1.1 – Overview

The Futures market is an integral part of the Financial Derivatives world. ‘Derivatives’, as they are called, is a security whose value is derived from another financial entity referred to as an ‘Underlying Asset’. The underlying asset can be anything a stock, bond, commodity or currency. The financial derivatives have been around for a long time now. The earliest reference to the application of derivatives in India dates back to 320 BC in ‘Kautilya’s Arthashastra’. It is believed that in the ancient Arthashastra (study of Economics) script, Kautilya described the pricing mechanism of the standing crops ready to be harvested at some point in the future. Apparently, he used this method to pay the farmers much in advance, thereby structuring a true ‘forwards contract’.

Given the similarities between the forwards and the futures market, I think the best possible way to introduce the futures market is by first understanding the ‘Forwards market’. The Understanding of Forwards Market would lay a strong foundation for learning the Futures Market.

The forwards’ contract is the simplest form of derivative. Consider the forwards’ contract as the older avatar of the futures contract. Both the futures and the forward contracts share a common transactional structure, except that the futures contracts have become the trader’s default choice over the years. The forward contracts are still in use but are limited to a few participants, such as the industries and banks. The focus of this chapter is to help you understand the structure of a typical forwards transaction, after which we will break it down into its elements and understand its advantages and disadvantages.

1.2 – A simple Forwards example

The Forward market was primarily started to protect the interest of the farmers from adverse price movements. In a forward market, the buyer and seller agree to exchange the goods for cash. The exchange happens at a specific price on a specific future date. The goods’ price is fixed by both the parties on the day they agree. Similarly, the date and time of the goods to be delivered is also fixed. The agreement happens face to face with no intervention from a third party. This is called “Over the Counter or OTC” agreement. Forward contracts are traded only in the OTC (Over the Counter) market, where individuals/ institutions trade through negotiations on a one to one basis.

Consider this example; there are two parties involved here.

One is a jeweller whose job is to design and manufacture jewellery. Let us call him ‘ABC Jewelers’. The other is a gold importer whose job is to sell gold at a wholesale price to jewellers. Let us call him’ XYZ Gold Dealers’.

On 9th Dec 2014, ABC agreed with XYZ to buy 15 kilograms of gold at a certain purity (say 999 purity) in three months (9th March 2015). They fix the price of gold at the current market price, which is Rs.2450/- per gram or Rs.24,50,000/- per kilogram. Hence as per this agreement, on 9th March 2015, ABC is expected to pay XYZ a sum of Rs.3.675 Crs (24,50,000/Kg*15) in return for the 15 kgs of Gold.

This is a very straightforward and typical business agreement that is prevalent in the market. An agreement of this sort is called a ‘Forwards Contract’ or a ‘Forwards Agreement’.

Do note; the agreement is executed on 9th Dec 2014, irrespective of the price of gold 3 months later, i.e. 9th March 2015, both ABC and XYZ are obligated to honour the agreement. Before we proceed further, let us understand each party’s thought process and understand what compelled them to enter this agreement.

Why do think ABC entered into this agreement? Well, ABC believes the price of gold would go up over the next 3 months; hence they would want to lock in today’s market price for the gold. Clearly, ABC wants to insulate itself from an adverse increase in gold prices.

In a forwards contract, the party agreeing to buy the asset at some point in the future is called the “Buyer of the Forwards Contract”; in this case, it is ABC Jewelers.

Likewise, XYZ believes the price of gold would go down over the next 3 months, and hence they want to cash in on the high price of gold available in the market today. In a forwards contract, the party agreeing to sell the asset at some point in the future is called the “Seller of the Forwards Contract”, in this case, it is XYZ Gold Dealers.

Both the parties have an opposing view on gold; hence they see this agreement to be in line with their future expectation.

1.3 – 3 possible scenarios

While both these parties have their own view on gold, only three possible scenarios could pan out at the end of 3 months. Let us understand these scenarios and how they could impact both the parties.

Scenario 1 – The price of gold goes higher.

Assume on 9th March 2015, the price of gold (999 purity) is trading at Rs.2700/- per gram. Clearly, ABC Jeweler’s view on the gold price has come true. At the time of the agreement, the deal was valued at Rs 3.67 Crs, but now, with the increase in Gold prices, the deal is valued at Rs.4.05 Crs. As per the agreement, ABC Jewelers is entitled to buy Gold (999 purity) from XYZ Gold Dealers at a price they had previously agreed upon, i.e. Rs.2450/- per gram.

The increase in Gold price impacts both the parties in the following way –

| Party | Action | Financial Impact |

|---|---|---|

| ABC Jewelers | Buys gold from XYZ Gold Dealers @ Rs.2450/- per gram | ABC saves Rs.38 Lakhs ( 4.05 Crs – 3.67 Crs) by this agreement |

| XYZ Gold Dealers | Obligated to sell Gold to ABC @ Rs.2450/- per gram | Incurs a financial loss of Rs.38 Lakhs. |

Hence, XYZ Gold Dealers will have to buy Gold from the open market at Rs.2700/- per gram and sell it to ABC Jewelers at the rate of Rs.2450/- per gram, thereby facing a loss in this transaction.

Scenario 2 – The price of gold goes down.

Assume on 9th March 2015, the price of gold (999 purity) is trading at Rs.2050/- per gram. Under such circumstances, XYZ Gold Dealers view on the gold price has come true. At the time of the agreement, the deal was valued at Rs 3.67 Cr, but now, with the decrease in gold prices, the deal is valued at Rs.3.075 Cr. However, according to the agreement, ABC Jewelers is obligated to buy Gold (999 purity) from XYZ Gold Dealers at a price they had previously agreed upon, i.e. Rs.2450/- per gram.

This decrease in the gold price would impact both the parties in the following way –

| Party | Action | Financial Impact |

|---|---|---|

| ABC Jewelers | Is obligated to buy gold from XYZ Gold Dealers @ Rs.2450/- per gram | ABC loses Rs.59.5 Lakhs ( 3.67 Crs – 3.075 Crs) under this agreement |

| XYZ Gold Dealers | Entitled to sell Gold to ABC @ Rs.2450/- per gram | XYZ enjoys a profit of Rs.59.5 Lakhs. |

Even though Gold is available at a much cheaper rate in the open market, ABC Jewelers is forced to buy gold at a higher rate from XYZ Gold Dealers hence incurring a loss.

Scenario 3 – The price of Gold stays the same.

If on 9th March 2015, the price is the same as on 9th Dec 2014, then neither ABC nor XYZ would benefit from the agreement.

1.4 – 3 possible scenarios in one graph

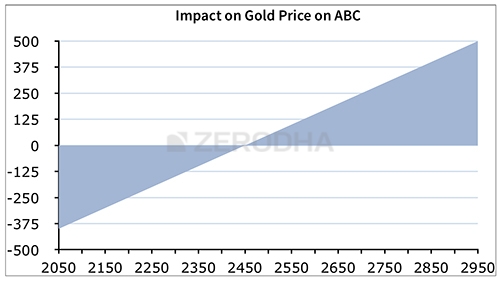

Here is a visual representation of the impact of gold prices on ABC Jewelers –

As you can see from the chart above, at Rs.2450/- per gram, there is no financial impact for ABC. However, as per the graph above, we can notice that ABC’s financials are significantly impacted by a directional movement in the gold prices. Higher the price of gold (above Rs.2450/-), higher is ABC’s savings or the potential profit. Likewise, as and when the gold price lowers (below Rs.2450/-), ABC is obligated to buy gold at a higher rate from XYZ, thereby incurring a loss.

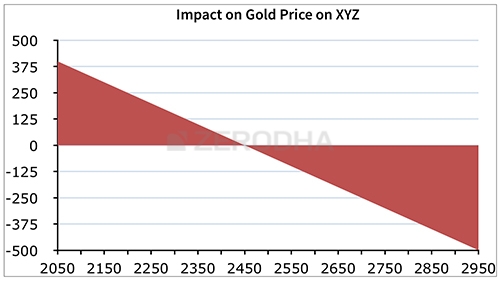

Similar observations can be made with XYZ –

At Rs.2450/- per gram, there is no financial impact on XYZ. However, as per the graph above, XYZ’s financials are significantly impacted by a directional movement in the gold prices. As and when the price of gold increases (above Rs.2450/-), XYZ is forced to sell gold at a lower rate, thereby incurring a loss. However, as and when the price of gold decreases (below Rs.2450/-), XYZ would enjoy the benefit of selling gold at a higher rate, at a time when gold is available at a lower rate in the market, thereby making a profit.

1.5– A quick note on settlement

Assume that on 9th March 2015, the price of Gold is Rs.2700/- per gram. Clearly, as we have just understood, at Rs.2700/- per gram, ABC Jewelers stands to benefit from the agreement. At the time of the agreement (9th Dec 2014), 15 Kgs gold was worth Rs. 3.67Crs, as of 9th March 2015, 15 kgs Gold is valued at Rs.4.05 Crs. Assuming at the end of 3 months, i.e. 9th March 2015, both the parties honour the contract, here are two options available to them for settling the agreement –

- Physical Settlement – – The buyer of a forward contract pays the full purchase price, and the seller delivers the actual asset. XYZ buys 15 Kgs of gold from the open market by paying Rs.4.05Crs and would deliver the same to ABC on the receipt of Rs.3.67 Crs. This is called a physical settlement

- Cash Settlement – In a cash settlement, there is no actual delivery or receipt of security. In cash settlement, the buyer and the seller will exchange the cash difference. As per the agreement, XYZ is obligated to sell Gold at Rs.2450/- per gram to ABC. In other words, ABC pays Rs.3.67 Crs in return for the 15 Kgs of Gold which is worth Rs.4.05Cr in the open market. However, instead of making this transaction, i.e. ABC paying Rs.3.67 Crs in return for the gold worth Rs.4.05Crs, the two parties can agree to exchange only the cash differential. In this case, it would be Rs.4.05 Crs – Rs.3.67 Crs = Rs.38 Lakhs. Hence XYZ would pay Rs.38 lakhs to ABC and settle the deal. This is called a cash settlement

We will understand a lot more about the settlement at a much later stage. Still, at this stage, you need to be aware that there are basically two basic types of settlement options available in a Forwards Contract – physical and cash.

1.6 – What about the risk?

While we are clear about the structure (terms and conditions) of the agreement and the impact of the price variation on either party, what about the risk involved? Do note, the risk is not just with price movements, there are other major drawbacks in a forward contract, and they are–

- Liquidity Risk – In our example, we have conveniently assumed that ABC finds a party XYZ who has an exact opposite view with a certain view on gold. Hence they easily strike a deal. In the real world, this is not so easy. In a real-life situation, the parties would approach an investment bank and discuss their intention. The investment bank would scout the market to find a party who has an opposite view. Of course, the investment bank does this for a fee.

- Default Risk/ / Counterparty risk – Consider this, assume the gold prices have reached Rs.2700/- at the end of 3 months. ABC would feel proud of the financial decision they had taken 3 months ago. They are expecting XYZ to pay up. But what if XYZ defaults?

- Regulatory Risk – The Forwards contract agreement is executed by mutual consent of the parties involved, and there is no regulatory authority governing the agreement. In the absence of a regulatory authority, a sense of lawlessness creeps in, which in turn increases the incentive to default.

- Rigidity – Both ABC and XZY entered into this agreement on 9th Dec 2014 with a certain gold view. However, what would happen if their view would strongly change when they are halfway through the agreement? The rigidity of the forward agreement is such that they cannot foreclose the agreement halfway through.

The forward contracts have a few disadvantages, and hence future contracts were designed to reduce the risks of the forward agreements.

In India, the Futures Market is a part of a highly vibrant Financial Derivatives Market. During the course of this module, we will learn more about the Futures and methods to trade this instrument efficiently!

So, let’s hit the road!

Key takeaways from this chapter

- The forwards’ contract lays down the basic foundation for a futures contract.

- A Forward is an OTC derivative, which is not traded on an exchange.

- Forward contracts are private agreements whose terms vary from one contract to the other.

- The structure of a forwards contract is fairly simple.

- In a forward agreement, the party agreeing to buy the asset is called the “Buyer of the Forwards Contract.”

- In a forward agreement, the party agreeing to sell the asset is called the “Seller of the Forwards Contract.”

- A variation in the price would impact both the buyer and the seller of the forwards’ contract.

- Settlement takes place in two ways in a forward contract – Physical and Cash settlement.

- A futures contract reduces the risk of a forward contract.

- The core of a forward and futures contract is the same.

Hello Kartik Sir,

I have this one doubt, if I am bullish on a stock price say TCS, and I have booked a future lot for that price and suppose the price rises, so I make a profit on my future contract. But I can also similarly buy on spot price and simply sell anytime or suppose I sell on the contract end date only. Then why do I even buy future contract if I can make similar profit on spot price as well?

You will trade futures for leverage. If you dont need that, than you are better off trading spot.

Hi Karthik, What do you mean by \”You will trade futures for leverage\”? Could you please simplify please? I had the same question – why would anyone enter into a futures contract?

Futures operates on leverage right? For every 100 of yours your broker provides you 300.

Hi Karthik, What do you mean by \”You will trade futures for leverage\”? Could you simplify please? I have the same question – why would anyone enter into a futures contract if they can simply buy that stock and make that profit in the cash market?

Could you explain how futures derivatives can influence spot prices, especially as the contract approaches expiry? Also, is this something a futures trader should be concerned about?

Its usually the other way round. But sometimes on short term basis futures do influence the short term prices, especially when there is a lot of speculative activity in the market.

thanks sir, just one feedback if possible would be great to get a notification through email once query answered

I understand, but that would be a problem as there are many comments coming in and the number of notifications will be too high 🙂

How do futures differ from options

I\’d suggest you check the modules 🙂

sorry sir, small misunderstanding.

Good luck and happy learning!

Hi Karthik, i found little difference in video and the module for forward market.

could you please clarify

Whats the difference?

Is the.PDF or Ebook available now?

PDF is, please feel free to dowload.

Sir, 2 days back, I send the requisite bank statement for the last 6 months to activate F&O, it has been approved and only Currency exchange BSE (not even Currency for NSE) is activated. What happen to NSE/BSE F&O and NSE Currency?.

I activated all the segments during the process , except for commodity.

Please talk to the support desk for this.

thank you sir

by absorbing this futures and options content can one do trading at a professional level, i have zero idea on f&o

You indeed can get started, Yashwanth. Once you get started and gain more experience, you start getting better at it.

Thank you Karthik for your response and giving me the clarity.

Happy learning!

Hi Karthik,

Can you help me understand this query of mine.In intraday can I place a buy order in the cash market using margin and put a sell order in current futures contract.

Thank you

Sure, you can do that as long as you ha sufficient margins for both positions.

Hi Karthik,

Do you have a page/chapter in this tutorial about arbitrage . I want you to explain what it is and how it’s used in simple terms

Yes, do check this – https://zerodha.com/varsity/module/trading-systems/

short covering simply means exiting the positions?

Yeah, thats right.

Hi… Sir , I just want to know that why futures and options are called derivatives.In mathematics we have learnt that derivatives are thoose quantities which tells change in something with respect something. like velocity is derivative of distance. Acceleration is derivative of velocity. So here in (F&o) what is changing w.r.t. to what? Please clear this confusion

The futures and options prices are derivatives of the spot price, Manoj.

So in real worls also forwards contracts are there. right? so other than exchanges, is there any legal law regarding forwards to avoid any legal issues in India. such as Indian contracts act?

Forwards are kind of phased out and replaced by futures now, Krishna.

Something like betting in real world

Hmm, if you think so 🙂

Thank you ver much Karthik for clearing my doubts.

Sure, happy learning 🙂

So you meant that we can also place buy/sell orders on October futures on August/September and I can hold the October futures till the expiry date of October month or I will have to close it on August/September expiry date since I have placed the orders before the October month.

Yes, of course. You can actively trade from the time the contract is introduced.

Thank you Karthik.

However I would like to know whether we can place an buy/sell order for October futures in the month of September before the expiry of the September month.

Yes, you can. October contract is available for you since August itself.

Thank you Karthik for your response and I have checked M2M however I still have a concern. For e.g.I have 2 lakhs in my trading account and I put a sale order in Upl September futures on 10th September and the cash needed for the contract is 1.5 lakhs.So I have 50,000 cash in my trading account and since I am holding the contract since I am bearing losses each day but once I get a profit of Rs 10000 I would exit my position. So my query is how much amount I will have ,will it be 210000 or something else ?

Well, assuming you get 10K profit straightaway, you will be left with 2.1L. Note, I\’m saying this with the assumption that there are no mark to markets.

Hi Karthik,

I have a concern regarding futures. I have sold a single lot of Upl Sep futures on 19th September on Nrml and holding it since then and I intend to keep it till expiry as I am bearing losses.But my worry is that I am getting the Combined equity contract note everyday mentioning the pay in / pay out amount.

I am new to futures however I used to trade in spot /Delivery at that moment I used to get a Combined equity contract note for the shares traded but not always though I am holding the scrip but in futures I am getting the note..so am bit confused.

Please explain if you can

The payin payout is for the mark to market (M2M) settlement. I\’ve explained the concept of M2M later in this module.

Are the contents on Varsity web and Varsity application different..

I saw the Varsity web has key takeaways while the app does not..

Yeah, the key takeaways is not included in-app, since the app has short bite-sized content anyway.

I am Activated F&O option segment,but future option did not seen that\’s why I can\’t able to buy,what can I do??

Avinash, I\’d suggest you speak to the customer support desk for this, they will guide you through this.

Ok, sir.. Thank you..!

Good luck!

Sir, I am a teacher in a state government aided school. My doubt is –

1) Am I allowed to do intraday trading beside my job?

2) If I am allowed, how I should pay income taxes of salary and trading -collectively or separately ? Plz clarify..

Actually I had asked this doubt to Nitin Kamath sir but he hasn\’t responded it. I hope you will clarify this… Plz..!

1) I guess so, please do get a confirmation from your employer as well

2) Intraday income adds to your overall income and gets taxed accordingly, please do check with the CA once. You can refer to this module as well – https://zerodha.com/varsity/module/markets-and-taxation/

when you guys will release video based learning?

We already have, check this – https://zerodha.com/varsity/module/introduction-to-stock-markets-video-series/

Sir,

If someone completes the full course given in zerodha versity, is it required to get paid courses from other institutions?

Will be sufficient enough to grasp the know how and master the trading strategies in due course by practice?

I am little bit confused about the advertisements. Please guide.

Regards

Surajit Mukhopadhyay

I\’d think that this is more than sufficient to help you get started (and much more). After a few months or maybe a year, please reassess and take a call.

Very nicely explained I am wiser

Happy learning!

\”They both merge on the settlement day.\”

So other days, it tracks the anticipated price on the settlement date and not the current price right?

(I pressed \”reply\” to your comments, but still, these are posting as new comments, instead of aligning under your corresponding comments.)

Anyway, I appreciate your time and effort you put towards my queries. 🙂

Its like this – all else equal, the price of futures tracks the underlying\’s price. Given the way futures pricing works, futures always trades at a slight premium to the spot. But at times, this can change and futures can trade at a discount as well, this purely depends on the demand and supply situation of the market. However, on expiry day, the futures price and the underlying price merge or rather the futures are settled keeping the underlying price in perspective.

I don\’t see any navigation arrow. I\’m on mobile browser by the way, not app or computer.

Can you explain the dynamics of how a derivative can influence spot market price? Is it because spot market participants may refer future price for reference?

When traders tend to rush to close an existing derivative position (like short unwinding), then there could be a spike in the derivative which in turn case influence the spot. But having said that, the influence is usually for a short term duration and cannot really be sustained for long.

Is future price meant to track current spot price or market\’s expected spot price on the settlement date?

They both merge on the settlement day.

Please have a \”next\” button at end of each article.

There is a navigation arrow on the left-hand side.

Can a financial derivative move price of the underlying?

Short term movement may be possible.

Great learning

Happy learning!

I hv a doubt

Suppose I purchase 2 lots of future for xyz share and it shoots up showing a good profit can I square it of as quickly as possible within matter of time and book profit or I hv to hold it

And can I use the money received for another trade or I hv to wait.

You can square this off at any point, Nishant. No need to wait till expiry.

in default risk its mentioned that XYZ would default yo pay up but what would he default as he would be giving the gold and the only party to do default would be ABC as they have to make payment. can u pls clear this out for me?

The fact that he/she may not pay up gold upon the settlement time is the risk of default.

Nice explanation!

Thx for making it simple n understandable….

Happy reading, Sudhir!

i use a stoploss whenever i trade futures but i have been noticing that many a times my stoploss doesnt get triggered and my position runs into a huge loss because of this…please tell me how can this be resolved?? (i am using kite and trade only intraday)

There is no guarantee that the SL will get triggered, especially when there are sudden and large moves. If you want guaranteed execution, then you\’ll have to place a SL Market order.

Well, Okay Karthik ,no worries, I know as a retail investor there\’s nothing much to do about swaps.😅, Thanks for the reply.

Good luck, Naren.

Hi Karthik,

Recently I watched \”The Big Short\” and was curious to know more about Swaps , I just know it\’s just a type of Derivative, but can you please give a brief intro about it and if possible an example in Indian market context.

Ah, that is a complicated instrument, don\’t think I can explain that in a comment box, Naren.

Sir, Can you please explain why there is a difference between the SPOT prices on difference platforms. For e.g.

ACC Cement SPOT prices on 25th February, 2021 on

Zerodha kite application: 1801.25

NSE official website : 1,808.70

why there is so much difference. I am taking about only SPOT prices. Sir, please explain.

NSE website is slightly delayed prices, Kite is realtime.

thank you karthik sir

Good luck!

dear sir

i have two trading and demat account one is with ZERODHA and 2nd one is UPSTOX (suppose if i want BUY Stock future from one Trading a/c and same stock future for the same month contract i want to SELL from my 2nd trading a/c so is there any penalty will be charged from SEBI ) please guide me

No penalty, you can trade.

dear sir

suppose if i have two different trading and demat account and i want to BUY STOCK FUTURE from one trading A/c ……. and in another from 2nd trading account i want to SELLor SHORT the same STOCK FUTURE for the same month contract (is this possible or not if yes , is there any penalty from SEBI or others )

Yes, this is possible. No penalty as such.

Hello sir,

For doing intraday scalping in BNF futures. Do I need to observe spot too?

Which PA should be observed? Spot or Futures?

Spot has no volume/vol indicators so I am confused.

Need your advice as I want to trade futures for intraday purpose only.

For scalping, please look at just the futures price. In fact, you only need to look at the price of the futures and nothing else.

Yes,

The bracket order. Is there a way by which my trailing stop loss gets automatically modified every times the trade moves in my favour?

Thanks,

Anuj.

I guess bracket order is no longer functional.

Hi,

Are the trailing stop loss orders currently blocked for F&O delivery segment? I am having to manually modify my stop loss each time the position moves in my favour?

Please let me know.

Thanks,

Anuj.

Anuj, are you talking about Bracket Order? We have that blocked for over a year now.

Hello Karthik

In one reply on January 14, 2019 at 11:40 am, you mentioned –

\”Liquidity Risk is about availability, meaning if you intend to sell 100 shares, but if there is no one biding for 100shares then you cannot really sell it. This is liquidity risk.\”

In line with the example given in the article, I will try to explain it for other readers…

Suppose you are ABC Jewelers, and you have entered into a contract with XYZ Gold Dealer. Now you are going to hold that contract for period of 3 months. During that period of 3 months, if you want to sell that contract to other Jewelers, you might not find such a Jeweler ready to buying your contract. And you will end with holding that contract till 9th March 2015, meaning you will not be able to liquidate it.

That\’s right, Nilesh. This is liquidity risk.

I came to know about forward/ feture market RANGAPPA SIR it\’s very beautiful. I have been contacted to trade in f&o freequintly over

phone its very proffitable. I wanted to know it I switeched on pationfully read all. know i want know ..about option . what type of risk

is their and how it works. kindly advice me how can I start F and O trading. Sofar I am trading in real cash market of equities and in

sip of mutual funds .

DEar sir kindly do the need ful.

We have a module on Options and MF also, I\’d request you to please check this – https://zerodha.com/varsity/module/option-theory/ and this – https://zerodha.com/varsity/module/personalfinance/

Why are mutual funds and ETFs not considered derivatives when they also derive value from underlying?

But they are not leveraged right?

If a trader wants to place a protective call order on banknifty by buying 40,000 quantities (1600 lots) of banknifty calls and shorting 40,000 quantities(1600 lots) of banknifty futures then how can it be done using Kite platform? is it possible to place such a huge order without having to place each order individually?

You can trade upto 2500 lots per order I think. At 2500 lots, there is an order freeze.

Valuable lessons

Hi Karthik.

There are lots of topics in the mobile app which need some correction in regards to the content. Is there any formal channel where I can be a part of Varsity and contribute towards making the modules error-free.

Thanks Robin, have sent you an email.

A very good introduction to futures in a very simple and practical way. Thankyou.

Happy learning!

Then what is physical settlement. I heard about that somewhere

Do check this Prasad – https://zerodha.com/varsity/chapter/quick-note-on-physical-settlement-2/

I don\’t want to sell below futures even on expiry date?can I retain them?please explain

1Reliance Aug

2.bank nifty Aug

No, on expiry day the contract ceases to exist and hence it is considered closed and settled.

Are the study material for mobile and pc same?

95% they are same. Except for a few minor changes in the app.

Hi Karthik Rangappa

need your personal mail id or phone number

Sorry, I wont be able to share that. Please do post your queries here and I\’ll be more than happy to answer them for you.

Hey Karthik!

Sir, I noticed something today that the Nifty June futures were trading at a discount of about 84 rupees from the Nifty. But I have always seen that the futures trade slightly higher than the spot market. So why is this happening?

Futures keep fluctuating between premium and discount, this is just the market dynamics at play.

I want to study about put and call option. From which module I can study. Can I skip Technical and fundamental analysis for this and study those later on. Also is there need to study any other module before jumping to put and call learning

Yes, you can start the Options module directly.

Hi Karthik,

Could you please help with freeze limit. What is its role as I am Naive.

Check this – https://support.zerodha.com/category/trading-and-markets/margin-leverage-and-product-and-order-types/articles/what-does-the-error-rms-rule-check-freeze-quantity-for-fo-including-square-off-order-mean

Karthik / Nithin,

Will this data be published in Kannada also, so that it will be easy for everyone to understand.

Not sure, Anil 🙂

Hi Karthik,

May be it\’s a silly doubt, but I want to clarify something.

If ABC jewellers thinks that the price will go high, why can\’t they just buy it normally and keep the stock with them? what\’s the use of forward markets?

KEY-TAKEAWAY ME SECOND OPTION ME LIKHA HE FUT CONTARCTS EXCHANGE PE NAHI HOTE HE LEKIN MCX PE TO GOLD APRIL FUT TO AVAILIBLE HE

I have opened ac with Zerodha, I want GTT for Future and Options

GTT is available for equity trades only – https://zerodha.com/z-connect/tradezerodha/kite/introducing-gtt-good-till-triggered-orders

Hi Karthik,

First of all i want to tell you that you have very good method/skill of explaining concepts. Awesome. I have been trying to understand F&O concept and you have explained in a very simple way. Thanks a lot.

-Vishal Kulkarni

Happy to note that, Vishal. Hope you continue reading on Varsity 🙂

Hi Karthik Sir,

I have one doubt. Recently when all f n o trades will become physically settled,how would bank nifty weekly and monthly options(long strangle) will get affected? Also suppose a position consists of one bank nifty future long and two banknifty put at the money options then how this new rule will affect the margin. Can you provide one example. Thank you in advance for your help.

Amlan, the index contracts will continue the same way, so no changes there.

Suppose a trader wants to trade 10000 quantities (500 lots) of banknifty futures intraday..since freeze limit is 2500 will the trader have to place 4 separate orders? Is there any way how it can be done quickly on kite without using any Algos? Also is Bracket order leverage provided by zerodha for such big intraday trades?

You will have to place 4 different orders here. Yes, all BO/CO orders are leveraged.

Best material at absolutely free of cost.We all will have a great debt of your knowledge sir.sir what if xyz gold dealers brought the contracted amount of gold on the same day of the agreement he would also book some profits!! isn\’t it?

Yes, but that is also a contradiction of the contract right, Mahesh? The contract settles on the expiry date.

can these contracts be made on some other price than cmp.

If it is a forward, then yes, these are not standardized contracts and can be customized.

Sir, Liquidity risk is not clear, and also what does role of investment bankers. Please make it understand.

Liquidity Risk is about availability, meaning if you intend to sell 100 shares, but if there is no one biding for 100shares then you cannot really sell it. This is liquidity risk.

hello sir from where i can gain complete information about intraday?

There is a lot of content available here, Ayush. I\’d suggest you get started on Varsity.

Can i use borrowed money for trading without any certification if mutually agreed by lender.

This depends on the terms of the agreement with your lender. Some clearly state that you should not be trading with the funds borrowed.

lets take a real example my friend is ready to give me loan for certain fixed monthly interest for trading in markets. My concern is that will regulators would have any problem if i trade by using that money. For example consider loan amount to be 10 lakh and 2 percent that is 20000 monthly interest.

No Ricky, nobody will have a problem with this. As far as the regulator is concerned, the funds are coming in from a registered bank account. However, on a personal note – I\’d suggest you don\’t do this. I\’ve seen many do this only to end up in a bad state at a later point.

Thank You for your valuable personal advise.Even personally i would not lend anyone money for trading.

Yup, I\’ve seen this is happening over and over again.

Good luck!

Hi,

I have been trying to understand derivatives trade, and have read about the reasons why many prefer this to the spot segment; but one thing I still don\’t get is, how a public listed company benefits from the derivatives trade, since they themselves can not trade in them. Can any company refuse to have its derivatives traded in the f&o market?

The company does not really benefit from getting listed under F&O nor can they refuse this. This is basically dependent on the trading pattern, based on which the exchange takes a call.

Hlo sir I am new user of zerodha I want to gained knowledge for future trade so can u help regarding this

Pls reply contact me 8369003036

I\’d suggest you read through this module completely, Farook.

Hello .

Very lucid and easy to understand even for beginners.

I would like to request you though to use easier number (preferably round figures) while explaining hypothetical scenarios. For example : When we are trying to understand forward contracts between ABC and xyz for gold 2450*10*15 -4.06 crore etc , is very distracting. Kindly use simpler numbers especially for someone like me who is weak in Maths. Great explanations though.

Glad you liked the content, Sneha. Appreciate the feedback.

Hi Karthick,

with respect to the new rule by sebi under which it will put a limit to the exposure which retail traders can have in the derivatives market, will this rule apply even to the HNI (high net worth) traders as well?

I\’m not sure if there is any new rule like this. The most recent from SEBI is on physical settlement, check this – https://zerodha.com/z-connect/tradezerodha/policy-on-settlement-of-compulsory-delivery-derivative-contracts

I meant about the proposed rule which sebi plans to put in place wherein retail traders derivatives exposure will be decided by their income tax returns..will this apply to HNI traders as well?

Well, its hard to speculate on what SEBI will come out eventually. But I guess if you can prove to have enough net worth, then it should not be a problem to continue trading F&O I guess.

This is a beautiful, simple, effective delivery of the subject matter. All chapters are excellent. The question and answers

also removes lot of doubts.

Congratulations to the entire team.

Thanks for the kind words, Prem!

Good luck and happy learning!

Hi Karthik,

Recently there was news that sebi is considering to impose tighter restrictions on retail traders who do fno trading wherein their total exposure in fno positions wil be limited to some amount as determined by their income tax filing. Brokers are already protesting this move.. do you think such a decision will be implemented? Becoz at the end of the day it is the retail trader who wud not be able to grow his account becoz he cannot add his gains from previous trades as there wil be an upper cap and hence no compounding will be possible..

I personally think its a bad idea. Take a look at this – https://tradingqna.com/t/derivative-exposure-based-on-income-tax-returns-for-retail-traders-outcome-from-latest-sebi-board-meeting/36279

Hi Sir,

In case we hold a future contract of a stock and say its in a profit of 5rs a share,but then in middle if the stock dividend payout(Rs.8 /share) ex-date is reached and so the stock value is adjusted then,

1.Will the future price will also reduce?

2.If future price will reduced to Rs.8,then won\’t that lead us to a loss of Rs.3/share !!.

3.If it would lead us to a loss because of adjustment,then it means that no one will hold stock futures on the dividend ex-date?or will everyone short the stock future the previous day?

The contracts are all pre-adjusted to corporate actions. So, the effect is already known and reflects in the contract.

1.Means,will it lead us to a loss in this dividend payout situation if we hold the contract during exdate?

2.Had there been any situation , that in Spot market the stock price increase, but in future market very less people to buy so that future price decreases?If So in that case what to be done?

1) No – the futures contracts are not affected by corporate actions

2) Nope, since futures always mimics spot

Hi Karthik ,

1. Can i short Niftyfutures and carry it forward with a progressive/trailing stoploss for more than 1day to max till expiry of the month ?

2. what about shorting stocks or stockfuture?

1) Yes, of course, you can

2) If you short stocks, then the same has to be squared off the same day. However, you can carry over the stock futures until expiry.

suppose if a stock is trading at 200, and the results are weak and indicators are showing down trend , i expect 150-160 levels in a time period of week or or two, buying put option will be better than shorting stock regularly on mis?

And what if the stock is not traded in F&O?

Yes, because MIS is an intraday order whereas you can carry forward the PUT options overnight. In case the stock is not in F&O, then I\’m afraid you have no option but to short the stock and cover it by EOD.

Thank you Karthik , all doubts cleared.

Good luck, Neeraj.

Hi karthik,

I have two ques. for you related to this chapter,

1.) Why both the parties pick a date 3 months in future, When they can settle the deal now, If ABC thinks the price will go up so they fix the deal at CMP and XYS thinks the prices will go down so he also try to fix the deal at CMP, if they are both ready the settle the deal at CMP then whats the point in waiting for 3 months when they can settle rite now because of opposing views, they are waiting just to see that how much one profited or lost from the deal.

2.) Suppose the gold dealers XYZ is not buying the gold at the end of contract, he some how already had 15kgs of gold which he purchased sometime back at 2300000/kg, so if he decides to sell the gold at 2400000 CMP he is already getting 100000/kg profit, So how will the cash settlement will take place in this particular case.

1) Because these are forward dated contracts, view materialize at a later point. For example, you want to travel to USA in May, you\’d ideally want $ in May, right? Not really in Feb? Likewise.

2) Possible, end of the day, the difference has to be made good. By the way, this is the reason why futures were introduced – to standardize the structure of the transaction between buyers and sellers.

in liquidity risk , the investment bank has to be paid a fee to find a party and make a deal happen. what is the risk involved here? didn\’t get that part.

What in case you cant find a counterparty? In this case, you are holding to a position and exposed to the directional risk.

Can you provide a detailed process(with pictures) for placing Futures order on Kite including calculations of Margin in layman’s term?

I\’d suggest you attend the daily demo we conduct, happens twice a day, keep track of it here – https://www.youtube.com/user/zerodhaonline/featured

Lets say i want to place a buy order(Normal) at RS 100. And once the order is executed i want to place a stop loss at Rs95. Now the problem i face is once i have place the order i have to wait for it to go through and then only i can place the stop loss.

So is there any way i can place both the order and once the buy is executed automatically stop loss will be placed?

Have you learned about the Bracket and cover order? Check this – https://www.youtube.com/watch?v=2TrYyOHA7P4&list=PLkxTRam6E2V-okv6gwQlt6dLTsn0v6CD1&index=8 and this – https://www.youtube.com/watch?v=v4Buda7v-dY&list=PLkxTRam6E2V-okv6gwQlt6dLTsn0v6CD1&index=9

yes i know bracket and cover order. But those are for MIS. Is there something for the delivery trades?

No, not available for delivery trades.

I live in odisha and there is a cyclone. So no mobile connection no net connection. I hold a futures contract and i need to place a stop loss every morning(as long as i hold the contract). What would you do in that circumstance? Or any measures we can take before hand to deal with such problems?

Abhishek, I hope you are safe.

As far as the futures position is concerned, the request to place the order has to come from you, either via the terminal or by you calling our support center and confirming your ZPIN. There are no other options.

sir you can any providee the learning chapter in only equity maegin hpw to use and buy and sell share using margin please any provide

not so please give me a example

Check chapters 5 to 7 – https://zerodha.com/varsity/module/futures-trading/

1) lets say i hold 1 contract of SBI fut. Now next day sbi give dividend of say 10 rs per share. so the stock price will fall at the opening. But i hold a futures contract. what will happen in that case?

2) Also in case of stock split say 1:1 the price will half, does that mean i will now have 2 contract(i had 1 initially).

3) what if the ratio is not 1:1. say 3:1 now as the futures has a fixed lot what will happen in that case?

1) The futures price will be adjusted to the drop. You will not make any additional profits becuase of the dividend

2) Yes

3) Odd lots will be cash settled.

Hi Karthik,

Few questions

1. Can you short Futures and carry it for more than 1 day i.e Short Delivery of Futures?

2. I don\’t find Nifty Pharma F&O neither on NSE or on Zerodha Margin Calculator … However, there is a NiftyPharma a Index, but is there a F&O which you can trade?

1) Yes

2) Besides Nifty and Bank Nifty, no other futures are really liquid.

Thanks Karthik.

Assume i have squared off my Futures contract for profit.

1. When will the Profits available for me to withdraw (T, T+1 ..)?

2. When will the Margins be unblocked for me to Withdraw (T, T+1…)?

1) You can place a withdrawal request the same day

2) The moment you close the position

Hello sir,

SEBI is to likely to increase the trading time upto 5 pm or 730 pm.

What is your honest view on this?

And sometime later, to curb the retail participation in derivatives market, they would consider increasing the lot size or only allowing HNI to deal in derivatives market.

Your candid view on this also -)

Thank you

If this happens (increase in trading time), then this is good for scalpers. I personally think increasing lot size is also a good move, as it would curb excess speculation and encourage investments.

Hi,

I Buy XYZ futures @rs.100 on day 1 and sell it on day 10 at 12pm @rs.120.So my profit is Rs.20 per share.And when i sell it some one has to buy from me.So after he buy at 12pm price starts to shoot to Rs.122 and he hold it for the day without selling and continue as NRML.In this case did i lose any money apart from Profit???

No, you make your profit of 20.

Hi Karthick,

The writeup is amazing.I am going through all the modules to have more idea and to have solid knowledge

I have a question:

In cash settlement, whether ABC will buy actual gold from open market instead of XYZ ? The difference amount will be paid by XYZ to ABC which is a profit for ABC in this case ?

Yes, in cash settlement only the difference is paid, in cash.

Hi tell me about in future trading when we quit on fix contract date or any time pl tell about trading period.

You can square off the position anytime you wish.

NIFTY MOVES NIFTY FUTURES OR NIFTY FUTURES MOVE NIFTY?

Nifty spot moves Nifty futures.

In NRML,does BO and CO applicabe or not!

Yup.

Can we convert MIS to NRML in futures!

Yes, you can.

nice brokerage. study material are awsome . i will open a/c in zerodha . it is abest borkerage company

Thanks, we will look forward to you joining us.

lets say i but a lot of nifty50 fut to hold it for a few days. Day 1 i put the stop loss order. now if the SL is not hit, will this order be valid the next day or i will have to place a different order??

No, you will have to place a fresh order the next day.

Please make it available in hindi.

Few modules are already available in Hindi. Request you to check.

Explain roll over

Section 6.2 – http://zerodha.com/varsity/chapter/margin-calculator-part-1/

Hi Karthik,

I just want to trade in Nifty Options. Do I need to read up on all the modules or can I skip a few?

Thanks,

Sahil

Well, its always good to read up. However, if you are not up for it…then at least read the Options module before you start Options trading.

Hi Karthik,

Thanks for explaining the thing in very plain English with example. I am interested in commodity market but there is no course associated with commodity and mentioned that \”coming soon\”. When it is expected to launch the commodity course.

Dheeeraj – right now the focus is on Options, once options is done we will start with Commodities.

There is an annoying share prompt on the screen that refuses to go even if one shares the page.

Kindly remove as it is preventing smooth reading especially on mobile devices.

Got rid of it, thanks for pointing it Sunil.

not a problem sir , thanks for that this site is very useful for us

🙂

sir

why there is no pdf available after module 2 .please provide us

We are working on converting the content to e-book format. It takes a lot of time, request you to please bear with us in the meanwhile. Thanks.

Thank you for explaining things very well with examples!!!

Most welcome!

Karthik,

I want to understand how short covering in nifty futures makes underlying nifty index move.How it happens?whether arbitrage has a role to play in it.

Short covering is a term to express the fact that the traders with short position are closing their open positions. When they close their open positions they simply need to buy back the futures. This means there would be a surge to buy back shares, which would lead to a short rally in the market. As far as i can imagine, short covering has nothing to do with arbitrage.

Hi Karthik,

Short Covering:

People are expecting market may fall

Futures – short shares of ABC – Intention go down (opened the position)

Buy shares of ABC – Intention go up (so closed the position to make the profit)

People are expecting short/small rally may come to upside for some time, but the main trend is down.

Please correct if I am wrong about the short covering.

Thanks,

Siva.

True, short covering is when there is fear of increase in prices hence short sellers cover their positions in a panic to save themselves from booking a loss….by virtue of which the prices starts to increase. This is because when short sellers cover their positions, the need to buy back shares.

Hello sir

Can you tell me that I m trading in mcx and yesterday my unrealised profit was -4400, now is this amount deducted from my total account value or not for the next day trading starts, my all trades are normal to mis.

Yes, commodities are futures for which mark to market is applicable and the money will be deducted from your trading account.