7.1 – The trade information

I’m going to start this chapter by posting the same old question again – Why do you think margins are charged? Before you get annoyed and come chasing me, let me post the answer.

Margins are charged from a risk management perspective. It helps in preventing any undesired counterparty default. The risk management system at the broker’s office (often called the RMS system) is responsible for overseeing the overall risk management. You may be interested to know that the RMS is a computer program, and all orders placed by the clients reach the exchange only once this program approves it (which takes a fraction of a second), and people are monitoring if everything done is right/wrong.

When you place a trade, let us say to buy a futures contract (via a buy order entry form), you are essentially conveying the following details to the risk management system (RMS) –

- The contract you wish to buy (like TCS futures, IDEA futures etc.)

- The quantity you wish to buy ( number of lots)

- The price at which you want to buy (market or limit)

Once you place the order, the RMS system evaluates the margin requirement and allows your trade to go through (provided you have the required margin amount).

However, the information that you don’t normally provide to the RMS system is the following –

- The duration up to which you wish to hold your trade – is your trade intraday, or you would wish to hold on to it over multiple days?

- The stoploss point – If the trade goes against you, at what price point you would wish to book a loss and square off the position.

Now, what would happen if you provided these additional details to the RMS system? Obviously, with the additional information flowing to the RMS system, it would better clarify your risk appetite.

For example, the detail on the trade duration would let the system know how much volatility you are exposed to. If your trade is intraday, you are only exposed to 1-day volatility. However, if your trade is for multiple days, you are exposed to multiple days volatility and are also exposed to the ‘overnight risk’.

Overnight risk is the risk of carrying the position overnight. For example, assume I’m holding a long BPCL (a major oil marketing company in India) futures position overnight. BPCL is highly sensitive to fluctuations in crude oil prices. While I’m holding the BPCL futures, assume overnight the crude oil market shoots up by 5%. This will obviously harm BPCL the next day as it becomes more expensive for BPCL to buy crude oil from the international markets. Hence under holding a BPCL position overnight, I will suffer a loss. Therefore an M2M cut. This is called ‘overnight risk’. Anyway, the point that I’m trying to make here is straightforward – from the RMS system’s perspective, the longer you wish to hold the trade, the higher is the risk you are exposed to.

Likewise, think about the stoploss for the trade. By not expressing your intended stoploss, you keep the RMS system in total darkness concerning your risk appetite. Do note; this is not mandatory information that you need to reveal. However, if you do, the RMS system gets more clarity on your trade. For example, assume I buy BPCL futures Rs.649/-, in the absence of specifying a stoploss, I’m virtually exposed to unlimited risk. However, if I specify my stoploss as, let us say, Rs.9/-, then when BPCL falls to Rs.640/- (649 – 9), I would book a loss and get out of the trade. Hence, there is complete clarity on the amount of risk I’m willing to take, which is valuable information from the RMS system’s perspective.

So both – the duration and the stoploss of the trade give more clarity about your risk appetite to the RMS system. So what does this mean to you as a trader?

Well, think about it – the more clarity you provide in terms of the risk you face, the higher clarity the RMS system develops. The more clarity it has, the lesser the margins required!

Very loosely put, think about this as an equivalent to shopping for television at a consumer electronics store. I know this may not be very apt, but I hope the following analogy gives you the right message.

If you go to a consumer electronics store and inquire about a television’s price, the seller will assume you are a regular customer, and he will quote the normal selling price. However, if you tell him that you are likely to purchase 50 televisions, he will instantly drop the price.

If you tell him you are carrying the cash with you and are willing to finish the transaction right away, he will drop both his jaws and the prices even lower. The point is – as and when the shop keeper gets more information about the transaction, the more attractive the price gets.

7.2 – Product types

So far, one thing is clear, the more information (in terms of risk) you are willing to convey to the RMS system, the lesser is the margin required. Needless to say, the lesser the margins required, the more you can do with your capital. So, how does a trader convey this information to the RMS system? Well, there are specific product types that are meant for this purpose. While placing an order (to either buy or sell), you can specify the product type. There are many Product types, and they vary from one another, mainly in terms of their functionality and the information they convey to the RMS system. While the core functionality of these product types is standard, every broker calls them with different names. Of course, I will talk about the product types used at Zerodha; if you are still trading with another broker, I will request you to speak to them and identify the nomenclature used.

NRML – NRML is a standard product type. Use this when you intend to buy and hold the futures trade.

Remember, when you use NRML, the risk management system has no additional information on your trade length (as you can continue to hold the contract till expiry), nor does it have any information on the stoploss. You suffer losses (and therefore continue to pump in the required margins). Hence because of the lack of clarity, the broker’s RMS system charges you the full margins (i.e. SPAN and Exposure).

Use NRML when you intend to buy and hold the futures position over multiple days. However, do remember you can use NRML product type for intraday as well.

Margin Intraday Square off (MIS) – Zerodha’s MIS is a pure intraday product, meaning all trades placed as MIS product type will indicate that the trade will last only for the day. You cannot select MIS as an order type and expect the position to be carried forward to the next day. You have to mandatorily cut the position by 3:20 PM, failing which the RMS system will do the same.

Now because the product type is MIS, the RMS system clearly knows that it is an intraday trade, which is a notch better than NRML in terms of information flow. Remember, when the trade is intraday, the trader is exposed to only 1 day’s volatility. Hence the margin requirement is lower compared to the NRML margins.

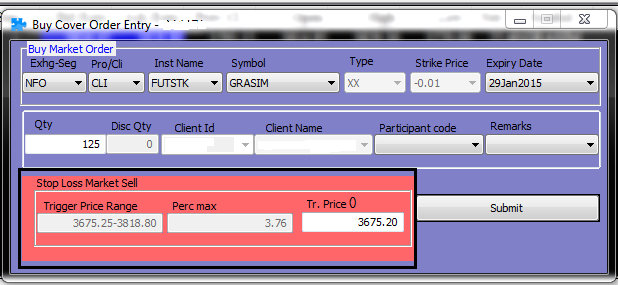

Cover order (CO) – The concept of cover order is simple. First, similar to MIS, the cover order (CO) is also an intraday product. However, the CO conveys additional information in terms of stoploss. This means, at the time of placing a CO, you will have to specify the stoploss as well. Hence CO conveys both the vital information –

- The length of the trade, which is intraday

- The stoploss, which is the maximum loss you will bear in case the trade moves against you.

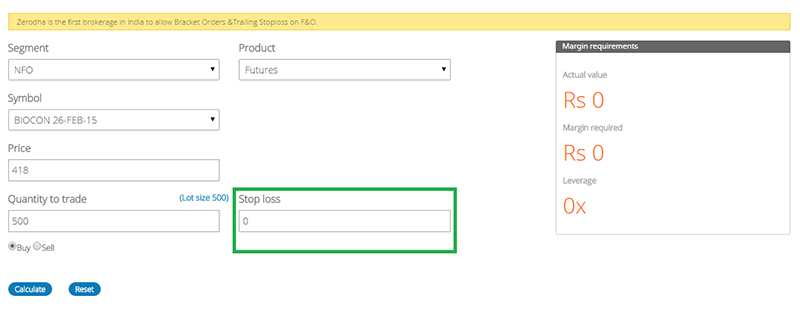

The snapshot below shows the buy CO form –

The area highlighted in black is where one is required to specify the stoploss.

I want you to be aware of this – by placing a CO, you are not only conveying that your trade is intraday but also conveying the maximum loss you are willing to bear. Hence under this, the margins should drop considerably (even lower than MIS).

Bracket Order (BO) – The bracket order is quite versatile. Consider the BO as an improvisation over the cover order. Needless to say, a BO is an intraday order, which means all BO orders have to be squared off within the day on or before 3:20 PM. While placing a BO, you will have to mention a few other things –

- The stoploss – At what place you would like to get out of the trade-in case the trade moves against you

- The Trailing stoploss – This is an optional feature where you can trail your stoploss. We have not spoken about “The trailing stoploss” so far. We will discuss the same towards the end of this chapter. But for now, remember the BO gives you an option to trail your stoploss; in fact, this is one of the most popular features of a BO.

- Target – If the trade moves in your favour, the BO also requires you to specify the price at which you would like to book the profits

The BO sends your order to the exchange, where simultaneously you can specify the target and the stoploss. This is a huge relief to active traders as it helps them in many ways.

The snapshot below shows the BO buy order form; the green box highlights the SL placements –

If you think about the Bracket Order, the trader conveys the same set of information to the RMS system as that of the CO. Besides, through the BO, the trader is also conveying the target price. Now, what difference does the information on the target price make to the RMS system? Well, it literally makes no difference to it from the risk management perspective. Remember, the RMS is only worried about your risk and not your reward. Hence, for this reason, the margin charged for BO and CO is the same.

Let us now keep the above discussion in perspective and look into a few other options available on Zerodha’s margin calculator.

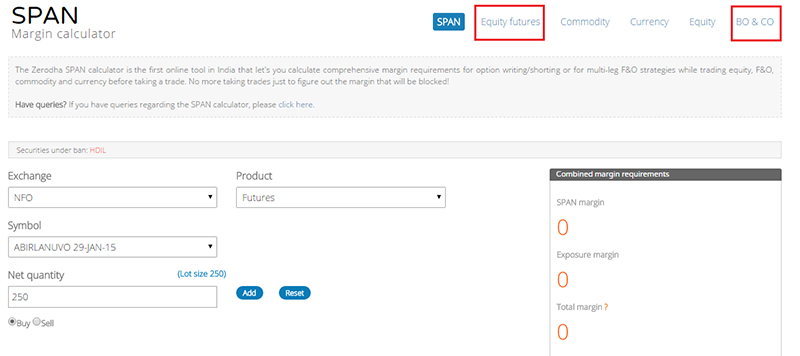

7.3 – Back to the Margin Calculator

Here is a quick recap – in the previous chapter, we introduced Zerodha’s margin calculator. The objective of the margin calculator is straight forward. It helps the trader figure out how much margin is required for the contract he wishes to trade. In our quest to understand the same, we also understood concepts of expiry, rollover, and spread margins. With this chapter’s help, we are now clear about the information flow to the RMS system and its impact on the applicable margins. Let us keep these in perspective and look at the other two options highlighted in red in the margin calculator – “Equity Futures” and “BO&CO”. Here is a snapshot highlighting these features –

Equity Futures – The equity futures section in the margin calculator is a ready reckoner, as it helps the trader understand the following –

- The NRML margin required for a particular contract

- The MIS margin required for a particular contract

- The number of lots that a trader can buy for the given amount of money in his trading account

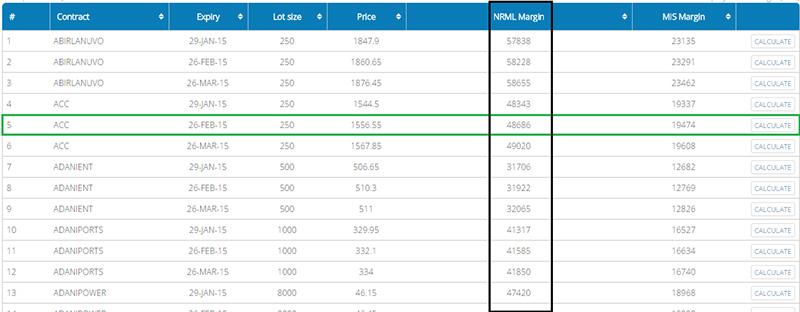

The Equity Futures section contains nearly 475 contracts (as of January 2015). To understand this better, let us take up a few tasks. We will solve these tasks by using the Equity Futures section of the margin calculator. And hopefully, in the process, you will understand how to use the section better.

Task 1 – A trader has Rs.80,000/- in his trading account. He wants to buy ACC Cements Limited Futures expiring 26th February 2015 and hold the same for 3 trading sessions. Find out the margin requirement for this contract. He also wants to trade Infosys January futures for intraday; what is the margin required? Does he have sufficient margins to initiate both the trades?

Solution – Let us deal with the ACC futures first. Since the trader intends to hold the futures contract for 3 working days, we need to look for NRML margins. Do note; this task can be achieved by using the SPAN calculator as well. We discussed this in the previous chapter. However, the Equity Futures calculator has a few more advantages over a SPAN calculator.

Visit the Equity Futures section, and you can see all the contacts listed here; scroll till you find the desired contract. I have highlighted the same in green. Do notice; the calculator is also listing the contract’s expiry date, lot size, and the price at which the contract is trading.

The black vertical box highlights the NRML margin for each contract.

From the table, it is clear that the ACC Feb 2015 requires a margin of Rs.48,686/-.

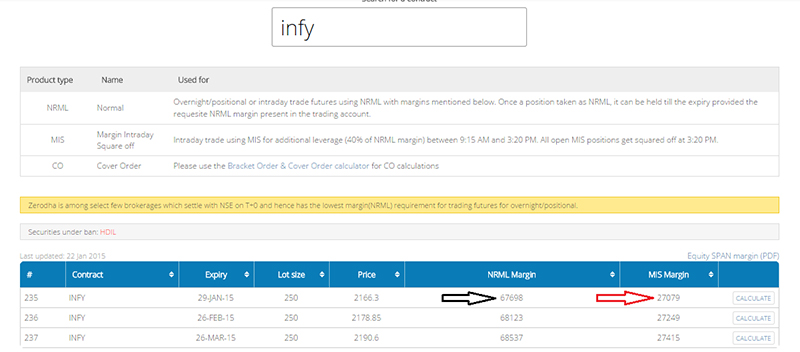

To determine the margin requirement for Infosys, I need to scroll down till I spot Infosys January contracts or type “Infy” in the search box provided.

As we can see, Infy’s NRML margin is Rs.67,698/-(highlighted in the black arrow), and MIS margin is Rs.27,079/-(highlighted in the red arrow). Do note the MIS margin amount is drastically lower compared to the NRML margin,

Clearly, since the trade is for intraday, the trader can choose MIS product type and benefit from a lower margin requirement, which is Rs.27,079/-. Do note; the trader can select NRML product type even for intraday; there is no harm doing so. But when one does this, the NRML margin amount gets blocked. If one is clear in his mind about the intraday trade, then it makes sense to opt for MIS and efficiently use the capital available.

Anyway, the trader’s total margin requirement would be –

- 48,686/- towards the ACC contract (NRML margin as the trader wishes to hold the position for 3 days)

- 27,079/- towards the Infosys contract (MIS margins as it is a pure intraday product).

- Total margin of Rs.75,765/- (48,686 + 27079)

Clearly, since the trader has Rs.80,000/- in his account, he can initiate both the trades.

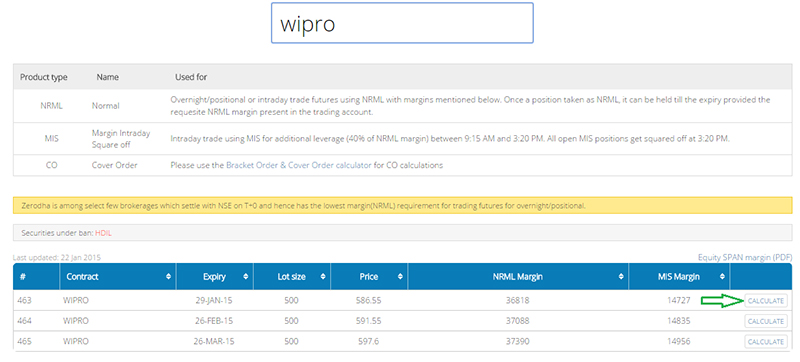

Task 2 – A trader has Rs.120,000/- in his trading account. How many lots of Wipro January Futures can he buy on an intraday basis and a multiple-day base?

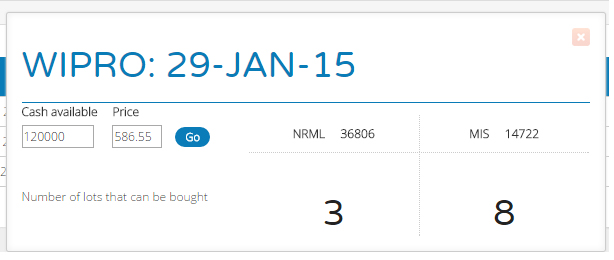

Solution – Search for Wipro in the search box provided. Next to the MIS margin column, there is an option to click on “Calculate” (highlighted in green arrow). Click on the same.

After you click on it, a form sort of window opens up; you need to enter –

- The amount of cash in your trading account (by default, this is set to Rs.100,000/- you can edit the same to meet your requirement)

- The price at which the contract is trading (in fact, this is pre-populated)

Have a look at the screenshot below –

The calculator suggests that I can trade up to 3 lots of Wipro futures under the NRML product type, considering NRML margin is Rs.36,806/- per lot. Under the MIS product type, I can trade up to 8 lots, considering the margin requirement is just Rs.14,722/- per lot.

And with that, we know all the Equity Futures section of the margin calculator’s functionalities, as easy as that. We now move over to the BO&CO calculator.

7.4 – BO&CO Margin Calculator

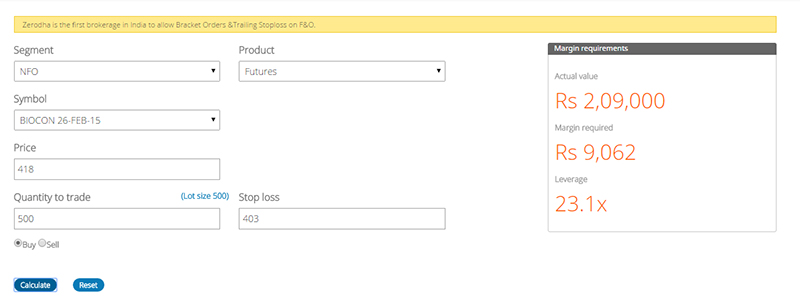

Both bracket order and cover order have similar margin requirements for reasons we discussed earlier. Using the BO&CO calculator is quite simple; it is quite similar to the SPAN calculator. In the following snapshot, I’m trying to calculate the margin requirement for Biocon Futures expiring in February 2015. Notice, I have selected everything that I need to, except for the stoploss.

Without selecting the stoploss, I proceed and press the ‘calculate’ button. When I do so, the calculator calculates the default stoploss that one can choose and the margin required. Now once I mention the stop loss, the calculator calculates the amount as shown below.

As per the BO&CO calculator, the stoploss one can choose Rs.403. Of course, you can vary the stoploss to any point, and the margins will change accordingly. Anyway, the margin required is Rs.9,062/-, which is remarkably lower compared to NRML margin of Rs.26,135/- and MIS margin of Rs.11,545.

7.5 – The trailing stoploss

Before we conclude this chapter, let us briefly discuss the ‘trailing stoploss’. The concept of trailing stoploss finds its application in bracket orders and, in general, plays a crucial role while trading. Hence I guess it is important to know how to trail your stoploss. Consider this situation (in fact, most of us would have been in this situation) – you buy a stock at Rs.250, with an expectation that the stock price will hit Rs.270 sooner or later. You keep a stoploss at Rs.240 (just in case the trade goes against you) and hope for the best.

Things move as expected; the stock rallies all the way from Rs.250 to Rs.265 (just a few Rupees away from your target of Rs.270), however thanks to market volatility, it starts to retrace back…all the way to hit your stoploss at Rs.240. So, in essence, you saw profits coming in for a brief while but were eventually forced to book a loss. How do you deal with such a situation? More often than not, we are always put in such a spot where we are right about the overall direction but get ‘stopped out’ due to market volatility.

Well, thanks to the technique of ‘trailing your stop loss, you can prevent yourself from being in this situation. In fact, at times, trailing stoploss gives you a chance of making a better profit than you originally thought about.

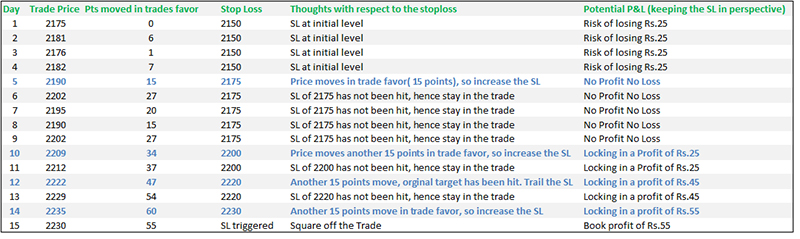

Trailing stoploss is a simple concept. All one needs to do is adjust the stoploss based on the movement in the stock. Let me illustrate this with an example. Here is a typical trade setup –

| Trade type | Long |

| Script | Infosys |

| Instrument | Futures |

| Futures Price | Rs.2175/- |

| Target | Rs.2220/- |

| Stoploss | Rs.2150/- |

| Risk | Rs.25 (2175 – 2150) |

| Reward | Rs.45 (2220 – 2175) |

Clearly, the idea is to go long at Rs.2175 and keep a stoploss at Rs.2150. The idea is to adjust the stoploss as and when the price moves in the trade direction. To be precise, for every 15 points of the price movement in the trade direction, the SL can be adjusted accordingly. The SL can be adjusted to any level with an idea of locking in the profits. When you adjust the SL intending to lock the profits, it is called “Trailing Stop Loss”. I was hoping you could note that I have randomly opted for a 15 point move in this example, but in reality, it can be any price move. Please look at the following table; as and when the price moves 15 points in the trades favour, I trail my SL and thereby lock in a certain amount of profit.

Please note that the original price target was Rs.2220, but thanks to the trailing SL technique, I can ride the momentum and close in on a higher profit.

Key takeaways from this chapter

- The more information one conveys to the RMS system in terms of trade duration and stoploss; the lesser is the margin requirement.

- Use NRML product type when you want to initiate a trade and carry it overnight.

- NRML margins are the highest (SPAN + Exposure)

- MIS is a pure intraday trade. Hence the MIS margin is lesser than the NRML margin.

- In an MIS trade, only time information is conveyed (intraday) but not the information about the stoploss

- A cover order (CO) is also an intraday product; besides, in a CO, one has to specify the stoploss

- A CO conveys both the time and the SL information. Hence margins are lesser than MIS.

- The margins for a Bracket Order (BO) is similar to a CO.

- In a BO product type, one can specify both the SL and target price at one go. Besides, one can also trail the stop loss.

- A trailing SL technique requires one to adjust the SL and when the script moves in favour of the trade.

- A trailing SL is a great way to ride the momentum in a script.

- There are no fixed trailing rules; one can choose the trailing SL based on the market situation.

Sensei, In the end you explained \”Trailing Stop Loss\” so, in your example there was a 15 point move. So does this happen automatically i.e. do you tell the system in the start to do this or do you keep tracking market regularly to do that manually?

You can set GTT for this, Sarthak.

Sir, this isn’t related to the current thread, but I have a question about algorithmic trading.

Have you covered the algo trading section, including DOM, footprint, and other advanced trading and price action terms?

If yes, could you please help me locate that option?

If not, could you please explain these concepts DOM, footprint, and other algo trading terminology in simple, layman’s terms? It would be really helpful for us.

No, we have not covered this. That said, we recently did an online session on Algo and Ai techniques for trading – https://varsitylive.zerodha.com/home

Imagine reading all of this stuff, and then heading to comments only to know that bo and co orders are no more available 😂

Aryan, my bad 🙂

At least you know that they did exist….just in case if they ever come back!

All the chapters are good but out dated stuff needs to be updated on real time basis.

second that!

Mr. Rangappa,

I request to update the content with latest changes. As it is waste of time reading outdated content which is of no use. Please please update, it will help new investers/traders.

I get your point, the idea is to explain the concept of margin and not really use this as a portal to share latest data. But as I said, point noted.

Thank you for your assistance. I am new to the market and do not have much knowledge about the regulations. 😓

Ok. But I do hope you are able to understand a bit via Varsity 🙂

Yes, of course, varsity is helping me a lot. Personally, I like it because the modules are very easily understandable, but I am still nervous about actually investing as a beginner.

Why is that Rachit? Will be happy to help 🙂

Because I think, this is new to me; therefore, it could be due to that

Sure. Happy learning 🙂

Hello Karthik, I recently used the Zerodha margin calculator but noticed that the MIS margin was missing in the equity futures tab, alongside the NRML margin calculator as shown in the image. Additionally, I couldn\’t locate the BO & CO order margin calculator. Please assist.

BO & CO orders are discontinued. Post SEBI regulations, margins are standardized now, Rachit. Its just NRML.

Bracket Orders feature is removed. Please update the article accordingly.

Noted.

Is there an option for using trailing stoploss when i am trading equities?

Try GTT – https://support.zerodha.com/category/trading-and-markets/kite-features/gtt/articles/how-can-i-use-the-gtt-feature

Is auto trail stoploss features available ?

Explain : Means auto shift of stoploss towards expecting move in pre defined steps.

If yes, how to use.

If no, which trading app has features.

Looking for response

Thanks.

Check this – https://support.zerodha.com/category/trading-and-markets/kite-features/gtt/articles/how-can-i-use-the-gtt-feature

What if the price goes below 2150 ?

Depends on what position.

Trailing stoploss contract are time limited contract or you can hold on to it for long time ?

You can keep it, check this – https://support.zerodha.com/category/trading-and-markets/kite-features/gtt/articles/how-can-i-use-the-gtt-feature

Where exactly is the trailing stoploss order in Kite? It was discontinued 5 years ago, right?

Yes, but the closest to this is a GTT, but there is no trail feature in GTT.

in trailing stoploss example table. the target is 2220 which triggered before trailing stoploss. so the trader get profit of Rs 45 only not 55. i think if target hit the stoploss is not trailed further

Thats right. The idea with a trailing stoploss is to trail it as and when market moves in the favor of the trade.

Sure thanks

Happy learning, Ayush!

Actually I am saying that is the articles written here and updated with the latest tools that we use in kite like for for example.

Kite here https://zerodha.com/margin-calculator/Commodity have two section f/o and equity futures. Which should have options for mis, nrml, bo/co. But there is no option instead.

On the other hand I can see the BO in equity. Which is spot market. I don\’t understand why is it.

Also there is other product types like amo,iceberg that are not covered here. Though I found they were pretty simple things.

I understand, taking up the task of updating the contents soon 🙂

Is this updated with latest one in kite. As I can\’t find any option for product type and leverage for f/o or equity futures.though i don\’t understand that it is there for equity spot.

Sorry, I\’m unable to get your full query. Can you elborate?

This is the best module for far. Thoroughly enjoyed it. At the end of the day, I may not become a trader but very satisfied with the knowledge earned.

The next time when someone says \”Margin Call\” in an YouTube video or an article, I can now follow along.

Glad to note that, no knowledge goes waste 🙂

Happy learning!

I\’m confused with one things.

If I first sell future contact then how many days it will hold in my portfolio? If I place order in NRML (CNC)

Futures will show up in positions and not really in the portfolio. You can hold the position for as long as you with, but at the end of the month the contract will expire.

Good afternoon sir!

When I open the equity futures calculator, I can\’t see MIS margin, it only displays NRML and NRML margin and the lot size…it doesn\’t show MIS even when I click on calculate…how to fix this

Margins are now similar, Harsh.

Okay thank you.

Do you mean to say now whatever will be my position i.e. long future short future intra day, till expiry, with stop loss, without stop loss i have to pay the same margin.

If yes, where I can read the same in detail

Check this, Anant – https://support.zerodha.com/category/trading-and-markets/margins/margin-leverage-and-product-and-order-types/articles/upfront-margin-requirements

Sir,

As per this chapter if I put normal order and MIS intraday order

then normal order requires more margin and MIS requires less margin.

But when i order from the kite app for both the orders margin requirement is showing same. Why?

The margins system went through a change, Anant. The leverage is the same across all products now.

Are these calculator updated? because i cannot find BO&CO calculation

BO&CO as a product does not exist anymore.

Great sir.. enjoyed these lessons on Futures

Happy learning! Glad you liked the content.

Thank you for the well defined lesson. I have few queries,

First, how can we put a stoploss on NRML entry for multiple days.

Second, if the next day is gap up/down and goes against trade, will the SL trigger.

Third, can we trail stop loss in NRML entry on another day.

Thank you

1) YOu can try GTT for this – https://support.zerodha.com/category/trading-and-markets/kite-features/gtt/articles/how-can-i-use-the-gtt-feature

2) No guarantee here, depends on your stop loss price

3) Nope

I had a doubt,there are different types of order are there such as CNL,NRML,CO,bo.

is brokerage is vary from order to order?, or same brokerage for all order. what is the brokerage for intraday ordrs such as Mis,Bo,Co ?

All charges explained here – https://zerodha.com/charges#tab-equities

Hi mr karthik rangappa , first of all very special thanks for An excellent series of articles. Explains the nitty gritty details about stock market in a very clear and easy to understand manner. Very seldom any site on the web have this lucid explanation. Thanks a lot for sharing this info , many traders can hope to learn a lot from here.

Thanks for the kind words, Fahad. Keep learning!

Sir,

The margin required for a particular Equity future is almost showing same when I am looking either in marketwatch/ through calculator under \”F&O\”. However, the NRML margin required is showing differently under \”Equity future\”. Why is it such?

Is it something like market watch/calculator under F&O is showing in real time data and the one under \”Equity Future\” is showing data representing the time when that particular share future was first time floated?

Please help understand.

Yeah, they will all be similar Anirban. I\’d suggest you look at the margins displayed under in the order window.

Sir,

If I would like to buy TCS futures for NRML on 27 Apr, Do I require to pay the margin according to as reflected in \”F&O\”/\”Equity shares\”.

Also, what is meant by MWPL in \”Equity shares\”?

Yes, thats right. You can even check the margin required when placing the order on your order window. MWPL = market-wide position limit, basically gives you a sense of how the activity is picking up for a particular stock from the entire market perspective.

Sir,

Suppose a stock future is floated on 01.08 for Rs. 100/- and the expiry date is 31.08. On needs to lock Rs. 2/- as margin to trade the stock future initially. On 05.08, the price of the stock future increases to Rs. 109/-. On 05.08, someone wants to trade that stock future.

I would like to know whether the person who is trying to trade the stock future on 05.08 would require to lock Rs. 2/- as margin or may require to lock a different margin as per circumstances.

It will be slightly higher as the futures price has increased.

Sir,

Under \”F&O\” , I looked for TCS futures (27 APR) where for 1 lot the initial margin required is showing Rs. 1,03,183/-.

Whereas, when I checked the same through \”Equity shares\”, NRML margin is showing as Rs. 1,04,908/- for TCS futures 27 APR. Also, price is showing here for Rs. 3246.65/- whereas, when I looked in marketwatch for TCS APR future, it is showing now as Rs. 3201.35/-. I have the below queries:

(i) Why the required initial margin is shwoing different in \”F&O\” & \”Equity shares\”?

(ii) Why the price is showing different in \”Equity shares\” & \”marketwatch\”?

(iii) What is MWPL margin showing in \”Equity shares\”?

(iv) Where can I find \”MIS/CO margin\”?

(v) Is BO or associated stoploss feature available now?

Kindly help with the above to move further.

1) The way margin is calculated for EQ and F&O is slightly different, hence the difference. Remember, these are two different segments in the exchange.

2) Eq shares is not real-time. Marketwatch is real-time.

3) MWPL = Market-wide position limit

4) The margins are capped to 5 times max. We need to update this chapter

5) This product is no longer there.

Great explanation, but shouldn\’t these chapters be updated as these are very outdated?

Its on my to-do task, Rujhan. Will start updating this soon.

Thank you for all this education, Karthik. December 2022, you have indicated that you were working on updating the pages on Margins. Any idea when these would be updated? Would be very helpful if it could be sooner than later. 🙂 Thanks again.

Its on my to do list. I had to pause for multiple reasons. Will take it up again in April, Ananth.

Sir,

For an IPO when will its derived Future be listed? Will it be from the day the stock gets listed in the secondary market or from the Last Friday morning of the listing month?

Thanks for the content.

That depends on the trading activity, Vinayaka.

sir pls update the chapter ….🙃

i searched for MIS calculators but didnt found any on the zerodha\’s website…

Yes, we have started doing that. I just finished module 1, and I am onwards to Module 2 now. I will do it sequentially.

Hi Sir,

Thanks for the efforts you have taken to educate us absolutely free with so much depth (the comments too have so much to tell). So vast and easy to understand and one is really careful to deal with money too. Thanks for this. Though the content is 7 years old but can easily relate.. Thanks a lot.

I\’m glad you found the content useful. Happy learning, Radha.

Hello @karthik Rangappa , Thank you for detailed explainations on topics. Since these topics published 6-7 years back i see some screen shots shown in this page aren\’t available, like

1. in Margin calculater we won\’t see now SPAN+exposure margin separately

2. BO,CO order types i don\’t see when i tried to buy futures

and so on

Can you please update latest available scren shot options.

Hope my suggestion is in positive way.

I will do that shortly, Jagadeesha.

I think so the screenshots used in the examples are of old app. The new interface looks different than the screenshots.

Yes, I will be updating this module soon.

Thank you for giving such nice learning about the stock market.

I see this chapter (Margin Calculator (Part 2)) needs to update with the current version of kite Zerodha plateform

Thank you once again.

Oh yes, I plan to take up the updating task as the next project 🙂

Hello, Sir

I love your explanations for futures and options that help me to understand easily what is futures and options. But today in the Margin calculator and also in Zerodha Kite if I am using NRML and also Intraday the margins are showing the same. So can you explain that why its showing like that.

This is the new margin policy set by SEBI, Ramanathan. So at best 5 times leverage is all we get.

Is this chapter valid during these days? Because there is no CO and BO available right. Also, it is the same margin required for both MIS and NRML right.

BO/CO is not valid anymore. Margin is capped at 5x for EQ now.

Bt my doubt was like first Target got triggered and then the stop loss so y didn\’t v square off our position at target

Whichever event is triggered, that order will get executed provided the price is matched.

In the last example of trailing stop loss why didn\’t the trade got squared off when original target of 2220 was hit….?? As per the rule trade gets automatically squared off either when target or stop loss is hit. Here the target got hit then why didn\’t it got squared off….??

Thats because the SL was trailed and triggered right?

So their\’s no CO and BO or their is no extra leverage?

Yes, no extra leverage.

Does zerodha still provide CO and BO … Coz I couldn\’t see their margin calculator

Nope, we dont.

How the trade is not squared off even after target is triggered or achieved in trailing S.L example given at the last?why is there a need that the trade has to be squared off only if the trailing S.L locks next 15 point value?

Franklin, sorry, dint get your query. Need more info. Can you please elaborate?

Currently in margin calculator I am not seeing

1. MIS margin in Equity futures. I am seeing only NRML margin rate

2. There is no tab called \”BO and CO\”

Currently how can these margins be calculated?

After the new margin framework, the margins are the same across all product types. Please check this – https://zerodha.com/z-connect/tradezerodha/margin-requirements/new-margin-framework-for-fo-trades

Hello sir you have mentioned about calendar spreads in the chapter 6 (margin calculator) in future trade moudule you showed how risks decreases and p&l turning zero but you didnt mention how we will start earning profit when to use calendar is there any detailed chapter ????

We have a detailed chapter on that, check this – https://zerodha.com/varsity/chapter/calendar-spreads/

In this link for Equity Futures only NRML margin and rate is shown but MIS is not shown, so is there any other link which is available which tell how much futures can be purchased with respect to NRML and MIS as explained in WIPRO example of yours

You can check for the margin required in the kite order window – https://support.zerodha.com/category/trading-and-markets/kite-web-and-mobile/holdings/articles/margins-on-kite-order-window

Hello Sir,

In the last image of the above text, I see when the \”Pts moved in trades favour\” goes to 15 from trade price of 2175 to 2190. In that case, the stop loss is increased from 2150 to 2175 (i.e, increased by 25 points). Why is that?

Based on my understanding, stop loss should also be increased by 15 points only, from 2150 to 2165.

Can you please help me in clarifying this doubt?

Shivam, this depends on the trailing stop loss (number of points), that the trader sets at the start of the trade.

Hello Sir, Im here again.. I had conversation with you in Module 2 chat section as well.

I had started studying Zerodha varsity material in last week of July-21, and completed first four modules, now heading to the module 5 Options. I have studied each page of every module in depth, infact did revision as well to get myself in good platform. I really dont know at least about the basic words in stock market before getting in Zerodha varsity…

I learning like a nursery kid in stock market, A for Apple, B for Ball like that. Its really a fun of reading this, Just giving thanks is not enough for your team great efforts. A Heartfelt Thanks Sir. Kudos to your team.

Regards

Suresh Babu

Thank you so much, Suresh! Very happy to note that you are liking the content on Varsity. Happy learning 🙂

Hi Karthik,

Any plan on updating the content like for Trailing Stop Loss, Bracket Order, screen shots which are completely changed between what was there in 2015 and how they are bit different in 2021 on Kite. Also, I am very new to futures and would you please share the URL from NSE\’s webpage which has all details around the available futures like screenshot from few chapters on this module.

Regards

Kamal

Will try and do that. Goto NSE website and click on the \’Derivatvies\’ section in the midsection of the site. You will find the info. Unfortunately, the URL does not change, hence it is not much of use to share the link.

Hi If I sell some shares and do an intraday trade on the same day using the sale proceeds of the said shares as Intra Day Margin will there be any Exchange penalties imposed as per the new Margin Rules ?, Or is it that I have to wait for the next day to do the intraday trade (after early pay in has been recorded)

No penalty as such. The only thing to note is that you should not buy back the sold shares on the day you sell.

With new margin rules , how will the futures trade be impacted?

I also have a confusion, say if I submitted a margin of 200000(required for example) to enter into long contract and if share price fall MTM loss of 15000 is adjusted and margin is now 185000, do I need to pay MTM loss of 15000 to continue my position?

I guess more people will shift to option strategies rather than naked positions. Yes, you will have to bring in additional cash to sustain the new margin.

In the above example, the target price of 2220 was reached in the 12th row. Why the trade did not get a trigger for a square off and why it continued further?

It is because of trailing the profits.

Sir,

I don\’t understand the difference between equity futures and F&O options available in zerodha margin calculator. Can you please explain?

Futures and options are two different derivative instruments, have explained this over multiple modules, suggest you read the same. Thanks.

For nrml order i can carry the position as well as the loss/profit also tilll the day of expiry or i am suppose to increase margin in case of loss. suppose in 1 kg gold i had loss of 200 points ie. 20000 at the eod. now my iniital margin NRML 4.5 lakhs stands sufficent or i have to add 20000 or the calculations would be done on the contract expiry or squaring position whichever is earlier

The margins will vary based on the movement in the underlying price, Abhishek. In this case, most likely the margins will increase slightly with the decrease in the price of the underlying.

In the trailing stop loss description / table you are showing the trade price movement across days (1 to 15). You mentioned trailing stop loss as a feature of BO type, and BO is for intraday. So the questions are:

a. Is the days illustration to be read as trade price movement points within a day

and

b. is the trailing stop loss as a feature available for NRML as well?

Poornima, BO order type is suspended for now. Its no longer available

1) Not sure if I understand this

2) You can use GTT

Is there anything like trailing target ? if not , can you introduce ? will it be useful in increasing the profits

No, you will have to trail it manually.

This is such a wealth of information for beginners like me. Thank you Mr. Karthik and team.

Happy learning, Rohini!

Hello Sir, is BO order type discontinued with Zerodha? Or where can I see it is current version?

Thats right, we have suspended BO for now.

I keep 6500 IOC shares in demat account and sell 1 lot future\’. I leave it as it is till expiry.

What will happen on expiry?

How it will be settled?

What I get back ?

You will have to give delivery of the shares by expiry.

I am new to trading. Kindly request to advise me on the confusion that I have. I understand the BO and CO are intraday features. However, I feel having trailing stop loss for CNC sell orders – Let us say using GTT mode (assuming I go long on a stock) would be great, is it available? If yes, how to do setup that. If No, what’s that I have to understand for it’s absence in CNC trading.

Prakash, GTT is a good option, but you cannot trail with GTT. I\’m sure you\’d read this, if not I\’d suggest you give this a quick read – https://zerodha.com/z-connect/tradezerodha/kite/introducing-gtt-good-till-triggered-orders

Sir when i tried using NRML and setting a stoploss then I did not see any fall in the margin(premium of the option) amount, but i did witness a change in the margin requirements when i tried using MIS and opting for CO. So why is this happening?

The idea and the mechanism should remain intact, that if RMS gets more information/clarity then margin should fall so then incase of NRML with stoploss why did the margin requirement not fall?

P.S.-am talking about Options. Sorry for asking options related doubts here!

Thanks in advance!

Thing with CO is that the SL is kind of baked into the main order itself. In NRML, you have to explicitly place the SL which you control fully, meaning you can cancel it anytime. Hence the broker cannot afford to give your better leverage with NRML.

\”the duration and the stoploss of the trade gives more clarity about your risk appetite to the RMS system.

Well, think about it – the more clarity you provide in terms of the risk you face, the higher clarity the RMS system develops. The more clarity it has, the lesser the margins required!\”

sir does this(fixing a stoploss) cause margin requirements when buying/selling CE or PE to fall?

Yes, hence the lower margins for BO/CO orders.

Hi Karthik,

Few questions

1. I think margin calculator changed over the years in zerodha, I cannot see separate margin amounts for MIS, CO and BO for futures – https://zerodha.com/margin-calculator/Futures/ and even the calculate option is present only for NRML orders. Any reason to remove for other order types?

2. As per some comments, it is not possible to convert CO/MIS orders to NRML incase trade is going against our view? Can you confirm.

1) Margins are the same for both

2) MIS to NRML and the otherway is possible, not CO to MIS.

Also, amazing that this thread is still so active though published in 2015. Itself explains the quality.

Amazing content and the way it is presented. Stared this content just 3 days back and have completed 3 module. So is the intrest it developed. I\’m already into my 30s and was not actually expecting myself to be involved so much in the writen content provided so many video materials are already availble in the market. but the content here littrally made me up for nights and complete modules.

One ques though, I started using the varsity app, but there are some major gaps in the content. Some points not covered in there. Some detail discription here. but in here, we don\’t have quiz to validate if we collected everything well. What to follow?

Happy to note that you liked the content 🙂

The content is the same in the app, its just that the app has more functionalities like tracking the progress, quiz, certificates etc. You can follow either or both actually 🙂

In the SL trailing example, for every movement of 15pt in stock, SL moved by 25pts for first 2 instance, but on 3rd instance it moved only by 20 pts and only 10 pts on 4 instance. How did this happened. From where did the system get this adjustable information or is it mannual?

That a manual SL trail 🙂

Sir ,

I want to carry for forward reliance futures,say I bought nov expiry at 2034 @ 505 qty .The margin required is 2.58 Lakhs as per zerodha and I have 2.6 lakhs as fund balanace.Suppose reliance falls by 5 % , 10% etc,What will be impact on my portfolio ??Till what amount of loss ,I do not need to add funds to my zerodha account . Any chances of auto square off my position ?

With the fall, there will be marked to market loss, which will be adjusted from margins, and hence you will fall short or margin, which you will have to make good, if you wish to carry forward the position. The loss is the lot size * the number of points RIL has moved against you.

Hii sir,

Sir, I know, you have already said that there is not set rules for trailing stoploss. So, Obviously i will not ask this one..😊

But Sir, How do you use this technique. I mean, what your startegy towards trailing stoploss.

I am sure that technique will be so helpful for me…😊😊

THANKUUU!

I trail it based on the strength of the underlying\’s price movement. If there is a lot of momentum, I trail it aggressively, else take it as it goes 🙂

Hi Sir,

First of all thank you for the amazing educational content that you have published here. Truly blessed to have this.

My query is, in case of Trailing SL, how does the Target changes. For eg: in your eg: Infosys Fut Target of 2220 was already reached. So doesn\’t the system sq off the position? How to increase the target. Sorry if my question is stupid. I am new to investing and learning the concepts. Thanks in advance.

Sumit, you keep increasing the target as and when the price moves in your direction. There is no set rules to manage this, you will have to use your discretion and trail accordingly.

Thank you for the valueable information.

In BO table target reached on the day 12 (2220/-) then how it\’s continued next few days till SL is triggered.

Can you please elaborate

I m bit confused.

BO orders are intraday orders, Yuvraj, just like MIS and CO orders.

Sir, in the above situation the Target was already @2220, so while traling the stoploss the target set becomes invalid?

Target remains intact, the Sl moves in the direction of the trade along with the underlying. Hence this is called \’trailing\’ SL, where the SL trails the underlying towards the target.

Sir

If I am option buyer ,my premium value debit is already blocked and my option loosing value,then why margin requirements of zerodha increases as expiry date comes nearby?

This is due to the physical delivery obligation, do check this – https://zerodha.com/varsity/chapter/quick-note-on-physical-settlement-2/

Respected Sir,

I, new to trading, but due to poor knowledge, I cannot understanding few things, I be thankful, if you guide me.

Q 1) I am doing bank nifty – CE and PE. Whether it is futures or options? [Not related to equity]

Q 2) Whether I get margin amount from zerodha or I have to trade every time with my own cash?

Q 3) If i get, then how much?

Truly

S Pavan

1) CE and PE is options, not futures

2) Any derivative is leveraged, hence you get the margins

3) Depends on the instrument. Do check this – https://zerodha.com/margin-calculator/SPAN/https://zerodha.com/margin-calculator/SPAN/

Thank you!

Hi Karthik,

Before asking my doubt, I would like to appreciate and thank you a zillion times for all your efforts to put things across in such a simple manner. You are simply a rockstar.

Moving onto my doubt, I would like to know how the trailing works in BO. In the example given above, you opted for 15 points. On day 1 when the trade price was 2175, the SL was 2150 i.e 25 points behind. When the price moved to 2190 on day 5, the SL moved to 2175, according to my understanding it should have moved to 2165 (2150+15) instead of 2175?

Also, on day 10 when the price moved to 2209 i.e. 34 points above the initial price, the SL should have moved to 2190 (2175+15) instead of 2200?

Please help me understand this.

Thank you for all your hard work.

Thanks for the kind words, Harsh 🙂

You need to stick to the minimum SL levels when placing a BO. Have a look at this – https://support.zerodha.com/category/trading-and-markets/margin-leverage-and-product-and-order-types/articles/minimum-trailing-stoploss, this will give you a perspective.

In trailing stop loss example… if trade goes 15 points in my favour, shouldn\’t stop loss move by 15 instead of 25?

Also why will trade not get square off at initial target?

Thanks sir ,

I really appreciate the kind of value and response you provide in varsity

Sir as this was written on 2015 Hopeing sir

now in the margin calculator We Cant Find

(MIS,BO,CO)

Can You Please help me sir!

Check this Kiran – https://zerodha.com/marketintel/bulletin/249809/latest-intraday-leverages-mis-bo-co

Thanks, could you also help me in interpreting the margins given there. E.g. for Stock F&O the margin is given as

3.33x(30% of NRML margins) so how much will be that??

Check this Ayush – https://zerodha.com/margin-calculator/SPAN/

HI,

This is a brilliant article.

But I couldn\’t find MIS or BO&CO calculator in the Margin Calculator.

Could you point me to where I can find those?

Check this, Ayush – https://zerodha.com/marketintel/bulletin/249809/latest-intraday-leverages-mis-bo-co

Sir, there is no MIS margin given for the equity futures and what does MWPL means?

MIS is available. MWPL = Market wide position limit.

Learning Document is quite old and contains lot of errors( Like calculation mistakes in the table ) . since zerodha is doing quite a good job and company is growing day to day so please update the beginners document also.

Can you please point to the mistakes?

Sir, If I have rs 110,000 and want to write 2 lots of nifty 9700CE Intraday, margin blocked would be rs 82,856mas per span calculator. Now I will have rs 17,144 left. I want to also write 9000PE which will give me a significant margin benefit. Will zerodha allow me to write the 9000pe because after the margin, the total cost for intraday will be 108,000. What will happen in this case?

You can use the margin calculator for this, Ron – https://zerodha.com/margin-calculator/SPAN/

Good evening Karthikji

SEBI circular on hedged margin r said to be effective from May 1st. Is it true news or postponed ? If so my question is

1)How to execute that trade? Suppose In Nifty Sell 9300 & Nifty buy 9200 bull call spread…. which one to execute 1st to avail of margin benefits? Or will zerodha apps design strategy to execute it directly

2)To what extent margin r expected to fall ?

This is yet to come effective. No formal announcements on it yet.

Thanks sir , i really appreciate the kind of value and response you provide in varsity … this encourages me to invest …

Happy reading 🙂

Thanks sir,

So, in BO the stop-loss (trailing) acts as a trigger rather than a stop-loss limit? correct me if I am wrong.

Yes, do check this for more details – https://support.zerodha.com/category/trading-and-markets/margin-leverage-and-product-and-order-types/articles/what-are-bracket-orders-and-how-to-use-them

question continued..

Is Stoploss placed is a SL or SL-M ?

thanks for your answer in advance sir.

It can be either SL or SL-M.

Hi Karthik, is there any product which allows stoploss and target price setting in an order which is not intra-day. Basically BO/CO without intraday facility.

Yes, you can use the GTT order – https://zerodha.com/z-connect/tradezerodha/kite/introducing-gtt-good-till-triggered-orders

Hello,

Thanks for detailed explanation , but one question ?

In the infosys example, when the target was hit (2220) why the order was not execute ? does it mean the the price was not 2220 and it was 2222 ?

what if the SL 2230 was not hit and the price went down further without hitting 2230 ? like 2220 ..

This was a trailing SL right?

Do we get margin while buying call and put options also?

Or do we get only while selling call and put options and for futures only?

I tried with margin calculator to check margin for call and put but did not get anything on calculator when I said BUY for call and put

Kindly let me know

You don\’t need margins for buying options, you just need the premium amount. Yes, while selling options you need to have margins.

Sir,

In MIS orders i.e. Margin Intraday Square Off, what is the significance of the word MARGIN ?

Thanks

Margin implies you are leveraging your trade.

How to define SL and Target sir in NRML Mode ?

The same way you\’d for MIS mode, except that you\’d be looking at EOD charts instead of intraday charts.

Sir

Can we buy and sell futures in current mid and far month as nrml and define stop loss and targets as well? Or it is possible only with MIS?. If possible how do we do it?.

You can buy the current/mid/far month contracts in NRML mode. To do this, select NRML as the product code.

concept of margin is confusing ? do we pay for the rest of the amount if we make any loss

Hmm, the margin is the initial amount you pay at the time of entering the position. Your settlement is via mark to market.

I was talking about this only. Where\’s MIS margin calculator I am unable to find it.

Ah, I think MIS is no longer available. However, MIS margin is roughly about 45% of NRML margin for stocks and about 35% of NRML for indices.

while using NRML, why am i not able to use BO or CO?

BO/CO are intraday order types, you cannot take the position forward. However, NRML is used for overnight positions, hence no BO/CO.

equity futures in margin calculator is only showing normal margin requirement, its not showing mis margin? where can find it?

Check this – https://zerodha.com/margin-calculator/Futures/

Dear Karthikji,

There\’s fuss that SEBI may lower margin requirement for F&O trading only on hedged position. Although my question is is of assumption nature, not to be contrued as advice & only ur opinion is needed.

My question is- Suppose we\’ve Rs 1.5 lakh amount for trade. Now considering Nifty Futs (NRML) at round fig of Rs 1 lakh & selling Nifty call options 100 pt above spot. Assuming overall cost of 2 legs trade at Rs 1.20(NRML) lakhs approx. Suppose if margin requirement falls 40% also, then cost of these two trades r at Rs 70k approx. And we\’ve balance margin of Rs 80k. Hope u r clear upto here.

Bt my biggest doubt here is that how we\’ll take another trade of Nifty Futs to make use of remaining balance ?? B\’coz if we\’ll place another Nifty Futs first THEN ZERODHA SOFTWARE SYSTEM WILL RECOGNISE IT AS NAKED TRADE & NOT HEDGE ONE. And it\’ll show insufficient margin. How to tackle this problem & make best use of margin if new margin methods come into force ?? Or will there be any software modifications.

Kindly elaborate in details & thanking for giving your patient time! 🙂

Harsh, I get your point. Firstly we need to wait for SEBI to clarify this and to figure to what extent the margins will drop for hedged positions. Assuming so, you will not be in a position to take a full Nifty fut for 70K. Btw, your margins will reduce if you buy Fut + Buy Put, no need to sell call.

SEBI new rule margin calculator is update or not yet

Not yet, I suppose. But will happen soon.

Hi,

I am trying to calculate margin requirement for shorting Bank Nifty option under BO. In SPAN calculator, we do not have option for stop loss for options. Could you tell the margin requirement for this sample trade?

Ex: I would like to short 30100PE at 80 with spot at 30230 and stop loss at 102. What would be margin required.

The SPAN margin calculator does not consider the SL.

Good morning Karthikji

3rd point of above mentioned questions u gave positive answer in which sense ??. I mean is trailing SL automatically moves up as points move in our favour? ?

Sry again pls

Yes, thats right.

Good morning Karthikji

I\’ve never done intraday trade but mostly F&O esp options selling or Nifty Futs. I\’m looking forward to intraday now especially in Nifty & some of its stable stocks like Reliance, TCS etc & BO seems quite enticing bt don\’t know how to use. I\’ve FEW QUERY regarding this…

1)In Kite BO section is target, Fixed SL & Trailing stoploss r only in number form or stocks/index price form??

2)If it\’s number then say Nifty at 11000 then I\’ll set like this

Target= 70

Fixed SL= 30

Trailing SL= 10

Am I right to fill desired way?

3)from (2), suppose I don\’t want to modify once trailing SL is set. So is trailing SL then automatically moves up on every 10 points Nifty move or we\’ve to manually adjust it every 10 pts ??

4) Upto how much percentage( 5%,10%,20%..) can BO allows to keep SL. Suppose Reliance at 1300. Then can we at least set SL based on its daily Volatility number ??

5)If system automatically square off at 3.20PM then will there be extra hefty cost ??

Kindly thoroughly see my 3rd questions especially. Need ur opinion Sir

Thanking you for giving ur valuable time 🙂

1) Number of ticks, check this – https://zerodha.com/z-connect/tradezerodha/zerodha-trader-software-version/bracket-orders-trailing-stoploss-sl

2) Check the above link. Make sure you go through the comments as well. Check this as well – https://support.zerodha.com/category/trading-and-markets/margin-leverage-and-product-and-order-types/articles/what-are-bracket-orders-and-how-to-use-them

3) Yup

5) Not really, but if the order gets executed in mutiple chunks, then its 20/- per order

Very nice tutorials.

I had some confusion on the trailing stoploss section here. I understood the chart until day 10. But after day 10, I am a bit loss on how stoploss moves and why the interval changes from 25 to 20 and then to 10. Is the booking of profit auto generated by the system? Would appreciate if you can clarify further on this. Thanks

Its not auto-generated, Jitendra. You will have to keep a track and move the SL accordingly. You can increase the SL level if you feel the volatility is picking up or reduce if the volatility or momentum is not picking up.

Dear Sir,

I am a great fan of your teaching, very simple and engaging.

Thanks for the wonderful session.

Makarand

Happy learning, Makarand.

Hello Karthik, i am new to trade and learning things and following your post.. i need you to guide me on this topic

how to make my amo order successfull. Previously i tried but didnt execute. how amo order works and what type of order should i place. MKT or LMT or SL … any material to learn about this..What is the percentage of getting amo order successfully executed.

Market AMO orders are more likely to execute during the pre-open as long as there are buyers/sellers in the scrip you are trading. Limit AMOs will get completed based on the price you have placed it at.

This article on the Support Portal has more details.

Hi,

Zerodha is charging Call and Trade Charges for BO/CO. Is Call & Trade Charges will be charged if I place MIS orders for Intraday.

Please confirm.

Thanks.

The Call and Trade Charges are applicable when you call the support desk to close a position or when you don\’t close an MIS/BO/CO position and we will have to do it on your behalf.

Hello Karthick,

1.How do I post a screenshot in this post , I have tried using the Print screen option but doesn\’t get pasted here .

The query is about Trailing stop loss from Intraday Perspective

2. In the New Kite version I can see Stop loss , Target , Trailing stop loss , I understand Stop-loss can be mentioned with regards to my risk appetite but Target and Trailing stop loss is something is I always miss on It .

Let me explain my scenario with an example

I buy a long position with EMA and expect the stock price to move up and it does move up after a EMA cross over and I wait for some time to sell it off at a point when it reaches to the top but I understand no can determine the peak position and it starts going down after it has achieved its peak .

a)How do I determine the \” target\” for any position that I create long/short

b) how do I implement the Target in the kite platform . Is it just putting the Intended price I can expect it to touch

c) what value should I put in \”Trailing stop loss\”, am Little confused in that part . Can you please explain me in detail on this .

Thankyou in Advance.

1) You can upload this on Google Drive and share the link

2a) This is a tough ask ;). I usually look at the immediate resistance for placing targets for long positions.

2b) You can choose SL limit to sell at the target price and book your profits. Alternatively, you can use a bracket order.

2c) This depends on how you want to trail. If I\’m trading Nifty intraday, I\’d trail by 10-15 points everytime the index moves in my favor.

In response to your Responses to your previous mail,

2a) How about for Short Position , Is there any logic or is it when it starts retracing back I buy back the stock at any given point

. Your suggestions please

2b) In Bracket Order how would I mention the Target without knowing how much peak/Bottom it can go . Is it necessary to mention that value ?

2c) what would be your suggestion for Individual stocks,what is the ideal price points I should keep as trailing stop loss

Thankyou in advance

In response to your Responses to your previous mail,

2a) How about for Short Position , Is there any logic or is it when it starts retracing back I buy back the stock at any given point

. Your suggestions please

2b) In Bracket Order how would I mention the Target without knowing how much peak/Bottom it can go . Is it necessary to mention that value ?

2c) what would be your suggestion for Individual stocks,what is the ideal price points I should keep as trailing stop loss

Also you had mentioned about a WhatsApp group that you have . Is that for sharing updates or what\’s it for . Can I also join if yes what\’s number to join.

Thankyou in advance

Sorry, I don\’t have any whatsapp group 🙂

Must be a wrong information.

2a) For short positions you can look at the immediate support as the target price. You can even trail the position by locking in certain points

2b) No one can really call the top and bottom in the market, so your guess is as good as mine 🙂

2c) Think of it in % terms. For intraday, maybe lock in every quarter percent move?

when there is margin shortfall for short options there is margin penalty. Does that means that if someone is ready to pay margin penlaty then he can take the position from less then sufficient margin and pay margin penalty.

When you are short of margins, you either need to add more funds to satisfy the margin requirements or close the position. You cannot carry forward the position with less margins.

There are many times when after taking position my margin available became negative for one or two days but my position had been carryforward and I paid certain margin penalty.thanks

I am using kite api for trading. Is there a formula or documentation for zerodha margin calculator, so that my algo can properly manage risk before placing option spread orders. I tried kite forum sir but got reply that it is out of scope for them. Can you guide me sir?

Mani, I\’m not the right person for this. Its best to check with the tech guys on the forum 🙂

By the way, have you seen this – https://kite.trade/docs/connect/v3/ ?

I have sir. I am trying to calculate margin requirement for hedged positions sir, It seems there is no api available for the same. Is there a documentation or website about SPAN and exposure margin math? so that I can calculate it from my end

Mani, SPAN is a licensed product from CBOE. Check this – http://www.cboe.com/trading-tools/calculators/margin-calculator

yes sir, I found that too. Guess I have to make do with what ever is available

Enjoying these classes on futures! Kudos to the entire team for your exceptional work.

If you had written a book , you would mint money, unlike other garbage books out there which confuses the reader with heavyweight jargons , your articulations are much better than most of the books I wasted my time on!

Hey Bharath, that\’s very big of you to say that 🙂

The idea with Varsity is to educate everyone with an intent to learn about markets, for free. We will strive hard to keep it that way 🙂

Hi Karthik,

I have a query regarding the BO orders. Is it possible to place a trailing stop loss (BO) on an open long option position?

Let say i have an open CE position for Auro Pharma expiring on 25th Oct, can i place a BO order to set a trailing stop loss on this position ?

Thanks.

Dan, BO has the trailing feature, but these are day orders, you cannot carry forward the position overnight.

does increase in implide volatilty figure displayed on nse option chain increase or decrease the margin required for shorting options as the case may be .

Also while trading in same day i see margin available and margin used constantly changing for nrml positions and also change by substantial amount so how this work does margin change happen end of the day or constanlty.

Increase in IV increases the margin requirement to take an F&O position as the price risk for the contract has increased.

The margin used/available keeps updating based on the marked to market losses/profit constantly. This way you are informed if your account balance is in negative and you\’d need to add funds to continue holding on to your position.

Recently I was planning on opening an account in zerodha. So I did my due diligence and i find out from quora and twitter that there\’s been a lot of technical glitches going on the zerodha\’s trading platform. And people are losing tons of money because of it. So I\’m rethinking my position about opening an account in zerodha.

Pranab, we have over a million customers, of which very few make a big deal of small issues online. Please do check our ratings on Google and also playstore. I\’d suggest you experience Zerodha and build your own opinion.

What is the span and exposure margin in case of mis trade as you have mentioned that mis margin is usually very less w.r.t nrml margin

Margins have actually increased now, check this – https://support.zerodha.com/category/trading-and-markets/trading-faqs/articles/what-is-asm

Suppose i have short option position on expiry day say 2lakh and the option expire worthless and i did not square off position , will my blocked margin would release on same expiry day only and would i be able to withdraw that amount on same evening or not

Hi Karthik,

Can you please share your inputs on the below?

1. Can intraday buy first – sell next positions on equity shares (spot market) be converted to long ( to hold for more than a day)

2. Can intra day sell first – buy next position on equity shares (sport market) be converted to long?

3. Can intraday buy first – sell next positions on equity futures be converted to long ( to hold for more than a day)

4. Can intra day sell first – buy next position on equity futures be converted to long?

I’m thinking the answers are yes, no, yes, yes. Am I right?

Kind regards,

Guru

1. Yes, you can buy in MIS and convert it to CNC to receive delivery of the shares.

2. No, you cannot convert an MIS short position. We cannot allow this as it leads to short delivery.

3 & 4. Yes, you can take both long and short positions in futures(both intraday and carry forward) and hold it till expiry. This chapter explains all your queries on this topic 🙂

Thanks Faisal. Have a good weekend ?

does zerodha has screener?

Smallcase has, check https://screener.smallcase.com/

No Margins for Avenue Supermarket ltd? Why? FnO, Equity, nothing why?? even all technical indicator are in favor. bullish trend.

1. DMart isn\’t an F&O trading stock.

2. We provide 3X leverage for Intraday Equity(The same information is available in our Margin calculator).

Chanu, I\’d request you to check the Support Portal before posting here. All your queries are already answered there

for example, if I want to place an order and having 50k in my Zerodha ac, can u tell me possible scenario placing an order as :

F&O / Equity futures / Equity / BO & CO

Please Took Bank of Baroda As share purchased at opening 149 sold at 152 highest o day 30-7-18. Please include margin in possible order.

Thank you

Request you to please use this friendly calculator for this – https://zerodha.com/margin-calculator/Futures/

Thanks a lot for this. Getting confident chapter by chapter 🙂

Good luck, Arun!

Hi

Just wanted a clarity on Nifty IT.

In order to buy one lot of Nifty IT under Bo Co order, the exact premium shows as infinity, any particular reason for this ?

Can any light be thrown as to how much funds are required to buy one lot of nifty IT under Bo Co ?

Nifty IT index is not tradable, Uday.

Can you tell if the information filled in the RMS system is visible to others. I am asking because if the people who have the money like fund mangers etc can manager the trade and put the small retail trades out as the many times yhe stoploss will get hit and we will slowly lose out on many trade.

No, there is no way anyone else would have access to this information.

Dear sir, would like to know why the leaverage has been reduced from 56.5x to 33.3x for BO and CO ? 🙁 🙁

Which stock are you talking about, Daniel?

It is regarding the BO and CO margin calculator. When I had a glimpse few months back 56.5x leverage was give to a stoploss less that 1.5% but right now its showing only 33.3x 🙁

Well, if you ask me, 33.3x is more than the required amount of leverage 🙂

Thank you for reverting sir 🙂

Good luck, Daniel!

now you reduce 33x to 25x

Which scrip?

Hello Karthik Rangappa

If I place a BO order to buy 100 share and its got executed in to 6 order, does that mean Brokerage will charged for 6 order.

I heard In BO/CO it will be charged on every order executed, in the above case 6 SL order and 6 target order, so total 12 is this right?

please clarify this point. I am confused about the brokerage charge completly.

Rajendra, you will be charged only once for the buy(entry) order, i.e., 0.01% of order value or max ₹20.

However, for the sell, since 6 orders will get executed, you will be charged 6 times(0.01% of order value or max ₹20). 12 orders will placed(SL and Target) but only 6 will be executed and you will be charged only for the executed ones

Sir

What is difference between future and equity future.

Futures and equity futures are used interchangeably. They both essentially mean the same.

Thank you sir!

Hi Karthik,

In Trailing SL example, why is SL increasing by 25 points for every 15 point movement in price? Why is this 25 points each time?

Thanks for your great work!

Well, you can set the trail to whichever value you desire. 25 was used in this example.

Got it. Thanks!

Cheers!

For trailing stoploss example I think stoploss and target was set manually for every 15 points desired move (help me here if I am wrong) cause in BO points and trailing SL move together i.e. If we put 1 trailing stoploss the stoploss will move 1 point for same

point movement in our direction.

Yes, at least, in this example, it was a manual trail.

Thanks!

A quick question on the margin calculator.

While shorting index options, do I Need the actual total margin or the total margin minus the premium receivable ?

Here is an example

Nifty 9000CE 28 March 2018

Span

Rs: 1,29,623

Exposure margin

Rs: 23,425

Premium receivable ?

Rs: 1,06,148

Total margin ?

Rs: 1,53,047

What will be the amount required in my account for shorting 1 lot and what will be required amount of I were to subsequently short a second lot after shorting the first lot both as separate orders.

You will require the Total Margin to take the position. Premium receivable is only credited to your Account on T+1 Day.

The same margin requirements will be applicable for the second lot too

So if I place the second order on the next day.. I just need the balance amount of the total margin minus the premium receivable from the first left? Is my understanding correct? Also Will I be able to withdraw the premium received after it is received?

That is correct, the premium is added as free cash to your account and can be used to take trades or withdraw on T+1 Day. However, the margin will remain blocked for the position.

there is no bracket order for swing trades?

No, bracket and cover orders are intraday product types.

Hello sir,

I have only do intraday in equity, not for future and option.

I have some query on margin/leverage provided by zerodha in equity intraday.

If i have only 50000 in my account and zerodha give margin up to 5 times in intraday. Then i have now purchase share of total 250000 rupees. Suppose value of stock is 100 rs. Then i bought 2500 shares for intraday.

Now suppose that day stock value decrease and down 50 rs. Than total loss is 2500 *50 = 125000 . Now actually i have only 50000 rs. So my maximum loss can be up to 50000. Now who will be pay other 75000 loss? Can zerodha call me for deposit other 75000 rs.?

No, any trade that goes below the margins required will be closed by the risk management team.

So you say that order squared off automatically, right?

Then which time that can be square off?

Is there any loss percentage are there to be triggerd?

What is maximum loss from my side?

The moment the order gets below the stipulated margins, then order gets squared off. Else, if its an intraday trade, it would be squared off by 3:20 (in case you do not initiate the sq off yourself).

Hey Karthik ,

The margin for MIS Nifty Futures is mentioned as 40%. So does it mean if I have money for 10 lots of Nifty future index, in intra day I can buy 14 lots (40% more)?

Please tell me how many nifty 50 index future lots I can buy in intra day if I have the money to buy 1 lot in positional? Like how many time more can I buy.

Cheers.

Please check this – https://zerodha.com/margin-calculator/SPAN/

Can\’t find for intra day. MIS Margin for Nifty index futures?

Look under the product type.

I am not sure if you understand or if I am missing something here. I think if I select Futures under Product and Nifty Futures, it gets added in the grid, but just says the normal margin required, not the MIS margin. Usually I think with normal margin, I can trade 3 -11 times in other instruments. I want to know how many times I can trade in Nifty futures intraday?

Say you have 2L as cash in your account – assuming 60K as NRML margins, you can trade upto 3 lots. I can buy and sell three lots of Nifty as many times as I want on a particular day. No restriction on this.

Thank you sir for your timely response.

Cheers!

Hi sir,

As u said stoploss order\’s are only for intraday(derivatives and non derivatives)

my question is how to place a stoploss order for non-delivery,what ever the product type may be(derivatives or non derivatives)

Thanks in advance.

You can place the stoploss across any segment. However, you cannot carry forward the stoploss order overnight.

Thank you sir,

In that case how to deal with the overnight risk in the market\’s???

Let\’s assume this way

I placed a stoploss for xyz share today which I can\’t Carry forward to tomorrow,and as the market\’s open tomorrow let say that stock opened with lower circuit??

In that case how to protect my capital?

2)sir can u plz say what is reason behind that not to carry stoploss for delivery trades.

3)does all brokers in India only allow stoploss for one day or it varies from broker to broker.

Kindly answer my questions.

Thanks in advance sir.

The overnight risk is perhaps one of the biggest risks a positional trader carries. This is a standard practice amongst brokers.

Thank-you sir,

As I go through the module and comments I have been stucked with few more questions???

1)If we have to place a stoploss on day to day basis than do we have to pay the brokerage for that on day to day basis even if we don\’t exit from the script?

2)in MIS,BO&CO can I change the stoploss or target price multiple no of times accordingly,for doing so is there any Levy on me.

Thanks in advance.

1) No as brokerage is charged only on executed orders.

2) No charges for order modification.

Hey Karthik. Great Explanation as always. Thankyou 🙂 . I had a few questions if you could please address :

1 Whats the point of having Span Margin Section in Zerodha, one can calculate the margin easily using the Equity Futures section. Is there any extra feature in Span Margin that I am

missing out .

2 These margins for future contracts are decieded by NSE or it varies from broker to broker.

3 What does Zerodha nd Other Brokers normally do , when the margin balance falls below the maintaince margin during the market time. Do they square It off or call the client or what ?

4 Also in a case like Satyam , when the share & future value fell 70/80% on a single day. Say I was long on Satyam through futures, and I am unaware abt the falling future price of it ,