It’s the economy, stupid! Cloudy with a chance of rate cuts

We love IndiaDataHub’s weekly newsletter, ‘This Week in Data’, which neatly wraps up all major macro data stories for the week. We love it so much, in fact, that we’ve taken it upon ourselves to create a simple, digestible version of their newsletter for those of you that don’t like econ-speak. Think of us as a cover band, reproducing their ideas in our own style. Attribute all insights, here, to IndiaDataHub. All mistakes, of course, are our own.

Will farmers struggle despite above-average rains?

Little more than a month ago, it looked like the rains, despite all the optimistic predictions, were refusing to arrive.

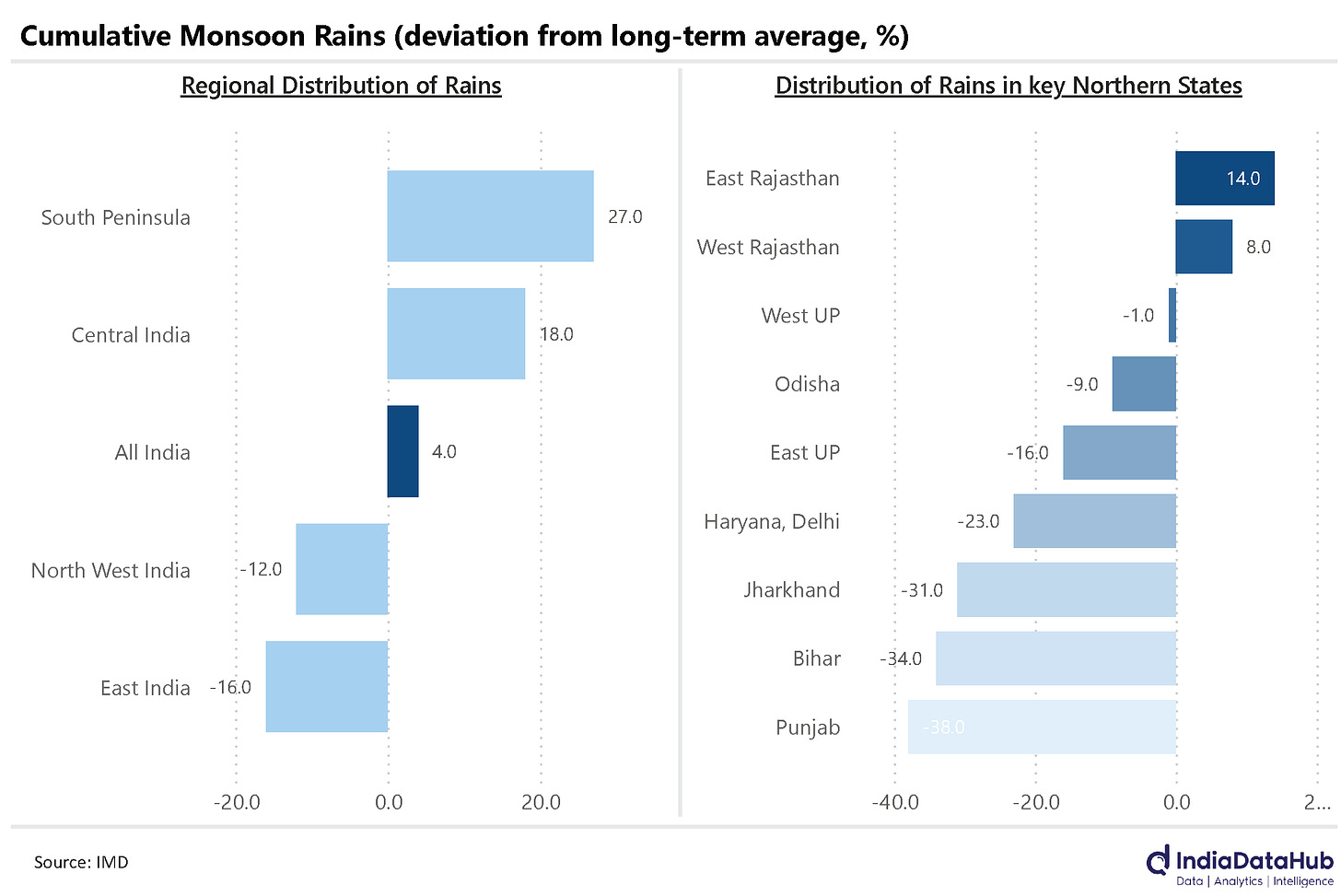

July more than made up for it. With above-average rainfall through July, the total rain we’ve got this monsoon is now 4% higher than average.

That’s only if you take the country as a whole, though. Zoom in and a more complex picture emerges. While South and Central India saw far heavier rains than usual, most of North India actually saw a lot less rain than it is used to. That said, there are exceptions within exceptions. Even though the monsoon touches Kerala before it gets anywhere else, this year, Kerala saw less rain than average. Meanwhile, Rajasthan, the desert state, has seen more rain than usual.

Here’s the big question — if North India has seen less rain than usual, what happens to all its farming? Punjab saw 40% less rain than usual, but it’s irrigated well enough to make it through. On the other hand, the long belt running from East UP, through Bihar, through Jharkhand and up to Odisha might struggle to find water for its crops.

But the monsoon isn’t done yet. Let’s hope the picture improves, once again.

The kharif round-up

Overall, though, the kharif season looks like it’s going strong. Sowing was 3.5% higher than it was last year. This graph should tell you how much the acreage of different crops has grown:

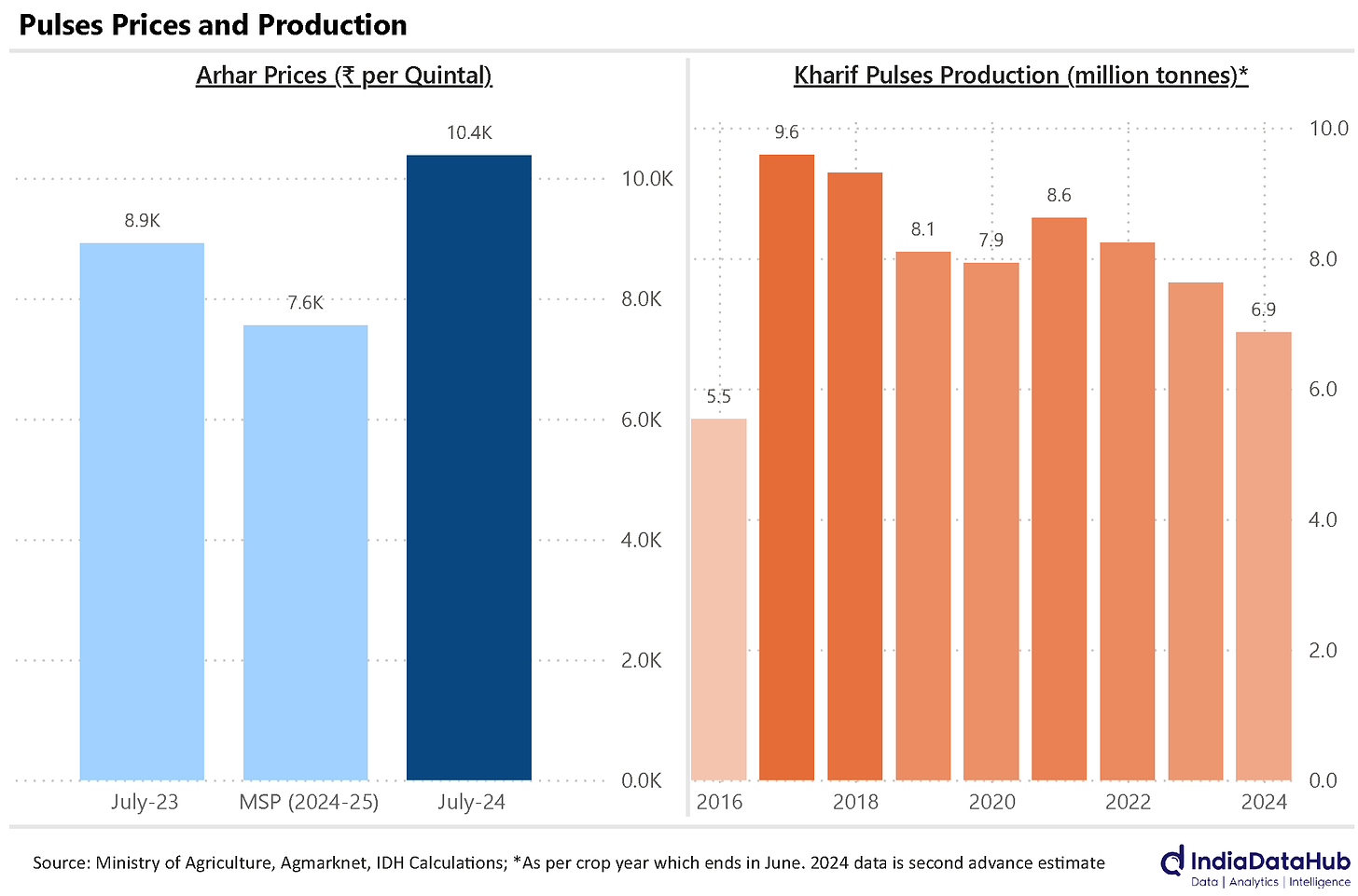

Pulses are an interesting story. Last year, the kharif pulses supply was the lowest it had been in 8 years. As supply dried up, prices shot up. This hit arhar daal in particular. Currently, arhar sells for 15% more than it did last year, and at 33% above its MSP.

Prices send a signal, and farmers seem to have responded to it. The acreage for pulses has gone up more than 20%, this year, with that for arhar shooting up 70%.

Services trade slows down

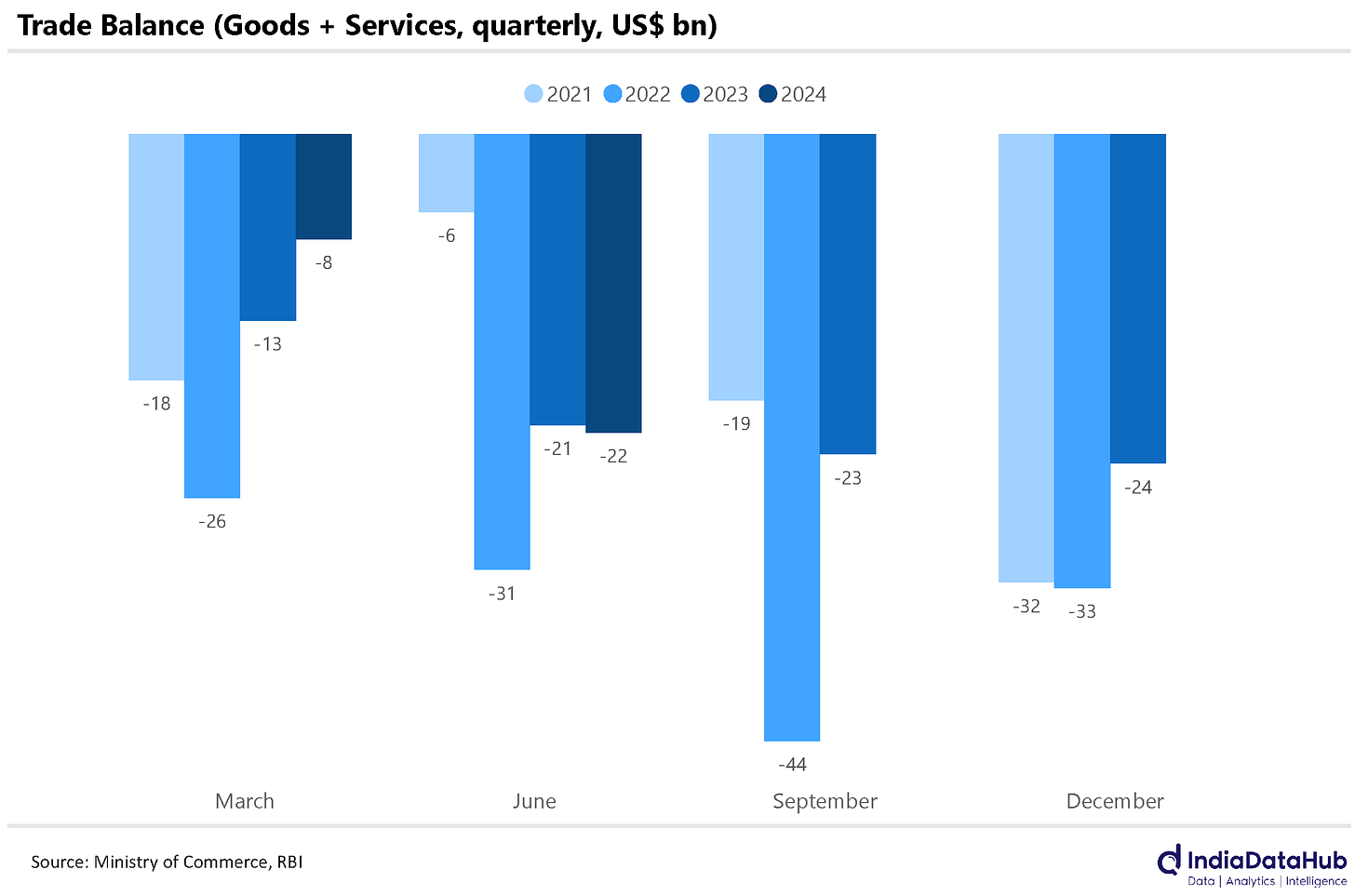

We generally import more goods than we export. In the June quarter, India’s goods trade deficit was up 10% from last year. As per June’s data, though, this increase was nullified by services, with our services trade balance rising 13%. Adding it all together, our trade deficit for the quarter — $22 billion — is pretty much exactly where it was last year.

While our trade surplus in services has improved, overall, our services trade seems to have slowed down. After two months of double-digit growth, our services exports grew by a mere 4%, year-on-year. Meanwhile, our services imports declined 4%. Looks like this is what sent our services trade balance up.

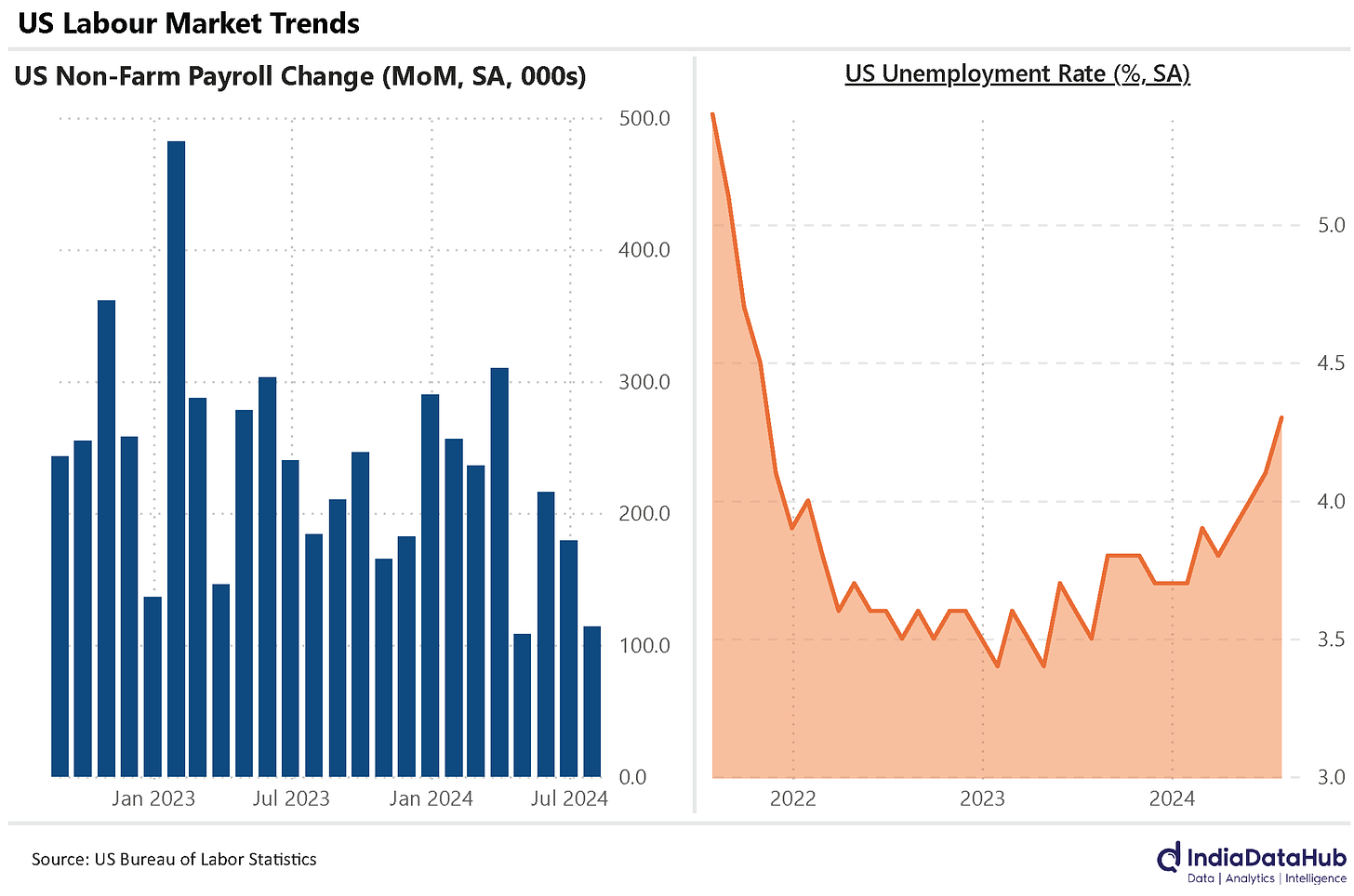

The US labour market gives way

Ever since the pandemic starting cooling down, the American job market was red hot. Unemployment was as low as it could possibly be, while the economy was churning out hundreds of thousands of new jobs every month.

Not any more, though. Job creation has been a lot slower in July than was expected. While markets expected 175,000 new non-farm jobs, only 114,000 new ones were actually created. That’s the second worst number for any month since the pandemic. What’s more, the numbers for May and June were revised downwards too.

Meanwhile, unemployment is also starting to rise. July’s unemployment rate came at 4.3%, the highest it has been since October 2021 — when we were still mid-way through the pandemic.

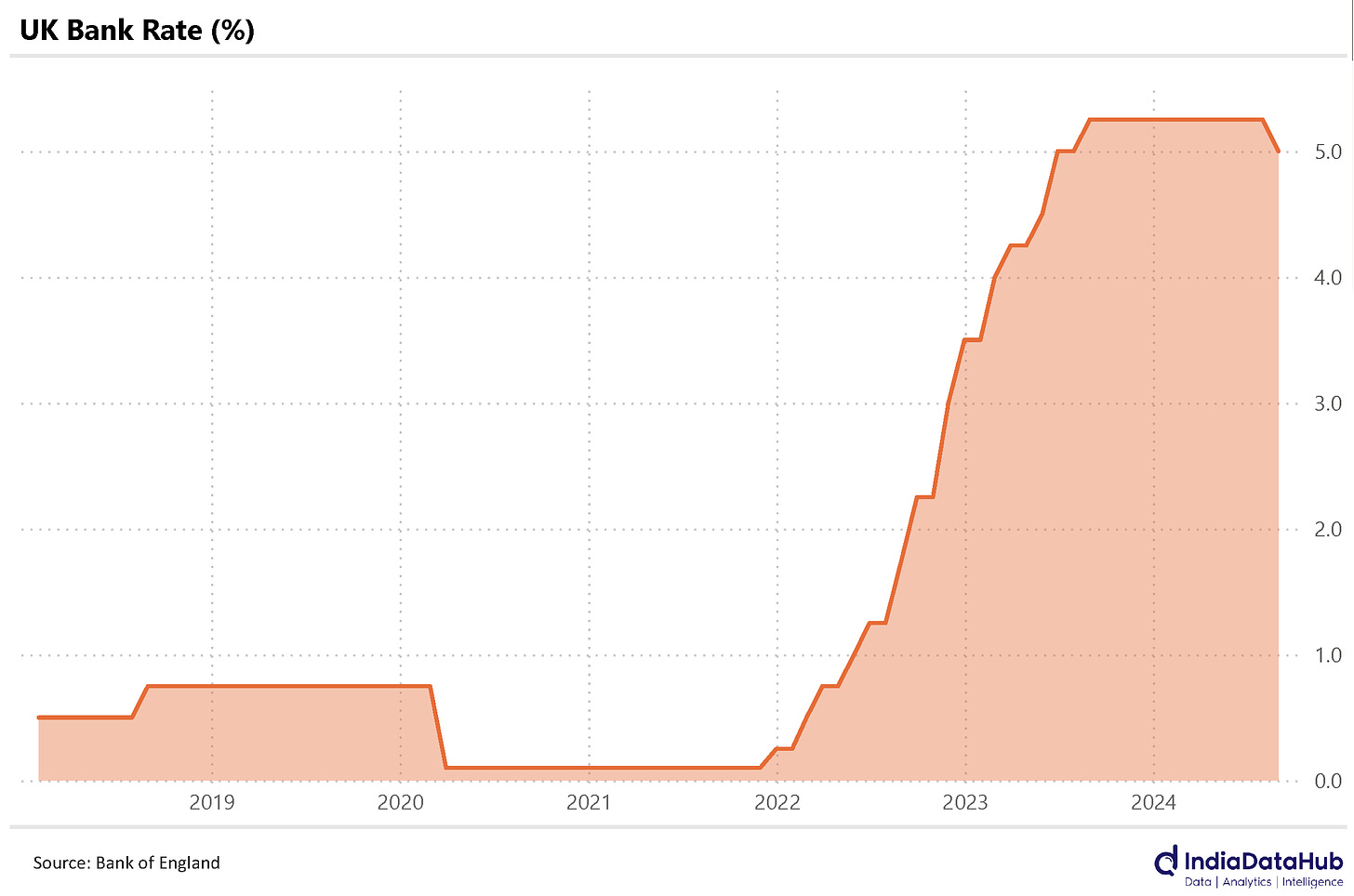

Rate cuts in the US, finally?

The US Fed didn’t cut rates last week. But it’s almost certain that there’s one coming in September.

Weak labour market data reinforces the chances of one. If job creation is slowing, the economy is probably starting to flag under high interest rates. There’s a lot more pressure on the US Fed to take action. The markets place a 100% probability on there being a rate cut in September. They place a 22% probability that the cut will be as high as 0.5%.

The Bank of England, meanwhile, has already cut rates to 5%, in a vote won by the narrowest of margins: 5-4.

While others are contemplating rate cuts, Japan raised its rates for the second time since 2007 — to 0.25%. Before this, Japan’s rates were at 0% for more than a decade. That is, if Japanese banks wanted to lend money, they could basically get it for free. People took advantage of this very fact, actually, for ‘carry trades’ — where they’d borrow for cheap in Japan, and invest in assets abroad.

The Bank of Japan is also going to hold back on buying long-term government bonds. That will pull down the demand for them, and they’ll fall in price — sending interest rates up.

Looks like this is the end of an era.

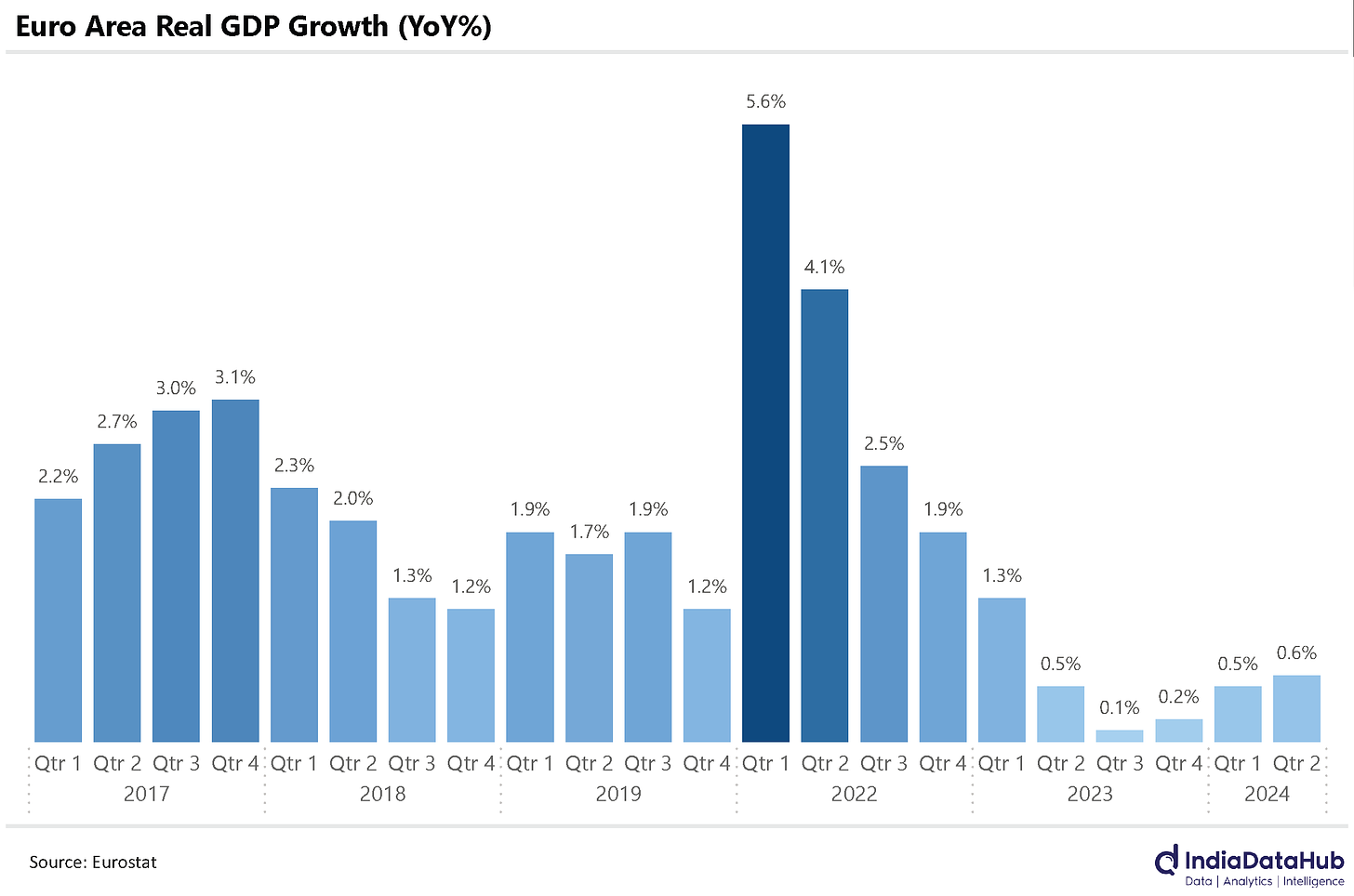

The European economy is dawdling

Europe has a problem.

It can’t seem to get any growth going. This June quarter saw a paltry 0.6% growth in the Euro area’s GDP since last year, marking the fifth consecutive quarter where it grew at less than 1%.

The traditional answer is to cut down on interest rates. That’s what the US Fed is probably considering too, after all. But that can come with a cost — inflation — and with inflation for July ticking up to 2.6%, that’s not something Europe can afford either.

So, where does it go from here?

That’s all for the week, folks!

The first chart in the sub-section titled ”The kharif round-up” is the wrong chart (US Labor market trends).

Hi, thanks for pointing out. We’ll update this.