Everything you need to know about zero GST on health and term insurance

The government has announced that from 22 September 2025, premiums for health and term insurance will no longer attract GST. At first glance, this looks like an 18% price cut. But it’s not that simple. Whether you actually save depends on when you buy your policy, when coverage kicks in, and whether you’re starting fresh, renewing, or already tied to a multi-year plan.

In this article, we break down the common situations people are asking about, from new purchases to renewals, grace periods, and even free look cancellations, so you know when the GST exemption really applies.

Does the GST exemption mean a direct 18% discount on health and term insurance policies?

With the new GST exemption on health and term insurance, you no longer see the 18% GST added on top of your premium. Now, many people argue this doesn’t automatically translate into an 18% discount, because when a service is exempt, insurers can’t claim back the GST they pay on their own costs, called Input Tax Credit (ITC). Normally, that blocked ITC would push up the base premium.

Think of it this way: Earlier, you paid ₹100 + 18% GST = ₹118.

Now the GST is gone, so it should just be ₹100. The only catch is that insurers are also paying GST on their own expenses, and since they can’t claim it back (because of the exemption), some of them might be tempted to increase the ₹100 to recover that cost.

For now, though, the large insurers we work with have chosen to absorb this cost themselves. Which means customers should still see the full 18% benefit in their premiums, without any immediate hike in the base policy price.

So, in most cases, yes, you can expect a straight 18% discount.

Will the GST exemption apply to both new policies and renewals?

Yes. Since GST is a transaction-based tax, the exemption covers:

- All new individual policies and

- Renewal premiums payable for all existing individual policies.

When will this be applicable?

The GST exemption will apply from 22 September 2025. But this naturally brings up a few questions:

- I’ve already paid my premium. Will I still get the exemption?

- What if I want to buy a new policy before 22 September?

- My renewal is due right now. How will this work?

- I’ve already renewed my policy. What happens in that case?

Let’s address these one by one.

I’ve already paid my premium. Will I still get the exemption?

If it’s a new policy, the answer depends on a couple of dates:

- Policy issuance date: The date the insurer actually issues the policy document.

- Risk commencement date: The date your insurance coverage officially starts.

- Premium receipt date: The date when the insurer receives your money.

Now, the exemption is tied to the risk commencement date. So:

- If the policy is issued on or after 22 September, and the risk commencement is also on or after 22 September, the GST you paid will be refunded.

- If your risk commencement date is before 22 September, even if the policy document is issued after 22 September, then GST will still apply on that premium.

How can the risk commencement date be different from the policy issuance date?

For some insurers, the risk commencement date, i.e., the day your coverage actually begins, is immediately after you pay the premium. The policy issuance date, however, is when the insurer finishes all formalities (like medical checks, underwriting, and documentation) and issues the policy document.

That’s why the two dates can differ. For example, you might pay on 15 September; coverage (risk) starts the same day, but the official policy document is issued only on 25 September. In this case, even though issuance is after 22 September, the GST exemption won’t apply because your coverage began before the cut-off date.

Does it make sense to buy a new policy before 22 September, or should I wait?

Now that many customers are asking for the GST exemption, insurers have made some temporary adjustments. For new policies purchased between now and 22 September, many insurers are taking prior consent from customers to issue the policy only after 22 September, even if payment is made today. That way, both the issuance date and risk commencement date fall after the cut-off, and you get the exemption.

However, some insurers still start coverage immediately once payment is received. In those cases, the risk commencement date will fall before 22 September, and GST will apply. If your insurer follows this practice, you’re better off waiting until 22 September to buy the policy; otherwise, you’ll most likely end up paying GST.

Disclaimer: If you delay issuance, obviously, you will not have coverage during this period.

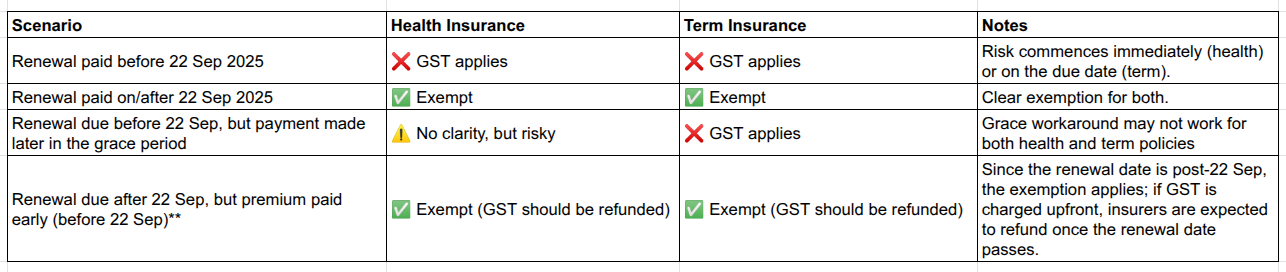

What if my renewal premium is due between now and 22 September?

For renewals, almost every insurer starts coverage the moment you make the payment, even if the updated policy document is issued later. This means the risk commencement date will fall before 22 September, and GST will still apply.

For example, let’s say you’re adding a new family member (like a newborn) at the time of renewal. The insurer may take a few days to issue the updated policy, but since coverage begins right from the date of payment (except for the new member), GST will be charged if you pay before 22 September.

In short, if your renewal premium is due now and you pay before 22 September, you will most likely not get the GST exemption.

My policy renewal date is after 22 September, but I’ve already paid the renewal premium in advance. Will I still get the exemption?

Yes. Since your renewal date falls after 22 September, the GST exemption applies. Even if you’ve paid early, insurers are expected to refund the GST once the renewal date passes. If you don’t receive the refund automatically, you should follow up with your insurer after 22 September.

My renewal is due between now and 22 September. Can I make use of the grace period, delay payment until after 22 September, and get the exemption?

- Health insurance: Technically, yes. If you push your payment into the grace period and settle it after 22 September, your risk cover will usually begin from that payment date, which means the GST exemption should apply. But we’ve spoken to a few insurers, and they have not confirmed this explicitly. Also, this comes with serious risks. During the grace period, you’re effectively uninsured: if you fall ill or get hospitalised, claims won’t be honored. And if you’re diagnosed with a major condition, the insurer can even question or refuse renewal altogether. In short, delaying just to save GST isn’t worth the exposure

- Term insurance: Different story. For most term policies, the risk commencement is tied to the renewal due date, not when you make payment. Which means even if you pay after 22 September (within grace), the risk date is treated as before 22 September. In this case, GST will still apply.

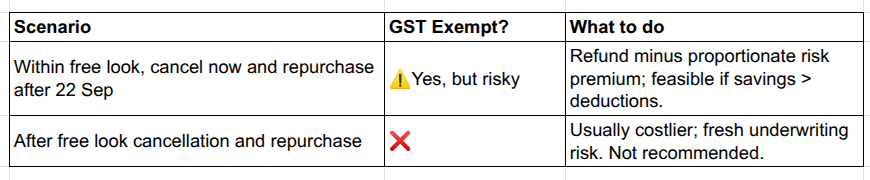

I’ve recently bought a new policy, but I’m still in the free look period. Can I cancel and repurchase after 22 September to get the exemption?

If you are still within the free look period, you can cancel the policy, and the insurer will refund your premium after deducting certain charges, typically stamp duty charges & proportionate risk premium for the days you were covered.

Example: If you bought a policy on 10 September and cancelled it on 20 September, the insurer may deduct 10 days’ worth of premium and refund the balance.

However, if you’re outside the free look period, the math usually doesn’t work in your favour. You’ll lose more in charges than you save in GST. Plus, repurchasing a policy means going through fresh underwriting, and if any health issues crop up, issuance may not be guaranteed. For these reasons, we don’t recommend cancelling and “re-logging” just to save on GST.

What about multi-year policies where I’ve already paid upfront?

Unfortunately, there’s no adjustment possible. If you’ve already paid for two or three years in advance, you won’t get the GST exemption, whether it’s for a new policy or a renewal. The exemption applies only to transactions (issuance or renewal) on or after 22 September 2025.

Quick Summary Tables

New policies

Renewals

Free look/cancellations

Multi-year prepaid

Conclusion

From 22 September 2025, premiums on health and term insurance will no longer attract GST, which in most cases means a straight 18% saving. The catch lies in the dates: when your coverage begins, when you renew, or if you’ve prepaid for multiple years. Bottom line? Align your issuance and renewal dates carefully if you want the benefit.

If you’re unsure whether waiting, renewing now, or switching makes sense for your situation, chat with Ditto’s IRDAI-certified experts to make educated insurance buying decisions today.

Woah, this is very helpful.

Register