What is a credit score, and why is it important for you?

As soon as you get your first credit card or open a bank account, you start hearing people preach about credit scores. And, if you have chosen to be blissfully unaware, here’s a simple explanation.

A credit score is a three-digit number between 300 and 900 that defines your creditworthiness; the lower levels reflect low, and higher levels reflect higher. Just like good grades open new opportunities to get into better schools and colleges, a higher credit score opens avenues for you to avail of loans at better terms.

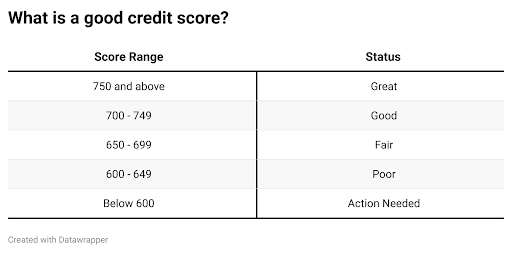

According to CIBIL, the Credit Information Bureau India Limited, an ideal credit score exceeds 750. This benchmark is significant because data from CIBIL indicates that 79% of loans are approved for individuals with scores over 750. Banks use this score to assess your loan repayment capacity, and it is good to maintain or increase this threshold if you want easy access to loans. Here is a table summarising the credit score ranges and their implications.

From the above table, if you’ve noticed your credit score does not meet the desired standards, you must be neglecting some important bits of your financial behaviour. Firstly, make sure there is no imbalance in your debt-to-income ratio; simply put – just keep your debt, such as any mortgages, loans, credit card bills, and so on, to less than 50% of your income.

Your payment history greatly impacts your credit score and financial behaviour; make sure to repay your loans and EMIs on time; defaulting on your payments can affect your credit score by several points.

Do not exceed your credit utilization ratio; it is nothing but the proportion of overall credit available to you. Ideally, you shouldn’t exceed more than 30-40% of your credit limit. Apart from this, if you have been applying for multiple loans and credit cards simultaneously, banks could consider this a red flag and question your ability to repay heavy debt.

So, what can you do to improve your credit score?

It is human nature not to heed technicalities sometimes; keep a calendar reminder or whatever, but make sure to track your credit score. Not very often, but the credit report does show wrong scores; although you have paid your loans timely, ensure you track this and rectify any errors.

Ensure you do not default in making any repayments; this is the holy grail if you want to demonstrate yourself as a responsible and creditworthy individual. Banks rely highly on this as a criterion when deciding whether to sanction a loan and at what interest rate.

Another way to improve your credit score would be to go for long-term loans; the longer the repayment period, the lower the instalments, and it is easier for you to make timely payments.

The core idea is when you begin to focus on your finances, understanding things like your credit score and planning for the future can help you succeed in the long run. So, stay informed and happy investing 🙂