Are Indian Banks Really Resilient?

While many concerns have been raised about credit growth outpacing deposit growth and, hence, building risk in the banking system, the Indian banking system seems to be showing signs of strength.

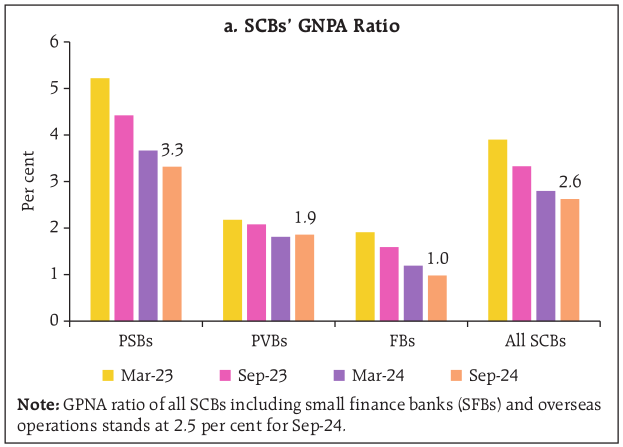

In September 2024, industry-level Gross Non-Performing Assets (GNPAs) hit a 12-year low of 2.6%. Last year, the system-level GNPA was 3.2%.

If a borrower has not been repaying their dues for more than three months, he/she is classified as Gross NPA or GNPA.

The banking system classifies a loan account as a defaulter or ‘Gross Non-Performing Asset (GNPA)’ if the borrower does not pay the loan dues for three consecutive months.

GNPA shows how big the bad loans are compared to the total loans in the banking system.

We looked at the RBI’s Financial Stability Report for December 2024 for what it has to say about the banking system’s resilience, starting with GNPA. Here is a summary of what we read.

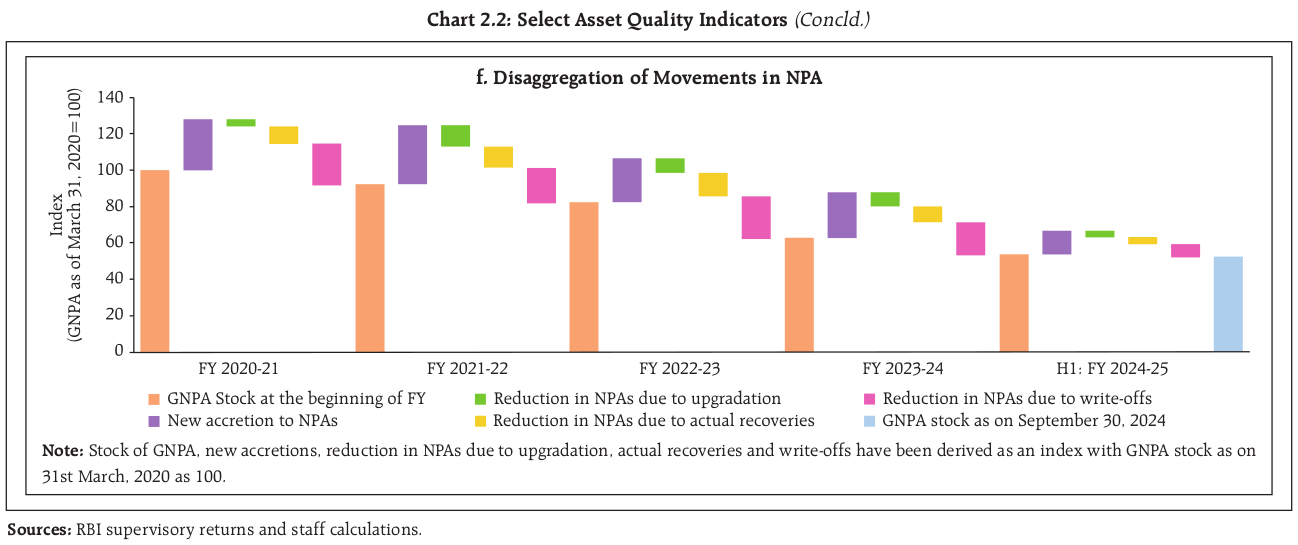

What has caused the GNPAs to come down?

- The borrower profile has improved. Banks are being more prudent in assessing a borrower’s creditworthiness.

- NPA-classified borrowers actually started paying up or were upgraded to standard accounts after reclassification.

- Banks are writing off NPAs. Write-offs occur when a bank is reasonably sure that certain accounts are not recoverable. The bank stops efforts to collect repayments and also stops recording those accounts as NPAs. Hence, the size of NPAs reduces. The RBI’s Financial Stability Report for December 2024 shows that write-offs are the biggest reason for NPA reduction.

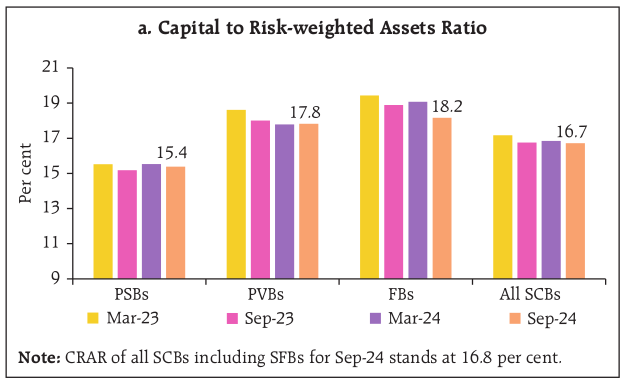

Now, let’s look at the system-level capital adequacy.

The Capital to Risk-Weighted Assets Ratio of India’s banking system stands at 16.8% and has hovered around that number for the last year. It is comfortably higher than the minimum required limit of 9%.

In very simplistic terms, if the banks have lent out loans worth 100, they have a capital worth 16.8. The minimum capital they should have is 9. The higher this number, the better a bank’s ability to grow its loan book or handle shocks.

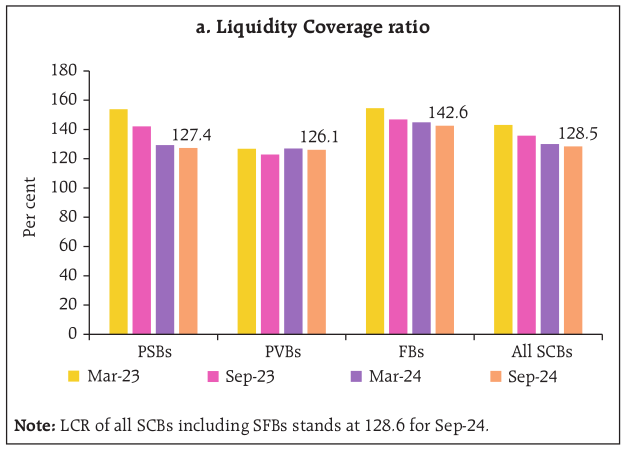

Having a strong capital reserve and low levels of bad loans means little if a bank does not have liquidity. The bank needs enough liquidity to honor

- All its short-term liabilities and

- Withdrawal requests on the savings accounts and fixed deposits as and when they come

The overall liquidity coverage ratio (LCR) of the banks has come down but, at 128.5, is comfortably above the minimum requirement of 100%.

The LCR shows how much liquid funds a bank has to meet all obligations, even under stress over the next 30 days.

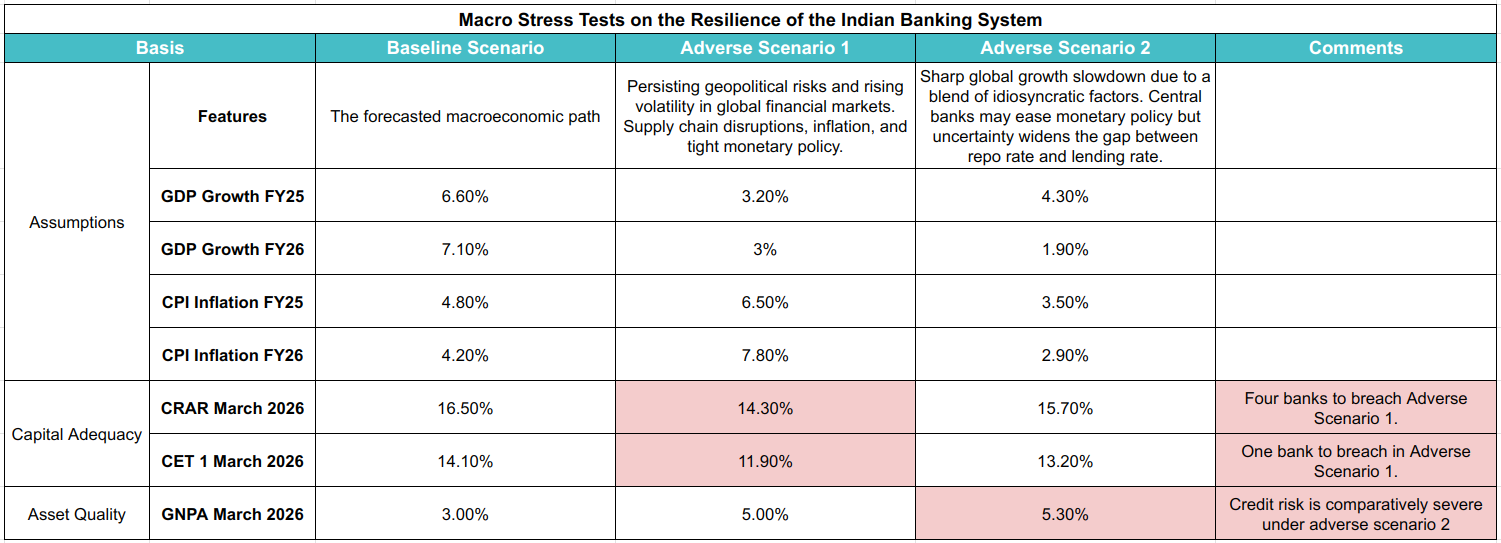

For every version of its Financial Stability Report, the RBI runs macro stress tests on the whole banking industry to check for its resilience under stress. It computes a baseline scenario and then runs stress tests under two different scenarios.

It seems our banking system will largely stay afloat even under maximum stress. Check this table for a summary of their stress tests.

The Baseline scenario is how the economy is expected to be. Adverse Scenario 1 shows how the economy would be if the geopolitical tensions continue. Adverse Scenario 2 shows how an external system-wide shock might hit the economy.

Adverse Scenarios 1 and 2 present different scenarios. One is not necessarily more intense than the other. In most likelihood, Adverse Scenario 2 seems incapable of causing any system-level shocks. The banking system will function well even under Adverse Scenario 1, but a few banks could go under.

The RBI also runs a sensitivity analysis on the system. While stress tests construct stress scenarios at the macro level, sensitivity analysis constructs stress scenarios for specific factors.

Credit risk: If system-level GNPAs fall by 2 standard deviations, their capital adequacy will fall to 13.1%, and CET1 will fall to 10.3%. Both will still be well above the respective regulatory minimum levels. A shock of 4.4 standard deviations will be needed to bring the system-level CRAR below 9%.

Interest rate risk: A parallel upward shift of 250 bps in the yield curve would reduce the system-level CRAR by 114 bps, and four banks could fall below the minimum requirement of 9%.

Equity price risk: Banks have limited exposure to equities due to regulatory restrictions. Therefore, even a 55% drop in equity prices would impact the system-level capital adequacy by only 58 bps.

Liquidity risk: Liquidity risk shows the impact of a run on deposits in case of a crisis. LCR is 128% in the baseline scenario, 121% in stress scenario 1, and 115% in stress scenario 2. No bank will fall below the minimum LCR of 100% under scenario 1, but two banks could breach under scenario 2.

The Indian banking system’s resilience stands on two pillars:

- The visibly strong financial health of its banks

- The second is the macro tests and sensitivity analysis that prove its structural ability to handle shocks.

And both seem to be promising.

Great read Vineeth