10.1 – The Pricing Formula

If you were to take a conventional course on Futures trading, you would probably be introduced to the futures pricing formula right at the very beginning of the course. However we have deliberately opted to talk about it now, at a much later stage. The reason is simple – if you are trading futures based on technical analysis (I assume a vast majority of you are doing this) then you would not really need to know how the futures are priced, although a good working knowledge would help. However if you aspire to trade futures by employing quantitative strategies such as Calendar Spreads or Index Arbitrage then you certainly need to know this. In fact we will have a module dedicated to ‘Trading Strategies’ where we would discuss some of these strategies, hence the discussion in this chapter will lay down a foundation for the forthcoming modules.

If you recall, in some of the earlier chapters occasionally we discussed the ‘Futures Pricing Formula’ as the prime reason for the difference between the spot price and the futures price. Well, I guess it is time now to lift the veil and introduce the ‘Future Pricing Formula’.

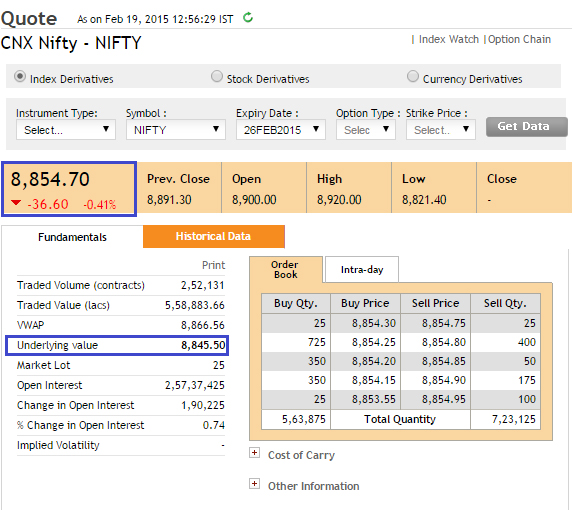

We know the futures instrument derives its value from its respective underlying. We also know that the futures instrument moves in sync with its underlying. If the underlying price falls, so would the futures price and vice versa. However, the underlying price and the futures price differs and they are not really the same. To give you a perspective as I write this, Nifty Spot is at 8,845.5 whereas the corresponding current month contract is trading at 8,854.7, please refer to the snap shot below. This difference in price between the futures price and the spot price is called the “basis or spread”. In case of the Nifty example below, the spread is 9.2 points (8854.7 – 8845.5).

The difference in price is attributable to the ‘Spot – Future Parity’. The spot future parity the difference between the spot and futures price that arises due to variables such as interest rates, dividends, time to expiry etc. In a very loose sense it is simply is a mathematical expression to equate the underlying price and its corresponding futures price. This is also known as the futures pricing formula.

The futures pricing formula simply states –

Futures Price = Spot price *(1+ rf )– d

Where,

rf = Risk-free rate

d – Dividend

Note, ‘rf’ is the risk-free rate that you can earn for the entire year (365 days); considering the expiry is at 1, 2, and 3 months one may want to scale it proportionately for time periods other than the exact 365 days. Therefore a more generic formula would be –

Futures Price = Spot price * [1+ rf*(x/365)]– d

Where,

x = number of days to expiry.

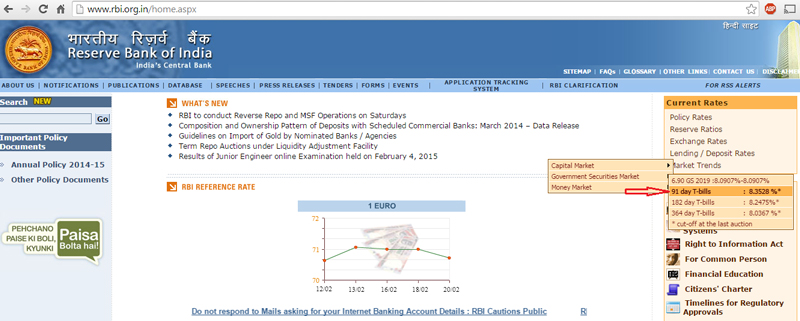

One can take the RBI’s 91 day Treasury bill as a proxy for the short term risk-free rate. You can find the same on the RBI’s home page, as shown in the snapshot below –

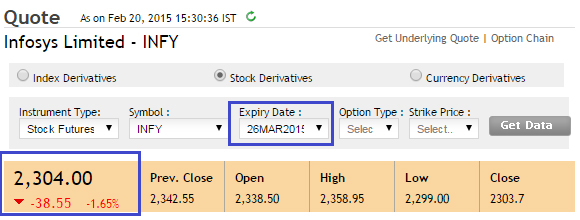

As we can see from the image above, the current rate is 8.3528%. Keeping this in perspective let us work on a pricing example. Assume Infosys spot is trading at 2,280.5 with 7 more days to expiry, what should Infosys’s current month futures contract be priced at?

Futures Price = 2280.5 * [1+8.3528 %( 7/365)] – 0

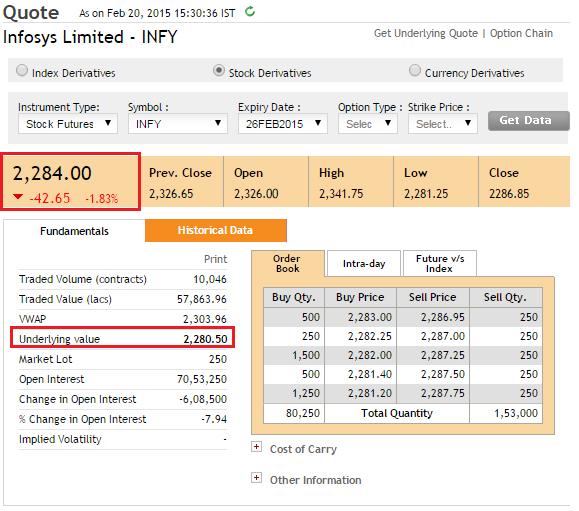

Do note, Infosys is not expected to pay any dividend over the next 7 days, hence I have assumed dividend as 0. Solving the above equation, the future price turns out to be 2283. This is called the ‘Fair value’ of futures. However the actual futures price as you can see from the image below is 2284. The actual price at which the futures contract trades is called the ‘Market Price’.

The difference between the fair value and market price mainly occurs due to market costs such as transaction charges, taxes, margins etc. However by and large the fair value reflects where the futures should be trading at a given risk free rate and number of days to expiry. Let us take this further, and figure out the futures price for mid month and far month contracts.

Mid month calculation

Number of days to expiry = 34 (as the contract expires on 26th March 2015)

Futures Price = 2280.5 * [1+8.3528 %( 34/365)] – 0

= 2299

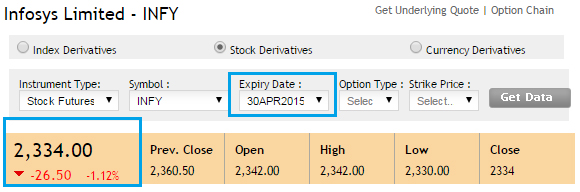

Far month calculation

Number of days to expiry = 80 (as the contract expires on 30th April 2015)

Futures Price = 2280.5 * [1+8.3528 %( 80/365)] – 0

= 2322

From NSE website let us take a look at the actual market prices –

Snapshot of Infosys’s mid month contract

Snapshot of Infosys’s mid month contract

Clearly there is a difference between the calculated fair value and the market price. I would attribute this to the applicable costs. Besides, the market could be factoring in some financial yearend dividends as well. However the key point to note is as the number of days to expiry increases, the difference between the fair value and market value widens.

In fact this leads us to another important commonly used market terminology – the discount and the premium.

If the futures is trading higher than the spot, which mathematically speaking is the natural order of things, then the futures market is said to be at ‘premium’. While ‘Premium’ is a term used in the Equity derivatives markets, the commodity derivatives market prefer to refer to the same phenomenon as ‘Contango’. However, both contango and premium refer to the same fact – The Futures are trading higher than the Spot.

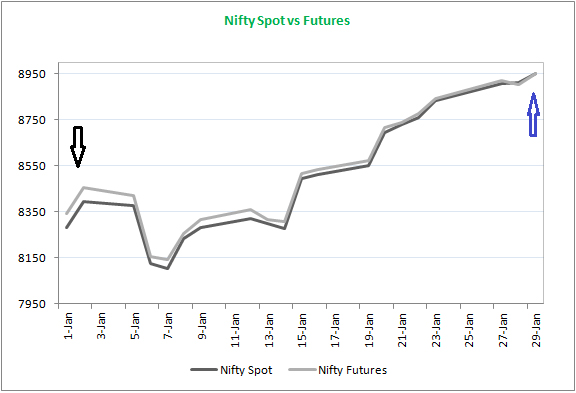

Here is a plot of Nifty spot and its corresponding futures for the January 2015 series. As you can see the Nifty futures is trading above the spot during the entire series.

I specifically want to draw your attention to the following few points –

- At the start of the series (highlighted by a black arrow) the spread between the spot and futures is quite high. This is because the number of days to expiry is high hence the x/365 factor in the futures pricing formula is also high.

- The futures remained at premium to the spot throughout the series

- At the end of the series (highlighted by a blue arrow) the futures and the spot have converged. In fact this always happens. Irrespective of whether the future is at a premium or a discount, on the day of the expiry, the futures and spot will always converge.

- If you have a futures position and if you fail to square off the position by expiry, then the exchange will square off the position automatically and it will be settled at the spot price as both futures and spot converges on the day of the expiry

Not always does the futures trade richer than the spot. There could be instances – mainly owing to short term demand and supply imbalances where the futures would trade cheaper than its corresponding spot. This situation is when the futures is said to be trading at a discount to the spot. In the commodities world, the same situation is referred to as the “backwardation”.

10.2 – Practical Application

Before we conclude this chapter, let us put the futures pricing formula to some practical use. Like I had mentioned earlier, futures pricing formula comes very handy when you aspire to trade employing quantitative trading techniques. Please note, the following discussion is only a preview window into the world of trading strategies. We will discuss all these things plus more in greater detail when we take up the module on “Trading Strategies”. Consider this situation –

Wipro Spot = 653

Rf – 8.35%

x = 30

d = 0

Given this, the futures should be trading at –

Futures Price = 653*(1+8.35 %( 30/365)) – 0

= 658

Accommodate for market charges, the futures should be trading in and around 658. Now what if instead the futures contract is trading at a drastically different price? Let’s say 700? Clearly there is a trade here. The difference between the spot and futures should ideally be just 5 points, but due to market imbalances the difference has shot up to 47 points. This is a spread that we can capture by deploying a trade.

Here is how one can do this – since the future contract is trading above its fair value, we term the futures market price as expensive relative to its fair value. Alternatively we can say, the spot is trading cheaper with respect to the futures.

The thumb rule in any sort of ‘spread trade’ is to buy the cheaper asset and sell the expensive one. Hence going by this, we can sell Wipro Futures on one hand and simultaneously buy Wipro in the spot market. Let us plug in the numbers and see how this goes –

Buy Wipro in Spot @ 653

Sell Wipro in Futures @ 700

Now we know that on the expiry day, both the spot and the futures converge into one single price (refer to the Nifty graph posted above). Let us assume a few random values at which the futures and the spot converge – 675, 645, 715 and identify what happens to the trade –

| Expiry Value | Spot Trade P&L (Long) | Futures Trade P&L (Short) | Net P&L |

|---|---|---|---|

| 675 | 675 – 653 = +22 | 700 – 675 = +25 | +22 + 25 = +47 |

| 645 | 645 – 653 = -08 | 700 – 645 = +55 | -08 + 55 = +47 |

| 715 | 715 – 653 = +62 | 700 – 715 = -15 | +62 – 15 = +47 |

As you can notice, once you have executed the trade at the expected price you have essentially locked in the spread. So irrespective of where the market goes by expiry, the profits are guaranteed! Of course, it goes without saying that it makes sense to square off the positions just before the expiry of the futures contract. This would require you to sell Wipro in spot market and buy back Wipro in Futures market.

This kind of trade between the futures and the spot to extract and profit from the spread is also called the ‘Cash & Carry Arbitrage’.

10.3 – Calendar Spreads

The calendar spread is a simple extension of the cash & carry arbitrage. In a calendar spread, we attempt to extract and profit from the spread created between two futures contracts of the same underlying but with different expiries. Let us continue with the Wipro example and understand this better –

Wipro Spot is trading at = 653

Current month futures fair value (30 days to expiry) = 658

Actual market value of current month futures = 700

Mid month futures fair value (65 days to expiry) = 663

Actual market value of mid month futures = 665

From the above example, clearly the current month futures contract is trading way above its expected theoretical fair value. However the mid month contract is trading close to its actual fair value estimate. With these observations, I will make an assumption that the current month contract’s basis will eventually narrow down and the mid month contract will continue to trade close to its fair value.

Now with respect to the mid month contract, the current month contract appears to be expensive. Hence we sell the expensive contract and buy the relatively cheaper one. Therefore the trade set up would require me to buy the mid month futures contract @ 665 and sell the current month contract @ 700.

What do you think is the spread here? Well, the spread is the difference between the two future contracts i.e 700 – 665 = 35 points.

The trade set up to capture the spread goes like this –

Sell the current month futures @ 700

Buy the mid month futures @ 665

Do note – because you are buying and selling the same underlying futures of different expiries, the margins are greatly reduced as this is a hedged position.

Now after initiating the trade, one has to wait for the current month’s futures to expire. Upon expiry, we know the current month futures and the spot will converge to a single price. Of course on a more practical note, it makes sense to unwind the trade just before the expiry.

Let us arbitrarily take a few scenarios as below and see how the P&L pans out –

| Expiry Value | Current month P&L (Short) | Mid Month P&L (Long) | Net P&L |

|---|---|---|---|

| 660 | 700 – 660 = +40 | 660 – 665 = -5 | +40 – 5 = +35 |

| 690 | 700 – 690 = +10 | 690 – 665 = +25 | +10 + 25 = +35 |

| 725 | 700 – 725 = -25 | 725 – 665 = +60 | -25 + 60 = +35 |

Of course, do recall the critical assumption we have made here is that i.e. the mid month contract will stick close to its fair value. From my trading experience this happens most of the times.

Most importantly please do bear in mind the discussion with respect to spreads in this chapter is just a sneak peek into the world of trading strategies. We will discuss these strategies in a separate module which would give you an in depth analysis on how one can professionally deploy these strategies.

Key takeaways from this chapter

- The futures pricing formula states that the Futures Price = Spot price *(1+Rf (x/365)) – d

- The difference between futures and spot is called the basis or simply the spread

- The futures price as estimated by the pricing formula is called the “Theoretical fair value”

- The price at which the futures trade in the market is called the ‘market value’

- The theoretical fair value of futures and market value by and large should be around the same value. However there could be slight variance mainly due to the associated costs

- If the futures is rich to spot then the futures is said to be at premium else it is said to be at a discount

- In commodity parlance Premium = Contango and Discount = Backwardation

- Cash and carry is a spread where one can buy in the spot and sell in the futures

- Calendar spread is an extension of a cash and carry where one buys a contract and simultaneously sells another contract (with a different expiry) but of the same underlying

Do I really need to remember the formula ??

Not really, its good to know 🙂

wipro spot is 204.10 , wipro jun future is 183.59 . pls tell how to take arbitradge trade in this condition (as far i know we can not sell spot)

Arbitrage = buy cheaper asset and sell expensive one. But unfortunatley you cant sell in spot and hold position.

Hi Karthik, am I right to say that we need to use the spot market technical chart of the underlying asset for trading the same asset\’s in the futures market? as the futures price of the asset follows the spot market price fluctuations.

Thats right. Thats what I\’d suggest. But there is no harm looking at futures price charts as well 🙂

Dear Sir,

According to the module, the futures price is calculated using the following formula:

Futures Price = Spot Price × [1 + rf × (x/365)] − d

I would like to clarify whether actual market forces, such as the interaction of buyers and sellers, or demand and supply, also play a role in determining the futures price in practice, or whether the price is determined strictly by this theoretical formula.

Thank you.

Yes, it does. The futures pricing formula is only a theoretical reference. Market forces plays a big role in the futures price.

Sir,

In the calendar spreads, you have assumed that the current month expiry futures to be expensive and the mid month futures to be cheap. Hence, you have cited to go short for current month and long for mid month.

During the expiry, we know that the spot price and the current month future value will be equal. However, in the material, the expiry price is taken as the final price for the current month futures as well as the mid month futures. However, I believe the mid month futures final price will vary from the same.

Am I missing somewhere or is it approximated in the material?

The current month is usually cheaper compared to mid month, that said, this can reverse too. The current month and spot converge upon expriy only and not in the middle of the series.

1) sir how much difference would be ideal to find between fair future value and market future value(you have taken=42 in wipro example)

2) how much spread would be ideal for calendar spreads (you have taken=35 in wipro example)

Best to define it as a percentage = something like 0.3% to 0.5% or more? But do backtest to figure if that is a reasonable expectation to have.

Good Morning Mr. Rangappa!

I shall not bore you with the specific numbers but here\’s the rounded off version.

SILVERM Spot – Rs. 1.62L

SILVERM 28NOV2025 FUT – Rs. 1.48L

SILVERM Fair Price – Rs Rs. 1.64L (Using the 91-day T-Bill rf to be 5.4251% from RBI)

So Mr. Rangappa, the futures are available at a discount, so can we consider this commodity future to converge with its spot price as we approach expiry? (Backwardation)

Would this constitute a good trade with a reasonable expectation?

Also to execute a Cash and Carry Arbitrage here, one would have to \’buy the cheaper asset and sell the expensive one\’

So that means we go long on FUT and short spot silver?

and here while we operate on a margin and leverage for FUT, would we need the full amount to short spot?

And what instrument on Zerodha do we use to carry shorting of spot say SILVERBEES?

and does one\’s approach change if we already own the spot we intend to short? say I already own some amount of silverbees

Shorting spot silver is not possible, Pavan.

Yes, but the spot data is not officially published right? So its hard to stitch a trade here plus in spot silver, you also have to consider taxation into perspective.

I have recently observed that since many weeks there are multiple stocks for which next month future is trading significantly below their current month future even though there is no upcoming dividend. For Eg: Britannia, Coal India, REC, and many others.

What\’s the likely reason

This is most likely linked to the demand – supply situation. Cant think of any other reason 🙂

but these type of opportunities are usually taken away by the arbitragers very quickly but its been days since I am observing this

Yes. Any arbitrage opportunities that relies on speed and latency will be taken away by institutional players.

so isn\’t this an opportunity like that ?

Hmm, not sure. I\’ve not really tracked this closely 🙂

Sir i not able to solve equation (1+8.3528%(80/365) )

Please help ?

Please use excel, you can figure this out 🙂

I solve that on calculater i understand how to calculat 👍

But my 1 question is that how to do reverse cash and carry arbitrage if spot is expensive than future?

To reverse, you just square off right?

But in spot the short position is only for intraday?

Short EQ is only intrday, if you want to carry forward the short, you will have to use derivative contracts.

Hi! considering a imaginary situation :

spot price does not change for say a month , so futures price consistently declines to merge with spot during expiry day. isn\’t this counts as price decay.

No, that would just be following the Spot-fut pricing framework 🙂

How does this work when Fut is at discount.

E.g

AngleOne Spot 2312

Current Month Fut 2274 (1.64% in discount)

Middle month Fut 2181 (5.64% in discunt)

Buy Middle Month at 2181

Sell current month at 2274

Would it be a good trade?

Yes, but please ensure there is no expectation of any corporate action.

Thanks for the reply. I will check.

Hi Karthik,

Cud you please elaborate on corporate action? And what cud be possible scenerio?

Regards,

Manish

Which corporate action? There are many, and we have tried to explain all of that in the chapters 🙂

Hi,

In case of Future contract in premium, we sell the future and buy the spot.

But how do we buy SPOT in the market. Please could you help on this.

Spot refers to the regular cash market, that you can easily buy.

I am referring to Nifty 50, how can you buy Nifty 50 Spot in the market. Is there any alternative to it which comes close to buying spot Nifty 50

You can via Nifty bees 🙂

Sir, what is the winning rate in % of this strategy..

That depends on multiple factors, including risk appetite, risk capital, etc. There is no standard answer to it unfortunately 🙂

I will make an assumption that the current month contract’s basis will eventually narrow down and the mid month contract will continue to trade close to its fair value. Is the following assumption specific to a particular stock or applicable to the entire market?

This is with respect to all contracts while trading spreads.

Hi Kartik,

When trading futures should I buy based on the Futures chart or spot chart? I ask this because many times price in future is trading above break point and spot price has still not crossed it.

Regards

I\’d say trade based on spot chart.

In the above example of Wipro, if we take the future contract then the Net gain or loss is affected in margin only.

Assuming I buy spot and sell future near month, should I buy the the number of shares in spot equalling the margin amount level?

Sorry, dont have the full context. But there is no margin benefit as such, if that is what you are looking for.

What if futures are trading in discount. What can we do in that case Ex = adani green spot trading at 1035.05

Future at

1028.95

Fair price for future is

1041.61

The futures will get adjusted. Check this – https://youtu.be/MX-6rdHDPbE?si=oYapxvhfNYw1cYVJ

`Dec is actually at fair value, so I’d not take this trade up`

So Does it means we should only take/initiate trade when current month Fut is at premium or at Discount value?

As currently Dec Month Fut is at Fair Value and Next Month (Jan) Fut is at Discounted value.

That\’s right, we take up trades only when the price of asset deviates away from the fair value.

Thank you so much Karthik, Zerodha Varsity content is Awesome !!!

Quote: `always sell the higher priced once and buy the lower priced one.`

Query:

In Today\’s closing Price for UBL (20 Dec 2024): UBL Dec Month Fut Value & Fair Value is 2027.

Dec Month: (Fut – Fair) Value = (2027-2027) = 0

For Jan 2025 Fut UBL Contract: Fut Value: 2007, Fair Value: 2039

Jan Month: (Fut – Fair) Value = (2007 – 2039) = -32

So Trade should be: Sell Dec Month Fut and Buy Jan Month Future is it correct?

If you calculations are right, then Dec is actually at fair value, so I\’d not take this trade up 🙂

Hi …. just like in this example if the case is vice versa for eg: current month future trading near spot and the mid month future is trading at the higher price than the fair value it means we buy the current month and short the mid month contract

Yes, the easier way to remember, always sell the higher priced once and buy the lower priced one.

Thanks for this lesson. How often do you come across Cash & Carry Arbitrage or Calendar Spread opportunities?

They continue to exist, but it is getting increasingly difficult to grab these opportunities by a retailer, thanks to the algos at play 🙂

rather than 2 atm put buy , go for one ITM put buy (eventually you are shorting the future) along with longing futute at discount . Loss shall be limited may be zero and profit -> linear like future .

1 ATM put = delta of 0.5. 2 = 0.5+0.5 = 1 = futures delta.

Can we say that cash n carry strategy needs more capital to trade than calender spread as we have to buy spot which need huge amount?

Secondly,spread is more in cash n carry so profit is comparatively more than calender spread strategy.

Thank you.

Yes, of course. With calendar spreads, you have reduced risk, hence reduced margins. About reward, yes, you can say that.

Hi sir , I have one doubt pls revert me

You have told that one can take RBI’s tbills as risk free rate

Can we take this at any time or we need to look another best risk free rate as per current situation

You can take this at any point, Kamesh.

Hi Sir,

Thanks for making such wonderful materials.

My question is in future pricing formula we add Risk free rate in order to determine. Why so? Is the future contract price do not involve any risk? so we add back that

Risk free rate is to account for the opportunity cost, Ankit, and yes, futures involves risk, its not risk free 🙂

hai Karthik,

can i do calendar future spread on every month. if yes.. what is the best time to deploy this strategy.

if not on every month, how can i find chances to delpoy and at what time.

You can, and the best time to deploy is when the spreads are wide enough. Unfortunately you cant fix a particular date for this.

Hi Karthik,

How does price of NIFTY FUTURES get\’s affect if say huge number of market participant go long in NIFTY FUTURE, will the NIFTY FUTURE\’S price get increased?

at time, I see nifty moves, 30-40 points but nifty future moves more than the underlying (say 45-55pts), what causes this?

Kindly direct me towards resource from where i can learn more about NIFTY SPOT AND FUTURE\’S relation.

Thankyou

– Mohit

Yes, if there are many people buying/going long then the prices tend to go up 🙂

But for every long in futures, isn\’t there equal no of shorts people took? So in case of futures, how can we say more people were participated in long, hence the future prices increased?

Hence the need to correlate it with the price movement.

Hi Karthik

On an intraday basis some times Future closes by some 10 to 30 points higher and some other days the opposite, Why does this happen, Is there a way to find on which days the future would trade higher/lower than spot

Its hard to predict, but it happens due to the simple demand and supply situation.

Okay Thanks karthik,

On Expiry day If future price is trading at discount than spot, what will happen here, Will spot reduce to future price or future rise to spot price?

Either could happen, but they do converge to a single price on the expiry day.

Hi Karthik, Today I observed that Nifty Futures were trading higher than spot Nifty. Also I was looking for trades in Apr 3rd 23000 CE. The price action of this contract was following the Nifty futures and not spot nifty . Please have a look at the chart of Nifty Apr Fut and Nifty 50 along with APR03 23000CE for the last 30 mins of March 27th i.e expiry day. I am very confused . What needs to be followed in that case ? And why did 23000CE contract value increase so much despite the nifty50 was almost flat?

You can track futures, but the futures tracks spot 🙂

Okay. Thanks but still my query is not addressed. If I have to address you in tradingqna.com what is your user id? I was not able to mention or find you there. Thanks!

Sorry, can you please state your query again?

I meant to ask: Whenever I have doubts, How can I address you on the tradingqna.com platform? I was not able to find your name or id in particular.

I\’m more active here 🙂

Futures Price=Spot price×[1+rf×(365x)]−d

Karthik, In the above formula, X denotes calendar days or trading days? Sensibull said its calendar days and all days including weekends and holidays included?, People I\’ve known said its trading days. Which one is correct?

YOu can include them, its ok. Another thing that you can do is to calculate with and without the holidays and see which price is closest to the market and use that format 🙂

In calculating future price, say am calculating the price for next week expiry, If there are 2 holidays in between expiry Do I have to exclude the holidays? also what about weekends? include or exclude?

Thanks

You can include the days, thats ok.

Hi Karthick,

Is there in any module for different of arbitrage technique, if not can you brief about in any module

You can check this – https://zerodha.com/varsity/module/trading-systems/

Mid month futures\’ price will be different(not equal to the spot) when near term contract expires. Why did you subtract the spot price from 665??

I\’d suggest you check this – https://zerodha.com/varsity/chapter/calendar-spreads/

Sir, owing to demand and supply, future at premium indicates to huge demand to buying side. am I right ?

Yes, thats correct.

What is the calculation of loss. In what scenario we face loss in it.

Take the difference between the buy and sell price of futures and multiply with the lot size. You will get the P&L.

sir ,

it means , in calendar spread , one should make position at the start of the month and hold on to the expiry . and make good profit, as at the start , the difference between the two spread in colander spread is enough good .

Yeah, generally speaking, the higher the time to expiry, the larger the spread. But there are times when this can also expand basis volatility in the market.

Nicely explained.

`Futures Price = Spot price * [1+ rf*(x/365)]– d` Here you used multiplication with rf*(x/365) but in examples it\’s show %. Which one is correct?

If you use –

rf*(x/365) = daily interest

Percentage = annual

So based on what you are trying to do, use can use the appropriate formula. But both work.

Hi kartik,

I have this question, how does SGX nifty predict exactly where Nifty will open the next day? Doesn\’t the future\’s value be derived from the underlying and not the other way round?

Thanks,

Kunal

Its not exact right? The directional movement is known, values will differ.

1. If the contract is valid for 90 days then why we are taking 365 in the formula?

2. In the future we can minus dividends from underlying assets (As per the formula), What are we doing with options to remove price variation of dividends?

1) To get the annualized number right

2) The options formula too has a method to factor in the dividends.

Sir, First of all, Hats off to you!!! It\’s really wonderful for the novice like us who know nothing about markets in general. You are doing a great job!

My question is I cannot see futures market data live or historical in sensibull. Where and how can I find it? Second query is if futures and options both are derivatives, then which one should I choose and why? At least, which one is easier to learn and get profit?

Thanks, Prakash.

YOu can try downloading from NSE, they used to provide historical data, maybe they still do. Can you check once? I cant tell you which one is easier to make a profit, but I can tell you that futures is easier to understand 🙂

In terms of commodies i.e. for example am looking to buy a 1 kg lot of gold – FUT 5 Dec 23 – what would be the gold price i will book this lot at ? is it going to be the same as gold spot price currently in MCX or will be gold Spot price + X amount ? and where we could find this in zerodha ? Thank you

This will be gold futures price as on MCX.

If the prices of the stock or Nifty remain same for the entire month (theoretically) what would be the price of the future lot? For example, let\’s say on the 1st day of the month…. Nifty is at 20000 and Nifty future for the current month is at 20100. I buy the future at 20100 today. Now for the entire month, the nifty remains same at 20000, what will be the future price at the expiry? And how will it reflect in the P&L?

So difference between the spot and futures will be noticed by market participants and they would try to arbitrage it away, hence the price would converge 🙂

Sir, if that\’s the case, if buying spot and selling futures then, won\’t theta decay affect spot option bought.

Theta decay is only for options, not for futures Sam.

Thank you so much sir

Happy learning 🙂

Also where can I get 3 months futures as automatic Excel . Please share link sir. 🙏

Not sure about this, please check with a NSE authorised data vendor for this.

Hi Karthik sir, thanks for knowledge you are providing.

I have 2 doubts. Please answer sir. Thanks in advance

1. What is present dividend factor for nifty in fair price calculation.where can I see. Please share link if possible sir.

2.can you please share risk free interest rate link of RBI ( i know it\’s not accurate but proxy)

1) This will be unpdated on NSE\’s website. I know it used to be somewhere here – https://www.nseindia.com/market-data/live-equity-market?symbol=NIFTY%2050, but unable to get find now. Maybe you can do some digging around 🙂

2) Check on the left-hand side – https://rbi.org.in/ under policy rates.

I got your point that market price can be different than theoretical price.

But is there any chance that market price can go below theoretical price.

if yes, then can you please tell any instance when future jas gone below spot price in nifty.

I am not able to get any such instance from last 3 years.

Yes, this keeps happening. Nifty is either at a discount or premium to spot. I think around Covid time, Nifty was at a discount to spot. Can you check March 2020 once?

HEY, I JUST USED YOUR FORMULA TO CALCULATE NIFTY FUTURE PRICE (TODAYS DATE IS 10th july 2023).

I have some confusions in the formula.

Here are the calculation i just undertook (10th july 2023) –

nifty price 19355.90

Risk free rate (as per rbi website) – 6.72

number of days to expiry – 13 (trading days left to expiry) / 17 (total days left to expiry)

Futures Price = 19355.90 * [1+6.72/100( 13/365)]

= 19402.22689

Futures Price = 19355.90 * [1+6.72/100( 17/365)]

= 19416.48132

Now, the problem is that the actual future price for 27th july expiry NIFTY is 19524.00.

Can you explain this???

The price you\’ve calculated is the theoretical price. The price that you see is the market price. Both can be different. The market price is determined based on the actual demand and supply. At any given point, there will be price difference between the two 🙂

Sir, why do we see high change in profit/loss in futures as compared to equity shares for same amount of fluctuations in the chart.

Hello Karthik sir,

I have been facing an issue regarding the constantly changing “Premium/discount of stock futures prices compared to spot.”

Say, I short a stock future when it is trading at a discount of Rs. 10 compared to spot. After a while, the discount reduced to Rs. 5 compared to spot.

(I refer spot charts to trade in futures)

If the lot size is 1000, this extra Rs. 5000 loss causes unnecessary dent on the portfolio. (due to reduction in discount to spot)

Simply put,

When short, spot prices fall but futures do not &

When long, the spot rises but futures do not.

Such fluctuations skew the returns.

Have any thoughts on how to tackle this?

Many thanks!!!

Shubham, basing your trades only on premium and discount is not a great idea. There should be other factors that should drive your trade and not just the premium and discount. One good way to start is by reviewing the checklist we discussed in the TA module.

Mr. Karthik,

My question is in Far month futures. I found the decay in Nifty futures price is less but where as the decay in Bank nifty futures price is higher. Please guide me what formula defines for Index futures pricing changes.

Decay is also a function of individual script volatility. Not all instruments have the same decay.

Sir,

I have the following queries here:

(i) Do we always make profit for the \”Cash and Carry arbitrage\” trade?

(ii) Is the amount of profit equals the difference of spot price and future price?

(iii) Suppose initially the future price is greater than spot price. Is there any probability that before expiry the future price drops below spot price?

(iv) To make the sure shot profit in the \”Cash and carry arbitrage\”, does one need to simultaneously square off both the positions od spot and future?

(iv) Is it make sense/much better to go for the \”Cash and carry Arbitrage\” when the fair price (calculated through formula) is much lower than the market price?

(v) In case of backwardation, is it possible to buy future and sell the spot (since shot selling should not be allowed in CNC, as we studied)? Please help understand here.

(v) Will it be good choice for trading with futures of two different months even if the mid month\’s market price is not close to fair price?

(vi) Won\’t it be better choice to trade between two different futures rather than spot & future since the former one requires much lesser margin? Please suggest.

(vii) Is this sure shot profit applicable even if one initiates opposite trades between mid & far month future/ current & far month future?

Request your much valuable help on the above please.

1) Nope, no guarantees in market

2) Yes

3) No

4) Yes

5) Yes, or higher. Either situation works. But futures higher works as you can short futures and buy spot

6) Tough

7) Yes, please see my other chapter on the calendar spread

8) Yes, please see above

9) No guarantee 🙂

Is number of contracts in future trading affects respective stock price ?

For example: Infosys (Share price 1427, MAY future 1437 ), If big institutions make short positions in INFY MAY FUT, will it directly affect the share price ? Will INFY share price fall because of large number of short positions in INFY future contracts ?

Sometimes it does have an impact. But generally speaking, the higher the liquidity, the lower the chances of such price interdependence.

Thanks for your reply. I went through the other method on the link you provided. I think that whole module on Trading Systems is useful.

I am commenting here just to maintain the thread.

1. My initial thought was that calendar spread is longer term, like you take in the beginning of the month and exit at expiry. But in the new method, you exit almost always the next day. I think the P&L is very small.

2. My other observation is that calculation based on theoretical fair value formula does not give correct results.

3. Lastly, I would like to say that I \”discovered\” this strategy when I was playing with different combinations in Sensibull. Then I came across your this article on future pricing where I found some justification of what I saw in Sensibull: It showed constant profit for the entire range of the underlying (Banknifty/Nifty in my case). The profit changes at different times in the day, but it increases in fixed steps as the expiry nears. So the way I enter is by first looking at Sensibull and then take trade. I keep the positions till expiry and exit just before expiry. Max profit if I sell current month and buy far month (not near month). I have seen profit in the range of 4-11% for the last 2 months. Is what I am observing and doing, the correct way of doing it?

1) Yes, the idea is to run it like an algo and set up high-frequency trades 🙂

2) So, you just take the spread here, with the assumption that the futures price has baked in all the theoretical calculations

3) Thats roughly how this works. Yeah, you are in the right direction.

In the calculation of the Calendar Spread P&L, I do not understand the calculation for the mid month P&L. You have correctly calculated the \”Current Month P&L (short)\” (second column in the table) as expiry price of the current month future is same as spot price.

But for the Mid or Far month P&L, the price of the future on the expiry day of current month future is not the same as the underlying price as expiry is still one or two months away. Thus, for the third column, \”Mid Month P&L (Long)\” calculation should use the price of the Mid Month future on the day of expiry current month future. I think, here the fair price formula of the future price computation should be used.

Another point is that the future computation formula assumes simple interest. It should instead use compounding interest formula: Spot price * [(1+ rf/365)^x]– d, where ^x denotes \”to the power x\”. Only with this exponential relation, the current month future premium will reduce faster near the expiry.

Yeah, the mid month is based on the assumption that its trading at these levels when the current month expires. But I get your point that the mid-month will not expire and converge. Do check out the other method of calender spread here – https://zerodha.com/varsity/chapter/calendar-spreads/

Hi Karthik, is there a way to buy nifty futures at nifty spot price. Let’s say nifty spot trading at 18000 and nifty futures at premium of 18060. Now I would like to buy nifty futures at spot price 18000 instead of 18060.

Not exactly at the same price, but sometimes, Nifty futures can go below the spot and trade at a discount to spot price.

What is unwinding at expiry means, pls elaborate

Its referred to the closing of the position on the expiry day.

Most importantly please do bear in mind the discussion with respect to spreads in this chapter is just a sneak peek into the world of trading strategies. We will discuss these strategies in a separate module which would give you an in depth analysis on how one can professionally deploy these strategies.

Which module you are referring to?

Check the module on trading stratergies.

Hi Karthik, one more question about an example of Wipro under section 10.2 – Practical Application. Looking at the P&L table and the last line in second last paragraph which says that \”This would require you to sell Wipro in spot market and buy back Wipro in Futures market.\” not sure if this will be other way around i.e. \”This would require you to sell Wipro in FUTURES market and buy back Wipro in SPOT market.\” This is how I interpret it as a beginner :). Thanks

There is another way too, but its just that its not easily doable 🙂

Hi Karthik, I have a question on the relationship between \”Risk-free rate\” and the \”RBI’s 91-day Treasury bill%\”. Is \”RBI’s 91-day Treasury bill%\” the only value to be taken to calculate the fair value of the futures or there are other sources also than \”RBI’s 91-day Treasury bill %\”? Thanks

Its just the RBI ref rate.

I had the understanding that interest on the leverage is priced into the futures price. Shouldn\’t that be a part of the formula?

Brokers dont charge you for the leverage, Rakshay.

Do they calculate future prices based on the T bill interest rate every time, or do they even take interest in any other bonds,debt funds

?

Usually it\’s the 91 day bill.

I bought 1 lot of december future of banknifty and sold 1 lot of bankifty of january month having 220 rs spread ,it will converge or there may be a chance it will increase.

They wont converge as they are of two different expiries.

Thanks a lot for your response. Let me figure out what to do.

Sure, happy learning.

Karthikji,

I will clarify using the following example.

1) Nov 22, 2022: Buy 1 lot Silvermic Feb23 Fut @ 100 and Sell Silvermic Apr23 Fut @110

2) Nov 23, 2022: Sell the Feb23 Silvermic @ 105 and retain Apr23 Silvermic as it is trading at 115

3) Nov 24, 2022: Buy Feb23 Silvermic @ 98 and Buy Apr23 Silvermic @ 105

4) Nov 25, 2022: Retain Feb23 Silvermic as it is trading at 97 and Sell Apr23 Silvermic @ 103

And so on.

Is there something fundamentally wrong with this strategy?

Thanks for your valuable insights and help.

At the end of the day, you need to figure if the position is profitable either –

1) Individually or

2) As a strategy as a whole

In your case, there are multiple positions and the success of it depends on the strategy as a whole. One issue I see here is that the costs will start eating into your profits soon.

Is it okay to enter a calendar spread in futures and keep exiting the profitable leg daily and entering a similar position the next day, retaining the loss-making leg so that it turns profitable enough to exit at a future date? The process keeps repeating.

If no, what exactly is the problem with this strategy? Thanks in anticipation.

Yes, but this is based on the assumption that the loss will turn to a profit 🙂

Thank you so much karthik sir resolving my queries. Thanks a lot.

Happy learning 🙂

Sorry both Nov & Dec contracts exit on November expiry 3 pm. No need extra margin required?

Yes, as long as you unwind both, its not needed.

OK but unwind both contracts on November expiry no need extra margin?

Thats right, Mahesh.

Execute calendar spread in futures

Buy SHREECEM Dec future and

Sell SHREECEM Nov future.

Both contracts margin locked only 25000.

On expiry day any extra margin required or not.

YOu will need full margins for the Dec contract as the hedge (Dec Contract) will expire.

The difference b/w spot future price is not in mind but mid month future is discount as current month future… In this case,

Buy mid month future and

Sell current month future

Is always profitable on expiry day or not?

Not always, based on the execution price 🙂

Sir in calendar spread buying cheaper future and selling higher future. End of expiry day liquidity issue is there. What we will do that time?

Stick to the top 10 stocks and Nifty/Bank Nifty indices Mahesh.

Thank you Karthik for replying. Also is it ok to make out a conclusion from this video, that even if the market sentiment is extremely bearish for upcoming months, just like the 2008 scenario, even then the far month future would always be in premium from the spot ?

By the way, the discount and premium will also depend on the market\’s demand and supply dynamics.

Hi Karthik, around 5th sep, i saw that the far month nifty fut, that is the November future was around 140 points premium from the spot. Then for next 10-15 days it changed only about 2-3 points, but within last 3-4 days, it reduced by 40 points instantly. My question is, that just like an option premium decays with the passage of time, do a mid & far month future\’s premium also decay with time ?

2) Also, no matter how bearish the market is, i have noticed that the far month future is always in premium, why so ?

1) Yes, time decay affects all options contract

2) Do check this video – https://www.youtube.com/watch?v=FqRB7NGnOtA

Thank you!

Welcome!

So if Future and spot converge (settle down at single price by expiry) then when I get opportunity where there is big difference between future and spot, I can short future and buy spot. Ultimately I will be in profit by expiry

Is it true or is there any catch here?

Thats the idea, you can explore in this direction.

Hi Kartik,

Can the trading activity in nifty future somehow impact value of nifty?

To make it more generic, can the heavy trading in futures affect underlying somehow?

It can, sometimes.

Also, As yo said, future and spot prices converge on expiry, do they become equal necessarily? or pretty close to each other?

The settlement price is the basis that both converge to a single price point.

\”Not always does the futures trade richer than the spot. There could be instances – mainly owing to short term demand and supply imbalances where the futures would trade cheaper than its corresponding spot. This situation is when the futures is said to be trading at a discount to the spot.\”

Here when future is trading at discount to the spot, which is attributable to imbalance of supply and demand, what we can conclude? is it due to supply is more than demand?

If it is so then can we have bearish look on spot for short term?

Yes, it just means more activity in spot.

the support team of zerodha or anywhere else

Support team.

you told me in the above comments that if I need to short the spot I can use the securities lending and borrowing mechanism to do it.

so I just wanted to what is this securities lending and borrowing mechanism and if want to get started with it how can I do that, please guide me on this a bit

Ah, we dont have any connect on this. But please do call out support and ask to talk to the person dealing with SLB, you will get all the info you want.

where can I do that can you please guide me a little bit

Sorry, I lost context. Do what?

as you said above that even if there is way to short the spot, the opportunity gets picked up by the algos then can they have an opportunity where the algos can short the spot on a CNC basis

You can use the securities lending and borrowing mechanism to short spot.

1- is there a strategy to trade backwardation

2- and what can be derived if the current month, mid month and far month contracts are all below the spot price and also there is no dividend declaration

1) The obvious ones long/short fut and short/long spot will not work, even if you figure a way to short spot. Simply because the opportunities get picked up by algos

2) Demand supply dynamics are play. You can deploy calendar spreads – https://zerodha.com/varsity/chapter/calendar-spreads/

Hi please explain like the price of the future is lower than the price of the spot. The reason for the same and also who plays catch up in this case. eg today in the case of Dr. Lal path labs future is trading at 2395.25 and the stock is trading at 2636.70. The reason for such price variation and which side does play catch up

This happens mainly due to the supply and demand mismatch.

Sir just one doubt :

Sir in the calendar spread example we will sell the mid term contract also right , though it is not expiring.?

Yes. That is correct.

it is not hegded. In Basket I tried to Buy a asset at spot which is lower than its spot price but its showing total value rewquired

hello sir

spot rate =650

current month contract=700

midmonth contract=652

1)if i buy mid month contract at 652 and short current montjh contract at 700 ,if spot rate comedown to 25 pts before expiry so here my loss is zero.

2)Is the decline of 25 pts will reflect in spot rate,current month contract rate and mid month contract rate?

3)and anyway current contract has to converge to spotrate on expiry day my profit is 50 pts.

is my analysis corrrect sir.

1) This is based on the assumption that both contracts expiry on the same date, but that\’s not true

2) Not necessary

3) Yes, but that happens only on the expiry date.

Hello Karthik, a big fan of yours!

Is closing price of current month contract = opening price of mid month contract?

I think its not. Because of higher spread between spot and futures price at the beginning of the month.

Then is calender spread strategy always profitable?

Nope, that\’s not true as technically they are two different contracts 🙂

Hi

while calculating Banknifty fair value got confused…Please help

Taken (05/19/2022) close price (spot)= 33315

Rbi 91 days T-Bill was 4.91%

formula of may 26th expiry including saturday and sunday (total 7 days)…..33315*(1+4.91% (7/365))-0= 33346

formula for June 20th expiry (total 35 days)……33315* (1+4.91% (35/365))-0= 33471

if executed calendar spreads in those instruments settled daily M2M (profit & Loss)…..(Above example)

Both may(33290-future price) and june (33399-future price) futures are not trading near fair value which one to buy and sell in above example

Here is a better way to do this – https://zerodha.com/varsity/chapter/calendar-spreads/

Sir, I have one doubt sir. Kindly reply. If a future price is 2% discount to the spot price before the dividend and results announcement.. What it indicates? In such scenario one should avoid take Long positions on spot

Or Is it sure that spot will fall even on strong result and divnd meet? Or Such discount to spot is nothing to do with actual mkt reaction as per Results?. Pls reply sir.

That won\’t really have an impact on future prices as the price will be adjusted and the futures will reflect the adjusted price.

Sir Hdfc amc\’s june future is trading way below it\’s spot. Almost 40 points. Is this because the company has declared a dividend of Rs. 42/- in its results and a correction to that level is imminent?

Yes, it\’s an adjustment to the dividend.

Dear Sir,

Escort share was trading at 1754 rs on28 March 2022 at 1415 hrs..

Stcok suddenly observed 70 Rs up rally in 45 Min….and reached 1830 with final closing at 1798.

When i observed , escort April 2022 future price… i founf that it was trading at 1518 rs….i expected it to move up by atleast 50 rs during strong up rally of 75 rs…

My questions are

1) Why so much difference in future price and spot price.

2) Why future price is negative compared to spot price?

Srikanth, the difference can arise out of the demand-supply mismatch. In this case, the stock is also undergoing a corporate action.

Hello Karthik sir,

Sir in previous chapters we discussed that volatility also impacts the pricing of futures. Can you please put some light on that.

Not pricing per say, but the margins will be affected by volatility.

Thanks Karthik

Hi Karthik

I have a question on the calendar spread calculation example. Please refer to the table in your notes The third column is “Mid Month P&L(Long)”. You have calculated it at the same as the expiry value as that of the current month future. On this day, the mid month future need not sell at the expiry value of the current month future. It should be higher right? Let me reproduce the second row form the table

Expiry Value = 690

Current month P&L (Short)= 700 – 690 = +10

Mid Month P&L (Long) = 690 – 665 = +25 – Will this be sold at 690? It should be higher since it has one more month to expire right?

Please explain me if I am missing something. Thanks

Kalyan, I understand what you are saying. Yes, it\’s an assumption, and may not always be right. I\’d suggest you check this method instead – https://zerodha.com/varsity/chapter/calendar-spreads/

as in the example of wipro, why we are buying wipro in spot instead from futures.

if we are buying then what is the quantity of the wipro is preferred in spot market

Yash, that depends on so many things right. Leverage, capital availability etc.

hy sir

in what conditions, the nifty spot and future price at discount will converge.

the futures will only be at discount when the expiry is crossed.

They will converge upon expiry, Yash and that\’s the only known thing. When and how is tough to say.

Hi kartik

I want to ask you if i sell on 700 and buy on 660 a so expiry i will get perimum

Hello Sir. I have a very basic doubt. Market moves based on Demand and Supply. In the spot market, when then there is more demand, the price goes up. Increase in demand for Reliance, the stock price went from 1000 to 1150. But Derivatives is another market where Buyers and Sellers meet to trade on Contracts right. What if the demand is abnormally huge for Reliance Stock Futures in Derivatives Market. Can this make reliance future price go up from 1000 to 1300. Obviously that\’s not happening as I observe. Why do Equity Markets and Derivative Markets follow the same direction with minor price difference even when both markets have different set of participants. They Demand and Supply can vary in both the markets right? Sorry if I am wrong in my interpretation. Please do reply. Thanks in Advance.

This is because both these markets are interconnected, Anand. The price of Futures is based on the price of the spot. Traders base their decision in derivatives based on the movement in the spot.

Hi,

F & O will be shown as business income, how to valuate its closing stock

You can take the closing price on the day you wish to calculate the business income.

Why do professional always track future chart rather than spot chart

Both the charts are tracked, its just that with Futures, you get volumes (number of lots traded).

Why did Kartik u said it makes sense to square the position in futures just one day before the expiry

Because upon expiry, the futures is physically settled. Just to avoid the physical settlement headache.

is the calculation correct over here?

Futures Price = 2280.5 * [1+8.3528 % ( 7/365) ] – 0

i am getting 2304 here.

but the article says 2283.

please correct me if i am wrong somewhere.

Try this – 2280.5 * [1+8.3528 % * ( 7/365) ]

Do you have any videos doing futures live trading? If yes please do share it

Not yet, but noted!

Hi Karthik,

It\’s always a pleasure to read your articles, thank you for all your efforts.

Query regarding \”Cash & Carry Arbitrage\”, If you can help me to understand, in a situation where we have to Sell in Spot and Buy in Futures for a particular stock, how to we are going short the shares in Spot and carry it till the end of expiry.

Please let em know if I am missing something.

Amey, that\’s not possible to short the spot and carry it forward. You will have to do something like an SLB – https://www1.nseindia.com/live_market/dynaContent/live_analysis/slbs_chain/chainDataBySeries.jsp , get a little complex.

Got it Karthik. Thanks again for clearing doubts.

Good luck!

1) My point is even if a futures is trading near its fair value, and if we take opposite positions in spot and futures market, then also theoretically speaking price difference btw fut & spot (at the time of taking position) is guaranteed as profit. Isn\’t it?

2) How to deal the scenario when future is trading below spot price?

1) No, what you make will get adjusted towards applicable charges

2) The only way is to set up a synthetic i.e. buy futures + buy put + sell call. Gets a little cumbersome.

Hi Karthik,

First of all many thanks for creating such a wonderful and comprehensive educational stuff.

I have following questions regarding \”Cash & Carry Arbitrage\”

1) Irrespective of whether futures of any stock is priced at premium or is near its fair value, till the time there is difference btw spot & future price, can\’t it be traded? This spread (Future – Spot) will anyways be locked as profit.

2) In your Cash & Carry example, you have considered futures price to be higher than spot price. That\’s why short position is taken in futures and long in spot. However, if it\’s other way around then how to proceed? After all, in spot market short position is not possible beyond intra-day.

3) There must be different ideal spread value (future minus spot price) range for stocks in different price range (like – stocks in 3-fig, 4-fig, 5-fig price etc). Basically, how to determine whether current futures is trading near its fair value or is it drastically different? For eg.:

spot price of stock A is Rs 500,

current month future price = Rs 502 (calculated using formula)

Actual current month future price is Rs 505.

So, should it be considered at premium or around its fair value?

Thanks

Sumit

1) Yes, but for this, you need to ensure that the futures is trading far away from its fair value. Plus you need to ensure to carry out both the transactions happen i.e. sell/buy futures and buy/sell the spot

2) Yes, shorting spot is not possible

3) YOu need to apply fair value formula, get a sense of what is the right futures price, factor for some errors and then figure the price. Overtime, you will develop a sense for this.

Hello Karthik Sir,

As answer to another question, you\’ve explained that \’Spot and Futures converge upon expiry; not during expiry\’.

From this what I understood is that in Cash & Carry arbitrage, we\’ve to close our positions in both Spot and Futures just before expiry ( to be precise around 3.20 PM on expiry day) to realise the profit in that particular trade.

Is my understanding correct..?

Or is it in any other way that we should execute C&C arbitrage..?

It is better that way because you can avoid the hassle of physical delivery, Abu.

Hello Sir,

I am a little confused by this.

When ever the future price is trading below the spot what exactly does this signify? Future is trading at a discount, is this a bullish or bearish sign.

Does the Future lead the spot or the Spot lead the future?

Like during Covid 2020 time future was below the spot constantly and nifty kept falling down.

Yesterday on Friday 23/09/21 Future was below the spot by 10-20 points and eventually it moved up.

Not sure how to understand what can be done if future is below or above the spot.

It just means that the futures are either at a discount or premium to spot. Does not really signify bullish or bearishness. Spot leads the futures, small variations do happen and that is mainly due to the demand and supply situation.

Hi, why it is better to unwind just before the expiry as suggested here?

Its just that you don\’t have to deal with physical delivery.

Sorry Karthik Sir, the formula is working just fine.

I miscalculated days to expiry. 🙏

Good luck!

Sorry, Wrong Month has mentioned .

IRCTC dividend announcement date Was 29 june 2021 and no effective date has given . It\’s Been two month no effective date has updated and they are paying 5 rs per share .

So, I supposed to Take 5rs as a present Value of dividend to calculate the future value of contract .

Got it, in such cases, you usually minus the dividend value. No need to take the present value.

Futures Price = Spot price *(1+ rf )– d

Where d is the dividend.

Hi,

I checked the IRCTC future , it is trading at discount and I also checked the dividend dates .

On websites dividend declare date ( Aug 2021 ) has given but no effective date has mentioned . So , how would I calculate the present value of dividend .

The present value will be the same, considering there isn\’t much time gap between the dividend date and date you receive on.

Hello karthik sir, future price formula doesn\’t seem to work , or may be I\’m counting it all wrong, the current rf rate is 3.33 it seems

What prices are you getting now, Samay?

Hi Karthik,

I calculated the future pricing of SBILIFE.

where;

Spot price – 1181.45

Risk rate – ( 1+ 3.30 ) ( T – Bill 91 days)

Maturity – 35 /365 ( long on 27 aug )

Expire on – 30 September

I put all values in a formula where I my answer stands 1186.33

When I check on a website at that particular time future was trading at 1185 .

What\’s that mean ?

Is that future value is undervalued and at some later point it will jump to 1186 .

These differences could arise out of small discrepancies while factoring in the variables like maturity, risk rate etc. It\’s good to assume that the fair price is in a region rather than an exact price. In this case, maybe between 1184.5 to 1186.5 I\’m just giving a random example here, but I hope it conveys the thought.

Sorry for bothering you again and again

My next question is when we should deduct the dividend amount from spot price . when it is declare by the company or when it is credited to the shareholders account ( record date ) . To calculate the fair value of future .

Suppose : Declare date of dividend on 1 Sep 2021 and record date is 28 Sep 2021 and I buy to September future on 15 September 2021

So should I deduct dividend to calculate the fair value of future ?

Dont hesitate to ask your queries 🙂

You need to factor the dividend on the record data, Shubhika.

Hi.

I have a question regarding future pricing formula

I am taking a example of future ASHOKLEY as this company about to credit the dividend to the shareholders with effective date 31 Aug 2021.

SPOT PRICE – 134.15

dividend declared per share – 0.60

Now how we calculate dividend to get the fair value of September future contract

For all practical purposes, this is a small dividend amount, so it won\’t really have an impact on your futures price.

The spot price and future price are even different for expiry day… but you stated here, that will become same

Post expiry, the settlement price will be the same.

Hi Karthik,

Your articles have been helping me up my game. Thanks a ton!!

Just a quick one, I\’m having a hard time finding a source from where I can download continuous futures prices for some historical analysis I wanted to do for spread trading. Does zerodha provide this somewhere? Am not a programmer so am stuck at the first step. Would be of great help if you can guide me on this.

Regards

Anchit

It is available but via the APIs. I\’d suggest you contact NSE authorized data vendors for this.

Hello Karthik, My question is that if Spot and Future prices always converge, then why the spot price of TCS today (Rs. 3210, on 24/07/21)is different than its Future Price (Rs 3218.10, contract expires on 29/07/21)? Please clear my confusion, I will be obliged.

They converge, but that happens upon expiry, not during the expiry.

how to download this data for different expiry futures.

In Calendar Spread example, why/how can Mid Month future trading at lower than Current Month? Typically it should be trading at higher price , right? In continue, By knowing Calendar Spread strategy, every one would be Buying Current Month Expiry & Selling Mid Month Expiry( Square -off Position), Can liquidity be an issue in this case?

The price discrepancy occurs due to supply-demand situations in the market.

Hi Karthic,

I have a Lite trading Account with Edelweiss. How to go for \” Cash & Carry Arbitrage\” and \” Calendar Spreads\” in Futures contract. I can either take a buy position or sell position. But how to take both positions simultaneously, so as to get margin benefit.

For calendar spreads, check this – https://zerodha.com/varsity/chapter/calendar-spreads/

For margin benefit, I guess you will have to speak to your broker 🙂

Thanks.

Hi, can anybody tell me whether \”Trading Strategies\” module is available or not.

Please check this – https://zerodha.com/varsity/module/trading-systems/

Sir in currency,current month was trading at discount so I bought and sold next month which was trading near fair value.Have I executed in correct order

Trading at a discount should not really be a reason for you to trade next month, unless you have a specific reason for it.

Is it 100% guaranteed that spot and futures price will converge on expiry in every case ?

On expiry yes, spot and futures will converge.

Card 9/9 of chapter 2 – Future pricing on the varsity app is wrongly placed. You have included hedge effectiveness on the card while it should have been abt Systematic risk.

Checking this, thanks Praveen.

1) Can we find faire value of any future, readymade online?

2) how to find risk free rate (rf) for any particular stock?

1) Not sure, perhaps there are sites that offer this feature.

2) Rf is a standard rate and does not vary from one stock to another. This is available on RBI site.

Hi kartik you replied to one question from comment section that price can be on discount due to heavy future selling but according to mathematical equation there is no variable in the equation which affect by selling

Pls explain

What the equation does not capture is the demand and supply situation in that market, which can also lead to discount or premium.

Hi Karthik,

I have noticed a few inconsistencies while reading this chapter on mobile version on Varsity. Some content is skipped while publishing on the mobile version. Can you ask team to check?

If it\’s skipped, then its because its not so important to know and you can actually make your way through the markets with or without that.

Hi Kartik, thanks for the amazing explanation. I had a doubt in the last part of your explanation.

When we are selling current month futures and buying mid month futures, are we squaring off both the transaction on the expiry date of our current month futures?

If yes, then will not the mid month future price change based on the spot price at expiry? For example, if the spot price is 715(as given in your third scenario) wont the mid month future price change to 715*(1+8.35 %( 30/365)) – 0, which is 720.72? It\’ll be great if you could explain as to how we are squaring off this trade.

Cheers.

Yup, you need to. However, there is a better way to do this. Check this article – https://zerodha.com/varsity/chapter/calendar-spreads/

Hello sir

Does shorting or create long of future contract affects on the price of future, if no then why so many analysts emphasizes on data of contracts.

e.g- No. of contracts decreased but price increased it means short covering. While short cover doesn\’t affect on price of future. Please clarify…

It does not. They just comment on the Open interest (OI). OI on its own is not of much use, you need to match it with both price and volume to draw conclusions.

Above ultratech cash and carry arbitrage trade,paper traded it went well

Only concern is its capital intensive to buy/sell in spot market

Where retail guy or student like me can\’t execute the trade

Is there any way we can manage this

Hmm, no other way to reduce the margins Chandu.

https://drive.google.com/file/d/1Kag7ww2cgdFzouJfwWTzQPm6EeGG5caB/view?usp=drivesdk

Buying in spot requires huge capital

Kindly go through the link

Will do. Yes, spot requires cash.

Yes sir still money control has this utility

To confirm I applied future pricing formula and calculated some math,actually it woked!

Great! Happy trading 🙂

Hello Sir in previous modules you said tha the mid-month contract has high price than current month but here it appears reverse please explain

That is generally true, but at times, the supply-demand dynamics and cause the situation to flip.

Sir is there any application for scanning cash and carry arbitrage opportunity and calendar spread

Should I every stock is there opportunity

I thought of finding today since expiry is next week I thought almost spot and future price will converge now

2) Is it good idea to find for spread at beginning of expiry month or 15 days left to expiry

Chandu, I think Moneycontrol had a utility long back, not sure if it exists still.

Thank you so much Karthik Sir.

Regards

Ashish

Happy learning, Ashish.

Sir, First of all thank you so much for such valuable information. My question is :can we always take risk free rate equal to 91 day T- bills from RBI site , (currently this is 3.35% )to calculate fair value of Futures.

Yup, you can.

Thank you Karthik Sir for the quick response. Clear explanation. I understood now.

Another thing which i want to ask is, are all these rules, techniques, process and procedures limited to individual stock futures and will it differ if we talk about the index futures ?

Also, how does all this differ if we bring into context the commodity and the currency futures ?

Regards

Ashish

They work across any asset, Ashish. Both stocks and Index. Equity, Index, commodities, or FX.

Yes, even i thought so. So there\’s no arbitrage opportunity exists here right?

Secondly, i have seen lot of articles there\’s mentioning of a borrowing cost which is added to the risk free interest rate and then calculated the fair value of futures prices. Can you throw some light on it? Also, does borrowing comes under the definition of carrying cost and if that exists, how will the prices differ?

Another thing is that, i have read there should be a maximum gap of Rs 5 between the spot price and futures price and anything beyond that creates room for arbitrage. Does it apply to all trades ? I mean if a stock\’s spot price let say is Rs 65. Fair Value of Futures price is Rs 68 and the actual futures price is also Rs 68, does arbitrage exists here ?

Can you explain and give reasoning for the same ?

Regards

Ashish

The borrowing cost or the cost of carry is kind of baked into the price that you see, Ashish. So don\’t worry too much about it. The 5 Rupee thing is to mainly accommodate for the costs incurred. BEst to look at it from a % term so that you can use 1 percentage across all trades. For example, the arb should offer at least 1%, of which you can buffer 0.3% for costs and the rest as your P&L.

Hello Karthik Sir

I have understood the pricing and the opportunities that exist for arbitrage but i am confused at a point. As per your example, Wipro Spot is trading at Rs 653, Fair value of Futures is Rs 658 while actual value of futures (randomly) is Rs 700. Here, we can arbitrage and sell futures and buy the spot. But let\’s say a stock is trading at a spot price of Rs 4550, the fair value of futures is Rs 4707 and the actual futures value is 4600. Does arbitrage exist here ? I\’m confused between the following two choices –

1. Buy only futures and hold spot

2. Sell spot and buy futures

Kindly give the reasoning for both

Regards

Ashish

Ashish, the problem with this is that you cannot short spot here, hence it will be tough to carry forward this trade.

I\’ve found this part to be the most complicated one in the entire module.

Hmm, pricing is something good to know but can be skipped. Having said, if you have found something difficult, please do let me know and I\’ll try my best to explain.

Sir , In cash and carry arbitrage as u said buy wipro at the spot price and sell wipro futures

But wipro futures has a lot size whereas buying wipro at spot means? like quantity or by how?

Yes, you will have to buy to the extent of the lot size of Wipro to ensure the quantity matches.

Hi Karthik

I have a doubt… Future price is trading in premium what does it mean… Can v long ..

No, it just means that the futures is trading at a premium to spot. This does not necessarily mean it is a signal to go long.

During short covering, how stock price increase.Future price derived from spot price, so buying in cash is required, while short covering is in futures.Does future price influences cash price also

Sometimes, the reverse is true, although for a short period.

If i forgot to square off my position on expiry date then will exchange take share from my demat account without any penalty

And

Where is the option to give authority to take shares of my demat

Yes, depends on the position you will either get delivery of stock or shares will be debited from your DEMAT.

Hello kartik,

Why we take 90 days treasury bill rate ?

Secondly if we r using 90 days treasury bill rate then we can use x/90 for calculation .

We take that as a proxy for a risk-free rate. You need to consider this on an annualised basis, hence 365 basis works.

HI Karthik

I know when there is more days to expiry, there will be some difference between cash and future price because of some formula which i read from this article only. But my question is here yesterday for coal india, closing price for cash is 151.8 and today opening price is 155.5. Difference is 3.7. In futures yesterday closing price was 148.85 and today opening price is 151.85. Difference is 3. i want to know why there is difference of 3.7-3=0.7 here in case of profit. i mean if there is 2% profit in cash, why same 2% profit is not there in futures? Suppose if its closer to expiry, then same percentage of profit we will get?

Kiran, generally speaking, Futur trades at a higher price to spot, but under some circumstances, it could be the other way round as well. This can happen due to –

1) Dividends expected or

2) Demand and supply situation.

Hi, I had purchased one share of BHEL in spot market to see how can I sell it in Futures

Contract of BHEL. However I not not able to do so as I am only getting NSE n BSE option for sell . I am not getting futures option.

Futures is a different segment, also you need to buy and sell in the lot size prescribed.

Sir, you have promised to have a separate module on Trading Strategies, when would you release it ?

OR Trading System module is the Trading Strategy module

Yes, Trading system, check this – https://zerodha.com/varsity/module/trading-systems/

Sir if itc spot on 213 and future on 210 then how can made spread.

The difference is 3, that\’s the spread.

u said that future price will be low than spot when contracts sell heavily in the market? we knoew that futures are contracts,how supply and demand work in contract as we can make as much as contract if i could find a counterparty.kindly explain this concept easily

Sorry, I didn\’t get your query completely. Can you please elaborate on this?

Dear Sir,

If I purchase at 3715 and the LTP is 3720 and the settlement time becomes 3696.55 I would end up losing money right?

What time is the settlement price determined?

You had mentioned mainly make trades before closing, but this is bound to lose money.

Is there a way to avoid this?

The settlement price is important for trades held to expiry, otherwise, it may not be. The settlement price is nothing but the last 30 minute average of the traded prices.

Dear Sir,

Please see this link https://imgur.com/a/UM3fYG5.

There is a big difference between future close price and the settlement price.

Why is this possible?

If the closing price is higher than the settlement price, this would be I would have a M2M loss of the difference between close price and settlement price?

Can you please explain this?

Settlement price and close price are the same right? 3696.55 in this case. 3720 is the last traded price, which is different from the closing price. The CLosing price is the average of the last 30 minutes.

why are we calculating mid months p&l wrt to the expiry value of the current months contract in the calendar spread ?

We are not right? P&L is calculated wrt the underlying.

Sir why is the current month\’s expiry (660, 690, 725) is the selling price for the mid month\’s long contract. Shouldn\’t it be different since its a futures contract for current month as the last current month contract is expired?

Sorry, I dint really get your query. Can you please quote specific numbers?

Sir why is the expiry value of the current month (660, 690, 725) is the selling price for the mid month?

Its market driven right?