It’s the economy, stupid! FX reserves are falling, but why?

We love IndiaDataHub’s weekly newsletter, ‘This Week in Data’, which neatly wraps up all major macro data stories for the week. We love it so much, in fact, that we’ve taken it upon ourselves to create a simple, digestible version of their newsletter for those of you that don’t like econ-speak. Think of us as a cover band, reproducing their ideas in our own style. Attribute all insights, here, to IndiaDataHub. All mistakes, of course, are our own.

Prefer watching over reading? Here’s the video for you!

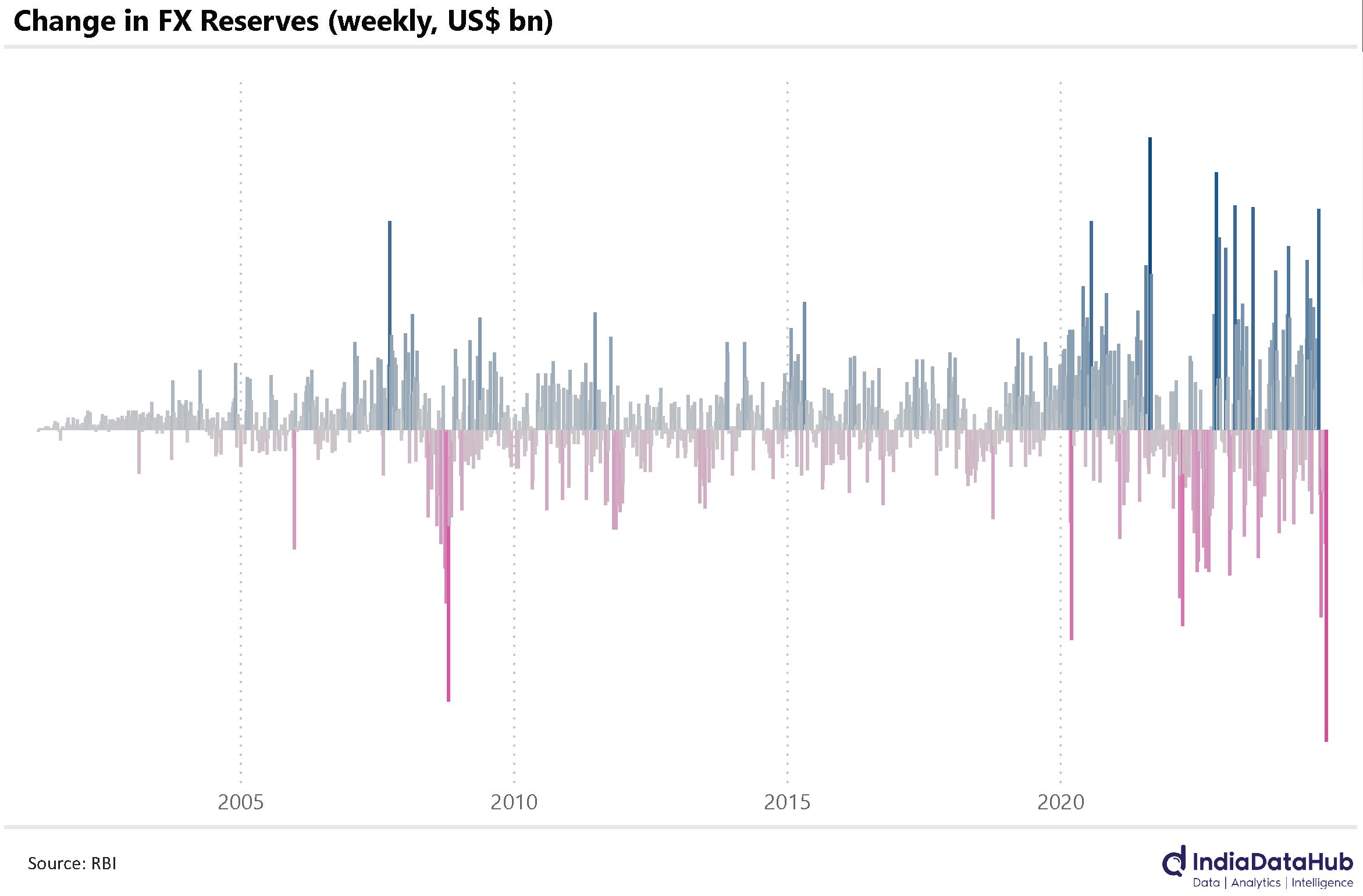

$18 Billion Gone in a Week—Rupee’s Not Going Down Without a Fight

This week’s data raised some eyebrows: India’s FX reserves fell by a record $18 billion in just one week, marking the steepest decline since data tracking began in 2001. In the last seven weeks alone, reserves have shrunk by $50 billion—or nearly 7%. To put it in perspective, this kind of fall was last seen during the 2008 financial crisis, when the global economy was in freefall.

But the world isn’t falling apart this time, so why are India’s reserves?

Turns out, the reasons are homegrown.

First, there’s the massive foreign portfolio investor (FPI) sell-off in Indian equities. We’ve covered this plenty of times before. But second—and more importantly—it’s the RBI’s changing playbook.

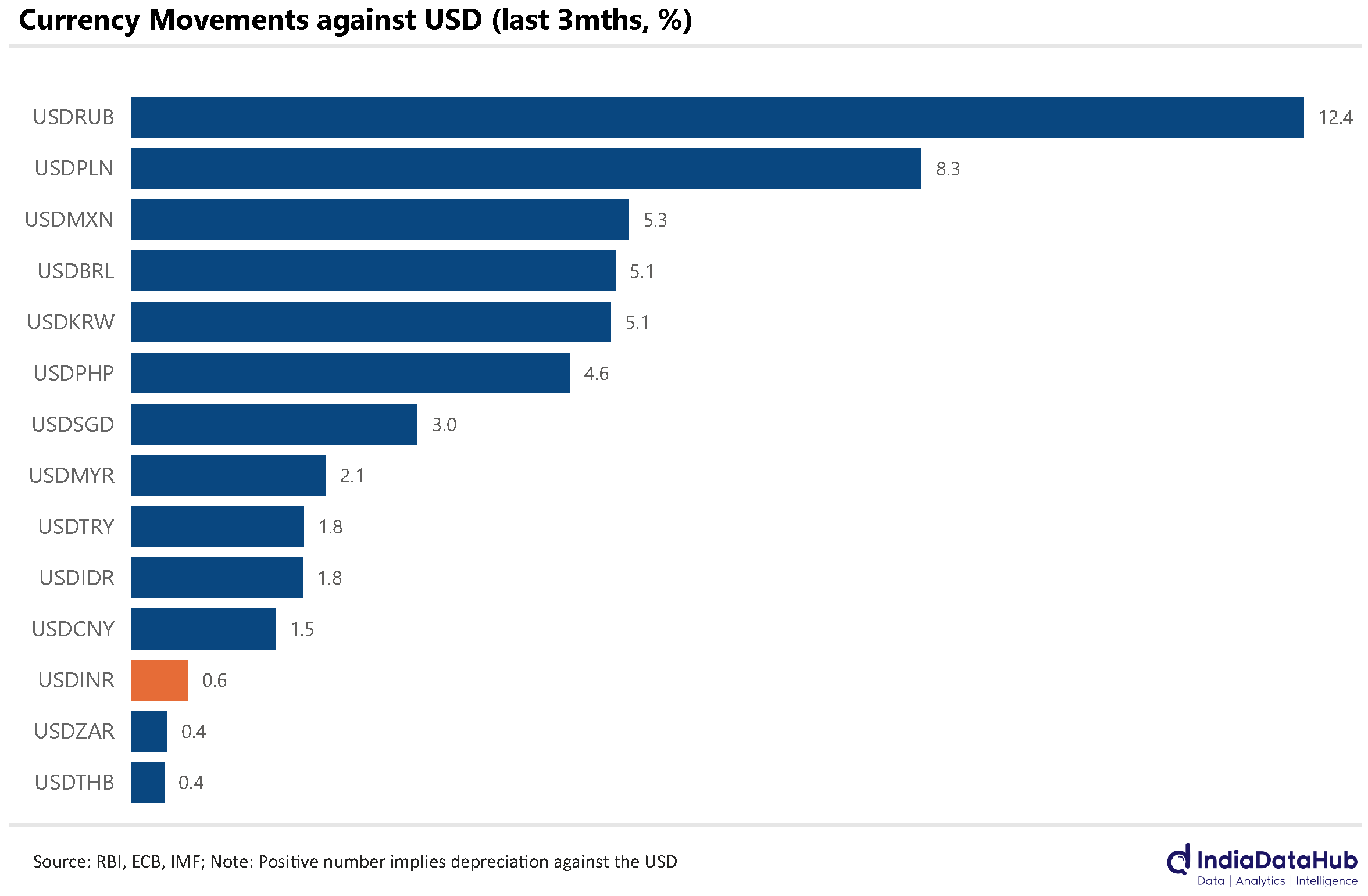

Historically, the RBI was okay with the rupee weakening gradually, in an “orderly” manner. But now? The central bank has been aggressively defending the rupee, to the point where it’s outperforming most emerging market currencies. To put it into perspective, the INR has moved just 0.6% against the USD over the last three months, while currencies like the Russian Ruble and South Korean Won have slid 12.4% and 5.1%, respectively.

With the USD rallying after the Trump win, the figures could be worse for INR, but that is not the case. INR is holding strong because the government is dipping into its forex reserves to fill all the demand that is coming for USD as INR is being sold. RBI is buying all these Rupees, spending USD from its foreign reserves, so as to not let this affect the exchange rate.

But why this sudden urgency to defend the rupee? It comes down to inflation. A weaker rupee makes imports more expensive, which fuels inflation. With food inflation already high and core inflation creeping up last month, the RBI can’t afford to let the rupee weaken further and add another layer of price pressure. Losing control over inflation would severely limit the RBI’s ability to manage monetary policy effectively—and that’s a risk they’re clearly not willing to take.

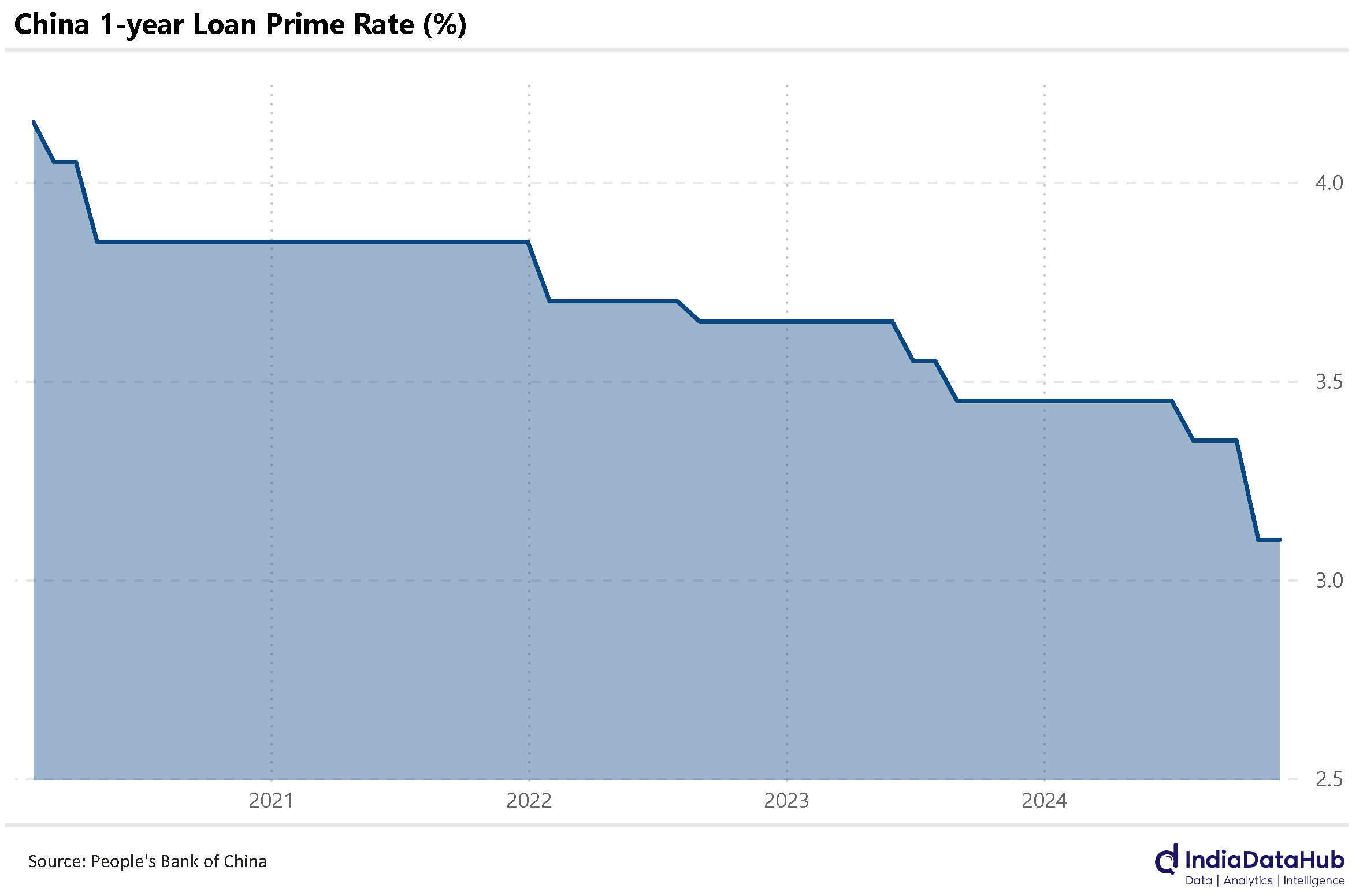

China Holds Rates Steady Amid Growing Economic Concerns

For the second month in a row, the People’s Bank of China (PBOC) decided to keep its Loan Prime Rate (LPR) unchanged. While some were hoping for a rate cut given the growth was stuttering and inflation below was 1%, this move didn’t really surprise anyone paying attention. It has kept the 1-year Loan Prime Rate unchanged at 3.1%

Here’s the thing—lowering interest rates probably wouldn’t have fixed the big problems plaguing China today. The real issue isn’t the cost of borrowing (a supply-side problem), but a lack of willingness to spend and invest (a demand-side problem).

Consumers are saving more and spending less because they’re worried about job security and the economy’s stability. On top of that, the fear of further drops in real estate prices is making households reluctant to spend or invest, even if borrowing becomes cheaper. Simply cutting rates isn’t enough to solve those issues.

If China’s looking for answers, perhaps fiscal policy is the right place to look. Unlike rate cuts, which only make borrowing cheaper, fiscal policy can directly inject money into the economy. Think cash transfers, tax cuts, or subsidies—basically putting money straight into people’s hands so they feel confident enough to spend instead of saving for a rainy day.

With everyone feeling jittery about job security and real estate, these kinds of moves may give demand the much-needed boost to get things back on track.

Chaos in Telecom Sector Continues

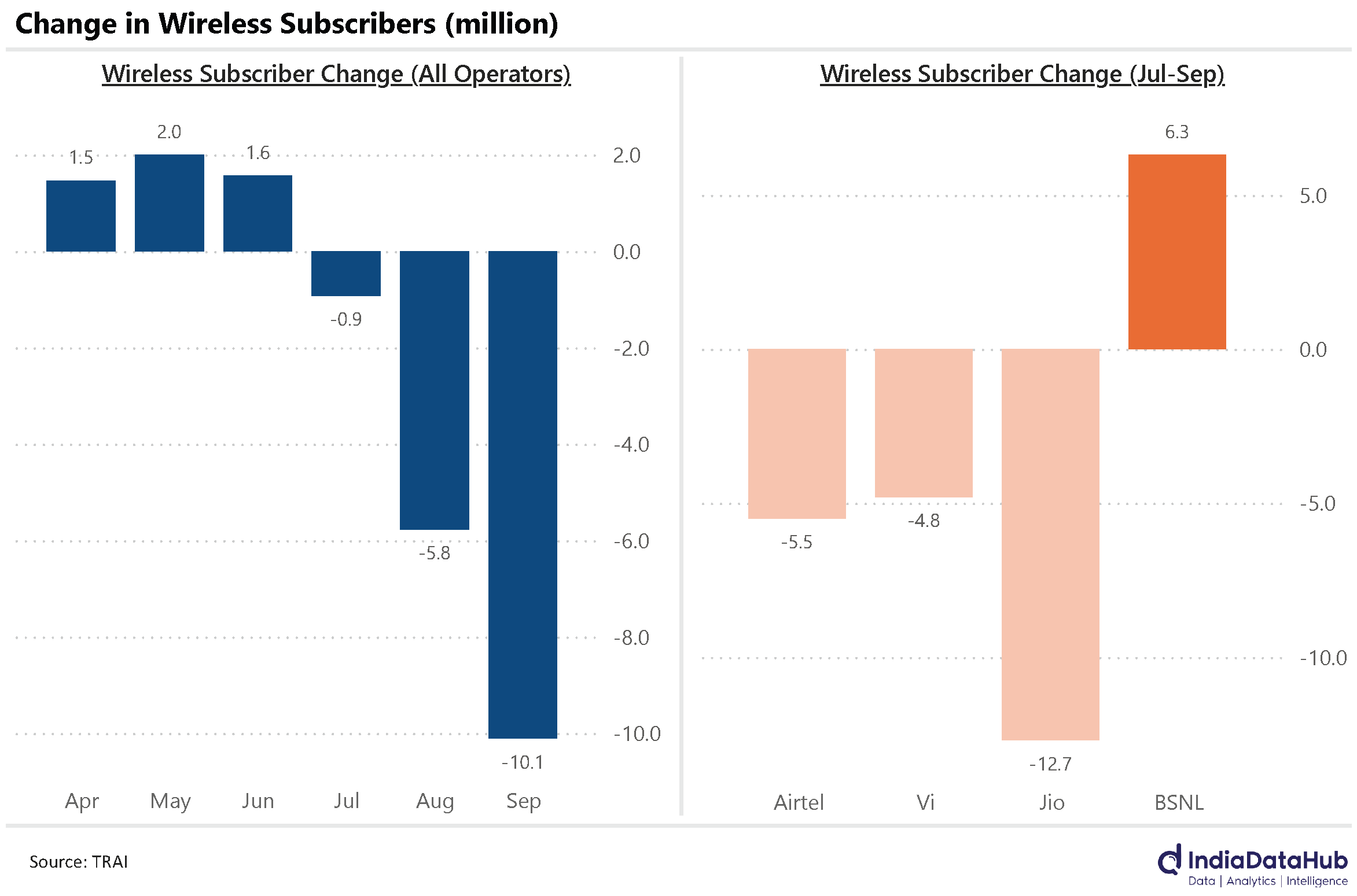

In the telecom world, it’s been a rough few months for wireless operators. September saw a whopping 10 million subscribers ditch their wireless connections, following a 6 million loss in August and roughly a million in July And for the first time in a while, even Jio is feeling the heat—it lost 8 million subscribers last month alone.

Meanwhile, BSNL is quietly having its moment. For the third month in a row, BSNL added subscribers—800,000 in September—taking its total gains to over 6 million in just three months.

At the risk of repeating ourselves (we’ve talked about this in a previous edition), the shake-up in wireless subscriptions can be traced back to the price hikes by private operators earlier this year. But what’s surprising is the sheer scale and intensity of this trend—it’s gone far beyond what anyone could have predicted.

And why wouldn’t it?. Wireless services, particularly mobile data, have become nearly ubiquitous in India. With a penetration rate that covers the vast majority of the population, wireless connectivity has shifted from being an aspirational service to a basic commodity.

The price hikes by private operators earlier this year pushed many budget-conscious users to look for cheaper alternatives like BSNL. For these users, switching providers or even giving up secondary connections altogether is a straightforward way to cut costs. Unlike earlier, when access to mobile data was limited and people were willing to pay more for reliability and speed, today, the average consumer expects basic service at the lowest possible price.

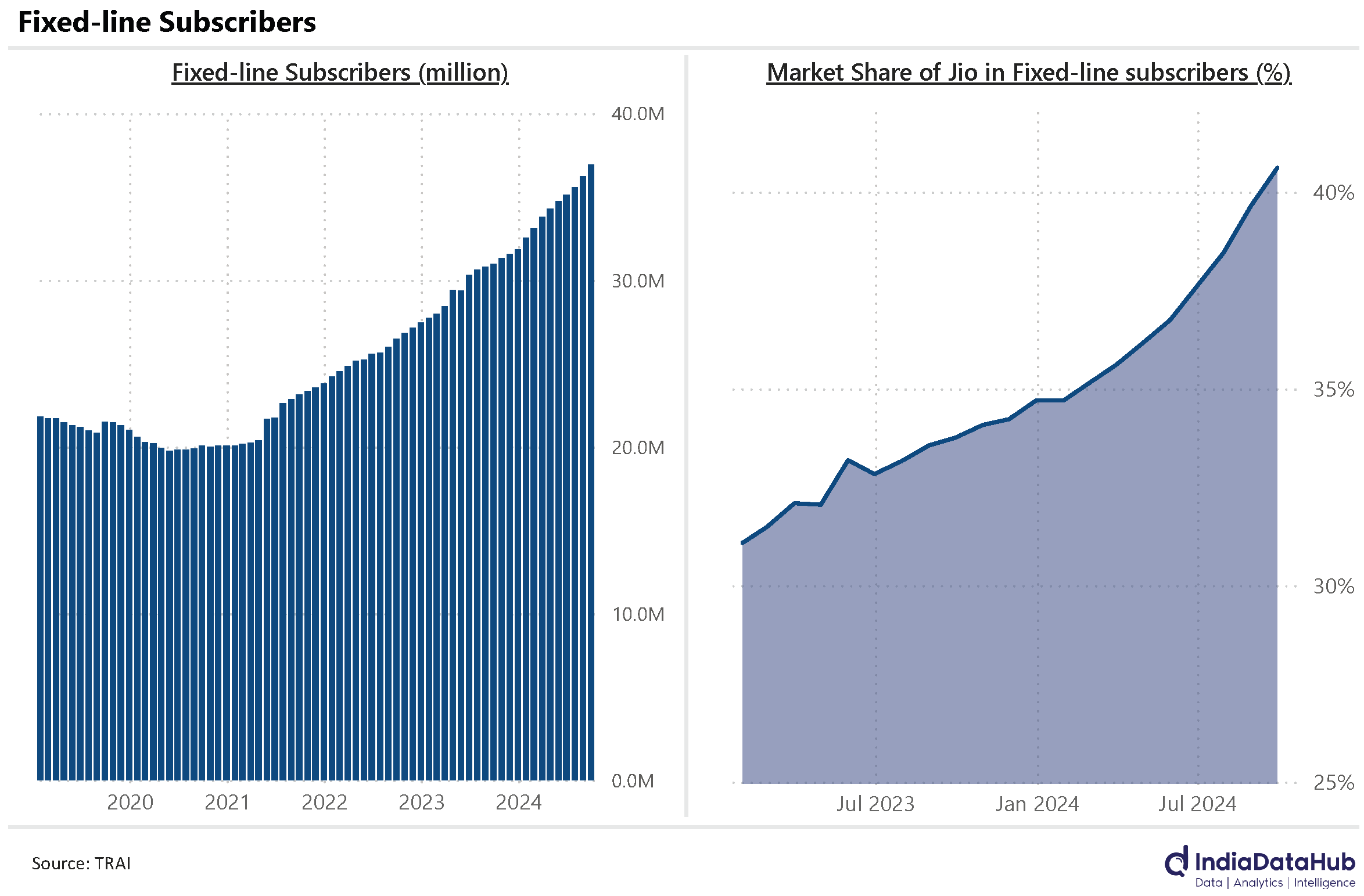

However, while wireless subscribers are dropping, fixed-line connections are booming. September alone saw 700,000 new fixed-line subscribers—the highest in nearly a year. Jio is leading the charge, adding a massive 5 percentage points to its market share in just six months, even as BSNL loses ground.

One key reason for this steady growth? Unlike the wireless segment, the fixed-line broadband space hasn’t seen tariff hikes yet. This price stability has likely played a significant role in attracting new subscribers, especially in a price-sensitive market like India.

That said, fixed-line broadband is often also seen as aspirational—a step up for households seeking better streaming, faster downloads, and more stable connectivity for work or education. It’s something people might be willing to spend some money on. But this logic will be tested if price hikes eventually hit the wired segment. Will it remain a growth story, or will we see the same subscriber drop-off happening in wireless? Only time will tell.

That’s all for this week, folks!

I sold TCS shares 17 numbers on today but amount not credited yet.

Can you pls let me know

Hi Arunava, proceeds from selling T1 holdings will not be available for further trades on the same day and will be available on the next day.

More here.