It’s the economy, stupid! Are RuPay users now richer?

We love IndiaDataHub’s weekly newsletter, ‘This Week in Data’, which neatly wraps up all major macro data stories for the week. We love it so much, in fact, that we’ve taken it upon ourselves to create a simple, digestible version of their newsletter for those of you that don’t like econ-speak. Think of us as a cover band, reproducing their ideas in our own style. Attribute all insights, here, to IndiaDataHub. All mistakes, of course, are our own.

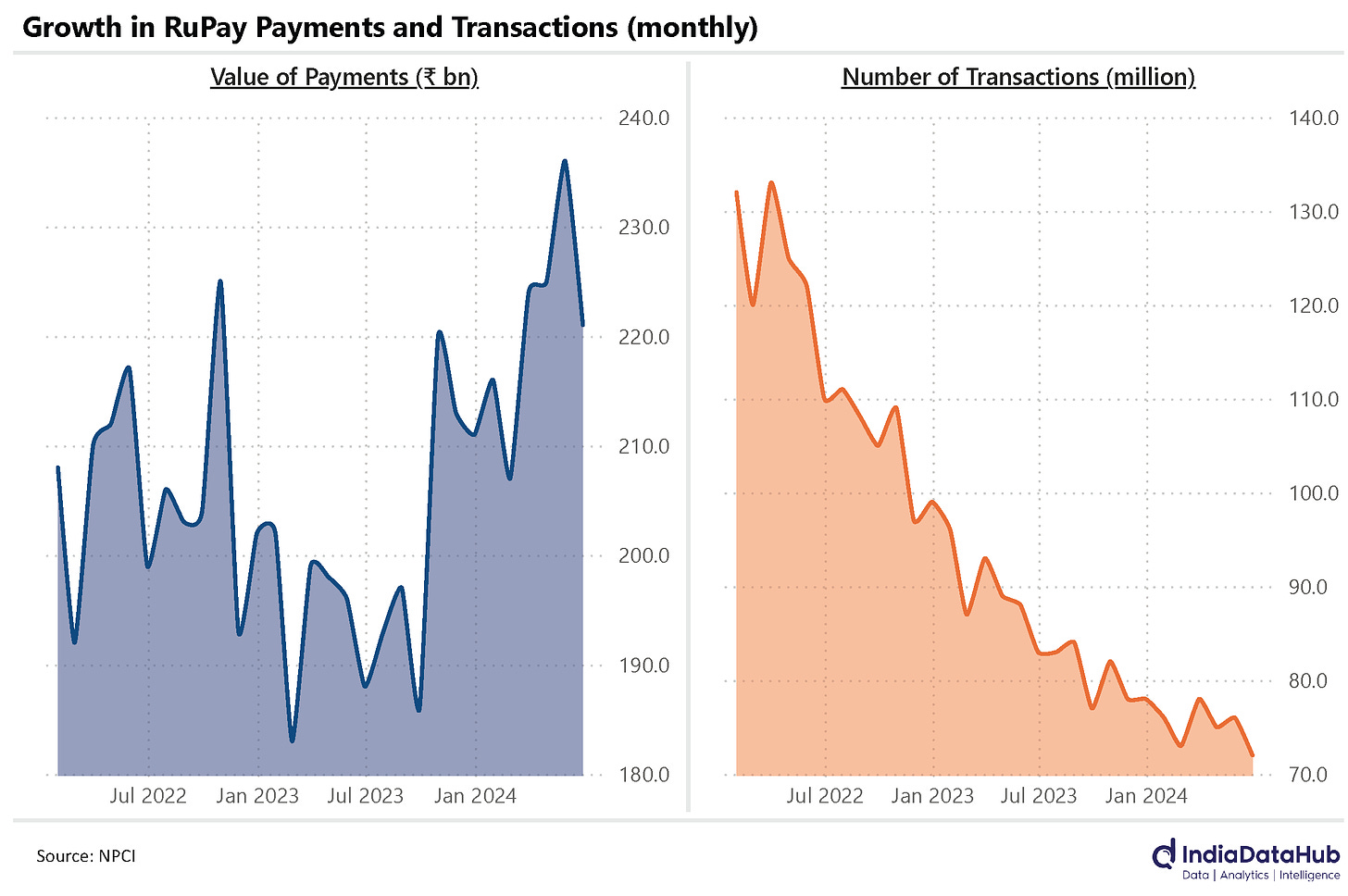

More payment, fewer payers on RuPay

Imagine this: you go to a store, pick up a T-shirt, walk to the payment kiosk and whip out your debit card. The cashier does some plastic magic. And voila! Your payment is done. Somewhere in the background, money leaves your bank account and goes to the store. Automatically.

How does this even happen?

Well, there are massive — often globe-spanning — networks that stitch different banks together. They’re run by multi-billion dollar corporations like Visa and Mastercard. When you make a purchase, these corporations talk to your bank, figure out whether you have enough money, tell the merchant’s bank if you’re good for the payment, and then ask your bank to send the money to the merchant’s bank. All of this in an instant.

A decade ago, the RBI tried a gambit. At the time, transactions would be routed abroad to foreign payment networks, even though there were Indian banks at both ends of the transaction. This was expensive. And so, the RBI stepped in to create its own network — RuPay. This was housed with the NPCI, which also runs the UPI network. The government put its might behind the project. All cards issued with ‘Jan Dhan’ accounts, for instance, were linked to RuPay. By 2017, RuPay pipped Visa to become India’s largest payment card network.

Cut to today. We have some interesting new data on the RuPay network. One, the number of monthly transactions on the network have declined significantly, with May being the 24th consecutive month of decline. The number of transactions through this period has fallen by almost a third.

At the same time, though, the value of payments on the network is growing by leaps. June was the fifth consecutive month of double-digit growth, with transactions growing 17%.

So, oddly enough, even as the number of transactions has fallen, the total value of transactions has increased. Putting the two together: it looks like fewer people are using RuPay cards, but for bigger purchases than ever before. The average ticket size for transactions on the network has almost doubled over the last two years.

Why? We don’t know for sure. What we do know, however, is that RuPay credit cards shot up in popularity in FY 2023, when they were first linked to the UPI network. The average credit card user is more affluent than someone that just has a debit card — especially if the debit card was issued for a Jan Dhan account. Is it these new credit card users that are driving up the ticket sizes on the RuPay network?

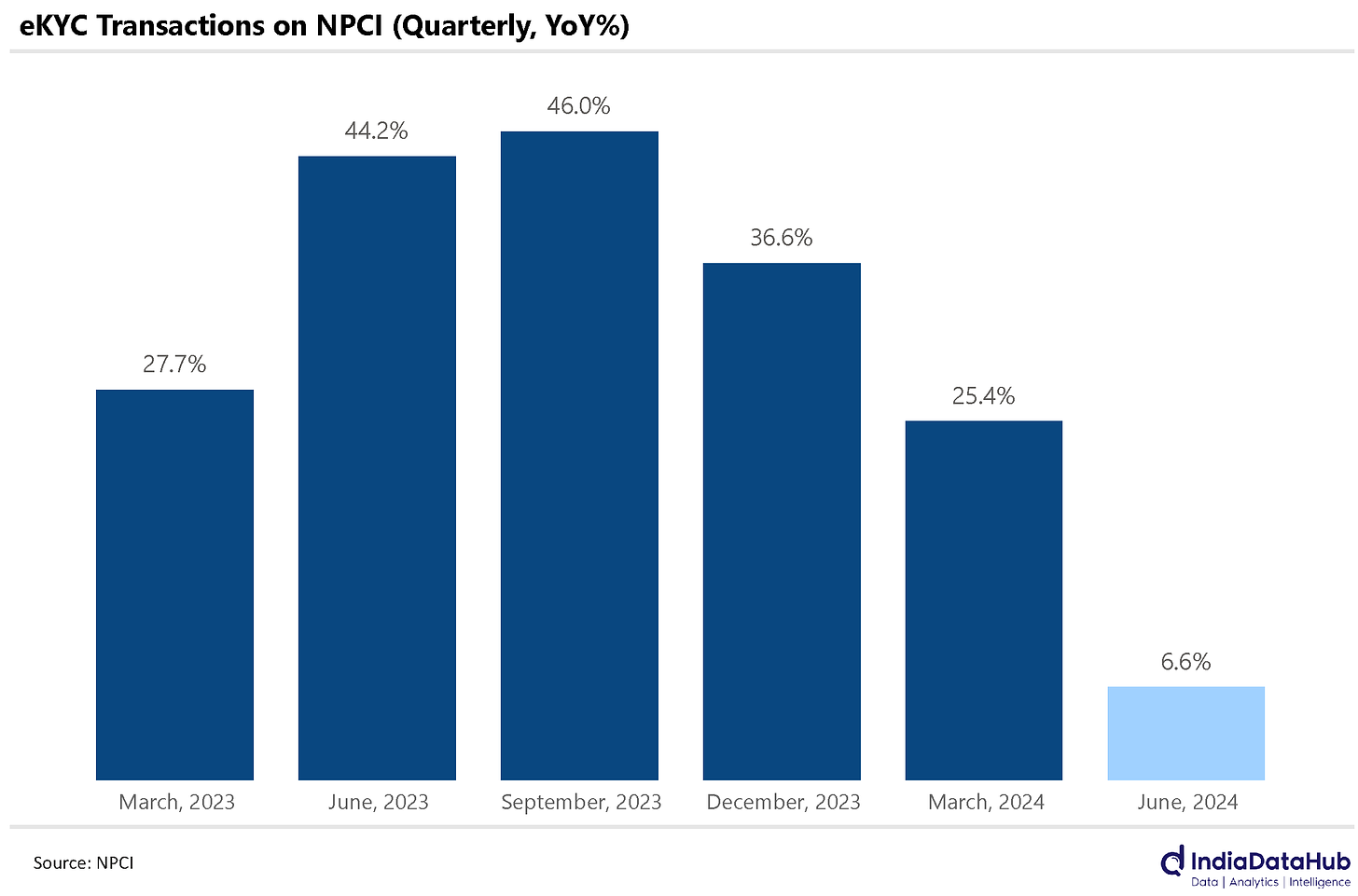

What happened to all the e-KYC?

Quarter after quarter, for well over a year, the number of eKYC transactions facilitated by NPCI grew by well over 25%, year-on-year. In the June quarter, though, their growth slowed down dramatically — to just 6.6%.

(Keep in mind, though: that’s more than 107 million successful transactions over the quarter. For just KYC. Not something most people have to do every day.)

What does this slowdown tell us? Might it be that fintechs, embattled by regulation and liquidity constraints, are adding customers much slower than they once were? That would certainly dovetail well the RBI’s recent zeal for enforcement.

Or is it just that the exponential growth-phase of the industry is coming to a close, and we’ll see a more mature industry in the months to come?

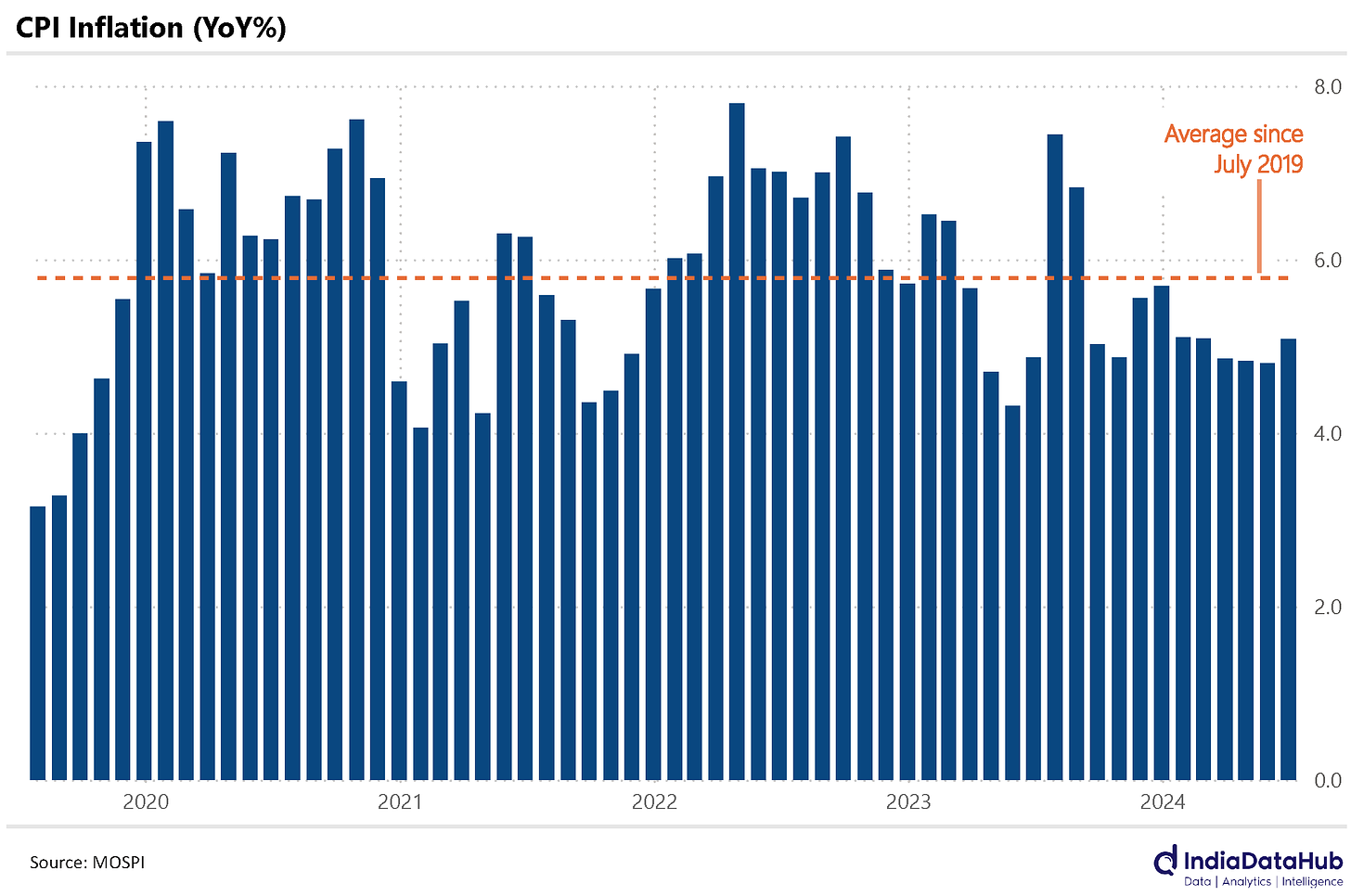

No relief on inflation

June’s inflation reading came in at a four-month high: 5.1%.

As usual, it’s food inflation that is sending prices up. Non-food inflation rose as well, but only by a negligible 0.02%, after a 17-month long decline.

Now, the big question is: what does this mean to the RBI?

For months now, our inflation has been a little too high for comfort — well above the RBI’s 4% target. Over the last five years, it’s been at a worrying-but-tolerable 5.8%. Currently, it’s not high enough for the RBI to actually step up its anti-inflation measures. But it’s too high for the RBI to reduce rates and let more money stream into the economy. The smartest thing to do is just wait and watch.

This will probably remain the case unless the economy’s growth itself suffers. At the moment, the RBI’s Monetary Policy Committee (MPC) sees no such risk. It expects 7+% growth this financial year. And so, to the MPC, there’s no need to do anything to boost growth, especially if it could inadvertently send prices up.

This can change, though. Economic data for May and June has been less promising than one would hope. If July’s data is weak too, the MPC will suddenly find that it has a big problem on its hands — right before its August meeting. In its last meeting, a third of the MPC voted for a rate cut. Who knows what will happen this time.

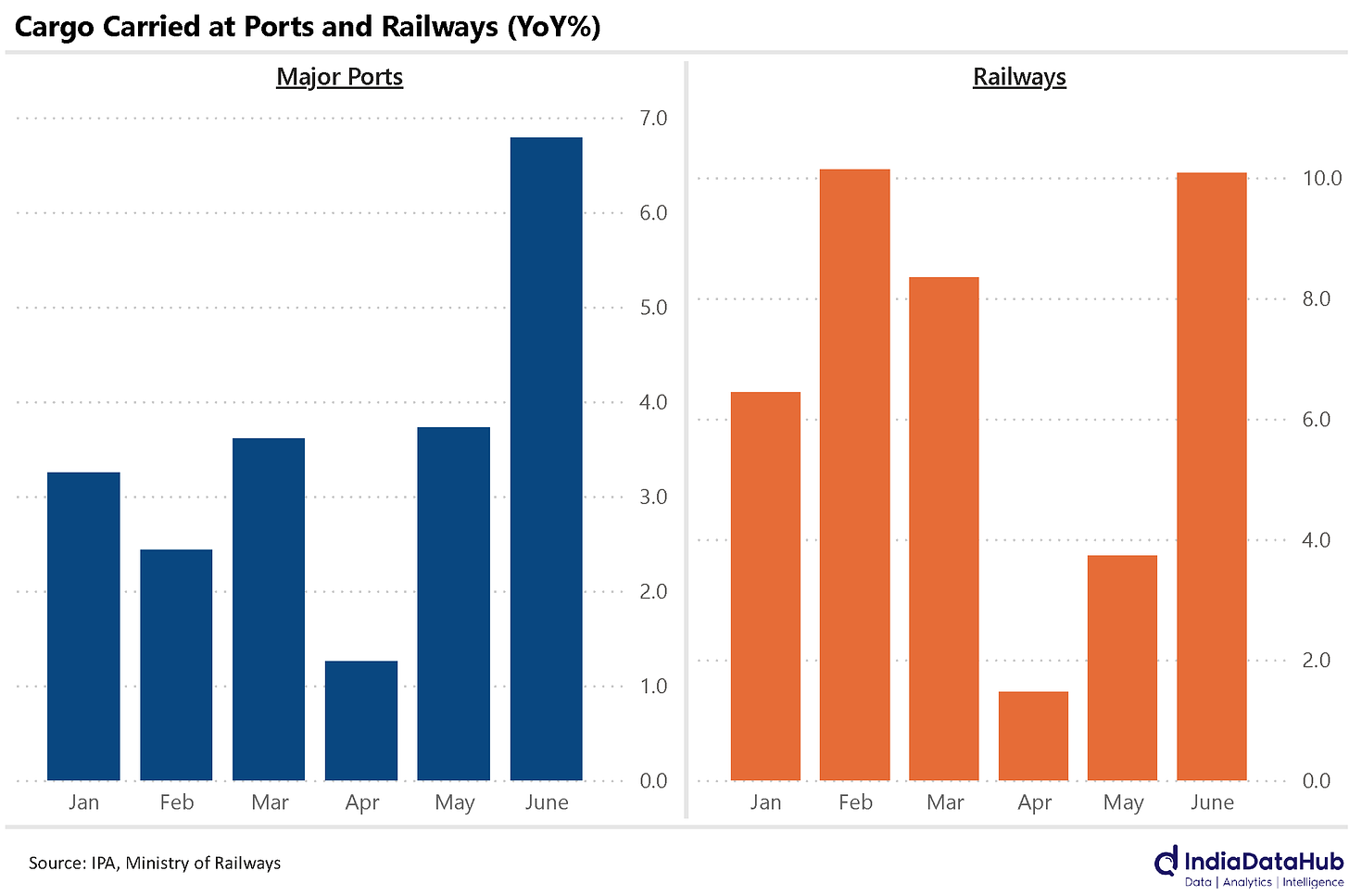

June was good, actually?

We wrote, last week, about how the June data suggested a slowdown in the economy. We’d looked mainly at automobile sales and fuel consumption to reach this conclusion.

Here’s a counterpoint: Foreign trade was looking up this June. Cargo traffic at our ports was up by almost 7% since June last year. Moreover, trade in manufactured goods was higher. See, while bulk cargo — things like coal or crude oil — is transported as-is, manufactured goods are usually sent in containers. And container traffic was up 13% in June. So, not only did we trade more, the quality of our trade was also better.

So, what explains last week’s data? If more goods are being ferried around our economy, why are we using less diesel? Why are we buying fewer trucks?

Well, you can use trucks to connect India’s ports with the rest of the country. Or, in the alternative, you can use trains. Now, railway freight grew 10% year-on-year this June. We were perplexed by why E-Way bills were going up last week. This bit of data solves that mystery.

So here’s an alternative explanation: there’s a shift going on in the Indian economy. People are starting to rely more on trains than on trucks. A lot of what one might send by road, last year, went through trains this time around. So, diesel consumption was flat. Nevertheless, June actually saw more trade, not less — and so, freight movement went up. It just went up via different modes of transport. Other discomforting numbers, such as falling auto sales, were just random variation in the data.

Is this true? Or is it just wishful thinking? We’ll know soon enough.

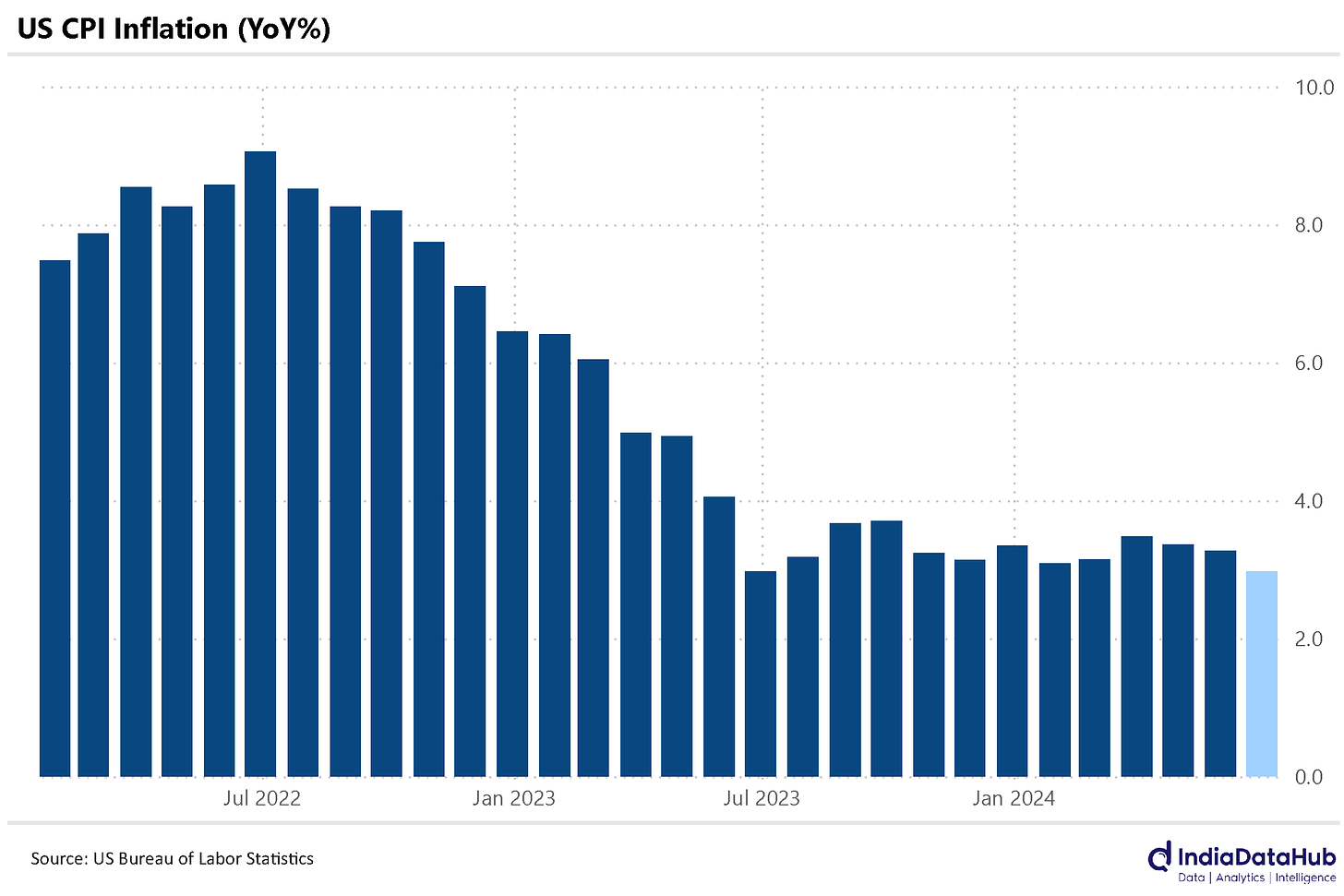

America slated for a rate cut!

America’s inflation was hovering just above 3% for more than a year, stubbornly refusing to go any lower. After posting a decline for three consecutive months, though, it finally hit the 3% mark in June — a 13-month low.

Does this mean a rate cut is in order? After all, rates have been high all these months precisely because inflation has been high.

Well, the markets certainly think so. Last week, we wrote about how the markets gave a 78% chance that there would be a rate cut when the US Fed met in December. In just a week, this has gone up to 96%! These are the best odds the markets have given for a rate cut in a long while. And while the markets have been wrong plenty of times before, perhaps one is finally near?

China gets cheaper, inflation spikes elsewhere

China has an odd sort of problem. It invested far too much into its economy at the cost of its consumers. As a result, its consumers never grew to buy things like Western consumers do. It was feasible to run the country this way earlier, when the economy was in the middle of its forty-five year long dream run. But now that its economic prospects look a little dulled, this lack of consumption is becoming a drag on its economy.

China simply can’t bring its people to consume any more. Not too long ago, it found itself in a four month interlude when prices just kept crashing, as people refused to buy anything. In June, retail sales were well below what anyone expected — growing at a mere 2%, compared to market forecasts of 3.3%.

And this showed up in Chinese prices, with inflation coming to just 0.2% year-on-year in June. This makes China a global outlier among emerging markets.

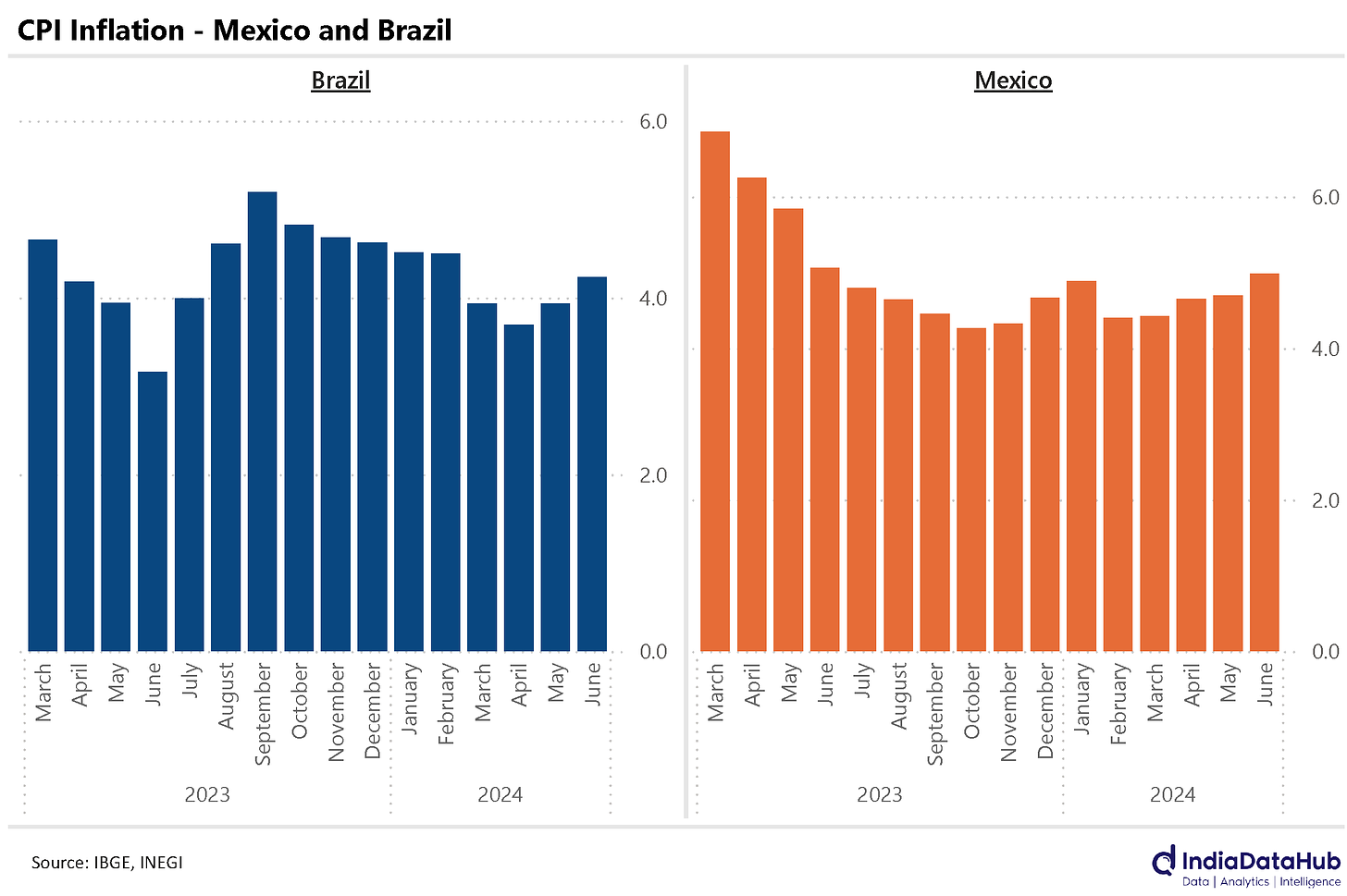

You see a more typical trend in Mexico and Brazil, which both saw inflation go up last month. Inflation was up 4.2%, year-on-year in Brazil last month — a 4-month high. It was up 5% in Mexico as well — the highest inflation reading the country has seen in a year.

Zooming out, there’s some sort of divergence in the inflation behaviour of developed and developing countries (with China being an outlier for both). It’ll be interesting to see how both sets of countries behave if (or when?) the United States cuts rates.

That’s all for the week, folks. Thanks for reading!