5.1 – Things you should know by now

Margins clearly play a very crucial role in futures trading as it enables one to leverage. In fact, margins are the one that gives a ‘Futures Agreement’ the required financial twist (as compared to the spot market transaction). For this reason, understanding the margins and many facets of margins is extremely important.

However, before we proceed any further, let us list down a list of things you should know by now. These are concepts we had learnt over the last 4 chapters; reiterating these crucial takeaways will help us consolidate all the learning. If you are not clear about any of the following points, you will need to revisit the previous chapters and refresh your understanding.

- Future is an improvisation over the Forwards.

- The futures agreement inherits the transactional structure of the forwards market.

- A futures agreement enables you to financially benefit if you have an accurate directional view of the asset price.

- The futures agreement derives its value from its corresponding underlying in the spot market.

- For example, TCS Futures derives its value from the underlying in the TCS Spot market.

- The Futures price mimics the underlying price in the spot market.

- The futures price and the spot price of an asset are different, attributable to the futures pricing formula. We will discuss this point at a later stage in the module.

- The futures contract is a standardized contract wherein the agreement variables are predetermined – lot size and expiry date.

- The lot size is the minimum quantity specified in the futures contract.

- Contract value = Futures Price * Lot Size

- Expiry is the last date up to which one can hold the futures agreement.

- To enter into a futures agreement, one has to deposit a margin amount calculated as a certain % of the contract value.

- Margins allow us to deposit a small amount of money and take exposure to a large value transaction, thereby leveraging the transaction.

- When we transact in a futures contract, we digitally sign the agreement with the counterparty; this obligates us to honour the contract upon expiry.

- The futures agreement is tradable. Which means you need not hold on to the agreement till the expiry

- You can hold the futures contract until you have a conviction on the asset’s directional view; once your view changes, you can get out of the futures agreement.

- You can even hold the futures agreement for a few minutes and financially benefit if the price moves in your .favour

- An example of the above point would be to buy Infosys Futures at 9:15 AM for 1951 and sell it by 9:17 AM in 1953. Since Infosys lot size is 250, one would stand to make Rs.500/- (2 * 250) within a matter of 2 minutes

- You can even choose to hold it overnight for a few days or hold on to it till expiry.

- Equity futures contracts are cash-settled

- Under leverage, a small change in the underlying results in a massive impact on the P&L

- The profits made by the buyer is equivalent to the loss made by the seller and vice versa.

- Futures Instrument allows one to transfer money from one pocket to another. Hence it is called a “Zero Sum Game.”

- The higher the leverage, the higher the risk.

- The payoff structure of a futures instrument is linear.

- The futures market is regulated by the Securities and Exchange Board of India (SEBI). Thanks to the watchful eye of SEBI, there has been no incidence of counterparty default in the futures market.

If you can clearly understand the points mentioned above, then I’d assume you are on the right track so far. If you have any questions on any of the above-mentioned points, you need to revisit the previous four chapters to get the concept right.

Anyway, assuming you are clear so far, let us now focus more on the concept of margins and mark to market.

5.2 – Why are Margins charged?

Let us now rewind to the example we quoted in the forwards market (chapter 1). In the example quoted, 3 months from now, ABC Jewelers agrees to buy 15Kgs of Gold at Rs.2450/- per gram from XYZ Gold Dealers.

We can now clearly appreciate that any gold price variation will either affect ABC or XYZ negatively. If the price of gold increases, then XYZ suffers a loss, and ABC makes a profit. Likewise, if the price of gold decreases, ABC suffers a loss, and XYZ makes a profit. Also, we know that a forwards agreement works on a gentleman’s word. Consider a situation where gold price has drastically increased, placing XYZ Gold Dealers in a difficult spot. Clearly, XYZ can say they cannot make the necessary payment and thereby default on the deal. Obviously, what follows will be a long and gruelling legal chase, but outside our focus area. The point to be noted here is that in a forwards agreement, the scope and the incentive to default is very high.

Since the futures market is an improvisation over the forwards market, the default angle is carefully and intelligently dealt with. This is where the margins play a role.

In the forwards market, there is no regulator. The agreement takes place between two parties with literally no intermediary watching over their transaction. However, in the futures market, all trades are routed through an exchange. The exchange in return takes the onus of guaranteeing the settlement of all the trades. When I say ‘onus of guaranteeing’, it literally means the exchange makes sure you get your money if you are entitled. This also means they ensure they collect the money from the party who is supposed to pay up.

So how does the exchange make sure this works seamlessly? Well, they make this happen using –

- Collecting the margins

- Marking the daily profits or losses to market (also called M2M)

We briefly looked into the concept of Margin in the previous chapter. The concept of Margin and M2M is something that you need to know in parallel to appreciate futures trading dynamics fully. However, since it is difficult to explain both the concepts simultaneously, I would like to pause a bit on margins and proceed to M2M. We will understand M2M completely and come back again to margins. We will then relook at margins keeping M2M in perspective. But before we move to M2M, I would like you to keep the following points in the back of your mind –

- At the time of initiating the futures position, margins are blocked in your trading account.

- The margins that get blocked is also called the “Initial Margin.”

- The initial margin is made up of two components, i.e. SPAN margin and the Exposure Margin.

- Initial Margin = SPAN Margin + Exposure Margin

- Initial Margin will be blocked in your trading account for how many days you choose to hold the futures trade.

- The value of the initial margin varies daily as it depends on the futures price.

- Remember, Initial Margin = % of Contract Value

- Contract Value = Futures Price * Lot Size

- The lot size is fixed, but the futures price varies every day. This means the margins also vary every day.

So, for now, remember just these points. We will go ahead to understand M2M, and then we will come back to margins to complete this chapter.

5.3 – Mark to Market (M2M)

As we know, the futures price fluctuates daily, under which you either stand to make a profit or a loss. Marking to market or mark to market (M2M) is a simple accounting procedure which involves adjusting the profit or loss you have made for the day and entitling you the same. As long as you hold the futures contract, M2M is applicable. Let us take up a simple example to understand this.

Assume on 1st Dec 2014 at around 11:30 AM; you decide to buy Hindalco Futures at Rs.165/-. The Lot size is 2000. 4 days later, on 4th Dec 2014, you decide to square off the position at 2:15 PM at Rs.170.10/-. Clearly, as the calculation below shows, this is a profitable trade –

Buy Price = Rs.165

Sell Price = Rs.170.1

Profit per share = (170.1 – 165) = Rs.5.1/-

Total Profit = 2000 * 5.1

= Rs.10,200/-

However, the trade was held for 4 working days. Each day the futures contract is held, the profits or loss is marked to market. While marking to market, the previous day closing price is taken as the reference rate to calculate the profit or losses.

| Day | Closing Price |

|---|---|

| 1st Dec 2014 | 168.3 |

| 2nd Dec 2014 | 172.4 |

| 3rd Dec 2014 | 171.6 |

| 4th Dec 2014 | 169.9 |

The table above shows the futures price movement over the 4 days the contract was held. Let us look at what happens on a day to day basis to understand how M2M works –

On Day 1 at 11:30 AM, the futures contract was purchased at Rs.165/-, clearly after the contract was purchased, the price has gone up further to close at Rs.168.3/-. Hence profit for the day is 168.3 minus 165 = Rs.3.3/- per share. Since the lot size is 2000, the net profit for the day is 3.3*2000 = Rs.6600/-.

Hence the exchange ensures (via the broker) that Rs.6600/- is credited to your trading account at the end of the day.

- But where is this money coming from?

- Obviously, it is coming from the counterparty. Which means the exchange is also ensuring that the counterparty is paying up Rs.6600/- towards his loss

- But how does the exchange ensure they get this money from the party who is supposed to pay up?

- Obviously, through the margins that are deposited at the time of initiating the trade. But more on this later.

Now here is another important aspect you need to note – from an accounting perspective, the futures buy price is no longer treated as Rs.165 but instead, it will be considered as Rs.168.3/- (closing price of the day). Why is that so, you may ask? The profit earned for the day has been given to you already using crediting the trading account. So you are fair and square for the day, and the next day is considered a fresh start. Hence the buy price is now considered at Rs. 168.3, which is the closing price of the day.

On day 2, the futures closed at Rs.172.4/-, clearly another day of profit. The day’s profit would be Rs.172.4/ – minus Rs.168.3/- i.e. Rs.4.1/- per share or Rs.8,200/- net profit. The profits that you are entitled to receive is credited to your trading account, and the buy price is reset to the day’s closing price, i.e. 172.4/-.

On day 3, the futures closed at Rs.171.6/- which means concerning the previous day’s close price, there is a loss to the extent of Rs.1600/- (172.4-171.6) * 2000. The loss amount will be automatically debited from your trading account. Also, the buy price is now reset to Rs.171.6/-.

On day 4, the trader did not continue to hold the position through the day but rather decided to square off the position mid-day 2:15 PM at Rs.170.10/-. Hence concerning the previous day’s close, he again made a loss. That would be a loss of Rs.171.6/- minus Rs.170.1/- = Rs.1.5/- per share and Rs.3000/- (1.5 * 2000) net loss. Needless to say, after the square off, it does not matter where the futures price goes as the trader has squared off his position. Also, Rs.3000/- is debited from the trading account by the end of the day.

Now, let us just tabulate the value of the daily mark to market and see how much money has come in and how much money has gone out –

| Day | Ref Price for M2M | Closing Price | Daily M2M |

|---|---|---|---|

| 1st Dec 2014 | 165 | 168.3 | + Rs.6,600/- |

| 2nd Dec 2014 | 168.3 | 172.4 | +Rs.8,200/- |

| 3rd Dec 2014 | 172.4 | 171.6 | -Rs.1,600/- |

| 4th Dec 2014 | 171.6 & 170.1 | 169.9 | – Rs.3,000/- |

| Total | +Rs.10,200/- | ||

Well, if you summed up all the M2M cash flow, you will end up the same amount that we originally calculated, which is –

Buy Price = Rs.165/-

Sell Price = Rs.170.1/-

Profit per share = (170.1 – 165) = Rs.5.1/-

Total Profit = 2000 * 5.1

= Rs.10,200/-

So, the mark to market is just a daily accounting adjustment where –

- Money is either credited or debited (also called daily obligation) based on how the futures price behaves.

- The previous day close price is taken into consideration to calculate the present-day M2M.

Why do you think M2M is required in the first place? Think about it – M2M is a daily cash adjustment by which the exchange drastically reduces the counterparty default risk. As long a trader holds the contract, the exchange by the M2M ensures both the parties are fair and square daily.

Keeping this basic concept of M2M, let us now move back to relook at margins and see how the trade evolves during its life.

5.4 – Margins, the bigger perspective

Let us now relook at margins keeping M2M in perspective. As mentioned earlier, the margins required to initiate a futures trade are called “Initial Margin (IM)”. Initial margin is a certain % of the contract value. We also know –

Initial Margin (IM) = SPAN Margin + Exposure Margin

Every time a trader initiates a futures trade (for that matter, any trade), few financial intermediaries work in the background, ensuring that the trade carries out smoothly. The two prominent financial intermediaries are the broker and the exchange.

![]()

If the client defaults on an obligation, it obviously has a financial repercussion on both the broker and the exchange. Hence if both the financial intermediaries have to be insulated against a possible client default, they need to be covered adequately using a margin deposit.

In fact, this is exactly how it works – ‘SPAN Margin’ is the minimum requisite margins blocked as per the exchange’s mandate, and ‘Exposure Margin’ is the margin blocked over and above the SPAN to cushion for any MTM losses. Do note both SPAN and Exposure margin are specified by the exchange. So at the time of initiating a futures trade, the client has to adhere to the initial margin requirement. The exchange blocks the entire initial margin (SPAN + Exposure).

SPAN Margin is more important between the two margins as not having this in your account means a penalty from the exchange. The SPAN margin requirement must be strictly maintained as long as the trader wishes to carry his position overnight/next day. For this reason, SPAN margin is also sometimes referred to as the “Maintenance Margin”.

So how does the exchange decide what should be the SPAN margin requirement for a particular futures contract? Well, they use an advance algorithm to calculate the SPAN margins daily. One of the key inputs that go into this algorithm is the ‘Volatility’ of the stock. Volatility is a very crucial concept; we will discuss it at length in the next module. For now, just remember this – if volatility is expected to go up, the SPAN margin requirement also goes up.

Exposure margin, which is an additional margin, varies between 4% -5% of the contract value.

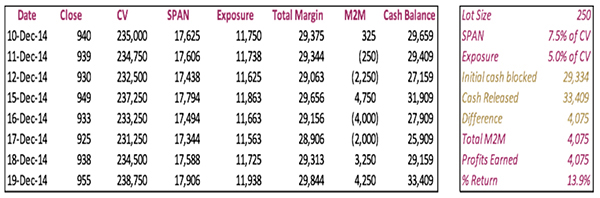

Now, let us look at a futures trade, keeping both the margin and the M2M perspective. The trade details are as shown below –

| Particular | Details |

|---|---|

| Symbol | HDFC Bank Limited |

| Trade Type | Long |

| By Date | 10th Dec 2014 |

| Buy Price | Rs.938.7/- per share |

| Sell Date | 19th Dec |

| Sell Price | Rs.955/- per share |

| Lot Size | 250 |

| Contract Value | 250*938.7 = Rs.234,675/- |

| SPAN Margin | 7.5% of CV = Rs.17,600/- |

| Exp Margin | 5.0% of CV = Rs.11,733/- |

| IM (SPAN + Exposure) | 17600 + 11733 = Rs.29,334/- |

| P&L per share | Profit of Rs.16.3/- per share (955 – 938.7) |

| Net Profit | 250 * 16.3 = Rs.4,075/- |

If you are trading with Zerodha, you may know that we provide a Margin calculator that explicitly states the SPAN and Exposure margin requirements. Of course, at a later stage, we will discuss the utility of this handy tool in detail. But for now, you could check out this margin calculator.

Keeping the above trade details in perspective, let us look at how the margins and M2M plays a role simultaneously during the life of the trade. The table below shows how the dynamics change on a day to day basis –

I hope you don’t get intimidated looking at the table above; in fact, it is quite easy to understand. Let us go through it sequentially, day by day.

10th Dec 2014

Sometime during the day, HDFC Bank futures contract was purchased at Rs.938.7/-. The lot size is 250. Hence the contract value is Rs.234,675/-. As we can see from the box on the right, SPAN is 7.5%, and Exposure is 5% of CV, respectively. Hence 12.5% of CV is blocked as margins (SPAN + Exposure); this works up to a total margin of Rs.29,334/-. The initial margin is also considered as the initial cash blocked by the broker.

Going ahead, HDFC closes at 940 for the day. At 940, the CV is now Rs.235,000/- and therefore, the total margin requirement is Rs.29,375/- which is a marginal increase of Rs.41/- compared to the margin required at the time of the trade initiation. The client is not required to infuse this money into his account as he is sufficiently covered with an M2M profit of Rs.325/- which will be credited to his account.

The total cash balance in the trading account = Cash Balance + M2M

= Rs.29,334 + Rs.325

= Rs.29,659/-

Clearly, the cash balance is more than the total margin requirement of Rs.29,375/- hence there is no problem. Further, the reference rate for the next day’s M2M is now set to Rs.940/-.

11th Dec 2014

The next day, HDFC Bank drop by Rs.1/- to Rs.939/- per share, impacting the M2M by negative Rs.250/-. This money is taken out from the cash balance (and will be credited to the person making this money). Hence the new cash balance will be –

= 29659 – 250

= Rs.29,409/-

Also, the new margin requirement is calculated as Rs.29,344/-. Clearly, the cash balance is higher than the margin required; hence there is nothing to worry about. Also, the reference rate for the next day’s M2M is reset at Rs.939/-

12th Dec 2014

This is an interesting day. The futures price fell by Rs.9/- taking the price to Rs.930/- per share. At Rs.930/- the margin requirement also falls to Rs.29,063/-. However, because of an M2M loss of Rs.2250/- the cash balance drops to Rs.27,159/- (29409 – 2250), which is less than the total margin requirement. Since the cash balance is less than the total margin requirement, is the client required to pump in the additional money? Not really.

Remember, between the SPAN and Exposure margin; the most sacred one is the SPAN margin. Most brokers allow you to continue to hold your positions as long as you have the SPAN Margin (or maintenance margin). The moment the cash balance falls below the maintenance margin, they will call you asking you to pump in more money. In the absence of which, they will force close the positions themselves. This call that the broker makes requesting you to pump in the required margin money is also popularly called the “Margin Call”. If you are getting a margin call from your broker, it means your cash balance is dangerously low to continue the position.

Going back to the example, the cash balance of Rs.27,159/- is above the SPAN margin (Rs.17,438/-); hence there is no problem. The M2M loss is debited from the trading account, and the reference rate for the next day’s M2M is reset to Rs.930/-.

Well, I hope you have got a sense of how both margins and M2M come into play simultaneously. I also hope you can appreciate how under the margins and M2M, the exchange can efficiently tackle a possible default threat. The margin + M2M combination is virtually a foolproof method to ensure defaults don’t occur.

Assuming you are getting a sense of the dynamics of margins and M2M calculation, I will now take the liberty to cut through the remaining days and proceed directly to the last day of trade.

19th Dec 2014

At 955, the trader decides to cash out and square off the trade. The reference rate for M2M is the previous day’s closing rate which is Rs.938. So the M2M profit would Rs.4250/- which gets added to the previous day cash balance of Rs.29,159/-. The final cash balance of Rs.33,409/- (Rs.29,159 + Rs.4250) will be released by the broker as soon as the trader squares off the trade.

So what about the overall P&L of the trade? Well, there are many ways to calculate this –

Method 1) – Sum up all the M2M’s

P&L = Sum of all M2M’s

= 325 – 250 – 2250 + 4750 – 4000 – 2000 + 3250 + 4250

= Rs.4,075/-

Method 2) – Cash Release

P&L = Final Cash balance (released by broker) – Cash Blocked Initially (initial margin)

= 33409 – 29334

= Rs.4,075/-

Method 3) – Contract Value

P&L = Final Contract Value – Initial Contract Value

= Rs.238,750 – Rs.234,675

=Rs.4,075/-

Method 4) – Futures Price

P&L = (Difference b/w the futures buy & sell price ) * Lot Size

Buy Price = 938.7, Sell Price = 955, Lot size = 250

= 16.3 * 250

= Rs. 4,075/-

As you can notice, either of which ways you calculate, you arrive at the same P&L value.

5.5 – An interesting case of ‘Margin Call.’

For a moment, let us assume the trade was not closed on 19th Dec, and in fact, carried forward to the next day, i.e. 20th Dec. Also, let us assume HDFC Bank drops heavily on 20th December – maybe an 8% drop, dragging the price to 880 all the way from 955. What do you think will happen? In fact, can you answer the following questions?

- What is the M2M P&L?

- What is the impact on cash balance?

- What is the SPAN and Exposure margin required?

- What action does the broker take?

I hope you can calculate and answer these questions yourself; if not, here are the answers for you –

- The M2M loss would be Rs.18,750/- = (955 – 880)*250. The cash balance on 19th Dec was Rs. 33,409/- from which the M2M loss would be deducted, making the cash balance Rs.14,659/- (Rs.33,409 – Rs.18,750).

- Since the price has dropped, the new contract value would be Rs.220,000/- (250*880)

- SPAN = 7.5% * 220000 = Rs.16,500/-

- Exposure = Rs.11,000/-

- Total Margin = Rs.27,500/-

- Clearly, since the cash balance (Rs.14,659/-) is less than SPAN Margin (Rs.16,500/-), the broker will give a Margin Call to the client, or in fact, some brokers will even cut the position in real-time as and when the cash balance drops below the SPAN requirement.

Key takeaways from this chapter

- A margin payment is required (which will be blocked by your broker) as long as the futures trade is live.

- The margin blocked by the broker at the time of initiating the futures trade is called the initial margin.

- Both the buyer and the seller of the futures agreement will have to deposit the initial margin amount.

- The margin amount collected acts as leverage, as it allows you to deposit a small amount of money and take exposure to a large value transaction.

- M2M is a simple accounting adjustment; the process involves crediting or debiting the daily obligation money in your trading account based on how the futures price behaves.

- The previous day closing price figure is taken to calculate the current day’s M2M.

- SPAN Margin is the margin collected as per the exchanges instruction, and the Exposure Margin is collected as per the broker’s requirement

- The SPAN and Exposure Margin are determined as per the norms of the exchange.

- The SPAN Margin is popularly referred to as the Maintenance Margin.

- If the margin account goes below the SPAN, the investor must deposit more cash into his account if he aspires to carry forward the future position.

- The Margin Call is when the broker requests the trader to infuse the required margin money when the cash balance goes below the required level.

Correct if wrong.

1) Contract value = Price × lot size

2) Margin = Contract value ÷ leverage

3) leverage= Contract value ÷ margin

Yup, thats correct.

pranam karthik sir,

what a wonderful teaching. i just felt, U R sitting in front of me and explaining me details. Thank U Sir.

Thanks, Madhav. I\’m so glad you liked the content, happy learning 🙂

thank you sir for this wonderful explanation but i have one question suppose I buy a futures contract at ₹100 expecting it to go up to ₹120. I keep ₹10,000 as margin (10% of total value, lot size 100).

Now, if the price actually reaches ₹120, I get ₹2,000 profit credited to my account. But if the next day it falls to ₹80 — how will this ₹4,000 loss be adjusted? Will it be deducted from my earlier profit or directly from the margin?

If the loss is deducted from the margin, then a margin call will be triggered, right? Since ₹6,000 is less than my exposure margin.

Yup, thats right.

Yes, it will be taken from the margins parked Arnav, which means you will have to top up your margins again.

Hey Mr. Karthik! Lovely work what you\’ve done here.

I had a query, now consider SILVERMIC expiring on 28NOV25. currently at Rs. 148298

Span Rs. 14,818

Exposure margin Rs. 1,854 (approx 1.25%)

Total margin – Rs. 16,672

What I understood from this Chapter; is that the Broker sends out a Margin call when Exposure Margin gets used up.

Let us assume SILVERMIC drops by 2%; – RS 1,45,332

This translates to a loss of Rs. 2967 to my margin – Rs. 13705

Now since this is above my exposure

New Span – Rs.14533

Do I get a margin call here? or will Zerodha square off my buy position?

This is in a scenario that I would have enough funds to cover this loss, say rs 10,000 standalone. Will they use this up?

Yes, the mandated margin should in place for you to continue holding the position. Else, in case of any shortfall the broker will square off the position.

Hi Karthik, i have a small doubt, is there any chance that a trader can hit a negative loss in his margin and that the RMS takes time to adapt to the market movement and we could hit a negative balance and own the money to the broker? as the RMS can react to the market movement but not predict it. Please correct me if my understanding is wrong somewhere

Yes, while there are checks and balances in place to ensure this does not happen, it can still happen. Especially when there are large price movements, in a short period. If you were trading in 2020, then you\’d know that Crude Oil went to the negative territory, and many brokers across the world took a hit, exactly for this reason.

Do we have to pay the remaining amount after giving the margin amount?

Not really, you hold the position with margins itself.

For eg – Margin required 1 Lach for HDFC 100 Shares at Rs 1000.

Day 1 – stock goes to 1020 – Profit 20* 100 = 2000 Will be added to the available Balance correct ? Can that be used for any other buy. While keeping some money for any drop in the share ?

Day 2 – New Price of HDFC share 1020 – Will the margin which was required to buy 100 shares was 1 Lach will that be now increased in the back end and interest would be charged on the revised Margin given. In this case it was 1 Lach will that remain same even if the stock goes 1100 from 1000 ?

And if the HDFC stock falls to 900 from 1000. M2M would 100 per share loss which would be debited from account end of day. What happens to margin ? Next day price would be 900 and margin taken was 1 Lach against 100 shares @1000 willnow margin would be re-calculated as per 900 buy price and hence the margin and interest would be reduced ??

Margin too changes based on price and volatility of the stock. In fact it changes multiple times in a day. Its best if you dont plan to take trades based on the P&L of the position. Also margins will be blocked as long as your position exists.

During drastic intra day price movements Can you square off my F&O positions without giving me a reasonable chance to make good this margin erosion ? As per NSE Clearing don\’t I have T+1 after 10:30 to pay this shortfall?

If the margins are triggered, yes, brokers can do that.

yes. i have . for example i have 4lakhs fund in zerodha. and i purchase stocks worth Rs 40,000/- only. it shows that i have used Rs3,00,000/- margin. now margin left is only Rs 1,00,000/- .. moreover it says now i can put order only worth Rs 10,000/-. any idea why so ???

Maybe you had someother positions? Best to check once with support desk.

i only do cash purchase in equity. NO FUTURES/OPTIONS. STILL ZERODHA ASKS FOR MARGIN EVERYTIME I PUT A BID. WHY??

You need to have cash in had to purchase securities 🙂

How\’s this span margin calculated 17438 ?

Based on your entire portfolio.

I want to ask few questions. I bought 70000 value HDFC shares in cash market. I pledged them and got margin to trade F&O. I don\’t have any other cash balance in my trading account. I want to trade one lot of nifty futures. Should I trade without infusing any money or will I get charged interest by zerodha.

Situation 2

I bought 35000 value G-sec and 35000 value of quity. I pledged both of them. Can I trade one lot of nifty futures? Do I have to maintain additional cash balance.

I am not able to fully understand the concept 50% margin is available from pledging shares. Rest 50% to be maintained in cash or cash quivalents. Can you provide me the list of cash quivalents acceptable in zerodha.

Check this – https://support.zerodha.com/category/console/portfolio/pledging/articles/pledging-terms-of-services#:~:text=When%20using%20collateral%20margin%20to,cash%20component%20funded%20by%20Zerodha

Yes, there is an interest of 12.775% per year or 0.035% per day.

Sure. Thank you.

Happy learning 🙂

Understood. Thanks for your inputs.

Cheers, good luck. Let me know if you have other queries.

Hi Karthik,

I have a doubt regarding GTT. Scenario is below.

I bought the SBI future at the closing price of 830. I create GTT with the stoploss of 820. Now on second trading day, this Future contract is opening at 810 which is below my stoploss. So at this time, what will happen to my open GTT order? Will it get triggered at 810 or it’ll wait for the price to come to 820?

It will be triggered at the specified price, Sajid.

Who will pay margin call if the buyer is not able to meet it?

The trader who initiated the position has to pay.

For 14th December, from where will the exchange generate M2M of Rs 4,750?

They will be M2M up until the position is open.

This was wonderfully explained. Such detailed eg and explanation is not present any where on youtube. Loved reading this content here. Thankyou Zerodha Varsity and the whole team, you guys are doing great work by educating people and that too in such a fantastic way!

Thanks for the kind words, and I\’m glad you liked the content on Varsity, Pooja. Happy learning 🙂

Hi sir

If future headge with option than M to M margin required. If my trade goes to wrong direction.

Futures will have mark to market, Gulshan, regardless of hedging or not.

Hi Karthik,

I dont know anything about stock market. If i start learning from today in how many months can i reach to a point where i can earn atleast 2 lakhs per month or 8lakhs per 4 months(if it is quareterly based style for holding long positions etc.,) and i want to do this full time like a regular job. once i am done understanding some basics from this varisty, where do i start my journey from. Of the total chapters read till Futures, i am able to grasp 50 percent. how many hours do i have to spend a day during the learning phase. plz guide me with detailed path.I mean how to make my own golden forumula or strategy/stratgies to apply in the market. There are many people in the market who are giving calls for stocks to hold for 10 days to 3 months and i did some paper trade and found that such calls yielded good results. I dont want to settle by grabbing such calls and make few bucks. I want to know – How are they anticipating that this particular stock is going to increase and how they are able to pinpoint or drill down to 4 to 5 stocks among thousands of stocks. I am amazed. is that a team work..would i be able to do it alone. Please answer.

Ravi, I wish I had an answer for you. The reality is that no one can fix a Rupee value target and say I\’ll acheive this every month. Its nearly impossible and besides, it adds a lot of stress. Also, while some take years to understand and get comfortable with markets, some only take few months. It varies for each person, and there are no fixed timelines.

I hold the stocks of a X company which is equivalent to its one future contract quantity. if I short the futures will there be a margin required for that trade even after holding the stocks required for settlement?

Yes, margins will be required for the trade Raja.

Can anyone explain me how margin is calculated for option selling, the examples given here are all for long trades , so how\’s it calculated for shorting the options?

Option margins for sell is similar to futures margins.

Hi, with M2M, it\’s like the position is squared off everyday at market close. And margin for intraday is lesser, when our why would you opt for nrml rather than buying intraday every morning and squaring off each day?

You could do that, but some of the large moves tend to happen at open (gap up/down), so you may miss that if you dont hold the position.

Hello,

I don\’t know if the question is already asked or not (if it is then sorry to ask again) but let\’s say I buy a stock future of \”xyz\” which has lot size of 100 at price Rs. 100. Let\’s assume it increased to Rs. 102 in 10 minutes from the time I buy on the same day. I assume my profit will be (102-100)*100 = 200. My position is now 10200 from initial 10000. My question is if I decide to terminate the trade (i.e sale the future) when will I get my profit value 200 in my account and when will the margin be released (which by SPAN and Exposure margin will be 12.5% of the contract value i.e.). Is the total value (initial margin + profit) instantly available? Can I use this money to buy another contract in some other stock?

Yes, you can.

Thank you for the content, really elaborate. But I suppose I am the backbencher here, but will still go ahead and ask this question-

1. I purchase HDFC Banks future current price INR 900 size 550 with initial margin blocked for INR 151000 (I had 151000 in my trading account). Now my cash balance in trading is 0. Will I be allowed to hold future position for lets say next 10 days?

2. Same as above, but this time I have 5000 in my trading account, now the price moves to 100 from 900, will I be required to add money to my trading account?

3. Is the future contract holder required to add cash to his trading account on a daily basis based on the M2M?

4. And on expiry how does the Rollover work? Do we need to need to purchase the underlying or automatically next months contract is allotted?

1) You can, provided you dont have a margin call. But I\’d suggest you have some buffer funds as margin.

2) Not really, as the prices have moved in your favor.

3) Yes, thats only if the prices are going against your position or if the volatility has shot up and therefore the margin requirements.

4) Here you go – https://www.youtube.com/watch?v=FqRB7NGnOtA

Hi Karthik, I had 500 lots of USDINR 83 CE MAY expiry and 250 lots of June USDINR Future. As the asset increased by 0.5 Paisa rapidly in a day, I exited the 250 lots of June Futures with profit. Had around 15 lakhs margin. Got a MSG in the evening that margin required now is 17 lakhs and to transfer funds or else the position would be squared off. Somehow managed to tranfer funds.

Now for hedging is it a good idea to buy futures in the next trading day son that the margin required for the CE becomes less???

If the idea is to hedge, then maybe you can initiate the position at the time of taking the trade itself?

Then can you make a module for OTC market also. how different from Central Exchange market? The risk involved in OTC market compared to regulated market. That will be really helpful for my studies because I am learning many Basics thing in your module which is highly correlated with my studies.

There is no OTC market as such which is accessible for retail, Ram.

Hey Karthick,

I follow Zerodha Varsity monthly and learn many new things from your modules, so thank you for your efforts to help us understand the market. Correct me if I\’m wrong, but in India, when losses go below the Exposure Margin, a Margin Call is issued. However, in the U.S., a Margin Call occurs when the losses go below the Maintenance Margin. Is that right?

Thanks Ram. Not really sure how it works in US.

Great explaination in the simplest way possible

Happy learning!

In FNO trade you gave the example where I buy at one price and 4 days later sell at a higher price earning a profit. In between, the M2M factor comes in. Whatever amount is credited or debited from my cash with you is accounted for in my books as a C/Asset, be it a negative or positive balance. At the end of the year how do I square off this account? Adjust it with my total profit/loss? Then my P/L account as in the example gets increased or reduced. Is this concept correct?

You will either have FO profit or loss and your tax P&L should give you this information. Of course, your CA can help you with this.

Sir,

?

If I have a collateral against Liquid Bees, could it be used for MTM cash margin if cash is below to SPAN Margin in Zerodha

Not for now, Rahul. Hopefully sometime in future.

is there any chance that my long position cannot be squared off in case of extreme loss over 12% daily and may carry upto expiry mounting the losses.

5

That can happen if the liquidity dries up.

Thanks Karthik, but if you can specifically answer for 2 & 3. Mentioning it here again:

2. “Also, the profits are released when you terminate the trade completely (at least in Zerodha) and not while you are in the trade” – does this still hold true after 8 years? I mean, we cannot withdraw M2M profits?

3. SPAN+Exposure margin needs to be maintained during the whole time when market is open or only at the end of the day during M2M? Let me illustrate the question with an example,

let\’s say the margin collected > SPAN at the start of the day as well as at the end of the day

but if in case of excess volatility, during the middle of the day price fluctuates to the extent that margin gets then position will be squared off then & there? Or it will only be checked at the end of the day?

1) M2M can be withdrawn on T+1 basis. But there is no M2M with options and the profits are realized only when you square off the trade.

2) It should be maintained for as long as you have an open position. If you have a position, do constantly check for margin requirements. It shoots up intraday when there is excess volatility.

Hi Karthik,

Where can I get information around MTF – is there any article around the same?

Nothing for now, Rahul.We dont really do MTF.

Hi Karthik,

Amazing content. I have couple of questions:

1. Is everything mentioned in the chapter still holds true in 2023? I mean, this chapter might have been written back in 2014

2. \”Also, the profits are released when you terminate the trade completely (at least in Zerodha) and not while you are in the trade\” – does this still hold true after 8 years?

3. SPAN+Exposure margin. needs to be maintained during whole time when market is open or only at the end of the day during M2M?

Most of the things are conceptually true even today. These are building blocks of futures. Small nuances change and that keeps happening as and when there are regulatory changes. For example, the biggest change is the way settlement is done for F&O contracts.

Hi Karthik,

\”Also, the profits are released when you terminate the trade completely (at least in Zerodha) and not while you are in the trade\”

– does this still hold true after 8 years?

Yes, thats still true. Only change, I\’d rather use the word square off instead of \’terminate\’ 🙂

I tried it but sometimes it shows something and sometimes something else. I think it is not reliable because it took expiry of option accurately but regarding future it does not . for example ,i had nifty 50 future long position expiring on 30 November and also had option put ITM expiring 16 November . although it hit target but max loss was showing different at different times .

Can you check once with Sensibull?

sir , I am a nifty future swing trader . generally i have hedge positions future hedged with option . the loss is capped but I am afraid of M2M , can it lead to unlimited losses while the loss is capped ?

I\’d suggest you enter these positions on an app like Sensibull and see how the P&L behaves. You will get a fair idea on the max loss 🙂

For index futures, the margin is calculated based on the current level/price of the index or the futures price?

For e.g. Current price is 15180 and the futures price is 15000. 30 is the multiplier.

Margin is 10 % and maintenance is 5%

So we calculate the value and margin of the contract based on 15180 or 15000?

Its based on the future prices.

Hi,

Can you please tell me how the margin call will be financed ? Whether it should be financed through bank transfer or pledge margin (cash component) is enough ?

Transfer from your bank account linked to trading account.

Sir, in options margin if the required margin in 150000 and final margin is 80000, can I still use the remaining required margins after executing and final margin is blocked from required margin.

To sum up ; Required margin – 150000

Margin required – 80000

After execution 80000 is blocked, then can I use for trading the remaining 70k.

Yes, you can use the margins released once the margin benefit kicks in.

The example calculations on Varsity android application for this particular module are wrong in my opinion. Did anyone check?

Can you highlight the issue, please? Thanks.

Sir , in another case, if my opening balance was 50 thousand and a Future margin cost 50 thousand same price as my whole balance. In this case , when am I likely to get a margin call, how much out of 50k when I loose am i going to get a margin call.

You will start getting margin calls as and when the position goes against your direction of trade. I\’d suggest you call the support desk for exact % levels.

Sir, now it\’s October and if I trade 23rd November future, even though it is October I can hold my trade till November 23rd right.

Yes, you can. As the contract mentions, the expiry of the Nov contract is in Nov.

nice compilation, very nice examples, good study material, proper flow of topics and their details. Great job. Very very thanks to all the team of Zerodha varsity for providing such an excellent study material. Thanks

Glad you liked the content, Doctor. Happy learning 🙂

Dear Karthik

I have pledged 10,00,000 Rupees worth of Nifty bees through my broker and I received 9 lakhs as margin to make position in F&o segment by which I have go long in Nifty futures but the next day Nifty is going down by 2% then I am in MTM loss of approx 2 lakhs but I have not any cash in my trading account Only I have margin worth of Rupees approx 8 lakhs can the loss is adjustable in margin or I have to pay in cash.

Please clarify this.

Do check with your broker once to figure their RMS policy, Shivam.

Dear Karthik

In case, heavy gap down in the morning, and client have only IM (SPAN + Exposure) say 12% in the account as per stipulation. In case, gap down is 18%, how the broker will recover the money i.e. 6% of the contract value. Client doesn\’t have any other funds in the account or doesn\’t hold any position. You will square off and recover 12%, is okay but what will happen with the rest 6%. Just an academic question.

The position will be squared off and the client is liable to repay the broker.

To buy nifty future, around 1 lac margin needed.

For that, I got around 5 lacs as margin( not as cash)

Suppose, worst case scenario in the history, 2008 fall and market fall 50%. So contract point of view, I am at loss of around 4 lac on m2m basis.

At that time, I have only 1 lac as cash.

Then what would happen?

Zerodha gives me atleast one evening to move money of 3 lac from bank( I believe it is must, right?) to zerodha or zerodha would Square off the position in the absence of cash?

If have enough margin,

How much cash money required in zerodha to avoid unnecessary Square off?

Moment M2M loss crosses 70%, we alert customer Pratik.

in the open positions section in zerodha, i can see the current profit and loss of these futures. That profit and loss is with respect to my entry price. So even if i check it 1 week after entry, it shows my current situation with respect to my entry price. However, my funds in zerodha will already include my profit/loss till the previous day because the margins are being settled daily. So if i exit now, I will only get whatever is balance for that last day. Is that right? (i hope ive been able to put my doubt clearly for you)

So you get the net P&L i.e.the difference between entry and exit price minus all the applicable charges. In Future, everything is marked to market, so when you exit, you will get whats the balance for the last trading day.

Isn\’t the leverage 5 times in Zerodha? Because in Futures the Contract value for NIFTY is 882500(17650*50) but margin is much lower (near 100000) and in case of options, margins for 17500 CE is around 80000. I understand that the volatility is lower but still 5 times leverage means margins should be around 176500 right? Or am I missing something here?

Yes, that\’s a recent regulation. I will have to update the content 🙂

I\’m assuming this span & exposure are calculated keeping in mind the worst case scenario’s, that is, the upper and lower circuits right. Cause this is the only reason it makes sense that if I\’ve collected or locked a certain amount then within a day what is the worst thing that can happen and as a regulator I\’m able to clear all the obligations from my end. Correct me if I\’m wrong.

There are no circuit limits for derivative contracts Shubham.

Future 1 lot stop loss ke saat (Interday ) buy-selle ke liye D mate Acount me kitna balence hona chaahie.

Example. Share praice 400 hai.

100 ka lot size hai.

Buy praice 400 hai

Stop loss 5 rupe niche hai.

Stop loss hit hone par 500 loss hoga.

(Acount me kitana paisa hona chaahie) .

In a short options trade, when does Zerodha actually square off the position – when the cash balance falls below SPAN or below SPAN + EXPOSURE?

In other words, can we keep a short options position in Zerodha as long as we have cash balance that covers SPAN margin requirement?

You need to maintain sufficient margins in your account, this can be in form of cash or both cash + collateral margin. As long as you\’re maintaining sufficient margins, the position won\’t be squared-off. We send margin call email/SMS if the required margin exceeds the available margins in your account. Ideally, you should add the funds immediately to avoid square-off.

Do check this – https://support.zerodha.com/category/trading-and-markets/margins/margin-leverage-and-product-and-order-types/articles/square-off-by-zerodha

I read the complete futures module and went for a trade. Got to know with a loss..you didn\’t explain gap up and gap down scenario with futures…in an example you are explaining the pnl calculation as if one stock is opening at the same price which is previous day\’s closing…what if one short sold the future at the last hour on a trading day being bearish and then next day there was a gap down opening in the stock of 1-1.5 percent which is normal. A stock being closed at 3340 on one day and being opened at 3290-3296 on next day is not very unusual. Stock price starts to rise and went to 3305. Trader preferred to exit the trade. As per your fourth method of pnl calculation he should be in profit since he short sold at 3340 and bought back at 3305. But with m2m logic he would be in loss. Broker also says m2m is used for futures.

As long as the price is below the previous day\’s reference price, you are in profit right? Here 3340 is the reference price, you\’d still make a profit if the stock trades at 3305.

ASSUME I BUY BIRLA SOFTWARE TWO LOTS @307 ON 1-12-2022 FOR FUTE JAN 25.2023 NOW PRICE IS KEEP ON DECLINING. IF I TAKE DELIVERY OF STOCK ON 25TH JAN 2023. THE STOCK WILL BE AVAIALBLE TO ME @ RS 307 WITHOUT ANY LOSS TO ME. SAY PRICE IS ON EXPIRY IS 280. IT MEANS I WILL GET STOCK AT 307 AND DELIVERY WILL BE TAKEN BY ME BY PAYING PRICE @ RS 307

PL CONFIRM, IF IT IS OK

No, you will have to take delivery at the settlement price, of the expiry day, in your example, it is 280.

Splendid work, thanks for sharing this info, it\’s very clear and easy to understand with explainations provided.

Thank you.

Happy learning!

Hi…In the varsity application…in this particular chapter…the calculations in HDFC Bank examples are wrong…The contract value calculation is correct…but the Span and exposure margin calculation is wrong….And many thanks for this absolutely incredible knowledge..Much support to zerodha team

Checking on this, Jay.

In the video session you mentioned about buying a particular months contract and selling the next month contract to reduce the margins but what will be the effect on the profits and the losses made. Please do help me understand this part.

When you initiate a spread position, your risk and reward will be limited.

Outstanding explanation!

Better than Investopedia!!

Happy learning 🙂

What is difference between required margin and final margin??

Its now replaced by SPAN and Exposure margin, Ankit.

Hi Karthik,

If the Pran margin amount goes below zero, and I don’t want to re-infuse any money, will I get back my exposure m@rain money by squaring off? Or that money too has gone. Thanks

Margins will be released back, Prasenjeet.

Do the same margin and M2M principals apply for Intraday trading?

Yes, it does.

hello sir, i want to ask that

whenever we take trade in futures our margin amount gets blocked and we cant use that money in any other work, but here above it is written if we do not maintain the span margin in our demat we will be charged with penalty, but how\’s that possible. if we have to enter into the trade we should have sufficient balance in our demat and thats get blocked.

\”SPAN Margin is more important between the two margins as not having this in your account means a penalty from the exchange.\’\’

Yash, there are few situations where the margins may increase more than the blocked margin (for example volatility of stocks shoots up and exchange imposes adhoch margin). So in such situations, the penalty may increase.

Thank you Karthik, can u pls clarify on this bit please \”Who is the counterparty incurring a loss in the transaction?\”

The counterparty can be anyone like you and me. Its just that they have an opposite view compared to yours.

Hi Karthik, Thanks a lot for the wonderful content. I have doubt with \”Futures is a zero-sum game\” statement. Suppose am buying futures, that means there is someone who is selling me, he may be shorting or squaring off his long position. Now if the price goes up, I will be making a profit, while he would be making a loss(my understanding), if shorted, but what if he was squaring off his long position? I am sure he doesn\’t incur any loss as he has squared off. Who is the counterparty incurring a loss in the transaction? Thank you in advance.

Ah, it is not in that context Raj. When you buy and hold stocks and the stock price increases, new wealth is created for shareholders. In futures, wealth just oscillates between buyers and sellers, no new wealth is created.

Do I read this document or it\’s better to go for VARSITY which is available on play store?

Which one is beneficial…?

Both are the same, Miquail.

In Intermidiate Quiz ((Future trading) of Varsity app, there is a quation No 6 \” At the trader shorts ICICI bank futures at 383, the stock closes at 379 for the day andcopen at 385 the next day. What is his M@M P&L ?

Ans. Is given as \”A profit of Rs 4/\”! But how? pls explain.

Manoj, short at 383, and close at 379, so an M2M profit of Rs.4/- for that day.

Um… I\’ve been learning through the varsity application and I\’ve really loved it all … So just wondering if there\’s also one where we can get similar learning opportunity about NFT, crypto, real estate and so on….

Not for now, Chetan. Guess I need to learn about this first myself!

Beautifully articulated and really helped me to understand the concept of margins and M2M.

But still, I have a doubt that if I take multiple future trades i.e buy and sell in a day how will be this calculated?

For a particular script the Buy price – sell price = P/L OR the overall buy price avg – overall sell price avg= P/L for the day.

Glad you liked the content, Sagar. If you take multiple lots, then the P&L is based on the average buy and sell.

Sir, th auto sq. Off conditions?

can\’t they wait for 2 trading days. Or pay it off till client replenishes it back.. 2ndly if it\’s loss for continous 10 days then how❓ it works

Nope, not possible Rizwan, this will be too much of a risk to the broker.

Hii Sir,

->How long will the broker wait for us to infuse funds to cash balance after the margin call?

->How will the Margin calls be done,is it through phone calls,mails,SMS,etc?

Depends on how your margin utilization is. If it is within the limits, the broker gives you a bit of time, but beyond a certain threshold, the broker will cut the positoion.

Ok thanks sir

Good luck!

Hello sir,

I have doubt in MTM loss in option selling , if ENd of the trading day my MTM loss is Rs 10000, in my trading account funds avilable only Rs 1000 ,

But having equity collatral l 15000 Rs, liquid collatral worth 120000 Rs , margin blocked for this trade was 40000 Rs,

At above condition what will happen end of the day sir

Prashant, there is no MTM when you sell options. In fact, M2M is just for futures.

Hello sir,

I have doubt in MTM loss , if ENd of the trading day my MTM loss is Rs 10000, in my trading account funds avilable only Rs 1000 ,

But having equity collatral l 15000 Rs, liquid collatral worth 120000 Rs , margin blocked for this trade was 40000 Rs,

At above condition what will happen end of the day sir

The MTM loss will be debited on the ledger. You\’ll be charged delayed payment charges for the debit balance till you clear it by adding more money or sell stock.

I booked in option selling but in ledger it shows debit of amount in net obligation …please explain

Yes, that means to say your funds are taken in for taking delivery obligation against your option position. Please do call the support desk, they will help you with it.

What if I cannot answer the Margin Call from the broker because I am busy with some other work? Will the broker wait for my call before squaring off?

No, thats too much risk right?

Excellent explanation, thank you for all your efforts.

Happy learning!

kindly guide me. above hdfcbank example valid in current margin rule where SPAN AND EXPOSURE both need to get reported to exchange

Yes, SPAN and Exposure are set by exchanges now. Still valid.

Please take proper lesson on new margin rule. According to the research that I have conducted so far most of the option seller stay\’s away from option selling because they don\’t have proper knowledge on option margin. At first zerodha calculator show less margin requirement and the margin keeps on varying after taking the position. So most of the people lost trust in zerodha. Before september it was not the case. If you already have any article regarding this mail me those article.

Please do check this, Venkatesh – https://support.zerodha.com/category/trading-and-markets/margin-leverage-and-product-and-order-types/articles/upfront-margin-requirements

Require clarification from your side that when there is Existing Position in Futures and on a particular day there is no new trade transaction, however, the rate of existing stock (trade) increase by 4% due to which Margin Penalty was there despite having M2M (Profit) on a particular day due to increase in price.\”

As per Above HDFCBANK Example There Must be no penalty or margin shortage.

Is there is any change IN rules for exchanges.

Did you have any open long call options that day? Either way, I\’d suggest you call the support desk for this.

Hello,

I am long in futures with enough cash balance, support the market falls and to avoid margin call, can I go short on futures, so will this compensate the M2M profit or loss?

Long and short future will offset your position 🙂

Can I the margin be 100% pledge margin?

Not possible. Please check this thread – https://tradingqna.com/t/requirement-for-50-50-cash-collateral/66248

whether option buyer get the m2m profit or not

Is it m2m applicable to equity ?

Yes, applicable to all futures contract.

Is it applicable to equity ?

I\’m guessing you are referring to EQ futures, yes, it is.

Hi Karthik,

If I Pledge shares with the broker, then can I get margin to trade in futures ? Also, in this case, how does P and L a/c gets settled on daily basis if I do not have a cash balance? Or it is necessary to maintain cash balance always ?

You have to maintain at least 50% in cash from your side, Kedar.

Thank you so much Karthink for such great content. Duly appreciate it.

I had a samll doubt. Its quit eevident that one must manitain some cash balance over and above the margin required to buy futures. Can you specify what amount of cash balance over and above the margin requiremnt would be sufficient? (As a %age of contract value)

Hmm, depends on the volatility of the underlying. Higher than volatility, higher buffer and vice versa. Can range between 5-10%.

And if both SPAN + EXPOSURE is decided by the exchange, that means that the required margin for F&O across all brokers will be same, unlike cash segment, right?

Thats more or less right, things are standardized now.

So in the example you mentioned of buying HDFC Bank Futures, on 10th Dec 2014, the total cash balance at the end of the day was Rs 29659. But the required margin was just Rs 29375. So the entire cash balance of Rs 29659 will be blocked or only Rs 29375 will be blocked and the rest we can use for another trades?

Only to the extent of margin required.

The word for making things better is \’improvement\’ not improvisation.

Noted. Thanks for correcting me.

Hi Kartik,

Want some more clarification for M2m.

Eg. I sell current month nifty future according to technical calculations. On that day it should give 100 points where as it didn\’t reach instead it went against the trend. I achieved target on 3rd day of trading.

How to calculate m2m. ?

EVERYDAYS CLOSING – traded day or

Previous day closing – opening of next day

Everyday closing is the reference price. So for today, it will be the difference between today\’s closing and y\’day closing multiplied by lot size.

Thanks for Reply Karthik but my question is not answered exactly. Please re-visit my question once. I want to understand that FOR SAME DIRECTIONAL VIEW for same security (SBI) when you are trading in futures you are getting 20.7 and when you are trading in spot you get 20.0. Theoretically, for same information there should not be different profit.

But these are two different instruments with two different payoff right?

Consider the below example:

Say in February SBI spot is trading at 300 at 9.30am and its April futures is trading at 310 (implied interest of 3.33%). Now at 11.30am spot went up to 320 and at 3.33% implied interest futures should be traded at 330.7 (ignore other things like brokerage, speculations, etc.). Now consider trader A who has longed at 9.15 in spot and at 11.30 he squares off. He gains Rs.20 (320-300). Now consider trader B who has longed at 9.15 in futures at 310 and at 11.30 he squares off. He gains Rs. 20.7 (330.7-310). The difference of 0.7 (20.7-20) is due to interest of 3.33%. Now, as per mark to market explanation trader B should get Rs.20.7 TODAY and trader A should get Rs.20 TODAY. So essentially, trader B receive interest of Rs 0.7 TODAY itself i.e. he doesn\’t have to wait for 2 months for receiving the interest amount. This is logically bothering me and my question is why MTM payable/receivable TODAY is calculated is not time adjusted?

The P&L for derivatives trade is settled on T+1 basis, meaning you will get the funds the very next day. No need to wait till the expiry of the contract.

What happens to my Future contract and balance if a stock crash overnight?

Suppose I have a Future position with 20 Lakh paid as M2M with a contract value of 100 Lakh. Suppose the stock crashed overnight (fraud, bankruptcy) and the stock start trading lower circuit to circuit with no liquidity in Futures for several days.

Now even if my position is squared off, my balance will be negative in 60 Lakh. As a client, what will be my liability at this point? Can I just forget about the negative balance and let someone else bear the loss instead?

What usually happens in such scenarios in real life?

In the event that you are unable to exit, then the position will be settled based on the settlement price available post expiry. You will be obligated to take delivery or give delivery of the stock based on the position you\’ve taken.

thanks a lot for making it simple and easy to understand …….

Good luck, Paridhi, happy learning 🙂

is seller have to pay some kind of margin?

Yes, margins are applicable to both long and short positions.

Thank you for your reply.

In case i use the pledged margin to buy shares worth Rs. 90,000, in how many days do i have to transfer the funds for this?

Please advise.

There is no time restriction as such.

Hi,

I have some basic confusion on shares pledged against margin.

If I pledge a scrip whose current market value is Rs 1 lakh , after 10% haircut, I will be eligible for a margin of Rs. 90,000 which i can use for trading.

Do I have to then pay the Rs. 90,000 back to the broker in a stipulated no. of days or can I continue to use the margin without any payin as my shares are pledged as collateral?

Please advise.

Thanks.

YOu can continue to hold the pledge and use the margins, Rahul.

Hi Sir,

Can you explain when the Span & exposure margin return in d mat account ? When ever I sold the future then same day SPAN & exposure margin will credit back to d mat or it will take time ?

Regards

Shamshad Rizvi

It will be released the same time. Any profit or loss will be settled by end of day.

But how can it be settled, since I don\’t have the adequate funds to receive delivery , and since there is no cash settlement, the counterparty has to deliver and i have to pay for that delivery, but due cash shortage I cant actually take the delivery and neither have i sold my position before expiry , so i am in a fix.

In the absence of sufficient margins, the position will be squared off by the broker. To avoid being stuck, the action of checking for margins and sq off the position starts 3 days before expiry. It is highly unlikely that the trade wont be closed in 3 days.

So if the order remains pending(since no buyer ), and i dont have the money to receive the delivery, what will be the scenario then.

It will be settled at expiry. Remember when you transact, there is a counterparty to the transaction. Upon expiry, everyone has to settle that.

Sir,

All through learning @varsity i feels indebtedness towards you, I truly regard you as Guru, the way you taught is awesome.

Hey Roshan, thanks for the kind words, I feel humbled. I hope you continue to learn and enjoy reading the content on VArsity 🙂

What is the probability of this case happening. Since i am just starting to look into future, i am caught cautious of these cases where i cant find buyer/seller to square off my position.

Happens if the instrument you are trading is illiquid.

One doubt that i have is, for ex – if there is a drastic downward movement of a stock and cash balance falls below SPAN requirements. in this case , broker will square off or sell off my position ,right, just wanted to confirm that that there must be a buyer for my squared off/selling position right, otherwise it wont get squared off, i know markets have a lot of people, but in case there is no buyer for my position that the broker has to square off, what happens in this case, if this case happens (assume).

Yes, in that case, the order will remain pending. This is a risk to the broker as well.

From this can we understand that our money will never become zero or negative because broker has square off our position when it reaches below SPAN ?

That\’s right, but if there are sudden and drastic price moves, then it will be tough for the broker to manage these positions as well.

Dear Sir,

So Divis Lab 25/02/21 future closed at 3720 while the settlement price is 3696 on 03/02/21. Please see attached imaged below.

I understand by the future costing, the near month contract is much above its fair value. Is this a good arbitrage opportunity to sell the future and buy the spot?

Also assuming if I have bought the future contract at 3715 while my M2M be 5 X lot size or 19 X lot size?

https://imgur.com/a/UM3fYG5

Yeah, you can sell Fut and buy spot, but assuming you lock in the difference, you need to check if its good enough to make up for the costs incured. If yes, then there is a small trade opportunity.

I want to know , if the expiry of an X share is 23 Jan and I have bought 1 lot on 15 Jan , on 16th Jan when I sell the holding booking some profit say 2%, and on the next day , ie . 17 Jan the price rise by 1% , the person who has bought the 1 lot from me gets the profit of 1% , right? . Then am I liable to pay him that 1% ,as I have sold it to him ?

If Yes then , what is the use of squaring of my trade before expiry..

Please answer

No, once you sold the contract, you have no further liabilities.

Respected sir,

Thank you for this outstanding work .thank u very much.your teaching is best.

I think u made a mistake on same topic in varsity app. You took cash balance of first day after closing price as sum of margin amount w.r.t closing price & m2m profit or smthmng else i cant found.

From above (varsity web) perspective it should be sum of margin amount at the time i bought future before closing & m2m profit. Due to this there is mismatch in final profit calculation. You stated initial blocked margin mismatched with what u considered . It should 93316 ₹ (in app)

Kindly revisit the app. N thank u very much for ur efforts🙏

Thanks, Tanjib. Let me relook at this.

is your theory updated with new sebi rule

Please see the last chapter on physical delivery.

Hi,

What happens if I don\’t close my futures position on expiry day and will the MTM be posted at the end of expiry for expiry day close price? please advise.

The position is deemed closed if you hold it to expiry. Yes, P&L will be marked to market.

sir suppose we sell 1lot of banknifty any option then the margin blocked for that position can be used same day after we square off our position or not and can we use the margin that is blocked for next day trade or not

YOu can, but do keep this in perspective – https://zerodha.com/z-connect/zerodha/bulletin-latest-at-zerodha/peak-margin-intraday-leverages-2nd-order-effects-dec-1st-2020

Is there any limit for future short position limit in amount/lot nos for a single demat account in future contracts. Once if one short in future when it needs to be square off. On expiry date or before. If the buyer wants to squre of as the price in increase, can the seller can wait till the expiry to square off/ price fall to buy the future contracts

I\’m assuming you are asking this from a retail investor\’s perspective. Yes, there is practically no limit. You can square off the position anytime you wish, no need to wait to expiry.

Hi Karthik,

From what I understand, longest contract one can purchase is only for 3 months. Also as per margin calculator I don\’t find much difference in pricing between 1 month and 3 months.

1. In that case why can\’t everyone buy 3 months contract to be on safer side and exit position when they book profits instead of 1 month contract?

2. Is buying the contract for 1 month and then for 2 months after 1 month expiry is same as buying for 3 months? Since futures price changes on daily basis so margins will be updated so how does it matter whether 1 month or 3 months?

3. For all stocks, we only have 3 (based on months) categories to buy contracts?

4. What if liquidity is less for stock i.e. there is no counter party to exit the position? Is this practically possible and how will this situation handled?

1) The price difference exists, look at it from a % point of view. Besides, longer-term contracts are not liquid enough

2) Technically they are the same.

3) Yes

4) You cant transact as easily as you could with a 1-month contract, higher the liquidity, easier to transact.

Dear Sir..

Above explanation is very good..

I need to know more about Exposure importance ..is it actually a loss ?

I am new to futures..pls guide..

No, it is just a part of the overall margins blocked.

Awesome job in writing this detailed article Karthik. I watched many videos on this topic over YouTube however all my questions and queries got quenched after reading your full article here.

Thank you so much.

Thanks, Sunil. Happy reading!

What is the meaning of the position here ?

What if the buyer after buying the futures is having the loss and his cash balance is less than SPAN amount and he is not willing to pay the broker the required difference in the cash balance and SPAN margin amount ?

Position refers to the long or short position you\’ve initiated in the market. Well, the buyer cannot refuse that because the position will be cut off by the broker the moment the margins (which is already blocked) dips below the specified level.

Hi sir,

There is no table of contents in pdf format of technical analysis module , fundamental analysis module and Options module.

Yes, we have converted the content directly to PDF.

Hi, I am placing banknifty fut sell using BO option Market order for a quantity of 100 means 4 lots. To change stop loss or target do I need to go to each order of these 4 lots and do manually as the buying price for each lot is different. What is the solution for this problem.

Depends on how the order has been executed. If all trades in 1 trade, then you modify just once, else manually all the legs.

Hi, I am placing banknifty fut sell using BO option Market order for a quantity of 100 means 4 lots. To change stop loss or target do I need to go to each order of these 4 lots and do manually as the buying price for each lot is different. What is the solution for this problem.

How to pledge cash market holding to increase margin ?

Do check this – https://support.zerodha.com/category/console/portfolio/articles/what-is-pledging

If a broker/consultant is given the authority to do trade in derivatives on our behalf with power of attorney given in favour of broker, with cash and securities transferred in our account with broker and now in trades he suffers loss in our a/c and in the a/c of other clients too,can he or the clearing corporation use our money and securities to cover the losses of others also.The power of attorney specifies that our funds and securities can be used as margin for trades done in our a/c only.INcase of need for money to meet the obligations who does the sale of shares .Dont the proceeds come to respective ledgers,I found your post/lecture very enlightening .Thanks

LMGoyal

No, no one can use your money to cover the losses of others. However, few brokers have done such things in the past, hence its best you dont allow anyone to use your account to trade on your behalf.

Hi Karthik, this is amazing content. I\’ve read this a couple of times over the years and keep returning to the Zerodha Varsity. Thank you for taking the time to write this.

One thing that\’s not super clear to me: why is SPAN + Exposure Margin charged in this way (% of contract value) rather than the total possible loss? e.g. today (1 Sep \’20) the zerodha margin calculator suggests that for selling a 13800 Call for Nifty 24 Sep and buying a 14000 call for the same expiry, the SPAN margin is ₹4.1k and the exposure margin is ₹25.8k. My maximum possible loss here is (200 points spread X 75 in a lot = )₹15K. Why is Span lower than this and why is exposure more than this? Ultimately more margin than what is strictly required is being blocked.

I\’ve heard some explanation about the broker won\’t know if you exit the buy position leaving a naked call, but that\’s not true – they\’re able to figure out when you do that and increase your margin requirement (even if just SPAN). So why is it done this way? I\’ve also traded options a little in the US and my brokerage (Schwab) would only block the max loss.

Hello Karthik,

First of all, thank you for such an outstanding resource and that too for free. All cash flows from my account are done only at the end of the day, right? I mean if at some point in time during the day, my cash balance was less than SPAN because the value of the future fell and my balance was insufficient, but at the end of the day, everything was fine and my cash balance was more than SPAN as the future price increases. So I don\’t have to worry because, at the end of the day, my cash balance is more than SPAN and the exchange will credit/debit money only at the end of the day. Am I correct?

Except for margins, everything is on an EOD basis. Margins have to be adequate through the time you have a position in the market.

What if on the very next day of entering into Futures Contract (ie.12 Dec) there is an extreme price movement and future price fall by rs. 130 ie. Future price falls to Rs.810

And available cash balance is not sufficient to meet SPAN as well as Exposure Margin. ie. Entire cash balance is wiped out by M2M loss still there is an shortfall..

Because available cash balance at beginning of the day rs.26659 is less than M2M Loss ie.130*250=32500..

Please reply….

Thanks for giving your precious time…

In such a case, the broker will cut your position immediately.

We come across terms like Collateral margins, cash margins etc when we are dealing with option trading. We have not fund these terms in your tutorials. Please explain what are these and the rules thereof. How are they required to be maintained with the exchange and in what form they are required to be maintained.

Yes, this is a good point, will add this to the module.

Hi Karthik,

Fantasti explanation.Please clarify the following qns :

1)who decides leverage ? It changes with vix but will there be any maximum/minimum cap on this ?

2)Currently NIFTY50 leverage is abt 5.7 times ..What is the maximum leverages we can get on nifty 50 when vix is about 12-13 ?

3)where can we get historical data for nifty leverage

Thanks in advance.

1) Used to be brokers, but not regulators have a say. Yes, ViX also plays a role. Higher the Vix, lower is the leverage

2) 12-13 on ViX is low. But I think going forward, the leverage will be fixed at 5 time at the most

3) This is not standardized, depends on broker to broker.

Sir, I have read most of the chapters you provided in Options. So I have one query regarding MTM in Option Writing. I\’m giving you an example, please clarify my doubts if possible, and if I\’m wrong somewhere please also rectify me. Suppose:

On 17.07.2020 @8.30 AM: I Pay-in Rs. 70000/- to create an IRON Condor of NIFTY.

On 17.07.2020 @9.30 AM: I formed an iron condor with following trades with 1 LOT:

Short NIFTY AUG 11500CE @LTP 66.90

Short NIFTY AUG 9500PE @LTP 70

LONG NIFTY AUG 9000PE @LTP 40

LONG NIFTY AUG 12000CE @LTP 20

For which a margin has been blocked of Rs. 64402/- (SPAN=23521 + EXPOSURE=40881).

It is showing Options Premium: Rs. 5767.5/-

Now I\’m remaining with (70000-64402)= Rs. 5598/- cash balance in my trading A/C.

All the trades taken in NRLM category, i.e for carry-forward purpose

lets not get into any calculations. That I was taught well by you sir.

Now, On 17.07.2020 @3.25 PM: I\’m having P/L= -1061.25/- **from where my series of query starts**

1. What happens to my Trading A/C cash balance If I don\’t want to book my losses?

2. When will the Premium receivable amount i.e 5767.5/- get credited into my a/c? If I get it the next day, then Would I have the trading A/C balance like this: {(70000-64402)+5767.5}=11365.5/-

3. If point No.2 happens then it means that, If I start to make losses, upto Rs. -11365.5/- I won\’t have to Pay-in extra Cash for the MTM losses, Isn\’t it?

1) MTM in options writing is not like Futures. The margin blocked increase for the short position in case the position goes against you. But for this case, the margin increase will be negligible

2) Premium received will get to your account on T+1 basis.

3) Like I mentioned, there is no M2M for options, adjustments are done with margin increase or decrease.

Hello Karthik,

For sure this question is already been answered, but I couldnt find its answer.

If I myself do not square off my futures position (long) till the date of expiry –

– how does it automatically get squared off?