12.1 –Defining Equity Capital

The last chapter we laid down few key thoughts on position sizing and with that, I guess it is amply clear as to why one has to incorporate position sizing at the core of every trading strategy. Position sizing technique helps you identify how much of your equity capital has to be exposed for a given trade. In this chapter, we will take that discussion forward and explore ways to position size.

A quick recap of sorts before we proceed. What is position sizing?

Position sizing is all about answering how much capital you will expose to a particular trade given that you have ‘x’ amount of trading capital. One classic position sizing strategy which most people employ is the standard 5% rule. The 5% rule does not permit you to risk more than 5% of the capital on a given trade. For example, if the capital is Rs.100,000/-, then they will not risk more Rs.5000/- on any single trade.

Here 5000 is the exposure to a trade and 10000 is the equity capital. You have decided to invest 5000 a trade based on a position sizing rule or a strategy.

Needless to say, there are many different ways to position size, which by the way, also means (unfortunately) that there is no single guided technique to position size. You as a trader need to experiment and figure out what works for you. Of course, I will discuss few position sizing techniques soon.

Now, irrespective of which position sizing technique you will follow, at some point the technique will require you to estimate your equity capital. For this reason, we will address the technique of estimating equity capital first and then proceed to learn position sizing techniques.

What do I mean by equity capital?

Equity capital is the basically the amount of money you have in your trading account based on which you decide how much capital to deploy in a trade. This may seem very trivial to you at this point. But allow me to illustrate why this is a tricky task.

Assume you have Rs.500,000 capital and you work with a simple position sizing principle of exposing not more than 10% capital to a single trade. Given this, assume you take a position worth Rs.50,000/-.

Now for the next trade, how much is your equity capital?

- Is it Rs.450,000?

- Is it still Rs.500,000 considering the fact 50K is deployed in a trade?

- Should it be 450,000 plus 50K ± the P&L from the trade that exists in the market?

Given that there are numerous outcomes and possibilities, estimating equity for the trade is not really a straightforward task. Hence, getting our act right in estimating the equity capital is very important before we proceed to learn position sizing concepts.

12.2 – Estimating Equity Capital

At this point, I’d like to go back to good old Van Tharp and talk to you some of the techniques he uses to estimate equity capital. These are some of the better techniques compared to the many out there. Essentially there are three techniques or models as he calls them –

- Core Equity model

- Total Equity model

- Reduced total equity model

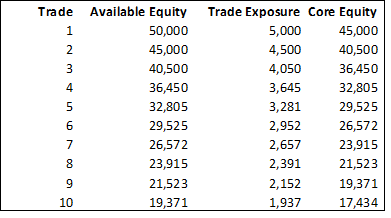

The core equity model requires you to deduct the capital allocated to a trade from the existing capital. This way, the exposure to a trade goes on reducing as you ladder up more and more positions. Let me give you an example – assume your equity capital is Rs.50,000/- and you follow a simple 10% position sizing formula. The 10% rule implies that you do not expose or risk more than 10% of your capital to a trade. So the first trade gets an exposure of Rs.5000. The core equity is now reduced to Rs.45000. Have a look at the following table –

Download the excel sheet here.

So, the first trade assumes the equity available is Rs.50,000, hence 10% of the available equity is exposed first trade i.e Rs.5000/-. The core equity model requires you to deduct the capital deployed to a trade and re work on the core equity model. So, the core equity is now Rs.45000/-, which is also the available equity for the 2nd trade.

For the 2nd trade, we again deploy 10% of the equity available i.e 10% * 45000 = Rs.4500/-. We deduct this amount to calculate the new core equity, which is now Rs.40,500/-. This also is now the newly available equity for the 3rd trade.

So for the 3rd trade, the capital exposure for the trade is Rs.4050 and the new core equity is Rs.36,450/-. So on and so forth, I’m assuming you get the drift.

I consider this as a slightly conservative equity estimation model as you tend to reduce the capital allocation as the number of opportunities increases. For all you know, your 5th trade (for which the equity exposure is far lesser) may be a great winner. The other side of the argument is that the 5th trade could be the worst loser compared to the rest.

Having said that, I like this model for the sake of its simplicity. Once you commit the capital to a trade, you kind of forget about that and move on with what is available.

The Total equity model aggregates all the positions in the market along with its respective P&L and cash balance to estimate the equity. Let me straight away take an example to explain this –

Free cash available – Rs.50,000

Margin blocked for Trade 1 = Rs.75,000

P&L on Trade 1 = + Rs.2,000

Margin blocked for Trade 2 = Rs.115,000

P&L on Trade 2 = + Rs.7000

Margin blocked for Trade 3 = Rs.55,000

P&L on Trade 1 = – Rs.4,000

Total Equity = 50000 + 7000 + 2000 +115000+7500+55000-4000

= Rs.300,000/-

So, as you can see, in the total equity model, free cash along with margins blocked and the P&L per position is taken into consideration. Now, if my position sizing strategy suggests a 10% exposure to a new position, then I’d expose Rs.30,000/- on a new trade. If the free balance in my account does not permit me to take this position, then I’d not really initiate a new position. I’d wait to close one of the existing positions to take a new position.

The fact that this model considers a live position along with its P&L into account for estimating equity makes it a little risky. I’m personally not a big fan of this equity estimation model. This is somewhat like counting the chicken before they hatch.

I do like the 3rd model to estimate the equity, this one is called the ‘Reduced Total Equity Model’.

This model kind of combines the best of both the core equity model and the total equity model. It basically reduces the capital allocation to a particular trade (similar to core equity model) and at the same time includes the P&L of the trade which is already in place (similar to total equity model). However, the P&L is only on the locked in profits.

Let me work with an example to help you understand this better. Assume I have a capital of Rs.500,000/-. Further, assume my position sizing strategy allows me to invest not more than 20% on a single trade, which is Rs.100,000/- per trade.

I’m looking at the chart of ACC and I decide to go long on ACC futures at 1800 by blocking a margin of approximately Rs.90,000/-, which is well within my position sizing limit of Rs.100,000/-.

I’ve now entered a position and waiting for the market to move. Meanwhile, as per the reduced total equity model, my the capital available for the 2nd trade is –

20%*( 500,000 – 90,000)

= Or about 20% of Rs.410,000/-

= Rs. 82,000/-

Note, because of the existing position, the exposure capital has reduced from Rs.100,000 to Rs.82,000/-. Up to this point, it works exactly like the core equity capital model.

Now, assume the stock moves, and ACC jumps by 25 points to 1850. Considering the lot size of 400, I’m now sitting on a paper profit of –

400*50

= Rs.20,000/-

I would now put in a trailing stop loss and lock in at least about 25 points out of 50 point move or in Rupee terms, I want to lock in Rs.10,000 as profits.

This means, for the long ACC position at 1800, I have to now place a stop loss at 1825 and locked in Rs.10,000/- as profits.

I will now add this locked in profits back to the total equity. Hence my total equity now stands at –

410,000 +10,000

=420,000/-

This means, my new exposure capital will be 20% of the total equity –

=20% * 420000

= Rs.84,000/-

As you notice, the exposure capital has now increased by an additional 2000/-.

I kind of like the reduced total equity model to estimate the total capital available to position size. If one follows tends to follow this technique, then it kind of forces you to practice basic stop loss principles, which according to me is very good.

Anyway, I’d like to close this chapter at this point. In the next chapter, we will consider one of the above-stated methods to estimate equity and look into few position sizing technique.

Key takeaways from this chapter

- Estimating equity capital is crucial for position sizing

- Core equity model deducts the capital allocated to a trade and recalculate the capital available

- Total Equity model requires you to add the free cash, margins blocked, and the P&L of the positions to estimate the equity capital

- Reduced Total Equity model requires you to add the free cash to the locked in profits of an existing position

Iam new in trading.its helping me lots thanks 🙏

Happy learning 🙂

How to do position sizing in options trading?

Should I calculate the risk per trade from spot chart and using delta of the contract?

Can you give brief explanation

You can always use delta as a proxy for identify the probability for the option to expiry ITM. For example, if the delta of an option is 0.6, then I\’d consider the option to have a 60% probability for it to expire ITM, hence I\’ll not sell it.

Stop loss limit is the exposure.

For eg;My total equity capital in my trading account is Rs.1000.

Trade 1 i want to go long – target 105; Buy price : 100; quantity – 1; stop loss limit : 97.5.

Thus my exposure for this trade is 2.5% of the capital deployed,

For the 2nd trade, even assuming the worst case scenario in trade 1 , i have protected capital of 97.5, hence why not consider 997.5 as total capital available and take 10%/5% as position sizing.

Sorry even if i am missing something fundamental. If i have misunderstood something, pls correct me with the above example. I have just started trading . I went through Module 2, but before starting on Futures, options , commodities etc. I came here right away to get a good grip on risk management.

Risk as they say is the fear if uknown happening, given this, it is always a good idea not to expose 100% of the capital on a single trade, no matter how attractive it is 🙂

Hi Karthik,

If there is a trailing stop loss, then why not consider the capital deployed in your example ie. 90K + the profits locked-in i.eINR 10K?If the stock is liquid & has good volume, then why stop loss limit price not be as considered for Total equity?

You also need to worry about the exposure for each trade right?

Sir in the above example, for 3rd model that is reduced total equity model as you have written long on futures ACC at 1800 and further ACC jumps by 25 points so it should be 1825 and not 1850 I guess its a typo so, if 25 points is changed to 50 points then the further calculations will be correct.

Checking on this, Ashay.

Sir, if I want to take a single trade at a time, what% of capital can I deploy in intraday cash segment.

In that case, you can use the % technique.

Hello kartik sir, myself Ritika Kumawat from mumbai, third year student, I want to ask that at last you said that after exiting the first trade ie., Acc, the strategy locks up half of the profit and remaining half gonna add in original position so now the capital is 4.2L and for 2nd trade used capital is 20% ie., 84k but as if we have exited the position of acc we just added the half profit into the 2nd trade, What if we include 90k that we have used in 1st trade and since we ve exited the trade we can add the 90k amount in the original amount plus profit/loss for 2nd trade?

Ritika, you can add that. But you will have to re-assess the position (portfolio) and its overall limits. Ensure that after adding back, you are position sized properly.

Karthik,

Here 5000 is the exposure to a trade and 10000 is the equity capital. You have decided to invest 5000 a trade based on a position sizing rule or a strategy.

Isn\’t the capital 1,00,000 rupees? it is mentioned as 10,000 in the above statement.

As always, all the content are very informative.

Thanks.

Karthik,

Here 5000 is the exposure to a trade and 10000 is the equity capital. You have decided to invest 5000 a trade based on a position sizing rule or a strategy.

Isn\’t the capital 1,00,000 rupees? it is mentioned as 10,000 in the above statement.

As always, all the content are very informative.

Thanks.

Ah, must be a typo Sankar. Let me check 🙂

Can someone give me the excel sheet of reduced equity model to calculate my position sizing?

Sir can we trail our stop-loss in zerodha for swing or positional trades l,if yes how?

Yes, you can set up a GTT order and modify it as and when the stock moves in your favour. https://zerodha.com/z-connect/tradezerodha/kite/introducing-gtt-good-till-triggered-orders

HII SIR THIS IS NAGARAJU

I FOUND ONE MISTAKE WHILE READING THIS PART

JUST CHECK ONES TOTAL EQUITY MODEL CALCULATION

THE TOTAL EQUITY WAS INPLACE OF 75000 YOU PUT 7500.

AND P&L ON TRADE -3 NOT TRADE -1.

JUST CHECK SIR…IF YOU HAVE A FREE TIME

THANK YOU SIR….

Thanks for pointing that, Nagaraju. Will look through this.

Ignore comment

Kelly Criterion??

What has been asked in a previous comment, the same doubt is buzzing in my mind.

Yes, the trade is live but surely we will get the principal amount (90,000) .

What if I trade next time keeping in mind that I have 5,10,000 in my accont.

Am I doing a big mistake if I include this amount while calculating my Total Equity Capital ?

Hope I have palced my question clear.

Thank you.

Regards

Abdul.

No, if your previous trade has generated profits, then you need to consider that as well into the trade.

I have a doubt regarding the \’Reduced Total equity model\’

In the example above, We added the locked in profit (Rs. 10,000) to the leftover money (Rs. 4,10,000) in trading account

leading us to the answer of Rs. 4,20,000.

But if we are to square off that position at 1825 or the stop loss is triggered, the cash inflow into the account will actually be the principle + profit (90,000 + 10,000), so the resultant equity capital will be Rs. 4,10,000 + Rs.(90,000 + 10,000), i.e. Rs. 5,10,000

Please correct me if I\’m wrong

Yes, but the assumption here is that you are taking the 2nd trade when the 1st trade is still live in the market. Yes, if you get out at 1825, then capital is 5.1L.

In above Total Equity Model Calculation is wrong

Total Equity = 50000 + 7000 + 2000 +115000+7500+55000-4000

= Rs.300,000/-

*7000 should be 75000/-

Ah, thanks for pointing, let me check.

Sir in markets most of them say we should not lose more than 2% of amount from our total capital so if i take trade based on 10% rule of allocating for a trade from our 5lakhs capital and in this trade if my stop loss is around some 2% means should we take the next trade or only this one trade because if we keep on taking the trades for total capital doesn\’t our risk increase more than 2%.

2% is a general risk management rule based on per trade basis. You can have multiple trades open simultaneously.

Risk management in option trade?

I have discussed this in the options module, largely in the greeks section.

Very lucid and clear way of explaining.Thank you so much, Karthik sir.

Welcome, happy learning Sudheer.

How to apply risk management for options trading?

What is the right amount of capital to start options trading?

Will talk about that soon.

Mr. Karthik I know you have already mentioned that you could not teach how to expect the market movements and that a trader has to find out what works for him /her (quantitative or technical or fundamental) . However, would it be possible to give some pointers or give the name of some books that deals with the same?

No book out there will tell you that, Sashidhar 🙂

TA gives you some sense of direction (on shorter term basis). People also use FA to get a sense of longer term direction.

Dear Sir,

Thank you very much for this great knowledge sharing. Can you please give us excel for \”Reduced Total Equity Model\”.

Will try and put that up.

Hi Karthik Sir,

I totally love topic!! Awesome!! Can you name few books of Van Tharp for position sizing?? It will be really helpful!! Thanks in advance!!

I think there is one book called Position Sizing itself.

Sir, Please give some name of books on trade that is lower than Rs. 400/-

Will let you know if I come across.

Hi Sir,

I’m a huge fan of you (After reading all modules on varsity ☺️). I am a beginner in stock market and thanks to you and varsity for giving as this knowledge.

I also keep reading several books.One of this books is COME INTO MY TRADING ROOM by Dr. Alexander Elder. A great book for trader\’s i must say. You can also write Next chapter on his rules i.e.

THE 2% SOLUTION—PROTECTION FROM SHARKS.(Maximum capital to risk on particular trade)

THE 6% RULE—PROTECTION FROM PIRANHAS

(Maximum capital to risk at particular Time).

You can write about this techniques as well as many more things given in the books like Trader\’s – speardsheet,dairy,record keeping, etc.

Sankalp, thanks for the very kind words!

The next chapter will have some of this stuff, stay tunned 🙂

Hi Karthik, I really appreciate the efforts u r putting into explaining all these concepts so lucidly.Just a request, if u can have a module on bond markets, it would be very useful.

Thanks for the kind words, Rahul. Yes, will try and put that up sometime soon.

Hi Sir,

Eagerly waiting for next Chapters. Please publish it soon.

Thank you.

Working on it, Sir. It should be up next week.

Hello karthik great module,

Are you planning to introduce a model on bond markets and fixed income.

I personally think it is quite a boring topic, so hearing the same from you would really help:)

Hopefully sometime soon, Umer 🙂

Thanks for the kind words!

Words are not enough Mr. Karthik, this varsity is amazing. I would run away from some concepts like option greeks and forex until varsity happened. It\’s really helpful, you should think on opening a coaching or something. India really needs to be educated about finance!

Thanks for the kind words, Umer. This will keep us motivated 🙂

I read few of Van Tharp\’s books as you suggested. He says it\’s possible to take a million dollars out of the market each year with a capital as low as $200,000. Does the statement hold true in Indian markets as well?

Theoretically yes, but trust me it not easy.

sir

where r pdf files of all modules ?

It\’s there at the end of the chapter list. PDFs for this module is not there yet.

can you educate us on index ETF, INVERSE ETFS AND Gold ETF?

The next module is in personal finance. Will include this in that module.

And yes

HAPPY INDEPENDENCE DAY.

Thanks, Sohail. Wishing you the same!

Hi Sir,

Plz make module on tracking fii investment stocks.

How to track which stocks they are buying these day.

Thanks

Thanks for the suggestion. Will try and put up a chapter on that sometime soon.

Module 10 >..< ?? ?? ??

After Module 9.

Hu karthik,

What i follow is 5% of total account size.

E.g i have 100000 than i take trade of 5000 Rs each. I.e total 20 trades.

Stoploss 3%, profit 6- 8%.

Whats your view on this?

In the next chapter, I would be talking about few more techniques 🙂

Sir, when the next module will be uploaded Ex- Financial modelling

The next module is on personal finance, maybe after this 🙂

Thanks for your patience and support!

how many more module is now left sir

Working on this module for now….plan is to include Personal finance (with a focus on MF), Trading strategies, and Financial Modelling.

The next module is on personal finance, maybe after this 🙂

Thanks for your patience and support!