest me some good books to begin with….?

Maybe Peter Lynch\’s \’One up on Wall Street\’, that\’s a great book to start with.

Thanks a lot….i have ordered that book…thanks again for your generosity.

Good luck and happy reading, Subrata 🙂

Hi Karthik

sorry for knocking you again….:-)

as per your recommendation (One Up on Wall Street by Peter Lynch) i have gone through the book..and it helps me to realise my mistakes.Thanks a lot for recomending me such a great book to start with….can you guide me some other good books for further knowledge?

Glad you liked the book, Subrata. I\’d also suggest you read Antifragile. Excellent book that one.

Thank you Karthik …i am going to order this book…and I can\’t express myself how glad i am ..i can proudly say that we all are very much fortunate to have a guide like you…

Its too big of you to say this, Subrata, thanks and happy learning 🙂

hi karthik your content is amazing and i learnt a lot from ur modules , i will tell my experience related to crypto trading( i apologise this is not related to stock trading) , actually in the middle of december 2017 RIPPLE(one type of crypto) trading at 14.85rs i placed buy order at 14.65rs in huge numbers, i thought it will hit my buy order but it never happened , at that time everyone knows ripple is going to rise because of inclusion in coinbase but how much rises no one knows, by december 30th it was trading at 250rs . I did spent many sleepless nights later cursing myself. I lost entire capital carrying that emotions later on so i have learnt a lesson that we should control emotions and be practical

This has happened to me several times, such incidents only help us get better at both trading and investing 🙂

Content is amazing. But questions is we realize a bais after mistake or we blame bias after mistake. Is there any way to know that we are in bias before huge miss?

So you got to learn from these mistakes and keep them in your mind so as to not repeat it next time 🙂

OMG ?? the Confirmation bias is so amazingly true !! When i wasn\’t able to understand the technical indicators i used to google \”technical indicators are unnecessary\” & \”not needed for intraday\”, only to feel good that yeah, i can trade nicely without even touching them ?? . Not only trading, i even google \”scientific & spiritual benefits of long hair\” so that i could grow them long & look psychedelic like Pink Floyd, because as usual no typical indian family would let a boy grow long hair like rockstars ?

Lol!

We all like validations in life 🙂

very well written, first day of my account opening and i read whole chapter. interesting!

Good to know that, Raj!

Keep learning 🙂

Hey! I wanted to read furthur on the psychological aspect of the stock market. Can you recommend a book or two for this?

Going through the comments, I see people have recommended \’The art of thinking clearly (Rolf Dobelli)\’ & \’Thinking, Fast and Slow (Daniel Kahneman)\’. Should I order that?

Thanks!

I\’d certainly recommend \’Thinking Fast & Slow\’, not sure about the other book.

Alright. Any other book which you think can also be relevant?

Hmm, nothing that occurs to me now.

Hi Karthik

It was really great to read about all these Behavioural biases & there are surely many more that exist.

My question is with regards to the Futures contract. If I take a futures contact X today as NRML then the next day can I convert it to MIS thereby lowering my margin requirements? Of course the logic will be to trade another contract Y as a Day trader or probably exit the Contract X as a day trader & convert Contact Y as NRML by 3:20 pm. So is my understanding correct here?

Yes, you can convert NRML to MIS and free up margin available. But you need to make sure to convert it back.

Thanks a lot Faisal 🙂

A Very Happy New Year to you & to all the Zerodhaits!!

Wishing you the same, have a great year ahead 🙂

Thank you. You have made my confidence level high. Please clarify my doubts

1) I can convert MIS to NRML (If I have sufficient money in my account) and Vice versa. Isn\’t true? Whether I have an option of adding money during the trade (before square off).

2) Suppose if you provide leverage of 20 times in intraday, but I want only 10times, Can I have an option of taking 10 times or I have to take full leverage compulsory?

3) why Zerodha\’s s Square off time is 3.20pm instead of 3.30pm

1) Yes, you can do that. You can also add funds to your account anytime during the trading hours

2) Yes, you can by proportionately adjusting the number of shares/lots

3) This is the ensure you have sufficient time to square off the orders

Thank you

Hi Sir,

Thanks for sharing your knowledge. I am a regular reader of all the modules written by you. I really like the way you narrate the things with examples, thanks for all that.

I request you write on mutual funds, theme based investments and ETFs. Since this will help many investors looking for diversified and long term investment.

Happy to note that, Kiran. Yes, MF has been on the cards for a long time. Will certainly do this sometime soon.

Sir, I have a query.

In the last chart (while discussing confirmation bias), there being a clear uptrend, the candle appeared to form a bearish harami. This coupled with the fact that the pattern was forming around the resistance zone made me to interpret the signal as a shorting opportunity. Can you please correct me where I went wrong?

I\’ve used that chart to illustrate the point, Ashish. Nothing much to analyse 🙂

Hi , is there a post on \”\”Hedging portfolio with Options\”\” on the cards?? Im waiting for that.

Not as of now, we will have something soon though.

sir any plan of writing a module on \’how to analyse Bonds\’ ?

Hopefully sometime soon 🙂

Hello, i am facing a minor problem, the font colour you are using in PDFs is not exactly black, so i have to convert them to word, make font colour black and then reconvert to PDF before printing, please do the needful

Which PDF are you facing this problem in, Sandip?

Please add \”Download pdf \” option for the rest of the chapters.

Please read the comments above, this will take time.

Sir one question I am new to investing.

Do the much popular \”magic formula \” always works. Is it wise to follow that formula.

The logic is quite interesting, Pradeep. I don\’t know if it always works though.

You should check it out. The original book by – Joel Greenblatt is quite short and straightforward, you should read it.

Superb Kartik ..

You did fantastic job.

Can you plz elaborate how you take quick decisions in trading from your experience?

The emphasis should be on rational decisions, not really quick decisions 🙂

by when pdf of this module will be available?

It will take sometime, Rohan.

Single is not mind

Sorry, quite dint get that.

Dear Karthik,

Thanks for your interesting articles in this module , please add trading plan and goal setting in this module,then this module will completed.

Thank you so much sir,

Good luck!

Hi.

I like the way you have written.

Our minds do this funny thing where they try and live in the past or in the future, rehashing old conversations and scenarios over and over again. But this just isn’t reality. Life doesn’t happen between your ears, it happens in the NOW.

Thank you !!

Absolutely! Training our minds to rationality is indeed the toughest things 🙂

Hi. There is a \’Download pdf\’ link for other chapters, but I don\’t see one for Chapter 9. Do let me know if I have somehow missed it. Otherwise, please add that. Thanks

We are yet to put up the PDF for this module.

Read the book \”Thinking fast and slow\” by Daniel Kahneman to learn about the system 1 and System 2 and various biases. You will able to make better decisions in trading if you can understand the various biases.

That book is a gem!

My sincere APOLOGIES for irrelevant question but this was necessary, so..

What should I do in the scenario of technical glitch in your trading system when I am unable to exit my open position and loss is continuously increasing ?

Naman, this can happen with any broker. I\’d suggest you call up the support and speak to the executive to help you exit the position.

Sir , i have gone through all the modules. And it was great learning. I became fan of your writing. waiting for the next module- Trading strategies. Thank you !!

We will be calling it Trading Systems\’ 🙂

Thank you Sir.

Cheers!

Pdf like other volumes….will it take long????

This will take slightly longer, trying to fix minor errors in the module.

Individual pdfs for chapters that are done….. I guess you would prefer releasing the whole….still thought of asking…. Have questions regarding T1 stock issue…. I know not the forum but don\’t have any other means…. Support team and even Nithin….. Both are silent about the issue…. No clear resolution…. Just asking if you can HELP??????

Yes, will put it up as a whole. Support has been very busy over the past few days Ameer. You will get a response soon.

Excellent article. I specially liked the anchoring bias because i have felt reasonably anchored to it.

Essel propack – i wanted to buy at 28 while stock was trading at 33 back in 2012. I stuck to my price which never came after that. Not to mention today the stock is at 272.

Enjoyed reading this article. Thanks a ton

Glad you liked it, Jeeth 🙂

Happy learning!

The one thing I understand about biases is that one learnes to avoid it through the help of his/her experience and conviction. Isn\’t it?

For example I\’m still a student I haven\’t really started trading full time, so I guess I won\’t be able to relate to it as much as other traders. Am I right Sir?

Not really, Umer. As long as you are aware of these biases, you are already one up over others. Obviously your understanding becomes firm when you go through it yourself 🙂

Waiting for trading strategies modules from 2016. Hope it comes soon. 😀

Btw why didn\’t you buy the stock at 370 and you should have maintained SL of 10-15% on the downside?

I believe if the conviction for the stock is strong better buy in small quantities and maintain a stoploss.

It kills me to see that you missed out on 20 fold returns.

I hope your wait is worth its time!

Well, that\’s a lesson I\’ve learned the hard way 🙂

Sir would it be possible to write a chapter on Arbitrage and it\’s types? I guess there aren\’t any material that deals with the same. Thank you.

The next module on Varsity will cover this.

Wonderful writing again Karthik Sir.For those of you who want to explore all the other kinds of bias that exist please read the book \”The art of thinking clearly\” by Rolf Dobelli.

I\’ll try and lay on hands on that as well, thanks for suggesting 🙂

Yes, Its a wonderful book that helps you to introspect.

Mr. Karthik, looks like you\’re a bit of a psychology and NLP techniques too. It was a great chapter as usual. Can I ask when are the pdf\’s going to be created? Thank you.

PDF\’s will most probably be up next week 😉

Karthik, thank you so much. These are very informative and helpful. Can you please publish the pdf

PDF will take a slightly longer time, Prashanth.

Hi Karthick, PDFs are still awaited, i have saved all these for flight readings. keep going on over and over again. What a collection of learnings. Take a Bow to you the master

Haha, glad to know Varsity gives you company during those long and boring flight journeys 🙂

Will upload the PDFs very shortly. Thanks.

Next module- Trading strategies., please sir.

Yes Sir!

suppose i buy a stock ,say deltacorp which CMP is 230 . i want to buy if it reaches to 232 . so i am placing a SL-MARKET buy order ,with a trigger price of 232. my question is how to place my order to limit my loss if the stock goes negative. can i place it in the buy order itself or i have to place SL-LIMIT order with trigger as 228

After you buy, please place a sell SL-limit order at 228.

Thank you for the read.. Before varsity I didn\’t have good reference material and used to read rich dad\’s guide to investing!!

What are your opinion on Robert kiyosaki and his books ???

I\’ve actually not read that book, Vishal 🙂

Hi Karthik

Earlier we could access P&L day by day but now it\’s showing only from 1st April, please fix this. I am not able ( I am sure others as well ) to see my brokerage as well other charges. Hope you guys can fix this at earliest.

Much Thanks

Rahul

Rahul, I guess the system is getting updated. This should be sorted sometime soon.

Work around for FROM DATE issue is just copy paste the date of ur choice…

Hi karthik,

Its very difficult, please fix as soon as possible