Is it life-as-usual for the world despite the Russia-Ukraine war?

A group of the world’s top economic experts in Europe and the US were polled for their views on the global economic fallouts of Russia’s invasion of Ukraine in 2022, and most of them had similar views as most of us – high inflation, slow growth, challenges to food and semiconductor production, shipping woes, and the like.

It has been over two and a half years since the war broke out. What are the challenges the world is facing today on account of the war? Or are there any challenges at all?

Oil Prices

As an immediate reaction to the war, Western countries imposed many sanctions on Russia and drastically reduced their purchases of Russian oil and gas, sending fuel prices higher. However, the rally was shortlived as China and India lapped up the Russian oil and gas. Most emerging economies continued their trade with Russia.

Fuel prices are perhaps the strongest external drivers of inflation for goods and services in any economy. Shipping and industrial production heavily depend on fuels. When oil and gas become expensive, the prices of food and consumer goods in general will almost certainly increase.

Emerging countries did not follow the West in cutting ties with Russia. Russia’s oil trade just got reallocated from Europe to China, India, and other emerging markets. So, these countries did not experience raging inflation on account of oil prices, as was widely expected.

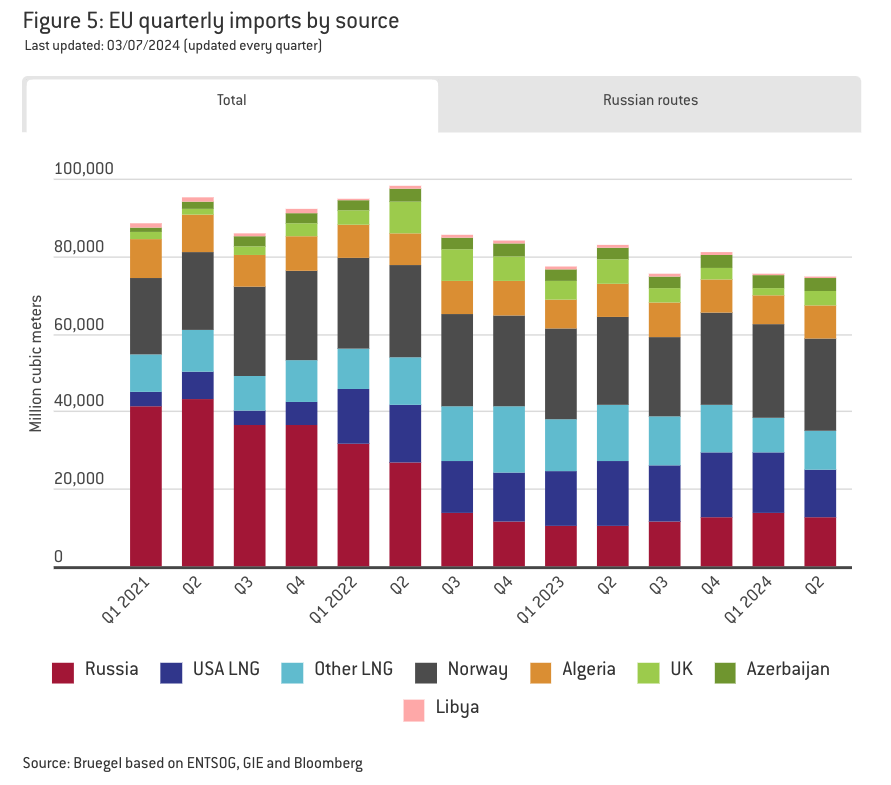

The war has hurt the EU the most. The region was heavily dependent on Russian fuel, and the war reduced business activity between the two regions. The EU continued to buy Russian fuel, but not as much as it was before the invasion.

Europe struggled with high energy prices for several months, but the situation seems to have normalized. They are buying more fuel from other regions, and their purchases of Russian fuel have also been gradually rising lately.

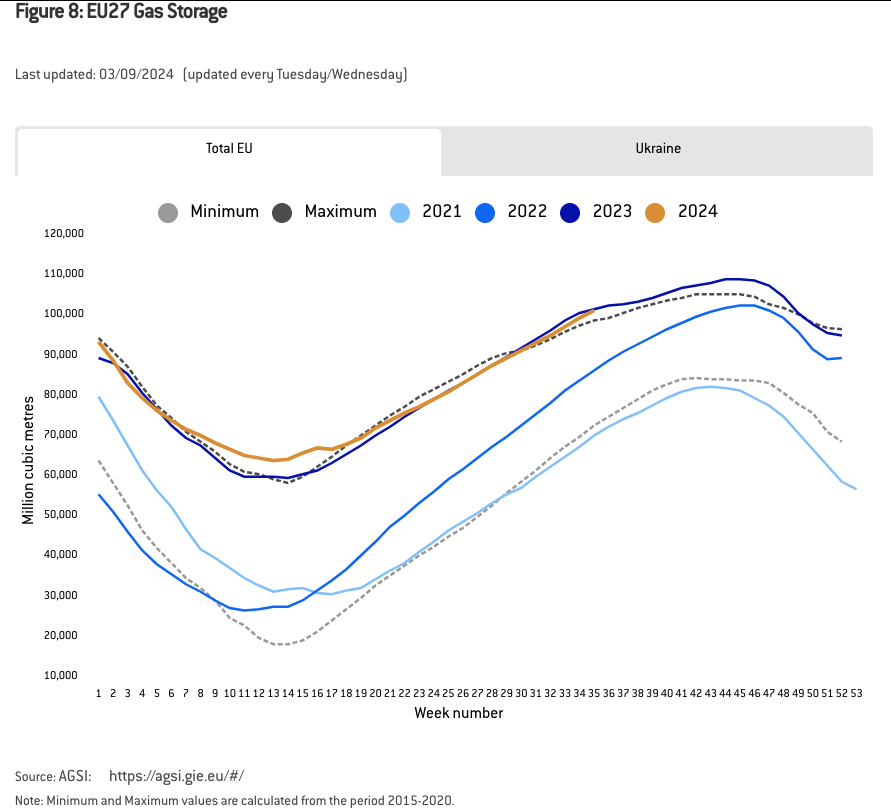

Another indicator of fuel price stability is the level of fuel inventory a country holds. After witnessing a major dip immediately after the incursion, the EU’s current natural gas inventory levels have been hovering above the average seen in the 2015-20 period.

Commodities and Agricultural Goods

Beyond fuel, there were challenges for agricultural commodities and minerals that Russia and Ukraine supply to the world.

Ukraine is one of the largest food exporters globally. Like the world significantly depends on China for manufacturing, it depends on Ukraine and Russia for agriculture and commodities.

As part of its invasion of Ukraine, Russia had blocked all Ukrainian ports to cripple its ability to sell the huge inventory of its agricultural goods. Ukraine had to shift to land routes to export its goods.

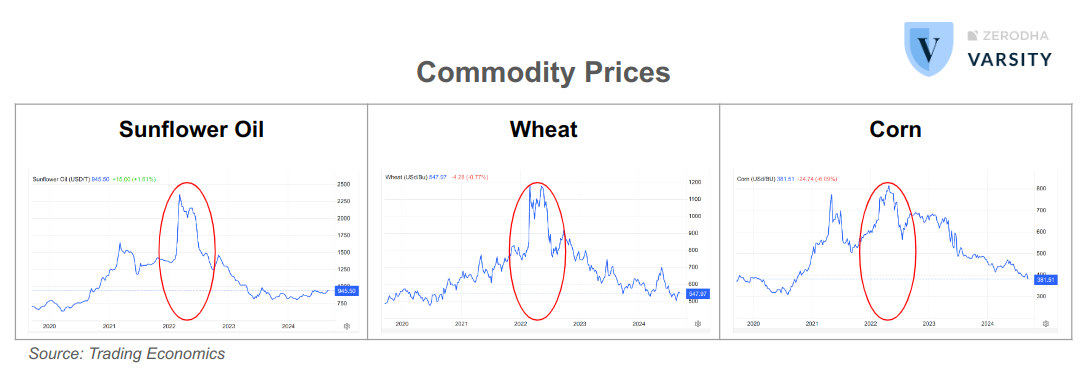

As a result, the prices of sunflower oil, wheat, maize, barley, and other commodities that Ukraine and Russia export skyrocketed the world over. Global supply chain disruptions, such as those caused by China’s prolonged COVID-related shutdown, were highly expected as the war began.

The woes were not limited to food. Ukraine supplies about 50% of the world’s neon, and Russia supplies 30%. Neon has applications in electronics, aviation, automotive, and semiconductors. Russia also supplies about a fifth of the world’s palladium, which has wide-ranging applications in chip-making, surgical instruments, water treatment, jewellery, and electronics.

Fears of a supply chain crisis and food shortages that could lead to famines in African and Middle Eastern countries grew food insecurity. Ukraine, often touted as one of the breadbaskets of the world, also became one of the most food insecure countries.

India is the largest consumer and importer of edible oils, importing more than half of the total edible oil it consumes. It is also the biggest consumer of sunflower oil, with ~85% of it coming from Russia and Ukraine alone. When the war broke out, sunflower oil imports became a challenge for India.

The demand and prices of soybean oil and palm oil, basically the substitutes for sunflower oil, went up. So, the prices of soybean and palm oils also rallied in the global markets. India imports soybean oil from Indonesia and Malaysia and palm oil from Brazil and Argentina. Higher fuel prices had made shipping expensive too.

Wheat, corn, and barley prices rose similarly. As the sixth largest exporter, Ukraine commands 9% of the global wheat exports. It also commands 12% each in maize and barley exports.

However, the high prices were short-lived.

In July 2022, about five months after the war started, Ukraine and Russia signed the Black Sea Grain Initiative to allow food and fertilizer exports from three Russian ports. The initiative was meant to stabilize global food prices and avoid famines.

Grain prices corrected by 40% soon after.

However, the initiative collapsed only a year later, in July 2023. While both countries could use their respective ports in the Black Sea, Russia felt that it was not benefitting from the initiative. It had large reserves of grains that it could not export due to the multiple sanctions imposed on the country.

Nevertheless, Ukraine managed to regain control of a few of its ports along the Black Sea, and its grain exports are now exceeding their pre-war levels.

While most commodity prices had shot up immediately after the onset of the war, they have largely stabilized now, even as the war continues.

Corn prices are still showing volatility and took longer to cool down because of other factors. A rising demand for biofuels in India and China is one reason global corn prices remain inflated. India’s push to blend ethanol in petrol and diesel has made it a net importer of corn for the first time in decades.

The stock market and our economy

The Nasdaq and S&P 500 declined for a few months when the war broke out but have since recovered and have given positive returns. The Indian market barely reacted to the war.

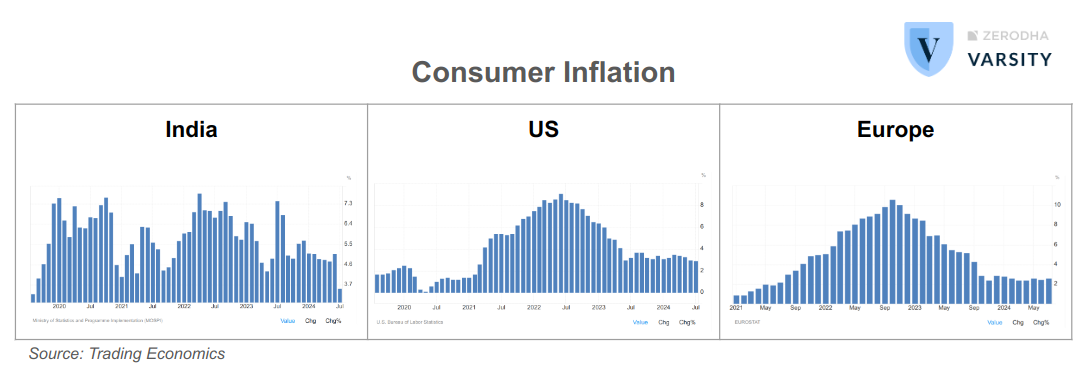

Consumer prices had been rising before the war began. The war may have added to inflation in the US, Europe, and India but these economies had already been tackling the ghosts of covid-era monetary policies. Particularly the US and Europe had resorted to rampant easing of monetary policy in an effort to revive their economies from covid-led slowdown.

The easy and cheap money led to high inflation levels post-covid. In response, most major economies tightened their monetary policies. They adopted aggressive and prolonged interest rate hikes to tame inflation. Now, most economies are reporting normalizing inflation numbers and might even start the next round of a slowly easing monetary policy.

Inflation has largely been driven by the monetary policies of the respective countries and less by the Russia-Ukraine war.

The fears that various economic experts expressed at the start of the war about inflation, slow growth, famines, etc., seemed to be materializing for a few months, but the world adjusted its business around the war. The impact on the world was limited in scope and magnitude.

The world’s economic indifference aside, both Ukraine and Russia continue to lose human lives. The war’s cultural, psychological, and economic repercussions could ripple through decades.