The virtues of youthful stupidity

Are mistakes the best teachers in life?

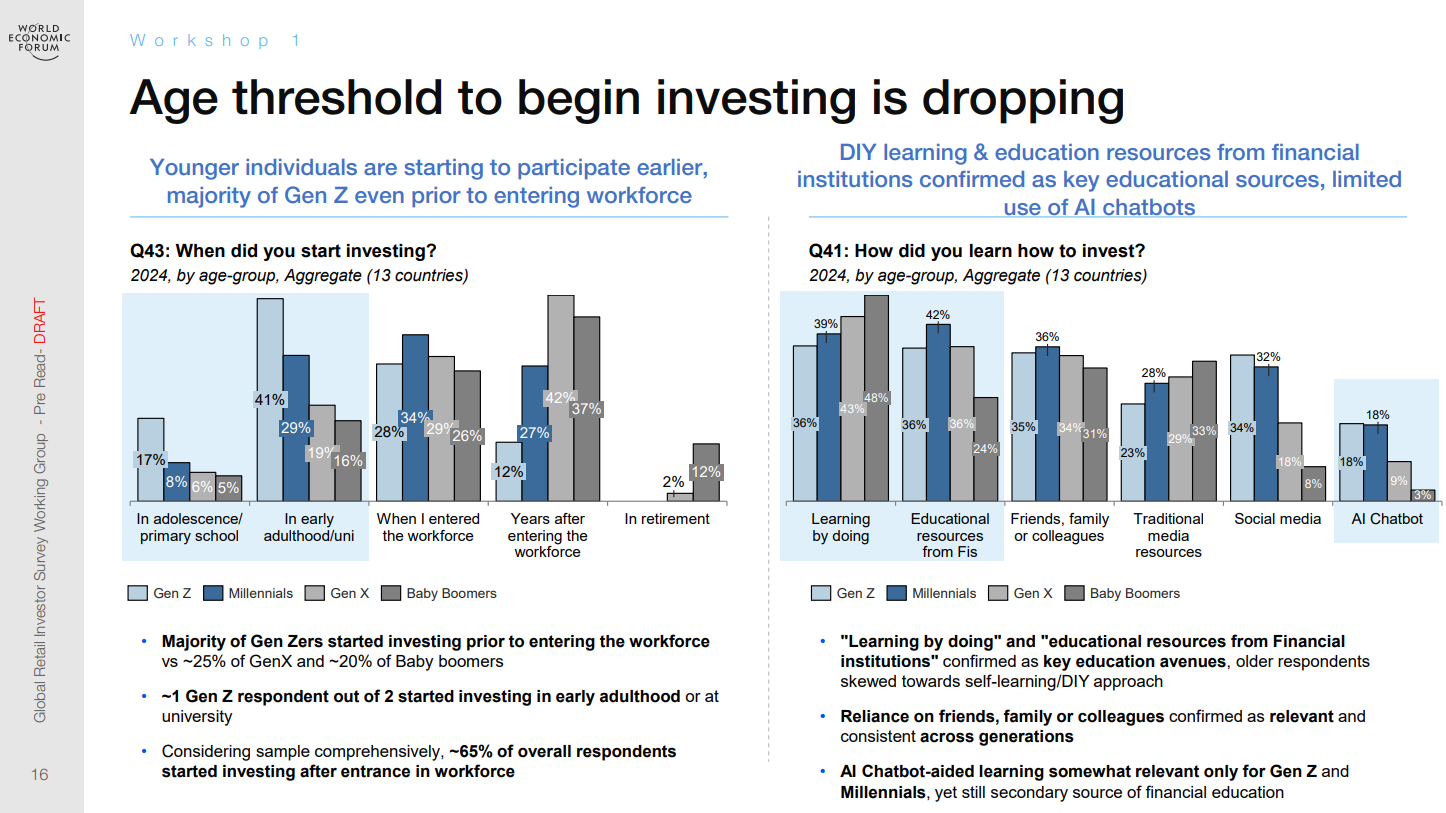

This question led to this post after Dinesh, the head of Rainmatter and the chief strategist at Zerodha, shared an image from a recent World Economic Forum. The image showed that with each successive generation, investors are starting to invest earlier, with the most stunning statistic coming from Gen Z: according to the survey, 1 in 2 Gen Z-ers started investing even before they hit adulthood.

On the same day that Dinesh (he desperately wants to be popular, so follow him) shared this report, I read another article quoting data about the US markets from Barron’s article:

On average, Gen Z—generally described as those born between 1997 and 2012—began saving and investing at 19 years old, according to the survey. Baby boomers—Americans born between 1946 and 1964—didn’t start until age 35, on average.

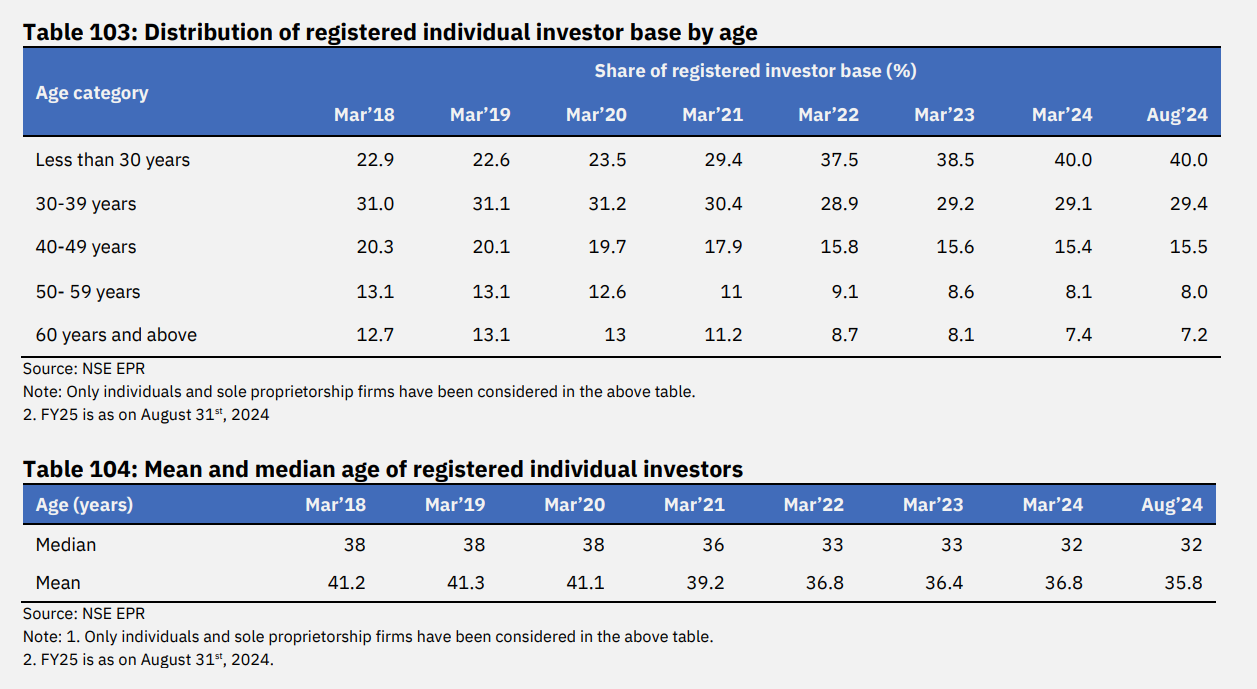

The rising participation of young investors is not just a US phenomenon but also happening in India. Here’s some data from NSE. Notice the almost doubling of investors under 30 years between 2020 and 2024:

That’s a remarkable change in investor demographics and a legacy of COVID-19. I don’t think we ever truly realized just how disruptive the pandemic was. It compressed a decade into a few years and caused more changes between 2020 and 2022 than in the previous couple of decades.

Living through these changes in real-time, it’s hard to comprehend their full scope. I don’t think we’ve truly grasped the extent of the changes that have occurred. When future historians document the impact COVID had on economies, financial systems, culture, and society at large, it will read like the script of a Rohit Shetty movie—dramatic and unbelievable.

Rise of the yutes

Coming back to the increased participation of young investors, this was, in large part, due to the lockdowns. People were stuck at home for well over a year and bored out of their minds. Since going outside for entertainment wasn’t an option, the stock market became the go-to place for cheap thrills.

All the major markets, including India, added more users in those 2-3 years of the pandemic than in the preceding decade—a large chunk of these new investors were under 25 years old. The pace at which the investor base expanded was kinda nuts.

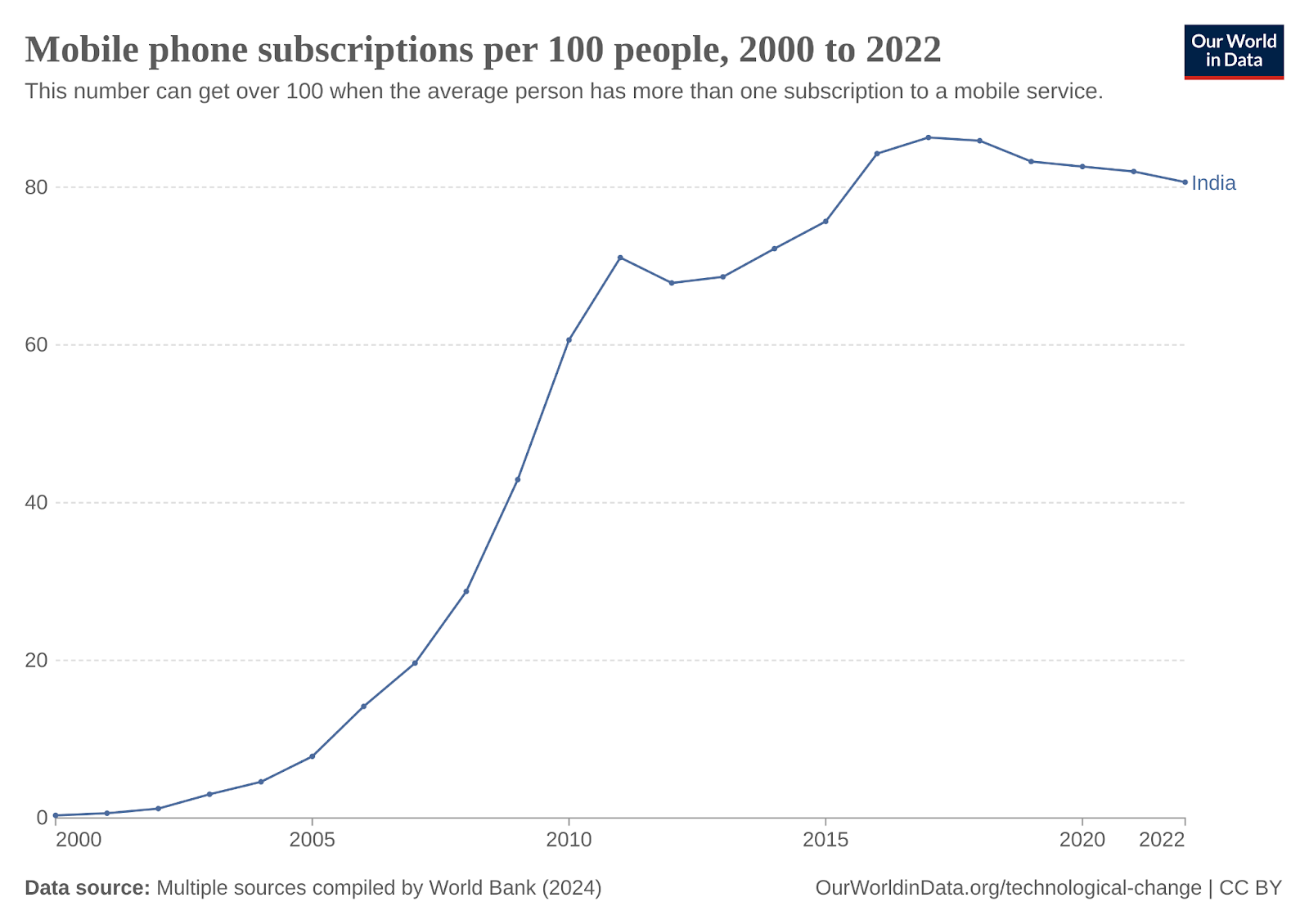

Brokers and investment platforms were able to handle this massive influx thanks to fully online investing enabled by Aadhaar, Digilocker, and UPI, widespread smartphone adoption, and access to cheap mobile data.

Source: OurWorldInData

The search for cheap thrills manifested in the form of a spectacular increase in penny stock volumes, options trading, the craziness with crypto, shitcoins, NFTs, and other assorted varieties of stupidity. Honestly, I think the period between 2020 and 2022 ranks up there in the top five craziest market phases in the 400-year history of modern financial markets.

The good and the bad

If you’ve been following the commentary by market experts in the last four years, you would’ve heard most people complain about how young people are doing utterly dumb things and how this will end in tears. This complaint goes something like, “These stupid kids have only seen good times, and when the next market crash hits, they’ll learn a painful lesson.” These complaints typically end with sanctimonious sermons that end with some version of “long-term investing blah, blah.”

While there’s some truth to these sermons, I have a slightly different take. Now, this might sound a little self-serving coming from someone who works in a brokerage firm, but I’ll leave that judgment to you. I think there’s a silver lining to all this craziness we’ve seen in the last four years.

How markets expand

One of the biggest challenges for a developing country like India is that we need deep and liquid capital markets. For this to happen, you need a wide investor base of individuals and institutions.

But guess what attracts people to the markets?

If you are thinking about financial education, etc., I hate to break it to you; that’s not the case.

Nothing attracts people to the markets like greed and bull markets. Put another way, throughout history, financial markets have expanded the most in terms of investor participation during crazy bull runs and periods of utter mania. Unreasonable expectations have brought more people into the markets than all the financial literacy programs. Unreasonable expectations and greed have done more for financial literacy than financial literacy itself 😜

I often half-jokingly say that nothing expands the financial markets like misselling. There’s some truth to it. Most people aren’t swayed by rational arguments about compounding and “10-12% returns in the long run” sales pitches. The number of people who enter the markets thinking they can make 50% a year vastly outnumbers the sane people who believe in long-term investing by an order of magnitude.

There’s a reason why endowment policies and ULIPs are the most sold financial products in India. The number of Indians who have invested in endowment policies and ULIPs is comparable to those who have invested in stocks and mutual funds. Misselling—whether through greed or setting the wrong expectations—works.

In a weird way, it seems like having a bit of misselling in the markets is unavoidable, maybe even necessary. I wish it weren’t true, but sadly, it is. This might sound hypocritical coming from someone like me, but hey, judge away.

All this craziness is good

Young investors doing dumb things is a good thing. The reason why I say that is that some of the most important lessons you learn in life are from making mistakes. Sure, financial education and spreading financial literacy are important, but nothing teaches you like losing a little money.

In other words, you can read all you want about how it feels to get punched in the face, but you will never truly know until you actually get punched. I’m not saying this works for everyone, but it’s got a pretty good track record compared to other ways of teaching people [1, 2, 3, 4, 5].

I have a few reasons why I am saying this.

Learn the hard Way

You are better off doing dumb things when you are younger and have less money to lose than when you are older and have more at stake. Blowing up an account when you are young and have only a few thousand rupees hurts, but it’s much better than losing lakhs later in life when you have more responsibilities.

There’s something to be said for having a mental library of mistakes to draw from. In an ideal world, you’d want people to read Varsity, Warren Buffett, Ben Graham, and Jack Bogle, but we don’t live in such a world. Humans are not theoretical creatures. In a way, learning by making mistakes with your money when you are young is the best financial lesson you will ever learn. Most people realize they were dumb once they get punched in the face.

The reading and learning will happen once people get all the stupidity out of the system. In a way, people doing stupid things is the best financial literacy intervention 😬

Risk tolerance is inversely proportional to age

In general, the younger you are, the more risk you can afford to take. So you are better off making the riskiest and dumbest mistakes when you are young. This way, you can quickly figure out what works for you financially. It’s well and good to read about investing, but some things you only learn the hard way.

Nobody starts out as an enlightened investor; humans simply aren’t built that way. Even the preachy people writing sanctimonious tweets and blogs about the virtues of long-term investing would’ve done their share of dumb things. That’s how it is with most things in life.

So, despite all the whining about the super dumb stuff these Gen Z kids are up to, the good thing is they’re making these mistakes while they’re really young. They are learning their lessons young when they have little at stake. The odds of them behaving well as they grow older are much higher.

Most experts who criticize these kids don’t realize how hard it is to get people to invest. I would argue that we have to celebrate the fact that these people have made their first investment, no matter how dumb they are. I get that this might sound self-serving, but that’s just how it is. The first step and perhaps the hardest thing in the markets is to get people in. Then comes the other hard part of keeping them in. This is where distributors, advisors, and brokers like us have a role to play.

Generational gripes

Throughout history, every generation has thought that the generation after them is the worst. It’s the same this time around as well. The investors who’ve been around for a while are judging the newer generation and complaining that these kids don’t know anything, they’ve never seen a bear market, etc. But I would argue that the kids are a little different.

Think about the fact that even as far back as 2010, the only asset classes you really had access to were stocks, bonds, and, with some difficulty, gold. But today’s market environment is radically different. Even within stocks and bonds, the menu of products available has grown maybe a hundredfold. Then there are all the other things like crypto, unlisted shares, international investing, digital gold, fractional real estate, and god knows what else.

That means the way this generation will start investing won’t be the same as the last. Plus, their journey from doing crazy stuff to making sensible investments is bound to be different. People who’ve been around in the markets tend to be set in their ways, and they also tend to be judgmental whenever there’s something “new” in the markets. The reality is that markets evolve. They always have.

What do I mean by that?

Take crypto for example. You can complain all you want about its uselessness, but the fact is, the asset class has survived for 14 years now. It’s never been more mainstream than it is today. It’s also more mainstream and institutionalized now than ever before. So, it’s up to the critics to prove that it’s a bad thing. To paraphrase Neil deGrasse Tyson, “The stock market is under no obligation to make sense to you.”

This isn’t to say that the fundamentals of investing have changed—not at all. Earn well, save as much as possible in boring index funds, and keep increasing the amount you invest is still the best advice for people, both young and old. But let’s be real—no young kid is gonna follow that advice.

What’s right isn’t entertaining, and vice versa. Some people want entertainment, and they’ll get it one way or another. With time, their entertainment itch will probably go away, and they’ll grow some common sense and invest the right way. It’s the circle of life—in general and in the markets.

Nice article Bhuvan. Keep it up. I also try to read Buffets letters to share holders and Howard Marks memos. Just made a beginning.

I think that’s growth only came coz of COVID 19 (when Earth is healing) During the lock down the Harshad Mehta story play a vital role to set of investing or steps to financial field specially Young generation.and the living example is Me🤣

Being a huge fan of Neil deGrace Tyson as a cosmos enthusiast and a stock market as well,

Though Neil Said Universe is under no obligation to make sense, i just realized how it applies to the stock market as well.

And hence all the thing said above by Bhuvan is under 100% obligation to anyone to make sense.

Would love to know such other perspective from him.

I agree with the thesis that it is good to make mistakes when you are young. We all do this. In multiple places. Certainly, in stock markets too.

However, it misses an important point.

It is a wrong assumption to make that an average 25 year old today will be financially better off at 45 (and therefore be in a position to benefit from their learning).

Unfortunately many of the 25 year olds may not even be employed by the time they hit 45.

In other words, you no longer live in a 40 years earning potential world (20 to 60) but maybe in a 20 year world (20 to 40). This is true for most of the people who are representative of a typical investor on Zerodha. So, you only have so much time to make mistakes and also somewhat limited to benefit from the learning (through better investments).

Of course, you have the entire lifetime to benefit from compounding (if that’s a lesson that you learn somewhat late in life, like most of us do).

Thanks,

Manish

It would be interesting to know how the volumes stack up? Also the age group wise participation in F&O.