You need 10+ years if you pay just the minimum due on credit cards!

India is adapting to the culture of credit cards at a staggering pace. While credit cards may seem like a means to financial freedom and accessibility, in many cases, they can be dangerous for your financial health.

My cousin, for instance, is an IT professional living in Bangalore who enjoys a comfortable lifestyle. He has a stable job and a good salary. He often travels and dines out. Last year, to support his lifestyle, he applied for a credit card.

Initially, he used it for small purchases but gradually began charging larger expenses to it, including vacations, electronics, and home improvements—common habits for many credit card holders.

As his expenses grew, like many others, he tried the minimum payment option. He loved it because it didn’t add immediate financial strain. He kept paying the minimum amount due, believing this strategy was practical since it allowed him to allocate his income to other areas.

A year into using his credit card, however, he noticed that despite regular payments, his debt hadn’t decreased. His outstanding balance ballooned due to high interest rates. He then realized he was only paying off the interest component to a large extent and barely touching the principal amount.

So, what really happens when you pay only the minimum amount due?

When you apply for a credit card, you are generally given a 30-day window to utilize its benefits. This 30-day window is also called the billing cycle. Let’s say you applied for the credit card and received it on the 1st of April. In this case, your billing cycle would be from the 1st of April to the 30th of April. In every billing cycle, all transactions made during that 30-day period are recorded, and a statement is generated.

This statement indicates the amount you owe and the due date by which you need to make the payment. The due date is generally 20-25 days from the issue date of the statement, and the period between the statement generated and the due date is also called the ‘grace period’. Considering the above scenario, the due date here would be the 25th of May.

If you make the full payment within that grace period, there are no consequences, and your credit score remains healthy. This is the ideal practice.

However, if you pay just the minimum amount due, which in most instances is 5% of your total outstanding amount, you may avoid late payment charges. Still, the remaining unpaid amount will start attracting interest, which can go up to 42% per annum. To remind you, if you have a good credit score, a personal loan will be available to you at 11% – 18% per annum.

Not just the unpaid balance, all future spending on the credit card also starts attracting interest.

Let me explain this to you with an example:

Assume you have just received a new credit card with a credit limit of ₹1 lakh. The card has an annual interest rate of 36%, which translates to a monthly interest rate of 3%. You start using the card for various expenses, and by the end of the first billing cycle, you have spent ₹50,000 on your credit card.

- Billing Cycle: 30 days

- Statement Date: 30th of the month

- Due Date: 20 days from the statement date (20th of the next month)

On the First Billing Cycle:

- The Outstanding Balance is ₹50,000

- Let’s assume the minimum payment due is 5% of the outstanding balance, i.e., ₹2,500

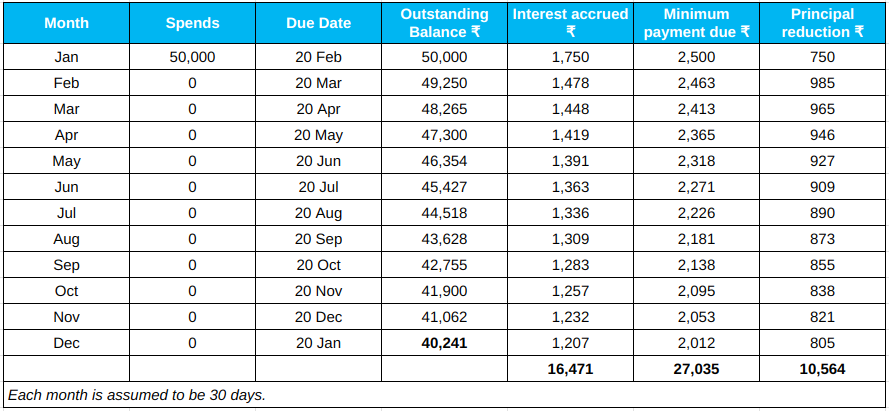

Here’s how the accrued interest and balance would look at the end of each month if you only paid the minimum amount due –

Do note that Interest calculation starts from the day an expense was made. For simplicity, all spends are assumed to be in the middle of the month. Therefore, the accrued interest of 1750 in the first row is for 35 days (from 15 Jan to 20 Feb).

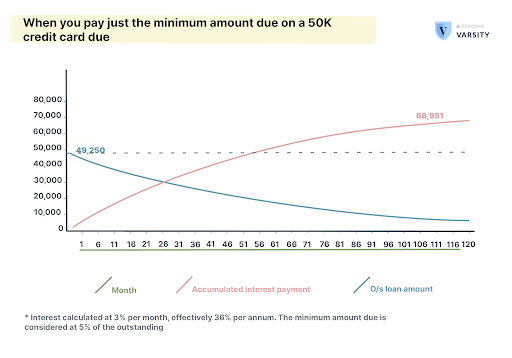

As you can see, after 12 months, your principal amount has come down by just ₹10,000 when you had paid about ₹27,000 in the form of minimum dues. If you continue like this, you might need over a decade to fully pay off your dues, and you will have spent huge amounts as interest in the meantime. In fact, if you made any more spends before paying off the dues, the new spends will attract 3% monthly interest from the very day when they were made.

Paying only the minimum amount due each month keeps you in a prolonged cycle of debt and accrues high interest costs. Moreover, because of the higher balance outstanding and future credit card transactions, you will be utilizing a larger portion of your total available credit limit. This can impact your credit score. I have explained how credit score works in an earlier post.

To sum it up, avoid making just the minimum due payments to avoid financial stress. Instead, budget well so you never fall into such debt traps.

Borrow mindfully!